United States

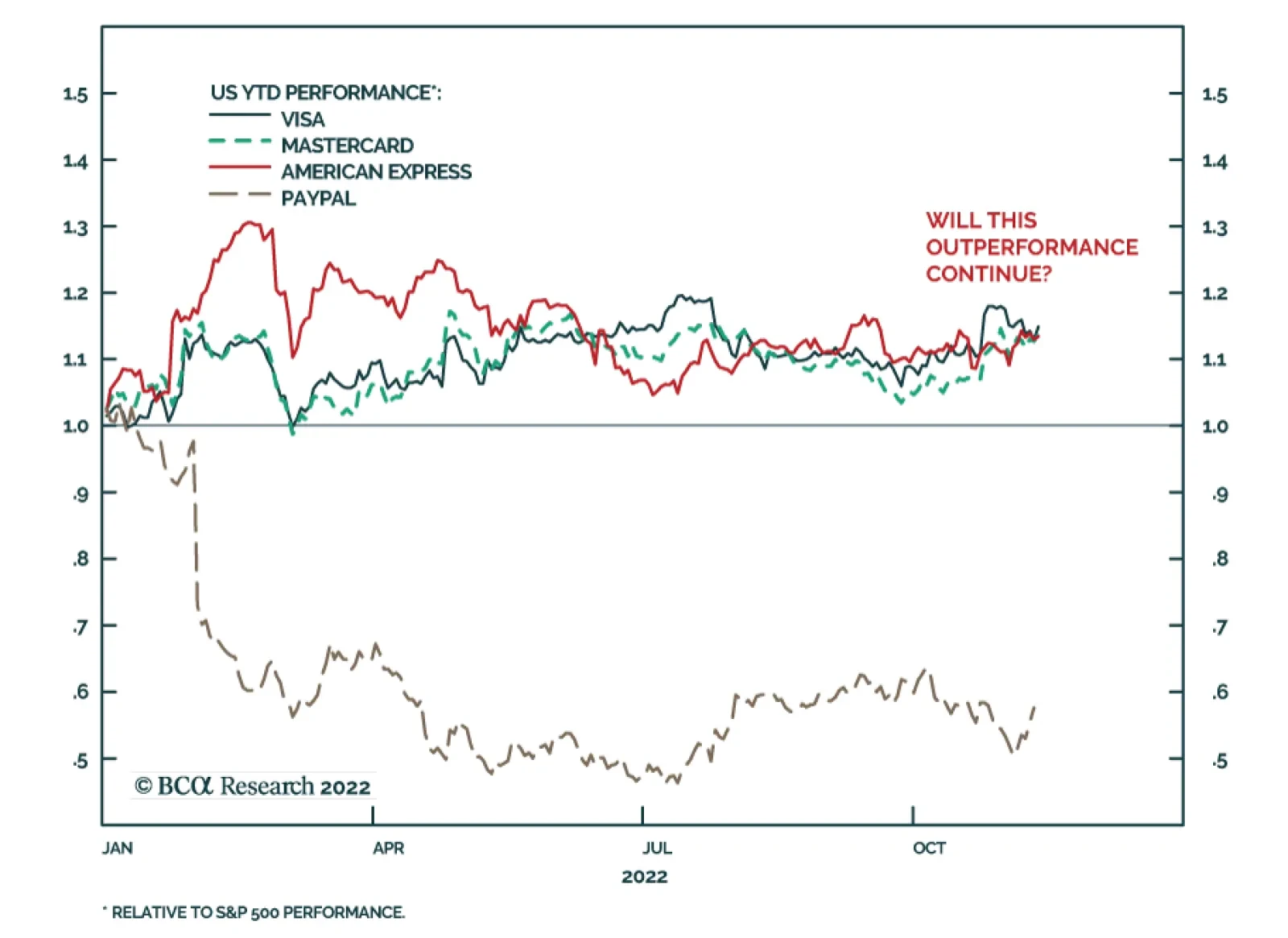

In this report we scrutinize the state of US consumer finances, which are a key driver of the Payment Processing Industry. We expect demand for services to pull back in the early 2023 on the back of still high inflation and tighter monetary policy. The payment processing companies thrive but live on borrowed time. We are overweight for now but monitor this position closely.

Stocks will only get temporary relief from gridlock. Inflation will abate but then remain sticky. US and global policy uncertainty and geopolitical risk will remain historically high.

Stocks will only get temporary relief from gridlock. Inflation will abate but then remain sticky. US and global policy uncertainty and geopolitical risk will remain historically high.

A client concerned about the slump in asset prices, the stubbornness of inflation, and rising bond yields asks what went wrong, and what happens next? This report is the full transcript of our conversation.

Central banker messaging after the latest rate hike announcements in the US, UK and Australia indicates a shift in focus from the pace of hikes to how high rates must rise to slow growth and bring down inflation. This represents the next stage of the global tightening cycle, where rates will go higher in countries where neutral rates are higher, like the US, compared to countries with lower neutral rates like the UK and Australia.