United States

This week we present our Portfolio Allocation Summary for November 2022.

While there is much variability in company profitability, earnings contractions have commenced and appear to be broad-based. We expect earnings growth to deteriorate further into year-end. Companies are reporting concerns about the trajectory of future economic growth and the uncertainty that it brings. Consumer spending on goods has slowed sharply, while spending on discretionary services has surprised on the upside. Business-to-business spending is still strong.

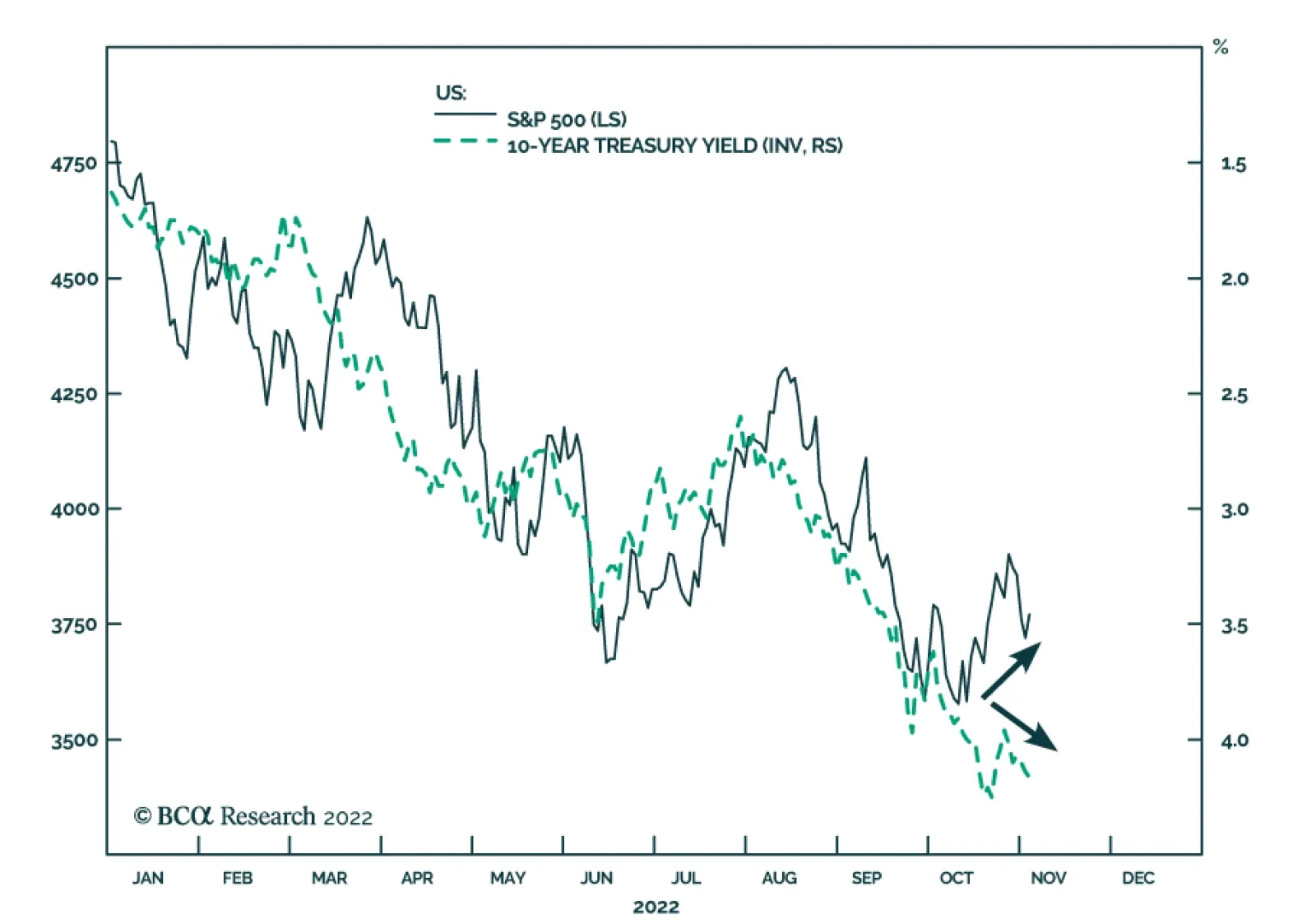

Financial markets slumped with the tough talk that followed last week’s FOMC meeting, but investors should recognize that the tone of the Fed’s communications is conditioned upon the inflation backdrop. Once it improves, Chair Powell and his colleagues will be able to relax their rhetoric.

As the FOMC explicitly acknowledged this week, monetary policy operates with substantial lags. We see the risks to stocks as tilted to the upside over the next 6 months but are neutral on global equities over a 12-month horizon.