United States

Provided that US inflation is due to excess demand rather than supply constraints, demand destruction will likely be needed to bring core inflation below 3.5%. Such growth contraction is positive for counter-cyclical currencies like the US dollar. In China, the Party's focus is to alleviate structural inequality and a long-term confrontation with the US; and authorities are not yet panicking about the cyclical state of the economy. Hence, an economic recovery is unlikely in the coming months.

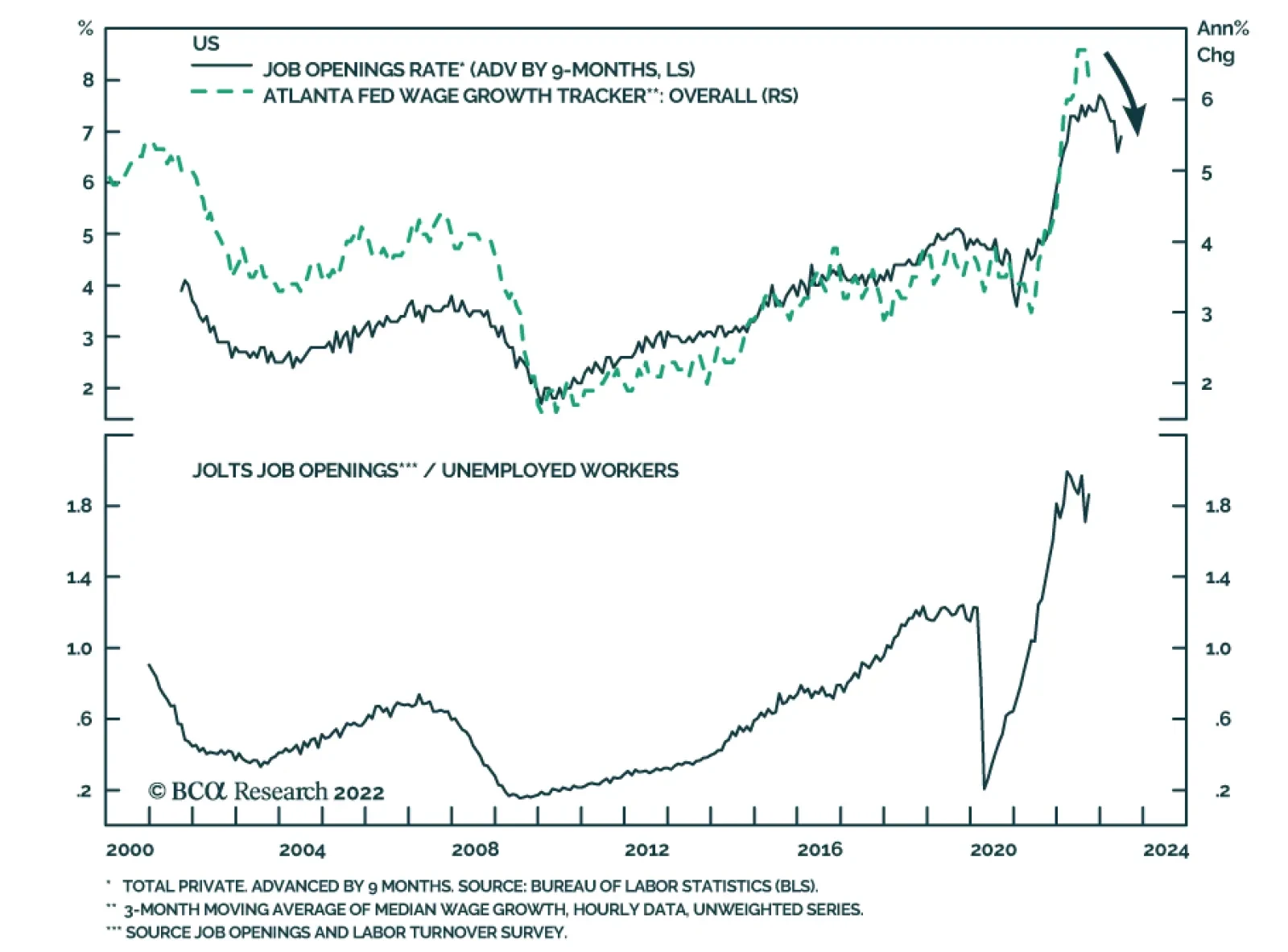

Older workers have deserted the labour force in the US and the UK, but not so in the Euro area and Japan. The result is that wage inflation is red hot in the US and the UK, but not so in the Euro area and Japan. Hence, the Bank of Japan is right to remain a lone dove, the ECB must pivot from its uber-hawkish stance quite soon, but the Fed and the BoE must not pivot from their uber-hawkish stance too soon. We go through the major investment implications.

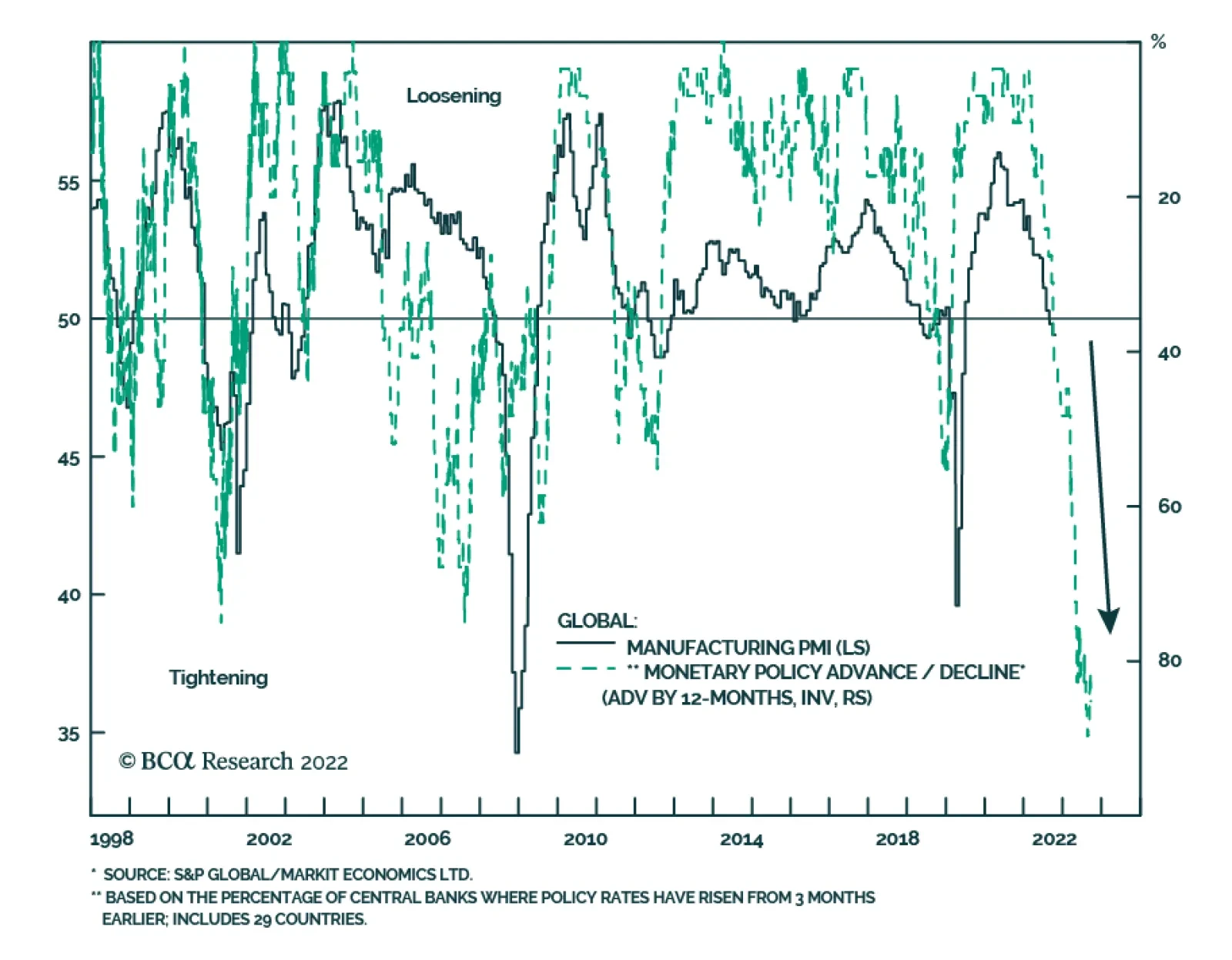

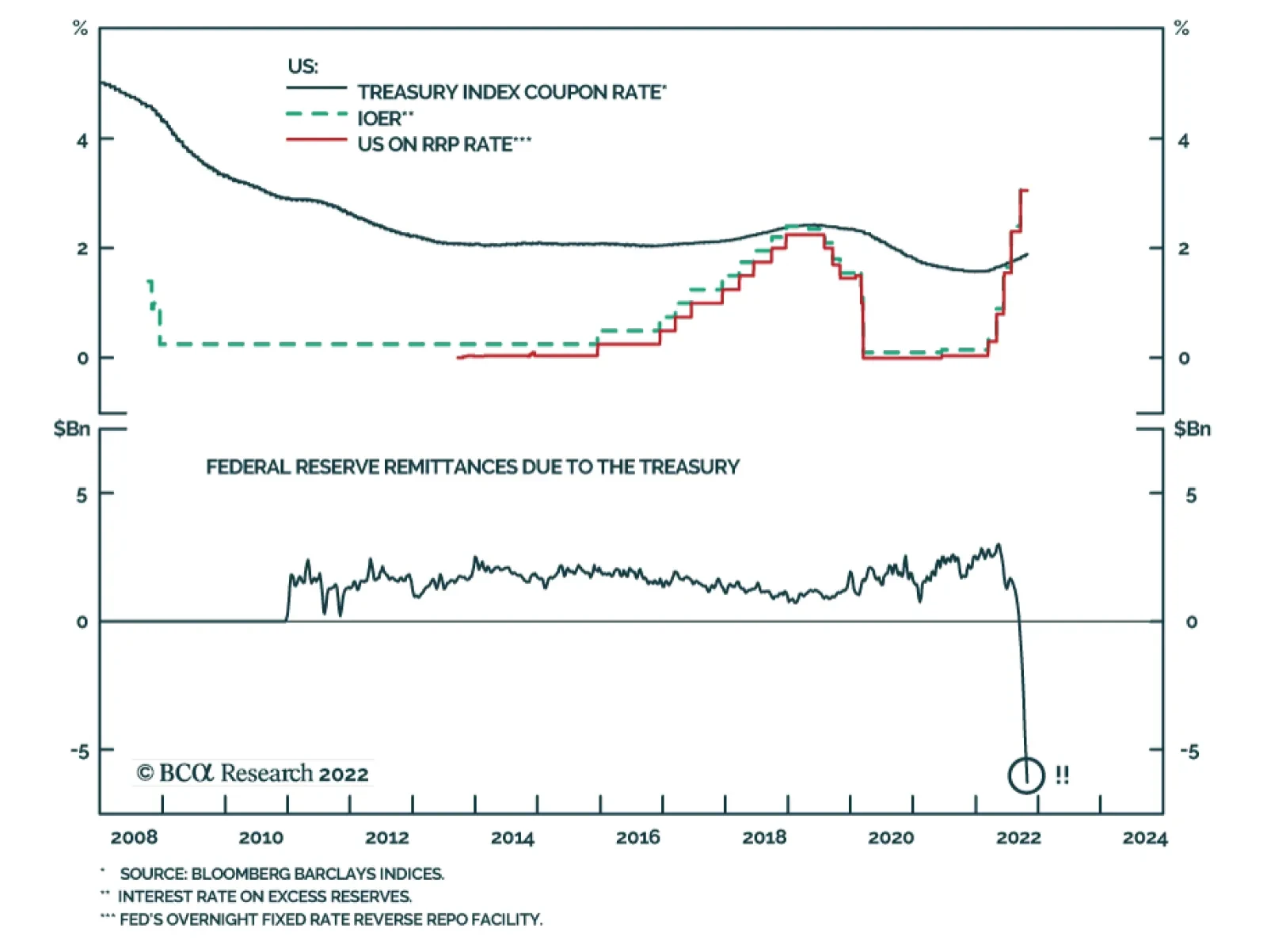

This week’s report examines the state of the global monetary tightening cycle and addresses some frequently asked questions about the Fed’s QT program. New yield curve trades are recommended for the US and German yield curves.