United States

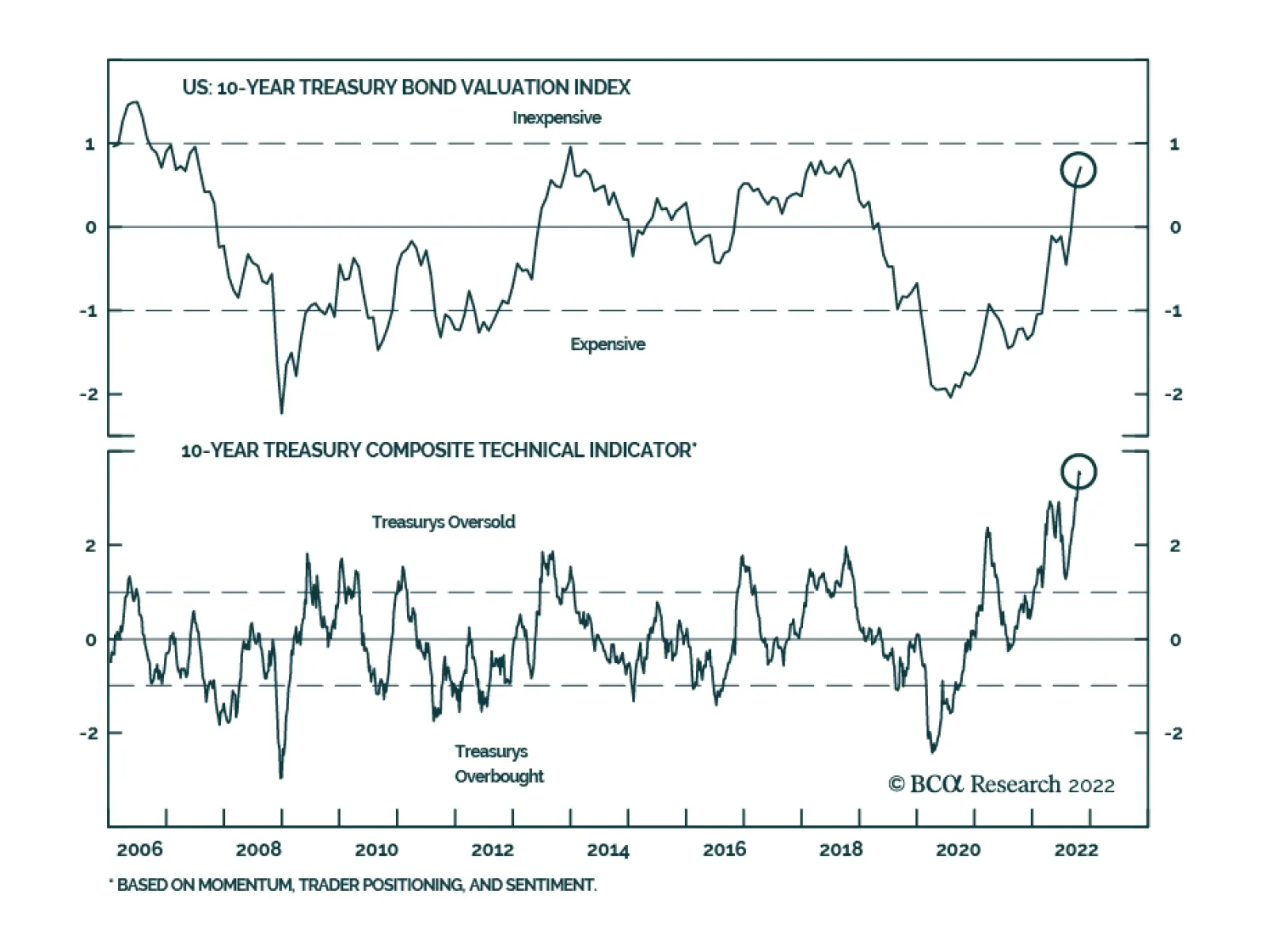

Yesterday we highlighted that the macroeconomic environment could support a rally in Treasuries over the coming months if easing price pressures allow the Fed to set the stage for a policy pivot. Our Composite Technical Indicator is also suggesting that…

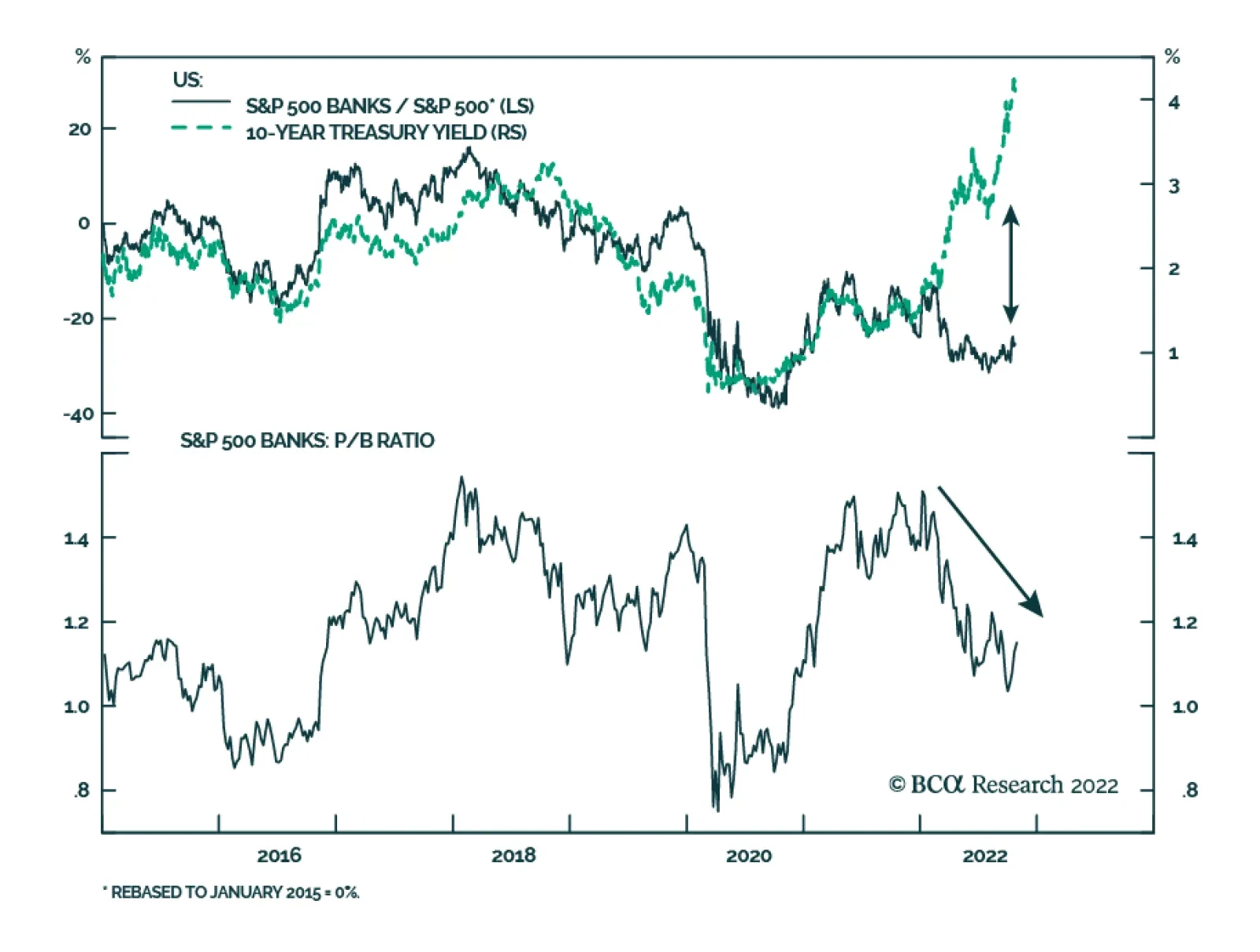

The S&P 500 Banks index is among the worst performing industry groups over the past 12 months, underperforming the broad index by 10.2%. Curiously, this poor performance occurred despite rising interest rates. According to our US Equity Strategists,…

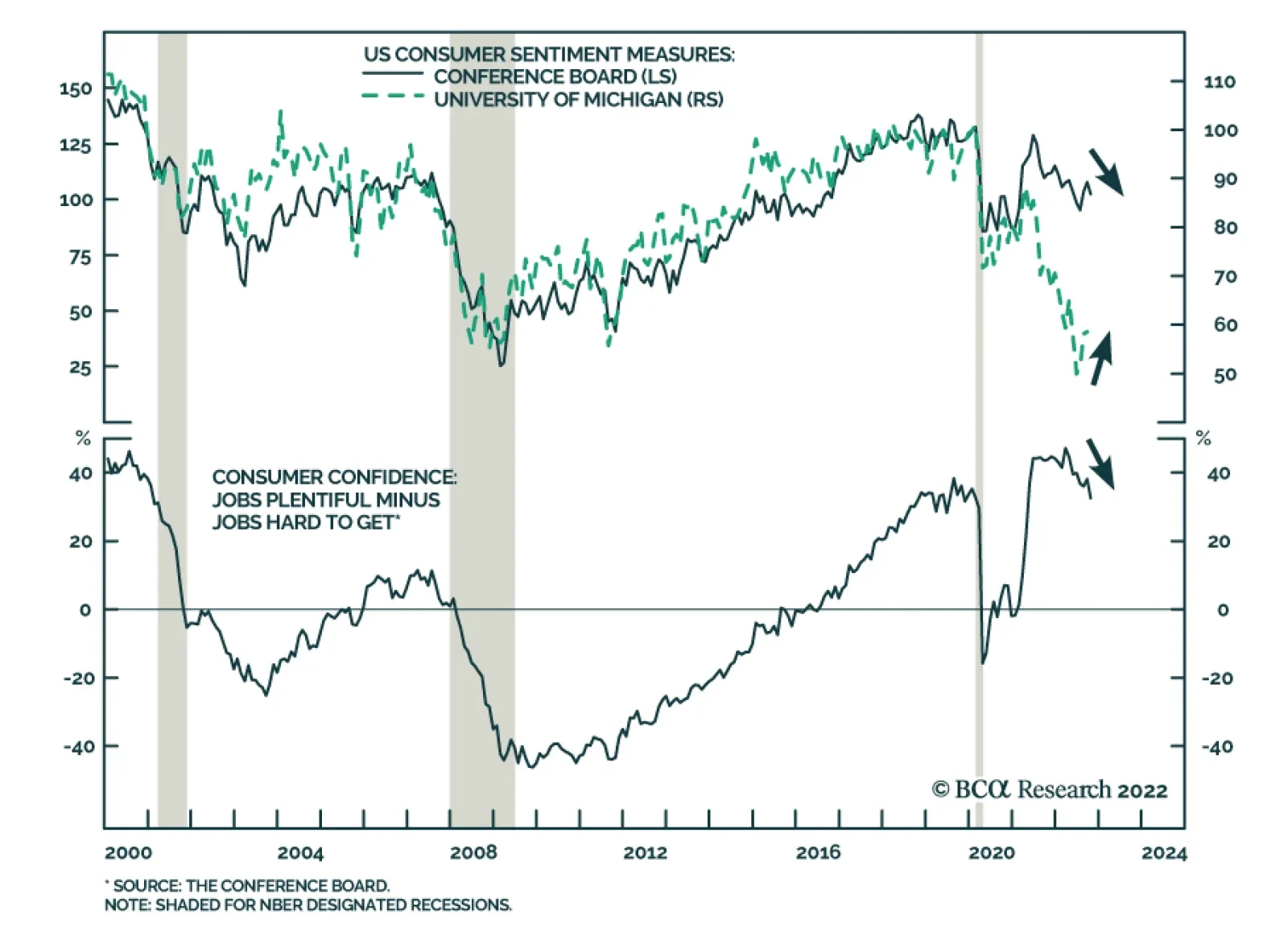

The Conference Board’s Consumer Confidence Index fell from 107.8 to 102.5 in October, significantly below anticipations of a milder decrease to 105.9. In particular, the Present Situation Index sunk to 138.9 from 150.2 while the Expectations Index declined…

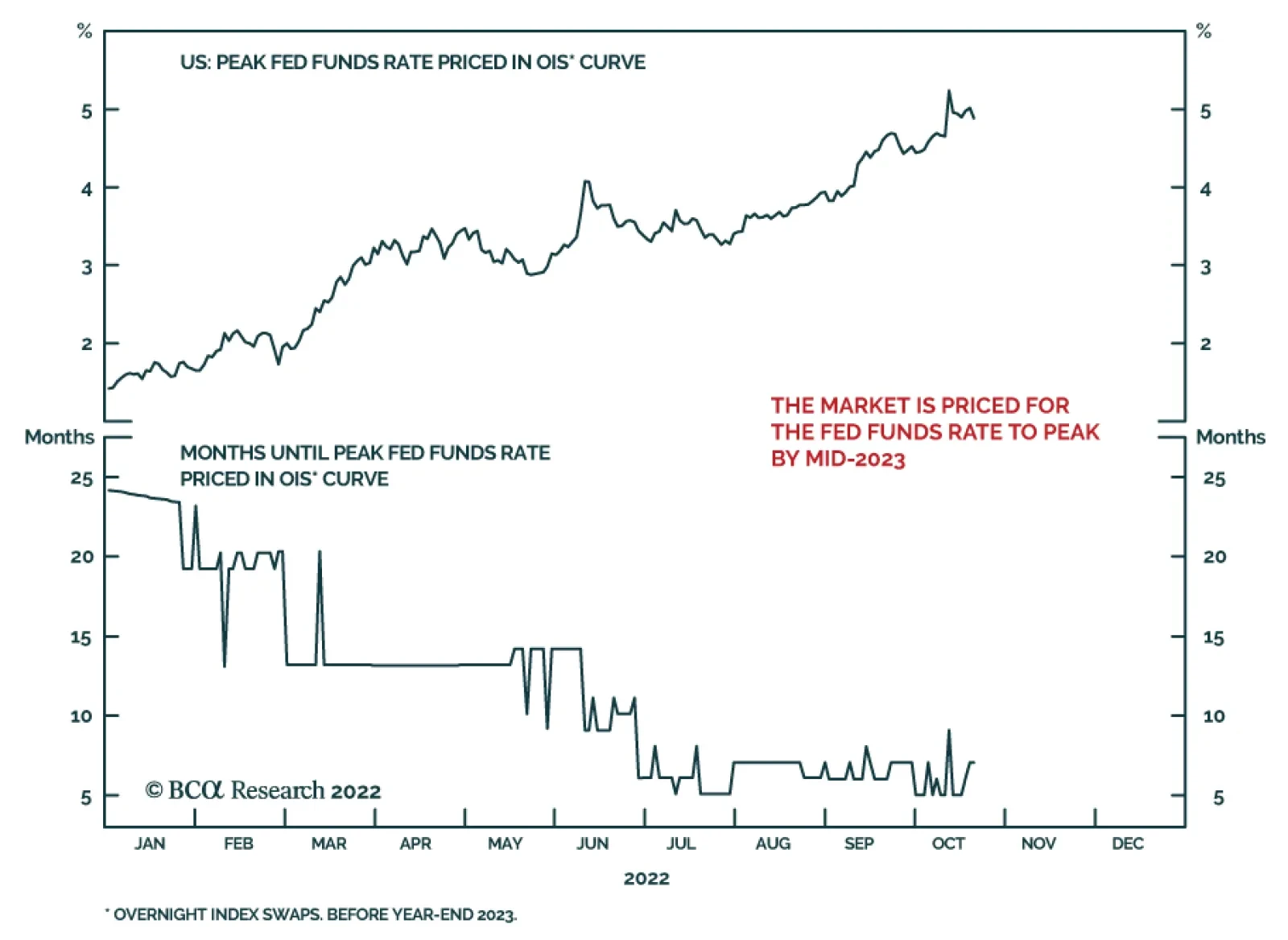

10-year US Treasury yields fell sharply on Tuesday after closing at a 14-year high of 4.25% on Monday. The question facing investors is how much further can bond yields rise? Our US Bond strategists recently analyzed past Fed tightening cycles and found…

According to BCA Research’s US Political Strategy service, if Republicans only take the House, US policy will be more dysfunctional than if they take the entire Congress. US opinion polls are breaking in favor of Republicans in the final lap of the midterm…

This week’s report takes a look at risk-adjusted return opportunities in US spread product.

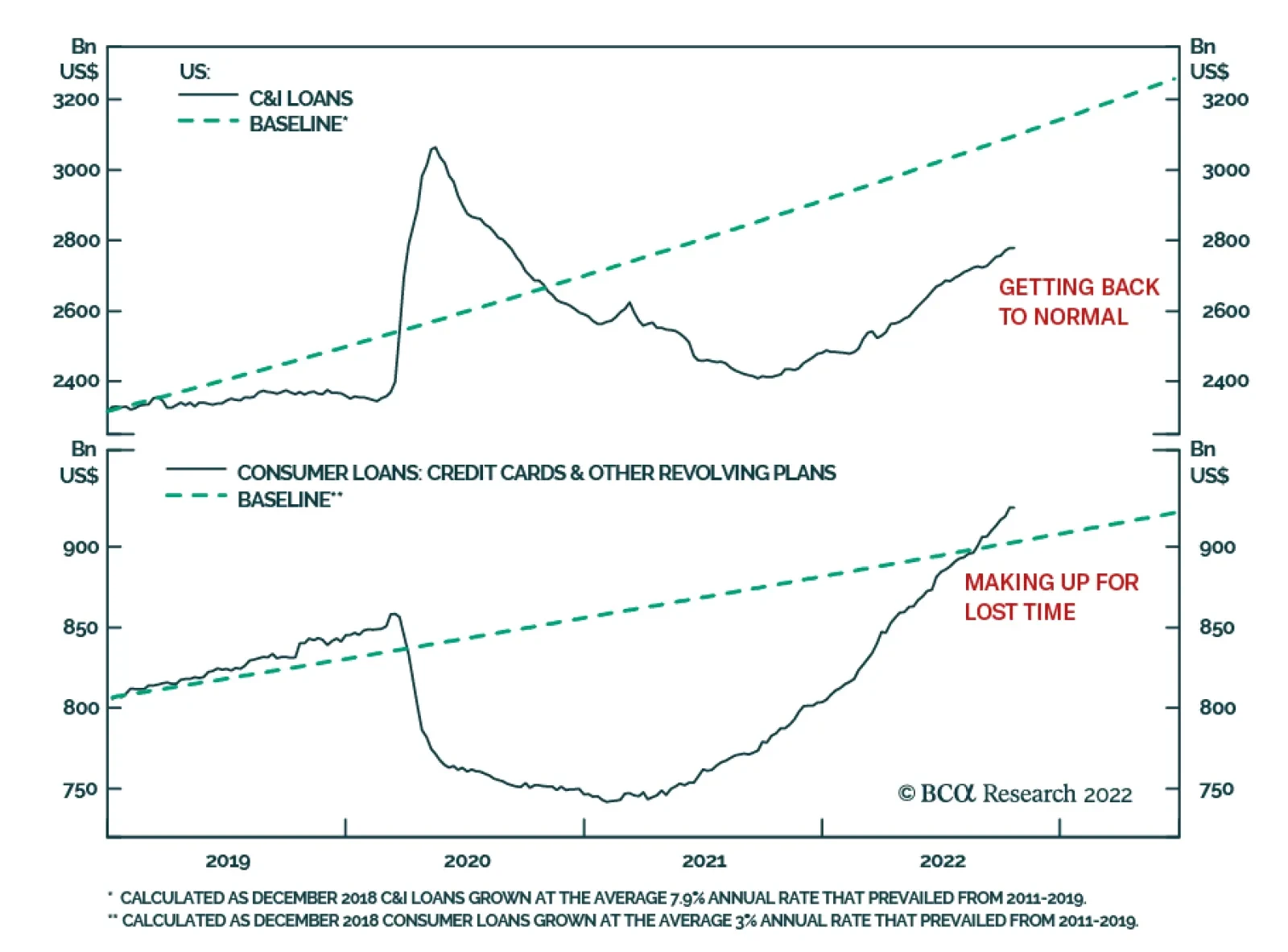

According to BCA Research’s US Investment Strategy service the biggest banks’ commentary validates their view that a recession has not yet begun and will not begin before late 2023. Except at the lowest end of the income and wealth distributions, consumers…

The midterm election will bring some relief from US policy uncertainty. But this relief will be short-lived unless Republicans win the Senate, which is still too close to call. Global policy uncertainty and geopolitical risk will remain high.

On their third quarter earnings calls, the largest banks indicated that their household and business customers remain in surprisingly robust shape. We interpret their observations as supporting our constructive near-term take on the economy and financial markets.

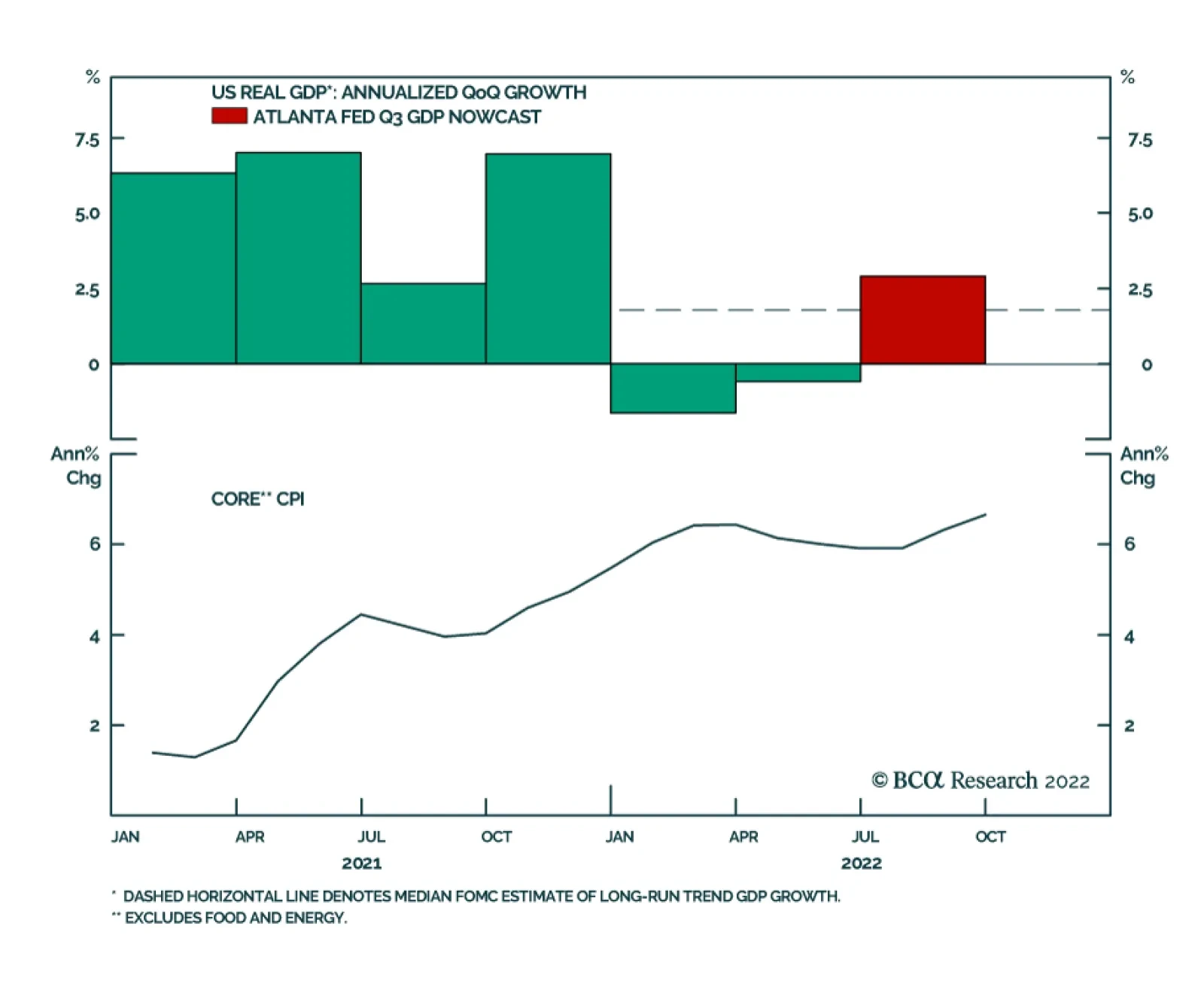

The October Fed Beige Book signaled a “modest” rise in economic growth, an improvement from the previous releases’ “unchanged” economic conditions. Notably, travel and tourism rose strongly and manufacturing activity either held steady or expanded in most of…