United States

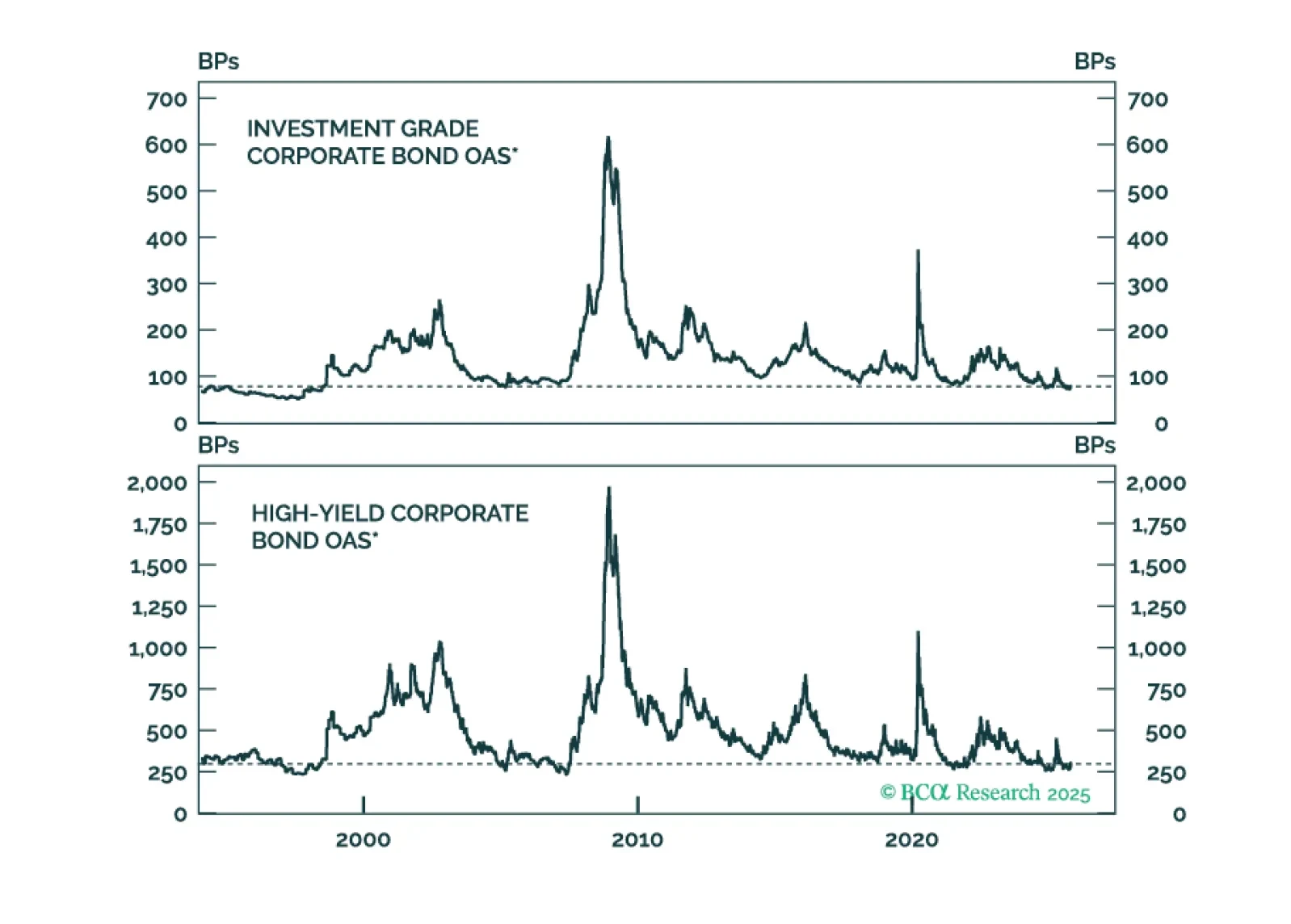

Our US Bond strategists find that neither IG nor HY spreads adequately compensate investors for risk, though the Ba credit tier offers the best relative trade-off. Expected excess returns across corporate credit are near multi-decade lows, with spreads for…

The unwind of 2020–21 froth is stressing floating-rate credit, with weak structures now meeting tighter funding. Our Chart Of The Week comes from Brian Payne, Chief Strategist for our Private Markets & Alternatives (PMA) service. Following…

We expect the divergence between resilient growth and weakening employment to be resolved by lower growth estimates, supporting long duration and steepeners. Economic activity and employment usually move together in a circular relationship: spending drives…

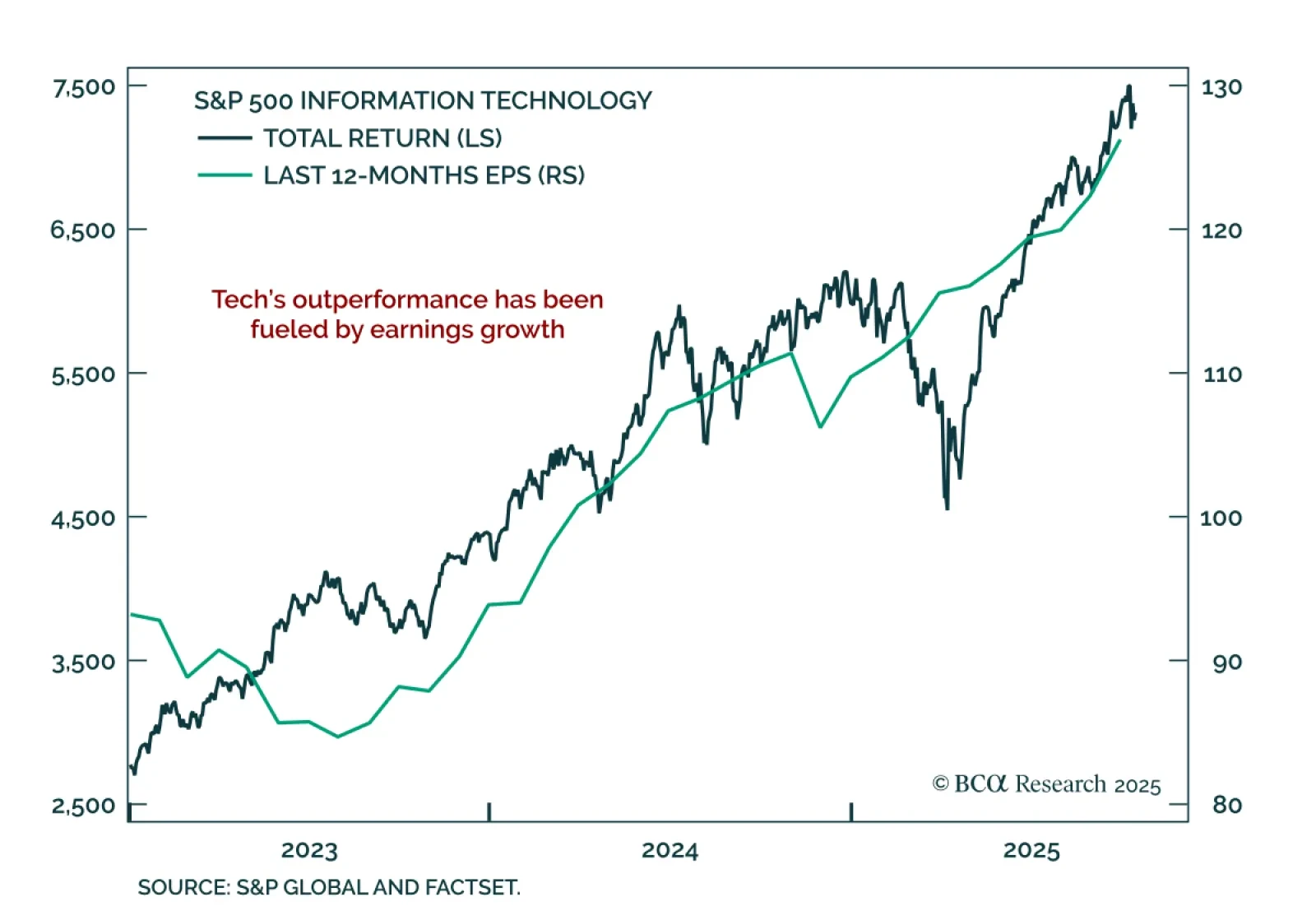

Our US Equity strategists see further room for the bull market to run, supported by solid GenAI-driven earnings growth, though a period of consolidation is likely. Broad adoption and monetization of GenAI, coupled with falling inference costs, should validate…

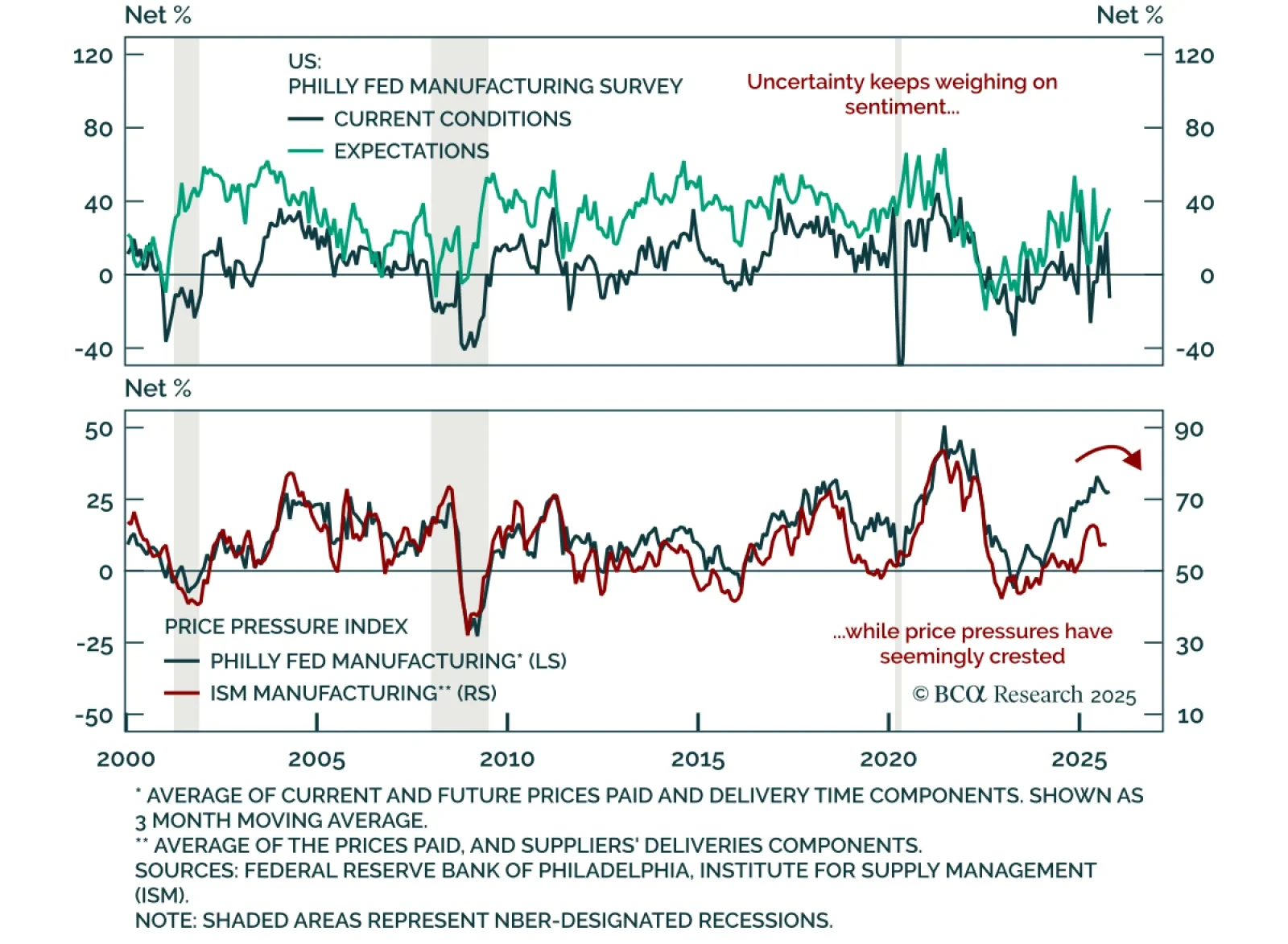

The October Philadelphia Fed manufacturing survey was mixed, showing weak headline data but steadier underlying components. The headline index fell to -12.8 from 23.2, the lowest level since April 2025. Underlying details were not as dire: shipments moderated…

This week’s Special Report evaluates the reward and risk in corporate bonds. We address the question of whether low expected excess returns today are justified by low risk or an example of overvaluation.

The October Empire Manufacturing survey beat estimates, but weak investment and hiring intentions temper its positive signal. The index rose to 10.7 from -8.7, indicating modest activity growth. New orders ticked up, and shipments increased after plunging…

Our GeoMacro strategists remain overweight equities and bonds for now but warn that markets will soon test their “melt-up” thesis, as the cycle transitions from cash- to leverage-driven growth. The dominant theme of 2025 is not AI, but USD debasement. While a…

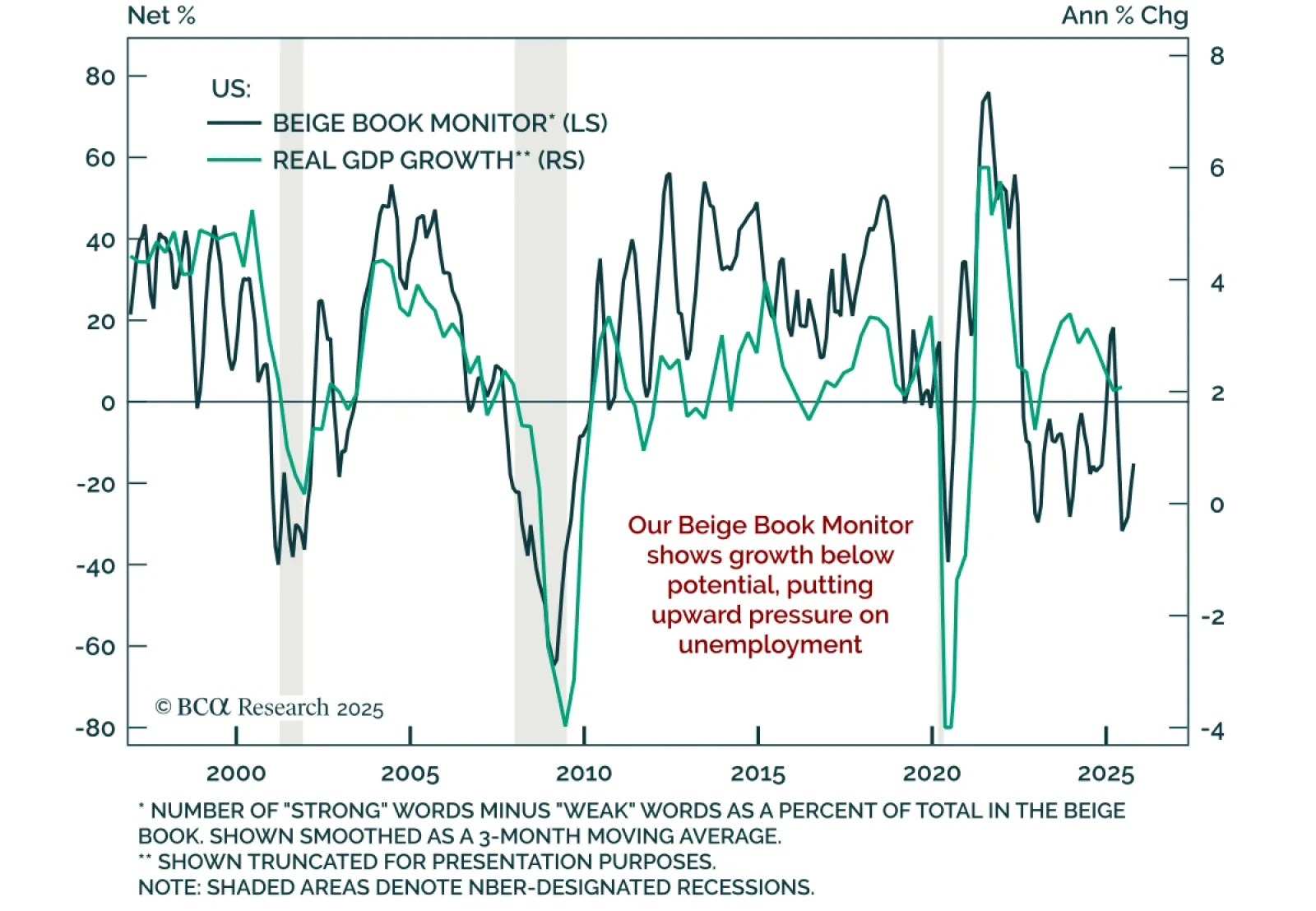

The October Fed Beige Book points to slowing growth as uncertainty continues to weigh on activity. Fed contacts reported consumer spending recently decreased, though auto sales were supported by EV purchases ahead of the expiration of tax credits. Lower- and…

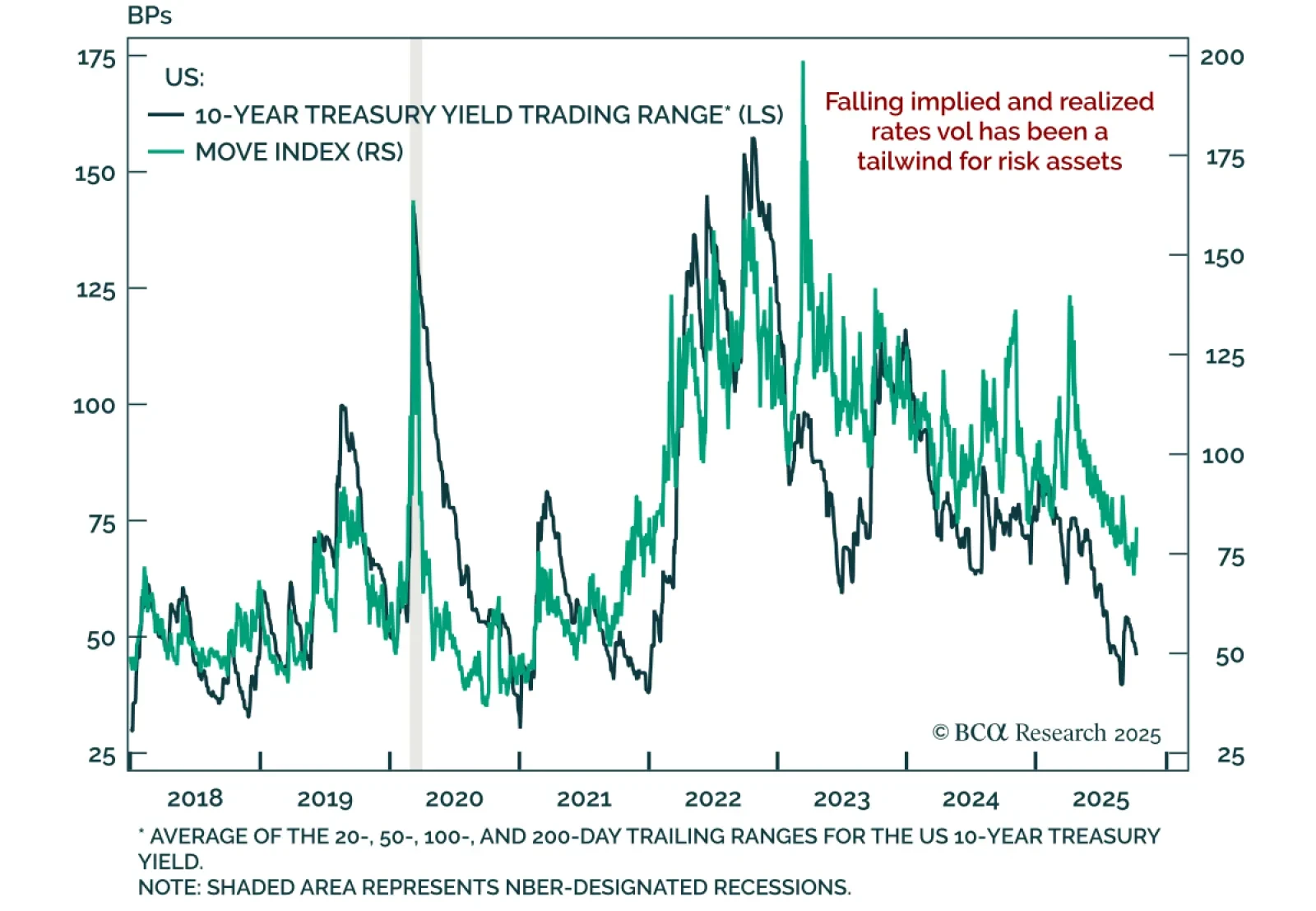

Cross-asset volatility fell in recent weeks, with lower rates volatility supporting risk assets. The MOVE index, which tracks implied USD rates volatility, recently dropped to its 20th percentile before rebounding. This decline reflects several forces. There…