United States

Is a Plaza Accord 2.0 necessary? If so, why? If not, what could stem the rise in the dollar, or will it continue to overshoot? In our view, there are fundamental reasons not to bet on a new accord, but that does not necessarily help with investment strategy.

The Fed’s asset sales are unlikely to lead to an additional outsized impact on long-maturity government bond yields beyond what expectations for the path of the fed funds rate would justify. However, the stance of monetary policy has tightened substantially over the past year, and is set to tighten even further over the coming several months. As such, investors should be focused less on the ostensibly unknown risk from the Fed’s balance sheet reductions and more on the known risk of conventional policy tightening, which is currently quite acute.

Is the US in a wage-price inflation spiral that could lead to more aggressive Fed rate hikes? Is it time to buy UK Gilts after a wild month of volatility? We answer "no" to both questions, as we discuss in this week’s report.

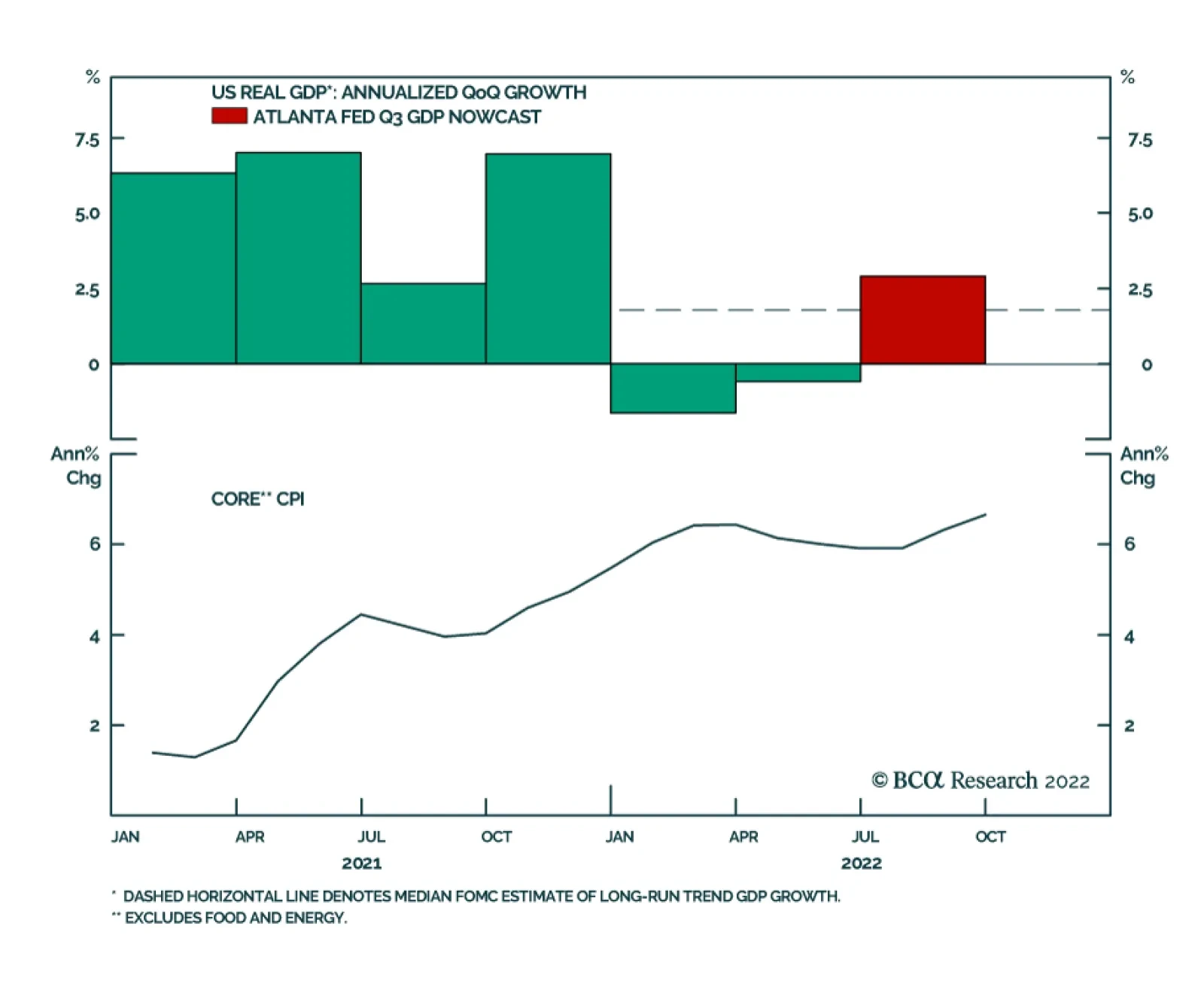

The Fed’s tone has taken a decidedly dovish turn during the past week and, despite September’s hot CPI print, there is mounting evidence that a period of disinflation is coming. This makes the case for a pause in the Fed’s tightening cycle in Q1 or Q2 of next year.