United States

The Fed says that to get back to 2 percent inflation, the US unemployment rate must increase by ‘just’ 0.6 percent through 2023-24. All well and good you might think, except that the Fed is forecasting something that has been unachievable for at least 75 years! Is the Fed gaslighting us? And what does it mean for investment strategy?

This week, we present our quarterly review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio for Q3/2022. We also discuss the model portfolio’s expected performance over next 3-6 months after our recent moves to reduce overall duration exposure and increase the underweight to US Treasuries.

This week we present our Portfolio Allocation Summary for October 2022.

We remain bearish on equities. Inflation is a monetary phenomenon that is embedded and perpetuated by a wage-price spiral. The Fed will “keep at it until the job is done.” Economic growth is slowing, and an earnings recession as soon as the end of this year is highly likely. US equities are not cheap and rising rates and slowing earnings growth will take their toll on performance. Don’t fight the Fed!

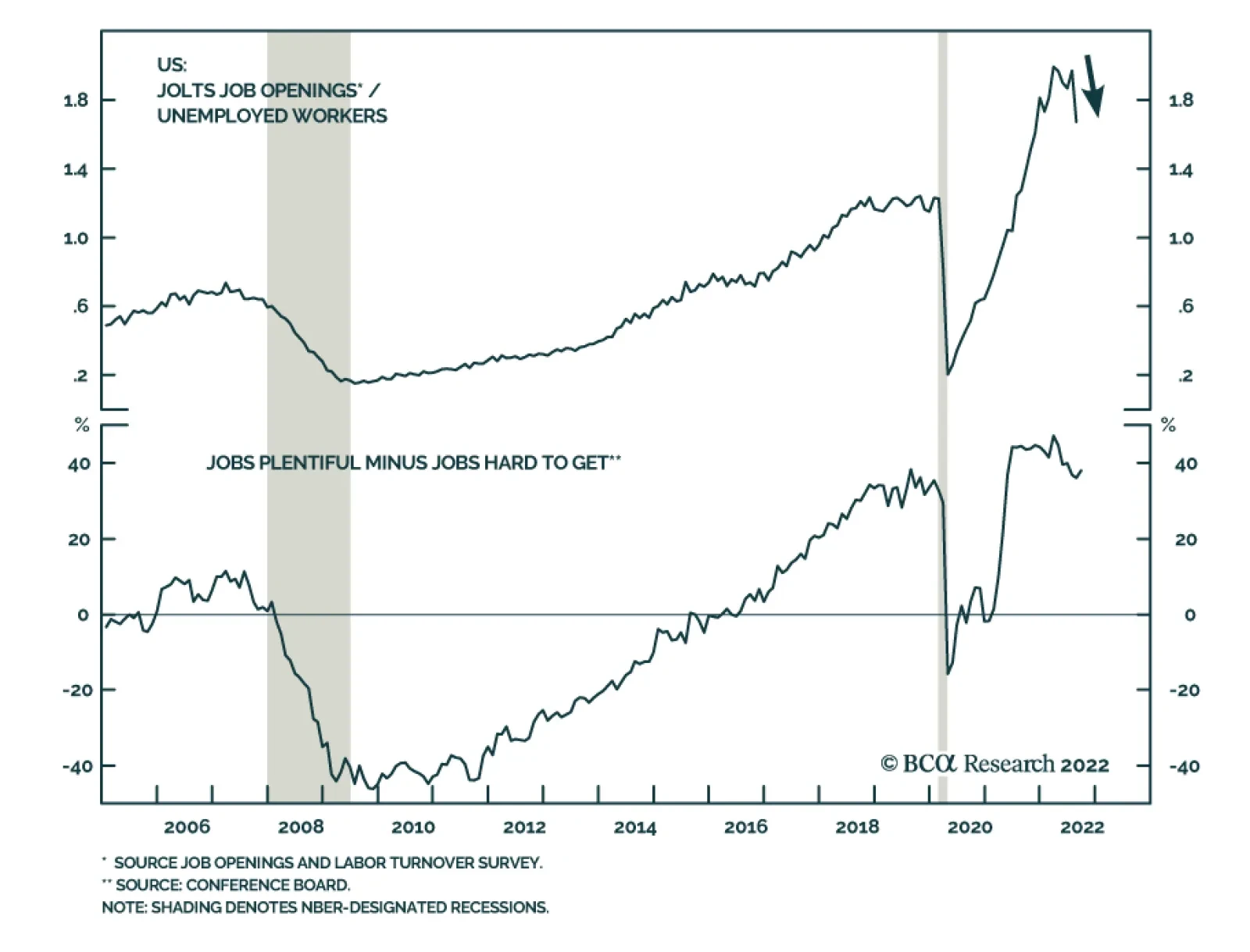

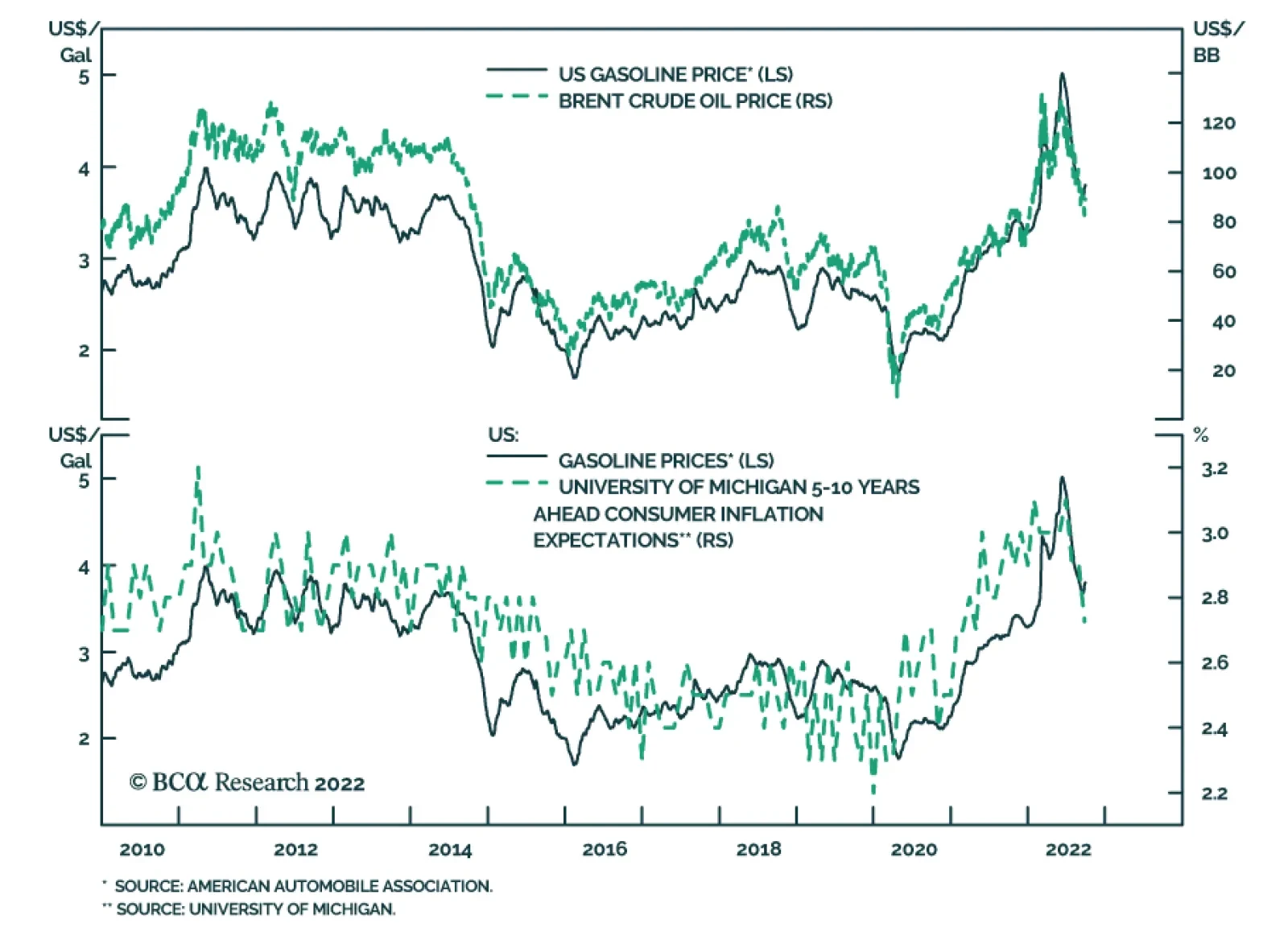

We share our thoughts about some of the less-discussed topics that came up across three weeks of face-to-face discussions with investors. We retain our conviction that the American consumer’s demise has been greatly exaggerated, and it continues to underpin our constructive near-term view on the US economy.