United States

The deceleration in US personal income and spending was larger-than-expected in July. Income and spending grew by 0.2% m/m and 0.1% m/m respectively, following 0.7% and 1.0% increases in June. Core PCE, the Fed’s favored inflation gauge, eased to 4.6% y/y…

Although US GDP growth was revised up to -0.6% from its preliminary estimate of -0.9%, it continues to point to a contraction in economic activity in Q2. It marks the second consecutive quarter of negative GDP growth – meeting the textbook definition of a…

Guidance from Jackson Hole is loud and clear: the central bank is committed to ensuring that inflation returns to target. Powell started his speech by highlighting that the FOMC’s “overarching focus right now is to bring inflation back down to [their] 2…

Listen to a short summary of this report. Executive Summary Housing Activity Should Start To Stabilize By The End Of The Year

Housing Activity Should Start To Stabilize By The End Of The Year

Housing Activity Should Start To Stabilize By The End Of The Year

Home prices in the US are set to decline, almost certainly in real terms and probably in nominal terms as well. Unlike in past episodes, the impact on construction from a drop in home prices should be limited, given that the US has not seen pervasive overbuilding. The drag on US consumption should also be somewhat muted. In contrast to what happened during the mid-2000s, outstanding balances on home equity lines of credit declined during the pandemic housing boom. US banks are on a strong footing today. This should limit the collateral damage from falling home prices on the financial system. Outside the US, the housing outlook is more challenging. This is especially the case in smaller developed economies such as Canada, Australia, New Zealand, and Sweden. It is also the case in China, where the property market may be on the verge of a Japanese-style multi-decade slide. Bottom Line: Softening housing markets around the world will weigh on growth. However, against the backdrop of high inflation, that may not be an unambiguously bad thing. We expect global equities to rise into year end, and then retreat in 2023. The Canary in the Coalmine On the eve of the Global Financial Crisis, Ed Leamer delivered a paper at Jackson Hole with the prescient title “Housing IS the Business Cycle.” Leamer convincingly argued that monetary policy primarily operates through the housing market, and that a decline in residential investment is by far the best warning sign of a recession. Table 1 provides supporting evidence for Leamer’s conclusion. It shows that residential investment is not a particularly important driver of GDP growth during non-recessionary quarters but is the only main expenditure component that regularly turns down in the lead-up to recessions. Table 1A Decline In Residential Investment Typically Precedes Recessions

The Risks From Housing

The Risks From Housing

US real residential investment was essentially flat in Q1 but then contracted at an annualized pace of 16% in Q2, shaving 0.83 percentage points off Q2 GDP growth in the process. The Atlanta Fed GDPNow model forecasts that real residential investment will shrink by 22% in Q3, largely reflecting the steep drop in housing starts and home sales observed over the past few months. Chart 1Housing Activity Should Start To Stabilize By The End Of The Year

Housing Activity Should Start To Stabilize By The End Of The Year

Housing Activity Should Start To Stabilize By The End Of The Year

The recent decline in construction activity is a worrying indicator. Nevertheless, there are several reasons to think that the downturn in housing may not herald an imminent recession. First, the lag between when housing begins to weaken and when the economy falls into recession can be quite long. For example, residential investment hit a high of 6.7% of GDP in Q4 of 2005. However, the Great Recession did not start until Q4 of 2007, when residential investment had already receded to 4.2% of GDP. The S&P 500 peaked during the same quarter. Second, recent weakness in housing activity largely reflects the lagged effects of the spike in mortgage rates earlier this year. To the extent that mortgage rates have been broadly flat since April, history suggests that housing activity should start to stabilize by the end of this year (Chart 1). Third, unlike in the mid-2000s, there is no glut of homes in the US today: Residential investment reached 4.8% of GDP last year, about where it was during the late 1990s, prior to the start of the housing bubble (Chart 2). The construction of new homes has failed to keep up with household formation for the past 15 years (Chart 3). As a result, the homeowner vacancy rate stands at 0.8%, the lowest on record (Chart 4). Chart 2Residential Investment Is Well Below Levels Seen During The Housing Bubble

Residential Investment Is Well Below Levels Seen During The Housing Bubble

Residential Investment Is Well Below Levels Seen During The Housing Bubble

Chart 3Home Construction Has Fallen Short Of Household Formation For The Past 15 Years

Home Construction Has Fallen Short Of Household Formation For The Past 15 Years

Home Construction Has Fallen Short Of Household Formation For The Past 15 Years

Chart 4The Homeowner Vacancy Rate Is At Record Lows

The Homeowner Vacancy Rate Is At Record Lows

The Homeowner Vacancy Rate Is At Record Lows

While new home inventories have risen, this mainly reflects an increase in the number of homes under construction. The inventory of finished homes is still 40% below pre-pandemic levels (Chart 5). The inventory of existing homes available for sale is also quite low, which suggests that a rising supply of new homes could be depleted more quickly than in the past. Chart 5While The Number Of Homes Under Construction Increased, The Inventory Of Newly Built And Existing Homes Remains Low

While The Number Of Homes Under Construction Increased, The Inventory Of Newly Built And Existing Homes Remains Low

While The Number Of Homes Under Construction Increased, The Inventory Of Newly Built And Existing Homes Remains Low

Why Was Housing Supply Slow to Rise? In real terms, the Case-Shiller index is now 5% above its 2006 peak (Chart 6). Why didn’t housing construction respond more strongly to rising home prices during the pandemic? Part of the answer is that the memory of the housing bust curtailed the homebuilders’ willingness to expand operations. Supply shortages also limited the ability of homebuilders to construct new homes in a timely fashion. Chart 7 shows that the producer price index for construction materials increased by nearly 50% between January 2020 and July 2022, outstripping the rise in the overall PPI index. Chart 6Real House Prices Are Above Their 2006 Peak

Real House Prices Are Above Their 2006 Peak

Real House Prices Are Above Their 2006 Peak

Chart 7Producer Prices For Construction Materials Shot Up During The Pandemic

Producer Prices For Construction Materials Shot Up During The Pandemic

Producer Prices For Construction Materials Shot Up During The Pandemic

Chart 8Constraints On Home Building Caused The Housing Market To Clear Mainly Through Higher Prices Rather Than Increased Construction

The Risks From Housing

The Risks From Housing

The lack of building materials and qualified construction workers caused the supply curve for housing to become increasingly steep (or, in the parlance of economics, inelastic). To make matters worse, pandemic-related lockdowns probably caused the supply curve to shift inwards, prompting homebuilders to curb output for any given level of home prices. As Chart 8 illustrates, this meant that the increase in housing demand during the pandemic was largely absorbed through higher home prices rather than through increased output. A Bittersweet Outcome Chart 9Unlike During The Great Recession, Prices For New And Existing Homes Should Fall In Tandem This Time Around

Unlike During The Great Recession, Prices For New And Existing Homes Should Fall In Tandem This Time Around

Unlike During The Great Recession, Prices For New And Existing Homes Should Fall In Tandem This Time Around

The discussion above presents a good news/bad news story about the state of the US housing market. On the one hand, with seasonally-adjusted housing starts now below where they were in January 2020, construction activity is unlikely to fall significantly from current levels. On the other hand, as the supply curve for housing shifts back out, and the demand curve shifts back in towards pre-pandemic levels, home prices are bound to weaken. We expect US home prices to decline, almost certainly in real terms and probably in nominal terms as well. Unlike during the Great Recession, when a wave of foreclosures caused the prices of existing homes to fall more than new homes, the decline in prices across both categories is likely to be similar this time around (Chart 9). The Impact of Falling Home Prices To what extent will lower home prices imperil the US economy? Beyond the adverse impact of lower prices on construction activity, falling home prices can depress aggregate demand through a negative wealth effect as well as by putting strain on the banking system. The good news is that both these channels are less operative today than they were prior to the GFC. Perhaps because home prices rose so rapidly over the past two years, homeowners did not get the chance to spend their windfall. The personal savings rate soared during the pandemic and has only recently fallen below its pre-pandemic average (Chart 10). Households are still sitting on about $2.2 trillion in excess savings, most of which is parked in highly liquid bank accounts. Outstanding balances on home equity lines of credit actually fell during the pandemic, sinking to a 21-year low of 1.3% of GDP in Q2 2022 (Chart 11). All this suggests that the coming decline in home prices will not suppress consumption as much as it did in the past. Chart 10Household Savings Surged During The Pandemic

Household Savings Surged During The Pandemic

Household Savings Surged During The Pandemic

Chart 11Despite Higher Home Prices, Households Are Not Using Their Homes As ATMs

Despite Higher Home Prices, Households Are Not Using Their Homes As ATMs

Despite Higher Home Prices, Households Are Not Using Their Homes As ATMs

The drop in home prices during the GFC generated a vicious circle where falling home prices led to more foreclosures and fire sales, leading to even lower home prices. Such a feedback loop is unlikely to emerge today. As judged by FICO scores, lenders have been quite prudent since the crisis (Chart 12). The aggregate loan-to-value ratio for US household real estate holdings stands near a low of 30%, down from 45% in the leadup to the GFC (Chart 13). Banks are also much better capitalized than they were in the past (Chart 14). Chart 12FICO Scores For Residential Mortgages Have Improved Considerably Since The Pre-GFC Housing Bubble

The Risks From Housing

The Risks From Housing

Chart 13This Is Not 2007

This Is Not 2007

This Is Not 2007

Chart 14US Banks Are Better Capitalized Than Before The GFC

US Banks Are Better Capitalized Than Before The GFC

US Banks Are Better Capitalized Than Before The GFC

The final thing to note is that home prices tend to fall fairly slowly. It took six years for prices to bottom following the housing bubble, and this was in the context of a severe recession. Thus, the negative wealth effect from falling home prices will probably not become pronounced until 2024 or later. A Grimmer Picture Abroad The housing outlook is more challenging in a number of economies outside of the US. While home prices have increased significantly in the US, they have risen much more in smaller developed economies such as Canada, Australia, New Zealand, and Sweden (Chart 15). My colleague, Jonathan LaBerge, has also argued that overbuilding appears to be more of a problem outside the US (Chart 16). Chart 15Rising Rates Will Weigh On Developed Economies With Pricey Housing Markets

Rising Rates Will Weigh On Developed Economies With Pricey Housing Markets

Rising Rates Will Weigh On Developed Economies With Pricey Housing Markets

Chart 16Canada And Several Other DM Countries Have Overbuilt Homes Since The Global Financial Crisis

Canada And Several Other DM Countries Have Overbuilt Homes Since The Global Financial Crisis

Canada And Several Other DM Countries Have Overbuilt Homes Since The Global Financial Crisis

Chart 17Slightly More Than Half Of Canadians Opted For Variable Rate Mortgages Over The Past 12 Months

Slightly More Than Half Of Canadians Opted For Variable Rate Mortgages Over The Past 12 Months

Slightly More Than Half Of Canadians Opted For Variable Rate Mortgages Over The Past 12 Months

The structure of some overseas mortgage markets heightens housing risks. In Canada, for example, more than half of homebuyers chose a variable-rate mortgage over the last 12 months (Chart 17). At present, about one-third of the total stock of mortgages are variable rate compared to less than 20% prior to the pandemic. Moreover, unlike in the US where 30-year mortgages are the norm, fixed-rate mortgages in Canada typically reset every five years. Thus, as the Bank of Canada hikes rates, mortgage payments will rise quite quickly. China: Following Japan’s Path? In the EM space, China stands out as having the most vulnerable housing market. The five major cities with the lowest rental yields in the world are all in China (Chart 18). Home sales, starts, and completions have all tumbled in recent months (Chart 19). The bonds of Chinese property developers are trading at highly distressed levels (Chart 20). Chart 18Chinese Real Estate Shows Vulnerabilities…

The Risks From Housing

The Risks From Housing

Chart 19...Activity And Prices Have Been Falling...

...Activity And Prices Have Been Falling...

...Activity And Prices Have Been Falling...

Chart 20...And the Bonds of Property Developers Are Trading At Distressed Levels

...And the Bonds of Property Developers Are Trading At Distressed Levels

...And the Bonds of Property Developers Are Trading At Distressed Levels

In many respects, the Chinese housing market resembles the Japanese market in the early 1990s. Just as was the case in Japan 30 years ago, Chinese household growth has turned negative (Chart 21). The collapse in the birth rate since the start of the pandemic will only exacerbate this problem. The number of births is poised to fall below 10 million this year, down more than 30% from 2019 (Chart 22). Chart 21China Faces A Structural Decline In The Demand For Housing

China Faces A Structural Decline In The Demand For Housing

China Faces A Structural Decline In The Demand For Housing

Chart 22China's Baby Bust

China's Baby Bust

China's Baby Bust

A few years ago, when inflation was subdued and talk of secular stagnation was all the rage, a downturn in the Chinese property sector would have been a major cause for concern. Things are different today. Global inflation is running high, and to the extent that investors are worried about a recession, it is because they think central banks will need to raise rates aggressively to curb inflation. A weaker Chinese property market would help restrain commodity prices, easing inflationary pressures in the process. As long as the Chinese banking system does not implode – which is highly unlikely given that the major banks are all state-owned – global investors might actually welcome a modest decline in Chinese property investment. Investment Conclusions The downturn in the US housing market suggests that we are in the late stages of the business-cycle expansion. However, given the long lags between when housing begins to weaken and when a recession ensues, it is probable that the US will only enter a recession in 2024. To the extent the stock market typically peaks six months before the outset of a recession, equities may still have further to run, at least in the near term. As we discussed last week, we recommend a neutral allocation on global stocks over a 12-month horizon but would overweight equities over a shorter-term 6-month horizon. In relative terms, the US housing market is more resilient than most other housing markets. We initiated a trade going long Canadian government bonds relative to US bonds on June 30, when the 10-year yield in Canada was 21 basis points above the comparable US yield. Today, the yield on both bonds is almost the same. We expect Canadian bonds to continue to outperform, given the more severe constraints the Bank of Canada faces in raising rates. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Follow me on LinkedIn & Twitter Global Investment Strategy View Matrix

The Risks From Housing

The Risks From Housing

Special Trade Recommendations Current MacroQuant Model Scores

The Risks From Housing

The Risks From Housing

Highlights The risk of a US recession has increased sharply over the past several months. We have not yet concluded that a recession over the coming year is inevitable, but substantial (further) supply-side and pandemic-related disinflation is likely needed for the US economy to avoid a contraction in output. The increased risk of a contraction has caused investors to ponder what the next recession might look like. One very important question concerns the likely behavior of short-term interest rates during the next recession, especially if it occurs sooner rather than later. The historical experience suggests that the Fed may cut interest rates to zero during the next recession, but that the re-establishment of a long-lasting zero interest rate policy and the associated resumption of large-scale asset purchases seem quite unlikely unless the recession is severe. In the post-WWII environment, severe US recessions have been accompanied by aggravating factors that appear to be missing in the current environment. In addition, there are several arguments pointing to the next US recession being a mild one. For fixed-income investors, the implication is that investors should not overstay their welcome in a long-duration position during the next US recession, and should be looking to reduce their duration exposure earlier rather than later. For equity investors, our findings underscore that meaningful downside risk exists for stocks even in a mild recession environment, because the decline in bond yields is not likely to offset a rise in the equity risk premium. Feature Over the past several months, investors have been faced with a sharp increase in the odds of a US recession. Gauging the risk of a recession has featured prominently in our recent reports, and we have concluded, for now, that a US recession over the coming year is not yet inevitable. Still, we acknowledge that the risks are quite elevated, and that substantial (further) supply-side and pandemic-related disinflation is likely needed for the US economy to avoid a contraction in output. Economic expansions do not last forever. This means that the US economy will eventually succumb to a recession at some point over the coming few years. One very important question for investors concerns the likely behavior of short-term interest rates during the next recession, especially if a contraction occurs sooner rather than later. A key aspect of this question is whether the Fed is likely to be forced back towards a zero or negative interest rate policy, and whether it will need to employ asset purchases as part of its stabilization efforts as it has during the last two recessions. If so, long-maturity bond yields are likely to fall significantly during the next recession; if not, investors may be surprised by how modestly long-maturity yields decline. In this report, we examine the historical record of short-term interest rates during recessions and discuss whether the next US recession is likely to be severe or mild. We conclude that the next US recession is more likely to be mild than severe, and that the 10-year Treasury yield is unlikely to fall below 2% during the recession (or fall below this level for very long). In the case of a more severe recession driven by unanchored inflation expectations, the implications would be clearly bearish for bonds. Within a fixed-income portfolio, one conclusion of our analysis is that investors should not overstay their welcome in a long-duration position during the next recession and should be looking to reduce their duration exposure earlier rather than later. For equity investors, our findings underscore that meaningful downside risk exists for stocks even in a mild recession environment, because the decline in bond yields is not likely to offset a rise in the equity risk premium. The Historical Recessionary Path Of Short-Term Interest Rates When projecting how the Fed funds rate is likely to evolve during the next US recession, most investors typically look to the average decline in short-term interest rates during previous recessions as a guide. Based on that approach, Table II-1 highlights that the Fed would likely have to cut rates into negative territory if a recession occurred over the coming 12-18 months, unless it is able to hike interest rates significantly more over the coming year than the market is currently expecting and the FOMC itself is projecting. But in our view, focusing on the historical recessionary decline in interest rates from their peak is not the right approach, because it ignores the fact that recessions typically occur when monetary policy is tight. If a recession occurs within the next 18 months, it will have happened in large part because of a collapse in real wage growth, not just because of the increase in interest rates that has occurred. Chart II-1 highlights that short-term interest rates remain well below potential GDP growth, highlighting that monetary policy would still be easy today – despite the quick pace of increase in short rates – if real wages were growing rather than contracting sharply. In our view, the right approach is to examine how much short-term interest rates have typically fallen during recessions relative to potential or average historical GDP growth. This method captures the degree to which monetary policy easing has typically been required relative to neutral levels to catalyze an economic recovery. Table II-1Based Only On The Historical Decline In Short-Term Interest Rates, The Fed Would Ostensibly Have To Cut Rates Into Negative Territory During The Next Recession

September 2022

September 2022

Chart II-1Monetary Policy Would Still Be Easy Today If Real Wage Growth Was Positive

Monetary Policy Would Still Be Easy Today If Real Wage Growth Was Positive

Monetary Policy Would Still Be Easy Today If Real Wage Growth Was Positive

Based on this approach, Chart II-2 highlights that the Fed might have to cut the target range for the Fed funds rate to 0-0.25% during the next recession, but there are some examples (like the 1990-1991 recession) that point to a cut to just 0.25-0.5%. The goal of this exercise is not to be specific about the exact level to which the Fed will have to cut the Fed funds rate, but rather whether the de facto re-establishment of a long-lasting zero interest rate policy and the associated resumption of large-scale asset purchases is likely. Chart II-2The Fed May Have To Cut To Zero During The Next Recession, But Probably Not Into Negative Territory

September 2022

September 2022

Structural bond bulls might note that there are five recessions in the post-war era that could potentially point to that outcome based on Chart II-2. However, these episodes involved circumstances that we doubt would be present during the next US recession, especially if one were to emerge over the coming 12-18 months. The 1950s Recessions The recessions of 1953-54 and 1957-58 were fairly sizeable based on the total rise in the unemployment rate, but the monetary policy stance at that time was wildly stimulative in a way that is very unlikely to repeat itself today. In the 1950s, the level of interest rates was still an artifact of WWII (with the Treasury-Fed accord having only been agreed upon in March 1951). Monetary policy was both overly responsive to a period of pent-up disinflation following the initial burst of government spending associated with the Korean war and insufficiently responsive to a strongly positive output gap (Chart II-3). This was meaningfully compounded by a poor understanding of the size of the output gap at that time; the deviation of the unemployment rate from its 10-year average was significantly smaller than its deviation from today’s estimate of NAIRU (Chart II-4). In sum, the economic and monetary policy conditions that existed in the 1950s and that contributed to an interest rate level that was well below the prevailing rate of economic growth do not exist today. As such, we strongly doubt that the Fed’s response to the next US recession would resemble what occurred during that decade. Chart II-3We Strongly Doubt The Fed's Response To The Next US Recession Would Resemble What Occurred In The 1950s

We Strongly Doubt The Fed's Response To The Next US Recession Would Resemble What Occurred In The 1950s

We Strongly Doubt The Fed's Response To The Next US Recession Would Resemble What Occurred In The 1950s

Chart II-4Low Interest Rates In The 1950s Were Partly Caused By Wrong Output Gap Estimates

Low Interest Rates In The 1950s Were Partly Caused By Wrong Output Gap Estimates

Low Interest Rates In The 1950s Were Partly Caused By Wrong Output Gap Estimates

1973-1975 The recession that began in 1973 occurred because of a huge energy shock that proved to be stagflationary in the true sense of the word. Excluding the 2020 recession, this was the third largest rise in the unemployment rate of any recession since WWII, following 2008/2009 and the 1981/1982 recessions. There are some parallels between this recession and the current economic environment, but the stability of inflation expectations so far does not point to a truly stagflationary outcome. As such, we do not see the 1973-74 recession as a reasonable parallel to today’s environment. In addition, manufacturing employment – which was heavily impacted by the permanent rise in oil prices due to the sector’s energy intensity – stood at 24% of total nonfarm employment in 1973, compared with 8% today. Finally, the weight of food and energy as a share of total consumer spending today is roughly half of what it was during the 1970s (Chart II-5). 2001 Of the five recessions potentially implying that the Fed may have to cut interest rates into negative territory during the next US recession, the 2001 recession is the most relevant parallel to today. It was a modern recession in which the Fed maintained very easy monetary policy for a significant amount of time, in response to concerns about a significant tightening in financial conditions and the impact of prior corporate sector excesses on aggregate demand. The total rise in the unemployment rate during this recession was not very large, but it took some time for the unemployment rate to return to NAIRU. Still, even though this justified a later liftoff, a Taylor rule approach makes it clear that the Fed overstimulated the economy in response to the recession – a view that is reinforced by the enormous rise in household debt that fueled the housing market bubble during that period (Chart II-6). The Fed was very concerned about the negative wealth effects of the bursting of the equity market bubble, which had been caused by a massive decline in the equity risk premium in the second half of the 1990s. These conditions are simply not present today. Chart II-5Today's US Economy Is Meaningfully Less Impacted By Energy And Food Prices

Today's US Economy Is Meaningfully Less Impacted By Energy And Food Prices

Today's US Economy Is Meaningfully Less Impacted By Energy And Food Prices

Chart II-6The Fed Clearly Overstimulated In Response To The 2001 Recession

The Fed Clearly Overstimulated In Response To The 2001 Recession

The Fed Clearly Overstimulated In Response To The 2001 Recession

2008/2009 Chart II-7A Repeat Of The 2008/2009 Recession In The US Is A Totally Implausible Scenario

A Repeat Of The 2008/2009 Recession In The US Is A Totally Implausible Scenario

A Repeat Of The 2008/2009 Recession In The US Is A Totally Implausible Scenario

Chart II-2 highlighted that the Fed would have to cut interest rates to -1% were the 2008/2009 recession to repeat itself, but we judge that to be a totally implausible scenario given the improvement in US household sector balance sheets and financial sector health since the global financial crisis (Chart II-7). As we discuss below, the next US recession is likely to be meaningfully less severe than the 2008/2009 and 2020 recessions, which we believe carries important significance for the path of interest rates and the response of long-maturity bond yields. The bottom line for investors is that, based on the historical experience of rate cuts during recessions, the Fed may end up cutting interest rates back to or close to the zero lower bound in response to the next recession. But the de facto re-establishment of a long-lasting zero interest rate policy and the associated resumption of large-scale asset purchases seems quite unlikely unless the recession is severe, which we do not expect. Will The Next US Recession Be Severe Or Mild? Chart II-8The Most Severe US Recessions Have Had Aggravating Factors That Do Not Appear To Be Present Today

September 2022

September 2022

How drastically the Fed will be forced to cut interest rates during the next recession will be driven by its severity. Chart II-8 presents the total rise in the unemployment rate during post-WWII recessions (excluding 2020), in order to gauge whether the factors that have led to severe recessions in the past are likely to be present during the next contraction in output. From our perspective, the most severe US recessions in the post-WWII era have been driven by factors that are very unlikely to repeat themselves in the current environment. We noted above that a repeat of the 2008/2009 recession is a totally implausible scenario, leaving the 1981-1982, 1973-1975, and 1950s recessions as potential severe recession analogues. In three of these four cases we see clear signs of an aggravating factor that we do not (yet) believe will be present during the next US recession. Chart II-9Inflation Expectations Have Not Yet Unanchored To The Upside, In Sharp Contrast To The 1970s

Inflation Expectations Have Not Yet Unanchored To The Upside, In Sharp Contrast To The 1970s

Inflation Expectations Have Not Yet Unanchored To The Upside, In Sharp Contrast To The 1970s

In the 1981-1982 recession, the unemployment rate rose significantly as the Federal Reserve confronted the fact that inflation expectations had become severely unanchored to the upside, causing a persistent wage/price spiral. While unanchored inflation expectations is a risk today, so far the evidence suggests that both households and market participants expect that currently elevated inflation will not persist over the long run (Chart II-9). If inflation expectations do become unanchored to the upside at some point over the coming 12-18 months (or beyond), we are very likely to change our view about the severity of the next recession. However, this would be a bond bearish outcome (at least initially), as it would imply sharply higher yields at both the short and long end of the yield curve in order to tame inflation and re-anchor inflation expectations. As noted above, in the 1973-74 recession, the unexpected and permanent rise in oil prices and outright energy shortages rendered a significant amount of capital and labor uneconomic, which is different than what has been occurring during the pandemic. Were the recent rise in natural gas prices to be permanent and no alternatives available, Europe’s current energy situation would be more reminiscent of the 1973-1974 recession than the pandemic-driven price pressures and supply shortages affecting the US and other developed economies. Chart II-10The US Is Currently Experiencing Fiscal Drag, But That Will Lessen Next Year

The US Is Currently Experiencing Fiscal Drag, But That Will Lessen Next Year

The US Is Currently Experiencing Fiscal Drag, But That Will Lessen Next Year

Finally, while the 1957-58 recession appears to be somewhat of an anomaly driven by a mix of factors, the 1953-54 recession was clearly exacerbated by a sharp slowdown in government spending following the end of the Korean war. It is true that the US is currently experiencing fiscal drag (Chart II-10), but this has occurred against the backdrop of a strong labor market, and IMF forecasts imply that the drag will be significantly smaller over the coming year than what the US is currently experiencing. There are several additional points suggesting that the next US recession will be comparatively mild: Chart II-11The Milder US Recessions Were All Seemingly Triggered By Tight Monetary Policy (As Would Be The Case Today)

The Milder US Recessions Were All Seemingly Triggered By Tight Monetary Policy (As Would Be The Case Today)

The Milder US Recessions Were All Seemingly Triggered By Tight Monetary Policy (As Would Be The Case Today)

Chart II-11 highlights that the milder recessions, those which have seen the unemployment rate rise by less than 3% from their previous low, have generally been the recessions that appear to have simply been triggered by monetary policy becoming tight or nearly tight. This would likely be the case during the next US recession. In the lead up to the 1970, 1990-91, and 2001 recessions, short-term interest rates approached or exceeded either potential growth or the rolling 10-year average growth rate of nominal GDP. The 1960-61 recession stands out slightly as an exception to this rule, in that interest rates were still moderately easy, which is based on our definition of the equilibrium short-term interest rate. But interest rates had risen close to 400 basis points from 1958 to 1960 (suggesting a change in addition to a level effect of interest rates on aggregate demand), and it is notable that the 60-61 recession was the mildest in post-war history, based on the total rise in the unemployment rate. Chart II-12Labor Scarcity May Mean That Firms Will Be Somewhat More Reluctant To Shed Labor During The Next Recession

Labor Scarcity May Mean That Firms Will Be Somewhat More Reluctant To Shed Labor During The Next Recession

Labor Scarcity May Mean That Firms Will Be Somewhat More Reluctant To Shed Labor During The Next Recession

We argued in Section 1 of our report that monetary policy is not currently restrictive on its own, and that the recessionary risk currently facing the US is the result of a combination of the speed of adjustment in interest rates, the fact that real wages have fallen sharply, and the fact that the Fed is determined to see inflation quickly return to target levels. However, what this also highlights is that a recession would likely cause a rise in real wages via a significant slowdown in inflation (at least for a time); this would likely help stabilize aggregate demand and cause a comparatively mild rise in the unemployment rate. While the odds and magnitude of this effect are difficult to quantify, the fact that the labor market has been so tight over the past year and that the participation rate has yet to recover to its pre-pandemic levels suggests that some firms may be reluctant to shed labor during a recession (Chart II-12), suggesting that the total rise in unemployment in the next recession could be relatively small. Finally, Chart II-13 shows that the excess savings that have accumulated over the course of the pandemic, now primarily the result of reduced spending on services, dwarf the magnitude of precautionary savings that were generated in the prior three recessions as a % of GDP. We agree that the savings rate would likely still rise during the next recession, but the existence of excess savings implies that the rise in the savings rate may be surprisingly small – which would, in turn, imply a comparatively mild rise in the unemployment rate. We noted above that the household sector has deleveraged significantly, which is strong evidence against an outsized or long-lasting decline in consumer spending as a possible driver of an above-average rise in the unemployment rate during the next recession. One question that we often receive from clients is whether excessive corporate sector leverage could cause a more severe decline in economic activity once a recession emerges. Chart II-14 illustrates that the answer is “probably not.” The chart presents one estimate of the US nonfinancial corporate sector debt service ratio, based on national accounts data. The chart highlights that the current debt burden for the nonfinancial corporate sector is very low, underscoring that elevated corporate sector debt would not likely act as an aggravating factor driving an outsized rise in the unemployment rate were a recession to occur today. The chart also shows that even if the 10-year Treasury yield were to rise to 4% and corporate bond spreads were to widen in the lead up to a recession, the nonfinancial corporate sector debt service burden would rise to a lower peak than seen in the last three recessions. One key risk to a mild recession view is a scenario in which inflation does not return to or below the Fed’s target during the recession. In that kind of environment, the Fed would not likely cut interest rates to as low a level as they have in the past relative to potential growth. But the historical record is clear that recessions cause a deceleration in inflation, and if a recession emerges over the coming 12-18 months it will likely happen after supply-side and pandemic-related disinflation has already occurred. That means that inflation is likely to move back to or below the Fed’s target in a recessionary environment. We should note that this assessment differs somewhat from the scenario described by my former colleague Martin Barnes, who wrote a guest report on inflation published in our July Bank Credit Analyst.1 Chart II-13Today’s Pandemic-Related Excess Savings Dwarf Precautionary Savings During The Prior Three Recessions

September 2022

September 2022

Chart II-14US Corporate Sector Debt Unlikely To Lead To A More Severe Recession, Even In A Higher Yield Environment

US Corporate Sector Debt Unlikely To Lead To A More Severe Recession, Even In A Higher Yield Environment

US Corporate Sector Debt Unlikely To Lead To A More Severe Recession, Even In A Higher Yield Environment

Long-Maturity Bond Yields And The Next US Recession What does our analysis imply for long-maturity bond yields and the duration call over the coming few years? In order to judge what is likely to happen to long-maturity bond yields in a recession scenario over the coming 12-18 months, we first project the fair value of the 5-year Treasury yield based on the following hypothetical circumstances: The onset of recession in March 2023 and a peak in the Fed funds rate at a target range of 3.75-4%. A recession duration of eight months, over which time the Fed steadily cuts the policy rate to 0-0.25%. An initial Fed rate hike in September 2024, nine months following the end of the recession, consistent with a relatively short return of the unemployment rate to NAIRU as an expansion takes hold. A rate hike pace of eight quarter-point hikes per year, with the Fed again raising rates to a peak of 4% A longer-term average Fed funds rate of 3%, which we regard as a low estimate. Chart II-15The 5-Year Treasury Yield Would Not Fall Enormously In A Mild Recessionary Scenario

The 5-Year Treasury Yield Would Not Fall Enormously In A Mild Recessionary Scenario

The 5-Year Treasury Yield Would Not Fall Enormously In A Mild Recessionary Scenario

Chart II-15 highlights the fair value path for the 5-year Treasury yield in this scenario. Not surprisingly, the fair value today is lower than the current level of the 5-year yield, highlighting that a shift to a long duration stance will be warranted at some point over the coming year if the US economy enters a non-technical, typical income-statement recession. However, the chart also highlights that a long duration position is not likely to be warranted for very long, given that the lowest level of the 5-year fair value path is substantially higher than it was in 2020 and 2021 and is also higher than its 10-year average. Chart II-16 reveals the importance of forecasting the near-term path of interest rates when predicting the likely behavior of long-maturity bond yields. Even though near- and long-term interest rate expectations should be at least somewhat differentiated, the chart highlights that the real 5-year/5-year forward Treasury yield is very closely explained by the real 5-year Treasury yield and a 3-year lag of our adaptive inflation expectations model (which is highly consistent with BCA’s Golden Rule of bond investing framework). Chart II-16 shows that long-maturity bond yields should be higher than they are based on the current level of real 5-year yields and lagged inflation expectations, underscoring the point that we made in Section 1 of our report that significant upside risk exists for long-maturity bond yields in a non-recessionary outcome over the coming year. In a recessionary outcome, it is clear that bond yields will fall as the Fed cuts interest rates, as Chart II-15 demonstrated. But, Chart II-17 highlights that during recessions, there is little precedent for a negative 5-10 yield curve slope outside of the context of the persistently high inflation environment of the late 1960s and 1970s. Applying that template to the fair value path that we showed in Chart II-15 suggests that the 10-year Treasury yield will not fall below 2% during the next recession. As we noted in our August report,2 a 10-year Treasury yield decline to 2% would result in significant performance for long-maturity bonds, but it would not end the structural bear market in bonds that began two years ago – a fact that we suspect would be very surprising to bond-bullish investors. Chart II-165-Year Bond Yields Strongly Explain Yields 5-Years/5-Years Forward

5-Year Bond Yields Strongly Explain Yields 5-Years/5-Years Forward

5-Year Bond Yields Strongly Explain Yields 5-Years/5-Years Forward

Chart II-17There Is Not Much Precedent For A Negative 5/10 Yield Curve During Modern Recessions, Suggesting 10-Year Yields Will Not Fall Below 2% During The Next Recession

There Is Not Much Precedent For A Negative 5/10 Yield Curve During Modern Recessions, Suggesting 10-Year Yields Will Not Fall Below 2% During The Next Recession

There Is Not Much Precedent For A Negative 5/10 Yield Curve During Modern Recessions, Suggesting 10-Year Yields Will Not Fall Below 2% During The Next Recession

It is true that bond yields may deviate from the fair value levels shown in Chart II-15 if investors expect a different outcome for the path of the Fed funds rate than we described. However, it is worth noting that changes in our assumed post-recession peak Fed funds rate and the long-term average do not substantially change the outcome shown in Chart II-15. If investors instead assume that the Fed funds rate will peak at 3% during the next expansion, that lowers the fair value path for the 5-year yield by approximately 5 basis points. Changing the long-term average Fed funds rate to 2.4%, the Fed’s current neutral rate expectation, would reduce it by about 25 basis points. These levels would still be significantly above the lows reached in 2011-2013 and in 2020, underscoring that the length of the recession and the speed at which the Fed begins to raise interest rates will be far more important determinants of the path of US Treasury yields. We strongly suspect that investors will recognize that a comparatively mild recession will not result in the same hyper-accomodative monetary policy stance that occurred during the past two recessions, implying that long-maturity bond yields will have less downside during the next recession than may be currently recognized. Investment Conclusions As we have presented, the historical experience suggests that the Fed may cut interest rates to zero during the next recession, but that the re-establishment of a long-lasting zero interest rate policy and the associated resumption of large-scale asset purchases seem quite unlikely unless the recession is severe. In the post-WWII environment, severe US recessions have been accompanied by aggravating factors that appear to be missing in the current environment. In addition to this, there are several arguments pointing to the next US recession being a mild one. In a mild recession scenario, we doubt that the 10-year Treasury yield would fall below 2%, or fall below this level for very long. For fixed-income investors, while bond yields will fall for a time if a recession emerges, the implication is that investors should not overstay their welcome in a long-duration position during the recession and should be looking to reduce their duration exposure earlier rather than later. For equity investors, our findings underscore that meaningful downside risk exists for stocks even in a mild recession environment, because the decline in bond yields is not likely to offset a rise in the equity risk premium. We noted in our July report that if a recession occurred within the coming 6-12 months, that the S&P 500 would likely fall to 3100, even if the recession were average. A mild recession may see the S&P 500 decline less severely than this, but stocks are still likely to incur significant losses during the next recession unless investors price in a much shallower path for short-term interest rates than we believe will be warranted. As noted in Section 1 of our report, we have not yet concluded that a US recession is inevitable over the coming 6-12 months. Still, we acknowledge that the risks are quite elevated, and that substantial (further) supply-side and pandemic-related disinflation is likely needed for the US economy to avoid a contraction in output. Additional changes to our recommended cyclical allocation may thus occur over the coming few months, in response to incoming data, our assessment of the likely implications for monetary policy, and the response of long-maturity government bond yields. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 Please see The Bank Credit Analyst "Inflation Whipsaw Ahead," dated June 30, 2022, available at bca.bcaresearch.com 2 Please see The Bank Credit Analyst "August 2022," dated July 28, 2022, available at bca.bcaresearch.com

Highlights The odds of a Goldilocks outcome for the US economy increased somewhat in August, but the risks of a US recession over the coming year remain quite elevated. We continue to recommend that investors stay neutrally positioned towards equities within a global multi-asset portfolio. The disinflationary impulse from the July US CPI report is less compelling than it seems, in that it appears to have been mostly driven by declining energy prices. It is far from clear that energy prices will continue to decline over the coming months and are, in fact, likely to rise even if an Iranian deal takes place. This implies that investors may have jumped the gun in pricing in substantial disinflation and sharply higher odds of a Goldilocks economic outcome. The OIS curve is implying a reasonable path for the Fed funds rate for the remainder of this year, but it is too low 12 months from now based on the Fed’s median rate expectation for year-end 2023. This suggests that a further upward adjustment in the OIS curve is likely warranted, and that a modestly short duration stance is appropriate. Investors believe that the rate hike path priced into the OIS curve would not be recessionary, because short-term inflation expectations are pricing in a very substantial slowdown in headline inflation. From the perspective of market participants, this would both raise the recessionary threshold for interest rates (via stronger real wages) and could potentially allow the Fed to reduce interest rates closer to its (very likely wrong) estimate of neutral. We agree that the odds of a recession will decline if headline inflation does fall below 4% over the coming year, but it is not yet clear that this will occur. And if it does, the resulting improvement in real wages would ultimately allow the Fed to raise interest rates to a higher level before short-circuiting the economic expansion. As such, we expect real long-maturity government bond yields to rise meaningfully in a scenario where real wages recover significantly and a recession is avoided, which will put heavy pressure on equity multiples. This underscores that stock prices face risks in both a recessionary and non-recessionary environment. There are arguments pointing to a decline in the dollar beyond the near term, even within the context of elevated recessionary odds in the US and our recommended neutral stance towards global equities. Stay neutral for now, but look for opportunities to short the dollar beyond the coming few months. Jumping The Gun On Goldilocks The odds of a Goldilocks outcome for the US economy over the coming six to nine months increased somewhat in August. The July CPI report presented some evidence of supply-side and pandemic-related disinflation (Chart I-1), and we saw more resilient manufacturing production in the US – even after excluding the automotive sector – than many manufacturing indicators have been indicating (Chart I-2). In addition, the regional Fed manufacturing index in the especially manufacturing-sensitive state of Pennsylvania surprised significantly to the upside in July, although this was at least somewhat offset by a collapse in the New York and Dallas Fed’s general business conditions indexes (Chart I-3). Chart I-1There Is Now Some Evidence Of Supply-Side & Pandemic-Related Disinflation In The US

There Is Now Some Evidence Of Supply-Side & Pandemic-Related Disinflation In The US

There Is Now Some Evidence Of Supply-Side & Pandemic-Related Disinflation In The US

Chart I-2US Manufacturing Production Has Been More Resilient Than Surveys Would Have Suggested

US Manufacturing Production Has Been More Resilient Than Surveys Would Have Suggested

US Manufacturing Production Has Been More Resilient Than Surveys Would Have Suggested

Against the backdrop of significant recessionary risks, and a debate about whether negative growth in the first half of the year already constitutes a recession in the US, these developments have been positive. The Atlanta Fed’s GDPNow model is pointing to positive (albeit below-trend) growth of 1.4% in Q3, which is consistent with consensus forecasts. The Atlanta Fed’s model is also forecasting the strongest real consumption growth since Q4 2021 (Chart I-4). Equity investors responded to incrementally lower recession odds and a slower pace of inflation by bidding up the S&P 500 from roughly 3800 at the beginning of July to over 4200 in August. Chart I-3Mixed Messages From The Regional Fed Indicators

Mixed Messages From The Regional Fed Indicators

Mixed Messages From The Regional Fed Indicators

Chart I-4The Atlanta Fed GDPNow Model Is Pointing To Positive Growth And Resilient Consumption In Q3

September 2022

September 2022

However, several other developments over the past month continue to highlight that the risks of a US recession over the coming year are quite elevated, which supports our recommendation that investors stay neutrally positioned towards equities within a global multi-asset portfolio: The August flash PMIs were fairly negative, especially for the services sector. The August flash S&P Global manufacturing PMI rose in Germany, but it fell in the US, France, and the UK. Services PMIs declined significantly in all four countries, especially in the US where survey participants noted that “hikes in interest rates and inflation dampened customer spending as disposable incomes were squeezed.” Survey respondents also noted that “new orders contracted at the steepest pace for over two years, as companies highlighted greater client hesitancy in placing new work.” Chart I-5The Conference Board's LEI Is Very Weak

The Conference Board's LEI Is Very Weak

The Conference Board's LEI Is Very Weak

The Conference Board’s leading economic indicator dropped for a fifth month in a row in July, which has always been associated with a US recession (based on the indicator’s current construction). Chart I-5 highlights that the indicator’s market-based and real economy components are both very weak, and that the Conference Board’s coincident indicator has now fallen below its 12-month moving average. While the Philly Fed manufacturing index picked up in July, the new orders component of the regional Fed manufacturing PMIs broadly sank further into contractionary territory (Chart I-6). Chart I-6The Regional Fed New Orders Components Are Very Weak

The Regional Fed New Orders Components Are Very Weak

The Regional Fed New Orders Components Are Very Weak

The Atlanta Fed model shown in Chart I-4 is pointing to a second quarter of negative growth from real residential investment, a component of GDP that reliably peaks in advance of economic contractions.1 Job openings are now pointing to a potential rise in unemployment. The relationship between job openings and unemployment is currently subject to heavy debate, as discussed in a recent report by my colleague Ryan Swift.2 However, abstracting from a theoretical discussion about movements along or shifts in the Beveridge curve, investors should note that the empirical record is fairly clear – Chart I-7 highlights that falling job vacancies occurred alongside a significant rise in the level of unemployment during the last two recessions. We acknowledge that the relationship has seen some deviations since 2018/2019, so this may highlight that a larger decline in job openings will be required for unemployment to trend higher. A 10% rise in the level of unemployment relative to its 12-month moving average has always been associated with a recession, implying that a sustained decline in job openings to 10M or lower would represent a likely recessionary signal – even if that recession proves to be a mild one (see Section 2 of this month’s report). Chart I-7Declining Job Openings Are Pointing To Potentially Higher Unemployment

Declining Job Openings Are Pointing To Potentially Higher Unemployment

Declining Job Openings Are Pointing To Potentially Higher Unemployment

Table I-1 highlights that the disinflationary impulse from the July CPI report is less compelling than it seems, in that it appears to have been mostly driven by declining energy prices (particularly gasoline and fuel oil). Outside of the clear impact that falling fuel prices had on airline fares, there is not yet compelling evidence that core inflation is decelerating due to easing supply-side and pandemic-related effects, or due to slowing demand. As we will discuss below, it is far from clear that energy prices will continue to decline over the coming months and are, in fact, likely to rise even if an Iranian deal takes place. This implies that investors may have jumped the gun in pricing in substantial disinflation and sharply higher odds of a Goldilocks economic outcome. Table I-1The Disinflationary Impulse From The July CPI Report Is Less Compelling Than It Seems

September 2022

September 2022

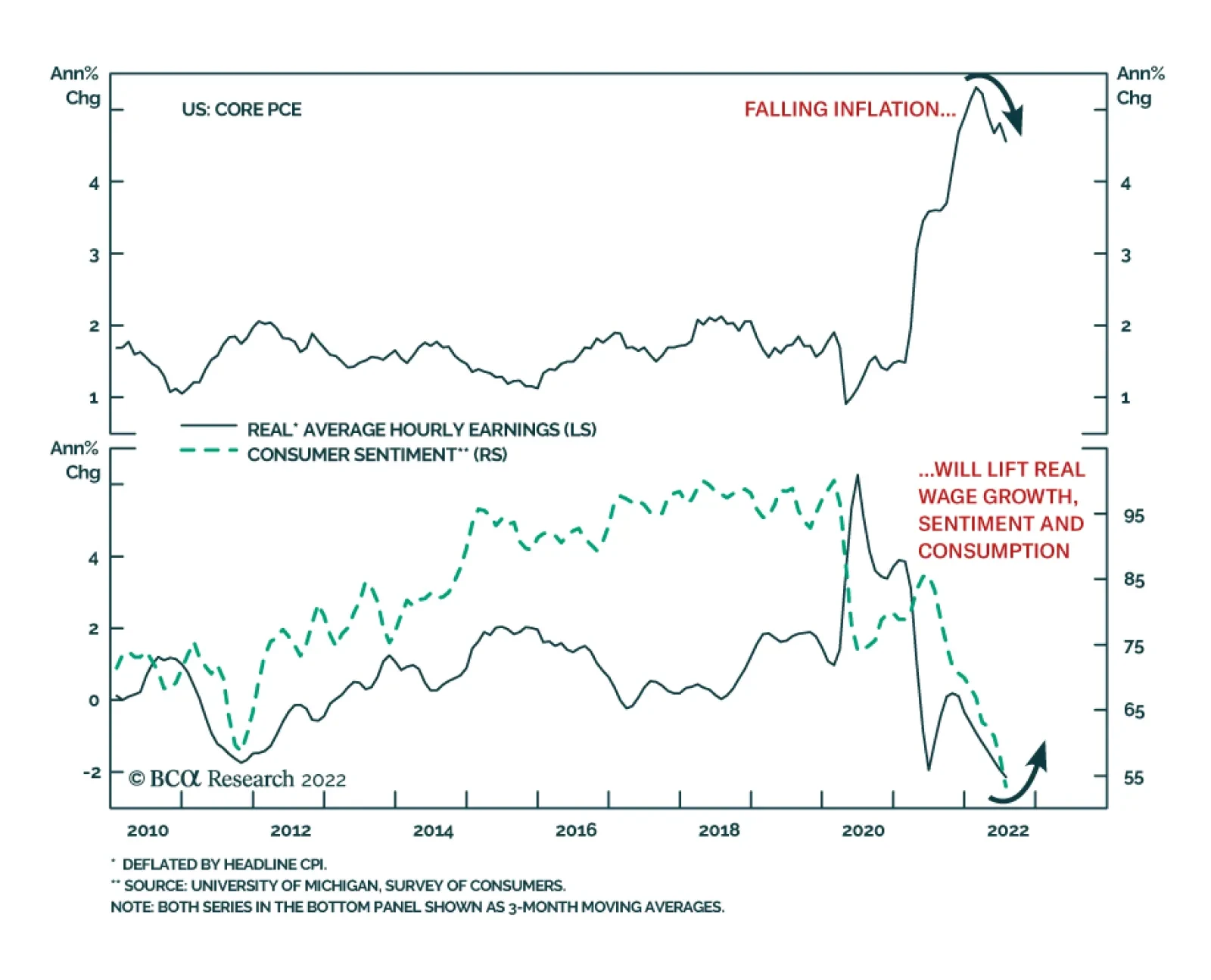

Inflation And The Fed As we discuss in Section 2 of our report, recessions occur because monetary policy becomes tight, a significant non-policy shock to aggregate demand or supply occurs, or some combination of both develops. We do not believe that monetary policy is currently restrictive on its own (Chart I-8), and we have not yet concluded that a US recession is inevitable. But when combined with the speed of adjustment in interest rates, the fact that real wages have fallen sharply (Chart I-9), and the fact that the Fed is determined to see inflation quickly return to target levels, it is clear that the odds of a recession over the coming 12-18 months remain elevated. Chart I-8Absent Declining Real Wages, The Current Level Of Interest Rates Would Not Be Restrictive

Absent Declining Real Wages, The Current Level Of Interest Rates Would Not Be Restrictive

Absent Declining Real Wages, The Current Level Of Interest Rates Would Not Be Restrictive

Chart I-9But Real Wages Are Declining, And The Pace Of Tightening Has Been Extraordinarily Rapid

But Real Wages Are Declining, And The Pace Of Tightening Has Been Extraordinarily Rapid

But Real Wages Are Declining, And The Pace Of Tightening Has Been Extraordinarily Rapid

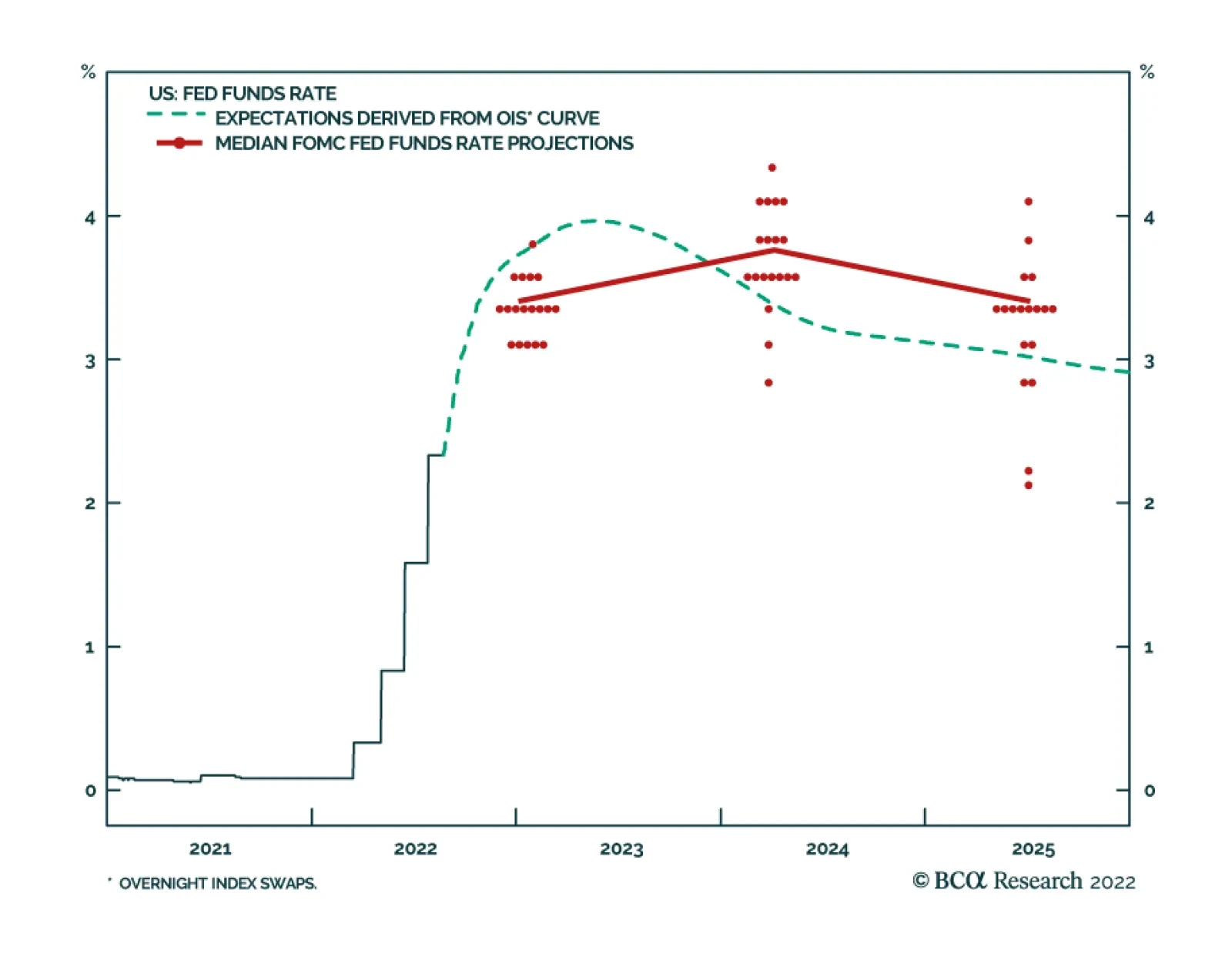

Many investors do not appear to fully appreciate the fact that the Fed will continue to tighten policy until it sees clear and unequivocal signs that inflation is easing. Importantly, the minutes of the July FOMC meeting highlighted that this is likely to be true even if unambiguous signs of easing supply-side and pandemic-related inflation present themselves. During the July meeting, FOMC participants noted that “though some inflation reduction might come through improving global supply chains or drops in the prices of fuel and other commodities, some of the heavy lifting would also have to come by imposing higher borrowing costs on households and businesses”. They also emphasized that “a slowing in aggregate demand would play an important role in reducing inflation pressures”. The upshot is that the Fed was aware before the July CPI report that energy-related inflation might fall, but also understood that they would still have to tighten enough to slow aggregate demand to reduce underlying inflationary pressures. It is true that investors are pricing in additional rate hikes from the Fed, but there are two caveats for investors to consider. The first is that while the OIS curve is implying a reasonable path for the Fed funds rate for the remainder of this year, it is too low 12 months from now based on the Fed’s median rate expectation for year-end 2023 (Chart I-10). This suggests that a further upward adjustment in the OIS curve is likely warranted. Second, and more importantly, investors appear to be making the assumption that the rate hikes already built into the OIS curve will not be recessionary. Investors are making this assumption because short-term inflation expectations are pricing in a very substantial slowdown in headline inflation (Chart I-11), which would both raise the recessionary threshold for interest rates (via stronger real wages) and could potentially allow the Fed to reduce interest rates closer to its (very likely wrong) estimate of neutral. Chart I-10A Further Upward Adjustment In The OIS Curve Is Likely Warranted

A Further Upward Adjustment In The OIS Curve Is Likely Warranted

A Further Upward Adjustment In The OIS Curve Is Likely Warranted

Chart I-11Short-Term Inflation Expectations Are Pricing In A Massive Deceleration In Headline Inflation

Short-Term Inflation Expectations Are Pricing In A Massive Deceleration In Headline Inflation

Short-Term Inflation Expectations Are Pricing In A Massive Deceleration In Headline Inflation

We agree with investors that the odds of a recession will decline significantly, ceteris paribus, if headline inflation does drop below 4% over the coming year. But we noted above that it is not yet clear that this will occur. In addition, we disagree with investors that this would result in a reduction in short-term interest rates, because this belief is based on the view that monetary policy is currently in restrictive territory even without the negative impact of sharply lower real wages. Absent the negative real wage effect, our view is that monetary policy would still be stimulative at current interest rates, which is why we believe that the 2023 portion of the OIS curve is too dovish in a non-recessionary scenario. The Outlook for Stocks The equity market rally that began in early July has been based on the assumption that significant supply-side and pandemic-related disinflation is now a fait accompli. If it is, then the odds of a recession over the coming year are indeed meaningfully lower, and the risk to corporate profits is less than feared. We noted above that investors may have jumped the gun in pricing in substantial disinflation and sharply lower odds of a US recession. But even in a scenario in which the odds of recession do come in significantly, stocks still face risks from a significant rise in real bond yields. Chart I-12Long-Maturity TIPS Yields Would Likely Rise In A Non-Recessionary Scenario, Compressing Equity Multiples

Long-Maturity TIPS Yields Would Likely Rise In A Non-Recessionary Scenario, Compressing Equity Multiples

Long-Maturity TIPS Yields Would Likely Rise In A Non-Recessionary Scenario, Compressing Equity Multiples

Investors have been focused on very elevated inflation as the driver of both rising inflation expectations and rising real bond yields, and have assumed that a meaningful slowdown in inflation (as forecast by short-term measures of inflation expectations) implies that the Fed funds rate will return to the Fed’s estimate of neutral. This belief, along with a lower projected Fed funds rate in 2024 than 2023 in the FOMC’s participant forecasts, is the basis for the 2023 “pivot” currently priced into the OIS curve. Given that the Fed funds rate has already reached the Fed’s neutral rate estimate, there is a meaningful chance that this estimate will be revised upwards by the Fed or challenged by investors if economic activity improves in response to a decline in inflation and a corresponding rise in real wages. Such a scenario would highlight to investors that the Fed’s estimate of neutral is likely too low, which would imply a significant increase in real 10-year TIPS yields (which are currently 160 basis points below their pre-2008 average). Chart I-12 highlights the impact that a rise in real long-maturity bond yields could have on equities, even in a non-recessionary scenario where 12-month forward earnings per share grows 8% over the coming year. A rise in 10-year TIPS yields to 1.5% by the middle of 2023 would cause a 16% contraction in the 12-month forward P/E ratio and a 10% decline in stock prices, assuming an unchanged 12-month forward equity risk premium (ERP). It is possible that the ERP could decline in a rising bond yield scenario. Chart I-13 highlights that the ERP is indeed negatively correlated with real bond yields (in part due to the methods that we use to calculate it). The counterpoint is that there are a number of risks that equity investors should be compensated for today that did not exist in the late 1990s or early 2000s, especially the risks of populist policies in many advanced economies and major geopolitical events (as Russia’s invasion of Ukraine recently highlighted). Chart I-14 illustrates that, since 1960, a long-term version of the equity risk premium, calculated using trailing earnings and our adaptive expectations proxy to deflate long-maturity bond yields, has been fairly well explained by the Misery Index (the sum of the unemployment and headline inflation rates). However, the chart also shows that the ERP has been structurally higher over the past decade than the Misery Index would have predicted. It is unclear if this is due to a riskier environment or the negative ERP/real yield correlation that we noted. Chart I-13The Equity Risk Premium Could Come Down As Bond Yields Rise, But That Is Not Guaranteed

The Equity Risk Premium Could Come Down As Bond Yields Rise, But That Is Not Guaranteed

The Equity Risk Premium Could Come Down As Bond Yields Rise, But That Is Not Guaranteed

Chart I-14A Structurally Higher ERP Over The Past Decade Could Represent Needed Compensation For Structural Risks

A Structurally Higher ERP Over The Past Decade Could Represent Needed Compensation For Structural Risks

A Structurally Higher ERP Over The Past Decade Could Represent Needed Compensation For Structural Risks

The conclusion is that investors do not yet appear to have a basis to bet on a declining ERP in a rising bond yield environment, underscoring that even a non-recessionary scenario poses a risk to stock prices. It is worth noting that this second risk facing stocks has essentially been caused by the Fed because of its maintenance of a very low neutral rate estimate that we feel is no longer economically justified. Bond Market Prospects Chart I-15Investors Should Stay Modestly Short Duration, For Now

Investors Should Stay Modestly Short Duration, For Now

Investors Should Stay Modestly Short Duration, For Now

Over the past few months, the Bank Credit Analyst service has continued to recommend that investors maintain a modestly short duration stance even as we recommended reducing equity exposure. The recent rise in the 10-year Treasury yield back to 3% has validated that view (Chart I-15), and reinforces our view that there is significant upside risk to long-maturity bond yields in a non-recessionary scenario. Our expectation that the Fed will raise interest rates to a higher level over the next year than the OIS curve is currently discounting also argues for a modestly short stance, based on BCA’s “Golden Rule” framework. The “Golden Rule” states that investors should set their overall bond portfolio duration based on how their own 12-month fed funds rate expectations differ from the expectations that are priced into the market. As we detail in Section 2 of our report, the Fed has always cut interest rates in response to a recession in the post-WWII environment, so we would certainly recommend a long duration stance if a recession emerges. But given our view that a recession is still a risk rather than a likely event, we feel that a modestly short duration stance is currently appropriate. Chart I-16US Corporate Bond Value Has Improved, But Not Enough To Trump The Cycle

US Corporate Bond Value Has Improved, But Not Enough To Trump The Cycle

US Corporate Bond Value Has Improved, But Not Enough To Trump The Cycle

As noted above in our discussion of the risks facing stock prices in a non-recessionary scenario, falling inflation that is not associated with a recession will ironically be a bearish signal for long-maturity bonds, because it means that the Fed will have greater capacity to raise interest rates without ending the recovery. The short end of the yield curve could be flat or move modestly lower in response to a significant easing in inflation, but the long end of the curve would be at serious risk of moving higher. We are thus very likely to recommend a short duration stance in response to solid evidence of true supply-side and pandemic-related disinflation, assuming it emerges outside of the context of a recession. Within the credit space, the rise in US corporate bond spreads since the start of the year has meaningfully improved the value of investment- and speculative-grade corporate bonds (Chart I-16), but not so much that it justifies a positive stance towards these assets relative to government bonds given the risks facing the US economy. We continue to recommend an underweight stance towards investment-grade and a neutral stance towards speculative-grade within a fixed-income portfolio. The Outlook For Energy Prices Chart I-17The EU's Oil Embargo Will Cause Russian Oil Production To Tank

The EU's Oil Embargo Will Cause Russian Oil Production To Tank

The EU's Oil Embargo Will Cause Russian Oil Production To Tank

The likely path of commodity prices, particularly that of oil, is an extremely important determinant of whether the US is likely to experience a recession over the coming year. We are among those who have downplayed the significance of oil price shocks in driving contractions in economic output over the past two decades,3 but the current situation is unique given the role that very elevated inflation has played in driving real wages lower. In a recent Strategy Report from our Commodity & Energy Strategy service, my colleague Robert P. Ryan underscored the impact that the European Union’s embargo of Russian oil will likely have on the energy market. If fully implemented, ~ 2.3mm barrels/day of seaborne imports of Russian crude oil will be excluded from EU markets by year-end. EU, UK and US shipping insurance and reinsurance sanctions are also scheduled to be implemented in December, which means that “surplus” Russian oil production cannot be fully reoriented to other countries. Chart I-17 presents the likely impact on Russia’s crude oil output, namely a ~ 2mm barrels/day decline in oil output by the end of next year – nearly equal to the amount of oil set to be embargoed. Our base case view remains that supply and demand in the oil market will remain relatively balanced going into the winter, but the removal from the market of Russian oil production because of the various EU embargoes – even if it is offset by the return of 1mm b/d of Iranian exports on the back of a deal with the US – will ultimately push crude oil prices higher and inventories lower (Chart I-18). The price impact of this event could happen earlier than the immediate supply/demand balance would suggest, if investors have not fully priced in the extent of the decline in Russian oil production that our commodity team is forecasting. Our commodity team’s forecast serves as an important reminder that the economic consequences of Russia’s invasion of Ukraine may not be fully behind us. It also highlights that the recent disinflation observed in the US, which was mostly driven by lower energy prices in July, may not be sustained. Chart I-19 highlights what could happen to US gasoline prices based on the path for oil shown in Chart I-18, and how that forecast is sharply at odds with the current gasoline futures curve. Chart I-20 highlights that US gasoline stocks are currently below their 5-year average; the last time this occurred was in Q1 2021, which was an environment of rising gasoline prices to levels that were higher than what would usually be implied by crude oil prices. Chart I-18Oil Prices Are More Likely To Rise Than Fall

Oil Prices Are More Likely To Rise Than Fall

Oil Prices Are More Likely To Rise Than Fall

Chart I-19Higher Oil Prices Would Cause Gasoline Prices To Deviate Significantly From Market Expectations

Higher Oil Prices Would Cause Gasoline Prices To Deviate Significantly From Market Expectations

Higher Oil Prices Would Cause Gasoline Prices To Deviate Significantly From Market Expectations

Chart I-20Gasoline Stocks Are Low In The US, Underscoring The Upside Risk To Prices

Gasoline Stocks Are Low In The US, Underscoring The Upside Risk To Prices

Gasoline Stocks Are Low In The US, Underscoring The Upside Risk To Prices

The upshot is that our commodity team expects oil prices to move higher over the coming 6-12 months, under the assumption that the EU’s embargo against Russian oil moves forward as announced. This poses a clear threat to imminent supply-side and pandemic-related disinflation, and underscores the risks to a Goldilocks economic outcome over the coming few months. The Dollar: Value, Technical Conditions, And The Cycle Chart I-21The Dollar Is Reliably Countercyclical, But It Has Registered Outsized Gains Over The Past Year

The Dollar Is Reliably Countercyclical, But It Has Registered Outsized Gains Over The Past Year

The Dollar Is Reliably Countercyclical, But It Has Registered Outsized Gains Over The Past Year

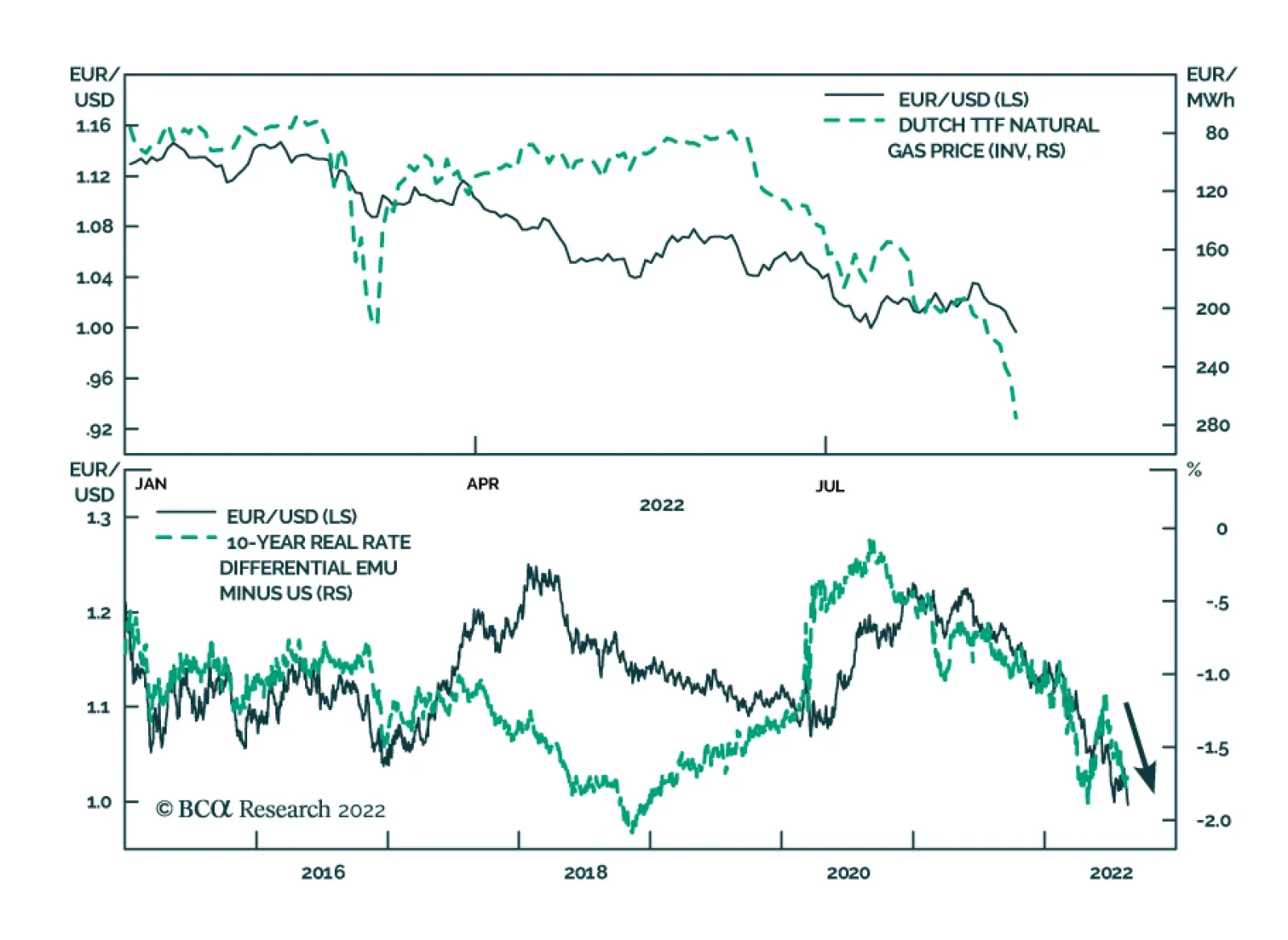

The US dollar moved higher over the past month, after first retreating from its mid-July high for the year. We tempered our view about the likelihood of a falling dollar over the near term in last month’s report, but from a bigger picture perspective we have been surprised by the degree of dollar strength this year. The US dollar is a reliably countercyclical currency, so clearly some of the dollar’s strength has been the result of weakness in risky asset prices (Chart I-21). But the bottom panel of Chart I-21 highlights that the broad trade-weighted dollar has performed even better over the past year than returns to the S&P 500 would have implied, underscoring that the magnitude of the dollar’s strength has been atypical. The last two times that the US dollar performed substantially better than the trend in risky assets would have implied were in 2012 and 2015, years in which euro area breakup risk was a driving force in markets. Alongside the fact that EURUSD has fallen below parity and USDEUR has outperformed even more than the broad trade-weighted dollar has, “excess” dollar returns point strongly to Europe’s energy woes in the aftermath of Russia’s invasion of Ukraine as the key driver of outsized broad dollar strength. Chart I-22 highlights that European natural gas prices have exceeded the level that we had forecasted would occur in a complete cutoff scenario, meaning that Europe’s energy crunch is likely happening now, rather than in the winter. However, even considering the negative economic outlook facing the euro area, there are arguments pointing to a decline in the dollar beyond the near term – even within the context of elevated recessionary odds in the US and our recommended neutral stance towards global equities. First, Chart I-23 highlights that EURUSD has undershot what the trend in relative real interest rates would suggest, which has historically led changes in the euro. This implies that the euro has declined partly because of the introduction of a sizeable risk premium, which may dissipate after the winter. Chart I-22The Euro Has Been Heavily Impacted By Europe's Energy Crunch

The Euro Has Been Heavily Impacted By Europe's Energy Crunch

The Euro Has Been Heavily Impacted By Europe's Energy Crunch

Chart I-23EURUSD Has Undershot What The Trend In Relative Real Interest Rates Would Suggest

EURUSD Has Undershot What The Trend In Relative Real Interest Rates Would Suggest

EURUSD Has Undershot What The Trend In Relative Real Interest Rates Would Suggest

Second, Chart I-24 highlights that the US dollar is extremely overbought and is technically extended to a point that has historically been associated with reversals in the broad dollar trend. Finally, Chart I-25 highlights that the US dollar is extraordinarily expensive based on our valuation models, underscoring that an eventual decline in the dollar may be quite severe. We agree that valuation is not usually an effective market timing tool, but investors should place a greater weight on valuation measures as they are stretched further. Based either on our models or a more traditional PPP approach, the degree of US dollar overvaluation is extreme – arguing for a bearish bias on a 6-12 month timeline barring an unambiguous move towards recession in the US. Chart I-24US Dollar And Indicator The US Dollar Is Heavily Overbought

US Dollar And Indicator The US Dollar Is Heavily Overbought

US Dollar And Indicator The US Dollar Is Heavily Overbought

Chart I-25The US Dollar Is Extremely Expensive

The US Dollar Is Extremely Expensive

The US Dollar Is Extremely Expensive