United States

Executive Summary US Support For A Military Coup?

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

A confluence of structural and cyclical factors makes the US highly prone to social and political instability, as in 2020. Today’s stagflationary economic environment further amplifies domestic political risk. The Biden administration’s decision to pursue a criminal investigation of former President Trump will drive political polarization higher, as will the overall 2022-24 political cycle. Investors should expect negative surprises from US politics, including social unrest, political violence, and domestic terrorism of whatever stripe. Such crisis events usually cause only a short-term spike in financial market volatility. A major crisis that affects election results could have a more lasting impact. The base case for US policy in 2023-24 is gridlock, which is marginally disinflationary. It would take an extraordinary surprise to change that. On a relative basis, US assets benefit from domestic political risk because geopolitical risk rises even faster. Recommendation (Tactical) INITIATION DATE Return Long DXY (Dollar Index) Feb 23, 2022 10.8% Bottom Line: Investors should expect volatility and negative “October surprises” in the short term, at least through the midterm elections. US domestic political risk is high and will also amplify global geopolitical risk. Feature The US’s rolling political crisis is escalating again and political violence is likely to rise in the lead up to the midterm elections on November 8 and the presidential election in November 2024. The Department of Justice (DoJ) refused on August 15 to release the affidavit underpinning the Federal Bureau of Investigation’s (FBI) raid on former President Trump’s Mar-a-Lago residence in Florida. Never before has a US president suffered a raid on his home by the country’s federal law enforcement agencies – though presidents have been investigated before. It is not yet clear what charges will be brought against Trump but it is highly likely that he will be indicted for something. The Justice Department released a redacted version of the search warrant suggesting that Trump may be accused of having kept state secrets at his home in violation of the Presidential Records Act and possibly also the 1917 Espionage Act. Speculation says that some information he took back from the White House relates to nuclear weapons.1 The DoJ is pursuing a criminal investigation. The former president could very well end up on trial, or even in jail, but it is also possible that changes in political power will prevent him from going. What are the investment implications, if any? The US will see significant social and political upheaval but the main investment implication is that the US will continue to play an unpredictable and disruptive role abroad, perpetuating a flight to safety in financial markets, at least until the midterm elections are over. Drivers Of US Political Instability The US political crisis should first be seen through the lens of geopolitics: The US is a continent-sized nation that is separated from the other world powers by large oceans. It is therefore highly defensible and economically insulated, with total exports accounting for only 10.2% of GDP. However, this insularity and relative security create space for a fast growing and evolving society that is primarily focused on doing business rather than strengthening the state. The rapid creation of wealth is good but also produces large disparities in region, class, and race that periodically undermine stability. Maintaining domestic stability across the continent would be a constant challenge even if the government were not a federal republic with short political cycles driven by fickle popular opinion. Freedom is a source of political contention as well as wealth creation. Over the past 70 years the society has become less religious and more secular, while the economy has become less manufacturing-oriented and more service-oriented. The shift to a high-tech and information-driven society has empowered the highly educated at the expense of the less educated. Capital owners have benefited from rising asset values, deregulation, and globalization, while labor has witnessed stagnant real wages. Agricultural and manufacturing regions have fallen behind. Social stability is especially hard to maintain during cyclical periods of economic distress, highlighted today by the rising Misery Index (Chart 1). While inflation may subside in the short run, it will probably persist in the long run, and unemployment has nowhere to go but up. There is a demographic and generational factor that is also driving US instability today: The Baby Boom generation did not begin their adult lives with a robust policy consensus, like their parents’ generation, which shared sacrifices during the Great Depression and World War II. Instead the Boomers began with deep divisions due to the Vietnam War and social revolution of the 1960s. As they grew in wealth and power in the 1980s-90s, pro-growth tax policy, deregulation, and rapid socioeconomic changes aggravated these divisions. Inequality surged (Chart 2). The Iraq War and 2008 financial crisis made matters worse. Chart 1US: High Misery Index

US: High Misery Index

US: High Misery Index

Chart 2US: High Inequality

US: High Inequality

US: High Inequality

Now the elites of this generation, who lead the two major parties, are trying to secure their economic and political interests before retirement and death. Bluntly, the pro-business faction is trying to prevent the pro-government faction from clawing back its wealth. Political polarization has reached the highest level since the early twentieth century (Chart 3). While polarization has subsided from the peaks of 2020, it could still exceed those peaks in the 2022-24 political cycle. The US will remain at or near “peak polarization” until generational change and geopolitical conflicts forge a new policy consensus. Bottom Line: The US is geopolitically secure but periodically struggles to maintain domestic stability. Today it is witnessing a confluence of structural and cyclical factors that generate social unrest and historic levels of political polarization. The 2022-24 election cycle will be tumultuous. Chart 3US: Peak Polarization

US: Peak Polarization

US: Peak Polarization

Disaffection Can Lead To Violence Any kind of fanaticism can lead to violent extremism. Militants have emerged from secular movements on the right and left, from communism to fascism, as well as from religious movements.2 In recent years the US has seen a rise in violence, including crime and terrorism. Mass shootings have spiked since the 2008 financial crisis. Terrorism has revived to the highest levels since the 1980s, 96% of which is domestic terrorism (Chart 4). Recent improvements to the social safety net may or may not reduce violence. The stagflationary economic backdrop bodes ill. Opinion polls are of dubious accuracy when they ask people to admit to militant or criminal inclinations, but they still take the temperature of society. Several recent polls suggest that as many as 25% of Americans are willing to consider violence as a means of resolving political problems (Chart 5). Chart 4US: Domestic Terrorism, Political Violence

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

Chart 5US Support For Political Violence?

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

In addition, 55% of Republicans and 40% of independents claim that a military coup could be justified when there is “a lot of corruption,” a subjective standard to say the least (Chart 6). While this number has spiked over the 2020 election cycle, it also shows a substantial pre-existing willingness to entertain authoritarian solutions to political disputes. We do not take these polls at face value given the difficult subject matter. When a major violent event occurs and real people die, popular “support” for political violence will collapse across the United States. Nevertheless these data suggest a high level of disaffection and discontent, which is supported by the structural socioeconomic problems cited above. Chart 6US Support For A Military Coup?

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

The January 6, 2021 incident at the US Capitol was the crescendo of an explosion of social unrest that occurred across the country in 2020, triggered by the aforementioned structural factors, the Covid-19 pandemic, race riots, and political conflict over the 2020 election. The number of homicides rose to 7.4 per hundred thousand people, the highest annual number since the 1990s, higher than in 2001 when the 9/11 terrorist attacks occurred, and reminiscent of the turbulent late 1960s. This year’s midterm elections will be the first major electoral test since the chaotic events of 2020 and none of the underlying drivers of unrest have been resolved. On the contrary, recent signs are pointing to another escalation of social and political upheaval. The 2024 election will also spark unrest and violence. Bottom Line: The number of violent incidents is rising while a substantial minority of public opinion appears willing to entertain violent means of resolving political disputes. From Reality TV To Real Rebellion? The FBI’s raid on Trump’s Mar-a-Lago estate is naturally triggering a backlash from Trump supporters and Republicans. These groups were already distrustful of the federal government and particularly the FBI for spying on the Trump presidential campaign in the 2016 election.3 Republican support for the FBI and DoJ will fall sharply from its current level in opinion polling taken in 2019 (Chart 7, top panel). Trump opponents will argue that Trump is being investigated because of wrongdoing while Trump supporters will think that the Biden administration is trying to prevent him from running for re-election in 2024. Any lack of transparency by the Justice Department will heighten suspicion and acrimony. Chart 7US Views On 2021 Rebellion

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

A fraction of radicalized Trump supporters could be motivated by this extraordinary event to conduct attacks. Already an armed suspect, allegedly linked to a right-wing extremist group and to the January 6 rebellion at the Capitol, attempted to storm an FBI field office in Cincinnati, Ohio. The Department of Homeland Security and FBI have warned about the risk of domestic terrorism for several years and have issued a new warning since the FBI raid on Mar-a-Lago.4 There is no easy way to resolve the dispute over the 2020 election or the January 6 rebellion because these events have taken on mythic status in the eyes of the different factions. For about half of Republicans, the January 6 incident was a patriotic defense of freedom – rather than an insurrection or attempt to prevent the peaceful and democratic transfer of power (Chart 7, bottom panel). Some small portion of those who view the election as stolen could become radicalized and act out violently. Trump received 46% of the popular vote in 2016 and 47% in 2020 (Chart 8). His favorability has suffered since the January 6 events but not as much as one might think. Among Republicans, Trump’s favorability remains largely unperturbed (Chart 9). While the vast majority of these voters are law-abiding, the decision to raid Trump’s home, and any future decision to press criminal charges, will drastically increase the risk of radicalization on the fringes. Chart 8Trump’s Share Of Popular Vote

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

Chart 9Trump’s Popular Support Post-2020

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

It does not take a social scientist to recognize the potential for an increase in political violence if the federal government is perceived as using the arm of the law to prevent a popular candidate from contesting past or future elections. The risk of political violence cannot be dismissed because the US is a particularly well-armed country. There were 120 civilian-held firearms per 100 persons in the United States as of 2017. By contrast, the nearest country is France, with only 20 firearms per 100 persons (Chart 10). That does not mean that a major incident of violence will necessarily stem from the right wing. Only five years ago an extremist left-wing gunman tried to assassinate a whole group of Republican lawmakers while they were playing baseball. Earlier this year the Department Homeland Security warned about violent reactions to the Supreme Court’s overturning of the Roe v. Wade decision on abortion.5 If and when a major incident of political violence occurs, the public reaction will be a powerful rejection of violence across the political spectrum. For example, President Bill Clinton’s administration benefited from the Oklahoma City bombing in 1995 (Chart 11). Much will depend on the nature of the attack and which faction is most able to capitalize on its victimization. Chart 10Right To Bear Arms Shall Not Be Infringed

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

Chart 11OKC Bombing Spurred Rally Round The Flag

OKC Bombing Spurred Rally Round The Flag

OKC Bombing Spurred Rally Round The Flag

Ultimately instability will generate a popular consensus opposed to political violence and supportive of law and order, just as it did in previous periods of American upheaval. The future policy consensus will be “federalist” in orientation due to America’s geopolitics: there will be an increasing need to unify the states to achieve other strategic imperatives like prosperity and national security. We call this theme “Limited Big Government.” This re-centralization process will involve the federal government intervening to stabilize the society. It is not obvious which political party will first capture this consensus. It depends on the nature and timing of any crisis events and the cyclical rotation of parties. Bottom Line: The US is a heavily armed country that is currently prone to social and political instability. The risk of political violence and domestic terrorism of whatever stripe is already very high. In addition, a substantial portion of the country’s right-wing faction believes that the 2020 election was stolen, that the January 6 rebellion was justified, and that the federal government is now abusing its law enforcement powers to prevent a candidate from running in 2024. Domestic terrorism risk will increase. Implications For The 2024 Election Federal agencies were well aware of the risk of a domestic backlash when they decided to raid Mar-a-Lago. Investigators may or may not produce ironclad evidence of wrongdoing by Trump, but polarization will continue to be the overriding dynamic in the short run. It is unlikely that any evidence will convince the different parties to change their opinions of Trump. Assuming Republicans retake the House of Representatives this fall, they will likely impeach Biden, though they will lack the votes in the Senate to remove him from office. US domestic policy will be effectively paralyzed as the partisan conflict continues. The 2024 election will be required to settle the Trump saga and the future direction of US national policy. Trump’s legal troubles could be a blessing or a curse for the Republican Party in the 2024 cycle: If Trump is disqualified or put in jail, then he will become a political martyr for his populist base, motivating Republican voter turnout. At the same time, the Republican Party establishment will gain the advantage of nominating a more favorable candidate who will be eligible to hold the presidency for eight years. Republicans would benefit. If Trump is not disqualified, then he will be even more incentivized to run for the Republican nomination to avoid legal prosecution. In that case he will hinder Republican appeal among moderate and independent voters – leaving them vulnerable to a party split or third-party challenge. Even if he wins, he will only be eligible for the presidency for four years, limiting his party’s prospects. Republicans would suffer. The takeaway from the above is that Trump’s interests continue to be at odds with the interests of the Republican Party elite. If the Democrats aggressively prosecute Trump and try to put him behind bars, they will in fact help unify and motivate the Republican Party opposition. Two further conclusions can be drawn: First, because of the January 6 incident and the political fallout, any future attempt by protesters or rioters to storm a major federal power center will likely be met with overwhelming force rather than accommodation. If that occurs, and state violence is seen as partisan, then the party that uses force will suffer in public opinion. As with domestic terrorism, a major crisis is likely to occur. But it will ultimately be conducive to a new national policy consensus. Second, US domestic instability will incentivize foreign powers to take advantage of US distraction to pursue their national interests aggressively in their own region. At the same time, the US government will also pursue a reactive foreign policy to attempt to divide the opposition and suppress domestic dissent. Therefore US domestic political instability increases global geopolitical instability. Market Response Will Be Volatility What are the investment ramifications of the above? US corporate earnings are heavily insulated from political crises that do not affect either US policy or the structure of the government and economy. Volatility sometimes pops briefly during domestic terrorist events but not in a way that affects the investment outlook (Chart 12). Investors should bear this in mind since another crisis event is coming. True, if the Mar-a-Lago raid affects the midterm election – and hence the composition of the US government in 2023-24 – then financial markets will respond to some extent. However, investors can safely ignore this risk because the stagflationary economy will be the chief factor in the midterms and already favors the opposition party. For the same reason it remains highly likely that Republicans will retake the House of Representatives, producing legislative gridlock in 2023. The result is disinflationary in the short run, though inflation will be a persistent problem over the long run. If Democrats somehow retain control of both houses of Congress, i.e. the “Blue sweep risk,” then investors would see a substantial change in the policy outlook, as Democrats would have a second chance to raise taxes and social spending. But the odds of a blue sweep are low. Our House election model implies that Democrats will lose 22 seats when they only need to lose a net of five seats to lose control. Our Senate model gives 47.5% chance of Democrats retaining control, too close to call at this point (Appendix). The odds of another blue sweep are only 20% according to online betting market PredictIt. Chart 12Market Historically Ignores Domestic Terrorism

Market Historically Ignores Domestic Terrorism

Market Historically Ignores Domestic Terrorism

US political instability has, if anything, supported the US dollar and US equity and bond outperformance for many years. The more unstable the US, the more unstable the world. Indeed, because of the US’s geopolitical position, the US often exports domestic instability to the rest of the world. That is the situation today as the Biden administration’s domestic-focused, reactive foreign policy exacerbates the conflicts with Russia and China. The Biden administration is willing to escalate strategic tensions with both China and Russia in the lead-up to the midterm elections – and this tendency will likely become the Biden Doctrine, lasting into 2024. Investors should remain defensively positioned, and overweight US assets, at least until the midterm election is over. Matt Gertken Senior Vice President Chief US Political Strategist mattg@bcaresearch.com Footnotes 1 Read the warrant behind FBI search of Trump’s Mar-a-Lago,” PBS, August 12, 2022, pbs.org. 2 See Katarzyna Jasko et al, “A comparison of political violence by left-wing, right-wing, and Islamist extremists in the United States and the world,” PNAS [Proceedings of the National Academy of Sciences of the United States of America] 119:30 (2022), July 18, 2022, pnas.org. See also Herbert McClosky and Dennis Chong, “Similarities and Differences between Left-Wing and Right-Wing Radicals,” British Journal of Political Science 15:3 (1985), pp. 329-63, jstor.org. 3 See Jessica Lee, “Did Obama Get Caught ‘Spying’ on Trump’s 2016 Campaign?” Snopes, September 29, 2020, snopes.com. See also Wall Street Journal Editorial Board, “Trump Really Was Spied On,” February 14, 2022, wsj.com. 4 See Department of Homeland Security, “Strategic Intelligence Assessment and Data on Domestic Terrorism,” July 11, 2022, dhs.gov; Christopher Wray, “Worldwide Threats to the Homeland,” Federal Bureau of Investigation, September 17, 2020, fbi.gov. See also Ryan Lucas, “FBI, Homeland Security warn about threats to law enforcement after Trump search,” NPR, August 15, 2022, npr.org. 5 See Stef W. Kight, “DHS memo: Violent extremism ‘likely’ in wake of Roe v. Wade decision,” Axios, June 24, 2022, axios.com. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

Table A3US Political Capital Index

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

Chart A1Presidential Election Model

Third Quarter US Political Outlook: Last Ditch Effort

Third Quarter US Political Outlook: Last Ditch Effort

Chart A2Senate Election Model

Third Quarter US Political Outlook: Last Ditch Effort

Third Quarter US Political Outlook: Last Ditch Effort

Table A4House Election Model

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Table A5APolitical Capital: White House And Congress

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

Table A5BPolitical Capital: Household And Business Sentiment

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

Table A5CPolitical Capital: The Economy And Markets

Trump Raid Heightens Political Risk

Trump Raid Heightens Political Risk

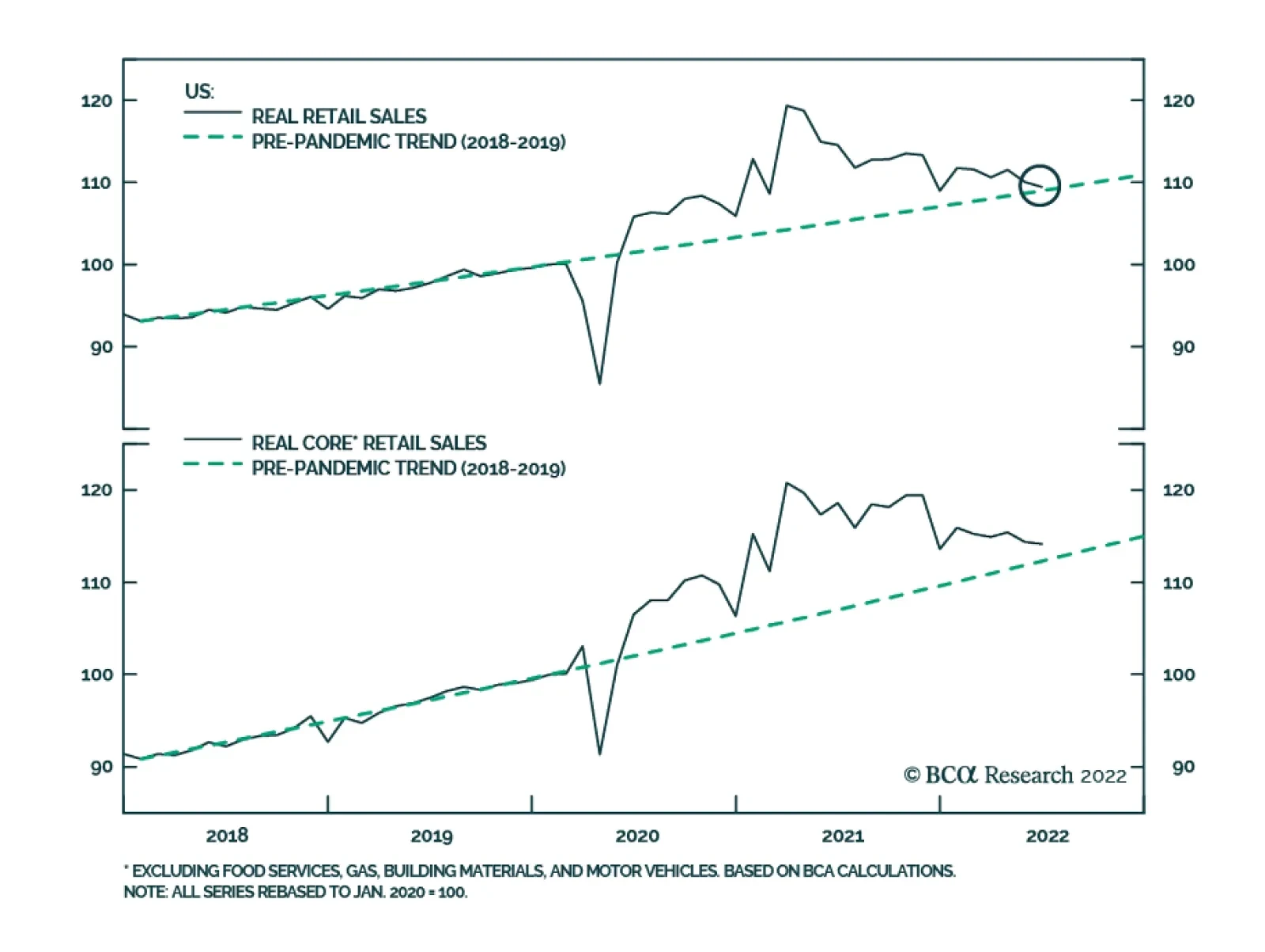

US retail sales were unchanged m/m in July, and the previous month’s positive surprise was revised downwards to 0.8% m/m. Declines in the sales of motor vehicles and parts, as well as in gasoline prices, offset gains from nonstore retailers, building…

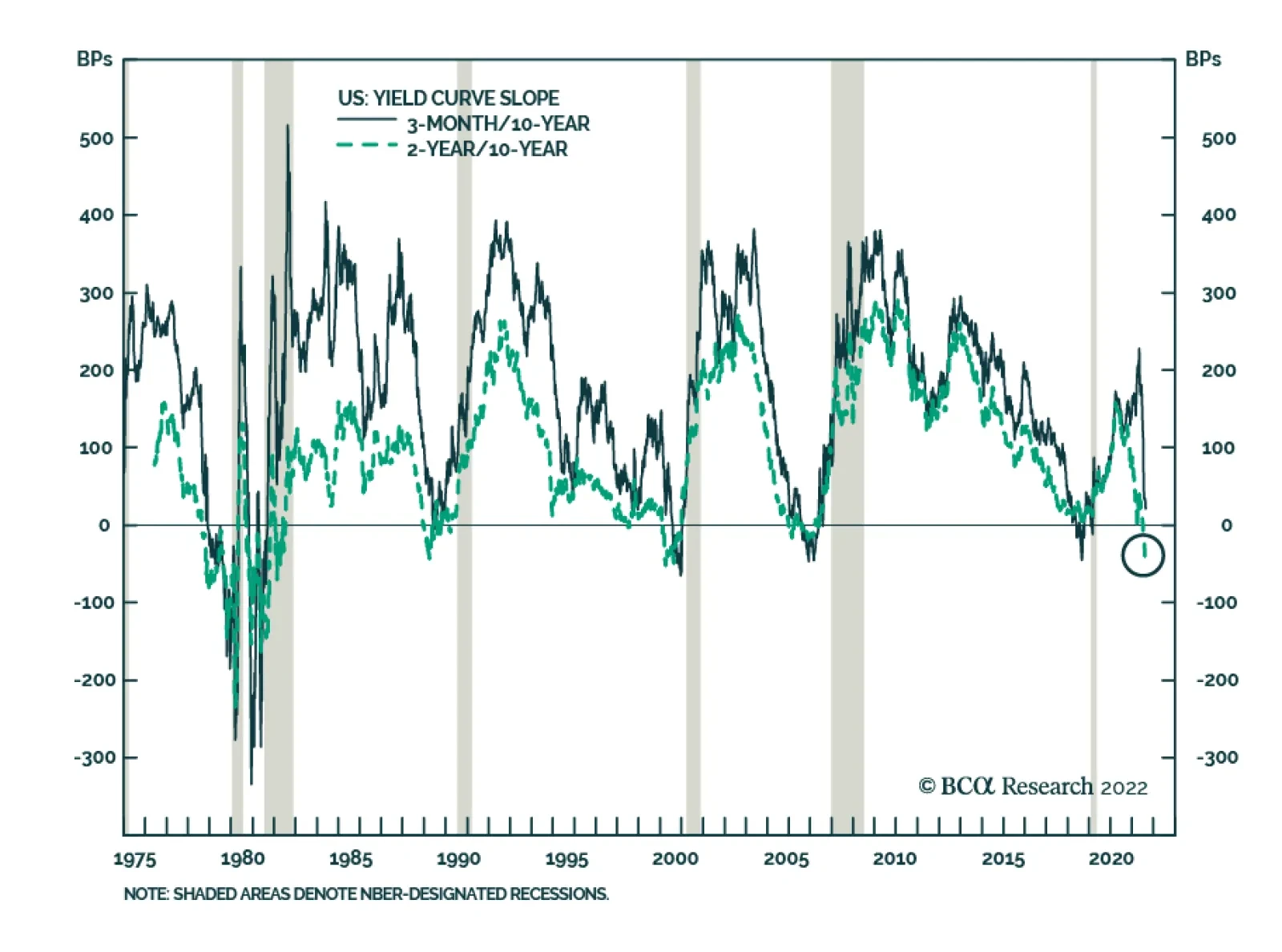

Despite all the worries, the most reliable yield curve slope measure, the 3-month/10-year segment, is not yet sending a recessionary signal. At 14bps, it is very flat, but recessions only follow an actual inversion, not a mere flattening episode. However, the…

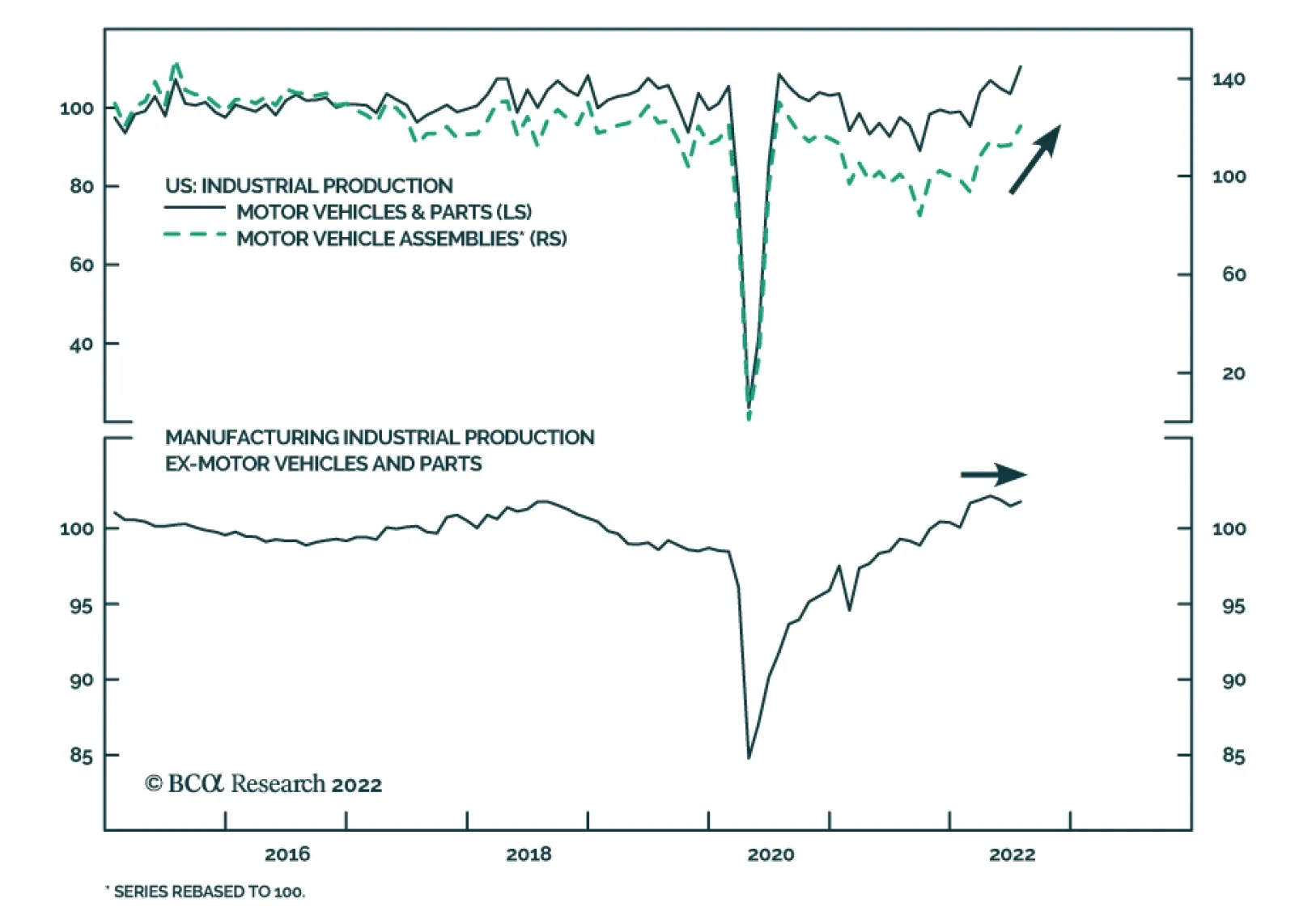

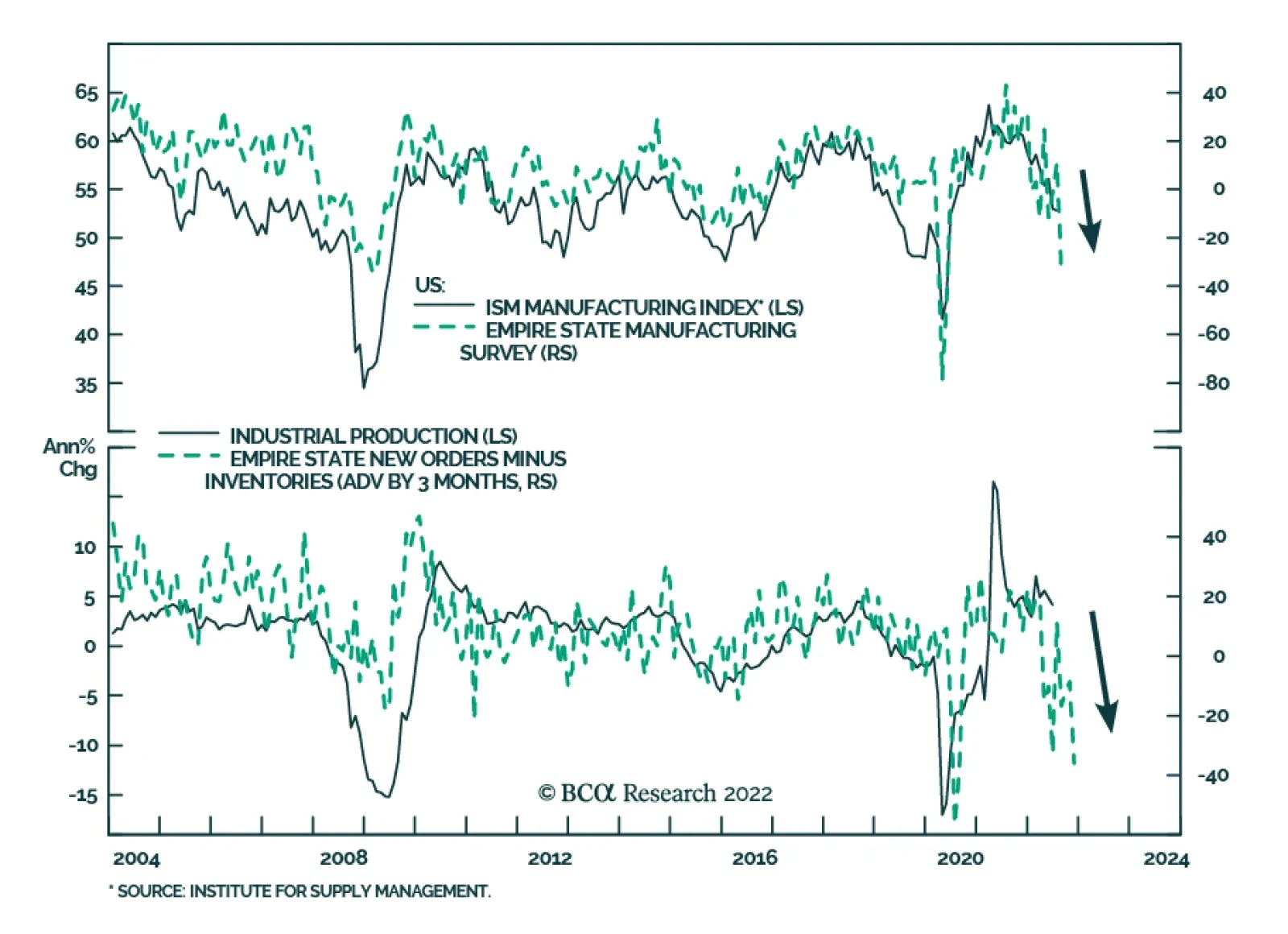

US industrial production grew 0.6% m/m in July, exceeding expectations of 0.3%. Capacity utilization also firmed to 80.3% in July, from 80.0%. These figures contrast with the previously released August Empire State manufacturing survey which sent a poor…

BCA Research’s US Political Strategy & US Equity Strategy services conclude that Biden’s legislative victories are not disinflationary. The bill does not stand alone but is part of the Biden administration’s “last-ditch effort” to pass two major bills…

Dear Client, This week, the US Bond Strategy service is hosting its Quarterly Webcast (August 16 at 10:00 AM EDT, 15:00 PM BST, 16:00 PM CEST). In addition, we are sending this Quarterly Chartpack that provides a recap of our key recommendations and some charts related to those recommendations and other areas of interest for US bond investors. Please tune in to the Webcast and browse the Chartpack at your leisure, and do let us know if you have any questions or other feedback. To view the Quarterly Chartpack PDF please click here. Best regards, Ryan Swift, US Bond Strategist Treasury Index Returns Spread Product Returns

The gauge of manufacturing activity in the state of New York slumped 42 points to a -31.3 contraction in August, largely disappointing expectations of a relatively more muted deterioration. Notably, new orders and shipments contracted by 36 points and 49…

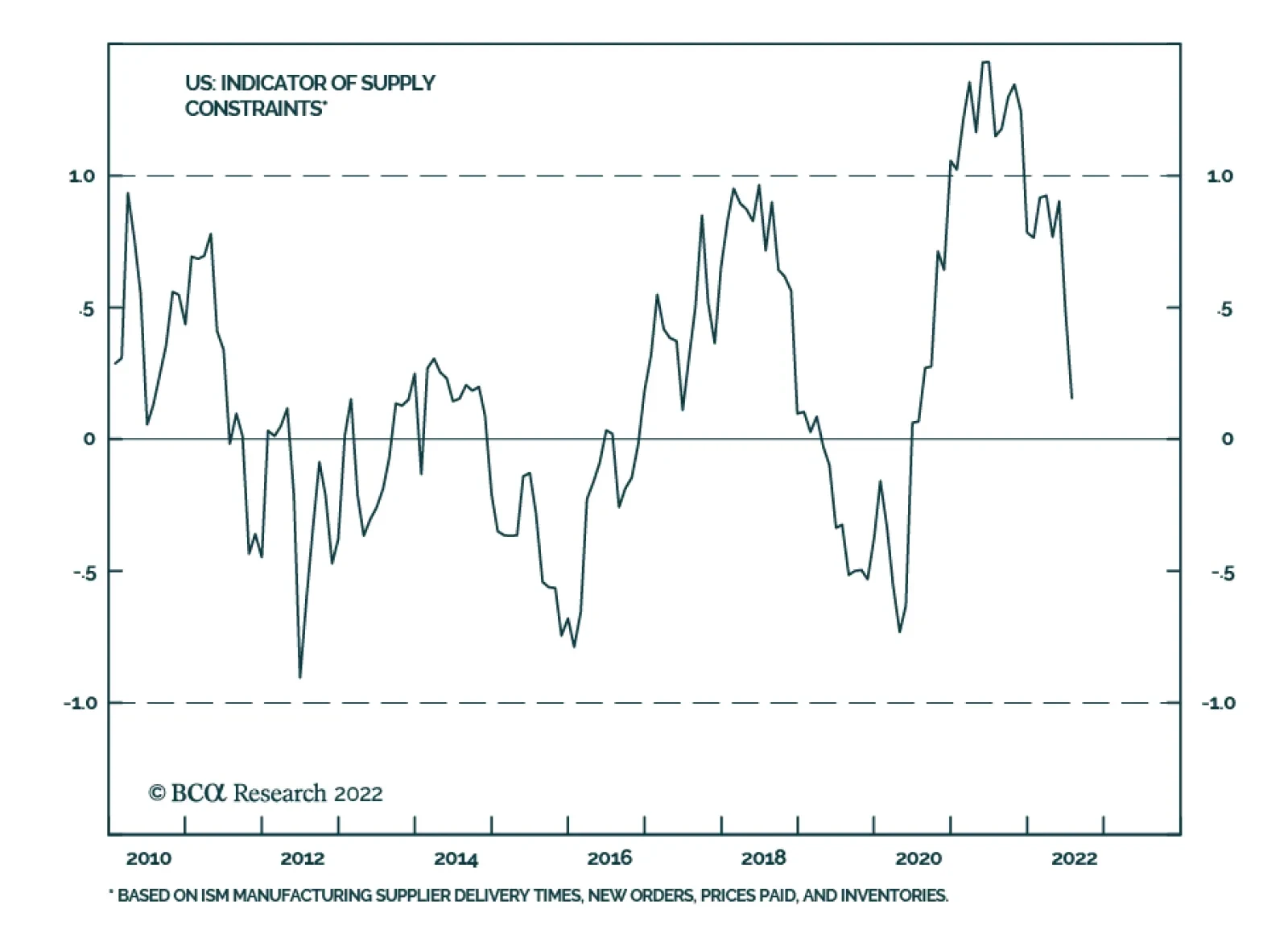

The supply bottlenecks caused by the pandemic are easing rapidly. Global trade is flowing once again as highlighted by the rapid decline in bulk and container shipping costs around the world. Companies are also taking notice. BCA’s indicator of US Supply…

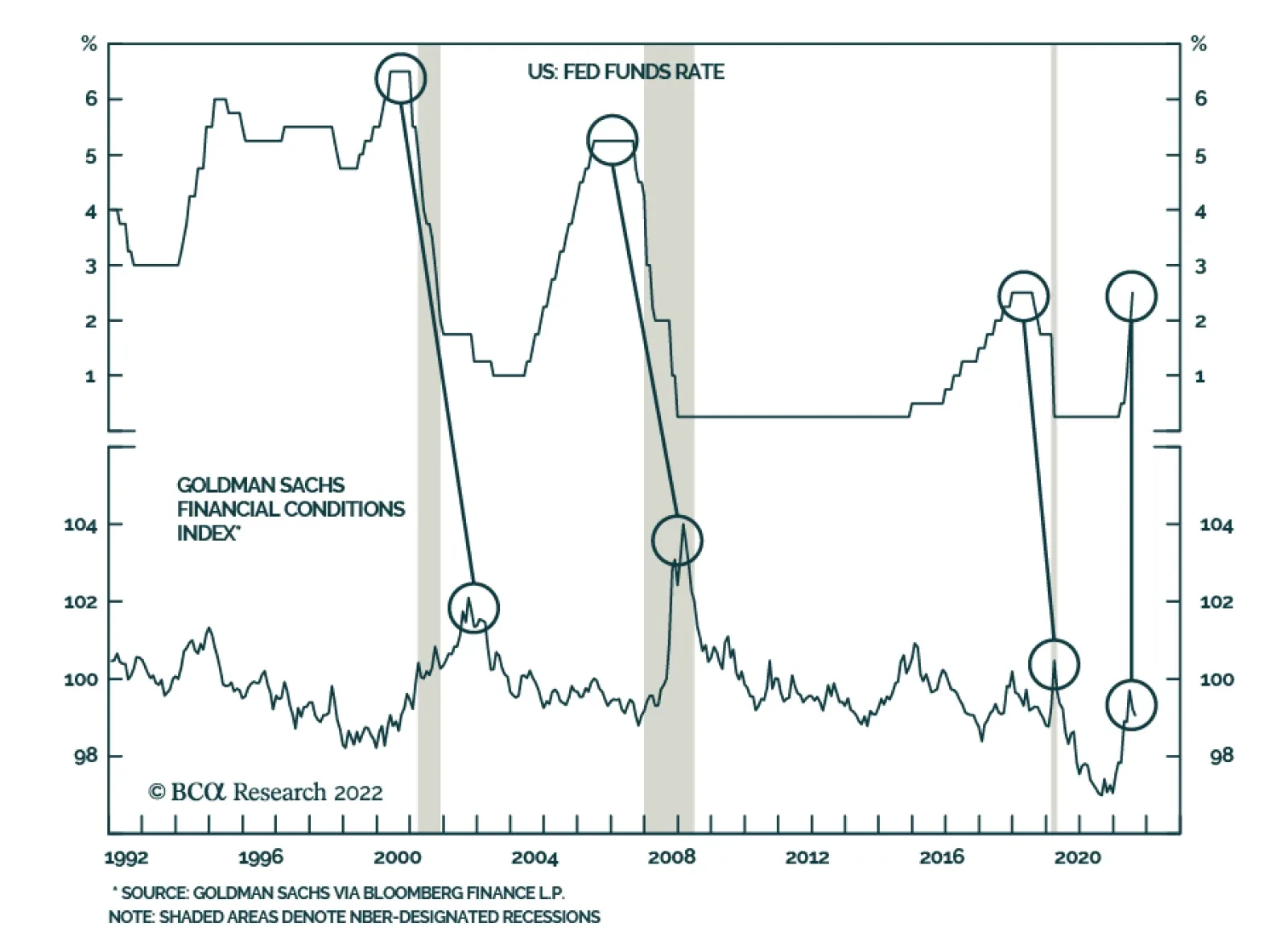

As illustrated by Goldman Sachs’ Financial Conditions Index (FCI), the US economy came under considerable pressure in H1 as a wide swath of financial markets sold off sharply. Every one-point move in the FCI equates to a one-percentage-point move in real GDP…

Executive Summary US Deficits Will Rise Before They Fall

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

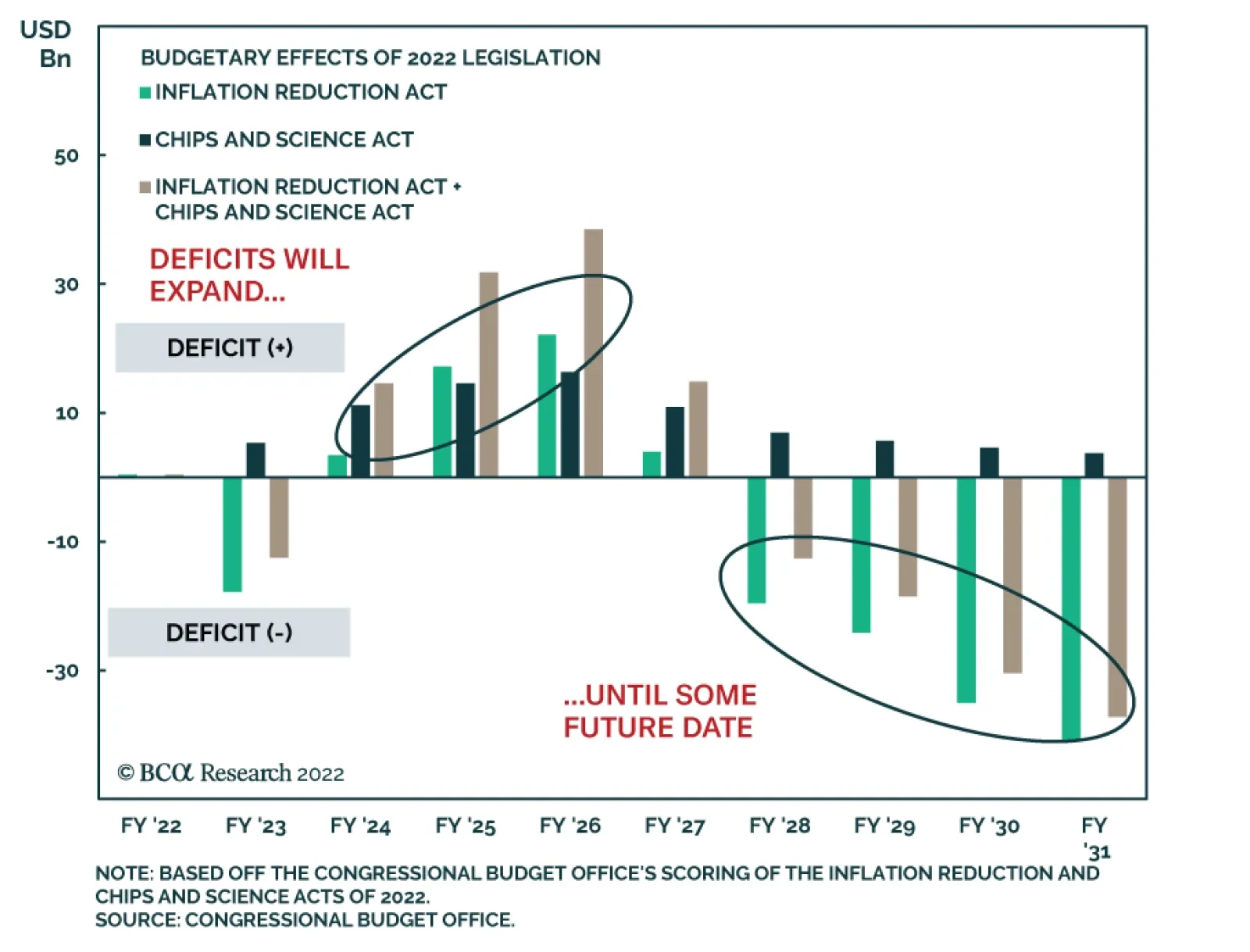

The Inflation Reduction Act combined with the Chips and Science Act will add $88 billion to the budget deficit through FY2027. The two bills would only reduce the deficit by $11.1 billion by 2031. The deficit that year will be $2 trillion. Hence Congress’s latest actions add to the deficit in the short run and are effectively deficit-neutral over the long run. That is not disinflationary. Gridlock is still the likeliest outcome of the midterm elections. That is disinflationary for 2023-24 because fiscal policy freezes. Whether gridlock will persist after 2024 is unknown. Federal investments in US computer chips and renewable energy could enhance productivity over the long run. That could well be disinflationary … but the magnitude and timing are unknown. Overall, US social spending, industrial spending, defense spending, and government intervention are rising as the nation-state responds to social unrest and geopolitical conflict. Inflation will depend on many things, but this policy trend is not disinflationary. Close Recommendation (Tactical) Closing Level CLOSING DATE Return Long US Treasuries Vs. TIPS 1.3768 AUG 12, 2022 1.53% Bottom Line: Close long US Treasuries relative to TIPS. But stay long the US dollar. Biden’s legislative victories underscore our strategic themes of Limited Big Government and Peak Polarization – and are not disinflationary. Feature President Biden’s approval rating ticked up to 40% after a series of policy wins, including the passage of the Inflation Reduction Act and the Chips and Science Act. These bills reinforce our strategic theme of Limited Big Government, i.e. a rising role for the state within the US’s free market context. When Biden unveiled his anti-inflation agenda back in June we argued that his only real options to reduce inflation before the midterm elections hinged on other people: namely the Federal Reserve, the Saudis, the Iranians, and also Capitol Hill. With regard to Congress, we expected Democrats to pass a budget reconciliation bill. We saw that they were repackaging this bill as an “inflation reduction” measure to improve their election prospects. But we argued that it would not fight inflation in any substantive way.1 Now that the bill is on the way to Biden’s desk, it is only fair to ask: What will be the impact? Will it reduce inflation or not? The short version is no. The bill does not stand alone but is part of the Biden administration’s “last-ditch effort” to pass two major bills before the midterms. These two laws are deficit-neutral at best but slightly stimulative in the short run – and hence marginally inflationary. These laws could prove disinflationary over the long run, as investments in semiconductors and renewable energy should drive innovation. But that is hard to predict. We are optimistic on that front but for the foreseeable future the effects are neutral or inflationary. To understand this view, we need to review BCA’s stance on inflation overall and then discuss the legislation. The BCA View On Inflation BCA sees this year’s inflationary bout as both a cyclical and a structural phenomenon. The cyclical rise in inflation stemmed from the pandemic and the ensuing economic stimulus. This cycle is peaking now. Commodity prices are moderating and goods spending has fallen two-thirds of the way back to where it stood prior to the pandemic, suggesting that inflation will take a step back. At very least inflation has stopped skyrocketing (Chart 1). Yet the structural drivers of inflation will persist. Chart 1Inflation Rolls Over ... For Now

Inflation Rolls Over ... For Now

Inflation Rolls Over ... For Now

The long-term inflation thesis hinges first and foremost on global population trends. Fewer prime-age workers as a share of the population means that the price of a prime-age worker goes up. It also hinges on the decline in the global glut of savings, the rise of mercantilism and trade protectionism (i.e. hypo-globalization), and the conclusion of household deleveraging in the wake of the 2008 crisis. Structurally looser fiscal policy – soft budgets – also plays a role. The decay of the liberal world order since 2008 financial crisis entails that western governments face the combined threats of social unrest at home and great power competition abroad. These governments’ answer is to take a more active role in the economy to appease popular wrath, improve energy security, and bulk up national defense. The result will be larger deficits. Larger budget deficits reduce the savings available to the private sector and constrain future supply, feeding into inflation. The result is that, in the United States, the neutral rate of interest will likely prove to be higher than expected, monetary conditions will be looser than expected in real terms, and hence the economy will overheat. At least until central banks and fiscal authorities impose austerity. Bottom Line: Inflation is a cyclical and structural phenomenon in the United States. Cyclically inflation is starting to moderate as various factors from the pandemic and fiscal stimulus wear off. But structurally inflation will be a persistent problem due to population aging, the end of the savings glut, hypo-globalization, geopolitical conflict, and a rising government role in the economy. New Laws Do Not Cut The Deficit Until 2027 At Best Now we can put the Biden administration’s policy into context. The stagflationary cyclical backdrop poses a severe challenge for the ruling Democratic Party. Midterm elections are only three months away and yet headline inflation is still running at 8.5% and core inflation is rising unabated at 5.9% year-on-year. The median voter suffers from high inflation in the form of falling real income and wages. Yet the Democratic legislative agenda has focused on increasing spending, which adds to inflation. If US gasoline prices continue to moderate, the median household’s inflation expectations will come down – and that is a positive short-term development for Democrats (Chart 2). That is why President Biden went to Saudi Arabia with his tail between his legs to beg for more crude oil production. That is why he is trying to do a deal with Iran too (though there our view is pessimistic). That is why he has urged Europe to wait until after the midterm to implement full oil sanctions on Russia. Hence also the Senate repackaged the -$4 trillion “Build Back Better” spending splurge as a +$300 billion “Inflation Reduction” fiscal reform. But will the Inflation Reduction Act truly reduce inflation? Will it affect the cyclical or structural drivers mentioned above? Chart 2Inflation Expectations Moderating

Inflation Expectations Moderating

Inflation Expectations Moderating

The title of the bill alone should prompt investors to be skeptical. The bill does not meaningfully reduce budget deficits. According to the Democratic Party it will generate $300 billion in savings over 10 years, mostly as a result of capping drug costs that Medicare pays to hospitals on behalf of about 64 million Americans. However, the Committee for a Responsible Federal Budget provides a more realistic scenario in which the savings amount to $160 billion, or about half as much as advertised (Table 1).2 The CBO estimates the bill will reduce the budget deficit by $100 billion over 10 years, one third of the official selling point. Table 1What Is Inside The Inflation Reduction Act Of 2022?

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Table 2 shows the CBO’s baseline estimates of the US budget deficit outlook as of July 2021, May 2022, and August 2022 (i.e. the latter with the new legislation). The trend line with the reconciliation bill is virtually indistinguishable from the May estimate (Chart 3). Table 2US Budget Balance Projections Before/After The Inflation Reduction Act

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Chart 3What Deficit Reduction?

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Table 3 shows the specific change in the budget deficit for each year, illustrated in Chart 4. The bill modestly reduces the deficit in 2023 but increases the deficit in subsequent years until 2028. When the bill’s savings peak at $41 billion in 2031, they will shave off 2% of the $2 trillion deficit. Table 3Change In US Deficit Due To Inflation Reduction Act And Chips And Science Act

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

In other words, the deficit reduction will not occur until after the 2028 election – by which time it will be swamped by other political and economic factors. In addition, the bipartisan Chips and Science Act will add $47.5 billion to the budget deficit through FY2026 and $79.3 billion through FY2031. Combining them shows that Congress is still adding to spending despite today’s 5.9% core inflation reading – while delaying the miniscule deficit reduction until the latter part of the decade. Credit should be given to the Democrats for offsetting their new spending with revenue increases. But in realistic terms Congress’s latest actions are deficit-neutral at best. The question was how to pay for the desired spending rather than how to impose budget consolidation. Austerity is politically impractical in the context of left-wing and right-wing populism. Chart 4US Deficits Will Rise Before They Fall

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

The new fiscal spending makes sense given the strategic predicament that the US faces. But it should flag to investors that the only real fiscal discipline on the horizon will come after the midterm election, when Congress is gridlocked and fiscal policy is basically frozen. Bottom Line: The Inflation Reduction Act combined with the Chips and Science Act will add about $88 billion to the budget deficit through FY2027. The two bills only reduce the growth of the budget deficit by $11.1 billion by 2031. They will not reduce investors’ inflation expectations over the next five years. Cyclical inflation expectations will fall for other reasons – such as Fed rate hikes, the slowdown in global growth, and looming gridlock. Reducing Drug Prices And EV Prices Is Not Generally Disinflationary What about the sector effects of the Inflation Reduction Act? Could they be disinflationary? The bill raises a minimum corporate tax rate of 15% to pay for renewable energy subsidies, it bulks up the Internal Revenue Service’s tax collecting capabilities to pay for an expansion of Obamacare subsidies, and it empowers Medicare to negotiate pharmaceutical prices, creating revenue savings for the federal government. Theoretically caps on drug prices will push prices down, while subsidies to buy electric vehicles (EV) will incentivize Americans to buy those cars and expand the domestic EV supply chain. Hence Democrats can at least claim to be reducing drug price inflation and arguably EV price inflation. Drug price caps are popular and could increase social stability. Electric car subsidies are less popular but tap into demands for domestic manufacturing and action on climate change. Neither will generate substantial opposition in the voting booth. However, the general level of prices will not fall as a result of these sector-specific interventions. Spending on motor vehicles is around 4.2% of total personal consumption expenditure (Chart 5, first panel). Spending on prescription drugs is around 3.2% of total personal consumption expenditure (Chart 5, second panel). Hence the bill could at maximum affect 7.4% of total consumer spending. But only certain drugs will face price caps and only EVs will be subsidized, so the effect is even narrower than that. Spending on cars grew by 1.7% between 2003-20, in line with economic growth. Drug spending grew faster, in line with an aging society, at 2.9% over the same period (Chart 6). Normally the contribution to inflation is negligible for cars but higher-than-average for drugs. True, after Covid-19 car prices surged while drug prices fell below average, but that process should normalize (Chart 7). Chart 5The Role Of Cars And Drugs In Inflation

The Role Of Cars And Drugs In Inflation

The Role Of Cars And Drugs In Inflation

Chart 6Growth Of Car And Drug Spending

Growth Of Car And Drug Spending

Growth Of Car And Drug Spending

Chart 7Change In Car And Drug Prices

Change In Car And Drug Prices

Change In Car And Drug Prices

Only 20 drugs will be eligible for Medicare negotiation per year. The top 20 drugs amount to around 18% of the pharmaceutical market. The new government-negotiated prices will begin to take effect in 2027. The effect will be to dampen domestic manufacturers’ incentive to produce generics, leading to supply constraints or substitution effects (e.g. imports). Hence overall drug prices will not fall as much as expected. The US lacks universal healthcare coverage, so price controls represent an economic transfer between corporations or between corporations and government – not between corporations and consumers. Capping drug prices will benefit insurers directly and consumers only indirectly. The profit will change from the hands of Big Pharma to Big Insurance (managed healthcare providers) (Chart 8). Incidentally big insurers will also benefit from the bill’s expansion of the Obamacare subsidies. Of course, Obamacare enrollees will see a marginal increase in disposable income – especially lower-income individuals, who have a higher propensity to consume. This is positive from the perspective of social stability but likely to be inflationary, not disinflationary. Lower insurance premiums mean more spending cash. Chart 8Big Insurance Versus Big Pharma

Big Insurance Versus Big Pharma

Big Insurance Versus Big Pharma

As for the bill’s green subsidies, EVs account for about 5.6% of cars sold. Subsidies will encourage the production of EVs and accelerate the growth of EV market share. The point is to make EV prices competitive with other cars since EVs are more costly to make, especially if they are to be made domestically. Non-EVs may have to lower their prices but, as we have seen, car inflation is not a major contributor to general inflation, at least not in normal times. Of course, no electric vehicles will qualify for the new rebate immediately. The law requires a large share of qualifying electric cars to be manufactured in North America, or at least not to be produced in “countries of concern” such as China. China is still the leader in making critical components of EVs, especially batteries. Such policies are not conducive to the most efficient manufacturing methods and lowest consumer prices. Rather they seek to shift supply chains to allied countries or to “onshore” them within the United States for strategic reasons, even at a higher cost to consumers. As such the new law reflects the US’s newfound populism, economic nationalism, industrial policy, and trade protectionism. It epitomizes the connection between great power competition and hypo-globalization, prioritizing supply chain resilience at the expense of economic efficiency. That makes sense from a national security point of view but is not likely to be disinflationary – quite the opposite. The bipartisan Chips and Science Act will dovetail with these measures to revive US industrial policy, steer capital into priority projects, and encourage domestic investment. This law and the climate change subsidies are federal investments that should boost productivity and enhance the supply side of the economy. We are optimistic over the long run regarding the productivity enhancements that could accrue from the government’s historic shift to re-initiate these kinds of investments. The space program in the 1960s may be too optimistic but it is still analogous. The US is already in the midst of Cold War II. If a major breakthrough in renewable energy eventually occurs that is tied to investments from the Inflation Reduction Act, then it will justify the bill’s anti-inflation moniker. But that remains to be seen. In the meantime, these investments will quicken US economic activity when the economy is already at full employment and inflation is running hot. Bottom Line: Cars do not contribute much to inflation in normal times and this bill gives subsidies to make electric cars in the US, which is not optimal for costs. Drugs contribute positively to inflation but Medicare caps will not lower drug prices until 2027 and general price effects are debatable. Overall, social unrest and great power competition are leading to greater government involvement in the economy, which is marginally inflationary. Economic Slowdown Is Disinflationary What will be the effect of this legislation on the midterm election campaign? Economic sentiment improved over the past month, even among Republicans. That led to a drop in polarization for the right reasons, i.e. a resilient economy, rather than the wrong reasons, i.e. the universal loathing of inflation (Chart 9). Polarization will stay near peak levels during the 2022-24 election campaign but the bipartisan Chips Act, the Biden administration’s adoption of hawkish foreign policy on trade and China, and the administration’s attempt to pursue at least a deficit-neutral approach to the budget reinforce our “Peak Polarization” theme. Long-term US policy consensus is developing beneath the still extreme polarization in the short term. Business activity is improving, which has contributed to the equity rally on the basis that the Fed is achieving a “soft landing” (Chart 10). We expect a hard landing due to the combination of negative macro and geopolitical factors but the latest data brings a positive surprise. Chart 9Economic Sentiment Ticks Up ... Even Among Republicans

Economic Sentiment Ticks Up ... Even Among Republicans

Economic Sentiment Ticks Up ... Even Among Republicans

Chart 10Business Activity Improves

Business Activity Improves

Business Activity Improves

In the short term, Biden and the Democrats will benefit from passing legislation (“getting things done”) and piggybacking on the fact that inflation is rolling over and the economy is showing some positive surprises. Biden’s approval rating is showing signs of stabilizing, albeit at a low level (Chart 11). The two parties are neck and neck in congressional ballot, with Democrats taking back the lead again from Republicans (Chart 12). If this trend continues it will mitigate the Democrats’ losses in the midterms. The Senate is competitive. Chart 11Biden’s Approval Will Perk Up At Least Somewhat

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Chart 12US Parties Neck And Neck In Generic Congressional Ballot

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

If inflation rolls over, real wages will improve, which will boost consumer confidence and, if it comes by October, could help the Democrats further (Chart 13). Chart 13Uptick In Real Wage Would Boost Consumer Confidence

Uptick In Real Wage Would Boost Consumer Confidence

Uptick In Real Wage Would Boost Consumer Confidence

Still, Democrats are likely to lose the House of Representatives in the midterms, as the ruling party usually loses seats and Democrats only have a five-seat margin. In other words, we would fade the emerging “Blue Sweep” risk (i.e. risk that Democrats keep control of both houses of Congress). A sweep is possible but unlikely, especially because many of Biden’s foreign policy problems can still come back to haunt him before the midterm. Two consecutive quarters of negative GDP growth usually results in an official recession. The jury is still out. Bankruptcies are ticking up and unemployment has nowhere to go but up (Chart 14). The stagflationary environment will probably persist through the midterm. Biden will face a rocky road to re-election. Chart 14Yet Unemployment And Bankruptcy Will Rise

Yet Unemployment And Bankruptcy Will Rise

Yet Unemployment And Bankruptcy Will Rise

Investment Takeaways Inflation expectations began to roll over due to the global slowdown, the drop in commodity prices, and the Fed’s rate hikes, but structural factors suggest inflation will remain a problem over the long run. The Inflation Reduction Act will not be implemented in time to have any effect on prices in 2022. It will slightly reduce the budget deficit next year but expand the deficit from FY2024-27. Combined with the Chips and Science Act the effect is slightly stimulative or inflationary until FY2028 at earliest. The bill increases policy uncertainty ahead of the midterms. Democrats will be able to take credit for any moderation of inflation through October and hence the election will become more competitive. But the election outcome is still highly likely to be congressional gridlock. Gridlock is disinflationary in 2023-24 because it implies that fiscal policy will shift to neutral – or even that real deficit reduction will occur if Biden compromises with a partially or wholly Republican congress. Structurally the US suffers from an imbalance of savings and investment. The global savings glut more than filled the gap and prevented inflation for several decades. Now the society is aging, the savings glut is depleting, globalization is retreating, and governments need to maintain spending to address high domestic and foreign challenges. US policy is forming a new consensus (“Peak Polarization”) that includes a larger role for government within the US context (“Limited Big Government”) in order to fight against social instability and geopolitical threats. The result is inflationary or at least not disinflationary. A high-tech and/or green energy productivity boom is possible and would combat the structural drivers of inflation. We are optimistic but the disinflationary impact is not forthcoming immediately and much remains to be seen. Matt Gertken Senior Vice President Chief US Political Strategist mattg@bcaresearch.com Jesse Anak Kuri Associate Editor jesse.kuri@bcaresearch.com Footnotes 1 Specifically we argued that the bill would be “mildly stimulating for the economy (i.e. inflationary) and none of the supply-side improvements would reduce inflation in time for the midterms.” We also implied that the act would probably not correct the US’s long-term rise in budget deficits as a share of GDP. 2 The difference has to do with the Affordable Care Act (Obamacare). Obamacare subsidies were expanded during the pandemic. The reconciliation bill will spend about $100 billion on extending the subsidies by three years. But it will be politically difficult for future congresses to revoke these subsidies. Hence the CBO assumes they will become permanent. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Table A3US Political Capital Index

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Chart A1Presidential Election Model

Third Quarter US Political Outlook: Last Ditch Effort

Third Quarter US Political Outlook: Last Ditch Effort

Chart A2Senate Election Model

Third Quarter US Political Outlook: Last Ditch Effort

Third Quarter US Political Outlook: Last Ditch Effort

Table A4House Election Model

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Table A5APolitical Capital: White House And Congress

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Table A5BPolitical Capital: Household And Business Sentiment

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation

Table A5CPolitical Capital: The Economy And Markets

No, The Inflation Reduction Act Will Not Reduce Inflation

No, The Inflation Reduction Act Will Not Reduce Inflation