United States

The US labor market is extremely tight. There are 1.8 job openings for every unemployed worker. This is a source of upside pressure on inflation as it boosts workers’ bargaining power and ultimately wages and firms’ labor costs. Indeed, the latest employment…

BCA Research’s Foreign Exchange Strategy service is neutral on the dollar over the next three-to-six months. The drivers of dollar downside have been clear. First, long-term interest rates in the US have fallen substantially. The US 10-year Treasury yield…

Listen to a short summary of this report. Executive Summary The Euro And The Chinese Credit Impulse

The Euro And The Chinese Credit Impulse

The Euro And The Chinese Credit Impulse

The US dollar has bounced off its 50-day moving average. In the recent past, that had led to a period of cyclical strength. The yen rally can be explained by the decline in Treasury yields and the fall in energy prices. Where next for the yen will depend on the time horizon. For investors trying to time the bottom, the euro is not yet a buy, but the common currency is incredibly cheap. Much depends on global/Chinese growth (Feature Chart). One of the key drivers of the dollar is volatility, and the correlation with the MOVE index. Less uncertainty will ease safe-haven demand. Stay short EUR/JPY and CHF/JPY. Remain long EUR/GBP. Maintain a limit sell on CHF/SEK at 10.76. RECOMMENDATIONS inception date RETURN Short EUR/JPY 2022-07-21 3.68 Bottom Line: We are tactically neutral the dollar but will be sellers on strength. Questions And Answers Chart 1Currencies And Yield Differentials

Currencies And Yield Differentials

Currencies And Yield Differentials

It is rare that we receive clients in our Montreal office. This has obviously been doubly the case due to the pandemic and the general hassle of travel nowadays. But when we do, it is a delight. In this week’s report, we got asked a few difficult questions on a tea date. The most important was not surprisingly the dollar view, but also our highest conviction trades in FX markets. We enjoyed the conversation and the intellectual debate, so we thought we would share this with our clients. Hopefully, this answers some of the most pressing questions. We have sliced this into as brief and concise a conversation as we could. Question: It is hard not to notice the steep decline in the dollar over the last few weeks. Should we fade this decline or lean into it? That is a tough question, but our educated guess is to fade it for now. That said, longer-term asset allocators should really be looking at buying extremely cheap G10 currencies on any declines. The drivers of dollar downside have been clear. First, long-term interest rates in the US have fallen substantially. The US 10-year Treasury yield has fallen from 3.5% to 2.7%. In real terms, they have also declined. The 10-year TIPS yield has fallen from 0.85% to 0.23%. On a relative basis, the market is also pricing in that the Fed will cut interest rates next year much faster than other central banks. More simply put, 2-year real bond yields in the US are rolling over, relative to the euro area and Japan, the biggest components of the DXY index (Chart 1). Related Report Foreign Exchange StrategyHow Deep A Recession Is The Dollar Pricing In? Specific to Japan and the euro area, there has also been another critical factor – the decline in energy import costs. Germany’s trade balance improved markedly in June (Chart 2). This has been the first genuine improvement in a year. There is also discussion to extend the life of existing nuclear power plants, which will help assuage energy import costs. In Japan, trade balance data comes out on Monday next week, so we will see what it reveals. But what has been clear is a political drive to restart nuclear power and wean the Japanese economy off its dependence on oil and gas (Chart 3). Japanese prime minister Fumio Kishida has been very vocal about this in recent speeches. Chart 2Euro Area And Japanese Trade Balances Are Improving

Euro Area And Japanese Trade Balances Are Improving

Euro Area And Japanese Trade Balances Are Improving

Chart 3A Nuclear Renaissance In Japan?

A Nuclear Renaissance In Japan?

A Nuclear Renaissance In Japan?

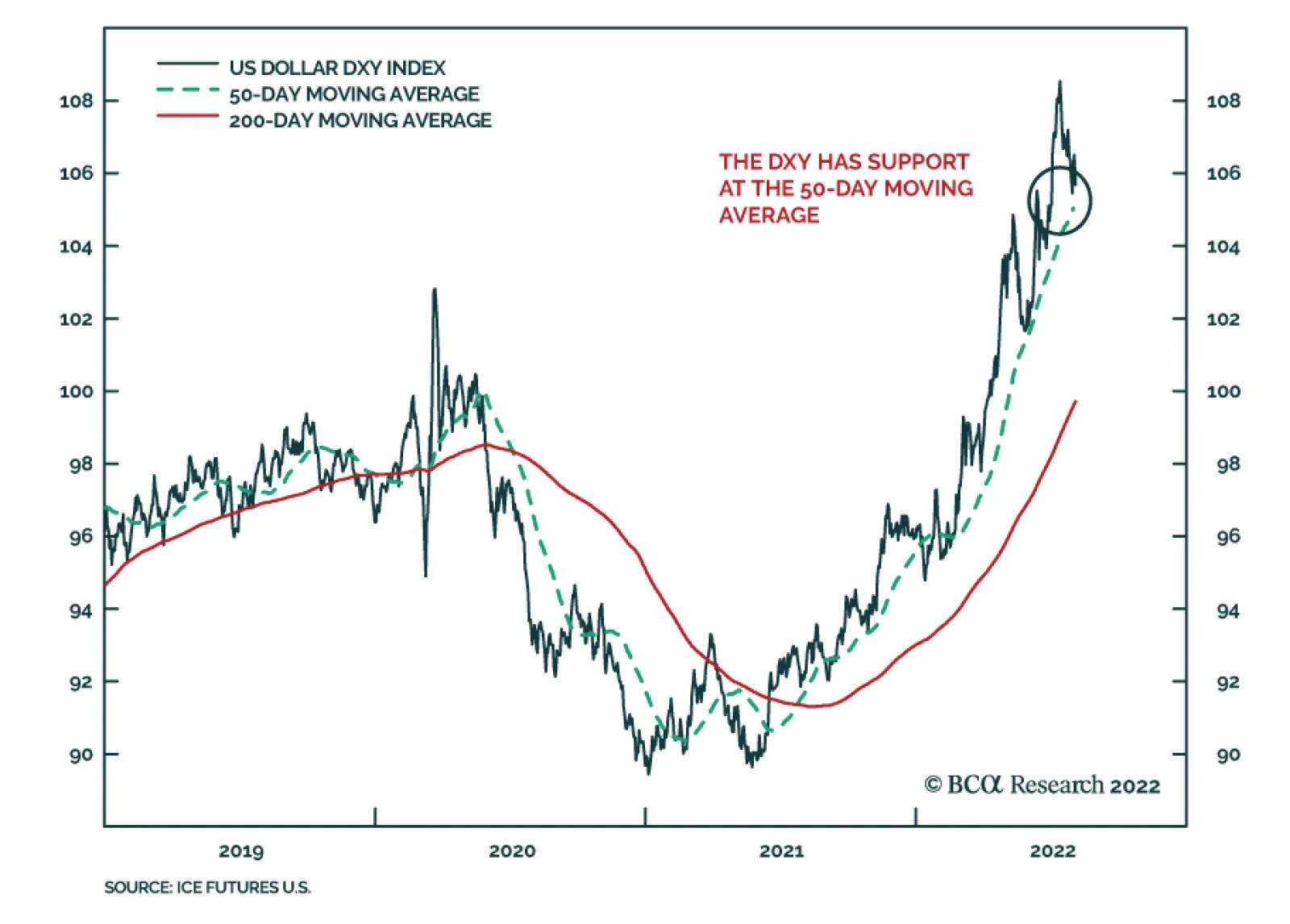

Turning to the more important part of your question, should we fade the decline or lean into it? We are of two minds on this to be honest, and here is why. The DXY has bounced off its 50-day moving average, which has been a sign in the past that the rally is not over (Chart 4). Our Geopolitical and Commodity & Energy colleagues are telling us not to trust the decline in oil prices. Our bond strategists think US yields are heading higher, with a whisper floor of 2.5%. Chart 4The DXY Has Support At The 50-Day Moving Average

The DXY Has Support At The 50-Day Moving Average

The DXY Has Support At The 50-Day Moving Average

Given these crosscurrents, there are many better opportunities that exist in FX at the crosses, rather than playing the dollar outright. But of course, the dollar call is critical. We would be neutral over the next three-to-six months but be incremental sellers of the dollar on strength. Question: Okay, neutral dollar for now, but bearish long term. We tend to consider longer-term investments as well, and we are confused about the euro, but even more so about the yen. Would you buy the yen today? If so, why? Our starting point for many currencies is valuation. On this basis, the yen is incredibly cheap. So, if you have a five-to-ten-year horizon, you can unlock incredible value in Japan, simply on a buy-and-hold basis. Our in-house curated model shows that the yen is at a multi-general low in value terms (Chart 5). Currencies mean-revert. Consider this for a minute – we are not equity experts, but Toyota trades at a P/E of 10.75, while Tesla trades at a P/E of 109.15. And yes, Toyota has electric cars. Chart 5The Japense Yen Is Incredibly Cheap

The Japense Yen Is Incredibly Cheap

The Japense Yen Is Incredibly Cheap

Chart 6The Yen Is A Favorite Short

The Yen Is A Favorite Short

The Yen Is A Favorite Short

It is true that a winner-takes-all mantra can be attributed to Tesla’s valuation over Toyota, but our colleagues in the Global Investment Strategy are telling us this era is over. As such, at a 40% discount, the yen is a long-term buy in our books. Interestingly, nobody likes the yen, at least by our preferred measure – net speculative positions. It is one of the most shorted G10 currencies (Chart 6). A cheap currency that is the most shorted ranks quite well in our evaluation of bargains in currency markets. Given my discussion above about the dollar, we have played the yen at the crosses. We are short EUR/JPY and CHF/JPY. On the euro, Japanese car manufacturers are simply becoming more competitive than their eurozone or US counterparts. This is not only related to the car industry, but according to the OECD, EUR/JPY is expensive on a purchasing power parity basis (Chart 7). Meanwhile, a short EUR/JPY trade is a perfect hedge for a pro-cyclical portfolio. The DXY index has historically traded in perfect inverse correlation to the euro-yen exchange rate (Chart 8). This suggests the collapse in the yen, relative to the euro, is very much overdone. In a risk-off environment, EUR/JPY will sell off. Meanwhile, there are also fundamental reasons to suggest that the yen should trade higher vis-à-vis the euro. Chart 7Remain Short ##br##EUR/JPY

Remain Short EUR/JPY

Remain Short EUR/JPY

Chart 8The DXY And EUR/JPY Usually Track Each Other

The DXY And EUR/JPY Track Each Other EUR/JPY And The DXY: Unsustainable Gap

The DXY And EUR/JPY Track Each Other EUR/JPY And The DXY: Unsustainable Gap

Question: Okay, let’s switch to the euro. I know you are short EUR/JPY, which has been working out well in the last few days. But the euro touched parity and I get a sense that it has bottomed. You have often mentioned that the euro has priced in one of the deepest recessions in the eurozone. I am surprised you are not trumpeting this currency and a once-in-a-lifetime buying opportunity. We agree somewhat with your conclusion but not the premise. Let’s consider the narrative over the last few months in the media. The first was that eurozone inflation will never catch up to the US, because the economy was structurally weak. Well, it did, albeit due to an exogenous shock. So, among a ranking of stagflationary candidates, the euro area is a top contender. If you believe in the idea that currencies are driven by real interest rates, rising inflation, and falling growth are an anathema for the exchange rate. When we typically have doubts about the euro area economy, and the outlook for its financial markets, we consult with our European Investment Strategy colleagues. We did just that and Mathieu Savary, who heads the service, mentioned two things: one – Chinese import volumes are imploding. For net creditor nations, this is a negative as their source of income is waning. The euro area falls into that category. The second thing to consider is that the dollar is a momentum currency. So is the euro. We mentioned earlier that the dollar bounced off its 50-day moving average, which explains euro weakness in recent trading days. In the end, Mathieu and the FX team did not really disagree, but I highlighted two charts to track. The euro tracks the Chinese credit impulse due to the importance of Chinese import demand for the euro area. It looks like our measure of that impulse has bottomed (Chart 9). If it has, you buy the euro on a long-term view. Relatedly, financial conditions are easing in China. As the Chinese bond market becomes more open and liberalized, bond yields become a financial conditions valve. That has been the case and has perfectly tracked the propensity for imports in the last few years (Chart 10). Chart 9The Euro And The Chinese Credit Impulse

The Euro And The Chinese Credit Impulse

The Euro And The Chinese Credit Impulse

Chart 10Financial Conditions Are Easing In China

Financial Conditions Are Easing In China

Financial Conditions Are Easing In China

In short, we will buy the euro if it touches parity, and even more so below parity with a 5–10-year view, but we think EUR/USD could touch 0.95 in the near term. I guess what we are saying is that a 5%-7% move is big in FX markets, but a 26% move (the undervaluation of the euro) is a whale. We do not see the catalyst for a whale in our current compass. Question: We have talked about the yen and the euro. I do not want to get into the pound, Australian dollar, and other currencies as you have told me your team has upcoming reports on those. But the Chinese yuan is very important in my investment portfolio. Any ideas on its next move? USD/CNY topped out near 6.8 in May. Since then, it has been in a trading range despite the DXY breaking to multi-decade highs (Chart 11). When a pattern like this emerges, it is always useful to revisit fundamentals. Those fundamentals are real interest rate differentials. We care about the yuan because China is a big trading partner of the US. As such, it is also a huge weight in the broad trade-weighted dollar index. China has huge problems, especially related to the property market, which need to be resolved. Bond yields have also collapsed. But the real interest rate in China is very attractive (Chart 12). It is also important to consider that if the dollar is the global safe haven, that means that the yuan could be becoming the haven in Asia. So, yuan downside is not a big risk for our long-term dollar bearish call. That said, we will be short CNY versus the yen, but not the dollar. Chart 11The RMB Has Been Relatively Resilient

The RMB Has Been Relatively Resilient

The RMB Has Been Relatively Resilient

Chart 12The RMB Has Undershot Real Rate Differentials

The RMB Has Undershot Real Rate Differentials

The RMB Has Undershot Real Rate Differentials

Question: I think I could sit with you all morning to discuss other aspects of FX, but I respect you have a tight stop due to the BLU meeting. Any concluding thoughts? I have one. Very often, we debate with our colleagues about capital flows. The dollar rises (in general), as capital inflows accelerate into the US and vice versa. It is often said that getting the dollar call right gets everything else right. So, if you can predict the path of the dollar, the performance of, say, US versus non-US equities becomes easy. Chart 13The Dollar And Earnings Revisions

The Dollar And Earnings Revisions

The Dollar And Earnings Revisions

We agree that the dollar is a real-time indicator of relative fundamentals. But here is one important observation: relative earnings revisions are deteriorating in the US vis-à-vis other countries (Chart 13). That has historically had an impact on exchange rates, as it affects equity capital flows. If the Federal Reserve also cut rates next year as the market is predicting, that will also be a negative for bond inflows. We think the global economy will avoid a deep recession, and that will allow growth to pick up outside the US. When the euro area and China bottom, then the dollar will truly peak, as capital flows to these economies will accelerate. So we are watching relative earnings and bond yield differentials closely. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Trades & Forecasts Strategic View Cyclical Holdings (6-18 months) Tactical Holdings (0-6 months) Limit Orders Forecast Summary

Executive Summary The US economy is experiencing a period of stagflation: booming nominal economic growth amid a lack of volume expansion. Very strong nominal growth (due to high inflation), a tight labor market, and more evidence of a wage-price spiral will cause the Fed to err on the side of hawkishness. Global trade volumes will contract and commodity prices will drop further. The former is bearish for Emerging Asian financial markets and the latter is negative for Latin American markets. Equities are currently rallying from very oversold levels and the rebound could continue in the coming weeks. However, if we are correct about our outlook on US inflation, Fed policy and global trade, then risk assets will resume their decline and the US dollar will rally. Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

Bottom Line: Stay defensive and continue underweighting EM in global equity and credit portfolios. The greenback will resume its uptrend sooner rather than later. This will depress EM share prices and fixed-income markets. Financial markets interpreted Fed chairman Powell’s comments in last Wednesday’s (July 27) FOMC press conference as a dovish pivot, catalyzing a sharp rebound in the S&P500. Is the bear market over? Should investors buy risk assets, including EM ones? Chart 1No Strong Rebound In EM Share Prices

No Strong Rebound In EM Share Prices

No Strong Rebound In EM Share Prices

We are hesitant to declare an end to the bear market and to recommend higher exposure to EM risk assets and currencies. In fact, the rebound in EM stocks has been feeble (Chart 1, top panel). As a result, the relative performance of EM equities versus their DM peers has fallen back to its lows of earlier this year (Chart 1, bottom panel). Overall, we reiterate what we wrote two weeks ago “…our macro themes of Fed tightening amid slowing global growth, the US dollar overshooting, and China’s disappointing recovery remain intact. These factors still warrant a defensive investment strategy, despite a possible near-term rebound in the S&P 500. EMs will lag and underperform in this rebound.” Can The Fed Afford To Pivot? With entrenched and persistent inflation in the US running well above the Fed’s target, the Fed cannot afford to – and will not – pivot for now. A simple rollover in inflation that reflects falling commodity and goods prices will not be sufficient for the Fed to make a policy U-turn and cut rates by 50 basis points next year (as fixed-income markets expect). We have been arguing that the US is already experiencing broad-based genuine inflation and has developed a wage-price spiral. Chart 2US Wage Growth Is At Its Fastest Rate In 40 years

US Wage Growth Is At Its Fastest Rate In 40 years

US Wage Growth Is At Its Fastest Rate In 40 years

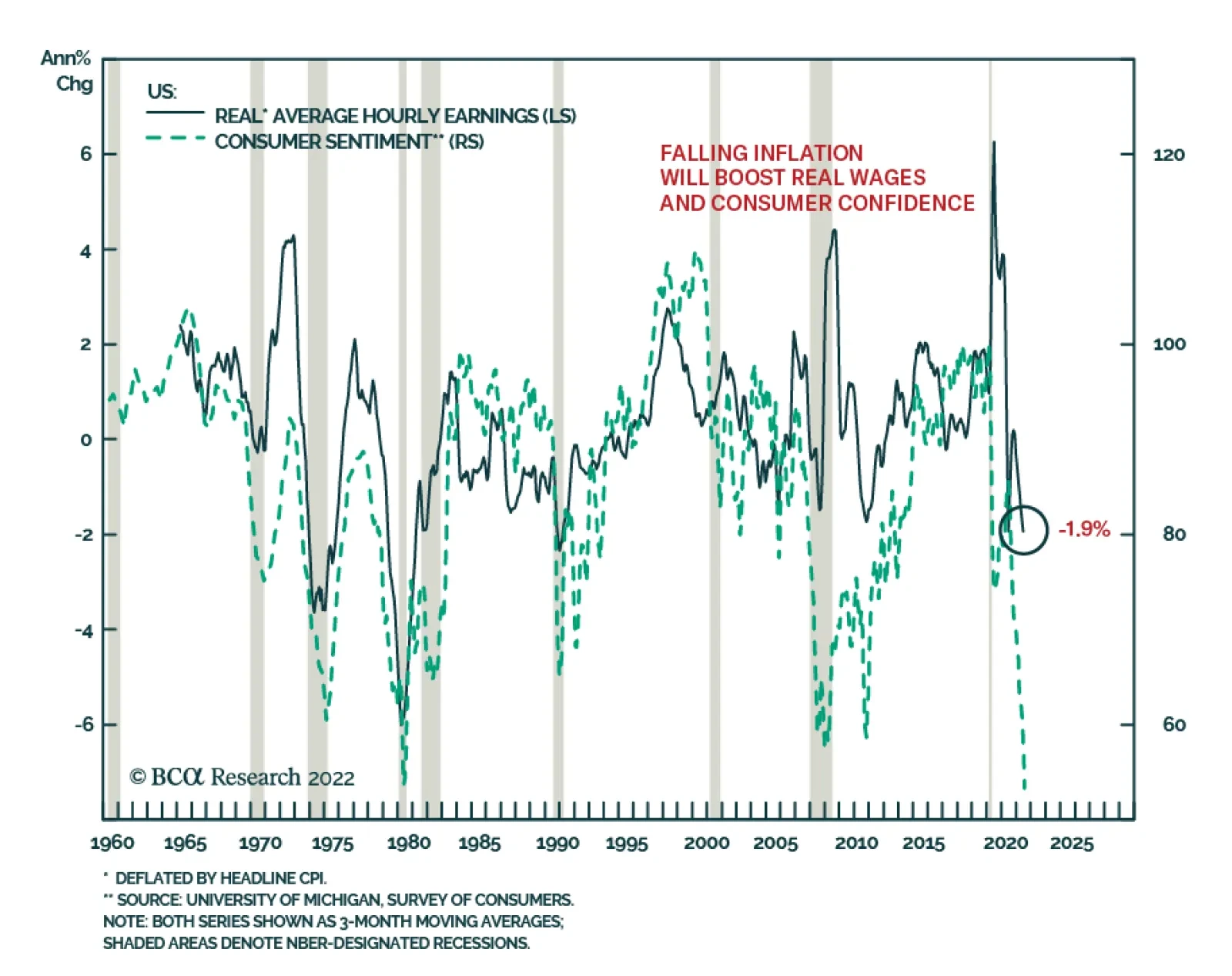

US wage growth has surged to a 40-year high of 5.7% (Chart 2). Even though the labor market is set to soften on the margin, its tightness will keep wage growth elevated. Importantly, real wages have fallen significantly, and employees will be demanding higher wages to offset lost purchasing power. US companies have been raising their prices at the fastest rate in decades. Prices charged by non-farm businesses rose at an annual rate of 8-9% in Q2, the highest in the past 40 years (Chart 3). Chart 3US Companies Are Raising Their Prices At Their Fastest Rate In 40 years

US Companies Are Raising Their Prices At Their Fastest Rate In 40 years

US Companies Are Raising Their Prices At Their Fastest Rate In 40 years

Chart 4Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

Strong Nominal, Weak Real Growth = Stagflation

Even though volumes have stagnated, corporate profits have been holding up because companies have been able to raise prices. Final sales to domestic purchasers in real terms registered zero growth in Q2 from Q1(Chart 4). This entails that the US economy is currency experiencing stagflation. Given that companies are able to raise prices (generating strong nominal sales) and are facing very tight labor market conditions, they might be willing to raise wages further. In brief, a wage-price spiral is unfolding in the US. US core inflation is running well above the Fed’s 2% target. The average of seven core PCE and CPI measures – our “super core” gauge of consumer price inflation − stands at 5.5% (Chart 5). Although falling commodity and goods prices (Chart 6) could cap the upside in core inflation, they are unlikely to bring it down below 4%. Hence, core inflation will remain well above the Fed’s target of 2%. This will lead the Fed to keep tightening monetary policy. Chart 5US Super Core Inflation Is At 5.5% and Rising

US Super Core Inflation Is At 5.5% and Rising

US Super Core Inflation Is At 5.5% and Rising

Chart 6US Import Prices From Asia Will Fall

US Import Prices From Asia Will Fall

US Import Prices From Asia Will Fall

Finally, in our opinion, financial markets are underappreciating how entrenched and persistent US inflation has become and are overlooking the unfolding wage-price spiral. The latest easing in US financial conditions will cause the Fed to refocus on inflation rather than growth. That is why we maintain our theme that the Fed and US equity markets remain on a collision course. We are open to the idea that the Fed could ultimately pivot earlier than required and eventually cut rates. However, odds are that the Fed has not yet pivoted and will ramp up its hawkishness in the coming months. The bar for the Fed to turn dovish is currently much higher than at any other time in the past 35 years, as inflation is much more entrenched and higher today. In our view, Powell would not like to be remembered as the chairman under whose watch inflation became enduring. He would prefer to be remembered as Paul Volcker, and not as Arthur Burns. Under the latter’s watch in the 1970s, the US experienced a devastating era of high and persistent inflation. Global equities, credit markets and US Treasurys were very oversold a few weeks ago. That is why even a minor hint from the Fed of a possible end to the hiking cycle produced such a strong rebound in stocks and fixed-income markets. This rally could persist in the coming weeks. However, if we are correct about the outlook on US inflation, Fed policy and global trade (see the section below), then risk assets will resume their decline and the US dollar will rally. Bottom Line: The US economy is experiencing a period of stagflation: booming nominal economic growth amid a lack of volume expansion. Very strong nominal growth (due to high inflation) a tight labor market, and more evidence of a wage-price spiral will cause the Fed to err on the side of hawkishness. As a result, the current rally in risk assets is unsustainable. Global Manufacturing / Trade Contraction Global manufacturing and trade are entering a period of contraction: According to manufacturing PMI data for July, Taiwanese new export orders for overall manufacturing and the semiconductor industry have plunged to 37 and 34, respectively (Chart 7). Meanwhile, their customer inventories have surged to a 10-year high (Chart 8). Taiwan is a major supplier of semiconductors and other inputs to many industries around the world. Hence, these data suggest that industrial companies globally have stopped ordering chips and other inputs. This development is a sign of broad-based industrial weakness. Therefore, we believe that global trade volumes are set to shrink in H2 this year. Chart 7Taiwan: Overall And Semiconductor New Orders Have Plunged...

Taiwan: Overall And Semiconductor New Orders Have Plunged...

Taiwan: Overall And Semiconductor New Orders Have Plunged...

Chart 8...And Customer Inventories Have Surged

...And Customer Inventories Have Surged

...And Customer Inventories Have Surged

A similar situation is unfolding in the Korean semiconductor sector. The DRAM DXI index (revenue proxy) is falling, and DRAM and NAND spot prices are deflating (Chart 9). Notably, Korea’s overall export sector is also reeling. Business confidence among Korean exporters is plunging – this includes the latest datapoint from August (Chart 10, top panel). The nation’s export volume growth is already close to zero and export value growth is only holding up because of higher prices (Chart 10, bottom panel). Chart 9Korea: Semiconductor Prices Are Deflating

Korea: Semiconductor Prices Are Deflating

Korea: Semiconductor Prices Are Deflating

Chart 10Downside Risks For Korean Exports

Downside Risks For Korean Exports

Downside Risks For Korean Exports

Chart 11US Goods Imports Are Set To Contract

US Goods Imports Are Set To Contract

US Goods Imports Are Set To Contract

US import volumes are set to shrink in the coming months. This will deepen the global trade slump. Chart 11 illustrates that US consumption of goods-ex autos has been contracting and retail inventory of goods ex-autos has skyrocketed. Together, these developments foreshadow a major contraction in US imports and global trade volumes. Commodity prices are heading south. Chinese commodity consumption will remain in the doldrums, and US/EU demand for commodities will weaken as global manufacturing contracts. The sanctions imposed on Russia initially led buyers to increase their precautionary and speculative purchases of various commodities, creating a tailwind for prices earlier this year. However, these precautionary and speculative purchases have since been halted or reversed, causing commodity prices to plunge. We made the case for falling oil prices in our July 21 report, and BCA’s China Investment Strategy’s Special Report on copper from July 27 concludes that copper prices will decline further. Chart 12China: Has The Post-Reopening Bounce Ran Its Course?

China: Has The Post-Reopening Bounce Ran Its Course?

China: Has The Post-Reopening Bounce Ran Its Course?

Finally, the Chinese manufacturing PMI rolled over in July following the rebound in May and June. New orders, backlog orders and import subcomponents have relapsed anew (Chart 12). The Chinese economy is facing considerable headwinds from the property market, rolling lockdowns resulting from the dynamic zero-COVID policy and a contraction in exports. As we argued in our July 13 report, policy stimulus has so far been insufficient. Bottom Line: Global trade volumes will contract and commodity prices will drop further. The former is bearish for Emerging Asian financial markets and the latter is negative for Latin American markets. Investment Strategy Although the rebound in global risk assets could persist for several weeks, their risk-reward profile is not attractive. Stay defensive and continue underweighting EM in global equity and credit portfolios. The Fed’s hawkish bias as well as contracting global trade are bullish for the US dollar. As a result, the greenback will resume its uptrend sooner rather than later. This will cap the upside in EM stocks and fixed-income markets. We continue to short the following currencies versus the USD: ZAR, COP, PEN, PLN, PHP, and IDR. In addition, we recommend shorting HUF vs. CZK, KRW vs. JPY, and BRL vs. MXN. Although we find good value in many EM local yields, we do not yet recommend buying them aggressively. The basis is our view on EM currencies versus the US dollar. For now, we prefer to bet on flattening yield curves. Our current favorite markets for flatteners are Mexico and Colombia. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategic Themes (18 Months And Beyond) Equities Cyclical Recommendations (6-18 Months) Cyclical Recommendations (6-18 Months)

Counterpoint’s August schedule: Next week, I am travelling to see clients in Australia, New Zealand, and Singapore, so we will send you a report on China’s 20th National Party Congress written by our Chief Geopolitical Strategist, Matt Gertken. Given that the outlook for the $100 trillion Chinese real estate market is crucial for the global economy and markets, Matt’s insights will be very interesting. Then on August 18, I will host the monthly Counterpoint webcast, which I hope you can join. We will then take a week’s summer holiday and return with a report on September 1. Executive Summary In the topsy-turvy recession of 2022, real wages have collapsed. This means profits have stayed resilient and firms have not laid off workers. Making this recession a ‘cost of living crisis’ rather than a ‘jobs crisis’. If inflation comes down slowly, then the ‘cost of living crisis’ will persist. But if inflation comes down quickly while wage inflation remains sticky, firms will lay off workers to protect their profits, turning the ‘cost of living crisis’ into a ‘jobs crisis’. Either way, this will keep a choke on consumer spending, and particularly the spending on goods, which is likely to remain in recession. Meanwhile, until mortgage rates move meaningfully lower, housing investment will also remain in recession. The double choke on growth means that the bear market in the 30-year T-bond is likely over. This suggests that the bear market in stock market valuations is also over, but that ‘cyclical value’ is now vulnerable to profit downgrades. Hence, equity investors should stick with ‘defensive growth’, specifically healthcare and biotech. Fractal trading watchlist: GBP/USD and Hungarian versus Polish bonds. In The 2008 Recession, Real Wage Rates ##br##Went Up So Employment Went Down…

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

…But In The 2022 Recession, Real Wage Rates##br##Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

Bottom Line: The bear market in the 30-year T-bond and stock market valuations is likely over, but equity investors should stick with ‘defensive growth’, specifically healthcare and biotech. Feature The US economy has just contracted for two consecutive quarters, meeting the rule-of-thumb definition of a recession. Other major economies are likely to follow. Yet many economists and strategists are in denial. This cannot be a ‘proper’ recession, they say, because the economy remains at full employment. But the recession-deniers are wrong. It is a recession, albeit it is a ‘topsy-turvy’ recession in which employment remains high (so far) because real wage rates have collapsed, circumventing the need for lay-offs. This contrasts with a typical recession when real wage rates remain high, forcing the need for lay-offs.1 The Topsy-Turvy Recession Of 2022 When do firms lay off workers? The answer is, when they need to protect their profits. Profits are nothing more than revenues minus costs, and in a typical recession revenues slow much faster than the firms’ biggest cost, the wage bill. In this event, the only way that firms can protect their profits is to lay off workers. Chart I-1 confirms that every time that nominal sales have shrunk relative to wage rates, the unemployment rate has gone up. Without exception. Chart I-1Unemployment Goes Up Whenever Firms' Wage Rates Rise Faster Than Their Revenues...

Unemployment Goes Up Whenever Firms' Wage Rates Rise Faster Than Their Revenues...

Unemployment Goes Up Whenever Firms' Wage Rates Rise Faster Than Their Revenues...

But what happens during a recession in which nominal sales do not shrink relative to wage rates? In this event, profits stay resilient, so firms do not need to lay off workers. Welcome to the topsy-turvy recession of 2022! In the topsy-turvy recession of 2022, there has been much greater inflation in consumer prices and nominal sales than in nominal wage rates (Chart I-2). The result is that real wage rates have collapsed, profits have stayed resilient, and firms have not needed to lay off workers… so far. Chart I-2...But In The 2022 Recession, Wage Rates Have Risen Slower Than Revenues, So Unemployment Hasn't Gone Up

...But In The 2022 Recession, Wage Rates Have Risen Slower Than Revenues, So Unemployment Hasn't Gone Up

...But In The 2022 Recession, Wage Rates Have Risen Slower Than Revenues, So Unemployment Hasn't Gone Up

In a typical recession, the pain falls on the minority of workers who lose their jobs, as well as on profits. Paradoxically, for the majority that keep their jobs, real wages go up. This is because sticky wage inflation tends to hold up more than collapsing price inflation. For example, in the 2008 recession, the real wage rate surged by 4 percent (Chart I-3), and in the 2020 recession it rose by 2 percent. Chart I-3In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

In The 2008 Recession, Real Wage Rates Went Up So Employment Went Down...

Yet in the 2022 recession, the real wage rate has shrunk by 4 percent, meaning that the pain of the recession has fallen on all of us (Chart I-4). In one sense therefore, this recession is ‘fairer’ because ‘we’re all in it together’. This is confirmed by the current malaise being characterised not as a ‘jobs crisis’, but as a ‘cost of living crisis’. In another sense though, the recession is unfair because the pain has not been shared by corporate profits, which have remained resilient… so far. Chart I-4...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

...But In The 2022 Recession, Real Wage Rates Went Down So Employment Went Up!

The crucial question is, what happens next? Using the US as our template, wage rates are growing at 5-6 percent, and this growth rate is typically stickier than sales growth. Assuming inflation drifts lower, nominal sales growth will also drift lower from its current 7 percent clip, meaning that it could soon dip below sticky wage growth. Once the growth in firms’ revenues has dipped below that in nominal wage rates, profits will finally keel over. To repeat, profits are nothing more than revenues minus costs, where the biggest cost is the wage bill (Chart I-5).2 Chart I-5Profits Are Nothing More Than Revenues Minus Costs

Profits Are Nothing More Than Revenues Minus Costs

Profits Are Nothing More Than Revenues Minus Costs

At this point, the downturn will become more conventional. To protect profits, firms will be forced to lay off workers who will bear the pain of the downturn alongside falling profits. Meanwhile, with inflation easing, real wage growth for the majority that keep their jobs will turn positive. But to repeat, this is the typical pattern in a recession. Accelerating real wage rates are entirely consistent with a contracting economy as we witnessed in both 2008 and 2020. As Two Huge Imbalances Correct, Demand Will Be Pegged Back All of this assumes that real demand will remain under pressure, so the question is what is pegging back real demand? The answer is: corrections in two huge imbalances in the global economy. A breakdown of the -1.3 percent contraction in the US economy reveals these two corrections:3 Spending on goods, which contributed -1.2 percent Housing investment, which contributed -0.7 percent. These corrections are not over. As we presciently explained back in February in A Massive Economic Imbalance, Staring Us In The Face: “The pandemic overspend on goods constitutes one of the greatest imbalances in economic history. An overspend on goods is corrected by a subsequent underspend; but an underspend on services is not corrected by a subsequent overspend. The pandemic overspend on goods constitutes one of the greatest imbalances in economic history. This unfortunate asymmetry means that the recent overspend on goods at the expense of services makes the economy vulnerable to a recession. And the risk is exacerbated by central banks’ intentions to hike rates in response to inflation” (Chart I-6). Chart I-6The Pandemic Overspend On Goods Constitutes One Of The Greatest Imbalances In Economic History

The Pandemic Overspend On Goods Constitutes One Of The Greatest Imbalances In Economic History

The Pandemic Overspend On Goods Constitutes One Of The Greatest Imbalances In Economic History

Then, in The Global Housing Boom Is Over, As Buying Becomes More Expensive Than Renting, we identified a second major imbalance that is starting to correct. Specifically, the global housing boom of the past decade, which has doubled the worth of global real estate to $370 trillion, was predicated on ultra-low mortgage rates that made buying a home more attractive than renting. But in many parts of the world now, buying a home has become more expensive than renting (Chart I-7). Disappearing US and European homebuyers combined with a flood of home-sellers will weigh on home prices and housing investment – at least until policymakers are forced to bring down mortgage rates (Chart I-8 and Chart I-9). Chart I-7Buying A Home Has Become More Expensive Than Renting!

Buying A Home Has Become More Expensive Than Renting!

Buying A Home Has Become More Expensive Than Renting!

Chart I-8Homebuyers Have Disappeared...

Homebuyers Have Disappeared...

Homebuyers Have Disappeared...

Chart I-9...While Home-Sellers Are Flooding The Market

...While Home-Sellers Are Flooding The Market

...While Home-Sellers Are Flooding The Market

Meanwhile, as Chinese policymakers try and gently let the air out of the $100 trillion Chinese real estate market, a collapse in Chinese property development and construction activity will have negative long-term implications for commodities, emerging Asia, and developing countries that produce raw materials. More Investment Conclusions In addition to the long-term investment conclusions just described, we can draw some shorter-term conclusions: If inflation comes down slowly, then the current ‘cost of living crisis’, which is pummelling everyone’s real incomes, will persist. But if inflation comes down quickly while wage inflation remains sticky, firms will be forced to lay off workers to protect their profits, turning the ‘cost of living crisis’ into a ‘jobs crisis’. Either way, this will keep a choke on consumer spending, and particularly the spending on goods, which is likely to remain in recession. Meanwhile, until mortgage rates move meaningfully lower, housing investment will also remain in recession. Equityinvestors should stick with ‘defensive growth’, specifically healthcare and biotech. This double choke on growth is likely to keep a lid on ultra-long bond yields, even if central banks need to hike short-term rates more than expected to slay inflation. Our proprietary fractal analysis confirms that the sell-off in the 30-year T-bond is likely over (Chart I-10). Chart I-10The Bear Market In The 30-Year T-Bond Is Likely Over

The Bear Market In The 30-Year T-Bond Is Likely Over

The Bear Market In The 30-Year T-Bond Is Likely Over

For the stock market, this suggests that the valuation bear market is now over, but that ‘cyclical value’ sectors are now vulnerable to profit downgrades. Hence, equity investors should stick with ‘defensive growth’, specifically healthcare and biotech. Fractal Trading Watchlist This week we noticed that the sudden 20 percent collapse of Hungarian versus Polish 10-year bonds, has reached the point of short-term fractal fragility that suggests an imminent rebound. Hence, we are adding this to our watchlist. Go long GBP/USD. But our trade is GBP/USD. UK political risk is diminishing, the BoE is likely to be as, or more, hawkish than the Fed, and the 260-day fractal structure of GBP/USD is at the point of fragility that has signalled major turning points in 2014, 15, 16, 18 and 21 (Chart I-11). Accordingly the recommendation is long GBP/USD, setting the profit target and symmetrical stop-loss at 5 percent. Chart I-11Go Long GBP/USD

Go Long GBP/USD Go Long GBP/USD

Go Long GBP/USD Go Long GBP/USD

Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Chart 1CNY/USD At A Potential Turning Point

CNY/USD At A Potential Turning Point

CNY/USD At A Potential Turning Point

Chart 2Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Expect Hungarian Bonds To Rebound

Chart 3Copper's Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Chart 4US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

Chart 5CAD/SEK Is Reversing

CAD/SEK Is Reversing

CAD/SEK Is Reversing

Chart 6Financials Versus Industrials Has Reversed

Financials Versus Industrials Has Reversed

Financials Versus Industrials Has Reversed

Chart 7The Outperformance Of Resources Versus Biotech Has Ended

The Outperformance Of Resources Versus Biotech Has Ended

The Outperformance Of Resources Versus Biotech Has Ended

Chart 8The Outperformance Of Resources Versus Healthcare Has Ended

The Outperformance Of Resources Versus Healthcare Has Ended

The Outperformance Of Resources Versus Healthcare Has Ended

Chart 9FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

Chart 10Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Chart 11The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

Chart 12The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

Chart 13Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Chart 14German Telecom Outperformance Has Started To Reverse

German Telecom Outperformance Has Started To Reverse

German Telecom Outperformance Has Started To Reverse

Chart 15Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Chart 16ETH Is Approaching A Possible Capitulation

ETH Is Approaching A Possible Capitulation

ETH Is Approaching A Possible Capitulation

Chart 17The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

Chart 18The Strong Downtrend In The 3 Year T-Bond Has Ended

The Strong Downtrend In The 3 Year T-Bond Has Ended

The Strong Downtrend In The 3 Year T-Bond Has Ended

Chart 19A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 20Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 21Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Chart 22Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Chart 23Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Chart 24USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

Chart 25The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

Chart 26A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 27US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

Chart 28The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 The best measure of wage rates is the employment cost index (ECI) because it includes all forms of compensation including benefits and bonuses. 2 In fact, stock market profits are even more cyclical because, as well as wages, there are other sticky deductions from revenues such as interest and taxes. 3 All expressed as annualised rates. Fractal Trading System Fractal Trades

Welcome To The Topsy-Turvy Recession Of 2022!

Welcome To The Topsy-Turvy Recession Of 2022!

Welcome To The Topsy-Turvy Recession Of 2022!

Welcome To The Topsy-Turvy Recession Of 2022!

6-12 Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Executive Summary Biden Taps China-Bashing Consensus

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

House Speaker Nancy Pelosi’s visit to Taiwan reflects one of our emerging views in 2022: the Biden administration’s willingness to take foreign policy risks ahead of the midterm elections. Biden’s foreign policy will continue to be reactive and focused on domestic politics through the midterms. Hence global policy uncertainty and geopolitical risk will remain elevated at least until November 8. Biden is seeing progress on his legislative agenda. Congress is passing a bill to compete with China while the Democrats are increasingly likely to pass a second reconciliation bill, both as predicted. These developments support our view that President Biden’s approval rating will stabilize and election races will tighten, keeping domestic US policy uncertainty elevated through November. These trends pose a risk to our view that Republicans will take the Senate, but the prevailing macroeconomic and geopolitical environment is still negative for the ruling Democratic Party. We expect legislative gridlock and frozen US fiscal policy in 2023-24. Close Recommendation (Tactical) Initiation Date Return Long Refinitiv Renewables Vs. S&P 500 Mar 30, 2022 25.4% Long Biotech Vs. Pharmaceuticals Jul 8, 2022 -3.3% Bottom Line: While US and global uncertainty remain high, we will stay long US dollar, long large caps over small caps, and long US Treasuries versus TIPS. But these are tactical trades and are watching closely to see if macroeconomic and geopolitical factors improve later this year. Feature President Biden’s average monthly job approval rating hit its lowest point, 38.5%, in July 2022. However, Biden’s anti-inflation campaign and midterm election tactics are starting to bear fruit: gasoline prices have fallen from a peak of $5 per gallon to $4.2 today, the Democratic Congress is securing some last-minute legislative wins, and women voters are mobilizing to preserve abortion access. These developments mean that the Democratic Party’s electoral prospects will improve marginally between now and the midterm election, causing Senate and congressional races to tighten – as we have expected. US policy uncertainty will increase. Investors will see a rising risk that Democrats will keep control of the Senate – and conceivably even the House – and hence retain unified control of the executive and legislative branches. This “Blue Sweep” risk will challenge the market consensus, which overwhelmingly (and still correctly) expects congressional gridlock in 2023-24. A continued blue sweep would mean larger tax hikes and social spending, while gridlock would neutralize fiscal policy for the next two years. Investors should fade this inflationary blue sweep risk and continue to plan for disinflationary gridlock. First, our quantitative election models still predict that Democrats will lose control of both House and Senate (Appendix). Second, Biden’s midterm tactics face very significant limitations, particularly emanating from geopolitics – the snake in this report’s title. Pelosi’s Trip To Taiwan Raises Near-Term Market Risks One of Biden’s election tactics is our third key view for 2022: reactive foreign policy. Initially we viewed this reactiveness as “risk-averse” but in May we began to argue that Biden could take risky bets given his collapsing approval ratings. Either way, Biden is using foreign policy as a means of improving his party’s domestic political fortunes. In particular, he is willing to take big risks with China, Russia, Iran, and terrorist groups like Al Qaeda. The template is the 1962 congressional election, when President John F. Kennedy largely defied the midterm election curse by taking a tough stance against Russia in the Cuban Missile Crisis (Chart 1). If Biden achieves a foreign policy victory, then Democrats will benefit. If he instigates a crisis, voters will rally around his administration out of patriotism. Nancy Pelosi’s visit to Taipei is the prominent example of this key view. The trip required full support from the US executive branch and military and was not only the swan song of a single politician. It was one element of the Biden administration’s decision to maintain the Trump administration’s hawkish China policy. Thus while Congress passes the $52 billion Chips and Science Act to enhance US competitiveness in technology and semiconductor manufacturing, Biden is also contemplating tightening export controls on computer chip equipment that China needs to upgrade its industry.1 Biden is reacting to a bipartisan and popular consensus holding that the US needs to take concrete measures to challenge China and protect American industry (Chart 2). This is different from the old norm of rhetorical China-bashing during midterms. Chart 1Biden Provokes Foreign Rivals

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Chart 2Biden Taps China-Bashing Consensus

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Reactive US foreign policy will continue through November and possibly beyond – including but not limited to China. The US chose to sell long-range weapons to Ukraine and provide intelligence targeting Russian forces, prompting Russia to declare that the US is now “directly” involved in the Ukraine conflict. The US decision to eradicate Al Qaeda leader Ayman Al-Zawahiri also reflects this foreign policy trend. Reactive foreign policy will increase the near-term risk of new negative geopolitical surprises for markets. Note that the 1962 Cuban Missile Crisis analogy is inverted when it comes to the Taiwan Strait. China is willing to take much greater risks than the US in its sphere of influence. The same goes for Russia in Ukraine. If US policy backfires then it may assist the Democrats in the election – but not if Biden suffers a humiliation or if the US economy suffers as a result. Chart 3US Import Prices Will Stay High From Greater China

US Import Prices Will Stay High From Greater China

US Import Prices Will Stay High From Greater China

US import prices will continue to rise from Greater China (Chart 3), undermining Biden’s anti-inflation agenda. Supply kinks in the semiconductor industry will become relevant again whenever demand rebounds (Chart 4). Global energy prices will also remain high as a result of the EU’s oil embargo and Russia’s continued tightening of European natural gas supplies. Chart 4New Semiconductor Kinks Will Appear When Demand Recovers

New Semiconductor Kinks Will Appear When Demand Recovers

New Semiconductor Kinks Will Appear When Demand Recovers

OPEC has decided only to increase oil production by 100,000 barrels per day, despite Biden’s visit to Saudi Arabia cap in hand. We argued that the Saudis would give a token but would largely focus on weakening global demand rather than pumping substantially more oil to help Biden and the Democrats in the election. The Saudis know that Biden is still attempting to negotiate a nuclear deal with Iran that would free up Iranian exports. So the Saudis are not giving much relief, and if Biden fails on Iran, oil supply disruptions will increase. Bottom Line: Price pressures will intensify as a result of the US-China and US-Russia standoffs – and probably also the US-Iran standoff. Hawkish foreign policy is not conducive to reducing inflationary ills. Global policy uncertainty and geopolitical risk will remain high throughout the midterm election season, causing continued volatility for US equities. Abortion Boosts Democratic Election Odds Earlier this year we highlighted that the Supreme Court’s overturning of the 1972 Roe v. Wade decision would lead to a significant mobilization of women voters in favor of the Democratic Party ahead of the midterm election. The first major electoral test since the court’s ruling, a popular referendum in the state of Kansas, produced a surprising result on August 2 that confirms and strengthens this thesis. Kansas is a deeply religious and conservative state where President Trump defeated President Biden by a 15% margin in 2020. The referendum was held during the primary election season, when electoral turnout skews heavily toward conservatives and the elderly. Yet Kansans voted by an 18% margin (59% versus 41%) not to amend the constitution, i.e. not to empower the legislature to tighten regulations on abortion. Voter turnout is not yet reported but likely far higher than in recent non-presidential primary elections. Kansans voted in the direction of nationwide opinion polling on whether abortion should be accessible in cases where the mother’s health is endangered. They did not vote in accordance with more expansive defenses of abortion, which are less popular (Chart 5). If the red state of Kansas votes this way then other states will see an even more substantial effect, at least when abortion is on the ballot. Chart 5Abortion Will Mitigate Democrats’ Losses

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

The question is how much of this Roe v. Wade effect will carry over to the general congressional elections. The referendum focused exclusively on abortion. Voters did not vote on party lines. Voters never like it when governments try to take away rights or privileges that have previously been granted. But in November the election will center on other topics, including inflation and the economy. And midterm elections almost always penalize the incumbent party. Our quantitative election models imply that Democrats will lose 22 seats in the House and two seats in the Senate, yielding Congress to the Republicans next year (Appendix). Still, women’s turnout presents a risk to our models. Women’s support for the Democratic Party has not improved markedly since the Supreme Court ruling, as we have shown in recent reports (Chart 6). But the polling could pick up again. Women’s turnout could be a significant tailwind in a year of headwinds for the Democrats. Bottom Line: Democrats’ electoral prospects have improved, as we anticipated earlier this year (Chart 7). This trend will continue as a result of the mobilization of women. Republicans are still highly likely to take Congress but our conviction on the Senate is much lower than it is on the House. Chart 6Biden’s And Democrats’ Approval Among Women

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Chart 7Democrats’ Odds Will Improve On Margin

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Reconciliation Bill: Still 65% Chance Of Passing Ultimately Democrats’ electoral performance will depend on inflation, the economy, and cyclical dynamics. If inflation falls over the course of the next three months, then Democrats will have a much better chance of stemming midterm losses. That is why President Biden rebranded his slimmed down “Build Back Better” reconciliation bill as the “Inflation Reduction Act.” We maintain our 65% odds that the bill will pass, as we have done all year. There is still at least a 35% chance that Senator Kyrsten Sinema of Arizona could defect from the Democrats, given that she opposed any new tax hikes and the reconciliation bill will impose a 15% minimum tax on corporations. A single absence or defection would topple the budget reconciliation process, which enables Democrats to pass the bill on a simple majority vote. We have always argued that Sinema would ultimately fall in line rather than betraying her party at the last minute before the election. This is even more likely given that moderate-in-chief, Senator Joe Manchin of West Virginia, negotiated and now champions the bill. But some other surprise could still erase the Democrats’ single-seat majority, so we stick with 65% odds. Most notably the bill will succeed because it actually reduces the budget deficit – by an estimated $300 billion over a decade (Table 1). Deficit reduction was the original purpose of lowering the number of votes required to pass a bill under the budget reconciliation process. Now Democrats are using savings generated from new government caps on pharmaceuticals (a popular measure) to fund health and climate subsidies. Given deficit reduction, it is conceivable that a moderate Republican could even vote for the bill. Table 1Democrats’ Inflation Reduction Act (Budget Reconciliation)

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Bottom Line: Democrats are more likely than ever to pass their fiscal 2022 reconciliation bill by the September 30 deadline. The bill will cap some drug prices and reduce the deficit marginally, so it can be packaged as an anti-inflation bill, giving Democrats a legislative win ahead of the midterm. However, its anti-inflationary impact will ultimately be negligible as $300 billion in savings hardly effects the long-term rising trajectory of US budget deficits relative to output. The bill will add to voters’ discretionary income and spur the renewable energy industry. And if it helps the Democrats retain power, then it enables further spending and tax hikes down the road, which would prove inflationary. The reconciliation bill, annual appropriations, and the China competition bill were the remaining bills that we argued would narrowly pass before the US Congress became gridlocked again. So far this view is on track. Investment Takeaways Companies that paid a high effective corporate tax rate before President Trump’s tax cuts have benefited relative to those that paid a low effective rate. They stood to suffer most if Trump’s tax cuts were repealed. But Democrats were forced to discard their attempt to raise the overall corporate tax rate last year. Instead the minimum corporate rate will rise to 15%, hitting those that paid the lowest effective rate, such as Big Tech companies, relative to high-tax rate sectors such as energy (Chart 8, top panel). Tactically energy may still underperform tech but cyclically energy could outperform and the reconciliation bill would feed into that trend. Similarly, companies that faced high foreign tax risk, because they made good income abroad but paid low foreign tax rates, stand to suffer most from the imposition of a minimum corporate tax rate (Chart 8, bottom panel). Again, Big Tech stands to suffer, although it has already priced a lot of bad news and may not perform poorly in the near term. Chart 8Market Responds To Minimum Corporate Tax

Market Responds To Minimum Corporate Tax

Market Responds To Minimum Corporate Tax

Chart 9Market Responds To New Climate Subsidies

Market Responds To New Climate Subsidies

Market Responds To New Climate Subsidies

Renewable energy stocks have rallied sharply on the news of the Democrats’ reconciliation bill getting back on track (Chart 9). We are booking a 25.4% gain on this tactical trade and will move to the sidelines for now, although renewable energy remains a secular investment theme. Health stocks, particularly pharmaceuticals, have taken a hit from the new legislation as we expected. However, biotech has not outperformed pharmaceuticals as we expected, so we will close this tactical trade for a loss of 3.3%. The reconciliation bill will cap drug prices for only the most popular generic drugs and does not pose as much of a threat to biotech companies (Chart 10). Biotech should perform well tactically as long bond yields decline – they are also historically undervalued, as noted by Dhaval Joshi of our Counterpoint strategy service. So we will stick to long Biotech versus the broad market. US semiconductors remain in a long bull market and will be in heavy demand once global and US economic activity stabilize. They are also likely to outperform competitors in Greater China that face a high and persistent geopolitical risk premium (Chart 11). Chart 10Market Responds To Drug Price Caps

Market Responds To Drug Price Caps

Market Responds To Drug Price Caps

Chart 11Market Responds To China Competition Bill

Market Responds To China Competition Bill

Market Responds To China Competition Bill

Tactically we prefer bonds to stocks, US equities to global equities, defensive sectors to cyclicals, large caps to small caps, and growth stocks to value stocks (Chart 12). The US is entering a technical recession, Europe is entering recession, China’s economy is weak, and geopolitical tensions are at extreme highs over Ukraine, Taiwan, and Iran. The US is facing an increasingly uncertain midterm election. These trends prevent us from adding risk in our portfolio in the short term. However, much bad news is priced and we are on the lookout for positive economic surprises and successful diplomatic initiatives to change the investment outlook for 2023. If the US and China recommit to the status quo in the Taiwan Strait, if Russia moves toward ceasefire talks in Ukraine, if the US and Iran rejoin the 2015 nuclear deal, then we will take a much more optimistic attitude. Some political and geopolitical risks could begin to recede in the fourth quarter – although that remains to be seen. And even then, geopolitical risk is rising on a secular basis. Chart 12Tactically Recession And Geopolitics Will Weigh On Risk Assets

Tactically Recession And Geopolitics Will Weigh On Risk Assets

Tactically Recession And Geopolitics Will Weigh On Risk Assets

Matt Gertken Senior Vice President Chief US Political Strategist mattg@bcaresearch.com Footnotes 1 Alexandra Alper and Karen Freifeld, “U.S. considers crackdown on memory chip makers in China,” Reuters, August 1, 2022, reuters.com. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Table A3US Political Capital Index

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Chart A1Presidential Election Model

Third Quarter US Political Outlook: Last Ditch Effort

Third Quarter US Political Outlook: Last Ditch Effort

Chart A2Senate Election Model

Third Quarter US Political Outlook: Last Ditch Effort

Third Quarter US Political Outlook: Last Ditch Effort

Table A4House Election Model

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Table A5APolitical Capital: White House And Congress

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Table A5BPolitical Capital: Household And Business Sentiment

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Table A5CPolitical Capital: The Economy And Markets

Biden's Midterm Tactics Bear Fruit… But There's A Snake

Biden's Midterm Tactics Bear Fruit… But There's A Snake

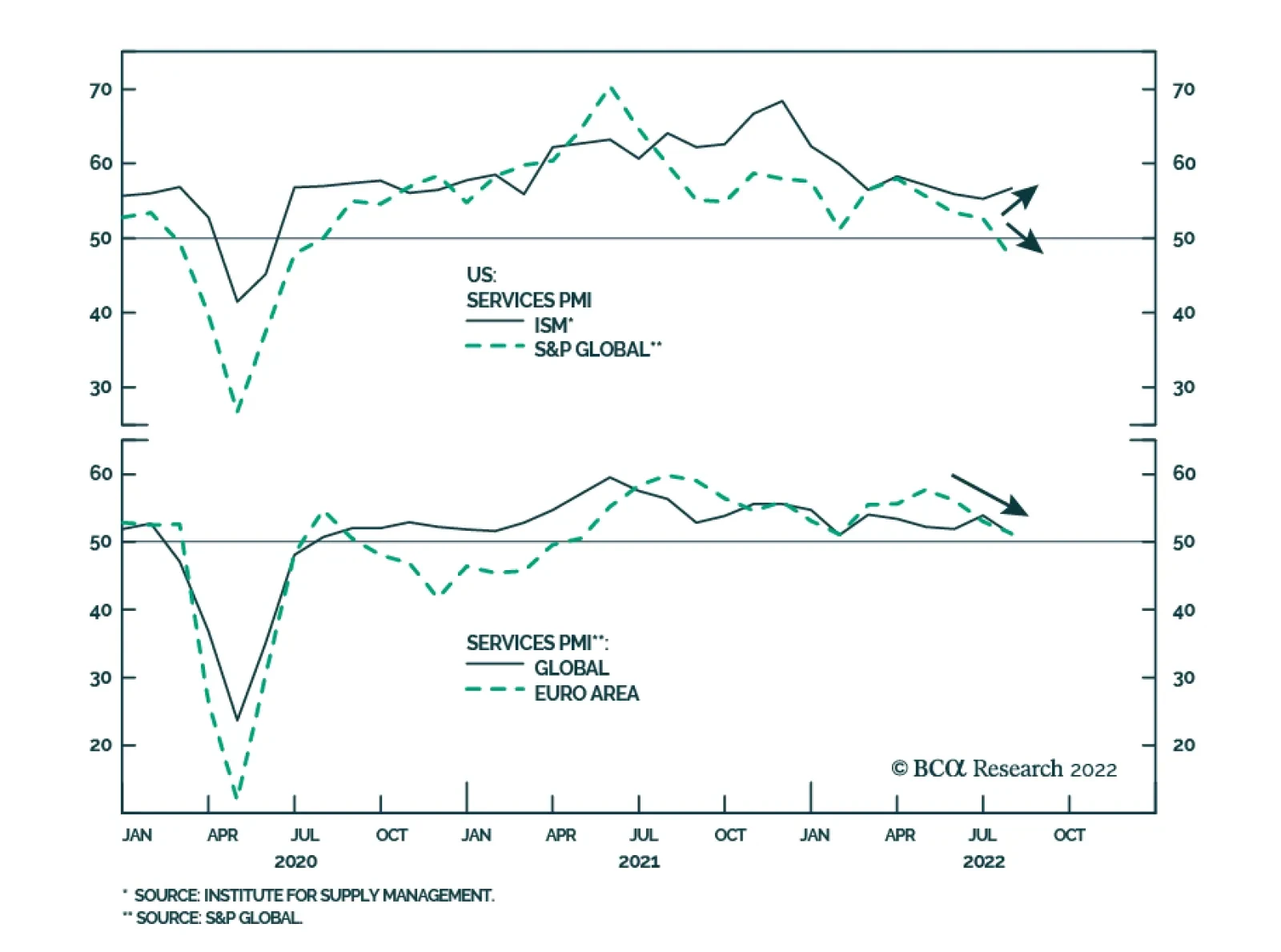

The final prints of July’s Eurozone and US Services and Composite PMIs were revised up from their preliminary estimates. Notably, the July Eurozone Composite gauge suggests that economic activity stagnated in June (final PMI estimate of 49.9 against a…

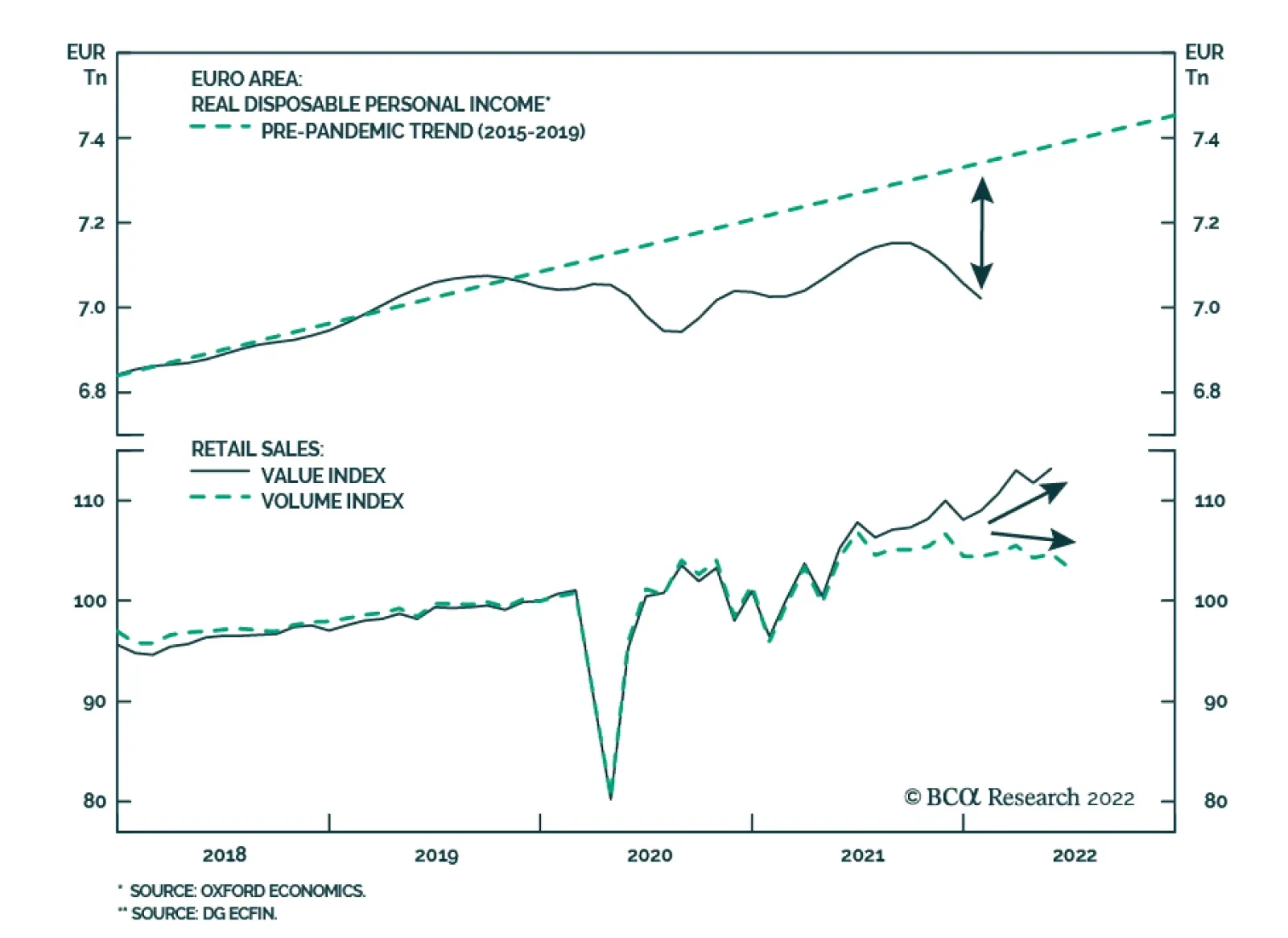

Eurozone retail sales disappointed in June. The 3.7% y/y contraction in sales volumes marks the first annual decline since February 2021 and is significantly worse than expectations of a 1.7% decrease. Similarly, the 1.2% m/m drop disappointed expectations…

Following the recent sharp post-FOMC rally, BCA Research’s Global Investment Strategy service has shifted their 12-month equity recommendation from overweight to neutral. They expect stock prices to rise further during the remainder of the year as US…

Executive Summary Government bond yields worldwide are falling due to fears of a global recession that will lead to monetary easing in 2023. This pricing is too optimistic with inflation likely to remain well above central bank targets next year. Even though US real GDP contracted modestly in the first half of 2022, the broader flow of US economic data is more consistent with an economy that is slowing substantially but not yet in recession. The Fed welcomes sharply slower growth to deal with high inflation, but will not unwind the 2022 rate hikes as quickly as markets expect given sticky core/wage inflation. The Fed rate cuts now discounted for 2023 will likely not be delivered. No Major Recessionary Signal From Global Yield Curves … Yet

No Major Recessionary Signal From Global Yield Curves . . . Yet

No Major Recessionary Signal From Global Yield Curves . . . Yet

Bottom Line: Falling global bond yields have helped stabilize risk assets – a path that will eventually lead to a rebound in yields if easier financial conditions help avoid a deep recession. Stay neutral overall duration exposure in global bond portfolios. The Great Recession Debate Begins Global bond yields have seen substantial declines over the past few weeks, as the market narrative has quickly changed from surging inflation and rate hikes to imminent recession and eventual rate cuts (Chart 1). The truth is somewhere in the middle, with global inflation in the process of peaking and global growth slowing rapidly but not yet in full-blown recession. Related Report Global Fixed Income StrategyMixed Messages & Range-Bound Bond Yields Bond markets are expecting central banks, most importantly the Fed, to quickly abandon the fight against high inflation for a new battle to tackle decelerating economic growth. The problem for investors is that weaker growth is needed – and, indeed, welcomed by policymakers - to create economic slack to help bring down elevated inflation. There is little evidence of such a disinflationary slack being created, with unemployment rates still near cyclical lows in the US, Europe and most of the developed world. The link between longer-term bond yields and shorter-term interest rate expectations remains strong in an environment of very flat government yield curves. For example, in the US, the 10-year Treasury yield has fallen from a peak of 3.47% in mid-June to 2.67% at the end of July. Over the same period, the 1-month interest rate, two-years ahead priced into the US overnight index swap (OIS) curve fell from a peak of 3.1% to 2.1% (Chart 2). Chart 1A Downward Adjustment Of Interest Rate Expectations

A Downward Adjustment Of Interest Rate Expectations

A Downward Adjustment Of Interest Rate Expectations

Chart 2A Lower Trajectory For Rates Priced In As Growth Slows

A Lower Trajectory For Rates Priced In As Growth Slows

A Lower Trajectory For Rates Priced In As Growth Slows

An even more dramatic decline in yields has been seen in Europe. The 10-year German Bund yield has fallen from a mid-June peak of 1.75% to 0.83% at the end of July, while the 1-month/2-year forward European OIS rate fell from 2.5% to 1.1%. The 2-year German yield, most sensitive to ECB rate hike expectations, also fell dramatically from 1.15% to 0.24%. There have also been substantial declines in bond yields and rate expectations in the UK, Canada and Australia over the past six weeks. As central banks continue to raise policy rates towards levels perceived to be at least neutral, if not mildly restrictive, there should a stronger correlation between future rate hike expectations and longer-term bond yields. Put another way, yield curves tend to flatten and eventually invert as policymakers move rates to levels that should slow growth and, eventually, reduce inflation. Currently, the “global” 2-year/10-year government bond yield curve, using Bloomberg Global Treasury index data, is slightly inverted at -13bps (Chart 3). More deeper curve inversions typically precede major contractions in global growth and equity prices. Chart 3No Major Recessionary Signal From Global Yield Curves . . . Yet

No Major Recessionary Signal From Global Yield Curves . . . Yet

No Major Recessionary Signal From Global Yield Curves . . . Yet

At the moment, global equities have performed in line with deeper curve inversions and contracting growth, with the MSCI World equity index down -7% on a year-over-year basis (bottom panel). Yet actual global growth is not yet in contraction. Global industrial production, while slowing, is still growing at a +3% year-over-year rate. The global manufacturing PMI remains above 50, indicative of a still-expanding manufacturing sector. Euro area, which is widely believed to already be in recession, saw real GDP growth (non-annualized) of +0.5% and +0.7%, respectively, in Q1 and Q2 of this year. Meanwhile, US real GDP shrank modestly over the first half of 2022, down only -0.6% (non-annualized) over Q1 and Q2, but with no corroborating evidence of recession from the labor market with the headline unemployment rate falling from 4.0% to 3.6% over that same period. Further adding to the confusing mix of signals between yield curves and growth is that the curve inversion at the global level is not yet evident across all countries. For example, the 2-year/10-year curve is inverted in the US and Canada, countries where central banks have been more aggressive on hiking rates in 2022 (Chart 4A) Yet in both countries, there have only been moderate declines in leading economic indicators and composite PMIs (combining manufacturing and services). In contrast, the 2-year/10-year curve in Germany and the UK – where the ECB and Bank of England have delivered fewer rates than the Fed and Bank of Canada – remains positively sloped but with similar moderate declines in leading economic indicators and composite PMIs to those seen in the US and Canada (Chart 4B). Chart 4AA Policy-Driven Slowdown In North America

A Policy-Driven Slowdown In North America

A Policy-Driven Slowdown In North America

Chart 4BAn Energy-Driven Slowdown In Europe

An Energy-Driven Slowdown In Europe

An Energy-Driven Slowdown In Europe

Chart 5Central Banks Cannot Pivot Dovishly Against This Backdrop

Central Banks Cannot Pivot Dovishly Against This Backdrop

Central Banks Cannot Pivot Dovishly Against This Backdrop

The deceleration of growth seen so far in this countries is nowhere near enough for central banks to begin contemplating a pivot away from hawkish rate hikes in 2022 to dovish rate cuts in 2023/24, as markets are now discounting. Inflation rates remain far too elevated, and labor markets remain far too tight, for policymakers to switch from the brake pedal to the gas pedal (Chart 5). This exposes global bond yields to a rebound from recent lows as central banks disappoint the market’s growing belief that policymakers’ focus will turn to growth from inflation. The language from recent central bank policy decisions, from the ECB’s 50bp hike on July 21 to the Fed’s 75bp hike last week to yesterday’s 50bp hike by the Reserve Bank of Australia, has been consistent, calling for a continued need to tighten policy. All three central banks essentially abandoned forward guidance, but described future rate moves as being “data dependent”, particularly inflation data. There is likely to be some relief from elevated inflation rates over the next few months. There have already been substantial declines in the growth of commodity prices, with the CRB Raw Industrials index now contracting in year-over-year terms (Chart 6). Global shipping costs and supplier delivery times have also declined, as evidence of some easing of supply chain disruptions that is helping bring down goods inflation. Yet given the starting point of such high headline inflation rates – at or above 9% in the US, UK and euro area – it is unlikely that there will be enough disinflation from the commodity/goods space to quickly bring inflation down by enough for central banks to breathe easier. This is especially true given that stickier domestically generated inflation stemming from wages and services will remain well above central bank targets over at least the next year, or at least until there is a substantial increase in slack-producing unemployment (i.e. a recession). What does all this mean for our view on the direction of global bond yields? We still see the current environment as more consistent with broad trading ranges for yields, rather than the start of a new major downtrend or uptrend. Europe was the one exception to this view, given how markets were pricing in a rise in ECB policy rates that was too aggressive, but even that has now corrected after the dramatic collapse in core European yields from the mid-June peak. Our Global Duration Indicator has been calling for a loss of cyclical upward momentum of bond yields in the latter half of 2022, which is now starting to play out (Chart 7). That indicator is focused on growth indicators like our global leading economic indicator and the ZEW expectations index for the US and Europe, all of which have been declining for the past several months. Chart 6Global Inflation Is Peaking

Global Inflation Is Peaking

Global Inflation Is Peaking

Chart 7Stay Neutral On Global Duration Exposure

Stay Neutral On Global Duration Exposure

Stay Neutral On Global Duration Exposure

However, there is a potential note of economic optimism from another key component of the Global Duration Indicator - the diffusion index of our global leading economic indicator, which measures the number of countries with rising leading indicators versus those with falling ones. That diffusion index has hooked up as the leading economic indicators of some important countries that are typically leveraged to global growth – China, Japan, Brazil, Korea and Malaysia – have started to move higher. If this trend continues in the months ahead, our Duration Indicator may signal a reacceleration of global bond yield momentum in the first half of 2023 as the global growth outlook improves. Bottom Line: Bond markets are overreacting to slowing global growth momentum by pricing in a quick reversal of 2022 rate hikes in 2023 across the developed world. Do not chase bond yields lower. The Fed Will Respond To Inflation Before Recession The Q2/2022 US GDP report showed an annualized decline of -0.9%, following on the annualized -1.6% fall in Q1 real GDP (Chart 8). This fulfills the so-called “technical definition” of a recession widely cited by the financial media. However, the official arbiters of recession dating – the National Bureau of Economic Research, or NBER – use a broader list of data to identify recessions that focus on income growth, employment and industrial production. None of those indicators contracted in the first half of the year, when the GDP-defined recession allegedly took place. We are sympathetic to the view that the US has not yet entered recession. However, recession odds are increasing, with many reliable cyclical data series slowing to a pace that has preceded past recessions. In Chart 9, we show a “cycle-on-cycle” comparison of the latest readings on some highly cyclical US economic data with readings from past recessions dating back to the late 1970s. In the chart, the data series are lined up such that the vertical line represents the NBER-designated start date of each recession, starting with the 1979/80 recession up to the 2008 recession. We show both the average path for each series across all of those recessions (the dotted line) and the range of outcomes from each recession (the shaded zone). Given the unique nature of the 2020 COVID recession, which was limited to just one quarter of collapsing activity due to pandemic lockdowns rather than typical business cycle forces, we did not include that episode in this chart. Chart 8No US Growth In H1/2022

No US Growth In H1/2022

No US Growth In H1/2022

The selected variables in this cycle-on-cycle analysis are: The year-over-year growth of the Conference Board leading economic indicator The ISM manufacturing index The University Of Michigan consumer expectations index The year-over-year growth of housing starts The year-over-year growth rate of non-financial (top-down) corporate profits. Chart 9The US Is Definitely Flirting With Recession

The US Is Definitely Flirting With Recession

The US Is Definitely Flirting With Recession

All five series selected have slowed over past several months, consistent with the run-up to previous recessions. However, in terms of timing, not all of the indicators shown are at levels that would be consistent with the US already being in a recession, as the real GDP contractions in Q1 and Q2 would suggest. Typically, the ISM index falls below 50 at the start of the recession, while the growth in the leading indicator turns negative about six months before the start of the recession. The current readings on both are still modestly above levels seen at the start of those past recessions. Corporate profit growth typically contracts for a full year ahead of recessions, and the latest complete reading available from Q1 was still showing positive, albeit slowing, growth. Chart 10The Fed Is OK With This Outcome, Given High Inflation

The Fed Is OK With This Outcome, Given High Inflation

The Fed Is OK With This Outcome, Given High Inflation