United States

According to BCA Research’s Global Investment Strategy service, the high market share commanded by big American firms could end up being a liability. This dominance could bait regulatory attention, thereby affecting these firms’ growth prospects. The…

Feature Clean energy names rallied yesterday on the back of the news that a reconciliation deal was struck to support Biden’s fiscal package. The deal, which was dubbed the “Inflation Reduction Act Of 2022”, includes approximately $370 billion in clean energy spending as well as EV tax credits for both new and used cars. The bill has been sent to President Biden for his signature. The bill is a boon to two of our long-term investment themes: “EV Revolution” and “Is It Time To Invest Green And Clean?”. In both reports, we argued that both themes were to benefit from the favorable legislative tailwinds thanks to this administration’s focus on climate change prevention policies. Since its inception in June 2021, the EV theme has outperformed the S&P 500 by 15%, while the “Green and Clean” theme is up 14% since the April 2022 inauguration report. When it comes to investing in green technology and EV, we recommend investors continue to treat them as long-term thematic calls. Technological innovation themes are intrinsically risky: They are rarely immediately profitable and require both continuous investment and technological breakthroughs to succeed. As such, they are fickle over short term but pay off over a longer investment horizon. On a tactical basis both EV and clean energy stocks may be ripe for a pullback after a robust rally (Chart 2). Chart 1

On The Clean Energy Deal

On The Clean Energy Deal

Chart 2

On The Clean Energy Deal

On The Clean Energy Deal

Thematic themes are best captured either via an ETF or a custom basket. Green energy ETFs are TAN, FAN, RNRG, CTEC, RAYS, and WNDY. Electric vehicle ETFs are ARKQ, IDRIV, DRIV, and KARS (See appendix for details). Bottom Line: We reiterate our structural preference for green technology and EV stocks on the back of strong legislative support and a continuous push for innovation and affordability. Appendix Table 1

On The Clean Energy Deal

On The Clean Energy Deal

Table 2

On The Clean Energy Deal

On The Clean Energy Deal

Listen to a short summary of this report. Executive Summary The Dollar Rises During Recessions

How Deep A Recession Is The Dollar Pricing In?

How Deep A Recession Is The Dollar Pricing In?

At 106.5, the dollar DXY index is certainly pricing in a recession deeper than during the Covid-19 crisis. The dollar tends to rise during recessions and only peaks when a global economic recovery is in sight (Feature Chart). One caveat: contrary to conventional wisdom, US economic data is deteriorating relative to the rest of the world. Historically, that has been a negative for the greenback. The key question facing investors is if markets are entering a riot point. That is a high probability. Historically, high volatility supports the dollar. As such, our recommended stance on the dollar is neutral over the next few months. Our highest conviction bets are short EUR/JPY and long Swiss franc trades. Valuations tend to matter when most investors least expect them to. On this basis, we are negative the dollar on a 12-to-18 month time horizon. Place a limit sell on CHF/SEK at 10.76. TRADES* INITIATION DATE PERCENT RETURNS Short EUR/JPY 2022-07-21 2.73% Bottom Line: Stand aside on the dollar for now. Continue to opportunistically play trades at the crosses. Short EUR/JPY bets make sense as a volatility hedge. Chart 1Any Dollar Bears Left?

Any Dollar Bears Left?

Any Dollar Bears Left?

In our conversations with clients, it is rare to find a dollar bear these days. One barometer is price action – the dollar DXY index is up 18% from its 2021 lows. More instructively, net long speculative positions are near a multi-decade high (Chart 1). In our meetings, we sense a specter of capitulation among fundamental dollar bears, as the macroeconomic environment becomes more uncertain. For chart enthusiasts, the DXY index staged a classic breakout, and the next technical level is closer to the 2002 highs near 120. We doubt the DXY index will hit this level, as significant headwinds are building. It is true that as markets increasingly price in the probability of a recession, especially in Europe, the dollar will be bought. But as we argue below, the dollar has already priced in a recession, deeper than was the case in 2020 (or admittedly, at any time since the end of the Bretton Woods system). This suggests that investors with a relatively benign economic backdrop should be fading any strength in the dollar. In other words, if your bet on a recession is low odds, fade dollar strength relatively to your colleagues. As such, our recommended stance on the dollar is neutral over the next few months, but bearish for investors with a longer-term horizon. For today, our highest conviction bets are short EUR/JPY and long Swiss franc trades. The US Dollar And Global Growth Chart 2The Dollar Tracks Global Growth

The Dollar Tracks Global Growth

The Dollar Tracks Global Growth

There are many important drivers of the US dollar. One is the path for global growth. If global activity is going to slow meaningfully, then as a countercyclical currency, the dollar tends to rise in that environment. The dollar has been closely correlated (inversely) to the trend in global PMIs, industrial production, and other measures of global growth (Chart 2). Across the world, global growth is slowing (Chart 3). Most manufacturing PMIs in the developed world peaked in the middle of last year. In the developing world, China’s zero Covid-19 policy has nudged many PMIs close to the 50 boom/bust level. As a rule of thumb, you do not want to be short the greenback when global industrial activity is slowing. That is the bull case. Chart 3AGlobal Growth Is Slowing In Developed Markets

Global Growth Is Slowing In Developed Markets

Global Growth Is Slowing In Developed Markets

Chart 3BGrowth Is Also Soft In Emerging Markets

Growth Is Also Soft In Emerging Markets

Growth Is Also Soft In Emerging Markets

The good news for dollar bears is that most of this information is already priced in. Looking back at recessions since the 1970s, the dollar is pricing in one of the most anticipated slowdowns in history (Chart 4). This alone is not a reason to turn bearish on the greenback, but it is a red flag towards the consensus view. In general, currencies are a relative game. The dollar tends to rise 10%-to-15% during recessions. We are already there, with the DXY index up 18% since the 2021 lows. It is also important to gauge how the US is faring relative to the rest of the world. Quite simply, US economy economic activity is deteriorating vis-à-vis its trading partners. This is visible in the Citigroup economic surprise indices, but also via a simple chart of relative PMIs (Chart 5). Historically, that has been a negative for the greenback outside of recessions. Chart 4The Dollar Overshoots During Recessions

How Deep A Recession Is The Dollar Pricing In?

How Deep A Recession Is The Dollar Pricing In?

Chart 5US Economic Momentum Is Deteriorating

US Economic Momentum Is Deteriorating

US Economic Momentum Is Deteriorating

The US Dollar And Interest Rates The Fed hiked interest rates by 75bps this week. This was as expected but given what the Bank of Canada delivered on July 13th, a 100bps hike was a whisper number in our books. More importantly, interest rate differentials (real and nominal) are increasingly moving against the US. As we go to press, 10-year bond yields are 2.67% in the US, but 2.62% in Canada, 3.41% in New Zealand, and even 3.1% in Australia. Chart 6The Euro And Relative Interest Rates

The Euro And Relative Interest Rates

The Euro And Relative Interest Rates

The key point is that the market consensus is centered around the Fed being the most hawkish central bank. That will face a critical test in the next few months, if the world enters a recession. This is especially true in the euro area. The market is pricing that interest rates in the eurozone will be 200bps lower next year, relative to the US (Chart 6). The historical spread between US and German 2-year yields has been 83 bps. If Europe indeed enters a deep recession, then that is already priced in the euro. If we get any green shoots in economic growth, then the euro is poised for a coiled-spring rebound. The market is also pricing in that US interest rates will peak next year, relative to other G10 economies (Chart 7). This could happen in one of two ways: The Fed turns more dovish and/or non-US growth loses steam, leading to lower interest rates outside the US. It is difficult to forecast how the economic scenario will evolve, but from an investor’s standpoint, the dollar has already overshot the level implied by relative interest rates (Chart 8). Chart 7US Short Real Yields Are Attractive

How Deep A Recession Is The Dollar Pricing In?

How Deep A Recession Is The Dollar Pricing In?

Chart 8The Dollar Has Overshot Rate Fundamentals

The Dollar Has Overshot Rate Fundamentals

The Dollar Has Overshot Rate Fundamentals

A Short Note On USD Valuations Valuations usually get little respect, especially over the last few years. The bull market in the dollar from 2011 to 2022 coincided with higher real interest rates in the US relative to the rest of the developed world. That said, a rising trade deficit (imports > exports) requires a lower exchange rate to boost competitiveness in the manufacturing sector, or less spending to reduce the trade deficit. Therefore, the natural adjustment mechanism for countries running wide trade deficits will have to be the exchange rate. Quite simply, rising deficits are a symptom of an overvalued exchange rate. Within a broad spectrum of developed and emerging market currencies, the US dollar is overvalued on a real effective exchange rate basis (Chart 9 and 10). While valuations tend to matter less until they trigger a tipping point, such inflections usually occur with a shift in animal spirits, especially when investors start to worry about huge external imbalances. Chart 9The Dollar Is Overvalued

The Dollar Is Overvalued

The Dollar Is Overvalued

Chart 10The Dollar Is One Of The Most Expensive Currencies

How Deep A Recession Is The Dollar Pricing In?

How Deep A Recession Is The Dollar Pricing In?

In the US, these imbalances are already starting to spark a shift. The US trade deficit has deteriorated. The basic balance in the US (the sum of the current account and foreign direct investment) is deteriorating. The dollar tends to decline on a multi-year basis when the basic balance peaks and starts deteriorating. It is remarkable that at a time when real rates are quite negative in the US, the dollar is the most overvalued in decades on a simple PPP model basis. This is a perfect mirror image of the dollar configuration at the start of the bull market in 2010, where the dollar was cheap and real rates were more supportive. According to economic theory, a currency should adjust to equalize returns across countries. In the early 80s, an expensive dollar was supported by very positive real rates. The subsequent dollar declines thereafter also coincided with falling real interest rates. If global growth shifts from relative strength in the US to overseas, interest rate differentials will tilt in favor of non-US markets. That will be solace for dollar bears. Conclusions In financial markets, it pays to be humble but also to be bold. Our recommended stance on the DXY (and by association, the euro and cable) is to stay on the sidelines. Our highest conviction trade is to short EUR/JPY. With the drop in commodity prices, resource-related currencies are becoming interesting, a topic we will discuss in upcoming bulletins. But momentum is your friend for now, which suggests prudence. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Strategic View Cyclical Holdings (6-18 months) Tactical Holdings (0-6 months) Limit Orders Forecast Summary

Listen to a short summary of this report. Executive Summary US Lead On Mega-Sized Firms: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

The US has been the star protagonist of global equity markets for decades. It offers investors the rare combination of a big economy and a large universe of mega-sized listed companies. In fact, the overwhelming majority of the top 20 largest firms globally by revenue today are American. But can the US maintain this degree of presence on this list over the next decade? We think that this is unlikely. For starters, a decline in the US’s footprint could be driven by the fact that there is a peculiar stagnation in the works in the middle tier of American firms. Given that this tier acts as a talent pool for big firms, a stagnation here could mean that the US spawns fewer super-sized firms. The high market share commanded by big American firms could also end up being a liability. This dominance could bait regulatory attention, thereby affecting these firms’ growth prospects. Finally, slowing GDP growth in the US, as compared to its Asian peers, will prove to be another headwind that American firms must contend with. What should strategic investors do to prepare for this tectonic shift? We recommend reducing allocations to US equities over the long run since the US’s weight in global indices will peak soon (or may have already peaked). Bottom Line: Irrespective of what the Fed does (or does not do), the US’s footprint in the global league tables of big firms by revenue will weaken over the next decade. Strategic investors can profit from this change by reducing allocations to US equities while increasing allocations to China as well as a basket of countries including Korea, Japan, Taiwan, and Germany. Dear Client, This week, we are sending you a Special Report by Ritika Mankar, CFA, who will be writing occasional special reports for the Global Investment Strategy service on a variety of topical issues. Ritika makes the case that the US economy’s ability to spawn mega-sized companies may become increasingly compromised over the next decade. We will return to our regular publishing schedule next week. Best Regards, Peter Berezin, Chief Global Strategist US: Home To The Largest Number Of Big Listed Firms 2022 has been a turbulent year for US markets so far. But it is worth bearing in mind that the US has been the star protagonist of global equity markets for decades. This is because the US has offered investors a near-perfect trifecta constituting of: (1) A mega-sized economy; (2) A large universe of mega-sized listed companies; and (3) A track record of market outperformance. Specifically: Largest Economy: For over a century now, the US has been the largest economy in the world – a title it is expected to defend over the next few years (Chart 1). Large Listed Companies: The US’s high nominal GDP has also translated into high sales growth for its listed space. This, in turn, powered a great rise in the American equity market’s capitalization (Chart 2). In fact, the US’s market cap is so large today that it exceeds the cumulative market cap of the next four largest economies in the world, by a wide margin. So unlike Germany or China (which have large economies but small markets), the US has a large economy and is also home to some of the largest, most liquid stocks globally. Chart 1The US Will Remain The World’s Largest Economy For The Next Few Years

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 2The Listed Universe In The US Has Grown From Strength To Strength

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 3Growing Sales In The US Have Powered Its Outperformance Over The Past Decade

Growing Sales In The US Have Powered Its Outperformance Over The Past Decade

Growing Sales In The US Have Powered Its Outperformance Over The Past Decade

Long History of Outperformance: And most importantly, the US market has a strong track record of outperformance. US markets have outperformed global benchmarks over the past decade thanks largely to the rapid sales growth seen by American firms (Chart 3). Notwithstanding the US’s star role in global markets thus far, in this report we highlight that the US’s heft will likely decline over the next decade. The Fed may or may not administer recession-inducing rate hikes in 2022. But irrespective of what the Fed does over the next 12-to-24 months, the US’s loss of influence in global equity markets appears certain because it will be driven by structural forces. Chart 4US Lead On Mega-Sized Firms: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Firstly, while behemoths such as Apple and Amazon have been attracting record investor attention, it is worth noting that the next tier of mid-sized American companies is no longer thriving as it used to. The reason why this matters is because history suggests that the pool of mid-sized companies acts as a superset for the big companies of tomorrow. So, if this talent pool is not booming today in the US, then there is likely to be repercussions tomorrow. Secondly, the US’s largest firms will have to contend with two structural headwinds over the next decade, namely increased regulatory attention and slowing growth. To complicate matters for American firms, competitors in Asia will not have this albatross around their neck. Hence, the US may remain the largest economy of the world a few years from now but is unlikely to be home to as many big, listed companies as it is today (Chart 4). The rest of this report quantifies the strength of these forces, and then concludes with actionable investment ideas. Trouble In The Talent Pool Chart 5The US Is Home To Nearly A Dozen Mega-Sized Firms Today

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

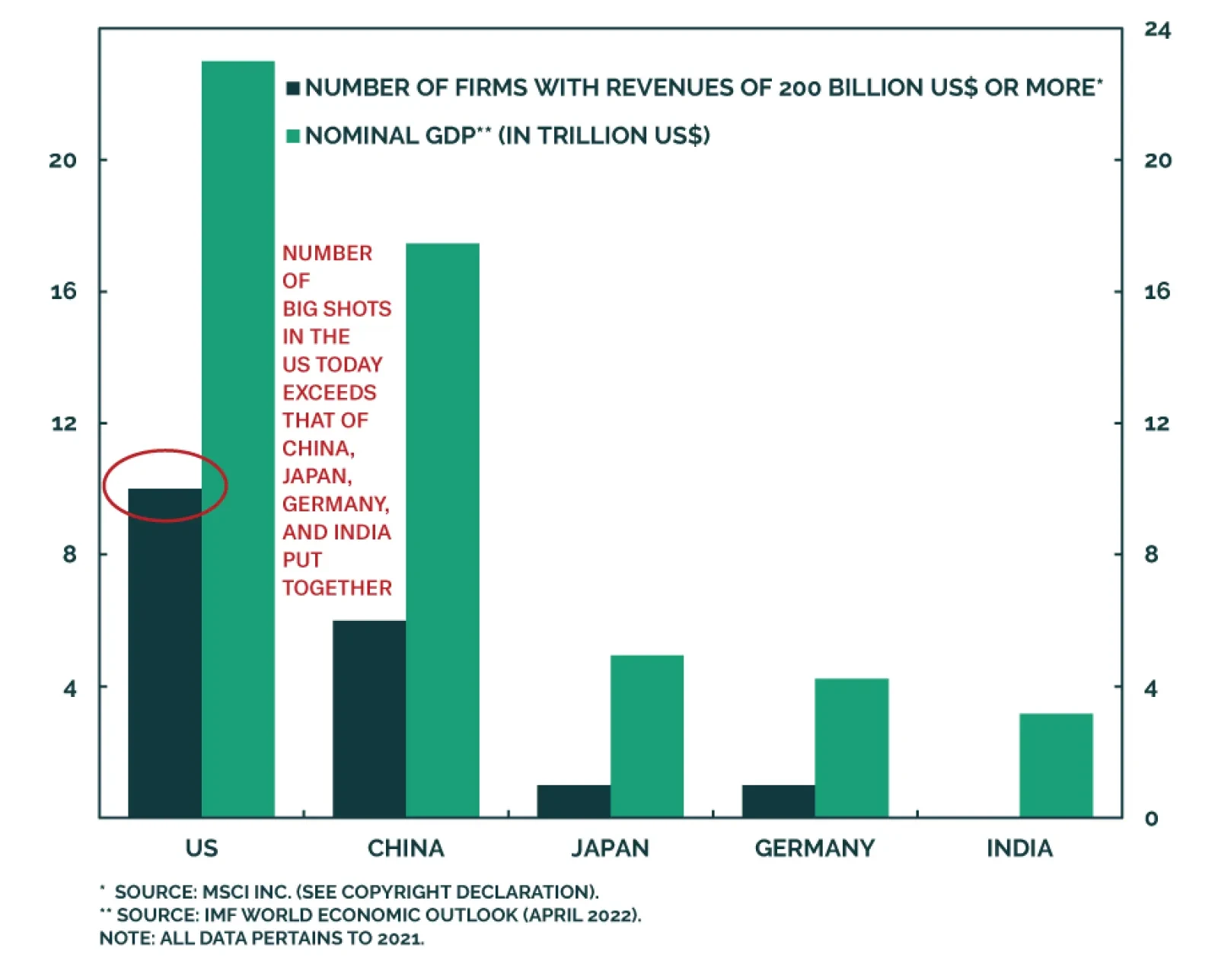

2021 produced a special milestone for the American economy. This was the first year that ten listed American firms1 surpassed $200 billion in annual revenues (firms we refer to as ‘Big Shots’ from here on) (Chart 5). The US has been a global leader when it came to the size of its economy for decades, but last year it also became home to the largest number of big, listed corporations (Table 1). American Big Shots were striking both in terms of their number as well as their scale. In fact, such was their scale that the combined revenue of these ten Big Shots now exceeded the nominal GDP of major economies like India (Chart 6). Table 1The US Today Dominates The Global List Of Top 20 Firms

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 6The Revenues Of US Big Shot Firms Are Comparable To India’s Nominal GDP!

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

While the world has been captivated by the size that the US’s Big Shots have achieved (as well as the ideas of their unconventional founders), few have noticed that the talent pool for tomorrow’s Big Shots is no longer burgeoning. History suggests that most Big Shot firms tend to emerge from firms belonging to a lower revenue tier. For instance, Amazon and Apple, which have revenues in the range of $350-to-$500 billion today, were mid-sized firms a decade ago with revenues in the vicinity of $50-to-$100 billion (Chart 7). Chart 7Most Big Shots Today Were The Mid-Sized Firms Of Yesterday

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

This is why it is worrying that all is not well in the US’s ecosystem of mid-sized firms. If we define firms with annual revenues of $50-to-$200 billion as ‘core’ firms, then their share in the total number of American firms has stagnated over the past decade (Chart 8). Even the revenue share accounted for by core firms has been fading (Chart 9). This phenomenon contrasts with the situation in China, where the mid-sized firms’ cohort has been growing over the last decade (Charts 10 and 11). Chart 8Share Of Mid-Sized Firms In The US Has Stagnated

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 9The Revenue Share Of US Mid-Sized Firms Is Also Falling

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 10Share Of Mid-Sized Firms In China Is Expanding

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 11The Revenue Share Of Chinese Mid-Sized Firms Is Rising

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Japan’s experience also suggests that when the mid-sized firms’ ecosystem weakens, the pipeline of future potential mega-cap companies get affected. In Japan, the proportion of core firms (Chart 12), as well as their revenue share (Chart 13), has not been growing as is the case, say, in China. And this is perhaps why, despite being the third-largest economy in the world today, Japan is home to only one listed mega-sized corporation with revenues of over $200 billion (Toyota).

Image

Chart 13The Revenue Share Of Japanese Mid-Sized Firms Has Plateaued

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

The US May Have Hit Peak Oligopolization The fact that ten Big Shot firms (i.e., firms with annual revenues of over $200 billion) exist in the US today is remarkable. After all, the number of Big Shot firms in the US today exceeds the total number of Big Shots in the next four largest economies of the world combined (Chart 14). Chart 14The US Today Is The Global Hub For Mega-Sized Companies

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

So why will the US’s leadership in this area come under pressure going forward? One reason is that the large size of American firms could itself become a liability. Specifically: Public Backlash Against The US’s Big Shots: The ten Big Shot firms of the US today account for more than a fifth of the revenue generated by all firms that constitute the MSCI US index (Chart 15). Also, the number of Big Shot firms, as a share of total firms, is high in the US (Chart 16). Chart 15Big Shots Account For More Than A Fifth Of Revenues Generated By The US Listed Space

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 16A Large Proportion Of Firms In The US Are Very Big

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Notably, market leaders across a range of key sectors in the US account for an unusually large chunk of the sector’s revenues. Financials, Information Technology, and Consumer Discretionary together account for about half of the US equity market index’s weight. The dominant firm in each of these three sectors (as defined by MSCI) accounts for 15%-to-25% of that sector’s revenue (Chart 17). Market power usually benefits investors. But too much market power can be a problem. The growing oligopolization of the US economy has caused public dissatisfaction over the influence of corporations in the US to hit a multi-year high (Chart 18). Over 60% of Americans want major US corporations to have less influence. It is for this reason that the record scale acquired by American firms could prove to be an issue. American mega-scaled firms’ high market shares will provide them with pricing power, but this very power will end up baiting regulatory attention and anti-trust lawsuits which, in turn, will restrict their future growth rates. The fact that the US Federal Trade Commission (FTC) today is headed by a leader who wants to return the FTC to its trust-busting origins, and made her name by writing a paper arguing for Amazon to be broken up,2 is indicative of which way the wind is blowing. Chart 17Market Leaders In The US Are Too Big

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 18Public Dissatisfaction With US Big Shot Firms Is High And Rising

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Interestingly, the speed at which the US restricts the market power of big firms will determine how quickly the US’s mid-sized firms begin to flourish again, thereby setting the stage for the US to spawn a new generation of big firms. Besides the growing regulatory risks for the US’s big firms, three other technical factors will end up slowing the pace at which the US can generate large firms, namely: Slowing GDP Growth: Since the US is a large and mature economy, the pace of its growth is bound to slow (Chart 19). Besides the deceleration in the US’s growth rate relative to its own past, it is projected to end up being lower than that of major economies like China. Chart 19US GDP Growth Is Set To Slow

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Big Business ≠ Big GDP Growth: While GDP growth receives a fillip when small firms grow, the high pricing power that very large firms command can end up constraining an economy’s growth rate. This is because large firms can charge monopolistic prices, thereby restraining demand. Secondly, mega-sized firms may actively invest in manipulating institutions to block upstarts,3 a dynamic that can restrict productivity growth as well. Chart 20The Revenue-To-Nominal GDP Ratio Is Already Elevated In The US

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Approaching Revenue Saturation: A cross-country comparison suggests that the revenue-to-nominal GDP ratio in the US is high1 (Chart 20). Only Japan has a superior ratio, which is likely to be an aberration rather than the norm (owing to Japanese firms’ unique tendency to prioritize revenues over profitability). Given that the US revenue-to-nominal GDP ratio is already elevated, it is likely that even as the US’s nominal GDP keeps growing, the pace of conversion of this GDP into revenues will stay the same or may even diminish over the coming decade. Prepare For A Brave New World “German judges…first read a description of a woman who had been caught shoplifting, then rolled a pair of dice that were loaded so every roll resulted in either a 3 or a 9. As soon as the dice came to a stop, the judges were asked whether they would sentence the woman to a term in prison greater or lesser, in months, than the number showing on the dice…On average, those who had rolled a 9 said they would sentence her to 8 months; those who rolled a 3 said they would sentence her to 5 months; the anchoring effect was 50%.” – Daniel Kahneman, Thinking, Fast and Slow (Farrar, Straus and Giroux, 2011) The US has been the largest economy in the world and has also been able to nurture some of the largest mega-scaled companies of today. Such is the might and size of these firms that it is impossible to imagine a world where American firms’ leadership could be disrupted. Moreover, it is mentally easier to extrapolate the US’s lead today into the future. It may even seem like there is no other alternative to the US since Japan’s economy has been stagnating, Europe lacks innovation, and the political environment in China is contentious. Also, it is true that the US today is the undisputed leader when it comes to qualitative factors such as the ability to attract top global talent, its education system, and its legal system. However, the case can be made that this belief (that the US’s lead on mega-sized companies will spill into the next decade) runs the risk of becoming a Kahneman-esque anchoring bias. This is because: History Suggests That Upsets Are The Norm: History suggests that the evolution of the top 20 global firms (by revenue) has been a story of upsets. For instance, Europe’s hold over this list in the 2000s was striking by all accounts (Chart 21). Back then, it would have been almost blasphemous to question Europe’s lead (Chart 22). But today firms from three Asian island-countries account for more companies on this list than all of pre-Brexit Europe put together. Chart 21In The 2000s, Europe Was The Epicenter Of Global Mega-Sized Firms

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Chart 22How The Mighty Can, And Do, Fall

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

China’s Disadvantages < Its Competitive Advantages: Despite its political baggage, China has the most formidable capability today to displace the US’s leadership position on the league tables of top 20 global firms by revenue. This is because China has a thriving ecosystem of core firms (Chart 11) and is set to grow at a faster clip than the US over the next five years (Chart 19). Moreover, while the Chinese government’s tolerance for large tech giants could remain low, the establishment could be keen to grow firms in the industrials as well as financials space for the sake of common prosperity. EM Listed Space Can Catch Up: The listed space in the US has developed at an exceptionally fast pace relative to its peers. The gap between US nominal GDP and listed space parameters is low (Chart 20), while the gap is wider for countries like Germany, China, and several other EMs. Even in a ceteris paribus situation where nominal GDPs were to stay static, an increase in the size of the listed universe in other countries can adversely affect the US’s current footprint. So, what can investors do to prepare for this coming tectonic shift? We recommend reducing allocations to US equities since the US’s weight in global indices will peak soon. It is worth noting that this strategic investment recommendation dovetails nicely with our earlier view that strategic investors should rotate out of US stocks. Currently, about half of the 20 largest firms globally by revenue are American (Map 1). Owing to the dynamics listed above, the number of American firms in the global league of top 20 could fall from this high level to 7 or 8 over the coming decade. Given that this change is indicative of things to come, we would urge investors to reduce allocations to US equities in a global portfolio over a strategic horizon. A confluence of micro and macro factors is likely to result in the US’s weight in global indices to crest sooner rather than later. Map 1Could The Global Epicenter Of Big Firms Drift Eastwards Over The Next Decade?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

In fact, US equities’ weight in a global index like the MSCI ACWI could have already peaked (Chart 23) and could fall by 500-to-600bps over the next decade if the last year’s trend is extrapolated into the future. As regards to sectors, health care appears to be the key industry where the US’s footprint could weaken (Table 2). Chart 23Loss Of US Influence Will Create Space For Underrepresented Markets To Grow

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Table 2China’s Weight In Top 20 Firms Is Set To Grow

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

As the US cedes its leadership position, we expect the global epicenter of mega-sized listed corporates to drift eastwards (Map 1). Specifically: China: Currently, less than a quarter of the 20 largest firms globally by revenue are Chinese (Map 1). It is highly likely that the number of Chinese firms in the global list of top 20 firms will increase. China should be able to spawn more mega-sized companies since it already has a cache of promising large and mid-sized companies. Chinese companies will also benefit from the high growth rate of China’s domestic economy. From a sectoral perspective, financials and industrials appear to be two sectors where China’s footprint could grow the most (Table 2). Asia Ex-China: Asian countries like Korea, Taiwan, and Japan could potentially end up growing their weight in global equity indices by becoming home to more than one company that makes it to the global league tables of large companies. Besides the high GDP growth rate on offer in their domestic markets (Chart 20), firms in these countries could increase scale by feeding a stimulus-fueled industrial boom in the US. Additionally, these Asian countries have a competitive advantage when it comes to high-tech manufacturing capabilities (Chart 24). This will ensure that they will accrue any offshore opportunities that arise. Taiwan has the potential to grow its presence in the Information Technology space, given its innate competitive advantages (Chart 24) and the positive structural outlook for global semiconductor demand. In the case of India, it is worth noting that the country’s influence in the world economy will be ascendant over the next decade as its growing middle class flexes its muscles. Despite this, the probability of an Indian firm making an appearance among the largest firms of the world is low given the unusually small size of Indian companies today. Europe: Distinct from the Asian countries listed above, Germany could benefit from the industrial boom in the US given its capabilities when it comes to high-end manufacturing (Chart 24). Even as we believe that oil faces a bleak future on a structural basis, if a commodities supercycle were to take hold over the next decade, then the UK and France could improve their presence in global equity benchmarks given that Europe is home to some large firms in the energy sector. A commodities supercycle will also end up benefiting China and the US, since some large energy producers are also located in these countries. Chart 24Korea, Japan, And Germany Have An Edge In Manufacturing, While Taiwan, Japan, And China Have An Edge In Semiconductors

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

America's Lead On Mega-Sized Companies: Is A Peak Nigh?

Appendix The Methodology The starting point for most country-level economic analyses tends to be a country’s nominal GDP. But as market economists we realized that some key advantages could be unlocked by focusing on ‘revenues’ generated by the listed universe of a country. These advantages include: Investment Focus: As compared to nominal GDP which ends up picking up signals about the health of the listed ‘and’ unlisted firms in any country, focusing on listed firms’ revenues allows us to home-in on the health of the listed space. This is a valuable merit since the listed space is what public equity investors can buy into. For example, India is the fifth largest economy of the world and is also one of the fastest growing economies globally. But India is also characterized by a listed space where the largest companies have revenues of only around $100 billion. This makes India less investable than countries like Taiwan or South Korea that have far smaller nominal GDPs as compared to India but are home to firms with revenue of around $200 billion. Taking note of this difference - between the size of a country’s nominal GDP and the size of investable firms in a country - is key for our clients. Focus On Cause, Not Effect: It is fashionable today in the financial press to focus on the daily changes in market capitalization of assets (and non-assets too). But it is critical to note that the market cap of a stock or the price of a security is a dependent variable. Revenue, on the other hand, is a key independent variable that influences prices. So, a focus on forecasting movement in revenues of companies in a country ten years down the line, can be a more fruitful exercise for strategic investors. Steady And Stable: Revenue generated by a firm, is also a superior measure as compared to the market capitalization of a firm because the latter can be volatile. Whilst it could be argued that earnings of a company as a variable also offer stability and influence prices, earnings suffer from one drawback which is that it is a function of revenues as well as costs. Revenues of companies on the other hand have a direct theoretical link to the nominal GDP of a country. So, to rephrase a popular adage - market cap is vanity, nominal GDP is sanity, but revenue is king. This is the reason why in this Special Report, we analyze investment opportunities through the lens of revenues generated by listed firms in some of the largest economies of the world. We do so by focusing on the constituents of MSCI Country Indices (Equity) for major world economies in 2021. Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Footnotes 1 Based on MSCI ACWI data for 2021. 2 Kiran Stacey, “Washington vs Big Tech: Lina Khan’s battle to transform US antitrust,” ft.com, August 2021. 3 Kathy Fogel, Randall Morck, and Bernard Yeung, “Big Business Stability And Economic Growth: Is What’s Good For General Motors Good For US?”, NBER Working Paper No. 12394, nber.org, July 2006.

Preliminary estimates indicate that real US GDP growth declined by an annualized 0.9% in Q2, marking the second consecutive decline and against expectations it would return to positive growth. Private domestic business investment was the largest negative…

The Q2 GDP contraction is fueling fears that the US economy is in recession (see The Numbers). Regardless of whether this is indeed the case – i.e. whether the advance release will be revised and, whether the NBER classifies it as one – there are two key…

Executive Summary If a loss of wealth persists for a year or more, it hurts the economy. The recent $40 trillion slump in global financial wealth is larger than that suffered in the pandemic of 2020, the global financial crisis of 2008, and the dot com bust of 2000-01. Partly countering this slump in global financial wealth is a $20 trillion uplift in global real estate wealth. However, Chinese home prices are already stagnating. And the recent disappearance of US and European homebuyers combined with a flood of home-sellers warns that US and European home prices will cool over the next 6 months. With the loss of wealth likely to persist, it will amplify a global growth slowdown already in train, aided and abetted by central banks that are willing to enter recession to slay inflation. The optimal asset allocation over the next 6-12 months is: overweight bonds, neutral stocks, and underweight commodities. A variation on this theme is: overweight conventional bonds and stocks versus inflation-protected bonds and commodities. Fractal trading watchlist: US telecoms versus utilities, and copper. We Have Just Suffered The Worst Loss Of Financial Wealth In A Generation

The World Is $20 Trillion Poorer. Why That Matters

The World Is $20 Trillion Poorer. Why That Matters

Bottom Line: On a 6-12 month horizon, overweight bonds, neutral stocks, and underweight commodities. Feature Since the end of last year, the world has lost $40 trillion of financial wealth, evenly split between the crashes in stocks and bonds (Chart I-1). The slump in financial wealth, both in absolute and proportionate terms, is the worst suffered in a generation, larger than that in the pandemic of 2020, the global financial crisis of 2008, and the dot com bust of 2000-01.1 Chart I-1Global Stocks And Global Bonds Have Both Slumped By $20 Trillion

Global Stocks And Global Bonds Have Both Slumped By $20 Trillion

Global Stocks And Global Bonds Have Both Slumped By $20 Trillion

Partly countering this $40 trillion slump in global financial wealth is a $20 trillion uplift in global real estate wealth. But in total, the world is still $20 trillion ‘asset poorer’ than at the end of last year. Given that global GDP is around $100 trillion, we can say that we are asset poorer, on average, by about one fifth of our annual income. Does this loss of wealth matter? A Loss Of Wealth Matters If It Persists For A Year Or More Some argue that we shouldn’t worry about the recent slump in our wealth, because we are still wealthier than we were, say, at the start of the pandemic (Chart I-2). Yet this is a facile argument. Whatever loss of wealth we suffer, there is always some point in the past against which we are richer! Chart I-2We Have Just Suffered The Worst Loss Of Financial Wealth In A Generation

We Have Just Suffered The Worst Loss Of Financial Wealth In A Generation

We Have Just Suffered The Worst Loss Of Financial Wealth In A Generation

Another argument is that people do not care about a short-lived dip in their wealth. This argument has more truth to it. For example, in the extreme event of a flash crash, an asset price can drop to zero and then bounce back in the blink of an eyelid. In this case, most people would be oblivious, or unconcerned, by this momentary collapse in their wealth. But people do care if the slump in their wealth becomes more prolonged. How long is prolonged? The answer is, if the slump persists for a year or more. Why a year? Because that is the timeframe over which governments, firms, and households make their income and spending plans. Governments and firms do this formally in their annual budgets that set tax rates, wages, bonuses, and investment spending. Households do it informally, because their wages, bonuses, and taxes – and therefore disposable incomes – also adjust on an annual basis. Into this yearly spending plan will also come any change in wealth experienced over the previous year. For example, firms often do this formally by converting an asset write-down to a deduction from profits, which will then impact the firm’s future spending. This illustrates that what impacts your spending is not the level of your wealth, but the yearly change in your wealth. Spending Is Impacted By The Change In Wealth The intellectual battle here is between Economics and Psychology. The economics textbooks insist that it is the level of your wealth that impacts your spending, whereas the psychology and behavioural finance textbooks insist that it is the change in your wealth that impacts your spending. (Chart I-3and Chart I-4). In my view, the psychologists and behavioural finance guys have nailed this better than the economists, through a theory known as Mental Accounting Bias. Chart I-3The Change And Impulse Of Stock Market Wealth Are Both Negative

The Change And Impulse Of Stock Market Wealth Are Both Negative

The Change And Impulse Of Stock Market Wealth Are Both Negative

Chart I-4The Change And Impulse Of Bond Market Wealth Are Both Negative

The Change And Impulse Of Bond Market Wealth Are Both Negative

The Change And Impulse Of Bond Market Wealth Are Both Negative

Nobel Laureate psychologist Daniel Kahneman points out that we categorise our money into different accounts, which are sometimes physical, sometimes only mental – and that there is a clear hierarchy in our willingness to spend these ‘mental accounts’. Put simply, we are willing to spend our income mental account, but we are much less willing to spend our wealth mental account. Still, wealth can generate income through interest payments and dividends, which we are willing to spend. Clearly, the level of income generated will correlate with the amount of wealth – $10 million of wealth will likely generate much more income than $1 million of wealth. So, economists get the impression that it is the level of wealth that impacts spending, but the truth is that it is the income generated by the wealth that impacts spending. We are willing to spend our income ‘mental account’, but we are much less willing to spend our wealth ‘mental account’. What about someone like Amazon founder Jeff Bezos who has immense wealth but seemingly negligible income – Mr. Bezos receives only a token salary, and his huge holding of Amazon shares pays no dividend – how then can we explain his largesse? The answer is that Mr. Bezos’ immense wealth generates tens of billions in trading income. So again, it is his income that is driving his spending. Wealth also generates an ‘income substitute’ via capital gains. For example, you should be indifferent between a $100 bond giving you $2 of income, or a $98 zero-coupon bond maturing in one year at $100, giving you $2 of capital gain. In this case the capital gain is simply an income substitute and fully transferred into the spending mental account. Nowhere is this truer than in China, where the straight-line appreciation in house prices through several decades has allowed homeowners to regard a reliable capital gain as an income substitute (Chart I-5). Which justifies rental yields on Chinese housing that are the lowest in the world and lower even than the yield on risk-free cash. In other words, which justifies a stratospheric valuation for Chinese real estate.

Image

Usually though, we tend to transfer only a proportion of our capital gains or losses into our spending mental account. As described previously, a firm will do this formally by transferring an asset write-down into the income statement. And households will do it informally by transferring some proportion of their yearly change in wealth into their spending mental account. The important conclusion is that spending is impacted by the yearly change in wealth. Meaning that spending growth is impacted by the yearly change in the yearly change in wealth, known as the wealth (1-year) impulse, where a negative impulse implies negative growth. Cracks Appearing In The Housing Market Given the recent slump in financial wealth, the global financial wealth impulse is in deeply negative territory. Yet by far the largest part of our wealth comprises housing, meaning the value of our homes2 (Chart I-6). In China, the recent stagnation of house prices means that the housing wealth impulse has turned negative. Elsewhere in the world though, the recent boom in house prices means that the housing wealth impulse is still positive, meaning a tailwind – albeit a rapidly fading tailwind – to spending (Chart I-7 and Chart I-8). Chart I-6Housing Comprises By Far The Largest Part Of Our Wealth

Housing Comprises By Far The Largest Part Of Our Wealth

Housing Comprises By Far The Largest Part Of Our Wealth

Chart I-7Chinese House Prices Have Stagnated, US House Prices Have Surged

The World Is $20 Trillion Poorer. Why That Matters

The World Is $20 Trillion Poorer. Why That Matters

Chart I-8The Chinese Housing Wealth Impulse Is Negative, The US Housing Wealth Impulse Is Fading

The Chinese Housing Wealth Impulse Is Negative, The US Housing Wealth Impulse Is Fading

The Chinese Housing Wealth Impulse Is Negative, The US Housing Wealth Impulse Is Fading

In China, the recent stagnation of house prices means that the housing wealth impulse has turned negative. Still, as we explained in The Global Housing Boom Is Over, As Buying Becomes More Expensive Than Renting, the disappearance of homebuyers combined with a flood of home-sellers is a tried and tested indicator that US and European home prices will cool over the next 6 months. US new home prices have already suffered a significant decline in June (Chart I-9). Some of this is because US homebuilders are building smaller and less expensive homes. Nevertheless, it seems highly likely that the non-China housing wealth impulse will also turn negative later this year. Chart I-9US New Home Prices Fell Sharply In June

US New Home Prices Fell Sharply In June

US New Home Prices Fell Sharply In June

To be clear, the wealth impulse is just one driver of spending growth. Nevertheless, it does have the potential to amplify the growth cycle in either direction. With global growth clearly slowing, and central banks willing to enter recession to slay inflation, the rapidly fading global wealth impulse will amplify the slowdown. Therefore, the optimal asset allocation over the next 6-12 months is: Overweight bonds. Neutral stocks. Underweight commodities. A variation on this theme is: Overweight conventional bonds and stocks versus inflation-protected bonds and commodities. Fractal Trading Watchlist After a 35 percent decline since March, copper has hit a resistance point on its short-term fractal structure, from which it could experience a countertrend move. Hence, we are adding copper to our watchlist. Of note also, the underperformance of US telecoms versus utilities has reached the point of fragility on its 260-day fractal structure that has signalled previous major turning points in 2012, 2014, and 2017 (Chart I-10). Hence, the recommended trade is long US telecoms versus utilities, setting a profit target and symmetrical stop-loss at 8 percent. Chart I-10US Telecoms Versus Utilities Are At A Potential Turnaround

US Telecoms Versus Utilities Are At A Potential Turnaround

US Telecoms Versus Utilities Are At A Potential Turnaround

Fractal Trading Watchlist: New Additions Copper’s Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 The value of global equities has dropped by $20tn to $80tn, the value of global bonds by $20tn to around $100tn, while the value of global real estate has increased by $20tn to an estimated $370tn. 2 Strictly speaking, housing wealth should be measured net of the mortgage debt that is owed on our homes. But as the wealth impulse is a change of a change, and mortgage debt changes very slowly, it does not matter whether we calculate the impulse from gross or net housing wealth. Chart 1CNY/USD At A Potential Turning Point

CNY/USD At A Potential Turning Point

CNY/USD At A Potential Turning Point

Chart 2Copper's Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Copper's Selloff Has Hit Short-Term Resistance

Chart 3US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

Chart 4CAD/SEK Is Reversing

CAD/SEK Is Reversing

CAD/SEK Is Reversing

Chart 5Financials Versus Industrials Has Reversed

Financials Versus Industrials Has Reversed

Financials Versus Industrials Has Reversed

Chart 6The Outperformance Of Resources Versus Biotech Has Ended

The Outperformance Of Resources Versus Biotech Has Ended

The Outperformance Of Resources Versus Biotech Has Ended

Chart 7The Outperformance Of Resources Versus Healthcare Has Ended

The Outperformance Of Resources Versus Healthcare Has Ended

The Outperformance Of Resources Versus Healthcare Has Ended

Chart 8FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

Chart 9Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Chart 10The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

Chart 11The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

Chart 12Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Chart 13German Telecom Outperformance Has Started To Reverse

German Telecom Outperformance Has Started To Reverse

German Telecom Outperformance Has Started To Reverse

Chart 14Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Chart 15ETH Is Approaching A Possible Capitulation

ETH Is Approaching A Possible Capitulation

ETH Is Approaching A Possible Capitulation

Chart 16The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

The Strong Trend In The 18-Month-Out US Interest Rate Future Has Ended

Chart 17The Strong Downtrend In The 3 Year T-Bond Has Ended

The Strong Downtrend In The 3 Year T-Bond Has Ended

The Strong Downtrend In The 3 Year T-Bond Has Ended

Chart 18A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 19Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 20Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Chart 21Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Chart 22Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Chart 23USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

Chart 24The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

Chart 25A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 26GBP/USD At A Potential Turning Point

GBP/USD At A Potential Turning Point

GBP/USD At A Potential Turning Point

Chart 27US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

Chart 28The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

Fractal Trading System Fractal Trades

The World Is $20 Trillion Poorer. Why That Matters

The World Is $20 Trillion Poorer. Why That Matters

The World Is $20 Trillion Poorer. Why That Matters

The World Is $20 Trillion Poorer. Why That Matters

6-12 Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

US services spending collapsed during the COVID-19 pandemic, and remains significantly below the level that would have prevailed had the pandemic not occurred. This raises the question of whether services consumption will ever return to “normal.” In this report, we address this question by examining the weakest components of services spending, with an eye towards any evidence indicating that this weakness is permanent. A category analysis of services spending highlights that the spending gap currently exists due to a combination of work-from-home trends and evidence of lasting aversion to COVID-19. The latter is unlikely to be permanent, and the former will be partially or fully offset by a permanent increase in substitutable goods spending. In a non-recessionary scenario, our analysis suggests that the US services spending gap will continue to close, which will provide support for overall consumption as goods spending slows in response to weak real wage growth and higher interest rates. The COVID-19 pandemic has been enormously disruptive, socially as well as economically. In the US, a massive shift from services to goods spending represents one of the most significant economic disruptions caused by the pandemic, which persists even today. Chart II-1The Pandemic Caused An Extreme Shift In Spending From Services To Goods

The Pandemic Caused An Extreme Shift In Spending From Services To Goods

The Pandemic Caused An Extreme Shift In Spending From Services To Goods

Chart II-1 presents our best estimate of the real goods and services spending gaps relative to potential GDP, which illustrates how extreme the shift from services to goods has been. The real goods spending gap exploded during the pandemic to a level that had not been seen since the early-1950s, and services spending collapsed in an unprecedented fashion and remains at a level that is lower than at any other point over the past seven decades (aside from the worst of the pandemic itself). Chart II-2 highlights that the overall output and household consumption gaps have not yet turned positive, despite an extremely strong labor market. This underscores that weak services spending is playing a role in depressing consumption, and thus overall economic activity. Chart II-2Weak Services Spending Is Playing A Role In Depressing Consumption

Weak Services Spending Is Playing A Role In Depressing Consumption

Weak Services Spending Is Playing A Role In Depressing Consumption

This persistent weakness in services spending raises the question of whether services consumption will ever return to “normal,” defined as the level of spending that would have likely prevailed had the pandemic never occurred. In this report we address this question by examining the weakest components of services spending, with an eye towards any evidence indicating that this weakness is permanent. We conclude that the services spending gap currently exists due to a combination of WFH trends and evidence of lasting aversion to COVID-19. While the effect of the former may be permanent, we do not believe that the effect of the latter will be. And, in cases where certain categories of services spending are likely to be permanently lower, at least some of this decline in spending is likely to be partially or fully offset by a permanent increase in substitutable goods spending. In a non-recessionary scenario, our analysis suggests that the US services spending gap will continue to close, which will provide support for overall consumption as goods spending slows in response to weak real wage growth and higher interest rates. The Pandemic, Remote Work, And Services Spending During the very early phase of the pandemic, COVID-19 was spreading rapidly in industrialized economies. Following recommended or mandatory stay at home orders from governments in many countries, most office-based businesses rapidly shifted to work-from-home (WFH) arrangements as an emergency response. This, in conjunction with forced closures of “close contact” businesses such as restaurants, entertainment, and travel caused US services spending to collapse. However, by the summer of 2021, many of these pandemic control measures had been significantly eased or lifted in the US. In addition, several national US surveys found many office workers preferred the flexibility afforded by WFH arrangements. Many employers, correspondingly, found that the productivity of their employees did not suffer while working from home, or that it even improved. These findings led many in the business community to conclude that WFH policies are not, in fact, emergency measures that will ultimately be reversed and instead reflect the “new normal” for work. While this “new normal” is still in the process of being defined, it seems fairly clear that some form of hybrid work arrangements will be permanent for many businesses. Chart II-3 presents the Kastle Systems Back to Work Barometer, which reflects keycard swipes in office buildings in the top 10 US cities. The chart highlights that urban office building activity has recovered to less than half of its pre-pandemic level, and that there has been no evidence of a continued uptrend over the past 3 months. Chart II-4 reinforces this point by highlighting that public transit use in major US cities has lagged the recovery in air travel, and also has not substantially changed over the past few months. Chart II-3Urban Office Building Activity Has Recovered To Less Than Half Of Its Pre-Pandemic Level

Urban Office Building Activity Has Recovered To Less Than Half Of Its Pre-Pandemic Level

Urban Office Building Activity Has Recovered To Less Than Half Of Its Pre-Pandemic Level

Chart II-4Urban Public Transit Use Has Lagged The Recovery In Air Travel

Urban Public Transit Use Has Lagged The Recovery In Air Travel

Urban Public Transit Use Has Lagged The Recovery In Air Travel

This underscores that investors have a basis to question whether at least some US services spending may be permanently impaired by the pandemic, as was the case for overall output for several years following the 2008/2009 global financial crisis. To answer this question, we present a detailed review of the most lagging categories of US services spending on pages 8-15, focused on whether WFH trends and/or activity in central business districts can plausibly explain the gap in spending in each category. The US Services Spending Gap: Key Observations And Conclusions As discussed in greater detail below, we make the following observations about the US services spending gap: Among the seven major categories of US services spending, health care accounts for the largest portion of the services spending gap. Reduced health care spending has little to do with work from home trends, and more to do with an aversion to contracting the disease in a healthcare environment and the reluctance to place elderly relatives in nursing homes given the higher risk that COVID presents to those who are older. Some recreation services spending has been impacted by WFH trends and thus may be permanent, but a lingering fear of crowded indoor spaces and still-recovering international tourism appear to be more important drivers of the recreation services spending gap. Some portion of reduced transportation services spending may be permanent (either in whole or in part), as the spending gap in road transportation seems strongly connected to WFH trends. But the sizeable and impactful decline in real spending on motor vehicle leasing is likely to recover as motor vehicle production improves over the coming year, suggesting that transportation services spending will continue to improve over the coming year relative to its pre-pandemic trend even if a spending gap in this category of services spending is permanent or long-lasting. Personal care and clothing services is mostly responsible for the spending gap in other services, and clear WFH effects do suggest that a reduction in spending in this category may be permanent. However, these categories are relatively small, and in some cases have been partially offset by what is likely to be a permanently positive spending gap on equivalent goods. The takeaway for investors is that the services spending gap currently exists due to a combination of WFH trends and evidence of lasting aversion to COVID-19. While some investors may interpret these observations as suggesting that the gap will act as a permanent or long-lasting drag on consumer spending, we disagree for two important reasons. First, we agree that some form of hybrid work arrangements will be permanent for many businesses, and that a spending gap may be permanent or long-lasting for spending categories most closely tied to WFH effects. But this also suggests that the goods-equivalent spending that has occurred as a result of this decline in services spending will also be permanent. In other words, some of the drag that permanent WFH effects will have on overall consumer spending will be offset by a permanent increase in certain categories of goods spending. Chart II-5Some Of The Permanent Drag On Services Spending Will Be Offset By Permanently Higher Goods Spending

Some Of The Permanent Drag On Services Spending Will Be Offset By Permanently Higher Goods Spending

Some Of The Permanent Drag On Services Spending Will Be Offset By Permanently Higher Goods Spending

Chart II-5 highlights the sum of spending for two pairs of clearly substitutable services/goods categories: miscellaneous personal care services plus personal care products, and sporting equipment, supplies, guns, and ammunition plus membership clubs and participant sports centers. The chart highlights that the sum of these four categories is currently above its pre-pandemic trend, highlighting that permanently lower spending in some services categories affected by WFH trends will likely be offset by permanently higher spending in some goods categories. Second, we doubt that a strong aversion to a COVID-19 infection will be permanent, as the endemicity of the disease has yet to be recognized by the public and normalized by political leaders and health professionals. This is especially true given that the availability and awareness of Pfizer’s Paxlovid antiviral therapy is still in its early stages in the US, and remains severely restricted in other developed economies and (for now) essentially unavailable in the emerging world. As an additional point concerning the lingering societal fear of COVID-19, estimates for the likely annual disease burden from “endemic COVID” are now coming into focus. In a recent New York Times opinion piece, the author cited forecasts from a number of medical professionals that endemic COVID-19 will likely infect roughly half of the US population per year, and will kill on the order of 100,000-250,000 Americans annually.1 That compares with roughly 50,000 fatalities over the course of a year from the worst flu season experienced over the past decade, implying that COVID-19 will end up being between 2-5 times as bad over the longer term as worst-case flu. If the disease burden of endemic COVID-19 ends up being on the higher end of that estimate, then it is likely that an aversion to crowded spaces and shared human settings will be permanent. But we suspect that the eventually-widespread availability of Paxlovid – and other treatment options that have yet to be developed – makes it more likely that annual fatalities will be on the lower end of that range. Chart II-6“Endemic COVID” Will Still Be A Significant Killer, But It Will Not Likely Cause A Permanent Fear Of Crowded Spaces

August 2022

August 2022

While tragic, a disease with a fatality rate of 30 per 100,000 people (equivalent to 100,000 US deaths per year) will rank behind accidents, chronic lower respiratory diseases (such as bronchitis, emphysema, and asthma), stroke, and just in line with Alzheimer’s disease as a leading cause of death (Chart II-6). It is certainly unwelcome that a new leading cause of death has emerged. But given that COVID-19 will never go away, we doubt that this will be enough to cause a permanent change in public behavior, suggesting that US services spending will return to normal over time. To the extent that some services spending declines are permanent, we expect that to be partially or fully offset by a permanent increase in substitutable goods spending. Investment Conclusions As we discussed in Section 1 of our report, the risk of a US recession is quite elevated. In a non-recessionary scenario, our analysis suggests that the US services spending gap will continue to close, which will provide support for overall consumption as goods spending slows in response to weak real wage growth and higher interest rates. Chart II-7In A Nonrecessionary Scenario, Excess Savings Will Support Services Spending

In A Nonrecessionary Scenario, Excess Savings Will Support Services Spending

In A Nonrecessionary Scenario, Excess Savings Will Support Services Spending

Chart II-7 highlights that the excess savings that have accumulated since the onset of the pandemic – which can be deployed to support spending – have accrued heavily to upper income earners, who are typically responsible for a significant amount of services spending. While it is true that upper income earners have also suffered a significant wealth shock from the combined effect of falling stock and bond prices, we strongly suspect that excess savings and the transition to endemic COVID-19 will support services spending and cause it to move toward the level that would have prevailed had the pandemic not occurred. In a recessionary scenario, we doubt that services spending would fall significantly, given that it is still extraordinarily depressed relative to history. However, some cyclical categories of services spending would decline, and Chart II-1 highlighted that services spending does tend to decline during recessions. The key point for investors is that changes in services spending would not be large enough to cushion a meaningful decline in goods spending were a recession to emerge. While the emergence of a US recession is not yet a foregone conclusion, the risk that it will occur is an important reason supporting our a neutral asset allocation stance. As noted in Section 1 of our report, further signs of an impending recession would cause us to recommend that investors underweight risky assets over the coming 6-12 months. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Gabriel Di Lullo Research Associate Overall Household Consumption Expenditures for Services Household consumption expenditures for services is composed of seven categories of services spending: Housing and Utilities, Health Care, Transportation Services, Recreation Services, Food Services and Accommodations, Financial Services and Insurance, and Other Services. In order to gauge to what degree services spending is likely to be permanently impaired by the COVID-19 pandemic, we estimate the “services spending gap” for each of these seven categories based on the pre-pandemic trend of overall services spending and the pre-pandemic weight of each category (Chart II-8). Chart II-8The Services Spending Gap Is Fairly Broad-Based

August 2022

August 2022

Spending fell in all seven services categories during the early phase of the COVID-19 pandemic, but the pace of their respective recoveries has been varied. Spending in many of these sectors has not yet fully recovered relative to its pre-pandemic trend (Charts II-9 and 10), contributing to a spending gap of more than $350 billion real dollars.2 Chart II-8 presents a breakdown of this spending gap by category, and we analyze the drivers of each of these gaps by examining subcategories of services spending on pages 8-15. Our subcategory analysis focuses on areas of services spending that are well below their pre-pandemic level, rather than relative to the hypothetical level of spending that would have prevailed had the pandemic not occurred. This is due to BEA data limitations that prevent us from accurately attributing category spending gaps to subcategories in real terms. Charts II-8-10 underscore that the services spending gap is very broad-based. However, four categories stand out as being particularly impactful: health care, recreation services, transportation services and other services. We discuss the causes of the spending gap in these four categories below, with the goal of determining whether they will likely abate as the pandemic continues to recede, or whether they are likely to be permanent. Chart II-9Four Categories Of Services Spending Stand Out…

Four categories Of Services Spending Stand Out...

Four categories Of Services Spending Stand Out...

Chart II-10…As Being Particularly Impactful Drivers Of The Services Spending Gap

...As Being Particularly Impactful Drivers Of The Services Spending Gap

...As Being Particularly Impactful Drivers Of The Services Spending Gap

Health Care Real US personal consumption on health care services is currently $126 billion below our estimate of its pre-pandemic trend, and is currently just below its pre-pandemic level (Chart II-11). “Missing” health care spending accounts for the largest share of the overall spending gap for household consumption expenditures for services. Chart II-11“Missing” Health Care Spending Accounts For A Large Part Of The Overall Services Spending Gap

August 2022

August 2022

Health care spending initially experienced a V-shaped recovery following the onset of the pandemic, but the pace of recovery has since slowed. The sectors displaying the most significant deviations from their pre-pandemic levels are physician services, dental services, and nursing home spending (Chart II-12). The gap in spending on hospital, physician, and dental services is clearly related to the COVID-19 pandemic, in the sense that some households likely fear contracting the disease in a healthcare setting (especially given the invasive nature of dental treatments). It is also possible that households have been visiting doctor and dentist offices less frequently due to work-from-home policies, in cases where these offices were located in or adjacent to central business districts. Nursing home spending is very much the outlier in the health care sub-sectors, in the sense that its recovery has been more U-shaped than V-shaped. As the pandemic placed the elderly at great risk, we suspect that many family members decided to remove them from nursing homes (or postpone moving them into a nursing home), due to the concern that a communal living environment significantly increased the risk of COVID exposure. Bottom Line: We strongly doubt that the gap in healthcare services spending is permanent. The increasing availability of Paxlovid should help physician services, dental services, and nursing home spending recover, although it is possible that nursing home spending will be the most lagging of the three. Still, we expect that the health care services spending gap will close meaningfully over the coming year if a US recession is avoided (and possibly even if a recession does occur). Chart II-12Some Households Likely Fear Contracting COVID In A Healthcare Setting

Some Households Likely Fear Contracting COVID In A Healthcare Setting

Some Households Likely Fear Contracting COVID In A Healthcare Setting

Chart II-13Lingering Fears Of Crowded Indoor Spaces And Still Weak Tourism Explain Weak Recreation Services Spending

Lingering Fears Of Crowded Indoor Spaces And Still Weak Tourism Explain Weak Recreation Services Spending

Lingering Fears Of Crowded Indoor Spaces And Still Weak Tourism Explain Weak Recreation Services Spending

Recreation Services Real spending on recreation services is currently $75 billion below its pre-pandemic trend, and remains well below its pre-pandemic level (Chart II-14). Despite only accounting for 6% of household consumption expenditure for services, the sharp decline in spending in certain sub-sectors of recreation services has been large enough to significantly contribute to the overall services spending gap. Chart II-14The Recreation Services Spending Gap: Concerts, Amusement Parks, Movies, And Gyms

August 2022

August 2022