United States

According to BCA Research’s US Investment Strategy service, if the recession is further away than moves in the bond, equity and foreign exchange markets imply, risk assets are poised to rebound. The current rate hike campaign’s real-time impact on…

Executive Summary Surge In Yields Tanked Equities

Surge In Yields Tanked Equities

Surge In Yields Tanked Equities

In this week’s report, we conduct a post-mortem analysis of the past week’s market panic and probe the effect of the new developments on US equities. Inflation is embedded. US equities won’t find a bottom until inflation turns decisively. The Fed will continue to tighten monetary policy, and rates will rise until inflation rolls over. The Fed “put” is also no longer at play as the Fed has signaled that it cares far more about combating inflation than about the performance of the stock market. Economic growth is decelerating and is already surprising on the downside. Watch rates. With rates stable, the S&P 500 performance will be a function of earnings growth. With rates rising, the multiple will contract and will exacerbate the damage done by the earnings recession. Bottom Line: The S&P 500 is unlikely to find a bottom until inflation turns and monetary conditions stabilize. In addition, economic growth is slowing and an earnings recession is likely. We believe US equities will follow a “fat and down” trajectory in light of the recent developments. We recommend that investors “not be heroes” and keep sector allocation close to the benchmark. Overweight defensives vs. cyclicals. Feature The May CPI reading showed that despite the Fed’s “heroic actions,” inflation has not yet peaked—a data point that has shocked both the market and Fed officials. In an unprecedented move, the Fed, which prides itself on its transparent communication style and its ability to move the market by guiding its expectations, leaked its intention to raise rates by 75 bps to the WSJ despite the communications blackout period. Since last Friday, equity markets around the globe have been in turmoil, with the S&P 500 falling 8%. The NASDAQ is down 7%. Is this just a leg down of the “Fat and Flat” market we have called for with a rebound waiting in the wings, or is there a structural change in the inflationary backdrop and a relentless bear market set to continue? To answer these questions, we will revisit our macroeconomic calls to better understand what expectations need to be adapted to the new reality and what we should expect for US equities over the next three to six months. Sneak Preview: US equities are likely to fall further as monetary conditions continue to tighten and earnings growth is set to contract. We believe that equities will trade in a wide “channel” with multiple rallies and pullbacks, but the general direction is down until inflation turns decisively, and fears of recession dissipate. Why Did Equities Tank? The last few days in the markets were simply brutal. What were investors (and the Fed) panicking about? Here is our hunch: Inflation is not abating, while growth is slowing. Are we in the early innings of stagflation? We believe that stagflation is certainly a high risk. The Fed’s aggressive tightening of monetary conditions is bound to further slow economic growth and taper demand. However, the Fed has no means of controlling the supply side of the equation such as prices of food or energy, which surge because of constrained supply. Will monetary tightening be even more aggressive than expected? Will 75-bps rate rises become the Fed’s new normal? During the press conference, Chairman Powell reassured the market that a 75-bps rate hike is an extraordinary measure. However, both 50-bps and 75-bps rate hikes will be on the table in July. Are the markets on the cusp of a new monetary regime, and is the easy money of the past 12 years a thing of the past? The Fed’s balance sheet has increased from $2 trillion in 2009 to an unprecedented $9 trillion in 2022. This ultra-easy monetary policy has lifted asset values both in private and public markets. The new monetary regime of liquidity being drained from the financial markets to combat inflation is bound to be a major headwind for most asset classes. We believe that it will take a while to bring inflation back to the 2% target, and easy money in the near future is no longer in the cards. It is also unlikely that such a major Fed balance sheet expansion will ever be repeated. The Fed’s tightening via both rising rates and QT will result in a dearth of liquidity in the fixed income space— a credit/counterparty “black swan” may materialize, with MBS most exposed to this risk yet again. Withdrawal of liquidity is a hit to many asset classes, from private markets to unprofitable small-cap growth companies to fixed income markets. This is a serious concern that should be monitored. Incorporating New Data Into Macro And Market Calls We have been writing about these calls for a few months—let’s revisit them here to consider what may have changed recently. Peak Inflation Is Elusive We have never quite bought the argument of transitory inflation. To us, inflation is a product of excessive demand fueled by ultra-easy fiscal and monetary policy and supply chains hobbled by the pandemic. Recently, the situation has been exacerbated by shortages of food and energy. Inflation has spread from pandemic-related goods to “stickier” service items and is broad-based (Chart 1). The wage/price spiral is relentless (Chart 2), as consumer inflation expectations are on the rise, and the job market is on fire. Chart 1Inflation Is Entrenched And Broad-based

Inflation Is Entrenched And Broad-based

Inflation Is Entrenched And Broad-based

While we always believed that it would take inflation a long time to reach the coveted 2% level, we assumed that peak inflation was behind us. Our view that inflation was going to roll over was more down to a base effect rather than the Fed’s actions. In addition, we observed that demand for goods pulled forward by the pandemic had started fading, suppressed by rising prices and negative real wage growth. The Citigroup Inflation Surprise Index had also turned (Chart 3). Chart 2Wage-Price Spiral Is Relentless

Wage-Price Spiral Is Relentless

Wage-Price Spiral Is Relentless

Chart 3Inflation Was Surprising On The Downside

Inflation Was Surprising On The Downside

Inflation Was Surprising On The Downside

It is little consolation that we were in good company when rattled by the May headline inflation reading, which came in at 8.5% year on year, and 1% higher than in April. Headline inflation was certainly affected by the price of food and energy, while core inflation was down to a higher price of shelter and goods (Chart 4). While energy is excluded from core inflation, it permeates all aspects of the economy, increasing costs of raw materials, manufacturing, and transportation, which eventually get passed through to the prices of goods and services. The same is the case with the rising wage bill. Chart 4Inflation Picked Up Because Of Prices Of Shelter And Core Goods

Adaptive Expectations: Revisiting Our Views

Adaptive Expectations: Revisiting Our Views

Importantly, what is next? It would help if US shale producers ramped up production, and the Saudis opened their oil spigots, bringing the price of energy down. Short of that, the price of oil should become a function of a slowing economy and fading demand for goods as interest rates rise (Chart 5). While the Fed has little control over food and energy prices, wage-price dynamics fall squarely in its court. The key channel through which the Fed controls inflation is by cooling the economy and reducing the demand for labor. Rising unemployment is the only way to extinguish inflation in a decisive way. Chart 5Rates Surged

Rates Surged

Rates Surged

Eventually, inflation will turn but it may be in fits and starts, and each data point will have a heavy effect on the pace of monetary tightening and the direction of equity markets, with lower inflation readings igniting rallies and higher readings triggering sell-offs. Inflation is embedded. Of course, sooner or later, it will abate but until then we expect a much more aggressive monetary policy. Monetary Conditions Have Tightened Dramatically As we summarized in our “Market Capitulation Scorecard,” one of the key conditions of an equity market bottom, and potentially, even a sustainable rebound, is stabilization in monetary conditions. We hypothesized that this could happen as the Fed tightens monetary conditions and growth slows and inflation turns, pulling down long rates. We also believed that the market focus is going to start shifting away from concerns about inflation to concerns about economic growth. Friday’s inflation reading has changed that – now investors worry about inflation and growth. Rates have initially skyrocketed, with the 10-year Treasury yield moving by 30bps points over the course of three days from 3.18 to 3.48. Real rates increased from 0.38% to 0.63%. US financial conditions have tightened sharply (Chart 6), moving to the neutral level. What’s next is the most difficult question of this report. It is likely this fast and furious move in rates has accomplished in five days what usually takes weeks. Tighter monetary policy, as it stands now, until more data comes in, is priced in. These moves capture changes in dot-plot expectations revised by the Fed, with the peak rate moving from around 3% to 4%. And, of course, that move got priced into the equity space with the S&P 500 pulling back sharply (Chart 7). Chart 6Financial Conditions Are Moving Into Restrictive Territory

Financial Conditions Are Moving Into Restrictive Territory

Financial Conditions Are Moving Into Restrictive Territory

Chart 7Surge In Yields Tanked Equities

Surge In Yields Tanked Equities

Surge In Yields Tanked Equities

The Fed will continue to tighten monetary policy and rates will rise until inflation rolls over. However, once inflation abates, long rates are likely to stabilize, signaling slower growth ahead. The Fed Won’t Come To The Rescue The Fed “put” is no longer at play as the Fed has signaled that it cares far more about combating inflation than the performance of the stock market. In fact, falling equities will play into Powell’s hand as a negative wealth effect is likely to put a lid on inflationary pressures, with wealthier Americans paying the toll. Kansas City Fed President Esther George, the only member of the FOMC that voted against a 75bps rate hike in the June meeting (she was in favor of 50 bps) said in May: “The Federal Reserve is not targeting equity markets in its battle against inflation, but that is "one of the avenues" where the impact of tighter monetary policy will be felt".1 Further, the Fed is very concerned about a recent pick-up in the long-term consumer inflation expectations (Chart 8) and will likely err on the side of caution to manage these expectations and avoid a self-fulfilling prophecy. Chart 8The Fed Is Worried About Inflation Expectations

The Fed Is Worried About Inflation Expectations

The Fed Is Worried About Inflation Expectations

Economic Growth Is Slowing Fast, Both At Home And Abroad A tighter monetary policy is designed to slow economic growth. The World Bank has downgraded global GDP growth expectations from 4.1% to 2.9%, and import volumes are declining. The Atlanta GDPNow forecast is hovering around zero (Chart 9). The Philly Fed survey has just crossed into negative territory (Chart 10). Retail sales are contracting both in nominal and real terms. According to the Citi Economic Surprise Index, economic growth is surprising on the downside (Chart 11). While the probability of a recession has picked up over the past few weeks, it is earnings growth disappointment that will have an adverse effect on equities in the near term. Chart 9Consensus Expectation Are Still Too High

Consensus Expectation Are Still Too High

Consensus Expectation Are Still Too High

Chart 10Many Signs That Economy Is Slowing Sharply

Many Signs That Economy Is Slowing Sharply

Many Signs That Economy Is Slowing Sharply

Chart 11Economic Growth Disappoints

Economic Growth Disappoints

Economic Growth Disappoints

We maintain our view that economic growth is decelerating and is already surprising on the downside. Earnings Growth Will Contract And Take The Market With It We stated in last week’s “Is An Earnings Recession In The Cards?” report that this year’s sell-off has been triggered by fears of an aggressive Fed, tighter monetary policy, and rising rates. However, the decom- position of the total return demonstrates that the pullback was all about multiple contraction, while strong earnings growth helped absorb the blow. We hypothesized that the multiple contraction phase is complete and that the next leg of the bear market will be all about growth, and earnings growth in particular (Chart 12). Hence if rates stabilize, then multiples will stay at the current level, and returns will be a function of earnings growth. However, the 10-year Treasury rate increasing from 3.18 has resulted in the S&P 500 multiple contracting from 16.7 to 15.6 over the course of just three days, while earnings growth expectations have remained mostly intact. Currently, according to our very simple model (Chart 13), a 3.5% 10-year Treasury yield corresponds to the S&P 500 forward multiple of 16.8x, which is close to where the S&P 500 stands today. If rates rise further, the forward multiple will fall. Chart 12Multiple Contraction Will Be Followed By Earnings Growth Deceleration

Multiple Contraction Will Be Followed By Earnings Growth Deceleration

Multiple Contraction Will Be Followed By Earnings Growth Deceleration

Chart 13Higher Rates Translate Into Lower Equity Multiples

Adaptive Expectations: Revisiting Our Views

Adaptive Expectations: Revisiting Our Views

Our earnings growth model predicts that earnings growth will trend towards zero over the next three months (Chart 14). Chart 14Earnings Growth Will Trend To Zero And Then Contract

Adaptive Expectations: Revisiting Our Views

Adaptive Expectations: Revisiting Our Views

Our scenario analysis matrix shows that if multiples stay stable around 17x forward earnings, while earnings contract by zero to five percent next quarter, the index will be flat to slightly down (Table 1). Broadly speaking, with a stable multiple, the market will move in line with earnings growth. If rates continue to rise and the multiple falls to 16x, going another 11% down is likely. Table 1The S&P 500 Target Scenario Analysis

Adaptive Expectations: Revisiting Our Views

Adaptive Expectations: Revisiting Our Views

Watch rates. With rates stable, the S&P 500 performance will be a function of earnings growth, and the market is likely to be range-bound. With rates rising, a multiple will contract further, and equities will fall. Investment Implications: “Fat And Down” The SPX has discounted plenty of negative news now that it is officially in bear market territory. However, we believe that the S&P 500 is not yet close to the bottom. The market is again pricing in tighter monetary policy and rising rates, which is accompanied by multiple contraction. It is hard to see equities bottoming without inflation peaking. In addition, we are predicting that the next leg of the bear market will be driven by earnings growth, which is likely to contract due to an economic slowdown both at home and abroad. As such, “fat and down” may be a more likely outcome than just “fat and flat.” Bottom Line Equities will move in a wide range over the next three to six months. However, if rates are to rise further and earnings growth is to contract, they may be trading in a downward sloping “channel,” or “fat and down.” We recommend that investors “not be heroes” and keep sector allocation close to the benchmark. Overweight defensives vs. cyclicals. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Footnotes 1 https://www.reuters.com/business/feds-george-policy-not-aimed-equity-markets-though-it-will-be-felt-there-cnbc-2022-05-19/#:~:text=WASHINGTON%2C%20May%2019%20(Reuters),Esther%20George%20said%20on%20Thursday. Recommended Allocation Recommended Allocation: Addendum

Is Earnings Recession In The Cards?

Is Earnings Recession In The Cards?

Executive Summary The Fed has sought to convince one and all of its commitment to overcome high inflation and asset markets have taken heed, tightening financial conditions at a breakneck pace. As we write, the S&P 500 is down 23% year to date, the Bloomberg Barclays Treasury index is down 10%, its sister Corporate and High Yield indexes are down 15% and 12%, respectively, and the dollar had risen by 10% at its peak last week. According to Goldman Sachs’ Financial Conditions Index, the combination has amounted to a 3-percentage-point drag on GDP. Financial markets’ reaction function vis-a-vis monetary policy actions in this tightening cycle has been markedly different than in the previous three tightening cycles. Where tighter financial conditions had previously followed tighter monetary policy with a lengthy lag, they moved ahead of the Fed this time. If the recession is further away than moves in the bond, equity and foreign exchange markets imply, or if inflation eases across the rest of the year in line with our expectations, risk assets are poised to rebound. All Together Now

All Together Now

All Together Now

Bottom Line: The FOMC appears to be on course to induce a recession in its quest to bring inflation to heel. The outlook for financial markets depends on when the recession arrives and how bad it will be, however, and we see scope for positive surprises on both counts. Feature 2022 has not been a good year for financial markets and the action over the last week and a half has made it decidedly worse. In six sessions through Thursday, the S&P 500 nosedived 11%, swooning into bear market territory and unwinding nineteen months of advances. The benchmark 10-year Treasury note’s yield needed just three sessions to back up 45 basis points, from 3.05% to 3.5%. The upheaval has not been unique to the US – inflation and decelerating growth are global phenomena and central banks around the world are scrambling to tighten monetary conditions to rein in rising consumer prices while markets agonize about the effect on growth – but the Fed has been at the center of the storm and last week’s FOMC meeting inspired more swings. This week’s report highlights the most important takeaways from the latest FOMC meeting and how financial markets and Fed policy may interact going forward. There are several factors that are at least slightly different this time. Those differences may keep volatility elevated but they do not condemn stocks and bonds to continued declines. Financial markets have made huge pre-emptive moves that may be subject to reversals as inflation data improve and/or growth holds up better than expected. Prioritizing Price Stability Times have changed. Until inflation began to stir last year, the Fed had been able to prioritize the full employment element of its dual mandate for the entire post-crisis period. Chair Powell made it abundantly clear that price stability is the FOMC’s top priority now, opening his post-meeting remarks with the “overarching message” that it has the means and the will to bring inflation back down to its target level. Living up to this commitment will not be as much fun as trying to prod the economy back to full employment, and it looks as if it will ultimately result in a recession. Following 150 basis points (bps) of hikes so far this year, the target range for the fed funds rate now stands at 1.5-1.75%, and the revised Summary of Economic Projections (SEP) indicated that the median FOMC participant expects another 175 bps of hikes across the year’s remaining four meetings, bringing the funds rate to 3.25-3.5% by year end, at the low end of the money markets’ expectations range (Chart 1). Chart 1Markets And The Fed Are On The Same Page

Markets And The Fed Are On The Same Page

Markets And The Fed Are On The Same Page

During the press conference, Powell repeatedly cited the committee’s concern over rising inflation expectations, calling out the increase in 5-year inflation expectations in the University of Michigan’s preliminary June survey as “quite eye-catching.” The series rose from 30 basis points, to 3.3%, after spending the last four months at 3% and the previous ten in a tight 2.9-3.1% range. The reading was the highest since 2008, when the average national gasoline price first rose above $4 per gallon (Chart 2). Chart 2An "Eye-Catching" Move ...

An "Eye-Catching" Move ...

An "Eye-Catching" Move ...

Threading The Needle FOMC participants’ median projections for real growth, unemployment and inflation at the end of 2022, 2023 and 2024 were benign to pollyannaish, signaling their confidence that the committee will be able to thread the needle, wrestling inflation back to target while maintaining trend growth and capping the unemployment rate at 4.1%. That would meet anyone’s definition of a soft landing, but soft landings have been notoriously elusive. It is fiendishly difficult to fine-tune a complex multi-faceted economy with central bankers’ blunt tools. Empirically, every unemployment rate increase of at least one-third of a percentage point has led to a recession (Chart 3), so even the modest one-half point rise envisioned in the SEP could bring some challenges. A closer examination of past unemployment rate increases suggests a potential way around the dour history, but it depends on reversing the decline in labor force participation that is not yet fully understood. The labor force participation rate – the share of the 16-and-over population that is either working or actively looking for a job – remains more than a percentage point below its pre-pandemic level (Chart 4). If it recovered its early 2020 share, the labor force would expand by 2.8 million people. Chart 3... That Could Put Upward Pressure On The Unemployment Rate

... That Could Put Upward Pressure On The Unemployment Rate

... That Could Put Upward Pressure On The Unemployment Rate

Chart 4The Mystery Of The Missing Workers

The Mystery Of The Missing Workers

The Mystery Of The Missing Workers

If the participation rate were restored to its pre-pandemic level, the fortified labor force would allow for payroll expansion despite the unemployment rate increases envisioned in the latest SEP, as per the population growth and household-to-establishment-survey conversion rate estimates embedded in Table 1. It is reasonable to think that the expansion could continue, or the ensuing recession would be mild, despite a rising unemployment rate if payrolls manage to keep growing. An increasing unemployment rate/increasing payrolls scenario is plausible, but we cannot deem it probable when we do not know what has impeded the participation rate’s recovery. The committee is unlikely to be of one mind on the participation rate question, but it may hold the key to reconciling the sunny projections with the observed difficulty of achieving a soft landing. Table 1A Path To A Soft Landing

One Overarching Message, Multiple Potential Outcomes

One Overarching Message, Multiple Potential Outcomes

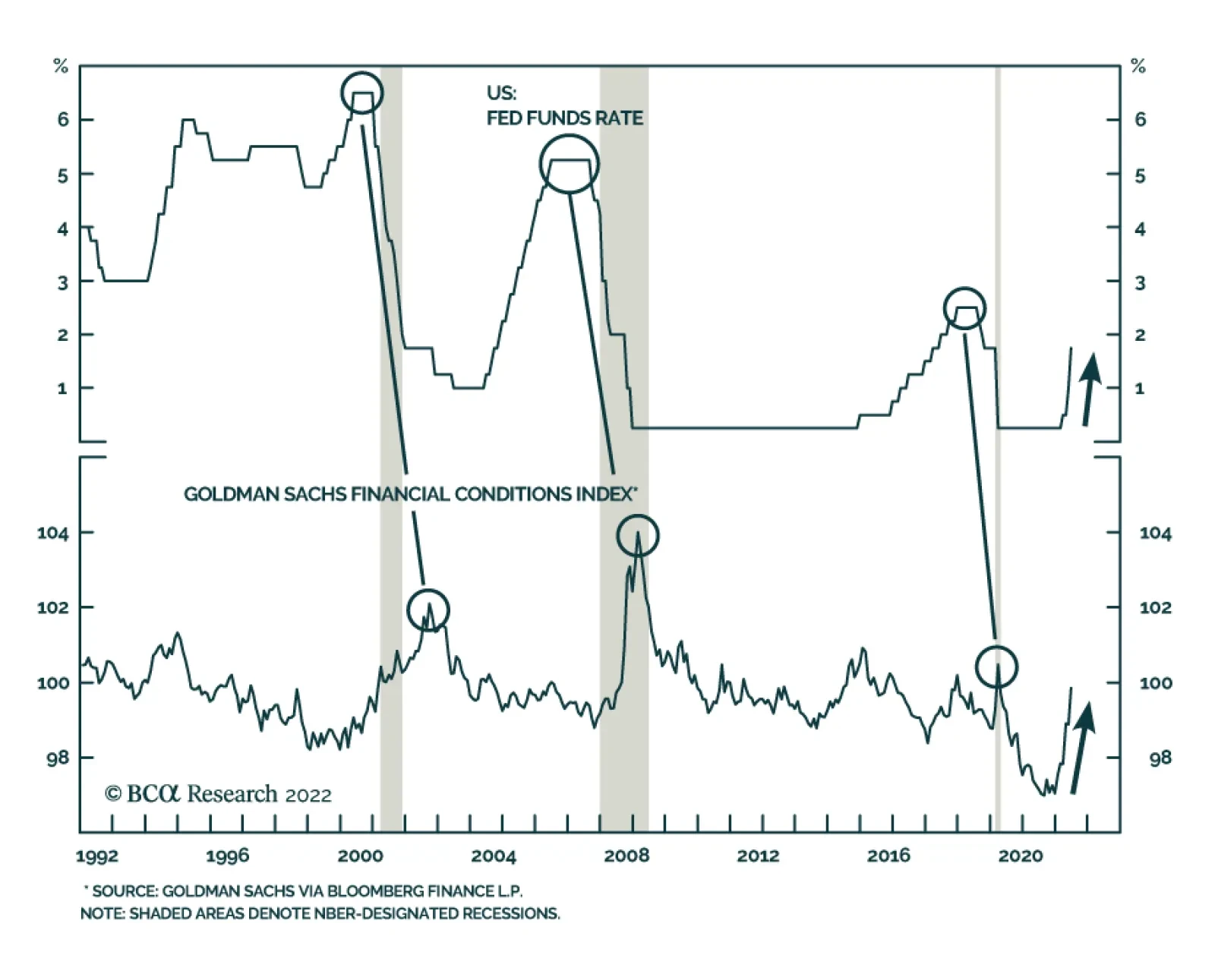

We’ll Take The Over We agree with Chair Powell and the FOMC’s assessment that solid consumer balance sheets and robust job gains have the economy on a sound footing, despite slowing growth. We do not see familiar underlying vulnerabilities that herald a reversal like an overreliance on debt, broad supply overhangs or an investment boom that has gone on too long. Inflation is the signal problem in the US and the rest of the world, and we continue to expect that it will recede in the second half as supply constraints in pandemic-squeezed segments ease and the pre-emptive backup in yields holds back some marginal demand for big-ticket items that require financing. No one knows the equilibrium fed funds rate in real time, but Powell indicated the committee thinks it’s around 3.5%, placing the year end 2022 median funds rate dot just shy of equilibrium and the median 2023 dot in modestly restrictive territory. A recession is the likely outcome of the rate hike campaign, but if the target rate doesn’t exceed the equilibrium rate until early next year, it may not begin until the middle of 2023 or early in 2024. Given that the consensus view now appears to be that a recession will begin this year if it hasn’t done so already, and financial markets have gone a long way toward pricing in its effects, we don’t see much upside to joining the bearish chorus now. We’ll take the over on the recession-by-year-end proposition. The Big Difference This Time When asked how high the funds rate has to go to arrest inflation, Powell offered the following description of how rate hikes work. “I … look at it this way: We move the policy rate that affects financial conditions, and that affects the economy. We have [more] rigorous ways to think about it, but ultimately it comes down to, ‘do we think financial conditions are in a place where they’re having the desired effect on the economy?’ And that desired effect is we’d like to see demand moderating.” Related Report US Investment StrategyInflation And Investing Two questions later, he approvingly noted how much bang the committee had already gotten for its buck to this point in the tightening campaign. “[T]his year has been a demonstration of how well [guidance] can work. With us having … done very little in the way of raising interest rates, financial conditions have tightened quite significantly through the expectations channel, as we’ve made clear what our plans are. I think that’s been … very healthy[.]” We stay away from making value judgments about policy, though we can see that a central banker would be in favor of anything that shortens the lag between policy actions and their economic effect. It is immediately obvious, however, that the current rate hike campaign’s real-time impact on financial conditions contrasts sharply with the last three decades’ campaigns (Chart 5). Every one-point change in the Goldman Sachs Financial Conditions Index (FCI) is calibrated to correspond to a one-percentage-point change in real GDP. The FOMC hiked by 175 bps ahead of the 2001 recession and the FCI eventually rose four points, peaking in October 2002, 29 months after the FOMC pushed fed funds to its terminal rate and 21 after it began cutting rates. After the 2004-6 “conundrum” campaign, when financial conditions eased despite 17 consecutive quarter-point rate hikes, the FCI tightened by five points, reaching its peak almost three years after the last hike and 18 months after the first cut. Chart 5Seize The Day

Seize The Day

Seize The Day

Chart 6Decoupling

Decoupling

Decoupling

Some of the response is a simple reflection of the about-face in the inflation backdrop. As our Chief Emerging Markets Strategist Arthur Budaghyan predicted in February 2021, Treasury yields and stock prices have flipped from several decades of positive correlation (rising stock prices offset falling bond valuations and vice versa) in a disinflationary environment to negative correlation in an inflationary environment. Now that Treasury bond, corporate bond and stock prices have been falling together, and the safe-haven dollar has risen amidst the general flight from risk, all of the FCI’s subcomponents have been reinforcing one another, making the index jumpier. More volatile financial conditions raise the probability of overshoots. To wit, has the FCI moved too far, too soon? The volcanic upward move in the 10-year Treasury yield has severed its reliable empirical link with the gold-to-commodity ratio (Chart 6, top panel) and the relative performance of cyclical and defensive equity sectors (Chart 6, bottom panel). They suggest a retracement could be in store. Projected policy rate differentials between the Fed and other currency majors’ central banks are narrowing as monetary policy makers rush to combat inflation. Gloom about growth is widespread. Any positive global growth surprise, from China regarding COVID or stimulus, from the Ukrainian theater, or from supply chain relief, could reel in the extended dollar. Investors should not lose sight of the potential that the coming recession could be mild. A 25% selloff in the S&P 500 may be nearly enough to address that outcome. As of Thursday’s close, the index’s forward four-quarter multiple was down to 15.5 from just under 22 at the start of the year – stocks were expensive, but the nearly 30% de-rating haircut has been severe. The 15.5 multiple assumes the next four quarters’ earnings grow almost 10% year-over-year, which looks ambitious. 5% growth would yield a 16.2 multiple, while no growth would price stocks at 17 times. Those multiples are not cheap, but a lot of froth has come out of the equity market. Against the gloom that has taken over financial markets, we think the next twelve months can be rewarding for investors in risk assets. We are alert to the principal ways our constructive view could be proven wrong and will change our view if it is invalidated by the evidence, but we remain overweight equities in a multi-asset portfolio over the cyclical three-to-twelve-month timeframe. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com

Listen to a short summary of this report. Executive Summary Higher Real Yields Have Weighed On Equity Valuations

Higher Real Yields Have Weighed On Equity Valuations

Higher Real Yields Have Weighed On Equity Valuations

I had the pleasure of visiting clients in Saudi Arabia, Bahrain, and Abu Dhabi last week. In contrast to the rest of the world, the mood in the Middle East was very positive. While high oil prices are helping, there is also a lot of optimism about ongoing structural reforms. Petrodollar flows are increasingly being steered towards private and public equities. EM assets stand to benefit the most. Producers in the region are trying to offset lost Russian output, but realistically, they will not be able to completely fill the gap in the near term. Today’s high energy prices have largely baked in this reality, as reflected in strongly backwardated futures curves. There was no consensus about how high oil prices would need to rise to trigger a global recession, although the number $150 per barrel got bandied about a lot. Given that most Middle Eastern currencies are pegged to the dollar, there was a heavy focus on Fed policy. Market estimates of the neutral rate in the US have increased rapidly towards our highly out-of-consensus view. Nevertheless, we continue to see modest upside for bond yields over a multi-year horizon. Over a shorter-term 6-to-12-month horizon, the direction of bond yields will be guided by the evolution of inflation. While US CPI inflation rose much more than expected in May, the details of the report were somewhat less worrying, as they continue to show significant supply-side distortions. Bottom Line: Inflation should come down during the remainder of the year, allowing the Fed to breathe a sigh of relief and stocks to recover some of their losses. A further spike in oil prices is a major risk to this view. Dear Client, Instead of our regular report next week, we will be sending you a Special Report written by Chester Ntonifor, BCA Research’s Chief Foreign Exchange Strategist, discussing the outlook for gold. We will be back the following week with the GIS Quarterly Strategy Outlook, where we will explore the major trends that are set to drive financial markets in the rest of 2022 and beyond. As always, I will hold a webcast discussing the outlook the following week, on Thursday, July 7th. Best regards, Peter Berezin Chief Global Strategist Peter in Arabia I had the pleasure of visiting clients in Saudi Arabia, Bahrain, and Abu Dhabi last week. This note summarizes my impressions and provides some commentary about recent market turmoil. The Mood in the Region is Very Positive In contrast to the rest of the world, the mood in the Middle East was upbeat. Obviously, high oil prices are a major contributor (Chart 1). Across the region, stock markets are still up for the year (Chart 2). Chart 1Oil Prices Have Shot Up

Oil Prices Have Shot Up

Oil Prices Have Shot Up

Chart 2Middle Eastern Stock Markets Are Doing Relatively Well This Year

Middle Eastern Stock Markets Are Doing Relatively Well This Year

Middle Eastern Stock Markets Are Doing Relatively Well This Year

That said, I also felt that investors were encouraged by ongoing structural reforms, especially in Saudi Arabia where the Vision 2030 program is being rolled out. The program seeks to diversify the Saudi economy away from its historic reliance on petroleum exports. A number of people I spoke with cited the Saudi sovereign wealth fund’s acquisition of a majority stake in Lucid, a California-based EV startup, as the sort of bold move that would have been unthinkable a few years ago. I first visited Riyadh in May 2011 where I controversially delivered a speech entitled “The Coming Commodity Bust” (oil was $120/bbl then and copper prices were near an all-time high). The city has changed immensely since then. The number of restaurants and entertainment venues has increased exponentially. The ban on women drivers was lifted only four years ago. In that short time, it has become a common-day occurrence. Capital Flows Into and Out of the Region are Reflecting a New Geopolitical Reality In addition to high oil prices and structural reforms, geopolitical considerations are propelling significant capital inflows into the region. The freezing of Russia’s foreign exchange reserves sent a shockwave across much of the world, with a number of other EM countries wondering if “they are next.” Ironically, the Middle East has emerged as a neutral player of sorts in this multipolar world, and hence a safer destination for capital flows. On the flipside, the region’s oil exporters appear to be acting more strategically in how they allocate their petrodollar earnings. Rather than simply parking the proceeds of oil sales in overseas US dollar bank accounts, they are investing them in ways that further their economic and political goals. One clear trend is that equity allocations to both overseas public and private markets are rising. Other emerging markets stand to benefit the most from this development, especially EMs who have assets that Middle Eastern countries deem important – assets tied to food security being a prime example. Assuming that the current level of oil prices is maintained, we estimate that non-US oil exports will rise to $2.5 trillion in 2022, up from $1.5 trillion in 2021 (Chart 3). About 40% of this windfall will flow to the Middle East. That is a big slug of cash, enough to influence the direction of equity markets. Chart 3Oil Exporters Reaping The Benefits Of High Oil Prices

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

Middle Eastern Energy Producers Will Boost Output, But Don’t Expect Any Miracles in the Short Term Russian oil production will likely fall by about 2 million bpd relative to pre-war levels over the next 12 months. To help offset the impact, OPEC has already raised production by 200,000 barrels and will almost certainly bump it up again following President Biden’s visit to the region in July (Chart 4). The decision to raise production to stave off a super spike in oil prices is not entirely altruistic. The region’s oil exporters know that excessively high oil prices could tip the global economy into recession, an outcome that would surely lead to much lower oil prices down the road. There was not much clarity on what that tipping point is, but the number $150 per barrel got bandied around a lot. Politics is also a factor. A further rise in oil prices could compel the US to make a deal with Iran, something the Saudis do not want to see happen. Still, there is a practical limit to how much more oil the Saudis and other Middle Eastern producers can bring to market in the near term. Today’s high energy prices have largely baked in this reality, as reflected in strongly backwardated futures curves (Chart 5). Chart 4Output Trends In The Major Oil Producers

Output Trends In The Major Oil Producers

Output Trends In The Major Oil Producers

Chart 5Energy Prices On Both Sides Of The Atlantic

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

Data on Saudi’s excess capacity is notoriously opaque, but I got the feeling that an extra 1-to-1.5 million bpd was the most that the Kingdom could deliver. The same constraints apply to natural gas. Qatar is investing nearly $30 billion to expand its giant North Field, which should allow gas production to rise by as much as 60%. However, it will take four years to complete the project. The share of Qatari liquefied natural gas (LNG) going to Europe has actually declined this year. About 80% of Qatar’s LNG is sold to Asian buyers under long-term contracts that cannot be easily adjusted. And even if those contracts could be rewritten, this would only bring limited benefits to Europe. For example, Germany has no terminals to accept LNG imports, although it is planning to build two. While there was plenty of sympathy to Europe’s plight in the region, there was also a sense that European governments had been cruising for a bruising by doubling down on strident anti-fossil fuel rhetoric over the past decade without doing much to end their dependence on Russian oil and gas. In that context, few in the region seemed willing to bend over backwards to help Europe. In the meantime, the US remains Europe’s best hope. US LNG shipments to Europe have tripled since last year. The US is now sending nearly three quarters of its liquefied gas to Europe. This has pushed up US natural gas prices, although they still remain a fraction of what they are in Europe. Huge Focus on the Fed Chart 6Most Of The Increase In Bond Yields Has Been In The Real Component

Most Of The Increase In Bond Yields Has Been In The Real Component

Most Of The Increase In Bond Yields Has Been In The Real Component

Most Middle Eastern currencies are pegged to the dollar, and hence the region effectively imports its monetary policy from the US. Not surprisingly, clients were very focused on the Federal Reserve. Many expressed concern about the abrupt pace of rate hikes. One of our high-conviction views is that the neutral rate of interest in the US has risen as the household deleveraging cycle has ended, fiscal policy has become structurally looser, and a growing number of baby boomers have transitioned from working (and saving) to retirement (and dissaving). The markets have rapidly priced in this view over the course of 2022. The 5-year/5-year forward Treasury yield – a proxy for the neutral rate – has increased from 1.90% at the start of the year to 3.21% at present. Most of this increase in the market’s estimate of the neutral rate has occurred in the real component. The 5-year/5-year forward TIPS yield has climbed from -0.49% to 0.84%; in contrast, the implied TIPS breakeven inflation rate has risen from only 2.24% to 2.37% (Chart 6). Implications of Higher Bond Yields on Equity Prices and the Economy Chart 7Higher Real Yields Have Weighed On Equity Valuations

Higher Real Yields Have Weighed On Equity Valuations

Higher Real Yields Have Weighed On Equity Valuations

As both theory and practice suggest, there is a strong negative correlation between real bond yields and equity valuations. Chart 7 shows that the S&P 500 forward P/E ratio has been moving broadly in line with the 5-year/5-year forward TIPS yield. The bad news is that there is still scope for bond yields to rise over the long haul. Our fair value estimate of 3.5%-to-4% for the neutral rate is about 25-to-75 basis points above current pricing. The good news is that a high neutral rate helps insulate the economy from a near-term recession. Recessions typically occur only when monetary policy turns restrictive. A few clients cited the negative Q1 GDP reading and the near-zero Q2 growth estimate in the Atlanta Fed GDPNow model as evidence that a US recession is either close at hand or has already begun (Chart 8). Chart 8Underlying US Growth Is Expected To Be Solid In Q2

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

We would push back against such an interpretation. In contrast to the -1.5% real GDP print, real Gross Domestic Income (GDI) rose by 2.1% in Q1. Conceptually, GDP and GDI should be equal, but since the two numbers are compiled in different ways, there can often be major statistical discrepancies. A simple average of the two suggests the US economy still grew in the first quarter. More importantly, real final sales to private domestic purchasers rose by 3.9% in Q1. This measure of economic activity – which strips out the often-noisy contributions from inventories, government expenditures, and net exports – is the best predictor of future GDP growth of any item in the national accounts (Table 1). Table 1A Good Sign: Real Final Sales To Private Domestic Purchasers Rose By 3.9% In Q1

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

As far as Q2 is concerned, real final sales to private domestic purchasers are tracking at 2.0% according to the Atlanta Fed model – a clear deceleration from earlier this year, but still consistent with a generally healthy economy. Growth will probably slow in the third quarter, reflecting the impact of higher gasoline prices, rising interest rates, and lower asset prices. Nevertheless, the fundamental underpinnings for the economy – low household debt, $2.2 trillion in excess savings, a dire need to boost corporate capex and homebuilding, and a strong labor market – remain in place. The odds of a recession in the next 12 months are quite low. Gauging Near-Term Inflation Dynamics A higher-than-expected neutral rate of interest implies that bond yields will probably rise from current levels over the long run. Over a shorter-term 6-to-12-month horizon, however, the direction of yields will be guided by the evolution of inflation. While the core CPI surprised on the upside in May, the details of the report were somewhat less worrying, as they continue to show significant supply-side distortions. Excluding vehicles, core goods prices rose 0.3% in May, down from a Q1 average of 0.7% (Chart 9). Recent commentary from companies such as Target suggest that goods inflation will ease further. Chart 9Goods Inflation Is Moderating, While Service Price Growth Is Elevated

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

Stripping out energy-related services, services inflation slowed slightly to 0.6% in May from 0.7% in April. A deceleration in wage growth should help keep a lid on services inflation over the coming months (Chart 10). Chart 10A Deceleration In Wage Growth Should Help Keep Services Inflation Contained

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

During his press conference, Fed Chair Powell described the rise in inflation expectations in the University of Michigan survey as “quite eye-catching.” Although long-term inflation expectations remain a fraction of what they were in the early 1980s, they did rise to the highest level in 14 years in June (Chart 11). Powell also noted that the Fed’s Index of Common Inflation Expectations has been edging higher. The Fed’s focus on ensuring that inflation expectations remain well anchored is understandable. That said, there is a strong correlation between the level of gasoline prices and inflation expectations (Chart 12). If gasoline prices come down from record high levels over the coming months, inflation expectations should drop. Chart 11Consumer Long-Term Inflation Expectations Keep Rising, But Are Still Not At Historically High Levels

Consumer Long-Term Inflation Expectations Keep Rising, But Are Still Not At Historically High Levels

Consumer Long-Term Inflation Expectations Keep Rising, But Are Still Not At Historically High Levels

Chart 12Lower Gasoline Prices Would Help Soothe Consumer Fears Over Inflation

Lower Gasoline Prices Would Help Soothe Consumer Fears Over Inflation

Lower Gasoline Prices Would Help Soothe Consumer Fears Over Inflation

The Fed expects core PCE inflation to fall to 4.3% on a year-over-year basis by the end of 2022. This would require month-over-month readings of about 0.35 percentage points, which is slightly above the average of the past three months (Chart 13). Our guess is that the Fed may be highballing its near-term inflation projections in order to give itself room to “underpromise and overdeliver” on the inflation front. If so, we could see inflation estimates trimmed later this year, which would provide a more soothing backdrop for risk assets. Chart 13AUS Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.35% (I)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.35% (I)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.35% (I)

Chart 13BUS Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.35% (II)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.35% (II)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.35% (II)

Concluding Thoughts on Investment Strategy According to Bank of America, fund managers cut their equity exposure to the lowest since May 2020. Optimism on global growth fell to a record low. Meanwhile, bears outnumbered bulls by 39 percentage points in this week’s AAII poll (Chart 14). If the stock market is about to crash, it will be the most anticipated crash in history. In my experience, markets rarely do what most people expect them to do. Chart 14Sentiment Towards Equities Is Pessimistic

Sentiment Towards Equities Is Pessimistic

Sentiment Towards Equities Is Pessimistic

Chart 15Global Equities Are More Attractively Valued After The Recent Sell-Off

Global Equities Are More Attractively Valued After The Recent Sell-Off

Global Equities Are More Attractively Valued After The Recent Sell-Off

Chart 16US And European EPS Estimates Have Been Trending Higher This Year

US And European EPS Estimates Have Been Trending Higher This Year

US And European EPS Estimates Have Been Trending Higher This Year

US equities are trading at 16.3-times forward earnings, with non-US stocks sporting a forward P/E ratio of 12.1 (Chart 15). Despite the decline in share prices, earnings estimates in both the US and Europe have increased since the start of the year (Chart 16). The consensus is that those estimates will fall. However, if our expectation that a recession will be averted over the next 12 months pans out, that may not happen. A sensible strategy right now is to maintain a modest overweight to stocks while being prepared to significantly raise equity exposure once clear evidence emerges that inflation has peaked. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Follow me on LinkedIn Twitter View Matrix

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

Special Trade Recommendations Current MacroQuant Model Scores

An Oasis Of Optimism: Notes From The Middle East

An Oasis Of Optimism: Notes From The Middle East

The Philadelphia Fed index for current activity fell 5.9 points to -3.3 in June, missing expectations of a slight improvement and marking the first negative reading since May 2020. The Future Expectations index fell more sharply to a nearly 14-year low of…

Executive Summary Was FAANGM A Bubble?

Was FAANGM A Bubble?

Was FAANGM A Bubble?

US inflation has become broad-based, and the labor market is very tight. Wages are a lagging variable, and they will be rising rapidly in the coming months, even as the economy slows. Although US growth will be slowing and global trade will be contracting, the Fed will remain hawkish over the coming months. This is an unprecedented environment and is negative for global and EM risk assets. The US trade-weighted dollar will continue to appreciate as long as the Fed sounds and acts in a hawkish manner and global trade contracts. Consistent with a US dollar overshoot, EM financial markets will undershoot. Even though EM equity and local bond valuations have become attractive, their fundamentals are still negative. A buying opportunity in EM will occur when the Fed makes a dovish pivot and China stimulates more aggressively. We reckon that these conditions will fall into place sometime in H2 this year. Bottom Line: For now, we recommend that investors stay defensive in absolute terms and underweight EM within global equity and credit portfolios. The dollar has more upside in the near term but a major buying opportunity in EM local currency bonds is approaching. Feature Last week, after a two and a half year hiatus, I travelled to Europe to visit clients. I also took the opportunity catch up with Ms. Mea, a global portfolio manager and a long-standing client. Prior to the pandemic, we met regularly to discuss global macro and financial markets. She was happy to resume our in-person meetings, and we met in Amsterdam over dinner last Friday. This report provides the key points of our conversation for the benefit of all clients. Ms. Mea: I am very happy that we are again able to meet in person. Video meetings are good, but in-person meetings are better. One’s body language often gives away their level of confidence regarding investment recommendations. Answer: Agreed. My meetings with clients this week have reminded me of the value of in-person meetings. Chart 1Our Calls On Various EM Asset Classes

Our Calls On Various EM Asset Classes

Our Calls On Various EM Asset Classes

Ms. Mea: Before our meeting I reviewed the evolution of your investment views since the pandemic erupted. Let me try to summarize them, and correct me if I miss something. Even though you upgraded your medium-term view on Chinese growth in May 2020 due to the stimulus, you remained skeptical of the rally in global risk assets. In Q2 2020, you upgraded your stance on EM bonds and in July 2020 you lifted the recommended allocation to EM equities and currencies from underweight to neutral (Chart 1). In the summer and fall of 2020, you were still wary of a deflationary relapse in developed economies. However, since January 2021, your outlook for the US shifted drastically to overheating and inflation. Since then, you have been very vocal about inflation risks in the US. At the same time, you have been warning about a major slowdown in Chinese growth. Regarding financial markets, in March 2021, you downgraded EM stocks and bonds to underweight and recommended shorting select EM currencies versus the US dollar (Chart 1). I should say that your call on US inflation and China’s slowdown have played out very well over the past 18 months. Let’s zero in on US inflation. It was just last year that many investors and analysts claimed that inflation is good for stocks because it helps their top line growth. Why then have global markets panicked? Chart 2Record Wealth Destruction In US Stocks And Bonds

Record Wealth Destruction In US Stocks And Bonds

Record Wealth Destruction In US Stocks And Bonds

Answer: Not many people have a deep understanding of inflation and its impact on financial markets because most investors lack experience in navigating financial markets during an inflation era. In fact, the US equity and bond market selloffs of the past 12 months have wiped out about $12 trillion and $3.5 trillion off their respective market value. This adds up to a combined $15.5 trillion or about 60% of US GDP and already exceeds the wipeouts during the March 2020 crash and all other bear markets (Chart 2). The way we think about macro and markets must change in an inflation regime. In our seminal February 25, 2021 Special Report titled A Paradigm Shift In The Stock-Bond Relationship, we made the case that the US economy and its financial markets were about to enter a new paradigm of higher inflation. We argued that US core CPI would spike well above 2% and US share prices and US government bond yields would become negatively correlated. A similar paradigm shift occurred in 1966 (Chart 3). In short, we argued that the era of low US inflation was over, and as a result, equities and bonds would selloff simultaneously. This will remain the roadmap for investors as long as core inflation is high. Chart 3A Paradigm Shift: US Stock Prices And Bond Yields Correlation Over Decades

A Paradigm Shift: US Stock Prices And Bond Yields Correlation Over Decades

A Paradigm Shift: US Stock Prices And Bond Yields Correlation Over Decades

Ms. Mea: Do you think the Fed is behind the curve? Answer: Yes, the Fed has fallen behind the curve, and, as we have repeatedly argued over the past 12 months, the US inflation genie is out of the bottle. There is a lot of confusion in the global investment community about how we should think about inflation, and about how and when the various measures of inflation matter. As consumers, we care about headline inflation because it affects our purchasing power. So, changes in all goods and service prices, including energy and food, matter to consumers. However, this does not mean that central banks should target and set policy based on headline inflation. Rather, central banks should target genuine broad-based inflation in the economy before it becomes entrenched. Ms. Mea: Can you explain why in certain cases a surge in energy, food and other prices leads to entrenched inflation but in other cases it does not? Answer: Let me give you an example. When consumers experience rapidly rising food and energy prices, they will likely demand faster wage growth from their employers. If businesses are enjoying strong demand for their goods/services and facing a tight labor market, they might have little choice but to agree to pay raises to sustain their business. Companies will then attempt to protect their profit margins by hiking their selling prices. Households may accept higher prices given their incomes are rising. This dynamic could cause inflation to become broad-based and entrenched. In this case, central banks should lift rates to slow the economy materially and cool off the labor market to end the wage-price spiral. If employees fail to negotiate hefty pay raises, odds are that inflation will not become broad-based. The more households spend on energy and food, the less income they will have to spend on other items, causing their discretionary spending to contract. In this case, there is no rush for central banks to tighten policy. If monetary authorities tighten materially, the economy will experience a full-fledged recession. In short, wage dynamics will determine whether inflation becomes broad-based. Labor market conditions will ultimately dictate this outcome. Ms. Mea: But why are wages more important than the price of fuel or food in determining whether inflation becomes broad-based? Answer: To be technically correct, unit labor costs, not wages, are key to inflation dynamics. Unit labor cost = (wage per hour) / (productivity). Productivity is output per hour. Given that labor is the largest cost component of US businesses, unit labor costs will swell and profit margins will shrink when salaries rise faster than productivity. CEOs and business owners always do their best to protect the their profit margins. Thus, accelerating unit labor costs will lead them to raise their selling prices. In the wake of wage gains, consumers might accept higher goods and service prices. If they do and go on to demand even higher wages, the economy will enter a wage-price spiral. This is why wage costs, more specifically unit labor costs, are the most important variable to monitor. If high energy and food prices lead employees to demand faster wage growth from their employers, and if they are granted wage increases above and beyond their productivity advances, inflation will become more broad-based and genuine. If consumers push back against higher prices, i.e., reduce their spending, corporate profits will plunge, and companies will freeze investment and lay off employees. Wages will slow and inflation will wane. Ms. Mea: Are all economies currently experiencing a wage-price spiral? Answer: The US and some other countries have been experiencing a wage-price spiral over the past 12 months. In other countries, including many developing economies, a wage-price spiral is currently absent. In the US, labor demand exceeds supply by the widest margin since 1950 (Chart 4). The upshot is that wages will continue to rise in response to persistently high inflation (Chart 5). Chart 4US Labor Demand Is Exceeding Labor Supply By The Widest Margin Since 1950

US Labor Demand Is Exceeding Labor Supply By The Widest Margin Since 1950

US Labor Demand Is Exceeding Labor Supply By The Widest Margin Since 1950

Chart 5US Wage Growth Is Already Very High

US Wage Growth Is Already Very High

US Wage Growth Is Already Very High

Wages in the US are currently rising at a rate of 6-6.5% or so. US productivity growth is around 1.5%. As a result, unit labor costs are rising at a 4.5-5% annual rate, the fastest rate for corporate America in the past 40 years (Chart 6). As Chart 6 demonstrates, unit labor costs have been instrumental in defining core CPI fluctuations over the past 70 years in the US. Chart 6US Unit Labor Costs Are Rising At The Fastest Rate Since 1982

US Unit Labor Costs Are Rising At The Fastest Rate Since 1982

US Unit Labor Costs Are Rising At The Fastest Rate Since 1982

Chart 7US Core Of Core Inflation Is High And Not Falling

US Core Of Core Inflation Is High And Not Falling

US Core Of Core Inflation Is High And Not Falling

In short, both surging unit labor costs and the acceleration of super core CPI measures like trimmed-mean CPI and median CPI suggest that US inflation has become broad-based and a wage-inflation spiral has taken hold in the US (Chart 7). Critically, wages are a lagging variable and are not reset all at once for all employees. American employees will continue to demand substantial wage hikes both to offset the last 12 months of lost purchasing power and to protect their purchasing power for the next 12 months. Hence, we will be witnessing faster wage growth in the coming months even as the economy slows. For many continental European economies and for several EM economies, wage growth is still weak. Chart 8 illustrates that nominal wage growth in India, Indonesia, China and Mexico are very subdued. Sluggish wage gains in emerging economies are consistent with the profile of their domestic demand. Domestic demand in these large developing economies remains extremely weak. In many cases, the level of domestic demand in real terms is still below its pre-pandemic level (Chart 9). Chart 8EM Wages Are Very Tame

EM Wages Are Very Tame

EM Wages Are Very Tame

Chart 9EM Domestic Demand Is Depressed

EM Domestic Demand Is Depressed

EM Domestic Demand Is Depressed

In China, deflation, rather than inflation, is the main economic threat. Headline and core inflation are within a 1-2% range (Chart 10), domestic demand is very weak, and the unemployment rate has risen in the past 12 months. Chart 10China's Inflation Is Subdued

China's Inflation Is Subdued

China's Inflation Is Subdued

Ms. Mea: Do you expect the US economy to contract? Answer: US growth will decelerate substantially, and certain segments of the economy could shrink for a couple of quarters. My expectation is that US corporate profits will contract materially. Slowing top line growth, narrowing profit margins, shrinking global trade and a strong dollar are all major headwinds for the S&P 500 EPS. EM EPS are also heading towards a major contraction. This is why I view EM fundamentals as negative even though EM valuations have become attractive. Ms. Mea: You have recently written that global trade volumes are about to contract. What is your rationale and is there any evidence that this is already happening? Answer: US and EU demand for consumer goods ex-autos has been booming over the past two years. Households have overspent on goods ex-autos (Chart 11). Given that their disposable income is contracting in real terms and a preference to spend on services, households will markedly curtail their purchases of consumer goods in the coming months. This will hurt global manufacturing in general, and emerging Asia in particular. Some forward-looking indicators are already signaling a contraction in global trade: US retail inventories (in real terms) have swelled (Chart 12, top panel). US retailers will dramatically reduce their orders. Chart 11Global Trade Volumes Will Shrink In H2 2022

Global Trade Volumes Will Shrink In H2 2022

Global Trade Volumes Will Shrink In H2 2022

Chart 12US Import Volumes Are Set To Contract

US Import Volumes Are Set To Contract

US Import Volumes Are Set To Contract

Besides, US railroad carload is already shrinking, signaling reduced goods shipments (Chart 12, bottom panel). Taiwanese shipments to China lead global trade and they point to an impending slump (Chart 13, top panel). Also, the Taiwanese manufacturing shipments-to-inventory ratio has dropped below 1 (Chart 13, bottom panel). Finally, industrial metal prices are breaking down despite easing lockdowns in China and continued sanctions on Russia (Chart 14). This is a sign of downshifting global manufacturing. Chart 13A Red Flag For Global Trade

A Red Flag For Global Trade

A Red Flag For Global Trade

Chart 14Industrial Metal Prices Are Breaking Down

Industrial Metal Prices Are Breaking Down

Industrial Metal Prices Are Breaking Down

Ms. Mea: Won’t a global trade contraction push down goods prices and help US inflation? Answer: Correct, it will bring down US goods inflation but not services inflation. Importantly, as we discussed above, US inflation has already spilled into wages and has become broad-based. Plus, it is hovering well above the Fed’s target. Hence, the Fed cannot dial down its hawkishness now, even if goods price inflation drops significantly. In brief, even though US growth will be slowing and global trade will be contracting over the coming months, the Fed is likely to remain hawkish. This is an unprecedented environment and is negative for global and EM risk assets. Ms. Mea: What are the financial market implications of entrenched inflation in the US and the lack of genuine inflationary pressures in many emerging economies? Answer: As long as the Fed sounds and acts in a hawkish manner and/or global trade contracts, the US trade-weighted dollar will continue to appreciate. The greenback is a countercyclical currency and rallies when global trade slumps. On the whole, the USD will likely overshoot in the near run. Consistent with a US dollar overshoot, EM financial markets will undershoot. Even though investor sentiment on EM equities and USD bonds is very low (Chart 15), a final capitulation selloff is still likely. In short, EM valuation and positioning are positive for future potential returns yet their fundamentals (business cycle, profits, return on capital, etc.) are still negative. A buying opportunity in EM will emerge when the Fed makes a dovish pivot, China stimulates more aggressively, and EM equity and bond valuations improve further. We reckon that these conditions will fall into place sometime in H2 this year. If the Fed turns dovish early without taming US inflation, it will fall behind the inflation curve and the US dollar will begin its bear market. Investors will respond by embracing EM financial assets. EM local currency bonds in particular offer value (Chart 16). Prudent macro policies and the lack of wage pressures entail a good medium-to-long term opportunity in EM local currency bonds. Chart 15Investor Sentiment On EM Stocks And USD Bonds Is Low

Investor Sentiment On EM Stocks And USD Bonds Is Low

Investor Sentiment On EM Stocks And USD Bonds Is Low

Chart 16US TIPS Yields Should Roll Over For EM Local Bond Yields To Decline

US TIPS Yields Should Roll Over For EM Local Bond Yields To Decline

US TIPS Yields Should Roll Over For EM Local Bond Yields To Decline

As EM currencies put in a bottom, local yields will come down. This will help their equity markets. Ms. Mea: Speaking of a capitulation selloff, how far can it go? Both for EM stocks as well as the S&P 500? Chart 17S&P500: Where Is Technical Support Line?

S&P500: Where Is Technical Support Line?

S&P500: Where Is Technical Support Line?

Answer: As long as US bond yields and oil prices do not start falling on a consistent basis, the S&P 500 will remain under selling pressure. Technicals can help us gauge the likely magnitude of the move. The S&P 500 has dropped to a major technical support, but it will likely be broken. The next support is around 3100-3200 (Chart 17). The EM equity index is sitting on a technical support now (Chart 18). The next support level is 15-17% below the current one. Chart 18EM Stocks in USD Terms Could Drop Another 15%

EM Stocks in USD Terms Could Drop Another 15%

EM Stocks in USD Terms Could Drop Another 15%

Critically, US equity investors should also consider whether the US equity bull market that has been in place since 2009 is over. If it is, then the S&P 500 bear market could last long, and prices could drop significantly. Chart 19Was FAANGM A Bubble?

Was FAANGM A Bubble?

Was FAANGM A Bubble?

A few observations that investors should keep in mind: First, over the past 12 years, FAANGM stocks have followed the profile of the Nasdaq 100 (Chart 19). In short, FAANGM stocks have risen as much as the Nasdaq 100 index did in the 1990s. Second, when retail investors rush into an asset class, it often signals the final phase of the bull market. Once the bull market ends, the ensuing bear market is vicious. The behavior of tech/internet stocks and the broader S&P 500 fits this profile extremely well. For several years after the Lehman crash, individual investors were hesitant to buy US stocks. However, the resilience of US equities led to a buy the dip mentality in 2019-20. Retail investors joined the equity party en masse in early 2020. The post retail frenzy hangover is usually very painful and prolonged. Based on this roadmap, it seems that the 2020-21 retail-driven rally was the final upleg in the S&P 500 bull market. By extension, we have entered a bear market that could be vicious and extended. All the excesses of the 10-year FAANGM and S&P500 bull markets will need to be worked out before a new bull market emerges. Finally, a high inflation regime raises the bar for the Fed to rescue the stock market. This also entails lower equity multiples than we have in the S&P500 now. Ms. Mea: What do you make of EM’s recent outperformance versus DM stocks? When will you upgrade EM versus DM? Answer: Indeed, EM stocks have recently outperformed DM stocks. We might be witnessing a major transition in global equity market leadership. We have held for some time that an equity leadership change from the US to the rest of the world and from TMT stocks to other segments of the global equity market would likely take place during or following a major market selloff. The ongoing equity bear market seems to be exactly that catalyst. Chart 20For EM Equities To Outperform, USD Needs To Weaken

For EM Equities To Outperform, USD Needs To Weaken

For EM Equities To Outperform, USD Needs To Weaken

If the S&P 500 bull market is over, the global equity leadership will also change away from US and TMT stocks to other stock markets and sectors. That said, to upgrade EM stocks, we need to change our view on the USD because EM relative equity performance versus DM closely tracks the inverted trade-weighted US dollar (Chart 20). In the near term, we believe the greenback has more upside potential. In particular, Asian currencies and equity markets cannot outperform when the Fed is hawkish and global trade is contracting. Latin American currencies have benefited since early this year from the spike in commodity prices. However, worries about a US recession, a strong dollar and a lack of strong recovery in the Chinese economy will push industrial metal prices lower. As shown in Chart 14 above, industrial metal prices are breaking down. This is a bad omen for Latin American markets. On the whole, we will likely be upgrading EM versus DM later this year. For now, we recommend that investors stay defensive and underweight EM within global equity and credit portfolios. We also continue to short the following currencies versus the USD: ZAR, COP, PEN, PLN, PHP and IDR; as well as HUF vs. CZK, and KRW vs. JPY. A major buying opportunity in local currency bonds is approaching. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com

Executive Summary

Does Powell Need To Channel His Inner Volcker?

Does Powell Need To Channel His Inner Volcker?

Economic growth is now a casualty, and not a driver, of monetary policy choices. Inflation is dictating where central banks are taking interest rates. Our baseline view remains that core US inflation will cool by enough on its own without the need for the Fed to deliver a policy-induced recession. However, the odds of the latter have increased after the upside surprise in the May US CPI report. The ECB has been dragged into the same morass as other major central banks – tightening policy because of soaring inflation, despite broad-based signs of sluggish economic growth. We still see the pricing of cumulative rate hikes in the euro area as being too aggressive, even after last week’s clear announcement from the ECB that a string of future rate hikes was coming. With the ECB also announcing an end to its QE program, but offering no details on a replacement, markets have been given the green light to push Italian yields/spreads higher (and the euro lower) until there is an ECB response to market fragmentation in European sovereign debt. Bottom Line: The Fed is still more likely than the ECB to follow through on rate hikes discounted in US and European interest rate curves - position for renewed widening of the Treasury-Bund spread. Italian bond yields will remain under upward pressure until the contours of an ECB plan to stabilize Peripheral Spreads alongside rate hikes are revealed – tactically position for a wider BTP-Bund spread. Central Bankers Cannot Worry About Growth … Or Your Investment Portfolio The US consumer price index (CPI) report for May was yet another bond-bearish shock in a year full of them. With US headline US inflation hitting an 41-year high of 8.6%, the Treasury market adjusted bond yields upward to reflect both higher inflation expectations and even more aggressive Fed tightening. Coming only a day after the June European Central Bank (ECB) meeting that provided guidance that a series of rate hikes would begin in July, that could include a 50bp hike at the September meeting, financial markets worldwide moved to price in the risk that policy-induced recessions were the only way to bring down soaring global inflation. The result: global bond yields soared to new highs for the year, while risk assets of all shapes and sizes were hammered. We have our doubts that today’s class of policymakers – especially the Fed - has the stomach to repeat the actions of former Fed Chair Paul Volcker, who famously pushed US interest rates above the double-digit inflation rates of the late 1970s to engineer a deep recession to crush inflation. The starting point of the current tightening cycle is even further behind the curve than during the Volcker era, in terms of “realized” real interest rates, with the 10-year US Treasury yield now over five percentage points below headline US CPI inflation (Chart 1). Related Report Global Fixed Income StrategyAssessing The Risks To Our Main Views Central bankers are now faced with the no-win scenario of pushing nominal policy rates higher to chase soaring inflation in a bid to maintain inflation fighting credibility, regardless of the spillover effects on financial market stability or economic growth expectations. More worryingly, the rate hikes needed to establish that credibility are not only becoming more frequent but larger. 50bps has become the “standard” size for developed market rate hikes. The Fed may have upped the ante with the 75bp hike at yesterday's FOMC meeting. Such is the reality of a funds rate still only at 1.75% but with US inflation pushing toward 9%. The timing of the latest hawkish shifts from the Fed, ECB and others is surprising, looking purely from a growth perspective. The OECD leading economic indicators for the US, euro area and China are slowing, alongside depressed consumer confidence and deteriorating business sentiment (Chart 2). Similar readings are evident in comparable measures in other major economies, both in developed and emerging economies. This would normally be the type of backdrop that would entice central banks to consider easing monetary policy - IF inflation was subdued, which is clearly not the case today. Chart 1Does Powell Need To Channel His Inner Volcker?

Does Powell Need To Channel His Inner Volcker?

Does Powell Need To Channel His Inner Volcker?

In fact, high inflation is the reason why economic sentiment has worsened. Chart 2Worrying Signs For Global Growth

Worrying Signs For Global Growth

Worrying Signs For Global Growth

Consumers see income growth that is lagging inflation, especially for everyday items like gasoline and food. Businesses are seeing input costs rising, especially for labor in an environment of tight job markets. Inflation has become broad-based, across goods, services and wages. This is true for countries that are more advanced in their monetary tightening cycles - the US, Canada and the UK - where inflation rates are remarkably similar (Chart 3). But it is also now true in countries with lower (but still accelerating) inflation rates and where central banks have been slower to tighten monetary conditions, like the euro area and Australia (Chart 4). Chart 3Inflation Turning More 'Domestic' (Services / Wages) Here

Inflation Turning More 'Domestic' (Services / Wages) Here

Inflation Turning More 'Domestic' (Services / Wages) Here

Chart 4Still No Major Services/Wage Inflation Overshoots Here

Still No Major Services/Wage Inflation Overshoots Here

Still No Major Services/Wage Inflation Overshoots Here

For the Fed, assessing the underlying momentum of US inflation, and setting monetary policy accordingly, has become a bit trickier. While headline inflation continues to accelerate in response to rising energy and food prices, core inflation ticked lower in both April and May and now sits at 6.1%, down from 6.5% in March. Longer-term survey-based measures of inflation expectations have been moving steadily higher, with the University of Michigan 5-10 year consumer inflation expectations survey now up to a 14-year high of 3.3% (Chart 5). Yet longer-term market-based inflation expectations have been more stable, with the 10-year TIPS breakeven now at 2.66%, down from the late April peak of 3.02%. There are also some mixed signals visible within the US inflation data. Core goods CPI inflation clocked in at 8.5% in May, down from the recent peak of 12.4% in February 2022, while core services CPI inflation accelerated to a 14-year high of 5.2% in May (Chart 6). A similar divergence can be seen when looking at the Atlanta Fed’s measures of “sticky” and “flexible” price inflation. Core flexible CPI inflation – measuring prices that adjust more rapidly – has fallen from a peak of 19% to 12.3% in May. At the same time, core sticky CPI inflation for prices that are slower to adjust sped up to an 31-year high of 5% in May. Chart 5Some Mixed Inflation Messages For The Fed

Some Mixed Inflation Messages For The Fed

Some Mixed Inflation Messages For The Fed

Chart 6US Inflation Will Eventually Be Lower, But 'Stickier'

US Inflation Will Eventually Be Lower, But 'Stickier'

US Inflation Will Eventually Be Lower, But 'Stickier'

Chart 7Stick With UST-Bund Spread Widening Trades

Stick With UST-Bund Spread Widening Trades

Stick With UST-Bund Spread Widening Trades