United States

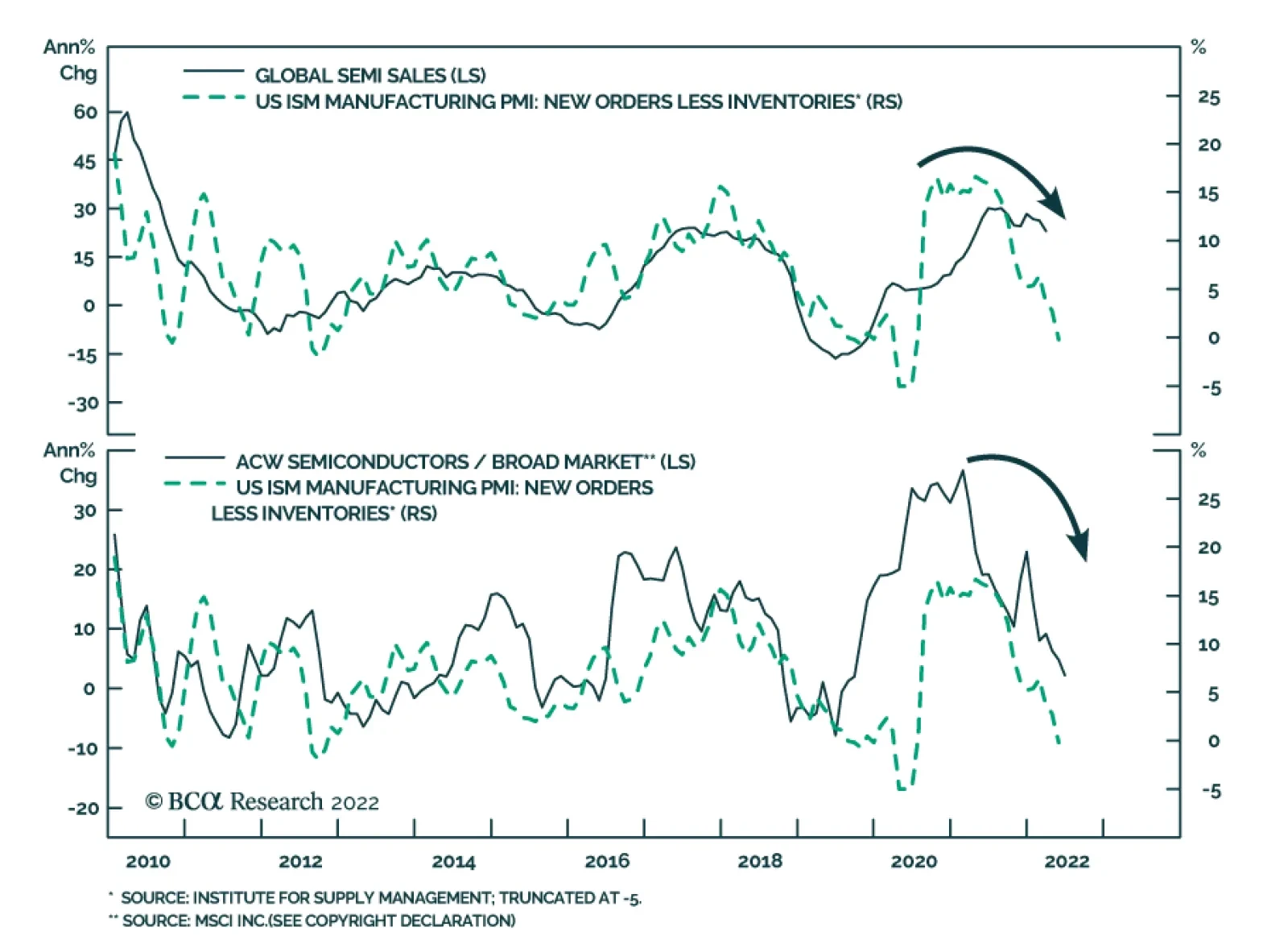

Global semiconductor stocks underperformed the broad market in the year-to-date equity selloff. However, over the past month they are up on both an absolute and relative basis. Have semiconductor stocks bottomed? The rollout of 5G networks, demand for…

Executive Summary Lower Rates Are A Tailwind For Growth Stocks

Lower Rates Are A Tailwind For Growth Stocks

Lower Rates Are A Tailwind For Growth Stocks

We remain in the bearish camp. While the market bottom is getting closer, there are still hurdles to overcome such as elevated economic and earnings growth expectations, which need to come down to prevent new disappointments. Notably, the market focus has shifted away from inflation and has turned towards worries about growth as is evident in the falling 10-year Treasury yield. The environment of slowing growth and falling rates is a tailwind for growth stocks, warranting an upgrade of Growth to at least a benchmark weight. Technicals also signal that Growth is oversold relative to Value. The valuation differential has also moderated. However, we are wary of upgrading Growth to an outright overweight and downgrading Value to underweight as there is still plenty of economic uncertainty. We also posit that in the next several months the markets will be “fat and flat”, i.e., a bear market punctuated by rallies and pullbacks. In this environment, a balanced allocation between Growth and Value will reduce portfolio volatility and result in higher compound returns. Bottom Line: In a commentary to our chart pack report, we upgrade the Growth/Value style preference to benchmark allocation. Feature This week we provide you with a style chart pack. In this accompanying note, we will make a case for upgrading Growth and downgrading Value, bringing these style allocations to equal weight. We are booking a profit of 13% since we established the position in January 2022. We are getting closer to upgrading Growth to overweight. Performance May started as another tough month for equities, but, as they say, all’s well that ends well. After pulling back 10% since the beginning of May, and briefly touching bear market territory of -20%, the S&P 500 rebounded in the last 10 days of the month bringing the index to where it ended April. As a result, the S&P 500 was flat, and the NASDAQ was down 2.4% in May. As expected, the rally brought about a change in leadership (Chart I-1), with Consumer Discretionary and Technology leading the pack. Energy and Utilities are the only sectors that avoided rotation. Since May 20, Growth has outperformed Value by 3%. Chart I-1Recent Performance

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Bear Market Rally Or The Real Thing? Since the start of the May rally, investors have been debating whether it has legs. Bulls argue that we are in the early innings of a sustainable rebound in equities – after all, much of the bad news is already priced in, 45% of NYSE and 70% of NASDAQ have recently hit new 12-month lows, screaming oversold conditions, and making bottom fishing tempting (Chart I-2). Bears consider this surge in performance a garden-variety bear market rally: Growth is slowing and none of the problems that have been haunting the markets over the past five months, such as inflation, war, China, and a hawkish Fed, have yet been resolved. Our views are closer to the bearish camp: We believe that, even if the market bottom is getting closer, there are still hurdles to overcome, such as elevated economic and earnings growth expectations, which need to come down to prevent new disappointments. As we discussed in the recent “What Is Next For Equities: They Will Be Fat And Flat” report, we believe that equities are likely to be range-bound over the next several months: A turn in inflation and a downshift in growth may ignite rallies on hopes of a gentler, data-driven Fed, and a shallower trajectory for the rate-hiking cycle (Chart I-3). However, we argue that the Fed “put” is no longer in play and the Fed will stay focused on inflation, inadvertently puncturing any budding rallies. In addition to a hawkish Fed, investors will have to process what may become a sharp economic growth slowdown and an earnings recession in the US on the back of rising costs, a stronger dollar, and slowing global demand for US goods. Chart I-2Is Much Of The Bad News Already Priced In?

Is Much Of The Bad News Already Priced In?

Is Much Of The Bad News Already Priced In?

Chart I-3Many Hope For A Shallower Hiking Cycle

Many Hope For A Shallower Hiking Cycle

Many Hope For A Shallower Hiking Cycle

Growth Vs. Value: Shifting Positioning To Equal Weight When Growth Is Harder To Find, Growth Stocks Shine As we argued in the “Fat and Flat” report, there are multiple signs that economic growth is slowing, and that earnings growth will disappoint. Our Business Cycle Indicator, which is a compilation of soft and hard data across production, consumer, and credit dimensions, is also signaling a slowdown (Chart I-4). Here we would like to emphasize our view: As of now, US economic growth is strong, and it is only its second derivative, i.e. a deceleration of growth, that is the root of our concerns. In a world where growth is becoming scarcer, companies that can deliver growth will shine. These are “growth” companies, i.e. large, stable companies with strong balance sheets that are able to generate positive cash flow and churn out strong earnings even under economic duress (Chart I-5). Quality growth outperforms during slowdowns (Chart I-6). This reasoning does not apply to speculative, barely profitable, growth companies which will fight for survival in a slow-growth world. Chart I-4We Are In A Slowdown Stage Of The Business Cycle

We Are In A Slowdown Stage Of The Business Cycle

We Are In A Slowdown Stage Of The Business Cycle

Chart I-5Large Cap Growth Is Synonymous With Quality

Large Cap Growth Is Synonymous With Quality

Large Cap Growth Is Synonymous With Quality

Chart I-6Growth Outperforms During Economic Slowdowns

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Of course, one might argue that economic growth has been slowing for about a year, initially by returning towards the pre-pandemic trend and, lately, as a result of monetary tightening. Yet, over the past six months, Growth has underperformed Value by nearly 11%. What is different now? First, inflation, and the monetary tightening that inevitably follows it, are the mortal enemies of growth stocks: Higher discount rates deflate the present value of future cash flows. Rising inflation and sharply rising Treasury yields are behind the recent sell-off in Growth stocks. However, recently, the market focus has shifted away from inflation, and seems to finally be turning towards worries about growth. As a result, the 10-year Treasury yield decreased from 3.12% to 2.75%, and its relentless climb may now be behind us (Chart I-7). Lower rates are a tailwind for Growth stocks which rebounded at the first whiff of rate stabilization (Chart I-8). Chart I-7Investors Concerns Have Shifted From Inflation To Growth

Investors Concerns Have Shifted From Inflation To Growth

Investors Concerns Have Shifted From Inflation To Growth

Further, our research on macroeconomic regimes suggests that a turn in inflation heralds a change in market leadership from Value to Quality and Growth (Chart I-9). Chart I-8Lower Rates Are A Tailwind For Growth Stocks

Lower Rates Are A Tailwind For Growth Stocks

Lower Rates Are A Tailwind For Growth Stocks

Chart I-9Growth And Quality Will Lead Markets When Inflation Abates

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Growth Not Yet Cheap But Oversold This year’s sell-off is characterized by a multiple contraction. Growth is a poster child of this trend: Its forward multiple has decreased by 8 points, with the style currently trading at just under 20x forward earnings, which is the 61st percentile relative to its 10-year history (compare that to 28x and the 94th percentile back in January). As for Value, it also became cheaper, contracting from 16.8x in January to 14.9x (Table I-1). Table I-1Valuations And EPS Growth Expectations

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

According to the BCA Valuations Indicator (Chart I-10), the Growth/Value valuations spread has moderated but by itself, is not an impetus for a switch. However, looking at technicals, Growth is extremely oversold relative to Value and is at levels last seen in 2006. Why Neutral, Not Overweight? We hope we made a compelling case for shifting allocation from Value to Growth. Then why not go overweight, but just neutral? Mostly because many of the macroeconomic developments we have described are tentative and are just conjecture at this point – there is still plenty of uncertainty about inflation, rates, and the Fed monetary response. Second, while Growth stocks are supposed to grow faster than Value stocks, at the moment analysts expect them to grow at 8% and 11% respectively. We expect earnings growth expectations for Value stocks to be downgraded since they are dominated by cyclicals. However, until the new numbers are in for both styles, we need to be careful. Chart I-10Growth Is Getting Cheaper Relative To Value... It Also Appears Oversold

Growth Is Getting Cheaper Relative To Value... It Also Appears Oversold

Growth Is Getting Cheaper Relative To Value... It Also Appears Oversold

Last, if we are right, and US equities are to test their bottom this summer in a “fat and flat” manner, there will be a frequent change in leadership, with Growth and Small outperforming during the rallies, and Value outperforming during pullbacks. Portfolios need exposure to both styles to achieve the highest compound returns as diversification reduces portfolio volatility. Once macroeconomic uncertainty dissipates, we will be able to pounce and shift Growth to overweight, and Value to underweight. For now, we are going to stay neutral out of an abundance of caution. Bottom Line Macroeconomic conditions are becoming more favorable for Growth as Treasury yields stabilize and economic growth slows, making the strong fundamentals and stable earnings of large-cap growth stocks more valuable. Growth is oversold relative to Value, and the relative performance differential of Growth vs. Value over the past six months has been staggering – it is time to book profits and prepare for the next chapter. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com S&P 500 Chart II-1Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-2Profitability

Profitability

Profitability

Chart II-3Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-4Uses Of Cash

Uses Of Cash

Uses Of Cash

Cyclicals Vs Defensives Chart II-5Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-6Profitability

Profitability

Profitability

Chart II-7Valuation And Technicals

Valuation And Technicals

Valuation And Technicals

Chart II-8Uses Of Cash

Uses Of Cash

Uses Of Cash

Growth Vs Value Chart II-9Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-10Profitability

Profitability

Profitability

Chart II-11Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-12Uses Of Cash

Uses Of Cash

Uses Of Cash

Small Vs Large Chart II-13Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-14Profitability

Profitability

Profitability

Chart II-15Valuations and Technicals

Valuations and Technicals

Valuations and Technicals

Chart II-16Uses Of Cash

Uses Of Cash

Uses Of Cash

Table A1Performance

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Table A2Valuations And Forward Earnings Growth

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Footnotes Recommended Allocation Recommended Allocation: Addendum

Chartbook: Style Chart Pack

Chartbook: Style Chart Pack

Executive Summary The default take on the economy and financial markets has been tilting increasingly bearish although the ongoing data flow has yet to pick a side. The data in the stories from the front page of The New York Times' Saturday Business section over the Memorial Day weekend nod in the direction of a Goldilocks outcome: households have been so well fortified by their pandemic savings that their spending is holding up despite stiff price increases but innovation and automation are allowing companies to protect their profits even in a tight labor market. We remain of the view that a wage-price spiral is unlikely and therefore see a plausible path for S&P 500 margins to hold up better than expected over the rest of the year. We are looking for an opportunity to add equity exposure to our ETF portfolio to restore its overweight allocation but we won't rush to do it while the S&P 500 is within 100 points of near-term technical resistance. Putting Excess Savings To Good Use

Putting Excess Savings To Good Use

Putting Excess Savings To Good Use

Bottom Line: We remain constructive on financial markets and the US economy over the next twelve months but are content to wait for a better tactical entry point to increase our ETF portfolio's equity exposure. Feature The Internet has drastically curtailed newspapers’ influence, but Page 1 is still not the place to go for alpha-generating investment ideas. Nearly all the juice has been squeezed from an investment idea by the time it makes it to the front page; if there’s any alpha to be found in the paper, it will be on the vitamin pages – B7, B12, D3. As Don Coxe, a favorite mentor, put it throughout his five-decade career as an investment strategist, “We don’t invest on the basis of Page 1 stories. We invest on the basis of stories on Page D7 that are going to Page 1.” Lately, the stories getting the most media airtime have accentuated the negative. Inflation is making 40-year highs; consumers are in a grim mood, at least according to the University of Michigan’s sentiment survey; the Fed was napping and may not be able to catch up; corporate profits will be the next domino to fall. Against that backdrop, we thought the front-page New York Times Saturday Business section stories reporting on coincident indicators over the Memorial Day weekend provided an interesting corrective. The data are moving fast and their positive cast may be fleeting, but the latest batch makes the case that it’s too soon to abandon our constructive market and economic view. Declining Profit Margins Might Still Beat Expectations The entire space above the fold was filled by a photograph of workers harvesting radishes. There was a large machine with moving conveyor belts behind them and as the workers bound the radishes into clumps, they tossed them onto the belt without turning their heads. Under the headline, “Farming Transformation In the Fields of California,” the article began, “It looks like a century-old picture of farming in California: a few dozen Mexican men … plucking radishes from the ground [.] But the[se] crews … represent the cutting edge of how America pulls food from the land.” “For starters, the young men … are working alongside technology unseen even 10 years ago. … [W]hat looks like a tractor retrofitted with a packing plant … carries [the radishes] through a cold wash and delivers them to be packed into crates and delivered for distribution in a refrigerated truck.” “The other change is more subtle, but no less revolutionary. None of the workers are in the United States illegally.” “Both of these transformations are driven by the same dynamic: the decline in the supply of young illegal immigrants from Mexico, the backbone of the work force picking California’s crops since the 1960s.” “The new demographic reality has sent farmers scrambling to bring in more highly paid foreign workers on temporary guest-worker visas, experiment with automation wherever they can and even replace crops with less labor-intensive alternatives.” The drying up of its inexpensive labor supply would seem to pose a mortal threat to farming profit margins. Temporary workers covered by the H-2A visa program earn two-and-a-half dollars an hour more than the $15 minimum wage applicable to local workers and must be provided with room, board and transportation to and from the fields. The industry has adapted, however, finding ways to mechanize the harvesting of crops that don’t need to meet aesthetic standards while tinkering with planting and growing techniques and genetic modifications to reduce labor intensity. Crops that resist mechanization hacks are leaving the United States for lower-cost climes as evidenced by a doubling of fruit and vegetable imports over the last five years. California acreage given over to asparagus, an especially labor-intensive crop, has fallen to 4,000 acres in 2020 from 37,000 two decades ago, while the nearby Mexican state of Sinaloa picked up the slack by increasing its harvest by around 30,000 acres. The adaptations seem to be working well for all but the formerly essential undocumented agricultural work force. As a vineyard worker who illegally crossed the border nearly 20 years ago said, “It scares me that they are coming with H-2As and … robots. That’s going to take us down.” What does this specific story have to do with corporate profit margins, a general subject of vital importance to all investors? It illustrates the difficulty employees confront in capturing and maintaining leverage when employers can radically alter the dynamic with investment. The sub-headline sums up labor’s plight well: “Growers are turning more and more to workers on seasonal visas, and mechanizing where they can. Meanwhile, labor-intensive crops are shifting south of the border.” Chart 1Input Costs Are Surging, ...

Input Costs Are Surging, ...

Input Costs Are Surging, ...

We reiterate that a wage-price spiral is not a foregone conclusion. Neither is an onshoring bonanza. Although the aggregate first-quarter S&P 500 profit margin narrowed versus the year-ago quarter (revenue-per-share growth (13.9%) outpaced earnings-per-share growth (11.2%) by nearly three percentage points), it managed to surprise to the upside (earnings’ 7% beat was over four percentage points wider than revenues’ 2.6%), and innovation and investment may allow it to do so going forward, despite soaring materials costs (Chart 1) and upward wage pressures. After an initial pandemic surge, however, wages have failed to keep pace with inflation for the last year (Chart 2) and growth in average hourly earnings, the most timely compensation series, may have peaked (Chart 3). Chart 2... But Wages Aren't Keeping Pace With Inflation ...

... But Wages Aren't Keeping Pace With Inflation ...

... But Wages Aren't Keeping Pace With Inflation ...

Chart 3... And They May Have Already Peaked

... And They May Have Already Peaked

... And They May Have Already Peaked

Households Are Not At Risk Of Drowning In Debt … The other two front-page stories challenge the narrative that high inflation will choke off consumption. “U.S. Spending Is Up Even With Buying Power Low” discussed the previous day’s release of the April Personal Income and Outlays report. The article expressed surprise that consumption rose 0.9% month-over-month when disposable income rose just 0.3% and was flat in real terms. Households squared the circle by saving less of their income, with the savings rate shrinking to 4.4%, the lowest level since the subprime boom, when it put in its all-time bottom (Chart 4). Chart 4Putting Their Cushion To Good Use

Putting Their Cushion To Good Use

Putting Their Cushion To Good Use

Leading up to the financial crisis, households took on increasing quantities of debt to maintain their spending and the article noted that revolving loan balances (primarily credit cards) grew at their fastest rate in 24 years in March. That narrow statement is true, strictly speaking, but an investor should place it in a fuller context. Outstanding credit card and other revolving debt held by banks remains shy of its post-crisis growth trend though it did just top its previous high set in early 2020 (Chart 5). Though the article quoted an economist tut-tutting that credit card-funded spending is unsustainable, household debt service payments as a share of disposable income remain below their pre-pandemic lows and miles from their subprime-era level (Chart 6). These are fraught times, but any comparison linking US households’ financial positions with 2007 is specious. Chart 5Outstanding Card Balances Are Still Below Trend ...

Outstanding Card Balances Are Still Below Trend ...

Outstanding Card Balances Are Still Below Trend ...

Chart 6... And Households Have Plenty Of Capacity To Take On More

... And Households Have Plenty Of Capacity To Take On More

... And Households Have Plenty Of Capacity To Take On More

… Because They Were Pre-emptively Insulated From Elevated Inflation We have been tracking households’ excess pandemic savings balance since CARES Act transfer payments began to flow into individual checking and savings accounts. We estimate that households ended April with between $2.1 and 2.2 trillion more in savings than they would have had if the pandemic had not occurred. They began dipping into their stash in last year’s fourth quarter, when the savings rate first edged below its 8.3% pre-pandemic level, and have done so with increasing zest this year, trimming almost $200 billion from the excess savings peak (Table 1). They drew down almost $60 billion in April alone, indicating that half of the excess savings (our working estimate of how much will be spent) would last for eighteen months if households saved at half their pre-pandemic rate, or another nine if they didn’t save anything at all. Table 1The Excess Savings Cushion Remains Quite Large

Read All About It

Read All About It

That’s a handy reference point to keep in mind when assessing the third front-page story, headlined, “Gas Prices Keep Surging, But Demand Isn’t Falling.” The same headline could be repurposed to top an article reporting on American Airlines’ upwardly revised second-quarter revenue outlook. American said in a filing before Friday’s open that it now expects 2Q22 revenue to exceed 2Q19 revenue (the airlines’ last pre-pandemic comparison) by 11-13%, up from its previous 6-8% guidance. A real-time Bloomberg headline accompanying the story credited the increase to “continued strength in demand and pricing.” The bottom line is that households have the means to satiate pent-up pandemic demand despite significantly higher prices. Spirited internal debates have revolved around households’ willingness to use those means. Without a similar fiscal transfer precedent, neither side can argue its case with high conviction, but the accelerating dissaving of the last six months and mounting evidence of consumers’ low sensitivity to higher airfares and gasoline prices suggest that the spending camp has the upper hand for now. Under an Occam’s razor standard, we don’t think the analysis requires anything as fancy as mental accounting gymnastics or Friedman’s permanent income hypothesis when there’s an age-old phrase that should especially resonate with the YOLO set: Easy come, easy go. ETF Portfolio Update Our cyclical ETF portfolio outperformed its benchmark by 43 basis points (bps) in May, bringing its outperformance since its January 31st launch to 87 bps. Our equity holdings accounted for the lion’s share of the value-add. Energy (XLE), our sole sector overweight, outperformed the S&P 500 by nearly 16 percentage points, while our Staples (XLP, 4-ppt underperformance) and Utilities (XLU, 4-ppt outperformance) underweights offset each other. Allocating some Discretionary exposure to outperforming homebuilders (ITB) was successful but was offset by concentrating all of our Materials exposure in metals and miners (XME). The Pure Value Index (RPV) and SmallCap 600 (IJR) overweights made undiluted positive contributions. Our high yield (JNK) overweight helped our fixed income performance, though it was held back by the allocation to variable-rate preferreds (VRP). VRP has struggled, but we still see going to the back of the creditor priority line at overcapitalized large banks as a source of alpha, and we maintain our modest allocation. We continue to seek an opportune time to remove some of the tactical restraints we imposed on the portfolio in early March. We are eager to bring the portfolio in line with BCA’s recent tactical equity upgrade to overweight but are reluctant to increase our equity exposure so close to the 4,200 resistance level that we expect will repel S&P 500 rallies in the immediate term. Friday’s selloff gave a buyer an additional 1% of headroom from the level we passed up on May 27th, but we intend to hold out for something in the neighborhood of 4,000. Investment Implications Viewed through a contrarian’s magazine-cover-indicator lens, the risk/reward profile of our constructive view has improved as the headlines’ bearish bias has become more pronounced. The zeal with which those in the bearish economic camp seized upon Walmart’s and Target’s first-quarter disappointments was revealing. Both companies’ earnings stunk – Walmart missed expectations by 12% and Target by 29% – but both companies beat revenues, by around 2%, just like their dollar-store and price-club peers who met or beat earnings expectations. Though it gave the commentariat something to do for a few days, the debate over the existence of a retail inventory glut isn’t supported by the aggregate data (Chart 7). Chart 7Retail Inventory Glut? Seriously?

Retail Inventory Glut? Seriously?

Retail Inventory Glut? Seriously?

No one knows what’s coming next against the unprecedented macro backdrop and everyone involved in forecasting and investing should approach their work with humility right now. For an investor, that means staying within sight of the shore in terms of deviations from benchmark indexes and managing portfolios more tactically by reducing holding periods and setting, and abiding by, tight stops on opportunistic plays. A preponderance of data has yet to cast doubt on our constructive take on the economy and markets (nor has it conclusively validated it, alas). The sense that we increasingly find ourselves in the minority makes us feel better about the potential returns to our view, however, and we are sticking with it. We continue to recommend overweighting equities in a balanced portfolio, and high yield within fixed income portfolios (NB: our US Bond Strategy team recommends an equal-weight allocation to high yield) over a twelve-month time frame and are looking for a better entry point to increase our equity exposures within our ETF portfolio. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Cyclical ETF Portfolio

Read All About It

Read All About It

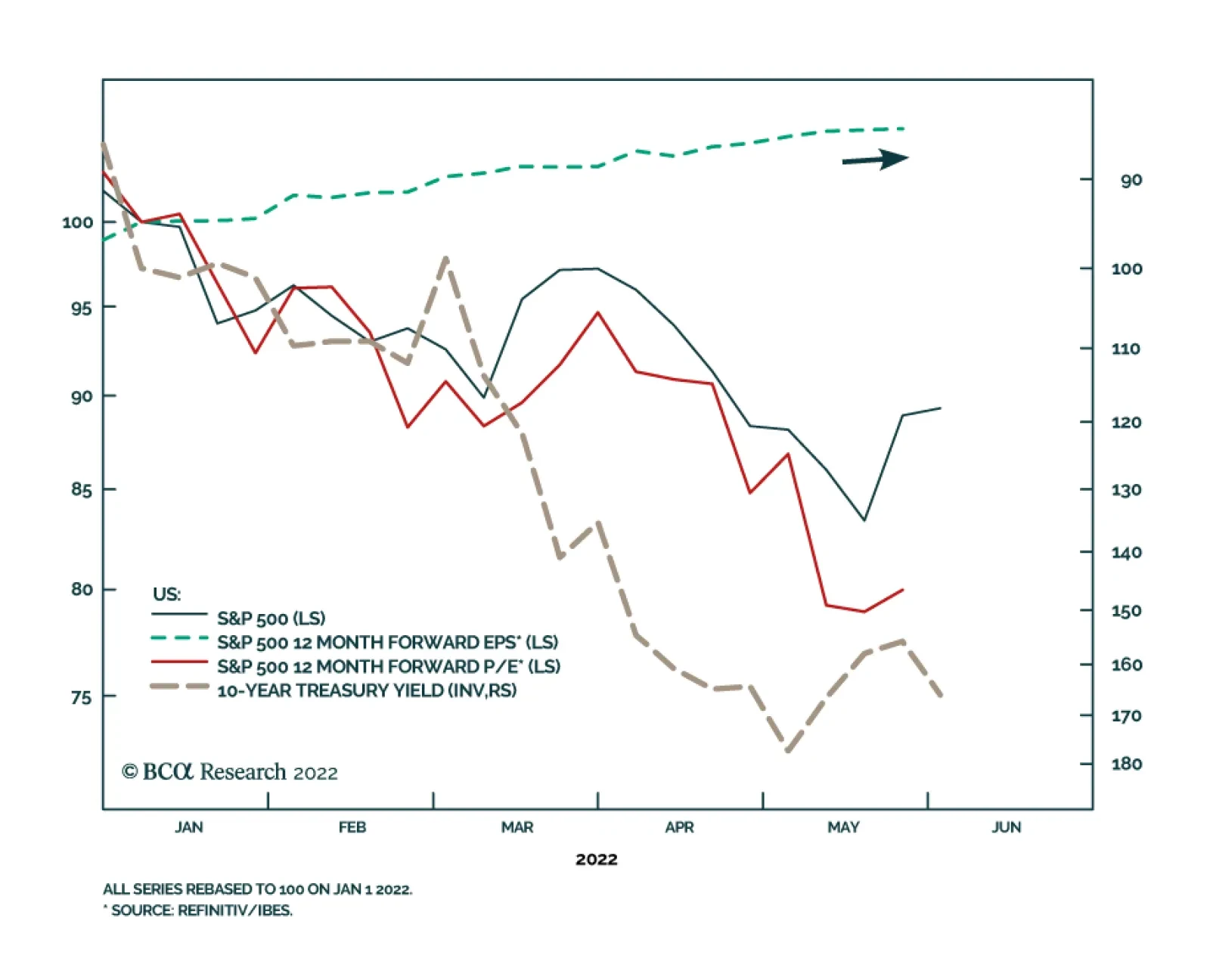

The S&P 500 has shed 13.8% since the beginning of the year on worries of a Fed-induced US recession, accelerating commodity prices and global growth slowdown. The selloff has been entirely valuation-driven. To the extent that Treasury yields provide…

The headline ISM Services index eased by 1.2 points in May to 55.9. This latest reading signals the slowest expansion in service sector activity since February 2021 and reflects a 4.6-point decline in the Business Activity component. However, details from…

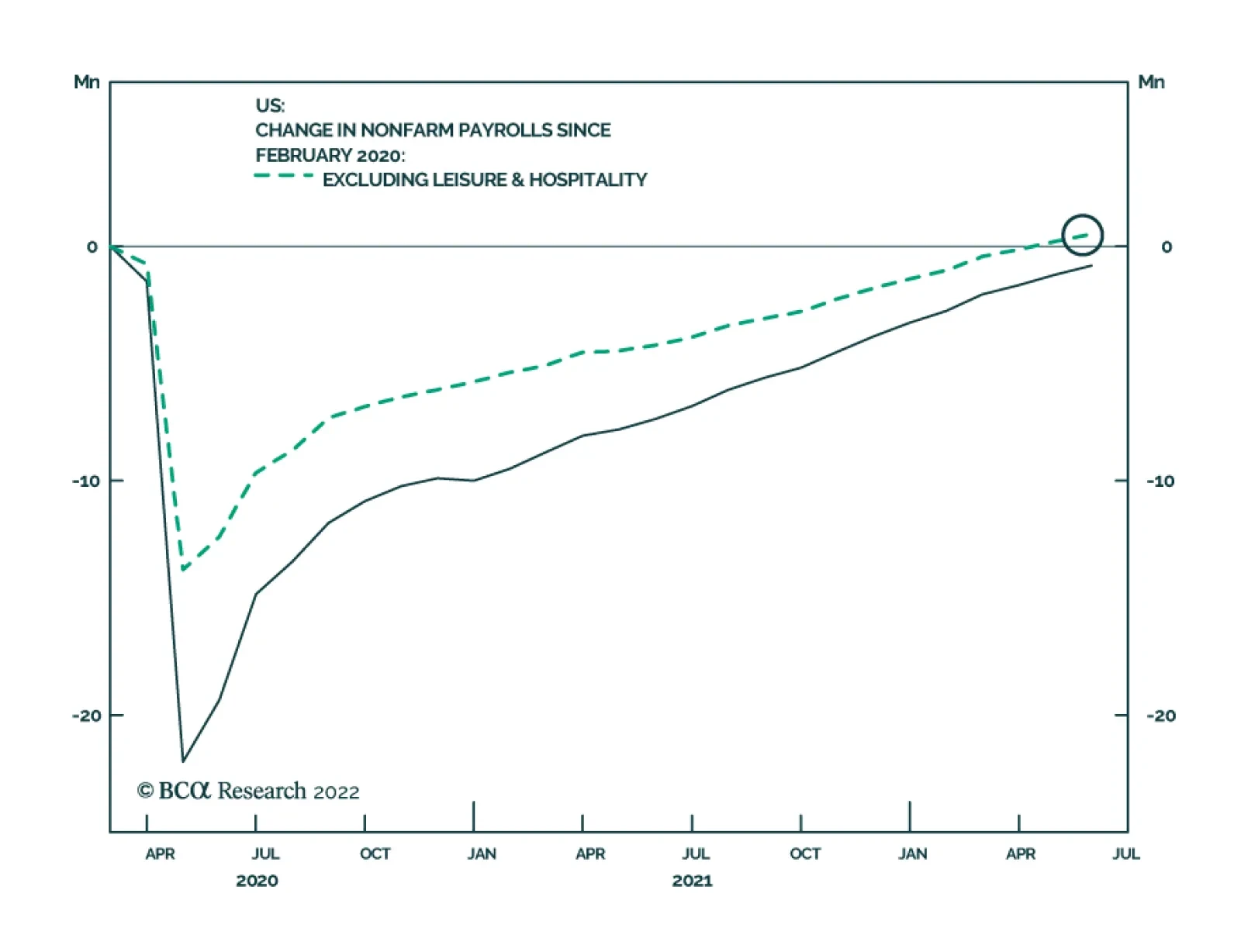

US nonfarm payrolls rose by 390 thousand in May, stronger than expectations of 318 thousand and down from an upwardly revised 436 thousand in April. The leisure and hospitality sector led the May payroll growth. Meanwhile manufacturing added 18 thousand jobs,…

US housing, one of the most interest-rate sensitive sectors of the economy, has cooled in line with the two-percentage point rise in mortgage rates. Housing market dynamics affect aggregate growth via the wealth effect it exerts on consumption as well as…

Executive Summary Return Of The 'Pocketbook Voter'

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

President Biden’s pledge to fight inflation ahead of the midterm elections got a boost with the Gulf Arab states pledging to increase oil production in July and August. Yet OPEC’s action should not be overrated. The Saudis are not clearly bailing out Biden … at least not yet. Biden’s other inflation-fighting tools are also limited. The Fed will hike rates, which will weigh on inflation, at least in the short run. A short-term moderation in inflation will cause big shifts in financial markets. It will not save the midterms for Democrats, but gridlock is disinflationary so the effect is the same. Inflation risks will persist over the long run. Recommendation (Cyclical) Inception Level Inception Date Return Small Vs. Large Cap Energy 0.6485 26-JAN-22 14.2% Oil And Gas Transportation And Storage Vs. S&P 500 0.0527 30-MAR-22 16.5% Bottom Line: Expect inflation to moderate in the short run. Oil prices will be volatile. Book a 14% profit on small cap versus large cap energy stocks and a 16.5% profit on the oil and gas transportation sub-sector relative to the broad market. Feature President Biden kicked off the summer – and the midterm election campaign – by defending his record thus far and pledging a three-pronged strategy to fight inflation. His options are limited but he received a boost from OPEC right off the bat. The bottom line is that disinflationary pressures are emerging. These include congressional gridlock, which is likely to return in January 2023. Biden’s policies will not save his party from a defeat in the midterms but moderating inflation will have huge investment consequences. Biden’s Three-Pronged Plan Consumer confidence is hurting while inflation eats away at real wage growth for Americans (Chart 1). Confidence is 14% higher than when Biden took office but 17.5% lower than when it peaked in June 2021. The latest survey from the Conference Board showed another decrease in May. This is foul weather for a ruling party that already stands to suffer a major check on its power when voters go to the polls in the fall. Biden’s approval rating is likely to stabilize but only at the current low level of 41.4%. Voters are focusing on the economy more than other issues like health care, the environment, or foreign affairs (Chart 2). Chart 1Consumer Confidence And Real Wages Tumble

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 2Return Of The 'Pocketbook Voter'

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

In the Wall Street Journal Biden laid out his party’s election pitch.1 First, he argued that the US economy is transitioning from rapid recovery to stable growth – i.e. that it is not going into recession. That would be good, but a recession is possible and the slowdown is politically deadly: Household Savings: Aggregate household savings have risen from $1Tn in 2019 to $3.9Tn today, which Biden cited as evidence of improving financial security. The problem is that inequality skews the picture and the average American is unlikely to feel secure. Low and middle income earners have depleted their savings or seen only a small increase (Chart 3). The Biden administration failed to improve inequality as promised while the uneven economic recovery means that lower-paid Americans do not have as much ability to buffer spending as the aggregate savings imply. They will be unhappy in November. Chart 3Normal Households No Longer Flush With Savings

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Jobs And Wages: Biden highlighted the role of his economic stimulus in lowering unemployment and argued that Americans have better paying jobs. But inflation has eroded real wages and incomes, as highlighted in Chart 1 above. Business Investment: Biden argued that business investment is brisk. But sentiment is turning. New orders of core capital goods have rolled over and capex intentions are falling (Chart 4). Manufacturing Comeback: Biden also touted the US manufacturing comeback, claiming that factory jobs are growing at fastest rate in 30 years. But again the tide is shifting against him, with the employment component of manufacturing purchasing manager indexes now signaling contraction (Chart 5). Biden, like Presidents Trump and Obama, has invested heavily in the “Buy America” re-industrialization narrative, so this trend is threatening. Chart 4Business Investment Setback

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 5Manufacturing Employment Weakening

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

A recession may indeed be avoided but the risk will not go away in time for the election. A recent study showed that at today’s extremely high level of inflation and extremely low level of unemployment, the odds of recession range from 60%-70% over the next 12-24 months.2 Second, Biden promised voters that he will fight inflation with all the powers of the White House. He laid out a three-pronged approach. However, his options are fairly limited and voters will not change their minds easily over the next five months: The Fed will hike rates: Biden argued that it is the Fed’s job to fight inflation and he will not interfere with rate hikes. While Biden offered admirable verbal support for an independent and non-partisan central bank, the truth is that real interest rates have not been this low since the highly politicized Fed chairmanship of Arthur Burns (Chart 6). While Biden has no reason to discourage rate hikes at the moment, he may change his tune as rates rise, growth slows, and the presidential election approaches. So may Powell, but by then it may be too late. In short, the Fed will hike, which will weigh on inflation, but it will not help Biden win voters this fall or avoid a recession by 2024. Congress will expand capacity: Biden argued that the bipartisan infrastructure bill that he signed into law and his other legislative proposals will boost the supply side of the economy. We are moderately optimistic about Congress’s ability to pass a party-line reconciliation bill that provides subsidies for the energy sector. This could pass under the consensus-building rubric of fighting Russia and climate change at the same time. But this measure, along with Biden’s Housing Supply Action Plan, child care and elderly care subsidies, and other proposals often look more like demand-side stimulus than supply-side reforms. They would fan inflation by increasing government spending and budget deficits. Moreover the administration cannot fix broken supply chains while China remains subject to strict Covid-19 lockdowns (Chart 7). In short, Congress may pass a reconciliation bill but it would be mildly stimulating for the economy (i.e. inflationary) and none of the supply-side improvements would reduce inflation in time for the midterms. Chart 6Biden Doesn't Need To Interfere With The Fed

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 7Supply Snarls Will Continue While China Struggles With Covid

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

The budget deficit will fall: Biden argued that budget consolidation will reduce inflation, pointing to this year’s estimated $1.7 trillion drop in the budget deficit and arguing that the deficit is falling lower than pre-pandemic levels. He also argued that robust tax revenues from the economic recovery justified his previous fiscal stimulus (the American Rescue Plan Act). However, the budget is merely normalizing from extreme pandemic heights – there have obviously not been any long-term fiscal reforms (Chart 8). If Congress passes a reconciliation bill then Biden may succeed at passing a minimum corporate tax, which would mark an important success. But while the fiscal drag is negative for inflation, it is also negative for the economy this year and for Biden’s party in the midterms, and long-term budget trends are inflationary. Chart 8No Sign Of Budget Control Over Long Run – Budget Deficits Are Inflationary

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

The takeaway is that the Fed’s actions are disinflationary. Congress may or may not pass a climate bill before the election, but if it does, the budget deficit will be the same or larger and the economy will be the same or slightly stimulated. In brief Biden’s anti-inflation plan is to avoid interfering at the Fed. Extremely low unemployment will not save Biden and the Democrats this election season, any more than it saved Trump and the Republicans in 2018 (Chart 9). The Fed will rein in inflation at least in the short run. The election will lead to gridlock, which will freeze fiscal policy. Bottom Line: Inflation expectations will moderate but not because of any supply-side reform or fiscal consolidation coming from the Biden administration this year. Chart 9Low Unemployment Will Not Save Democrats

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Will Biden Ease Russian Energy Tensions? No. Biden’s other avenues for reducing inflation – not addressed in his editorial – lie in the foreign policy realm. The Biden administration is turning toward foreign policy as gridlock settles over Capitol Hill. Biden’s foreign policy will be insular, reactive, and focused on the midterm elections. Could Biden facilitate ceasefire talks in Ukraine so as to ease energy pressures stemming from Russia? The short answer is no. Biden imposed an oil embargo on Russia and ultimately agreed to the EU’s embargo. Biden can afford to run large risks with Russia this year because a larger confrontation or crisis with Russia would not hurt the Democrats in the midterm elections. Indeed the best hope for the Democrats is to recreate the 1962 congressional election, when John F. Kennedy stared down Soviet leader Nikita Krushchev in the Cuban Missile Crisis in October just before the election. Kennedy’s Democrats lost four seats in the House, gained four in the Senate, and kept control of both. Biden’s approval rating is nowhere near Kennedy’s but his party’s outlook is bad enough that he may be willing to run the risk of a crisis that could lead to a favorable rally-around-the-flag effect in the fall (Chart 10). Biden’s clearance this week of the highly mobile artillery rocket system for Ukraine – despite the risk that Ukrainians would launch attacks into Russian territory – underscores this point. Bottom Line: Biden will not ease tensions with Russia ahead of the midterm to try to reduce energy prices. Chart 10Biden Can Risk A Bigger Russia Crisis

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Will Biden Lower China Tariffs? No. What about China – will Biden ease the Trump administration’s tariffs on China to reduce inflation before the midterm election? Treasury Secretary Janet Yellen has repeatedly signaled support for this idea. The Trump administration marked a historic increase in US tariffs and the Biden administration has so far offered relief only for US allies (Chart 11). Again the short answer is no. Protectionist sentiment will prevail during midterm election season and US voters have turned decisively unfavorable toward China in recent years (Chart 12). The China tariffs have not been the driver for US inflation so tariff relief would bring minimal price relief while exacting a high political cost of making Biden look weak, wishy-washy on his pro-democracy values, and (according to Republicans) corrupt. Biden would be offering unilateral benefits to China without gaining Chinese trade concessions. Chart 11Biden Keeps Trump's Tariffs On China

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 12Protectionist Sentiment To Prevail Amid Midterms

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Recently the Biden administration gave some indications of where it stands on China policy. Biden visited US allies in Asia Pacific and provoked China over the Taiwan Strait. Secretary of State Antony Blinken unveiled the administration’s comprehensive China policy and declared that the US would remain focused on China as the “most serious long-term challenge” despite Russia’s open belligerence in Europe.3 On paper, US-China trade relations do not look that bad. While China is falling short of its Phase One trade deal import promises, the truth is that a global recession intervened – and those promises were made under duress when the US slapped sweeping sanctions on Chinese exports. The commodity trade is booming, as is to be expected amid global energy shortages (Chart 13). The problem is that neither the US nor China has the domestic political capital to offer structural concessions in the short run, while both sides are girding for a century-long power struggle over the long run. Supply insecurity will result in the commodity trade suffering as a vast global substitution effect takes place. This is due to Russia’s energy breakup with Europe, growing Russia-China trade linkages, and ongoing US-China tensions. Global trade and US-China trade are set to slow, while China’s surge in energy imports from the US will abate for reasons of state security. Chart 13US-China Trade Faces Strategic Limits

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Bottom Line: No reduction in US tariffs on China is likely. Any reduction will have minimal macroeconomic effects and will be replaced by other punitive measures, given the underlying strategic competition and protectionist election politics. Meanwhile China’s “Zero Covid” policy will weigh on trade ties and sustain price pressures in the short run, as mentioned. Will Biden Lift Iran Sanctions? Probably Not. What about the Middle East? Can Biden convince the core OPEC states to pump more oil in lieu of Russian production? Or can Biden lift sanctions on Iran to undercut soaring gasoline prices? On this front Biden received welcome news on June 2 when Gulf Arab states promised to increase production by 638,000 barrels per day in July and August, up from an expected 430,000. At the same time news broke that Biden will visit Saudi Arabia, including potentially Crown Prince Mohammed bin Salman (MBS), and other Gulf partners sometime in June. There is not yet a clear understanding between Biden and MBS but it is possible that one will develop. The trigger for OPEC’s declaration is the EU oil embargo on Russia. EU is finalizing an embargo on 90% of oil imports – everything except the oil flowing through the Southern Druzhba pipeline to land-locked eastern European states. The embargo will impair Russian energy production: it could fall by as much as 2-3 million barrels per day, distribution interruptions will occur as Russia transitions to Asian buyers, and Russia’s long-term production capacity could be damaged. The result could be a destabilizing price spike. While the core OPEC states have just enough spare capacity to cover that gap in theory (Chart 14), they will not want to commit all spare capacity at once. Chart 14OPEC Spare Capacity

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

There is still a lot of uncertainty about how rapidly the embargo will be enforced, how much Russian production will suffer, whether the OPEC states will meet these new production increases (all except Saudi have been falling short), and what will be the OPEC policy beyond August. But for now it is clear that the Gulf Arab states are helping the US and EU by signaling some extra supplies at a critical time. The Gulf Arabs benefit from high oil prices and have previously ignored the G7’s pleas to increase production. But they also need to prolong the business cycle – a cycle-killing price shock from Russia is not in their interest. They are interested in keeping up revenues, maintaining domestic stability, and maintaining their position as the gatekeepers of the global oil supply and price. Secondarily, they are interested in maintaining close relations with the US, which guarantees their national security. OPEC supply easing at this juncture is obviously beneficial to Biden ahead of the US midterm election in November. But there is not yet an understanding on this front because the US is also negotiating to rejoin the 2015 nuclear agreement with Iran, which Saudi Arabia and the Gulf states oppose. Biden’s trip to the Gulf suggests that nothing is settled yet. The OPEC production increase is not proof alone that the US is breaking off talks with Iran. If the Gulf states thought the US were going to strike a deal with Iran, they might produce more oil to preempt the deal and grab more market share, which is what they did in 2014 in advance of the original 2015 US-Iran nuclear deal. The Saudis do not want US shale producers and Iranian exporters to form an unholy alliance that steals market share and compromises Saudi security. Still, we expect the US-Iran deal to fall apart. The Biden administration does not have a unified international coalition to enforce sanctions on Iran. Nor does it have the political capital or longevity to give Iran credible security guarantees that would convince it to freeze its nuclear program. Recent events support our view. The UN atomic watchdog says that Iran’s stockpile of highly enriched uranium has risen by 30% in three months. Meanwhile the US seized an Iranian tanker off Greece, Iran seized two Greek tankers, and Greece warned about dangers to shipping in the Persian Gulf. To develop a better understanding between Biden and MBS, the US needs to assure the Saudis that it will not renew the deal with Iran. The Saudis will not provide oil at Biden’s whim but they may provide if they have satisfaction that the US will scrap the deal, or otherwise compensate them, such as through increased defense assistance (which Biden threatened to cut off when he entered office). Investors should expect OPEC to fall short of its current promises – and yet to try to provide the minimum production increases necessary to prevent a destabilizing oil spike. OPEC’s interest is to make a windfall for as long as possible, which means not killing the cycle out of greed. This policy could be positive for oil prices after the immediate downward price adjustment. But for now investors should merely expect oil volatility as the EU’s embargo enforcement, Russian retaliation, Russian oil production, OPEC implementation, and US sanctions on Iran are all up in the air. A successful US-Iran deal would deepen the drop in oil prices. But odds are 60/40 that that deal will fail, leading to an escalation of tensions in the Middle East. Biden will have to underscore the US’s red line against Iranian nuclear weaponization. Oil supply disruptions will increase in frequency across the region. Bottom Line: OPEC has given Biden’s anti-inflation campaign a boost but it is too soon to declare that oil prices will substantially abate. The US-Iran deal will likely fail, increasing Middle Eastern instability and supply risks. Investment Takeaways Given that we expect continued volatility in the oil space, we are booking a 14% gain on our long small cap energy versus large cap energy trade. We are also booking a 16.5% gain on our overweight position in the oil and gas transportation and storage sub-sector. We will revisit these trades in future reports. Overall we maintain a defensive portfolio strategy. Biden’s anti-inflation campaign is meeting with some success in the Middle East but the US confrontation with Russia and the likely failure of US-Iran talks suggests that price spikes can still kill more demand and lead to further growth upsets. Matt Gertken Senior Vice President Chief US Political Strategist mattg@bcaresearch.com Footnotes 1 See Joseph R. Biden, Jr, “Joe Biden: My Plan for Fighting Inflation,” Wall Street Journal, May 30, 2022, wsj.com. 2 See Lawrence H. Summers and Alex Domash, “History Suggests a High Chance of Recession over the Next 24 Months,” Harvard Kennedy School, March 15, 2022, www.hks.harvard.edu. 3 See Antony J. Blinken, “The Administration’s Approach to the People’s Republic of China,” US Department of State, May 26, 2022, state.gov. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A3US Political Capital Index

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart A1Presidential Election Model

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart A2Senate Election Model

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A4House Election Model

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A5APolitical Capital: White House And Congress

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A5BPolitical Capital: Household And Business Sentiment

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A5CPolitical Capital: The Economy And Markets

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Executive Summary Investors face a dilemma. The faster that inflation comes down, the better it will be for valuations via a stronger rally in the bond price. But if a collapse in inflation requires a sharp deceleration in growth, the worse it will be for profits. Bond yields are likely in a peaking process, but the sharpest declines may come a few months down the road, after an unambiguous roll-over in food and energy inflation. The stock market’s valuation-driven sell-off is likely over, but the danger is that it morphs into a profits-driven sell-off. As such, the stock market will remain under pressure through 2022, though it is likely to be higher 12 months from now in June 2023. High conviction recommendation: Overweight healthcare versus basic resources. In other words, tilt towards sectors that benefit the most from rising bond prices and that suffer the least from contracting profits. New high conviction recommendation: Go long the Japanese yen. As bond yield differentials re-tighten, the yen will rally. Additionally, the yen will benefit from its haven status in a period of recessionary risk. Fractal trading watchlist: JPY/USD, GBP/USD, and Australian basic resources. If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

Bottom Line: The risk is that the valuation-driven sell-off morphs into a profits-driven sell-off. Feature In May, many stock markets reached the drawdown of 20 percent that defines a technical bear market. Yet what has caught many people off guard is that the bear market in stocks has happened during a bull market in profits. Since the start of 2022, US profits are up by 5 percent.1 The bear market in stocks has happened during a bull market in profits… so far. This shatters the shibboleth that bear markets only happen when there is a profits recession. The 2022 bear market has been a valuation-driven bear market. US profits rose 5 percent, but the multiple paid for those profits collapsed by 25 percent, taking the market into bear territory. None of this should come as any surprise to our regular readers. As we have pointed out many times, a stock market can be likened to a bond with a variable rather than a fixed income. So, just as with a bond, every stock market has a ‘duration’ which establishes which bond it most behaves like. It turns out that that long-duration US stock market has the same duration as a 30-year bond. This means that: The US stock market = (The 30-year T-bond price) multiplied by (US profits) It follows that if the 30-year bond price falls by more than profits rise, then the stock market will sell off. And if the 30-year bond price falls by much more than profits rise, then the stock market will enter a valuation-driven bear market. Therein lies the story of 2022 so far (Chart I-1). Chart I-1The Bear Market Is Valuation-Driven. Profits Are Up... For Now

The Bear Market Is Valuation-Driven. Profits Are Up... For Now

The Bear Market Is Valuation-Driven. Profits Are Up... For Now

Just As In 1981-82, Will The Sell-Off Morph From Valuation-Driven To Profits-Driven? In Markets Echo 1981, When Stagflation Morphed Into Recession, we argued that a good template for what happens to the economy and the markets in 2022-23 is the experience of 1981-82. Does 2022-23 = 1981-82? Then, just as now, the world’s central banks were obsessed with ‘breaking the back’ of inflation, and piloting the economy to a ‘soft landing’. Then, just as now, the central banks were desperate to repair their badly damaged credibility in managing the economy. And then, just as now, an invasion-led war between two major commodity producers – Iran and Iraq – was disrupting commodity supplies and adding to inflationary pressures. In 1981, just as now, the equity market sell-off started as a valuation sell-off, driven by a declining 30-year T-bond price. Profits held up through most of 1981, just as they have so far in 2022. In September 1981, US core inflation finally peaked, with bond yields following soon after. In the current experience, March 2022 appears to have marked the equivalent peak in US core inflation (Chart I-2 and Chart I-3). Chart I-2Does September 1981...

Does September 1981...

Does September 1981...

Chart I-3...Equal March 2022?

...Equal March 2022?

...Equal March 2022?

In late 1981, when the 30-year T-bond price rebounded, the good news was that beaten-down equity valuations also reached their low point. The bad news was that just as the valuation-driven sell-off ended, profits keeled over, and the valuation-driven sell-off morphed into a profits-driven sell-off (Chart I-4). In 2022-23, could history repeat? Chart I-4In September 1981, The Sell-Off Morphed From Valuation-Driven To Profits-Driven

In September 1981, The Sell-Off Morphed From Valuation-Driven To Profits-Driven

In September 1981, The Sell-Off Morphed From Valuation-Driven To Profits-Driven

Recession Or No Recession? That Is Not The Question History rhymes, it rarely repeats exactly. What if the 2022-23 experience can avoid the outright economic recession of the 1981-82 experience? This brings us to another shibboleth that needs to be shattered. You don’t need the economy to go into recession for profits to go into recession. To understand why, we need to visit the concept of operational leverage. Profits is a small number that comes from the difference of two large numbers: sales and the costs of generating those sales. As any company will tell you, sales can be volatile, but costs – which are dominated by wages – are sticky and much slower to change. The upshot is that if sales growth exceeds costs growth, there is a massively leveraged impact on profits growth. This is the magic of operational leverage. But if sales growth falls below sticky cost growth, the magic turns into a curse. The operational leverage goes into reverse, and profits collapse. Using US stock market profits as an example, the magic turns into a curse at real GDP growth of 1.25 percent, above which profits grow at six times the difference, and below which profits shrink at six times the difference (Chart I-5). Chart I-5A Model For US Profits Growth: (Real GDP Growth - 1.25) Times 6

A Model For US Profits Growth: (Real GDP Growth - 1.25) Times 6

A Model For US Profits Growth: (Real GDP Growth - 1.25) Times 6

Strictly speaking, we should compare US profits growth with world GDP growth because multinationals generate their sales globally rather than domestically. But to the extent that the US has both the world’s largest stock market and the world’s largest economy, it is a reasonable comparison. We should also compare both profits and sales in either nominal or real terms, rather than a mixture. But even with these tweaks, we would still find that the dominant driver of profit growth is operational leverage. ‘Recession or no recession?’ is a somewhat moot question, because even non-recessionary low growth is enough to tip profits into contraction. Therefore, the conclusion still stands – ‘recession or no recession?’ is a somewhat moot question, because even non-recessionary low growth is enough to tip profits into contraction. Such a period of low growth is now likely. If 2022-23 = 1981-82, What Happens Next? To repeat: The US stock market = (The 30-year T-bond price) multiplied by (US profits) This means that investors face a dilemma. The faster that inflation comes down, the better it will be for valuations via a stronger rally in the bond price. But if a collapse in inflation requires a sharp deceleration in growth, the worse it will be for profits. This was the precise set-up in December 1981, the equivalent of June 2022 in our historical template. In which case, what can we expect next? 1. Bond yields are likely in a peaking process, but the sharpest declines may come a few months down the road, after an unambiguous roll-over in food and energy inflation (Chart I-6). Chart I-6If 2022-23 = 1981-82, Then This Is What Happens To The Bond Yield

If 2022-23 = 1981-82, Then This Is What Happens To The Bond Yield

If 2022-23 = 1981-82, Then This Is What Happens To The Bond Yield

2. The stock market’s valuation-driven sell-off is likely over, but the danger is that it morphs into a profits-driven sell-off. As such, the stock market will remain under pressure through 2022, though it is likely to be higher 12 months from now in June 2023 (Chart I-7). Chart I-7If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

3. Long-duration defensive sectors will outperform short-duration cyclical sectors. In other words, tilt towards sectors that benefit the most from rising bond prices and suffer the least from contracting profits. As such, a high conviction recommendation is to overweight healthcare versus basic resources (Chart I-8). Chart I-8If 2022-23 = 1981-82, Then This Is What Happens To Healthcare Versus Resources

If 2022-23 = 1981-82, Then This Is What Happens To Healthcare Versus Resources

If 2022-23 = 1981-82, Then This Is What Happens To Healthcare Versus Resources

4. In foreign exchange, the setup is very bullish for the Japanese yen through the next 12 months. The yen’s recent sell-off is explained by bond yields rising outside Japan. As these bond yield differentials re-tighten, the yen will rally. Additionally, the yen will benefit from its haven status in a period of recessionary risk. A new high conviction recommendation is to go long the Japanese yen (Chart I-9). Chart I-9The Yen's Sell-Off Is Due To Bond Yields Rising Outside Japan

The Yen's Sell-Off Is Due To Bond Yields Rising Outside Japan

The Yen's Sell-Off Is Due To Bond Yields Rising Outside Japan

Fractal Trading Watchlist Supporting our bullish fundamental case for the Japanese yen, the sell-off in JPY/USD has reached the point of fragility on its 260-day fractal structure that marked previous major turning points in 2013 and 2015 (Chart 10). Hence, a first new trade is long JPY/USD, setting the trade length at 6 months, and the profit target and symmetrical stop-loss at 5 percent. Chart I-10The Sell-Off In JPY/USD Has Reached A Potential Turning Point

The Sell-Off In JPY/USD Has Reached A Potential Turning Point

The Sell-Off In JPY/USD Has Reached A Potential Turning Point

Supporting our bearish fundamental case for resources stocks, the outperformance of Australian basic resources has reached the point of fragility on its 130-day fractal structure that marked previous turning points in 2013, 2015, and 2021 (Chart I-11). Hence, a second new trade is short Australian basic resources versus the world market, setting the trade length at 6 months, and the profit target and symmetrical stop-loss at 10 percent. Chart I-11The Australian Basic Resources Sector Is Vulnerable To Reversal

The Australian Basic Resources Sector Is Vulnerable To Reversal

The Australian Basic Resources Sector Is Vulnerable To Reversal

Finally, we are adding GBP/USD to our watchlist, given that its 260-day fractal structure is close to the point of fragility that marked major turns in 2014, 2015, and 2016. Our full watchlist of 29 investments that are at, or approaching turning points, is available on our website: cpt.bcaresearch.com Fractal Trading Watchlist: New Additions GBP/USD At A Turning Point

GBP/USD At A Turning Point

GBP/USD At A Turning Point

Chart 1AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart 2Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Chart 3Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart 4US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

Chart 5BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart 6Homebuilders Versus Healthcare Services Has Turned

Homebuilders Versus Healthcare Services Has Turned

Homebuilders Versus Healthcare Services Has Turned

Chart 7CNY/USD Has Reversed

CNY/USD Has Reversed

CNY/USD Has Reversed

Chart 8CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart 9Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Chart 10The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

Chart 11The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart 12FTSE100 Outperformance Vs. Euro Stoxx 50 Is Reversing

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Reversing

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Reversing

Chart 13Netherlands Underperformance Vs. Switzerland Has Been Exhausted

Netherlands Underperformance Vs. Switzerland Has Been Exhausted

Netherlands Underperformance Vs. Switzerland Has Been Exhausted

Chart 14The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

Chart 15The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

Chart 16Food And Beverage Outperformance Has Been Exhausted

Food And Beverage Outperformance Has Been Exhausted

Food And Beverage Outperformance Has Been Exhausted

Chart 17The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 18The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart 19A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 20Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 21Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart 22Cotton Versus Platinum Is Reversing

Cotton Versus Platinum Is Reversing

Cotton Versus Platinum Is Reversing

Chart 23Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Chart 24The Rally In USD/EUR Has Ended

The Rally In USD/EUR Has Ended

The Rally In USD/EUR Has Ended

Chart 25The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

Chart 26A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 27Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Chart 28US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

Chart 29GBP/USD At A Turning Point

GBP/USD At A Turning Point

GBP/USD At A Turning Point

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Defined as 12-month forward earnings per share. Fractal Trading System

More On 2022-23 = 1981-82, And The Danger Ahead

More On 2022-23 = 1981-82, And The Danger Ahead

More On 2022-23 = 1981-82, And The Danger Ahead

More On 2022-23 = 1981-82, And The Danger Ahead

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

According to BCA Research’s Global Asset Allocation service, the jury is out on the probability of a recession – and is likely to stay out for a while. Global equities will probably move sideways, with significant volatility. Equity markets – with US…