United States

BCA Research’s Global Investment Strategy service concludes that US financial conditions have tightened by enough that the Fed no longer needs to talk up interest rate expectations. Like many central banks, the Fed sees financial conditions as a key driver…

Listen to a short summary of this report. Executive Summary US Financial Conditions Have Tightened Significantly This Year

US Financial Conditions Have Tightened Significantly This Year

US Financial Conditions Have Tightened Significantly This Year

US financial conditions have tightened by enough that the Fed no longer needs to talk up interest rate expectations. If inflation decelerates faster than anticipated over the coming months, as we expect will be the case, the Fed’s messaging will soften further. Bond yields in the US and abroad are likely to fall over the next 6-to-12 months, even if they do rise over a longer-term horizon. Stay overweight stocks, favoring non-US equities over their US peers. We are closing our short 10-year Gilts trade, initiated at a yield of 0.85%, for a gain of 7.5%. We are also opening a new trade going long Canadian short-term interest rate futures versus their US counterparts. Investors expect Canadian rates to exceed US rates in 2024, which seems unlikely to us given that the Canadian housing market is much more sensitive to higher rates than the US market. Bottom Line: After having tightened significantly over the past seven months, financial conditions should loosen modestly during the remainder of the year. This should benefit risk assets. Fed Focused on Financial Conditions Chart 1Tighter Financial Conditions Will Hurt Growth

Tighter Financial Conditions Will Hurt Growth

Tighter Financial Conditions Will Hurt Growth

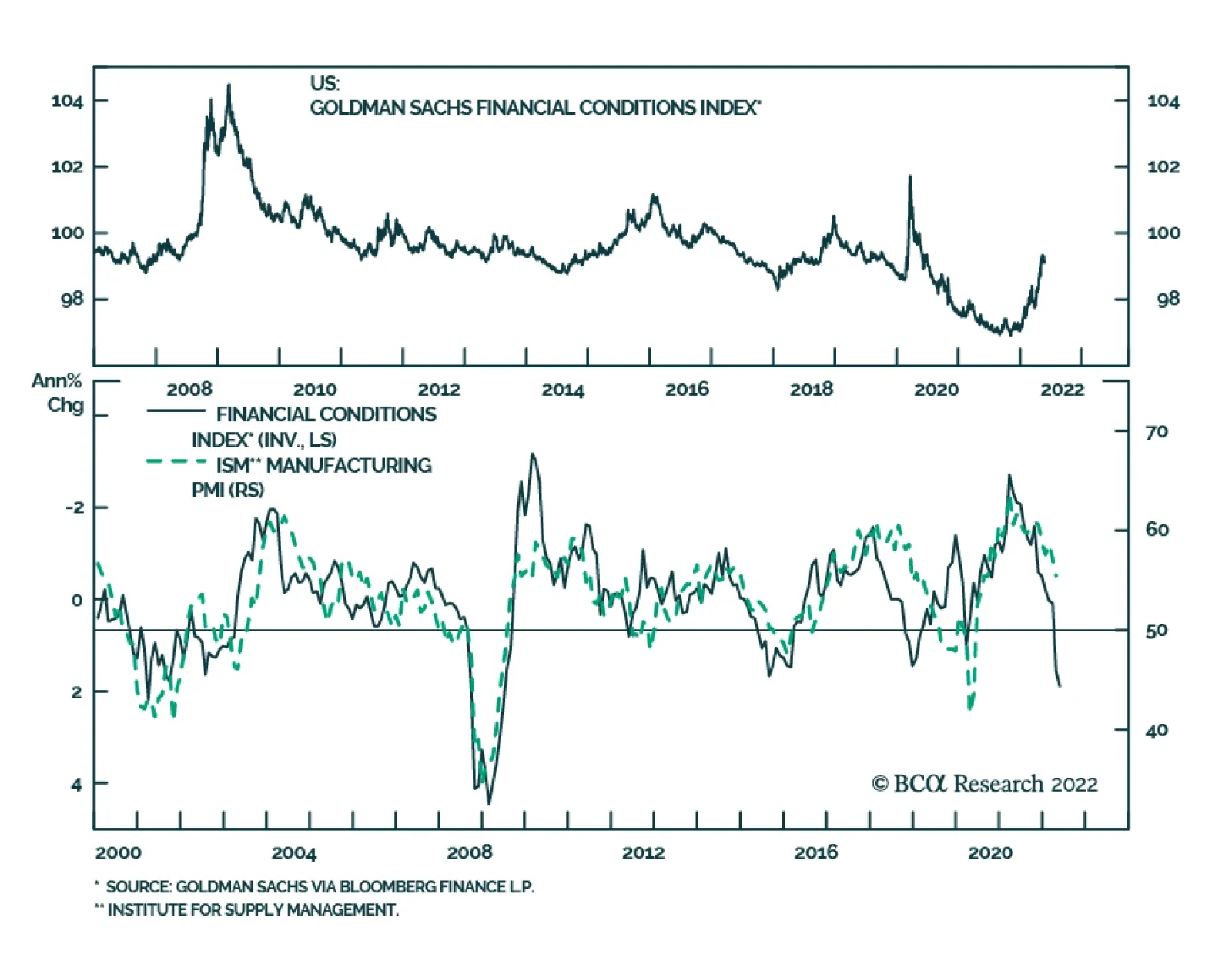

Like many central banks, the Fed sees financial conditions as a key driver of the real economy. While there are many financial conditions indices (FCIs), most include bond yields, credit spreads, equity prices, and the exchange rate as inputs. Higher bond yields, wider credit spreads, lower equity prices, and a strong currency all lead to tighter financial conditions and a weaker economy, and vice versa. Goldman’s US FCI is especially popular among market participants. It is calibrated so that 100 bps in tightening corresponds, all things equal, to a 100 basis-point decline in US real GDP growth over the subsequent four quarters. The Goldman FCI has tightened by 212 bps since the start of the year and by 225 points from its loosest level in November 2021. If the historic relationship between the FCI and the economy holds, the tightening in financial conditions would be enough to push US growth to a below-trend pace by the second quarter of 2023. In fact, the tightening in the Goldman FCI over the past 12 months already suggests that the manufacturing ISM will fall below 50 (Chart 1). Along the same lines, the Chicago Fed’s Adjusted National FCI, which measures financial conditions relative to current economic conditions, has moved slightly into restrictive territory. Aside from a brief period at the outset of the pandemic, the index has been consistently in expansionary territory since early 2013 (Chart 2). Chart 2The Chicago Fed Financial Conditions Index Has Moved Into Slightly Restrictive Territory

Are Financial Conditions Tight Enough?

Are Financial Conditions Tight Enough?

Other data are consistent with the message from the FCIs. Most notably, growth estimates for the US and for other major economies have come down over the past few months (Chart 3). Economic surprise indices have also fallen, especially in the US. Chart 3AGrowth Forecasts Have Softened As Economic Data Have Surprised To The Downside (I)

Growth Forecasts Have Softened As Economic Data Have Surprised To The Downside (I)

Growth Forecasts Have Softened As Economic Data Have Surprised To The Downside (I)

Chart 3BGrowth Forecasts Have Softened As Economic Data Have Surprised To The Downside (II)

Growth Forecasts Have Softened As Economic Data Have Surprised To The Downside (II)

Growth Forecasts Have Softened As Economic Data Have Surprised To The Downside (II)

Mission Accomplished? Chart 4The Fed Expects To Lift Rates Above Its Estimate Of Neutral

The Fed Expects To Lift Rates Above Its Estimate Of Neutral

The Fed Expects To Lift Rates Above Its Estimate Of Neutral

Given the recent tightening in financial conditions and weaker growth expectations, the Fed is likely to soften its tone. Already this week, Atlanta Fed President Raphael Bostic suggested that the Fed could pause raising rates in September in order to assess the impact of the Fed’s tightening campaign. The Fed minutes also conveyed a sense of flexibility and data-dependence about the timing and magnitude of future hikes once rates reach 2%. It’s worth stressing that the Fed expects rates to rise in 2023 to about 40 bps above its estimate of the terminal rate (Chart 4). Jawboning rate expectations higher would potentially undermine the Fed’s goal of achieving a soft landing for the economy. Inflation Will Dictate How Much Easing Lies Ahead There is a big difference between not wanting financial conditions to tighten further and wanting them to loosen. The Fed would only want to see an easing in financial conditions if inflation were to fall faster than expected. Chart 5 shows how the year-over-year change in the core PCE deflator would evolve over the remainder of the year depending on different assumptions about the month-over-month change in the deflator. The Fed would be able to reach its expectation of year-over-year core PCE inflation of 4.1% for end-2022 if the month-over-month change averages 0.33%. Monthly core PCE inflation averaged 0.3% in February and March and is expected to clock in at around the same level for April once the data is released tomorrow. Chart 5AUS Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.3% (I)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.3% (I)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.3% (I)

Chart 5BUS Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.3% (II)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.3% (II)

US Inflation Will Fall By More Than The Fed Expects If The Monthly Change In Core PCE Is Less Than 0.3% (II)

Regardless of tomorrow’s data print, as we discussed last week, we expect the monthly inflation rate to average less than 0.3 in the back half of the year. If that happens, inflation will surprise to the downside relative to the Fed’s expectations. Consistent with the observation above, market-based inflation expectations have already declined. The 5-year TIPS inflation breakeven has fallen from 3.64% in March to 2.98% at present. The widely watched 5-year/5-year forward breakeven rate is back down to 2.29%, at the bottom of the Fed’s comfort zone of 2.3%-to-2.5% (Chart 6).1 The Citi US Inflation Surprise Index has also rolled over (Chart 7). Chart 6Market-Based Inflation Expectations Have Come Down Of Late

Market-Based Inflation Expectations Have Come Down Of Late

Market-Based Inflation Expectations Have Come Down Of Late

Chart 7The US Inflation Surprise Index Has Rolled Over

The US Inflation Surprise Index Has Rolled Over

The US Inflation Surprise Index Has Rolled Over

Financial Conditions Abroad Financial conditions indices in the other major developed economies have tightened somewhat less than in the US because equities represent a smaller share of household net worth abroad and also because most currencies have weakened against the US dollar (Chart 8). Nevertheless, with growth momentum having already deteriorated sharply, central banks are signaling a more balanced approach towards policy normalization. Chart 8Financial Conditions Have Tightened More In The US Than Elsewhere This Year

Are Financial Conditions Tight Enough?

Are Financial Conditions Tight Enough?

ECB: Wait and See? In a blog post published on Monday, Christine Lagarde observed that inflation expectations have risen from pre-pandemic levels, implying that real policy rates are currently lower than they were two years ago. In her mind, this warrants ending net purchases under the Asset Purchase Programme early in the third quarter. It also warrants raising the deposit rate by 25 bps at both the July and September meetings, bringing it back to zero from -0.5% at present. Beyond then, Lagarde was circumspect about what should be done, stressing the need for “gradualism, optionality and flexibility.” She noted that “The euro area is clearly not facing a typical situation of excess aggregate demand or economic overheating … Both consumption and investment remain below their pre-crisis levels, and even further below their pre-crisis trends.” She then added: “The outlook is now being clouded by the negative supply shocks hitting the economy … households’ expectations of their future financial situation dropped to their second-lowest level on record in March and remained close to that level in April.” The market expects the ECB to raise rates by 170 bps over the next 12 months, bringing the deposit rate to 1.2% by mid-2023 (Chart 9). BCA’s Global Fixed Income team, led by Rob Robis, foresees only 50 bps of tightening over the next 12 months. Chart 9Markets Expect Rates To Rise The Most In The Anglo-Saxon World

Are Financial Conditions Tight Enough?

Are Financial Conditions Tight Enough?

The UK, Canada, and Australia: Frothy Housing Markets Will Limit Rate Hikes The Bank of England (BoE) hiked rates by 90 bps over the past 12 months. The UK OIS curve is priced for another 140 bps of rate hikes over the next year. According to the BoE’s forecasting models, this would raise the unemployment rate by two percentage points while lowering inflation to below 2% within the next two-to-three years. In our opinion, that is more tightening than the BoE would like to see. BCA’s strategists expect the BoE to deliver only another 75 bps of hikes over the next year. Chart 10Buildup In Leverage And Frothy Housing Markets Pose A Challenge To Monetary Policy In Some Developed Market Countries

Buildup In Leverage And Frothy Housing Markets Pose A Challenge To Monetary Policy In Some Developed Market Countries

Buildup In Leverage And Frothy Housing Markets Pose A Challenge To Monetary Policy In Some Developed Market Countries

The Canadian economy has been quite strong, with the unemployment rate falling to 5.2% in April, the lowest since 1974. The Canadian OIS curve is discounting 195 bps of interest rate hikes over the next 12 months, substantially more than the 150 bps of tightening our fixed income team foresees. By mid-2024, investors expect Canadian policy rates to be about 25 bps above US rates. This seems unreasonable to us, and as of this week, we are expressing this view by going long the June 2024 3-month Canadian Bankers’ Acceptance (BAX) futures contract (BAM4) versus the corresponding 3-month US SOFR futures contract (SFRM4). A more liquid option is to simply go long the 10-year Canadian government bond versus the 10-year US Treasury note. At present, Canadian 10-year government bonds are yielding 5 bps more than their US counterparts. Unlike in the US, where household debt has fallen over the past 14 years, debt in Canada has risen, fueled by a massive housing boom (Chart 10). High indebtedness and the prevalence of variable rate/short-term fixed-rate mortgages will limit the ability of the BoC to raise rates. The Australian OIS curve is currently discounting 262 bps of rate hikes over the next year which, if realized, would take the cash rate to 3.3% – a level last seen in 2013 when the neutral rate in Australia was much higher by the RBA’s own reckoning. BCA’s fixed income strategists expect only 150 bps of tightening over the next 12 months. Japan: Yield Curve Control Will Continue Chart 11Japan: Long-Term Inflation Expectations Are Far Lower Than In The Rest Of The World

Japan: Long-Term Inflation Expectations Are Far Lower Than In The Rest Of The World

Japan: Long-Term Inflation Expectations Are Far Lower Than In The Rest Of The World

The Bank of Japan expects inflation excluding fresh food prices to remain at about 2% in the second half of 2022, but then to slow to 1.1% in the fiscal year starting April 2023. The Japan OIS curve is discounting almost no tightening over the next 12 months. Long-term inflation expectations are far lower in Japan than in any other major economy, which makes ultra-low rates a necessity for the foreseeable future (Chart 11). China: Outright Easing Chart 12Covid Restrictions Have Eased Only Modestly In China

Are Financial Conditions Tight Enough?

Are Financial Conditions Tight Enough?

China faces a trifecta of problems: A weakening housing market; slowing external demand for manufactured goods; and the ongoing threat of Covid-related lockdowns. Despite a steep drop in the number of new Covid cases over the past month, China’s lockdown index has only eased modestly, as the authorities continue to fret about the next outbreak (Chart 12). The leadership in Beijing has responded with policy easing. The PBoC lowered the 5-year loan prime rate by 15 bps last week, the largest such cut since 2019. This followed a cut in the floor rate for first-home mortgages that was announced on May 15. BCA’s China strategists believe these measures will arrest the deep contraction in the property market but will not spark a full-blown recovery due to the ongoing commitment of the government to the “three red lines” policy.2 In normal times, a Chinese real estate slump would be a cause of grave concern for global investors. These are not normal times, however. Public enemy number one these days is inflation. A weaker Chinese property market would curb commodity demand, thus helping to cool inflation. That would be a welcome development for global investors. Investment Conclusions Global financial conditions have tightened to the point that betting on ever-higher rates, at least for the next 12 months, no longer makes sense. If global inflation decelerates faster than anticipated during the remainder of the year, as we expect will be the case, central banks will dial back the hawkish rhetoric. We took partial profits on our short 10-year Treasury trade earlier this month (initiated at a yield of 1.45%). As of this week, consistent with the earlier decision of BCA’s fixed income strategists to upgrade UK Gilts, we are closing our short 10-year Gilt position (initiated at a yield of 0.85%) for a gain of 7.5%. The coming Goldilocks environment of falling inflation and supply-side led growth will buttress equities. We expect global stocks to rise 15%-to-20% over the next 12 months, with non-US markets outperforming the US. Looking further out, the fate of Goldilocks will rest on where the neutral rate of interest resides. If the neutral rate in the US turns out to be substantially lower than 2.5%, then any growth recovery will falter as the lagged effects of restrictive monetary policy work their way through the economy. Conversely, if the neutral rate turns out to be substantially higher than 2.5%, then inflation will reaccelerate as the economy overheats. Given the choice, we would wager on the latter outcome. Thus, while we expect global bond yields to decline over a 12-month horizon, we foresee them rising over a 2-to-5-year time frame. Similarly, while stocks will strengthen over the next 12 months, they are likely to encounter another bout of turbulence starting late next year or in 2024 as central banks initiate a second round of rate hikes. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Follow me on LinkedIn Twitter Footnotes 1 The Federal Reserve targets an average inflation rate of 2% for the Personal Consumption Expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of 2.3%-to-2.5%. 2 The People’s Bank of China and the housing ministry issued a deleveraging framework for property developers in August 2020, consisting of a 70% ceiling on liabilities-to-assets, a net debt-to-equity ratio capped at 100%, and a limit on short-term borrowing that cannot exceed cash reserves. Developers breaching these “red lines” run the risk of being cut off from access to new loans from banks, while those who respect them can only increase their interest-bearing borrowing by 15% at most. Global Investment Strategy View Matrix

Are Financial Conditions Tight Enough?

Are Financial Conditions Tight Enough?

Special Trade Recommendations Current MacroQuant Model Scores

Are Financial Conditions Tight Enough?

Are Financial Conditions Tight Enough?

The US GDP declined at a 1.5% annual pace, a downward revision to the previous estimate of 1.4%. Consumption spending grew at 3.1% on an annual basis – stronger than the previously reported 2.7% and the Q4 2021 pace of 2.5%. Both goods and services…

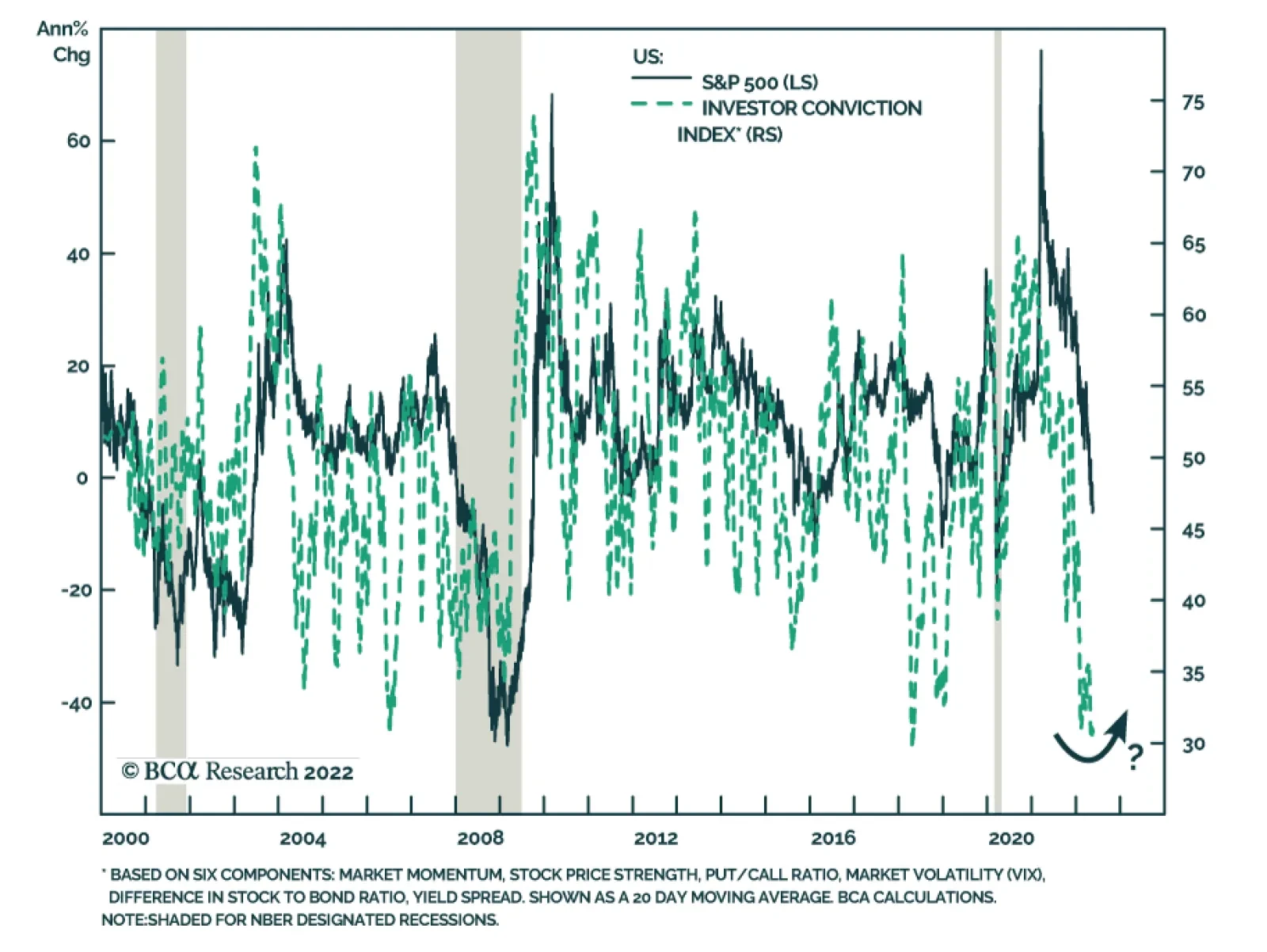

Market-based measures of investor confidence have deteriorated sharply this year. The VIX has trended higher, high-yield bond spreads have widened, and equity momentum is deteriorating. Our Investor Conviction Index – which aggregates six components to…

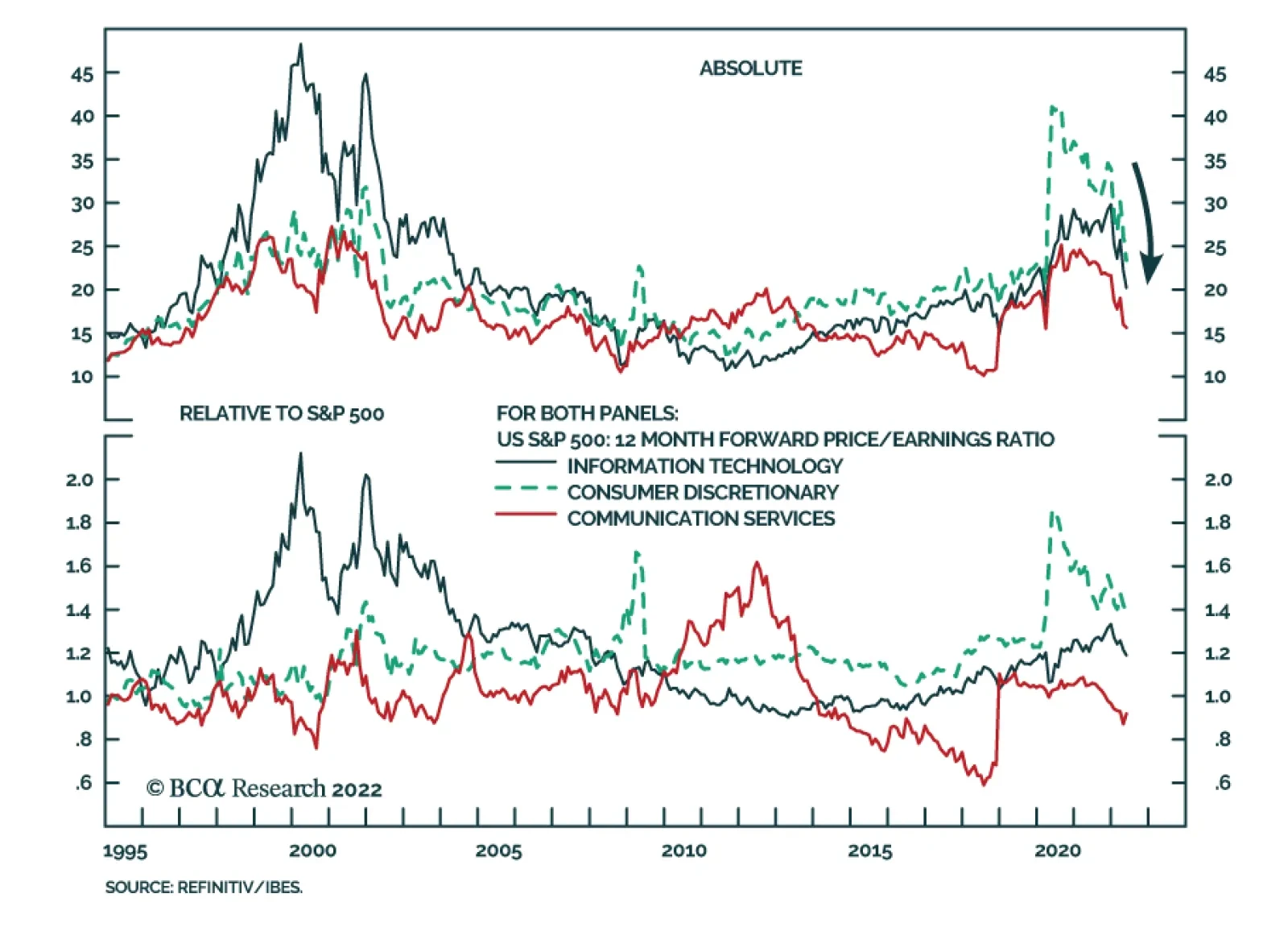

Rising bond yields have been a headwind to the performance of long-duration US tech stocks this year. Consumer Discretionary, Communication Services, and IT are the worst performing S&P 500 sectors so far in 2022. However, this negative force is now…

Highlights The Fed’s hawkish shift over the past six months has caused a sharp increase in US interest rates. In this report we examine the US housing market for signs of an imminent recession, given the housing sector’s strong interest rate sensitivity. In addition to a severe contraction in real home improvement spending, there are several other housing-related indicators that are ostensibly pointing in a bearish direction. The growth in total home sales and the MBA mortgage application purchase index are already in negative territory, housing affordability has deteriorated meaningfully, and the National Association of Home Builders’ (NAHB) housing market index is falling sharply. However, the breadth of house prices and building permits, consumer surveys, housing equity sector relative performance, and the fact that mortgage rates have likely peaked for the year point to a more optimistic outlook for housing. At a minimum, they do not yet suggest that the current slowdown in housing-related activity is recessionary. Structural factors are also supportive of the pace of housing construction in the US. While a slowdown in the housing market is clearly underway, it is not occurring after a period of excessive housing construction. The opposite is true: the US and several other developed market economies have underbuilt homes over the past decade. This should limit the drag on economic growth from housing-related activity, and reduces the odds that a housing market slowdown will morph into a housing-driven US recession. Feature Chart II-1The Fed's Hawkish Shift Has Caused An Extremely Sharp Rise In Interest Rates

The Fed's Hawkish Shift Has Caused An Extremely Sharp Rise In Interest Rates

The Fed's Hawkish Shift Has Caused An Extremely Sharp Rise In Interest Rates

The Fed’s hawkish shift over the past six months has caused US interest rates to rise at an extremely rapid pace. Panel 1 of Chart II-1 highlights that the spread between the US 2-year Treasury yield and the 3-month T-bill yield reached a 20-year high in early April of this year. Panel 2 shows that the two-year change in the 30-year mortgage rate will reach the highest level since the early 1980s by the end of this year if mortgage rates remain at their current level. Over the longer run, it is the level of interest rates that matters more than their change. However, changes in interest rates and other key financial market variables are also important drivers of economic activity, especially when they happen very rapidly. Given the speed of the recent adjustment in US interest rates, and the fact that the Fed funds rate will have likely reached the Fed’s neutral rate forecast by the end of this year, investors have understandably become concerned about the potential for a recession in the US. In this report we examine the US housing market for signs of an imminent recession, given the housing sector’s strong interest rate sensitivity. We conclude that while a slowdown in the housing market is clearly underway, several signs suggest that this slowdown is not recessionary. Investors should remain laser-focused on the pace of housing-related activity over the coming 6-12 months, but for now our assessment of the housing market is consistent with a modest overweight stance towards stocks within a multi-asset portfolio. A Brief Review Of The Housing Sector’s Contribution To Growth Table II-1 highlights the importance of the housing sector as a driver/predictor of US recessions. This table highlights that real residential investment is not a particularly important contributor to real GDP growth during nonrecessionary quarters, but it is the only main expenditure component exhibiting negative growth on average in the year prior to a recession.1 Table II-1Real Residential Investment Tends To Contract In The Year Prior To A Recession

June 2022

June 2022

When examining the contribution to economic growth from the housing sector, investors and housing market analysts often fully equate real residential investment with housing construction. In fact, while direct construction of housing units accounts for a sizeable portion of the contribution to growth from housing, it is just one of four components. This is an important point, as one of the often-overlooked elements of real residential investment has strongly leading properties and is currently providing a very negative signal about the housing sector. Chart II-2 breaks down what we consider as aggregate real “housing-related activity”, and Chart II-3 presents the contributions to annualized quarterly growth in housing activity from the four components. For the sake of completeness, we include personal consumption expenditures on furnishings and household equipment as part of housing-related activity, alongside the two main components of real residential investment: permanent site construction (including single and multi-family properties), and “other structures.” In reality, “other structures” is not predominantly accounted for by the construction of different types of residential properties; it is almost entirely composed of spending on home improvements and brokerage commissions on the sale of existing residential properties. Chart II-2Housing Construction Is An Important Part Of Residential Investment, But There Are Other Contributing Factors

June 2022

June 2022

Chart II-3Home Improvement Spending And Brokerage Commissions Also Drive Residential Investment

June 2022

June 2022

Aside from the link between existing home sales and the general demand for newly-built homes, the prominence of brokerage commissions in other residential structures investment helps explain why existing home sales are strongly correlated with real residential investment (Chart II-4, panel 1). Given that a distributed lag of monthly housing starts maps closely to permanent site construction (panel 2), starts and existing home sales explain a good portion of the contribution to growth from housing-related activity. Of the two remaining components of housing-related activity, Chart II-5 highlights that personal consumption expenditures on furniture and household equipment generally coincide with the pace of housing construction and new home sales. We take this to mean that the consumption component of housing-related activity is typically a derivative of the decision to build a new home or sell an existing one. Chart II-4Existing Home Sales Explain Commissions, And Housing Starts Explain Permanent Site Construction

Existing Home Sales Explain Commissions, And Housing Starts Explain Permanent Site Construction

Existing Home Sales Explain Commissions, And Housing Starts Explain Permanent Site Construction

Chart II-5The Pace Of Contraction In Home Improvement Spending Is Worrying

The Pace Of Contraction In Home Improvement Spending Is Worrying

The Pace Of Contraction In Home Improvement Spending Is Worrying

What is not coincident with construction and existing home sales is residential home improvement: Panel 2 of Chart II-5 highlights that it has strongly leading properties, and is currently contracting at its worst rate since the 2008 recession. Data on real home improvement spending is only available quarterly from 2002, so the ability to compare the current situation to previous housing market cycles is limited. But the pace of contraction is worrying and underscores that investors should be on the lookout for corroborating signs of a major contraction in the housing market. Is The Housing Data Sending A Recessionary Signal? In addition to the severe contraction in real home improvement spending shown in Chart II-5, there are several other housing-related indicators that are ostensibly pointing in a bearish direction. In particular, Chart II-6 highlights that both the growth in total home sales and the MBA mortgage application purchase index are already in negative territory, that housing affordability has deteriorated meaningfully, and that the National Association of Home Builders’ (NAHB) housing market index is falling sharply. However, there are also several signs pointing to a more optimistic outlook for housing, or at least indicating that the current slowdown in housing-related activity is not recessionary. We review these more optimistic indicators below. The Breadth Of House Prices And Building Permits In sharp contrast to previous periods of serious housing market weakness and/or recessionary periods, there is no sign yet of a major slowdown in US house price appreciation including cities with the weakest gains. In fact, Chart II-7 highlights that house prices have recently been reaccelerating on a very broad basis after having slowed in the second half of last year, which hardly bodes poorly for new home construction. Chart II-6A US Housing Sector Slowdown Is Certainly Underway

A US Housing Sector Slowdown Is Certainly Underway

A US Housing Sector Slowdown Is Certainly Underway

Chart II-7No Sign Yet Of A Major Deceleration In House Prices

No Sign Yet Of A Major Deceleration In House Prices

No Sign Yet Of A Major Deceleration In House Prices

It is true that US house price data is somewhat lagging, so it is quite likely that price weakness is forthcoming. However, there has been no sign of a major slowdown in prices through to March 2022, by which point 30-year mortgage rates had already risen 200 basis points from their 2021 low. More importantly, Chart II-8 highlights that a state-by-state diffusion index of authorized housing permits has done a very good job at leading the growth in permits nationwide, and is currently not pointing to a contraction in activity. Chart II-9 presents explanatory models for the growth in US housing starts and total home sales based on our state permits diffusion index, pending home sales, the change in mortgage rates, and housing affordability. The chart underscores that a contraction in housing activity is not what these variables would predict, even though starts and sales should be growing at a much more modest pace than what has prevailed on average over the past two years. Chart II-8Our Building Permits Diffusion Index Leads Housing Construction Activity, And Is Not Pointing To A Major Slowdown

Our Building Permits Diffusion Index Leads Housing Construction Activity, And Is Not Pointing To A Major Slowdown

Our Building Permits Diffusion Index Leads Housing Construction Activity, And Is Not Pointing To A Major Slowdown

Chart II-9Reliably Leading Indicators Of Construction And Home Sales Do Not Point To A Recessionary Outcome

Reliably Leading Indicators Of Construction And Home Sales Do Not Point To A Recessionary Outcome

Reliably Leading Indicators Of Construction And Home Sales Do Not Point To A Recessionary Outcome

Consumer Surveys The University of Michigan consumer survey shows that consumers feel it is the worst time to buy a home since the early-1980s (Chart II-10), which seems like a clearly negative sign for the housing market and an indication of the likely impact of tighter policy on housing-related activity. And yet, panel 2 highlights that this is the result of the fact that house prices in the US have surged during the pandemic, not that mortgage rates have risen too high. It is true that the number of survey respondents citing “interest rates are too high” is rising sharply, but this factor as a share of all “bad time to buy” reasons given is not meaningfully higher than it was in 2018, 2011, or 2006. It is clear that high prices are also the culprit for why consumers report that it is a bad time to buy large household durables and not that large household durables are unaffordable or that interest rates are too high (Chart II-11). Chart II-10Nearly The Worst Time To Buy A Home, Mostly Due To Prices (Not Interest Rates)

Nearly The Worst Time To Buy A Home, Mostly Due To Prices (Not Interest Rates)

Nearly The Worst Time To Buy A Home, Mostly Due To Prices (Not Interest Rates)

Chart II-11Same Story For Large Household Durables

Same Story For Large Household Durables

Same Story For Large Household Durables

It may seem counterintuitive for investors to see Charts II-10 and II-11 as in any way positive for the housing market. But, to us, the notion that elevated house prices are the main source of poor affordability supports the idea that a normalization of the housing market will occur through a combination of marginally lower demand, a slower pace of house price appreciation, and a sustained pace of housing market construction. This implies that existing home sales may be weaker than housing construction over the coming year, but the latter will help to support the contribution to overall economic growth from housing-related activity. Housing Sector Relative Performance Despite the significant slowdown in real home improvement spending and the recent decline in the NAHB’s housing market index, Chart II-12 highlights that home improvement retail and homebuilding stocks have not exhibited significantly negative abnormal returns over the past year – as they did in 1994/1995 and in the lead up to the global financial crisis. The chart, which presents a rolling 1-year “Jensen’s alpha” measure for both industries, attempts to capture the risk-adjusted performance of the industry versus the S&P 500. While the chart shows that both industries have generated negative alpha over the past year, the magnitude does not appear to be consistent with a recession. In the case of homebuilder stocks in particular, negative abnormal returns over the past year should have been meaningfully worse given the year-over-year change in mortgage rates. Chart II-13 highlights that homebuilder performance has not been cushioned by a deep valuation discount in advance of the rise in mortgage rates. Chart II-12Housing-Related Equity Sectors Are Not Warning Of A Housing-Driven Recession

Housing-Related Equity Sectors Are Not Warning Of A Housing-Driven Recession

Housing-Related Equity Sectors Are Not Warning Of A Housing-Driven Recession

Chart II-13Homebuilders Were Not Excessively Cheap Before Mortgage Rates Spiked

Homebuilders Were Not Excessively Cheap Before Mortgage Rates Spiked

Homebuilders Were Not Excessively Cheap Before Mortgage Rates Spiked

In short, the important takeaway for investors is that the relative performance of housing-related stocks is not yet consistent with a housing-led US recession. Mortgage Rates Are Not Restrictive, And Have Likely Peaked As we highlighted in Chart II-1, the two-year change in the US 30-year conventional mortgage rate will be the largest in history by the end of this year, save the Volcker era, if the mortgage rate remains at its current level. However, it is not just the change in interest rates that matters for economic activity, but rather also the level. Encouragingly, Chart II-14 highlights that the level of mortgage rates has not yet risen into restrictive territory relative to the economy’s underlying potential rate of growth. In addition, it appears that mortgage rates have overreacted to the expected pace of monetary tightening – and thus have likely peaked for this year. Two points support this view: First, panel 2 of Chart II-14 highlights that the 30-year mortgage rate is one standard deviation too high relative to the 10-year Treasury yield, underscoring that the former has overshot. And second, Chart II-15 highlights that the mortgage rate is still too high even after controlling for business cycle expectations, current coupon MBS yields, and bond & equity market volatility. Chart II-14Mortgage Rates Are Not Yet Restrictive, But Have Likely Peaked For The Year

Mortgage Rates Are Not Yet Restrictive, But Have Likely Peaked For The Year

Mortgage Rates Are Not Yet Restrictive, But Have Likely Peaked For The Year

Chart II-15No Matter How You Slice It, US Mortgage Rates Are Stretched

No Matter How You Slice It, US Mortgage Rates Are Stretched

No Matter How You Slice It, US Mortgage Rates Are Stretched

Structural Factors Supporting Housing Construction Chart II-16The US And Several Other DM Countries Have Underbuilt Homes Since The Global Financial Crisis

The US And Several Other DM Countries Have Underbuilt Homes Since The Global Financial Crisis

The US And Several Other DM Countries Have Underbuilt Homes Since The Global Financial Crisis

Our analysis above points to a scenario in which the housing market slows in a nonrecessionary fashion, supported by relatively buoyant construction activity. Structural factors, which are mostly a legacy of the global financial crisis, are also supportive of the pace of housing construction in the US and other developed market economies. We presented Chart II-16 in our June 2021 Special Report, which shows the most standardized measure of cross-country housing supply available for several advanced economies: the trend in real residential investment relative to real GDP over time. These series are all rebased to 100 as of 1997, prior to the 2002-2007 US housing market boom. The chart makes it clear that advanced economies generally fall into two groups based on this metric: those that have seen declines in real residential investment relative to GDP, especially after the global financial crisis (panel 1) and those that have experienced either an uptrend in housing construction relative to output or a flat trend (panel 2). The US, along with the euro area, the UK, and Japan, all belong to the first group, with commodity-producing and Scandinavian countries belonging to the second group. The point of the chart is that the US and most other major DM economies have seemingly experienced a chronic undersupply of homes in the wake of the global financial crisis, which should continue to support housing construction activity even if demand for housing is slowing because of a sharp increase in mortgage rates. Given that the trend in real residential investment to GDP is a somewhat crude metric of housing supply, Chart II-17 presents a more precise measure for the US. It shows the standardized trend in permanent site residential structures investment (both single- and multi-family) relative to both the US population and the number of households. The chart makes it clear that the US vastly overbuilt homes from the late-1990s to 2007, but also vastly underbuilt since 2008. Relative to the number of households, real permanent site residential structures investment is still half of a standard deviation below its long-term average – even after the surge in construction that occurred in 2020. Chart II-18 highlights a similar message: it shows that the US homeowner vacancy rate (the proportion of the housing stock that is vacant and for sale) was at a 66-year low at the end of the first quarter. Chart II-19 shows that the monthly supply of existing one-family homes on the market is also at a multi-decade low, but that the supply of new homes for sale spiked in April. Chart II-17More Precise Home Supply Measures Underscore That The US Needs To Build More Houses

More Precise Home Supply Measures Underscore That The US Needs To Build More Houses

More Precise Home Supply Measures Underscore That The US Needs To Build More Houses

Chart II-18The Homeowner Vacancy Rate Is Extremely Low

The Homeowner Vacancy Rate Is Extremely Low

The Homeowner Vacancy Rate Is Extremely Low

At first blush, this spike in the monthly supply of new homes relative to sales is quite concerning, as it has risen back to levels that prevailed in 2007. One point to note is that the increase in new home inventory relates to homes still under construction; the inventory of completed homes for sale remains quite low. In addition, from the perspective of a homebuilder, a rise in the monthly supply of new homes relative to home sales is only concerning if it translates into a significant increase in the amount of time to sell a completed home, as has historically been the case (Chart II-20). Chart II-19Existing Home Inventories Remain Low Relative To Sales...

Existing Home Inventories Remain Low Relative To Sales...

Existing Home Inventories Remain Low Relative To Sales...

Chart II-20...And Higher New Home Inventories Are Not Affecting Time-To-Sale Of Completed Homes

...And Higher New Home Inventories Are Not Affecting Time-To-Sale Of Completed Homes

...And Higher New Home Inventories Are Not Affecting Time-To-Sale Of Completed Homes

Chart II-20 highlights that a fairly significant divergence between these two series has emerged over the past decade. Despite roughly five-six months’ supply of new home inventory on average since 2012, the median number of months required to sell a new home rarely exceeded four. In early-2019 the monthly supply of new homes also spiked, and a relatively modest and nonrecessionary slowdown in housing starts was sufficient to prevent any meaningful rise in the amount of time required to sell a newly completed home. Notably, the models that we presented in Chart II-9 led the slowdown in total home sales and starts in late-2018/early-2019, and they are not pointing to a major contraction today. The key point for investors is that while a slowdown in the housing market is clearly underway, it is not occurring after a period of excessive housing construction. In fact, the opposite is true: despite a surge in construction during the pandemic, it remains below its historical average relative to the population and especially the number of households. This should act to limit the drag on economic growth from housing-related activity, and therefore reduces the odds that a housing market slowdown will morph into a housing-driven US recession. Investment Implications We noted in our May report that the inversion of the 2-10 yield curve has set a recessionary tone to any weakness in US macroeconomic data, and that a recession scare was likely. Recent negative housing market data surprises underscore that a slowdown in the US housing market is clearly underway, and that this will likely feed recessionary concerns for a time. Investors should continue to be highly focused on the evolution of US macro data when making asset allocation decisions over the coming 6-12 months, as the current economic and financial market environment remains highly uncertain. This should include a strong focus on the housing market, as consumer surveys highlight that the overall impact of falling real wages and high house prices could cause a more pronounced slowdown in housing-related activity than we expect – and that the change and level of interest rates would imply. Nevertheless, our analysis of the historical predictors of housing construction and sales points to the conclusion that the ongoing housing market slowdown is not likely to be recessionary in nature. This, in conjunction with the factors that we noted in Section 1 of our report, support maintaining a modest overweight towards stocks within a multi-asset portfolio over the coming 6-12 months. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 This is aside from the contribution to growth from imports, which mechanically subtract from consumption and investment when calculating GDP.

Highlights The economic and financial market developments that have occurred over the past month are consistent with several of the risks that we identified in our recent reports. We warned in our April report that the outlook for equities had deteriorated meaningfully since the beginning of the year and recommended that investors maintain, at most, a very modest overweight toward stocks in a global multi-asset portfolio. We see the performance of the equity market over the past month as reflecting the beginning of the recession scare that we warned was coming. Still, several factors continue to suggest that this is indeed a scare, and not an actual recession. Section 2 of this month’s report reviews the US housing market for signs of an imminent recession. While a slowdown in the housing market is clearly underway, we do not yet see signs that this slowdown is recessionary. It remains an open question how forcefully Russia is willing to weaponize its natural gas exports in response to a seemingly imminent European embargo on Russian oil, and whether Russia will deploy this strategy now or later. For now, our base case view is that the euro area economy will slow and will probably contract in Q2, but it will avoid a debilitating energy-driven recession. China’s zero-tolerance COVID policy has failed to contain the disease, and it is now clear that more and more outbreaks will occur across the country over the coming months. Our base case view is that additional fiscal & monetary support is forthcoming if the spread of the disease progresses as we expect. We are likely to downgrade our outlook for global economic activity as well as our recommended allocation to risky assets if it does not materialize. Our profit margin warning indicators have deteriorated over the past month, and it is now our view that a contraction in S&P 500 margins is likely. Still, a major decline should be avoided, and we expect that S&P 500 earnings will grow at a low, single-digit rate over the coming year. We continue to recommend a marginally overweight stance towards risky assets over the coming 6-12 months, along with a neutral regional equity stance, a modestly overweight stance towards value over growth, an overweight stance towards small caps, a modestly short duration stance within a fixed-income portfolio, and short US dollar positions. Not Out Of The Woods Yet Chart I-1In May, Global Stocks Nearly Fell Into Bear Market Territory

In May, Global Stocks Nearly Fell Into Bear Market Territory

In May, Global Stocks Nearly Fell Into Bear Market Territory

May was a painful month for the equity market. Globally, stocks fell more than 4% in US$ terms, led by the US. May’s selloff pushed global stocks close to bear market territory relative to their early-January high (Chart I-1), a threshold that was breached in intra-day terms in the US last week. We warned in our April report that the outlook for equities had deteriorated meaningfully since the beginning of the year and recommended that investors maintain, at most, a very modest overweight toward stocks in a global multi-asset portfolio. In our view, the economic and financial market developments that occurred over the past month are consistent with several of the risk we identified in our recent reports. We continue to recommend that investors remain minimally overweight risky assets. Our view that investors should not be underweight risky assets hinges on three expectations: the avoidance of a US recession over the coming year, a continuation of Russian natural gas exports to key gas-reliant European countries, and the announcement from Chinese policymakers of either significant additional stimulus in its traditional form or income-support policies of the type that prevailed in developed economies in the early phase of the COVID-19 pandemic. Confirmation of these expectations is likely to push us to upgrade our recommended stance toward risky assets, especially if equities continue to sell off in response to growth fears. Conversely, we are likely to recommend downgrading risky assets to neutral or underweight if evidence mounts that our expectations are unlikely to materialize. A US Recession Scare Is Underway We noted in last month’s report that the US economy would likely avoid a recession over the coming year, but that a recession scare was quite likely. We emphasized a probable slowdown in the housing market as the locus of investors’ recessionary concern, and the US housing market data is indeed now surprising significantly to the downside (Chart I-2). We see the performance of the equity market over the past month as reflecting the beginning of the recession scare that we warned was coming. Chart I-3 highlights that the composition of the US equity selloff since the beginning of the year has looked quite unlike the growth-driven selloffs that occurred over the past decade, in that real bond yields have been a strong driver of the decline in stocks. By contrast, May’s decline has looked more like a typical growth scare, with real bond yields somewhat cushioning the impact of a significant rise in the equity risk premium. Chart I-2The US Housing Market Is Clearly Slowing

The US Housing Market Is Clearly Slowing

The US Housing Market Is Clearly Slowing

Chart I-3May’s Selloff Was Driven By Growth Fears, Not Rising Interest Rates

June 2022

June 2022

Chart I-4 highlights that it is not just the housing market that is worrying investors. The chart shows that the Conference Board’s US leading economic indicator (LEI) is slowing quite sharply, in line with previous episodes of a major growth scare. And while the weakest components of the LEI modestly improved on average in April, Chart I-5 highlights that the collapse in real wage growth alongside the recently severe underperformance of consumer stocks has fed concerns that high inflation has eroded household purchasing power – and that a contraction in real spending is imminent. Chart I-4A Serious US Growth Scare Is Underway

A Serious US Growth Scare Is Underway

A Serious US Growth Scare Is Underway

Chart I-5The Decline In Real US Wage Growth Has Caused A Major Selloff In Consumer Stocks

The Decline In Real US Wage Growth Has Caused A Major Selloff In Consumer Stocks

The Decline In Real US Wage Growth Has Caused A Major Selloff In Consumer Stocks

In Section 2 of this month’s report we provide further analysis supporting the view that the US housing market will not drive the US economy into recession. But we do continue to believe that a slowdown in housing activity is likely, and that concerns about a housing-driven recession will linger. Still, several factors continue to suggest that the US is experiencing a recession scare, and not an actual recession: The Atlanta Fed’s GDPNow model is currently predicting US real GDP growth that is only modestly below trend in Q2, and the overall estimate continues to be dragged significantly lower by a sizably negative contribution from the change in inventories (Chart I-6). Without this negative inventories effect, the Atlanta Fed’s model would be forecasting real annualized growth of over 3%. After having decelerated significantly in the second half of last year because of a broadening in consumer price inflation, Chart I-7 highlights that real personal consumption expenditures reaccelerated and real personal income ex-transfers stabilized in Q1. Chart I-6No Sign Of A Major Decline In Q2 Consumer Spending

June 2022

June 2022

Chart I-7Real Income Growth Is Stabilizing, And Real Consumer Spending Is Accelerating

Real Income Growth Is Stabilizing, And Real Consumer Spending Is Accelerating

Real Income Growth Is Stabilizing, And Real Consumer Spending Is Accelerating

US manufacturing industrial production surged in April, led by motor vehicle production (Chart I-8, panel 1). It is true that industrial production is a coincident indicator and thus does not necessarily argue against the idea that a recession is imminent. A pickup in vehicle production is encouraging, however, as it suggests that the 15% surge in the level of new car prices over the past year that contributed to the erosion in household real incomes may be set to reverse (panel 2). Chart I-8A Pickup In Auto Production Should Help Lower Car Prices And Improve Consumer Purchasing Power

A Pickup In Auto Production Should Help Lower Car Prices And Improve Consumer Purchasing Power

A Pickup In Auto Production Should Help Lower Car Prices And Improve Consumer Purchasing Power

Services spending is likely to improve, as deliveries of Pfizer’s Paxlovid antiviral drug continue to ramp up and vaccines are eventually approved for children under the age of six. Charts I-9A and I-9B highlight several real services spending categories that remain below their pre-pandemic levels, which in our view have been clearly linked to the pandemic and are not likely to be permanently lower. Americans have not likely stopped going to the gym, amusement parks, movies, live concerts, or the dentist, nor have their stopped needing to put elderly relatives in nursing care homes. They are also highly unlikely to stop traveling. There is some internal debate at BCA about the impact that working-from-home trends will have on the level of services spending, but we would note that essentially all of the spending categories shown in Charts I-9A and I-9B have exhibited uptrends that only appear to have been affected by consumer responses to the Delta and Omicron waves of the pandemic. Widely-available treatment options that reduce the fatality rate of the disease close to that of the flu are likely to be perceived by the public as an effective end of the pandemic, boosting spending on lagging categories of services spending. Chart I-9AAn Eventual End To The Pandemic…

June 2022

June 2022

Chart I-9B…Will Cause A Further Improvement In Services Spending

...Will Cause A Further Improvement In Services Spending

...Will Cause A Further Improvement In Services Spending

Based on high-frequency data from OpenTable, the number of seated diners in US restaurants is not exhibiting any major warning signs for US consumer spending (Chart I-10). Real spending in restaurants has been strongly correlated with overall real personal consumption expenditures over the past two decades, and thus Chart I-10 is not suggesting that a collapse in overall spending is imminent. Chart I-10High-Frequency Data Does Not Yet Show A Major Pullback In US Consumer Spending

High-Frequency Data Does Not Yet Show A Major Pullback In US Consumer Spending

High-Frequency Data Does Not Yet Show A Major Pullback In US Consumer Spending

As a final point concerning the risk of recession in the US, investors should note that the recent behavior of inflation expectations is encouraging and points to a potentially imminent peak in Fed hawkishness. Over the past few months, we have expressed our concern about the pace of increase in long-dated household inflation expectations. We highlighted last month that long-term market-based inflation expectations were also exhibiting some potential signs of becoming unanchored. However, Chart I-11 highlights that the momentum of long-dated household inflation expectations is now starting to flag, and that long-term market-based inflation expectations recently decreased in response to escalating growth fears. Chart I-12 clearly shows a slowing pace of core consumer prices, which will act to restrain further significant increases in long-dated inflation expectations. Chart I-11Long-Dated Inflation Expectations Point To A Potentially Imminent Peak In Fed Hawkishness

June 2022

June 2022

Chart I-12Core Inflation Momentum Is Clearly Slowing

Core Inflation Momentum Is Clearly Slowing

Core Inflation Momentum Is Clearly Slowing

Chart I-13 highlights that investors expect the Fed to raise the policy rate by the end of the year to a level even higher than what Jerome Powell implied during the Fed’s May press conference: a target range for the Fed funds rate of 2.5-2.75%, corresponding to two more 50 basis point hikes and three 25 basis point hikes during the FOMC’s September, November, and December meetings. Chart I-13Expectations For Fed Rate Hikes This Year Are Likely To Come Down If Inflation Continues To Moderate

June 2022

June 2022

It is likely that the market’s expectation for rate hikes this year will fall over the coming few months if the monthly pace of core inflation continues to slow. The Fed itself may soon signal a less intense pace of tightening than Powell recently implied – a perspective that we feel is supported by the minutes of the May FOMC meeting. That would allow the US economy to “digest” the recent adjustment in interest rates with less uncertainty about the economic outlook, which would lower the odds that a “mid-cycle slowdown” morphs into a full-blown recession. A Debilitating Energy-Driven Recession In Europe Is Not In The Cards, For Now The key issue pertaining to the European economic outlook remains the question of whether Europe’s imports of Russian natural gas will be interrupted. A European embargo of Russian oil now seems likely, which would likely cause Russian oil production to decline. Our Commodity & Energy strategy service now expects Brent oil to trade at $120/bbl on average for the remainder of the year, $5/bbl higher than current levels (Chart I-14). We agree with our Commodity & Energy Strategy team’s updated oil price forecast, but we have a different view about the odds that Russia will respond to a European oil embargo by cutting its natural gas exports to the EU. We still think this is a risk, not yet a likely event, although it may still occur later in the year. A full and immediate cutoff of natural gas exports to gas-dependent European countries such as Germany and Italy would not only destabilize the Russian economy by substantially reducing its current account surplus, it would also cause a severe recession in Europe through a combination of gas rationing to industries by government decree and surging energy prices (Chart I-15). Chart I-14A European Embargo Of Russian Oil Will Cause Brent To Rise To $120/bbl

A European Embargo Of Russian Oil Will Cause Brent To Rise To $120/bbl

A European Embargo Of Russian Oil Will Cause Brent To Rise To $120/bbl

Chart I-15A Full Cutoff Of Russian Natural Gas Would Cause A Severe European Recession

A Full Cutoff Of Russian Natural Gas Would Cause A Severe European Recession

A Full Cutoff Of Russian Natural Gas Would Cause A Severe European Recession

That could erode European voters’ willingness to provide military support for Ukraine, but it could instead backfire and galvanize European public opinion against Russia – and remove leverage that may be potentially used to secure a ceasefire agreement that will preserve its military gains in eastern Ukraine. Chart I-16Europe Is Replenishing Its Gas Storage, But It Cannot Yet Withstand A Full Cutoff

June 2022

June 2022

Russia may respond to an oil embargo by throttling the amount of natural gas exported to key European countries in a fashion that raises natural gas prices and prevents European countries from building up sufficient storage for the upcoming winter – a process that is underway but is far from complete (Chart I-16). But it remains an open question how forcefully Russia is willing to weaponize its natural gas exports, and whether it will deploy this strategy now or later. For now, our base case view is that the euro area economy will slow and will probably contract in Q2, but it will avoid a debilitating energy-driven recession. China: The Only Way Out Is Through Among the three pillars of the global economy – the US, China, and Europe – the last is arguably the least important. Today, the US and China are the core drivers of global demand, and we are therefore more concerned about the economic impact of China’s zero-tolerance COVID policy than we are about a slowdown or mild recession in Europe. Given how contagious the Omicron variant of COVID-19 has shown itself to be, and given how widespread recent outbreaks have been, it is now clear that China’s zero-tolerance policy has failed to contain the disease and that more and more outbreaks will occur across the country over the coming months. Despite public statements to the contrary, we suspect that Chinese policymakers are well aware of this situation, but are constrained by the consequences of removing the zero-tolerance policy. Recent studies suggest that China could face intensive care demand that is sixteen times existing capacity and upwards of 1.5 million deaths by removing the policy,1 roughly 1.5 times the cumulative amount of deaths that have occurred in the US during the pandemic. But the economic consequences of maintaining the zero-tolerance policy will also be severe, and therefore also likely represent a constraint on policymakers. Charts I-17 and I-18 show that China’s labor market and industrial sector have already slowed sharply over the past few months, at a pace and magnitude that is unlikely to be politically sustainable for much longer. In addition, Chart I-19 shows that China’s credit impulse fell meaningfully in April. Chart I-17China’s Labor Market Is Cratering…

China's Labor Market Is Cratering...

China's Labor Market Is Cratering...

Chart I-18…As Is Its Manufacturing Sector

... As Is Its Manufacturing Sector

... As Is Its Manufacturing Sector

Chart I-19More Fiscal & Monetary Support Will Be Needed In China Soon, If COVID-19 Cases Continue To Spread

More Fiscal & Monetary Support Will Be Needed In China Soon, If COVID-19 Cases Continue To Spread

More Fiscal & Monetary Support Will Be Needed In China Soon, If COVID-19 Cases Continue To Spread

This would be tolerable if the decline in activity was likely to be short-lived as it was at the very beginning of the pandemic, but we no longer see this as a probable outcome. We acknowledge that reported cases of COVID-19 have steadily declined in cities in the Yangtze River region, and we agree that the Shanghai lockdown may soon end for a time. But we doubt that this will mark the end of outbreaks in the region, or prevent major outbreaks from occurring in other parts of the country. If China cannot relax its zero-tolerance policy or tolerate the degree of economic weakness entailed by its continued application, then additional fiscal and monetary support is likely. While China’s leadership has stepped up its pro-growth policy measures, as evidenced by the recent cut in the 5-year loan prime rate, we strongly suspect that more support will be needed. This support may take the form of traditional stimulus via local government spending, or it may involve the introduction of income-support policies of the kind that prevailed in developed economies in the early phase of the COVID-19 pandemic. Chart I-20The Chinese Housing Market Is Slowing Significantly, Lowering The Risk Of Speculation From Income Support Policies

The Chinese Housing Market Is Slowing Significantly, Lowering The Risk Of Speculation From Income Support Policies

The Chinese Housing Market Is Slowing Significantly, Lowering The Risk Of Speculation From Income Support Policies

Chinese policymakers who are eager to prevent another significant releveraging of the economy and who want to avoid another major deterioration in housing affordability may perhaps be forgiven for seeing the developed economy experience with these programs as a poor roadmap to follow. House prices have exploded in most advanced economies during the pandemic, which has significantly contributed to a major decline in affordability. However, with the benefit of hindsight, Chinese policymakers would likely be able to recalibrate any income support program to avoid some of the excesses that occurred in DM countries, such as policies that caused aggregate disposable income to increase in the US and Canada during the pandemic. In addition, Chart I-20 highlights that the starting point for the Chinese property market is one in which house prices are seemingly poised to contract at the worst pace since late 2014 / early 2015. The latter suggests that Chinese policymakers have more ability to support household income without causing an explosion in house prices and speculative activity than DM policymakers did in 2020. Regardless of its form, it is the view of the Bank Credit Analyst service that China cannot avoid the provision of significant additional fiscal/monetary support if it maintains its zero-tolerance COVID policy for the remainder of the year given our assumption that potentially major outbreaks will continue. It is our base case view that additional support is forthcoming over the coming weeks and months if the spread of the disease progresses as we expect. We are likely to downgrade our outlook for global economic activity as well as our recommended allocation to risky assets if it does not materialize. US Corporate Profits In A Nonrecessionary Slowdown Scenario Chart I-21US Forward Earnings Very Rarely Fall While The Economy Continues To Expand

June 2022

June 2022

Chart I-3 highlighted that the US equity market selloff in May shifted from one that was strongly driven by rising real government bond yields to one in which a rising equity risk premium was the dominant driver. And yet, the chart showed that there has been no negative contribution to US stock prices from falling earnings expectations, with expected earnings having continued to rise since the beginning of the year. While it may seem counterintuitive to investors that forward earnings expectations are not falling in the middle of a major growth scare, Chart I-21 highlights that this is not abnormal. The chart highlights that forward earnings expectations rarely decline outside of the context of a recession, because actual earnings typically do not decline when the economy is expanding. This means that the potential for earnings to decline shows up as a rise in the equity risk premium during growth scares, which is what has generally occurred since the beginning of the year (excluding energy, forward EPS estimates have fallen slightly this year). In last month’s Section 2, we noted that nonrecessionary earnings declines almost always occur because of contractions in profit margins. We argued that risks to US equity margins might rise later this year. In fact, since we published our report last month, some of these risks have already materialized: our new profit margin warning indicator has jumped significantly (Chart I-22), and our sector profit margin diffusion index has fallen below the boom/bust line (Chart I-23). As such, it is now our view that a contraction in S&P 500 profit margins is likely over the coming year, which contrasts with analyst EPS growth expectations of 9.5% and sales per share growth expectations of 8% (meaning that analysts are currently forecasting a margin expansion). Chart I-22A Contraction In S&P 500 Profit Margins...

A Contraction In S&P 500 Profit Margins...

A Contraction In S&P 500 Profit Margins...

Chart I-23...Now Looks Likely

...Now Looks Likely

...Now Looks Likely

Will a likely contraction in profit margins cause an outright decline in earnings over the coming year? Investors should acknowledge that this is a risk, but for now our answer is no. Chart I-24For Now, A Severe Contraction In Margins Does Not Seem Probable

For Now, A Severe Contraction In Margins Does Not Seem Probable

For Now, A Severe Contraction In Margins Does Not Seem Probable

Taken at face value, our sector diffusion index shown in Chart I-23 suggests that profit margins are set to decline by 2 percentage points over the coming year, which would indeed imply a 7-8% contraction in earnings per share assuming 8% revenue growth. However, the index is much better at predicting inflection points in profit margins than the magnitude of the change; in several cases over the past three decades the model correctly predicted a decline in profit margins, but implied a much larger change in margins than what actually occurred. In addition, our model shown in Chart I-22 has yet to cross above the 50% mark into probable territory, and Chart I-24 highlights that net earnings revisions and net positive earnings surprises are falling but have not yet reached levels that would be consistent with a major margin decline. In sum, we expect that S&P 500 earnings will grow at a low, single-digit rate over the coming year given our expectation of a nonrecessionary slowdown scenario. This implies that US equity returns will be uninspiring over the coming year, but they will be likely be positive and will likely beat the returns offered from bonds. Investment Strategy Recommendations Considerable uncertainty remains about the global economic and financial market outlook, and there are several identifiable risks that would warrant an underweight stance towards risky assets were they to materialize. We agree that an aggressively overweight stance is not justified. Chart I-25Without A Recession, The US Equity Risk Premium Is Very Likely To Decline

Without A Recession, The US Equity Risk Premium Is Very Likely To Decline

Without A Recession, The US Equity Risk Premium Is Very Likely To Decline

However, the fact that corporate profits do not usually fall while the economy is expanding underscores why investors should be reluctant to significantly cut their risky asset exposure unless a recession appears likely. Without a recession, the US equity risk premium is very likely to decline (Chart I-25), meaning that 10-year Treasury yields closer to 4% or a significant contraction in profit margins would be required for US stocks to post negative returns over the coming 6-12 months. We would not rule out either of these outcomes, but we also do not think that they are probable. To conclude, it is fair to say that global investors are not out of the woods yet, but we continue to recommend a marginally overweight stance towards risky assets on the basis that the US will avoid a recession over the coming year, Russia is not yet likely to push Europe into a debilitating recession, and China will further ease fiscal & monetary policy to support growth. In addition to a modest overweight towards stocks in a multi-asset portfolio, we continue to recommend the following: A neutral regional equity stance, with global ex-US equities on upgrade watch in response to an improvement in the European economic outlook and further fiscal & monetary support in China. The recent passive outperformance of global ex-US stocks has occurred mainly because US stocks have fallen more than global stocks, which have “caught up” to mounting US and global growth fears. As such, ex-US stocks have outperformed for the wrong reasons, and investors should wait for durable signs of an improving global growth outlook and a falling US dollar before shifting in favor of a global ex-US equity stance. A modestly overweight stance towards value over growth stocks on the basis of better valuation. However, most of the pandemic-related outperformance of growth stocks has already reversed (Chart I-26), suggesting that the outperformance of value is getting late. An overweight stance toward global small-cap stocks over their large-cap peers, as they are now unequivocally inexpensive and have remained resilient as global growth fears have intensified (Chart I-27). Chart I-26Modestly Favor Value Stocks Due To Better Valuation, But The COVID Effects On Equity Style Have Mostly Reversed

Modestly Favor Value Stocks Due To Better Valuation, But The COVID Effects On Equity Style Have Mostly Reversed

Modestly Favor Value Stocks Due To Better Valuation, But The COVID Effects On Equity Style Have Mostly Reversed

Chart I-27Small Cap Stocks Have Recently Proven Resilient, And Are Extremely Cheap

Small Cap Stocks Have Recently Proven Resilient, And Are Extremely Cheap

Small Cap Stocks Have Recently Proven Resilient, And Are Extremely Cheap

A modestly short duration stance within a fixed-income portfolio. Short US dollar positions, as the dollar is clearly benefiting from growth fears that will wane. In addition, the US dollar is very expensive, and extremely overbought. Concerning our recommended duration stance, we acknowledge that a slower pace of rate hikes than what investors currently expect and a slowing pace of inflation would normally argue for a long duration stance. But we do not expect the Fed to stop raising interest rates unless a recession seems likely, and a slower but steady path of tightening, in conjunction with easing inflation, makes it more likely that the US economy will be able to “digest” the recent adjustment in rates without tipping into recession. This, in turn, increases the odds that the Fed funds rate will peak at a higher level than investors currently expect, which should ultimately push long-maturity yields higher rather than lower. On balance, this suggests that investors should be modestly short duration, even if long-maturity bond yields move temporarily lower over the coming few months. Long-duration positions are perhaps reasonable on a 0-3 month time horizon, but over a 6-12 month time horizon we continue to recommend a modestly short stance. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst May 26, 2022 Next Report: June 30, 2022 II. Is The US Housing Market Signaling An Imminent Recession? The Fed’s hawkish shift over the past six months has caused a sharp increase in US interest rates. In this report we examine the US housing market for signs of an imminent recession, given the housing sector’s strong interest rate sensitivity. In addition to a severe contraction in real home improvement spending, there are several other housing-related indicators that are ostensibly pointing in a bearish direction. The growth in total home sales and the MBA mortgage application purchase index are already in negative territory, housing affordability has deteriorated meaningfully, and the National Association of Home Builders’ (NAHB) housing market index is falling sharply. However, the breadth of house prices and building permits, consumer surveys, housing equity sector relative performance, and the fact that mortgage rates have likely peaked for the year point to a more optimistic outlook for housing. At a minimum, they do not yet suggest that the current slowdown in housing-related activity is recessionary. Structural factors are also supportive of the pace of housing construction in the US. While a slowdown in the housing market is clearly underway, it is not occurring after a period of excessive housing construction. The opposite is true: the US and several other developed market economies have underbuilt homes over the past decade. This should limit the drag on economic growth from housing-related activity, and reduces the odds that a housing market slowdown will morph into a housing-driven US recession. Chart II-1The Fed's Hawkish Shift Has Caused An Extremely Sharp Rise In Interest Rates

The Fed's Hawkish Shift Has Caused An Extremely Sharp Rise In Interest Rates

The Fed's Hawkish Shift Has Caused An Extremely Sharp Rise In Interest Rates

The Fed’s hawkish shift over the past six months has caused US interest rates to rise at an extremely rapid pace. Panel 1 of Chart II-1 highlights that the spread between the US 2-year Treasury yield and the 3-month T-bill yield reached a 20-year high in early April of this year. Panel 2 shows that the two-year change in the 30-year mortgage rate will reach the highest level since the early 1980s by the end of this year if mortgage rates remain at their current level. Over the longer run, it is the level of interest rates that matters more than their change. However, changes in interest rates and other key financial market variables are also important drivers of economic activity, especially when they happen very rapidly. Given the speed of the recent adjustment in US interest rates, and the fact that the Fed funds rate will have likely reached the Fed’s neutral rate forecast by the end of this year, investors have understandably become concerned about the potential for a recession in the US. In this report we examine the US housing market for signs of an imminent recession, given the housing sector’s strong interest rate sensitivity. We conclude that while a slowdown in the housing market is clearly underway, several signs suggest that this slowdown is not recessionary. Investors should remain laser-focused on the pace of housing-related activity over the coming 6-12 months, but for now our assessment of the housing market is consistent with a modest overweight stance towards stocks within a multi-asset portfolio. A Brief Review Of The Housing Sector’s Contribution To Growth Table II-1 highlights the importance of the housing sector as a driver/predictor of US recessions. This table highlights that real residential investment is not a particularly important contributor to real GDP growth during nonrecessionary quarters, but it is the only main expenditure component exhibiting negative growth on average in the year prior to a recession.2 Table II-1Real Residential Investment Tends To Contract In The Year Prior To A Recession

June 2022

June 2022

When examining the contribution to economic growth from the housing sector, investors and housing market analysts often fully equate real residential investment with housing construction. In fact, while direct construction of housing units accounts for a sizeable portion of the contribution to growth from housing, it is just one of four components. This is an important point, as one of the often-overlooked elements of real residential investment has strongly leading properties and is currently providing a very negative signal about the housing sector. Chart II-2 breaks down what we consider as aggregate real “housing-related activity”, and Chart II-3 presents the contributions to annualized quarterly growth in housing activity from the four components. For the sake of completeness, we include personal consumption expenditures on furnishings and household equipment as part of housing-related activity, alongside the two main components of real residential investment: permanent site construction (including single and multi-family properties), and “other structures.” In reality, “other structures” is not predominantly accounted for by the construction of different types of residential properties; it is almost entirely composed of spending on home improvements and brokerage commissions on the sale of existing residential properties. Chart II-2Housing Construction Is An Important Part Of Residential Investment, But There Are Other Contributing Factors

June 2022

June 2022

Chart II-3Home Improvement Spending And Brokerage Commissions Also Drive Residential Investment

June 2022

June 2022

Aside from the link between existing home sales and the general demand for newly-built homes, the prominence of brokerage commissions in other residential structures investment helps explain why existing home sales are strongly correlated with real residential investment (Chart II-4, panel 1). Given that a distributed lag of monthly housing starts maps closely to permanent site construction (panel 2), starts and existing home sales explain a good portion of the contribution to growth from housing-related activity. Of the two remaining components of housing-related activity, Chart II-5 highlights that personal consumption expenditures on furniture and household equipment generally coincide with the pace of housing construction and new home sales. We take this to mean that the consumption component of housing-related activity is typically a derivative of the decision to build a new home or sell an existing one. Chart II-4Existing Home Sales Explain Commissions, And Housing Starts Explain Permanent Site Construction

Existing Home Sales Explain Commissions, And Housing Starts Explain Permanent Site Construction

Existing Home Sales Explain Commissions, And Housing Starts Explain Permanent Site Construction

Chart II-5The Pace Of Contraction In Home Improvement Spending Is Worrying

The Pace Of Contraction In Home Improvement Spending Is Worrying

The Pace Of Contraction In Home Improvement Spending Is Worrying