United States

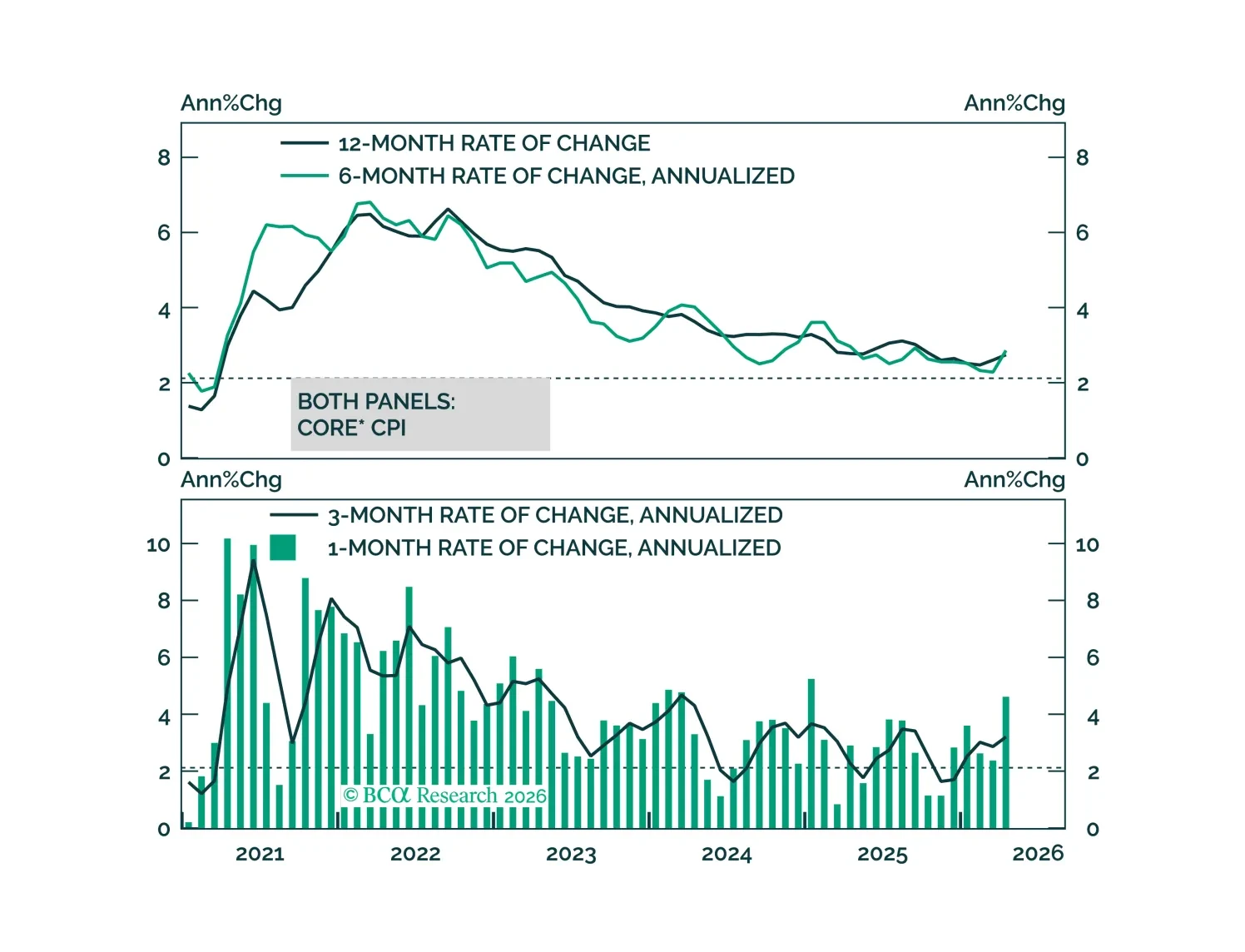

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.

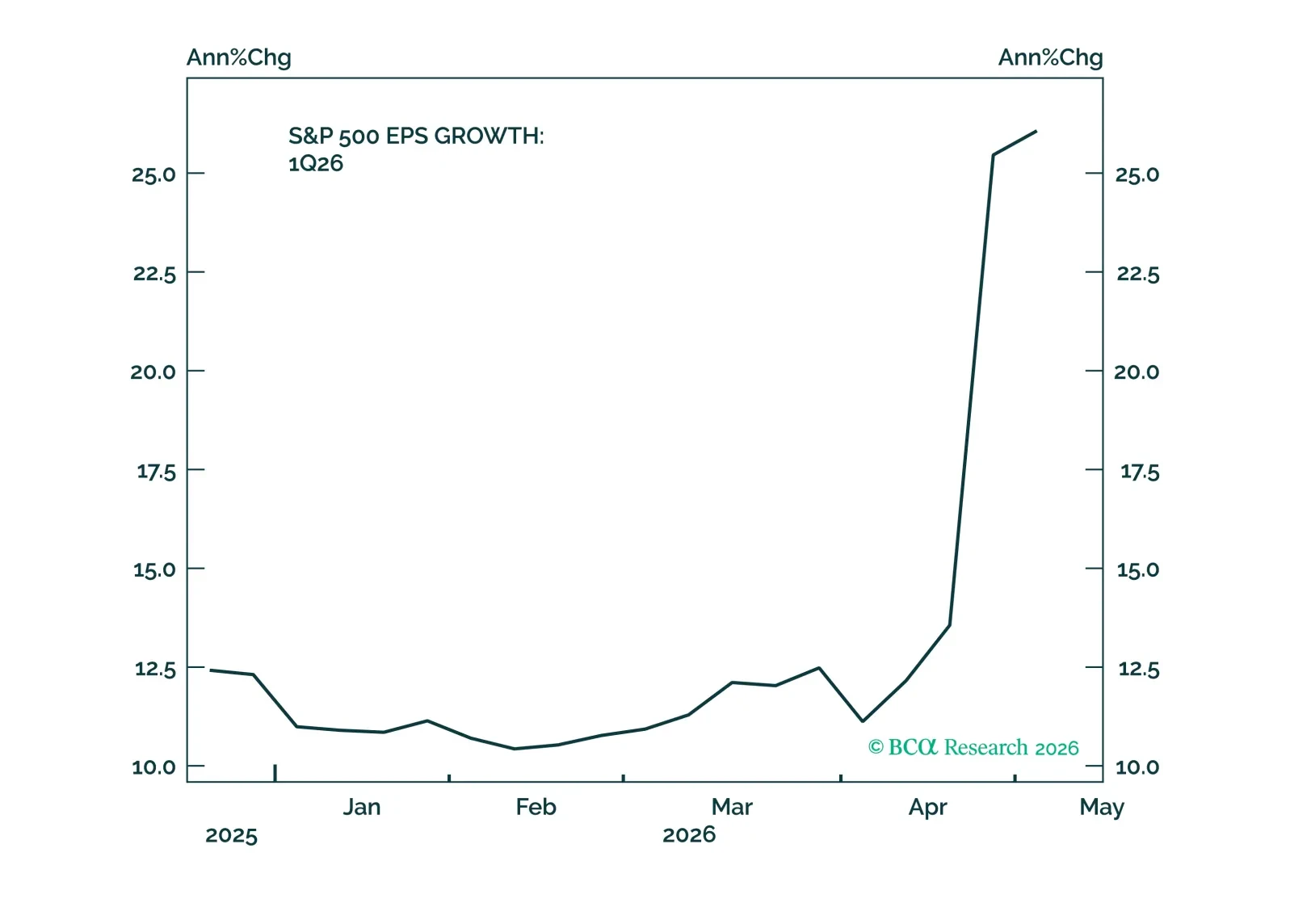

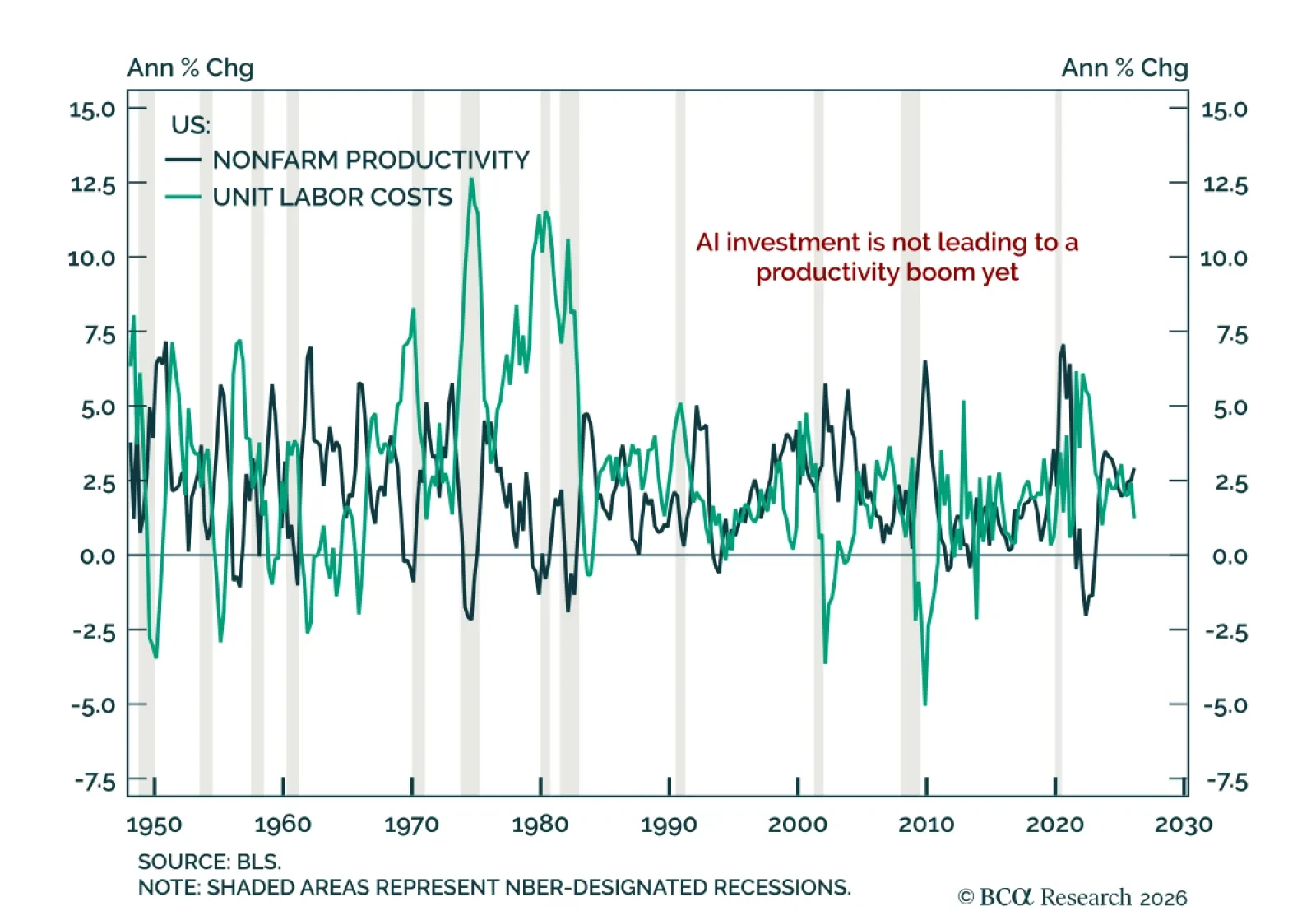

The investment cycle remains firmly intact, driving equity prices and fundamentals, as confirmed by both Q1 data and corporate commentary. Upside surprises, expanding margins, and rising capex expectations point to resilient demand. Companies confirm that AI-related demand is broad and visible, while geopolitical and credit risks remain contained and not yet systemic.

We take stock of earnings, AI capex and the labor market and explain why we think the repeated new highs in the S&P 500 are justified.

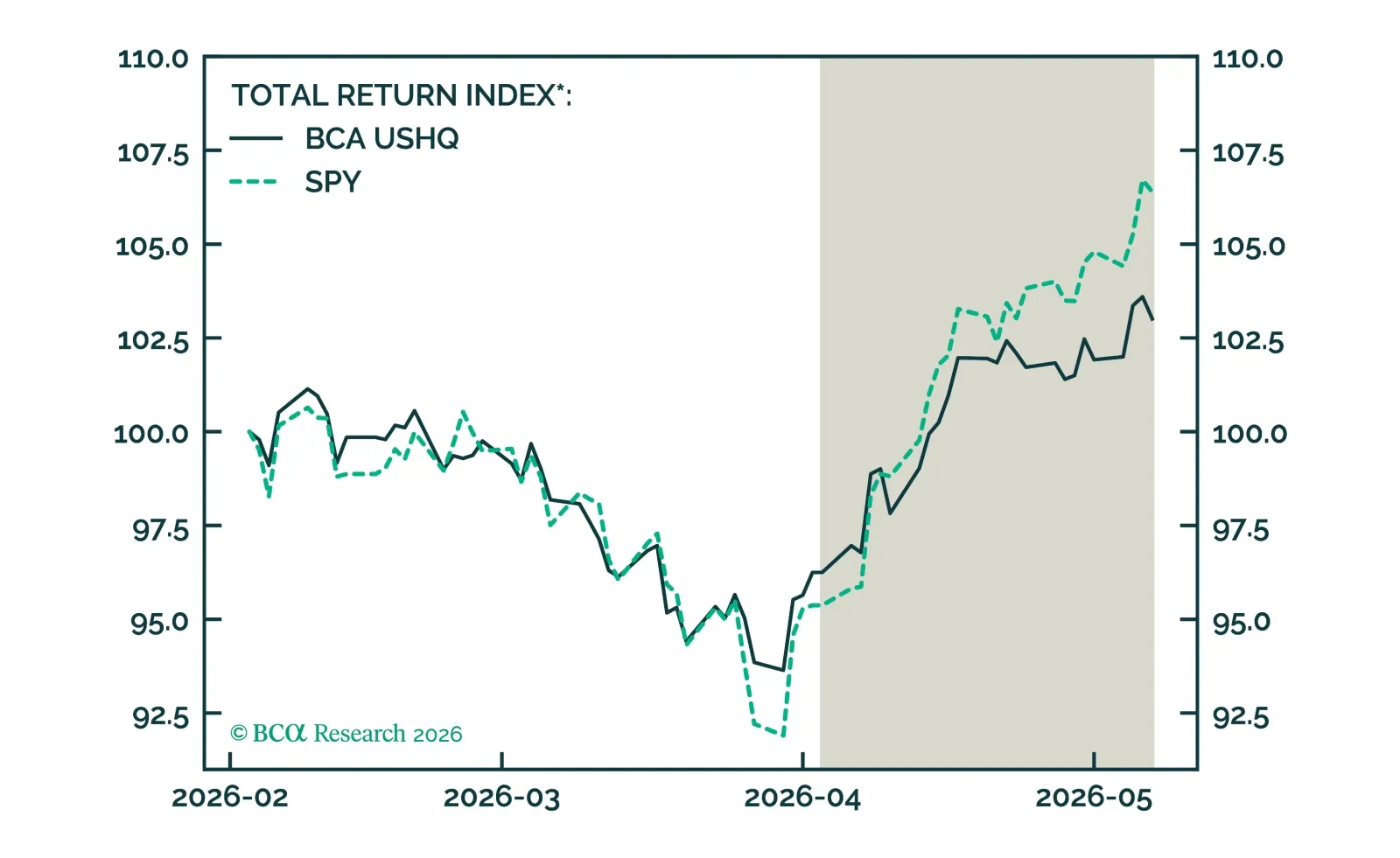

The US High Quality (USHQ) portfolio underperformed its benchmark through April, returning 7.02%, while its SPY benchmark returned 11.55%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark as well, with USHQ underperforming by approx. 338bps.

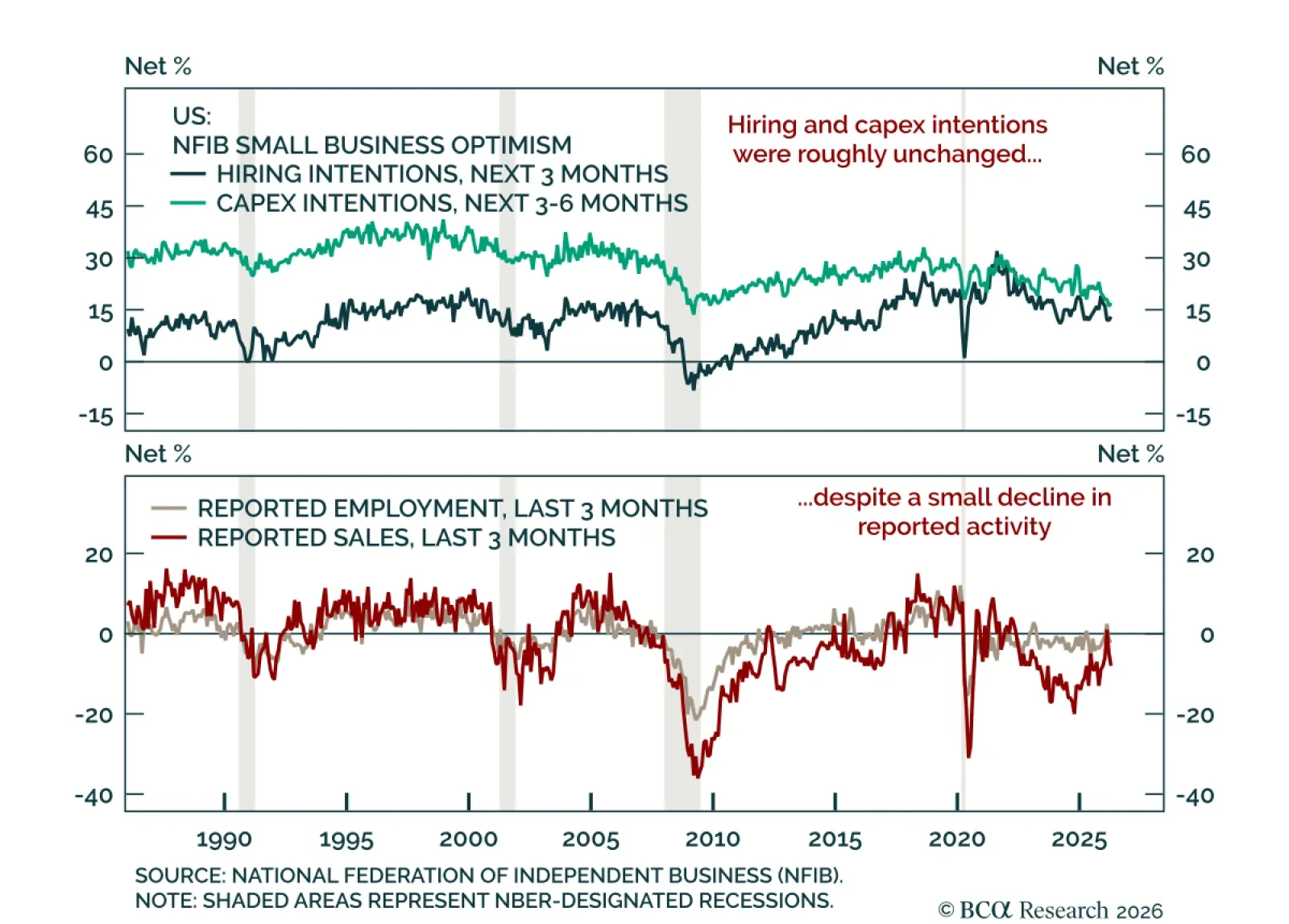

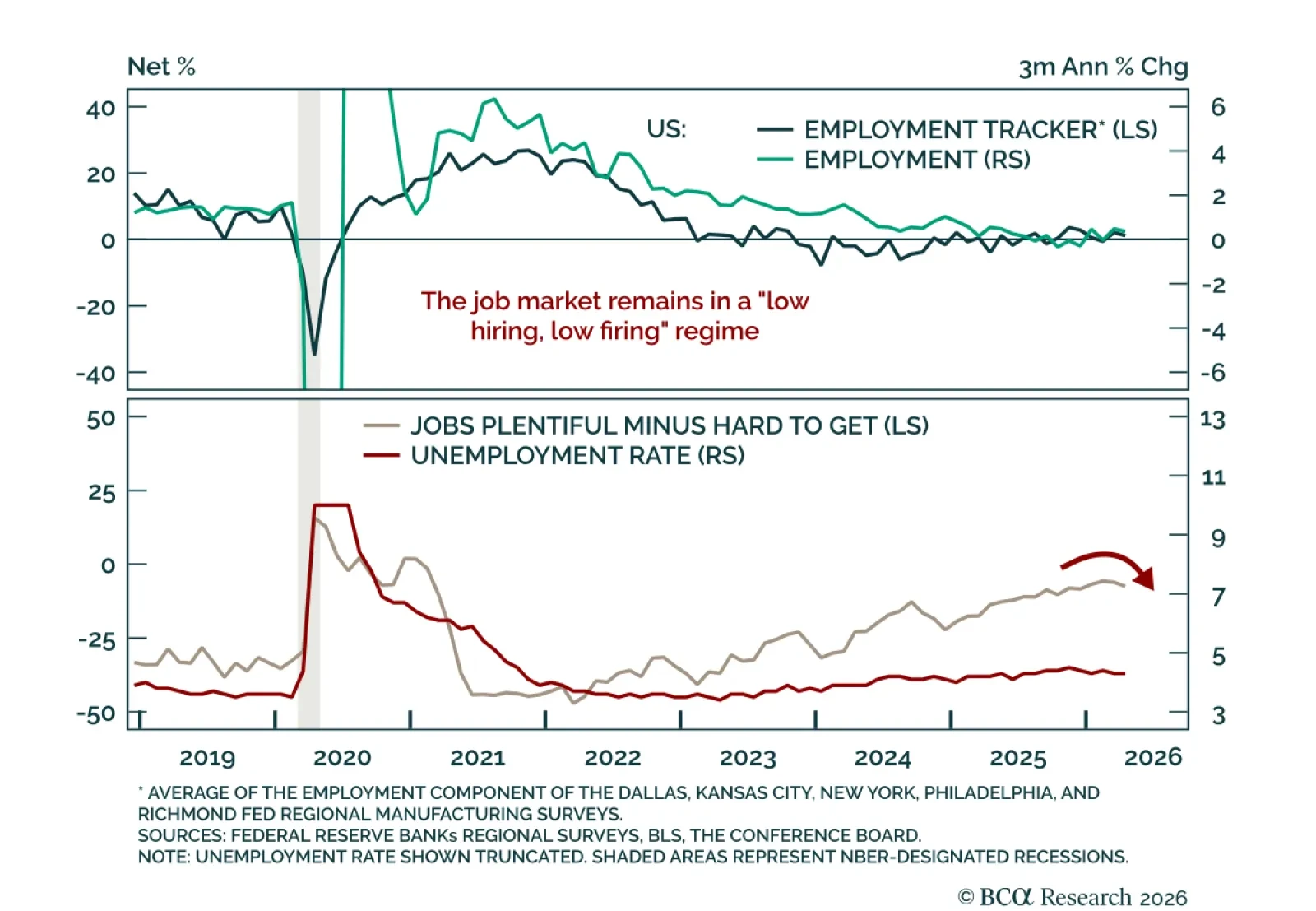

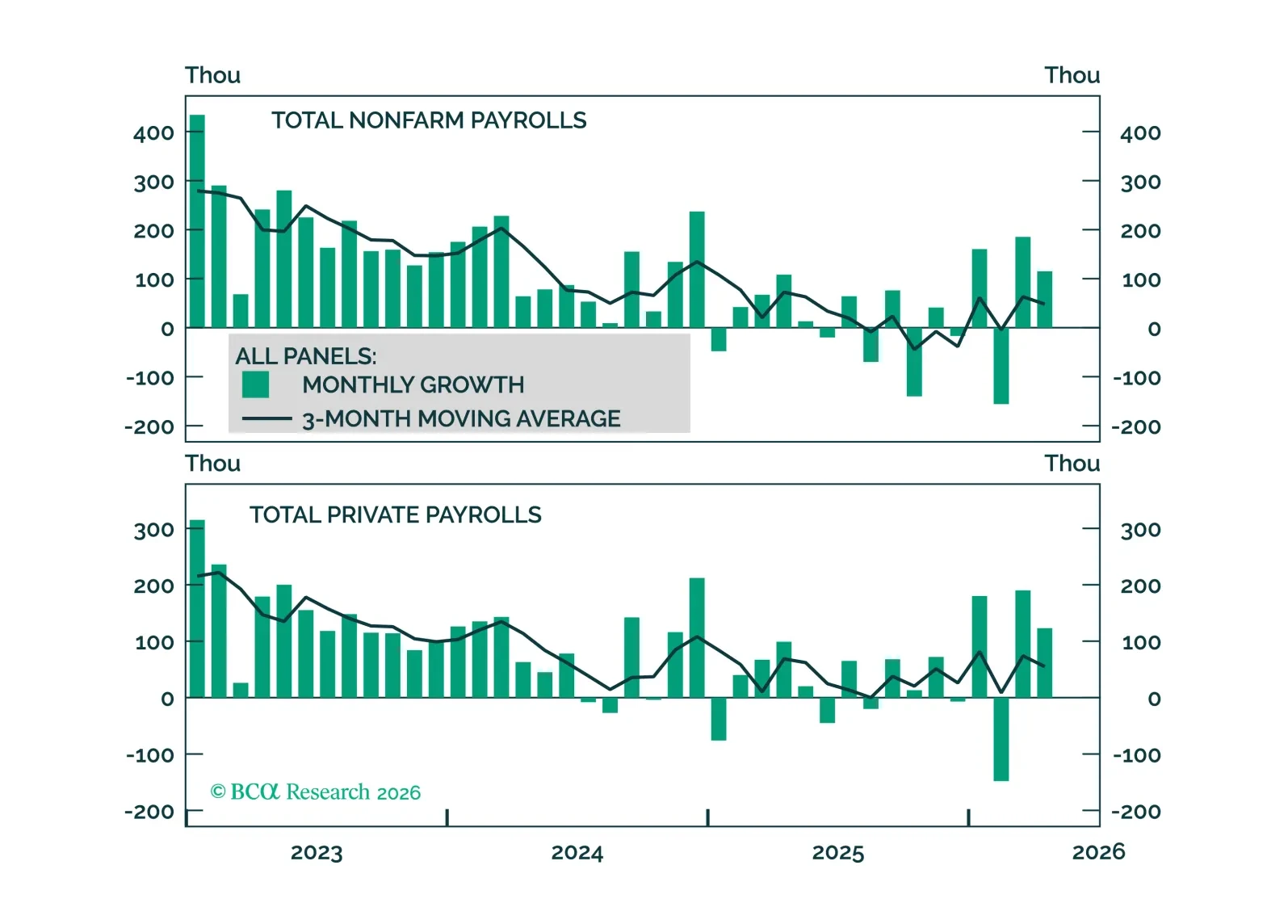

Improving job growth keeps Fed rate cuts off the table, but evidence of labor market tightening will be required before rate hikes become part of the discussion.

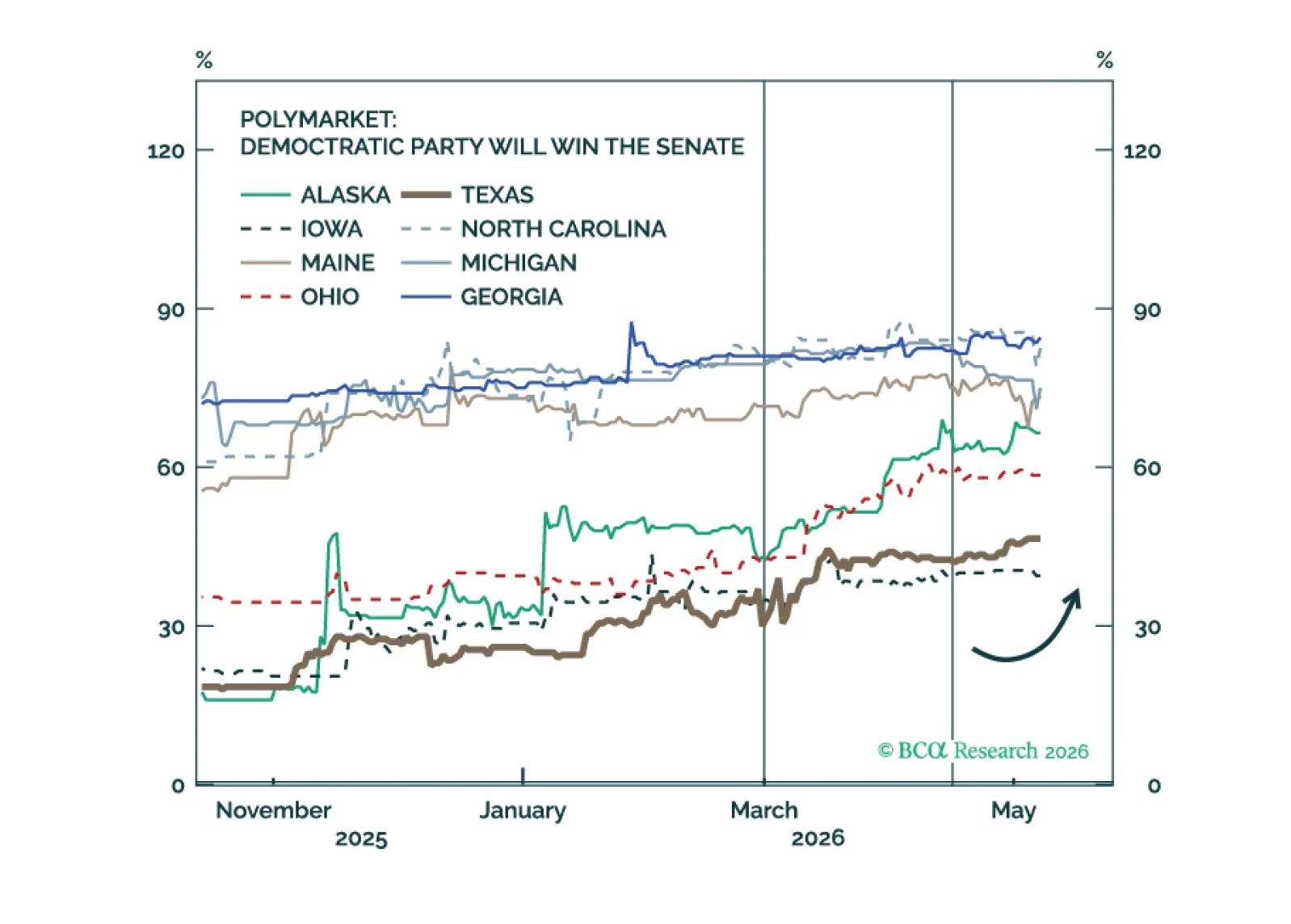

Aggregate Senate betting market pricing appears too pessimistic on Democrats relative to state-level odds and early polling, suggesting a potential mispricing and a relatively sanguine attitude towards the still-unresolved conflict in Iran and its aftermath.