United States

Highlights Chart 1Reduce Credit Exposure

Reduce Credit Exposure

Reduce Credit Exposure

Corporate bond spreads staged a nice rally during the past month. The average index spread for investment grade corporates is only 22 bps above its pre-COVID low and 33 bps above last year’s trough. The average High-Yield index spread is 5 bps above its pre-COVID low and 49 bps above last year’s trough (Chart 1). This rally occurred even as inflation data continued to surprise to the upside and employment data confirmed that the US labor market is extremely tight. With the economic data justifying the Fed’s hawkish pivot, the Treasury curve has flattened dramatically, and both the 2-year/10-year and 3-year/10-year slopes are now inverted (Chart 1, bottom panel). An inverted yield curve is a reliable late-cycle indicator, and we think current spread levels offer a good opportunity to reduce corporate bond exposure. This week, we downgrade investment grade corporates from neutral (3 out of 5) to underweight (2 out of 5) and high-yield corporates from overweight (4 out of 5) to neutral (3 out of 5), placing the proceeds into Treasuries. We also downgrade our recommended allocations EM Sovereigns (see page 8) and TIPS (see page 11), upgrade our recommended allocation to CMBS (see page 13) and adjust our recommended yield curve positioning (see page 10). Feature Table 1Recommended Portfolio Specification

The Beginning Of The End

The Beginning Of The End

Table 2Fixed Income Sector Performance

The Beginning Of The End

The Beginning Of The End

Investment Grade: Underweight Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 86 basis points in March, bringing year-to-date excess returns up to -154 bps. Our quality-adjusted 12-month breakeven spread shifted down to its 21st percentile since 1995 (Chart 2). As noted on the first page of this report, corporate spreads have rallied to within striking distance of their pre-COVID lows at the same time as the yield curve has become inverted beyond the 2-year maturity. We showed in last week’s report that an inversion of the 2-year/10-year Treasury slope is not necessarily a harbinger of imminent recession, but it does typically coincide with very low (and often negative) excess corporate bond returns.1 The combination of reasonably tight spreads and an inverted yield curve causes us to recommend downgrading investment grade corporate bond allocations from neutral (3 out of 5) to underweight (2 out of 5). It’s important to note that corporate balance sheets remain healthy (bottom panel) and we see no indication that a recession or default cycle will unfold during the next 6-12 months. That said, we must acknowledge that an inverted yield curve signals that the economic recovery is entering its late stages. Economic growth will be slower going forward and corporate spreads are unlikely to tighten much, especially from current depressed levels. Against this backdrop it makes sense to be more cautious on credit, sacrificing small positive excess returns in the near-term to ensure that we aren’t invested when the next downturn hits. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Beginning Of The End

The Beginning Of The End

Table 3BCorporate Sector Risk Vs. Reward*

The Beginning Of The End

The Beginning Of The End

High-Yield: Neutral Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 119 basis points in March, bringing year-to-date excess returns up to -96 bps. The 12-month spread-implied default rate – the default rate that is priced into the junk index assuming a 40% recovery rate on defaulted debt and an excess spread of 100 bps – shifted down to 3.7% (Chart 3). An inverted yield curve sends the same negative signal for high-yield excess returns as it does for investment grade. However, high-yield valuation is currently more attractive. The option-adjusted spread differential between Ba-rated bonds and Baa-rated bonds remains elevated at 86 bps, 41 bps above its pre-COVID low (panel 3). It is also likely that economic growth will remain sufficiently strong for defaults to come in below the spread-implied threshold of 3.7% during the next 12 months (bottom panel). The greater attractiveness of high-yield valuations relative to investment grade causes us to maintain a higher allocation to the sector, even as we downgrade our portfolio’s overall credit risk exposure. We therefore recommend a neutral (3 out of 5) allocation to high-yield corporates. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 14 basis points in March, dragging year-to-date excess returns down to -74 bps. The zero-volatility spread for conventional 30-year agency MBS tightened 3 bps on the month as a 4 bps tightening of the option-adjusted spread (OAS) was partially offset by a 1 bp increase in the compensation for prepayment risk (option cost) (Chart 4). We wrote in a recent report that MBS’ poor performance in 2021 was attributable to an option cost that was too low relative to the pace of mortgage refinancings, noting that the MBA Refinance Index was slow to fall in 2021 despite the back-up in yields.2 This valuation picture is starting to change. The option cost is now up to 40 bps, its highest level since 2016, and refi activity is slowing as the Fed lifts rates. At 28 bps, the index OAS remains unattractive. However, the elevated option cost raises the possibility that the OAS may be over-estimating the pace of mortgage refinancings for the first time in a while. If these trends continue, it may soon make sense to increase exposure to agency MBS. Emerging Market Bonds (USD): Underweight Chart 5Emerging Markets Overview

Emerging Markets Overview

Emerging Markets Overview

Emerging Market bonds underperformed the duration-equivalent Treasury index by 23 basis points in March, dragging year-to-date excess returns down to -505 bps. EM Sovereigns outperformed the Treasury benchmark by 40 bps on the month, bringing year-to-date excess returns up to -609 bps. The EM Corporate & Quasi-Sovereign Index underperformed by 62 bps, dragging year-to-date excess returns down to -439 bps. The EM Sovereign Index underperformed the duration-equivalent US corporate bond index by 7 bps in March. This comes on the heels of a sharp underperformance in February that was driven by Russian bonds which have since been removed from the index. Russian bonds have also been purged from the EM Corporate & Quasi-Sovereign Index, and this index underperformed duration-matched US corporates by 11 bps in March (Chart 5). The yield differential between EM sovereigns and duration-matched US corporates remains negative. As such, we downgrade our recommended allocation to EM sovereigns from underweight (2 out of 5) to maximum underweight (1 out of 5). In sharp contrast, the EM Corporate & Quasi-Sovereign Index continuous to offer a significant yield advantage (panel 4). We retain our neutral (3 out of 5) recommendation for EM Corporates & Quasi-Sovereigns. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds outperformed the duration-equivalent Treasury index by 5 basis points in March, bringing year-to-date excess returns up to -122 bps (before adjusting for the tax advantage). While the war in Ukraine has introduced a great deal of uncertainty into the economic outlook, the municipal bond sector should be better placed than most to deal with the fallout. Trailing 4-quarter net state & local government savings are incredibly high (Chart 6) and 2021’s federal spending splurge will continue to support state & local government coffers for some time. On the valuation front, munis have cheapened up relative to both Treasuries and corporates during the past two months. The 10-year Aaa Muni / Treasury yield ratio is currently at 94%, up significantly from its 2021 trough of 55%. The yield ratios between 12-17 year munis and duration-matched corporate bonds are also up significantly off their lows (panel 2). We reiterate our overweight allocation to municipal bonds within US fixed income portfolios, and we continue to have a strong preference for long-maturity munis. The yield ratio between 17-year+ General Obligation Municipal bonds and duration-matched corporates is 93%. The same measure for 17-year+ Revenue bonds stands at 101%, meaning that Revenue bonds carry a before-tax yield advantage versus duration-matched corporates. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve’s bear-flattening trend continued through March. The 2-year/10-year Treasury slope flattened 35 bps on the month and the 5-year/30-year Treasury slope flattened 44 bps. These slopes are now both inverted, sitting at -6 bps and -12 bps respectively. In last week’s report we noted the unusually wide divergence between very flat slopes at the long end of the yield curve and very steep slopes at the front end.3 For example, the 5-year/10-year Treasury slope is -18 bps but the 3-month/5-year slope is 204 bps. This divergence is happening because the market has moved quickly to price-in a rapid near-term pace of rate hikes that will end in roughly one year. However, so far, the Fed has only delivered 25 bps of those hikes and this is holding down the very front-end of the curve. The oddly shaped curve presents us with an excellent trading opportunity. Specifically, we recommend buying the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. This trade looks attractive on our model (Chart 7) and will profit if the rate hike cycle moves more slowly than what is currently priced in the market but lasts longer, as is our expectation. By entering our new 5-year bullet over 2-year/10-year barbell trade we also close our previous 2-year bullet over cash/10-year barbell trade at a loss. We continue to recommend a position long the 20-year bullet versus a duration-matched 10/30 barbell as an attractive carry trade. TIPS: Underweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 143 basis points in March, bringing year-to-date excess returns up to +271 bps. The 10-year TIPS breakeven inflation rate rose 22 bps on the month and the 5-year/5-year forward TIPS breakeven inflation rate rose 21 bps. Since last May we have been recommending that clients maintain a neutral allocation to TIPS versus nominal Treasuries at the long end of the curve and an underweight allocation to TIPS at the front end. This recommendation was premised on the view that the breakeven curve would steepen as falling inflation put downward pressure on short-maturity TIPS breakevens and long-dated breakevens remained at levels close to the Fed’s target. Recently, the 10-year TIPS breakeven inflation rate has shot up to levels well above the Fed’s 2.3%-2.5% target range (Chart 8) and our TIPS Breakeven Valuation Indictor has shifted into “expensive” territory (panel 2). Further, while inflation has remained high for longer than we expected, it still seems more likely than not that it will roll over between now and the end of the year as pandemic fears fade and consumers shift their spending patterns away from goods and toward services. As such, we think investors should take this opportunity to further reduce exposure to TIPS versus nominal Treasuries at both the short and long ends of the curve. That is, within our overall underweight allocation to TIPS we continue to recommend positioning in breakeven curve steepeners and in real yield curve flatteners. We also continue to recommend an outright short position in 2-year TIPS. ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities underperformed the duration-equivalent Treasury index by 26 basis points in March, dragging year-to-date excess returns down to -31 bps. Aaa-rated ABS underperformed by 21 bps on the month, dragging year-to-date excess returns down to -27 bps. Non-Aaa ABS underperformed by 49 bps on the month, dragging year-to-date excess returns down to -51 bps. During the past two years, substantial federal government support for household incomes has caused US households to build up an extremely large buffer of excess savings. During this period, many households have used their windfalls to pay down consumer debt and credit card debt levels have fallen to well below pre-COVID levels (Chart 9). Though consumer credit growth has rebounded, debt levels are still low. This indicates that the collateral quality backing consumer ABS remains exceptionally strong. This also indicates that while surging gasoline prices will weigh on consumer activity in the coming months, household balance sheets are starting from such a good place that we don’t expect a meaningful increase in consumer credit delinquencies. Investors should remain overweight consumer ABS and should take advantage of the high quality of household balance sheets by moving down the quality spectrum, favoring non-Aaa rated securities over Aaa-rated ones. Non-Agency CMBS: Overweight Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 20 basis points in March, bringing year-to-date excess returns up to -78 bps. Aaa Non-Agency CMBS outperformed Treasuries by 25 bps on the month, bringing year-to-date excess returns up to -67 bps. Non-Aaa Non-Agency CMBS underperformed by 5 bps on the month, dragging year-to-date excess returns down to -110 bps. CMBS spreads remain wide compared to other similarly risky spread products. Further, commercial real estate (CRE) lending standards have recently shifted into “net easing” territory and demand for CRE loans is strengthening (Chart 10). In light of today’s downgrade of corporate credit, non-agency CMBS look like an attractive alternative to add some spread to a portfolio. Increase exposure from neutral (3 out of 5) to overweight (4 out of 5). Agency CMBS: Overweight Agency CMBS underperformed the duration-equivalent Treasury index by 17 basis points in March, dragging year-to-date excess returns down to -39 bps. The average index option-adjusted spread widened 5 bps on the month. It currently sits at 48 bps, not that far from its average pre-COVID level (bottom panel). Agency CMBS spreads also continue to look attractive compared to other similarly risky spread products. Stay overweight. Appendix A: The Golden Rule Of Bond Investing We follow a two-step process to formulate recommendations for bond portfolio duration. First, we determine the change in the federal funds rate that is priced into the yield curve for the next 12 months. Second, we decide – based on our assessments of the economy and Fed policy – whether the change in the fed funds rate will exceed or fall short of what is priced into the curve. Most of the time, a correct answer to this question leads to the appropriate duration call. We call this framework the Golden Rule Of Bond Investing, and we demonstrated its effectiveness in the US Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018. Chart 11 illustrates the Golden Rule’s track record by showing that the Bloomberg Barclays Treasury Master Index tends to outperform cash when rate hikes fall short of 12-month expectations, and vice-versa. At present, the market is priced for 255 basis points of rate hikes during the next 12 months. Chart 11The Golden Rule's Track Record

The Golden Rule's Track Record

The Golden Rule's Track Record

We can also use our Golden Rule framework to make 12-month total return and excess return forecasts for the Bloomberg Barclays Treasury index under different scenarios for the fed funds rate. Excess returns are relative to the Bloomberg Barclays Cash index. To forecast total returns we first calculate the 12-month fed funds rate surprise in each scenario by comparing the assumed change in the fed funds rate to the current value of our 12-month discounter. This rate hike surprise is then mapped to an expected change in the Treasury index yield using a regression based on the historical relationship between those two variables. Finally, we apply the expected change in index yield to the current characteristics (yield, duration and convexity) of the Treasury index to estimate total returns on a 12-month horizon. The below tables present those results, along with excess returns for a front-loaded and a back-loaded rate hike scenario. Excess returns are calculated by subtracting assumed cash returns in each scenario from our total return projections.

The Beginning Of The End

The Beginning Of The End

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of March 31, 2022)

The Beginning Of The End

The Beginning Of The End

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of March 31, 2022)

The Beginning Of The End

The Beginning Of The End

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of -55 bps in the 5 over 2/10 cell means that we would expect the 5-year to outperform the 2/10 if the 2/10 slope flattens by less than 55 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Beginning Of The End

The Beginning Of The End

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 12Excess Return Bond Map (As Of March 31, 2022)

The Beginning Of The End

The Beginning Of The End

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy / US Investment Strategy / US Equity Strategy Special Report, “The Yield Curve As An Indicator”, dated March 29, 2022. 2 Please see US Bond Strategy Weekly Report, “The Omicron Impact”, dated November 30, 2021. 3 Please see US Bond Strategy / US Investment Strategy / US Equity Strategy Special Report, “The Yield Curve As An Indicator”, dated March 29, 2022. Recommended Portfolio Specification

The Beginning Of The End

The Beginning Of The End

Other Recommendations

The Beginning Of The End

The Beginning Of The End

Treasury Index Returns Spread Product Returns

Executive Summary Our recommended model bond portfolio outperformed its custom index by a robust +48bps in Q1/2022 – an impressive performance given the significant uncertainties stemming from the Ukraine war, surging commodity prices and hawkish central banks. This outperformance came entirely from the rates side of the portfolio (+52bps) as global government bond yields surged, driven by a large underweight to US Treasuries. The credit side of the portfolio was largely unchanged versus the benchmark (-4bps). Looking ahead, we see global bond yields as being more rangebound over the next six months. A lot of rate hikes in 2022 are already discounted (most notably in the US) and global inflation is likely to decelerate in Q2 & Q3. As the global monetary tightening cycle evolves, positioning more defensively in global credit, rather than duration management, will provide the better opportunity to generate alpha in bond portfolios. GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Bottom Line: In our model bond portfolio, we are downgrading US investment grade corporates to underweight, and reducing high-yield exposure in the US and Europe to neutral. We are also reducing inflation-linked bond allocations in the US and euro area to underweight versus nominals. Feature The first three months were horrific for global bond markets. The Bloomberg Global Aggregate index delivered a total return of -6.2%, the second worst quarter since 1990. No sector, from government bonds to corporate debt to emerging market spread product, was immune to the pressures from soaring energy prices, war-driven uncertainty and hawkish central bankers belated responding to the worst bout of global inflation since the 1970s. Related Report Global Fixed Income StrategyOur Model Bond Portfolio Strategy To Begin 2022: Choosing Our Battles Wisely That toxic cocktail for bond returns may lose some potency in the coming months if a de-escalation of the Ukraine tensions can be reached. However, the bigger drivers of bond market volatility – high global inflation and the monetary tightening necessary to combat it – are more likely to linger for longer than expected. Government bond yields are unlikely to fall much in this environment. Increasingly, global credit spreads, especially for corporate debt in the US, will face intensifying widening pressure as central banks rapidly dial back pandemic-era monetary accommodation, led by the US Federal Reserve. With that in mind, we present our quarterly review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio for the first quarter of 2022. We also present our recommended positioning for the portfolio for the next six months, as well as portfolio return expectations for our base case and alternative investment scenarios. As a reminder to existing readers (and to new clients), the model portfolio is a part of our service that complements the usual macro analysis of global fixed income markets. The portfolio is how we communicate our opinion on the relative attractiveness between government bond and spread product sectors. We do this by applying actual percentage weightings to each of our recommendations within a fully invested hypothetical bond portfolio. Q1/2022 Model Bond Portfolio Performance: Regional Allocation Drives Outperformance Chart 1Q1/2022 Performance: Big Gains From Rising Bond Yields

Q1/2022 Performance: Big Gains From Rising Bond Yields

Q1/2022 Performance: Big Gains From Rising Bond Yields

The total return for the GFIS model portfolio (hedged into US dollars) in the third quarter was -4.6%, outperforming the custom benchmark index by +48bps (Chart 1).1 In terms of the specific breakdown between the government bond and spread product allocations in our model portfolio, the former generated +52bps of outperformance versus our custom benchmark index while the latter underperformed by -4bps. In an extremely negative quarter for fixed income both in terms of the breadth and depth of losses, our regional allocation choices helped us continue generating outperformance after we transitioned to a neutral overall portfolio duration stance in mid-February. Throughout the quarter, we maintained a significant underweight on US Treasuries in the portfolio, even after we tactically upgraded our duration tilt. We expected US government debt to still underperform that of other developed markets, even in an environment where the rise in global bond yields was due for a breather. Our rationale worked – admittedly helped by the inflationary shock of the Russian invasion of Ukraine - with the US Treasury part of our portfolio generating a whopping +63bps of outperformance (Table 1). Table 1GFIS Model Bond Portfolio Q1/2022 Overall Return Attribution

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Meanwhile, our biggest government bond overweights were in Europe, a market we expected to perform defensively in a portfolio context. We were obviously caught offside on this call as energy prices and inflation expectations in Europe surged in response to the Ukraine conflict. In total, our portfolio lost -30bps in active return terms in euro area government bonds, with the losses spread evenly between the core and periphery. We did staunch the bleeding somewhat by reducing our allocation to the periphery in the last two weeks of the quarter and using the proceeds to fund an increased allocation to European investment grade corporates. The European corporate index spread has tightened -23bps since that switch. Turning to the credit side of the portfolio, the most successful position was our underweight tilt on emerging market (EM) USD-denominated corporates (+10bps) and sovereigns (+9bps) during a catastrophic quarter for EM risky assets driven by the conflict as well as weakness in the Chinese economy. We sustained losses from our overweight on US CMBS (-11bps) which was broadly offset by gains from our underweight on US MBS (+10bps). Lastly, while we were hurt by the sell-off in euro area high-yield (-13bps), where we were overweight to start 2022, we did scale back some of that exposure towards the end of the quarter when markets started to discount the risk of a “worst case” scenario of direct NATO intervention in Ukraine. The bar charts showing the total and relative returns for each individual government bond market and spread product sector in our model portfolio are presented in Charts 2 & 3. Chart 2GFIS Model Bond Portfolio Q1/2022 Government Bond Performance Attribution

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Chart 3GFIS Model Bond Portfolio Q1/2022 Spread Product Performance Attribution By Sector

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Biggest Outperformers: Underweight US Treasuries with a maturity greater than 10 years (+23bps) Underweight UK Gilts with a maturity greater than 10 years (+14bps) Underweight US treasuries with a maturity between 3 and 5 years (+12bps) Biggest Underperformers: Overweight euro area high-yield corporates (-13bps) Overweight US CMBS (-11bps) Overweight Spanish Bonos (-5bps) Chart 4 presents the ranked benchmark index returns of the individual countries and spread product sectors in the GFIS model bond portfolio for Q1/2022. Returns are hedged into US dollars (we do not take active currency risk in this portfolio) and adjusted to reflect duration differences between each country/sector and the overall custom benchmark index for the model portfolio. We have also color coded the bars in each chart to reflect our recommended investment stance for each market during Q1 (red for underweight, dark green for overweight, gray for neutral). Chart 4Ranking The Winners & Losers From The GFIS Model Bond Portfolio Universe In Q1/2022

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Ideally, we would look to see more green bars on the left side of the chart where market returns are highest, and more red bars on the right side of the chart were returns are lowest. That pattern largely held true in Q1/2022, especially at the tail ends of the chart. During a quarter where all the major asset classes in our portfolio lost money on a hedged and duration-matched basis, we outperformed by selectively underweighting the worst performers. Notably, we were underweight UK Gilts (-1280bps) and EM Sovereigns (-1103bps) on the extreme right side of the chart. We were also underweight US Treasuries (-531bps) which, despite being in the middle of Chart 4, contributed hugely to our portfolio outperformance due to their large market cap weighting in the benchmark index. Broadly, this means that, except for Europe and Australia, our highest conviction calls worked in our favor during the quarter. Bottom Line: Our model bond portfolio outperformed its benchmark index in the third quarter of the year by +48bps – a positive result coming largely from underweight positions in US Treasuries, UK Gilts, and EM credit. Changes To Our Model Bond Portfolio Allocations The uncertainty stemming from the Russia/Ukraine conflict led us to temporarily neutralize many of the recommended exposures in the model bond portfolio. We not only moved to neutral on overall portfolio duration, we also neutralized individual country yield curve tilts and inflation-linked bond allocations. While the situation remains fluid, the worst-case scenarios of the conflict expanding beyond the borders of Ukraine appear to have been avoided. This leads us to reconsider where to once again take active risks on the rates side of the portfolio. Chart 5Our Duration Indicator Calling For Slowing Global Yield Momentum

Our Duration Indicator Calling For Slowing Global Yield Momentum

Our Duration Indicator Calling For Slowing Global Yield Momentum

Duration On overall portfolio duration, we are maintaining a neutral (“at benchmark”) stance in the portfolio. Our Global Duration Indicator is currently signaling that the strong upward momentum of global bond yields should fade over the next few months (Chart 5). Slowing global growth expectations – a trend that was already in place prior to the Ukraine conflict - are the major reason why our Duration Indicator has turned lower. The war-fueled surge in energy prices has helped push global bond yields higher through rising inflation breakevens, which also prompted central banks – most notably the Fed and the Bank of England (BoE)- to signal a need for a faster pace of interest rate hikes in 2022 despite softening growth momentum. Looking ahead, that strong link between oil prices and bond yields will not be broken until there is some sort of de-escalation of the Ukraine conflict, which does not appear imminent. This supports a near-term neutral overall duration stance. Yield Curve Allocations In terms of yield curve exposure, we see some opportunities to adjust allocations (Chart 6). US curves have inverted and UK curves are flirting with inversion as markets are pricing in more Fed/BoE tightening, while curves in Germany and France have bear-steepened with longer-term inflation expectations going up faster than shorter-term interest rate expectations. In the US and UK, the yield curve flattening also reflects the “front loading” of Fed/BoE rate hike expectations. Overnight index swap (OIS) curves are pricing in 190bps of rate hikes in the US, and 134bps in the UK, by the end of 2022. This is followed quickly by rate cuts discounted in H2/2023 and 2024 in both countries. We see it as more likely that both central banks will deliver fewer hikes than discounted in 2022 and but will push rates to higher levels than priced by the end of 2024. That leads us to add a mild steepening bias into our US and UK government bond allocations in the model bond portfolio. We offset that by inserting a flattening bias in the German and French yield curve allocations to keep the overall portfolio duration at 7.5 years, matching that of the custom benchmark index (Chart 7). Chart 6Curve Flattening In The US & UK Is Overdone

Curve Flattening In The US & UK Is Overdone

Curve Flattening In The US & UK Is Overdone

Chart 7Overall Portfolio Duration: Stay Neutral

Overall Portfolio Duration: Stay Neutral

Overall Portfolio Duration: Stay Neutral

Chart 8No Change To Our Country Allocations To Begin Q2/22

No Change To Our Country Allocations To Begin Q2/22

No Change To Our Country Allocations To Begin Q2/22

Country Allocations Turning to our country allocations, we see no need to make major changes right now (Chart 8). We still prefer to maintain an underweight stance on countries that are more likely to see multiple central bank rate hikes in 2022 (the US, UK, Canada) versus those that are less likely (Germany, France, Japan, Australia). We are also staying neutral on Italian and Spanish government bonds with the ECB set to taper the pace of its asset purchases in Q2. Less ECB buying raises the risk that higher yields will be required to entice private sector buyers to buy Italian and Spanish debt with a smaller central bank backstop. Inflation-Linked Bonds Our Comprehensive Breakeven Inflation (CBI) indicators assess the potential for a significant move in 10-year breakeven inflation rates, based on deviations from variables that typically correlate with breakevens like oil prices or survey-based measures of inflation expectations. At the moment, none of the CBIs for the eight countries in our model bond portfolio are below zero (Chart 9), which would be a signal that breakevens are too low and can move higher. Chart 9Inflation-Linked Bond Exposure: Reduce Europe & The US, Increase Canada

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Canada has the lowest CBI, and last week, we added a tactical trade to go long 10-year Canadian inflation breakevens. We will add that position to our model bond portfolio this week, moving the Canadian “linkers” allocation to overweight versus nominal Canadian government bonds (within an overall underweight allocation to Canada in the model bond portfolio). On the other side of our CBI rankings are countries where the CBIs are well above zero and breakevens are more stretched: Germany, Italy, France and the US. We are currently neutral inflation-linked bonds in those four countries, but strictly as a hedge against the war-fueled risks of further increases in oil prices. Now, however, 10-year breakevens have widened to levels that already factor in more expensive oil, even with oil prices struggling to break out to new highs. As a result, we are downgrading the allocation to linkers in Germany, Italy, France and the US to underweight within the model bond portfolio (Chart 10). Corporate Bonds The most meaningful changes we are making to our model bond portfolio, and in our strategic investment recommendations, are to our corporate bond allocations: We are downgrading US investment grade corporate bond exposure from neutral to underweight (2 out of 5) We are downgrading US high-yield corporate bond exposure from overweight to neutral (3 out of 5) We are also downgrading euro area high-yield exposure from overweight to neutral (3 out of 5) Credit spreads across the developed market and EM space have fully unwound the surge seen after Russia invaded Ukraine on February 24 (Chart 11). We had turned more cautious on global spread product exposure in early March because of the war-fueled shock to energy prices and investor sentiment. We viewed this as a bigger issue for European and EM credit, with Europe heavily reliant on Russian energy supplies and EM market liquidity impacted by bans on trading of Russian assets. We therefore reduced exposures to European high-yield and EM hard currency debt in the model bond portfolio. Chart 10Our Inflation-Linked Bond Country Allocations

Our Inflation-Linked Bond Country Allocations

Our Inflation-Linked Bond Country Allocations

Now, while markets have become more sanguine about the prospects of a long war that can more directly draw in Western forces, a bigger threat to financial market stability has emerged – more aggressive tightening of global monetary policy led by the Fed. Chart 11Global Credit Spreads Have Returned To Pre-Invasion Levels

Global Credit Spreads Have Returned To Pre-Invasion Levels

Global Credit Spreads Have Returned To Pre-Invasion Levels

Chart 12Global Monetary Backdrop Turning More Negative For Credit

Global Monetary Backdrop Turning More Negative For Credit

Global Monetary Backdrop Turning More Negative For Credit

Already, the move away from quantitative easing by the Fed, ECB and BoE has led to a negative impulse for global credit returns (Chart 12). Excess returns for the Bloomberg Global Corporate and High-Yield indices are now essentially flat on a year-over-year basis, and the riskiest credit tiers of both indices are seeing the greater spread widening (bottom panel). Another indicator of tightening monetary policy, the flat US Treasury curve, is also signaling a poor environment for US credit market returns. Our colleagues at our sister service, BCA Research US Bond Strategy, have noted that when the 2-year/10-year US Treasury curve flattens below +25bps, the odds of US investment grade credit outperforming duration-matched Treasuries decline sharply. Dating back to 1973, the average excess return (over Treasuries) for the Bloomberg US investment grade index over the twelve months after the 2/10 curve flattens below +25bps is -0.56%. The 2/10 US Treasury curve is now inverted at -3bps, even with the Fed having only delivered a single +25bp rate hike so far in the current cycle. This is a highly unusual occurrence, as the Treasury curve typically inverts after the Fed has delivered multiple rate hikes in a tightening cycle. Bond investors are clearly “front-running” the Fed in discounting aggressive rate hikes in 2022 in response to US inflation near 8%. We think the Fed will deliver fewer hikes than markets are discounting this year, but will do more in 2023 and 2024. Yet the message from the now-inverted yield curve, and what it means for corporate bond performance, is too powerful to ignore. This underpins our decision to downgrade our recommended allocation to US investment grade to underweight. We do not, however, see a need to move the allocations for other corporate bond markets as aggressively. The credit spread widening seen so far in 2022 in the US and Europe – a trend that was already in place before the start of the Ukraine war – has restored more value to European corporate spreads compared to US equivalents. That can be seen when looking at our preferred measure of spread valuations, 12-month breakeven spreads.2 The historical percentile ranking of the 12-month breakeven spread is 63% for euro area investment grade and a much lower 23% for US investment grade (Chart 13). The absolute level of the euro area ranking justifies maintaining an overweight stance on euro area investment grade, both in absolute terms and relative to US investment grade. A smaller gap exists for high-yield, where the euro area 12-month breakeven spread percentile ranking is 50% versus 33% in the US. Those lower percentile rankings justify no higher than a neutral allocation to high-yield on either side of the Atlantic. On the surface, maintaining a higher allocation to US high-yield over US investment grade does appear counter-intuitive in an environment where the US Treasury curve is inverted and investors are growing increasingly worried that the Fed will need to engineer a major growth slowdown to cool inflation. However, that same high inflation helps to maintain a fast enough pace of nominal economic growth to limit the default risk for riskier borrowers. Moody’s estimates that the default rate for high-yield corporates will reach 3.1% in the US and 2.6% in Europe by year-end. Using those estimates, we can calculate a default-adjusted spread, or the current high-yield spread minus one-year-ahead expected default losses. That spread is currently 134bps in the US and 206bps in Europe, both well above the low end of the long-run range and closer to the long-run average (Chart 14). Those are levels that are consistent with a neutral allocation to high-yield in both regions, as current spreads offer a decent cushion in an environment of relatively low default risk. Chart 13More Attractive Spread Levels In Europe Vs. US

More Attractive Spread Levels In Europe Vs. US

More Attractive Spread Levels In Europe Vs. US

Chart 14Low Default Risk Helps Support High-Yield Valuations

Low Default Risk Helps Support High-Yield Valuations

Low Default Risk Helps Support High-Yield Valuations

Chart 15Persistent Headwinds To EM Credit Performance

Persistent Headwinds To EM Credit Performance

Persistent Headwinds To EM Credit Performance

Emerging Markets Finally, we continue to see more reasons to be cautious on EM USD-denominated credit, given the lack of support from typical fundamental drivers (Chart 15). Weak Chinese growth, slowing commodity price momentum (on a year-over-year basis), and a firm US dollar are all factors that weigh on EM economic growth and the ability to service hard-currency debt. We are maintaining an underweight allocation to EM USD-denominated sovereign and corporate debt in our model bond portfolio. Indications that China is ready to introduce more fiscal and monetary stimulus, and/or if the Fed’s messaging turned less hawkish – and less US dollar bullish – would be the signals necessary for us to consider an EM upgrade. Summing It All Up The full list of our recommended portfolio allocations after making all of the above changes can be seen in Table 2. The changes leave the portfolio with the following high-level characteristics: Table 2GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Chart 16Overall Portfolio Allocation: Underweight Spread Product Vs Governments

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

the overall duration exposure remains at-benchmark (i.e. neutral) the portfolio has now flipped to an underweight stance on the exposure of spread product to government bonds, equal to four percentage points of the portfolio (Chart 16) the tracking error of the portfolio, or its expected volatility in excess of that of the benchmark, is 80bps – a level similar to that before the changes were made and still well below our self-imposed 100bps tracking error limit (Chart 17) the portfolio now has a yield below that of the custom benchmark index, equal to 2.51% (Chart 18). Chart 17Overall Portfolio Risk: Moderate

Overall Portfolio Risk: Moderate

Overall Portfolio Risk: Moderate

Chart 18Overall Portfolio Yield: Below-Benchmark

Overall Portfolio Yield: Below-Benchmark

Overall Portfolio Yield: Below-Benchmark

The changes leave the portfolio much more exposed to a widening of global credit spreads than a rise in government bond yields – a desired outcome with bond yields already discounting a lot of tightening but credit spreads still at historically tight levels. Bottom Line: As the global monetary tightening cycle evolves, positioning more defensively in global credit, rather than duration management, will provide the better opportunity to generate alpha in bond portfolios. We are expressing that by cutting the exposure to corporate bonds in our model bond portfolio. Portfolio Scenario Analysis For The Next Six Months After making all the specific changes to our model portfolio weightings, which can be seen in the tables on pages 23-25, we now turn to our regular quarterly scenario analysis to determine the return expectations for the portfolio for the next six months. On the credit side of the portfolio, we use risk-factor-based regression models to forecast future yield changes for global spread product sectors as a function of four major factors - the VIX, oil prices, the US dollar and the fed funds rate (Table 3A). For the government bond side of the portfolio, we avoid using regression models and instead use a yield-beta driven framework, taking forecasts for changes in US Treasury yields and translating those in changes in non-US bond yields by applying a historical yield beta (Table 3B). Table 3AFactor Regressions Used To Estimate Spread Product Yield Changes

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Table 3BEstimated Government Bond Yield Betas To US Treasuries

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

For our scenario analysis over the next six months, we use a base case scenario plus two alternate “tail risk” scenarios. In the current environment, our scenarios center around developments in the Ukraine/Russia conflict and the impacts on uncertainty and commodity-fueled inflation. Base Case There is no further escalation of the Ukraine/Russia conflict, possibly resulting in a temporary ceasefire. Oil prices pull back on a lower war risk premium, helping lower inflation expectations. Global realized inflation peaks during Q2/2022, alongside some moderation of global growth in lagged response to high energy prices. Within that slower pace of global growth, the US outperforms Europe while Chinese growth remains weak because of COVID lockdowns (although that will eventually lead to more stimulus from Chinese policymakers). The Fed delivers 100bps of rate hikes by July, starting with a 50bp increase at the May meeting, before pausing at the September meeting in response to slowing US inflation and growth. There is a mild bear flattening of the US Treasury curve, but yields remain broadly unchanged over the full six month scenario period with the Fed not hiking by more than currently discounted. The Brent oil price retreats by -10%, the US dollar modestly appreciates by 2%, the VIX stays close to current levels at 20 and the fed funds rate reaches 1.5%. Escalation Scenario The is no reduction in Ukraine war tensions, with increased Russian aggression resulting in greater NATO military involvement. The risk premium in oil prices increases, delaying the expected peak in global inflation until the second half of 2022. Inflation expectations remain elevated. Global growth weakens more than in the base case scenario because of higher energy prices, but with US growth still outperforming Europe. China’s economy remains weighed down by COVID lockdowns and an inadequate fiscal/monetary/credit policy response. The Fed is forced to be more aggressive because of high inflation expectations, delivering 150bps of hikes by September. The US Treasury curve bear-flattens, but with Treasury yields rising across the curve through wider TIPS breakevens and greater-than-expected rate hikes keeping real yields stable. The Brent oil price rises +25%, the VIX index climbs to 30, the US dollar appreciates by +5% thanks to slowing global growth and a more aggressive move by the Fed to push the funds rate to 2%. De-Escalation Scenario There is a full and lasting ceasefire between Russia and Ukraine. The war risk premium in oil prices collapses, allowing global inflation to peak in Q2 and then decline rapidly. Global growth sentiment improves because of lower energy prices and diminished worries about a wider world war. European growth outperforms US growth (relative to expectations) as European natural gas prices decline. China responds faster than expected to the latest COVID wave with more aggressive policy stimulus. Lower inflation allows the Fed to be more patient on rate hikes, delivering only 75bps of hikes by July before pausing. The Treasury curve moderately bull-steepens, although the absolute decline in nominal Treasury yields is fairly small as lower TIPS breakevens are partially offset by higher real yields (as growth sentiment improves). The Brent oil price falls -20%, the VIX index drifts down to 18, and the US dollar depreciates by -3% as global growth improves and the Fed pushes the funds rate to a less-than-expected 1.25% by July. The excess return scenarios for the model bond portfolio, using the above inputs in our simple quantitative return forecast framework, are shown in Table 4A. The US Treasury yield assumptions are shown in Table 4B. For the more visually inclined, we present charts showing the model inputs and Treasury yield projections in Chart 19 and Chart 20, respectively. Table 4AGFIS Model Bond Portfolio Scenario Analysis For The Next Six Months

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Table 4BUS Treasury Yield Assumptions For The 6-Month Forward Scenario Analysis

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

Chart 19Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Chart 20US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

Given our neutral overall portfolio duration stance, and the mild changes in nominal bond yields implied by our forecasts, it should not be surprising that the rates side of the portfolio is expected to not contribute any excess return in Q2 and Q3. However, Fed rate hikes – which push up yields on spread product in the forecasting regressions – result in negative credit returns in all scenarios (especially in the cases where the VIX is expected to rise). Thus, the return on the credit side of the model portfolio, where we are now underweight credit risk, will be the main driver of performance, delivering a range of excess return outcomes between +29bps and +53bps. Bottom Line: The next six months will be about locking in the significant gains in our model bond portfolio performance from rising bond yields, and transitioning to outperforming via wider credit spreads in US investment grade and EM hard currency debt. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Shakti Sharma Senior Analyst ShaktiS@bcaresearch.com Footnotes 1 The GFIS model bond portfolio custom benchmark index is the Bloomberg Barclays Global Aggregate Index, but with allocations to global high-yield corporate debt replacing very high-quality spread product (i.e. AA-rated). We believe this to be more indicative of the typical internal benchmark used by global multi-sector fixed income managers. 2 12-month breakeven spreads compare the option-adjusted spread (OAS) of a credit market or sector to its duration, using Bloomberg bond index data. The breakeven spread is the amount of spread widening that must occur over a one-year horizon to make the total return of a credit instrument equal to that of duration-matched risk-free government debt. GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations* Cyclical Recommendations (6-18 Months)

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

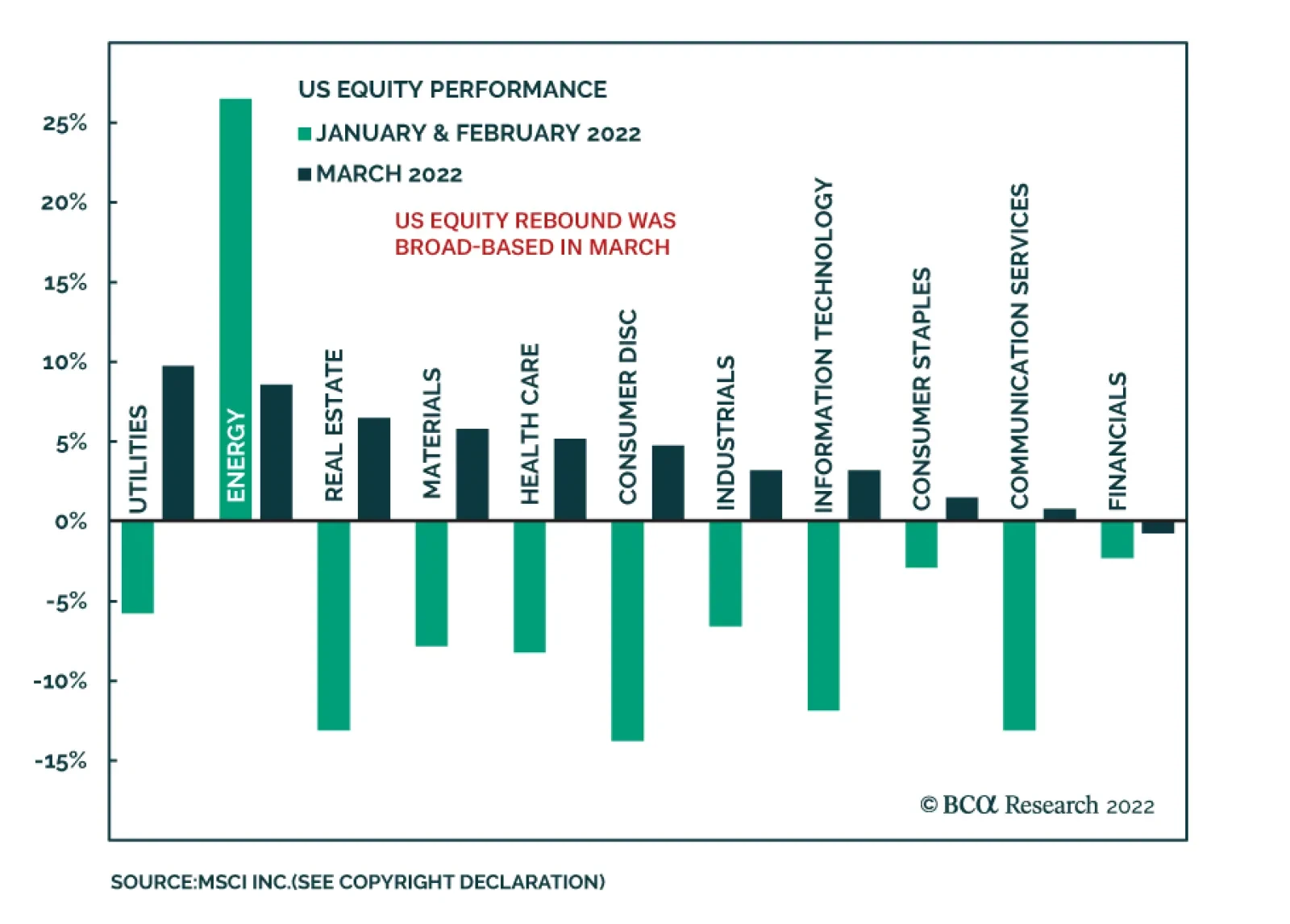

In our March In Review, we highlighted that US equities were the only major global bourse to post positive returns in March. Notably, the improvement was broad-based with nearly all US equity sectors ending the month in the green. Utilities led US stocks…

BCA Research’s US Investment Strategy service reviewed the performance of S&P 500 operating earnings, earnings multiples and returns in five inflation regimes to see how equities have responded to inflation over the last 75 years. In the extreme…

Executive Summary Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

Inflation Outlook: Inflation is becoming entrenched, spreading beyond a few pandemic-related items to “sticky price” categories. A wage-price spiral and unmoored inflation expectations translate into upside risk to the 2.5% consensus core PCE forecast. Consumer Spending: Americans are being forced to allocate a larger proportion of income towards food and gas, shifting consumption away from discretionary spending. As such, consumer spending alone may not be able to keep the economy afloat. On a 50bps hike: The rate hike increments are less important than the message the Fed is sending out to the market: Talking up 50 bp rate rises, the Fed is signaling that is it laser-focused on inflation, which is reassuring. Tightening and the economy: Aggressive monetary tightening will lead to slower economic growth, but this is not yet reflected in consensus economic growth forecasts. Recession Coming? Economic growth is slowing but off high levels, and recession is not imminent. Our recession indicator does not flash danger. However, we are watching out for a growth disappointment. Bottom Line: In a commentary to our bi-monthly sector chart pack report, we provide answers to the most frequently asked questions on the state of the US economy. Feature Performance Markets never cease to surprise. In March, US equities staged an unexpected rally despite the backdrop of a hawkish Fed, raging inflation, surging energy prices, and a war in the heart of Europe. The reversal was broad-based, not leaving a single sector in the red (Chart I-1). The S&P 500 has regained 9% since the market bottom on March 8, 2022 and is only 5.5% off its all-time high. The NASDAQ has rebounded 13%. Is this rally sustainable? In a report a couple of weeks ago, we aimed to answer this question. We recommended patience, although many ingredients, such as attractive valuations and oversold technical conditions, were already in place. Our reasons for patience were that: Economic growth expectations are still elevated and bottom-up earnings growth forecasts need to come down, to reflect slowing growth, a tighter monetary regime, and higher commodities and energy prices. Our view is unchanged. This week was a busy one: A media interview with The Deep Dive, and two virtual conferences in Australia, one run by Insider Network and the other by Equity Forum. In today’s cover report for our sector chartpack, we answer questions we received from the media and conference audience, that we believe will be of interest to clients. Chart I-1Powerful Rebound

INFLATION EXPECTATIONS

INFLATION EXPECTATIONS

Questions And Answers The Consumer Price Index (CPI) increased by 7.9% and the PCE price index, the Fed’s preferred measure of inflation, came in at 6.4% in February – readings not seen since 1982. What is your outlook on inflation? Inflation will come down, assisted by the arithmetic of the base effect. However, it is unlikely to revert to levels that the Fed and the US consumer will consider acceptable. Moreover, inflation could surprise further to the upside. The concern is that inflation is becoming entrenched. It has spread beyond a few pandemic-related items to goods for which prices are usually sticky (Chart I-2). There are also clear signs that price increases are feeding through to wage increases. Real wage growth remains negative at -2%, while demand for labor is robust – there are 1.7 open jobs per job seeker, and companies are raising wages to retain talent (Chart I-3). Subsequently, they will raise prices to pass on cost increases to customers. These are fertile conditions for a wage-price spiral, with inflation becoming even more entrenched. Chart I-2Even Sticky Prices Are Now Rising

Even Sticky Prices Are Now Rising

Even Sticky Prices Are Now Rising

Chart I-3Rising Wages Are In Lockstep With Rising Prices

Rising Wages Are In Lockstep With Rising Prices

Rising Wages Are In Lockstep With Rising Prices

Further, inflation expectations have become unmoored: According to a University of Michigan survey, consumers expect prices to rise by 5.5% over the next year, and by more than 3% a year over five to 10 years (Chart I-4). Concerningly, the upward adjustment in inflation expectations is relentless. The war in Ukraine exacerbates many causes of inflation: Its indirect effects are shortages of raw materials, energy, and shipping disruptions (Chart I-5). Chart I-4Inflation Expectations Are Unmoored

Inflation Expectations Are Unmoored

Inflation Expectations Are Unmoored

Chart I-5Supply Chains Remain Disrupted

Supply Chains Remain Disrupted

Supply Chains Remain Disrupted

Consensus forecasts for US core PCE inflation see it coming down to 2.5% by next year. The risk is that it could exceed that. Bottom Line: Inflation will come down but may not normalize any time soon. What is the effect of food and energy inflation on consumer spending? Negative real wage growth bites into consumer purchasing power, sapping confidence (Chart I-6). It does not help that food and energy prices are up by 8% and 14% respectively year over year (Chart I-7). However, the rising price of necessities has the most pronounced effect on low earners: Food accounts for more than a quarter of the after-tax income of the lowest quintile of earners, falling to just over five percent of income for top earners (Chart I-8). As many Americans are forced to allocate a larger proportion of income towards food and gas, they have to shift consumption away from discretionary spending. Thus, a high price for gasoline does not necessarily suppress demand for gasoline but rather reduces demand for, say, fast-food meals. Chart I-6High Inflation Saps Consumer Confidence

High Inflation Saps Consumer Confidence

High Inflation Saps Consumer Confidence

Chart I-7Food And Energy Prices Have Surged

Food And Energy Prices Have Surged

Food And Energy Prices Have Surged

This change in a spending basket explains a slowdown in consumer spending: PCE increased only 0.2% month-on-month in February, which is underwhelming compared to the 0.7% expected. It also explains rising credit-card balances (Chart I-9). Chart 8Rising Cost Of Food Cuts Into Discretionary Spending...

Sector Chart Pack Commentary

Sector Chart Pack Commentary

Chart I-9Many Consumers Are Struggling

Many Consumers Are Struggling

Many Consumers Are Struggling

At the same time, we know that US consumers have $2.3 trillion in excess savings – which are clearly not uniformly distributed across income groups. This nice stash of cash provides a solid consumer spending cushion for the US economy, but it may not be up to the challenge of keeping the economy afloat single-handedly. Bottom Line: For now, the US consumer is in good shape but there are cracks in the foundation as lower-income Americans are clearly struggling with rising food and gas prices. Fed Chair Jerome Powell noted last week that the Fed could raise rates from the traditional 25 basis points per meeting to 50 basis points if necessary. Do you think 50 basis points will have much of an impact on inflation or on the real economy? The Fed has gotten way behind the curve. In retrospect, it should have raised rates last summer – and it now understands its error. Its first hike this cycle came only when the economy had already over-heated (Chart I-10). At long last, the Fed, despite its dual objective, is laser-focused on inflation. As with most central banks, signaling is presumably more important than action – remember the famous Mario Draghi’s “whatever it takes.” Talking up 50 bp rate rises, the Fed is signaling that “the inflation cop is back in town.” And while it will be hard for the Fed to put the inflation genie back in the bottle, it is reassuring that it will at least try. As for a potential 50-basis-point rate rise, for now it does not present an immediate threat to the real economy: Real rates remain negative and monetary conditions are fairly loose, while the neutral rate (that elusive r-star) is still quite a ways off from where the rates are now (Chart I-11). Bottom Line: The rate hike increments are less important than the message the Fed is sending out to the market. Chart I-10The Fed Is Behind The Curve

Sector Chart Pack Commentary

Sector Chart Pack Commentary

Chart I-11The Market Expects The Fed To Move Aggressively To Combat Inflation

The Market Expects The Fed To Move Aggressively To Combat Inflation

The Market Expects The Fed To Move Aggressively To Combat Inflation

What will be the effect of monetary tightening on economic growth? Related Report US Equity StrategyHave US Equities Hit Rock Bottom? While early on, rate hikes can be shrugged off by a strong economy, over time, tighter financial conditions necessary to combat inflation, augur badly for growth. While financial conditions are still loose, they have already tightened on the back of higher long-term rates, widening credit spreads, and a strengthening dollar. The Goldman Sachs Financial Conditions Index points to the ISM Manufacturing Index falling below 50 later this year (Chart I-12). However, as we have pointed out in our “Have We Hit Rock Bottom Yet?” report, GDP growth forecasts do not reflect tighter monetary conditions and higher commodity prices (Chart I-13). The Atlanta Fed Nowcast points to only 0.9% annualized growth in Q1, yet consensus expectations have barely budged. Bottom Line: Aggressive monetary tightening will lead to slower economic growth. Chart I-12Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

Chart I-13The GDP Forecasts Have Not Been Revised Down To Reflect New Challenges

The GDP Forecasts Have Not Been Revised Down To Reflect New Challenges

The GDP Forecasts Have Not Been Revised Down To Reflect New Challenges

Investors are increasingly worried that the US is heading for a recession. What are your views? As my colleague, US Investment Strategist Doug Peta has put it: “Fed Chair Powell is attempting to steer the US economy between the Scylla of a recession and the Charybdis of entrenched high inflation.” Indeed, the Fed has a narrow margin of error for achieving a “soft landing.” The war in Ukraine makes the Fed’s objective even more challenging. Alan Blinder, a former Fed economist and current Princeton University professor who has a forthcoming book on monetary and fiscal policy history over the past 60 years, says the Fed has just once in the last 11 tightening periods nailed a “perfect soft landing” – in the early 1990s. But twice more, in the mid-1960s and early 1980s, the central bank raised interest rates without sparking an official recession—and such “soft-ish” landings, he said in a recent presentation, are not all that rare.1 This is a track record we find disturbing. However, we share Powell’s view that “the probability of a recession within the next year is not particularly elevated… all signs are that this is a strong economy and, indeed, one that will be able to flourish… in the face of less accommodative monetary policy.” We concur. A recession is unlikely in the next 12 months or so. The US economy is in the midst of a classic slowdown stage of the business cycle: Growth is still strong albeit slowing, inflation is elevated, liquidity is (still) abundant, capacity utilization is high, and the unemployment rate is low (Table 1). The American consumer is unhappy but has not tightened purse strings much yet. Importantly, growth is slowing off high levels so this stage can take a long time (Chart I-14). Table I-1Stages Of The Business Cycle

Sector Chart Pack Commentary

Sector Chart Pack Commentary

Doug Peta’s simple recession indicator, built from components that have reliably provided an advance warning, reinforces this conclusion. The 3-month/10-year segment of the yield curve is not yet close to inverting (Chart I-15). Chart I-14The Business Cycle Indicator Signals Slowdown

The Business Cycle Indicator Signals Slowdown

The Business Cycle Indicator Signals Slowdown

Chart I-1510-Year Treasury Yield Less 3-Months Treasury Bills Segment Is Not Inverted

10-Year Treasury Yield Less 3-Months Treasury Bills Segment Is Not Inverted

10-Year Treasury Yield Less 3-Months Treasury Bills Segment Is Not Inverted

The year-over-year change in the Conference Board’s Leading Economic Index is way above the zero line that has signaled past recessions (Chart I-16). The ISM Manufacturing PMI is well above 50. The Fed funds rate is nowhere near its equilibrium/neutral level, which we judge to be north of 3%, and it is highly unlikely to get there by the end of the year (Chart I-17). Chart I-16The LEI YoY% Is Way Above Zero

The LEI YoY% Is Way Above Zero

The LEI YoY% Is Way Above Zero

Chart I-17The Fed Funds Rate Is Far From Neutral

The Fed Funds Rate Is Far From Neutral

The Fed Funds Rate Is Far From Neutral

Excluding the pandemic, recessions over the last 50-plus years have occurred only when all three components sound the alarm; not one is flashing red now and not one is likely to do so during 2022. Bottom Line: We are watching out not for a recession, but for a growth disappointment. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com S&P 500 Chart II-1Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-2Profitability

Profitability

Profitability

Chart II-3Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-4Uses Of Cash

Uses Of Cash

Uses Of Cash

Communication Services Chart II-5Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-6Profitability

Profitability

Profitability

Chart II-7Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-8Uses Of Cash

Uses Of Cash

Uses Of Cash

Consumer Discretionary Chart II-9Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-10Profitability

Profitability

Profitability

Chart II-11Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-12Uses Of Cash

Uses Of Cash

Uses Of Cash

Consumer Staples Chart II-13Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-14Profitability

Profitability

Profitability

Chart II-15Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-16Uses Of Cash

Uses Of Cash

Uses Of Cash

Energy Chart II-17Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-18Profitability

Profitability

Profitability

Chart II-19Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-20Uses Of Cash

Uses Of Cash

Uses Of Cash

Financials Chart II-21Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-22Profitability

Profitability

Profitability

Chart II-23Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-24Uses Of Cash

Uses Of Cash

Uses Of Cash

Health Care Chart II-25Sector vs Industry Groups

Sector vs Industry Groups

Sector vs Industry Groups

Chart II-26Profitability

Profitability

Profitability

Chart II-27Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-28Uses Of Cash

Uses Of Cash

Uses Of Cash

Industrials Chart II-29Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-30Profitability

Profitability

Profitability

Chart II-31Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-32Uses Of Cash

Uses Of Cash

Uses Of Cash

Information Technology Chart II-33Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-34Profitability

Profitability

Profitability

Chart II-35Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-36Uses Of Cash

Uses Of Cash

Uses Of Cash

Materials Chart II-37Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-38Profitability

Profitability

Profitability

Chart II-39Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-40Uses Of Cash

Uses Of Cash

Uses Of Cash

Real Estate Chart II-41Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-42Profitability

Profitability

Profitability

Chart II-43Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-44Uses Of Cash

Uses Of Cash

Uses Of Cash

Utilities Chart II-45Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart II-46Profitability

Profitability

Profitability

Chart II-47Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart II-48Uses Of Cash

Uses Of Cash

Uses Of Cash

Table II-1Performance

Sector Chart Pack Commentary

Sector Chart Pack Commentary

Table II-2Valuations And Forward Earnings Growth

Sector Chart Pack Commentary

Sector Chart Pack Commentary

Footnotes 1 "Recession Risks Are Rising. Can the Fed Stick a Soft Landing?" Barron's (barrons.com) Recommended Allocation Recommended Allocation: Addendum

Sector Chart Pack Commentary

Sector Chart Pack Commentary

Executive Summary US inflation is running at its highest level in over four decades. Although we expect it will soon peak, it appears certain to remain above the Fed’s 2% target level for an extended period. The war in Ukraine and COVID’s assault on China could give rise to a new round of supply disruptions that keep inflation at very high levels even after the initial wave of bottlenecks is cleared. Long-term price stability may best position an economy to achieve its potential, but real S&P 500 earnings have grown twice as fast when CPI inflation is above its mean than they have when it is below its mean. Historically, inflation has only begun to squeeze nominal earnings growth at two-standard-deviation extremes. Meaningful equity de-rating has been a feature when inflation exceeds its mean, however, and investors will have to be alert for any signs that TINA might be losing its grip on financial markets. We do not think that low-to-no-yield Treasuries or cash yet offer an appealing alternative, but animal spirits are always subject to change. Bumping Up Against Tactical Limits

Bumping Up Against Tactical Limits

Bumping Up Against Tactical Limits

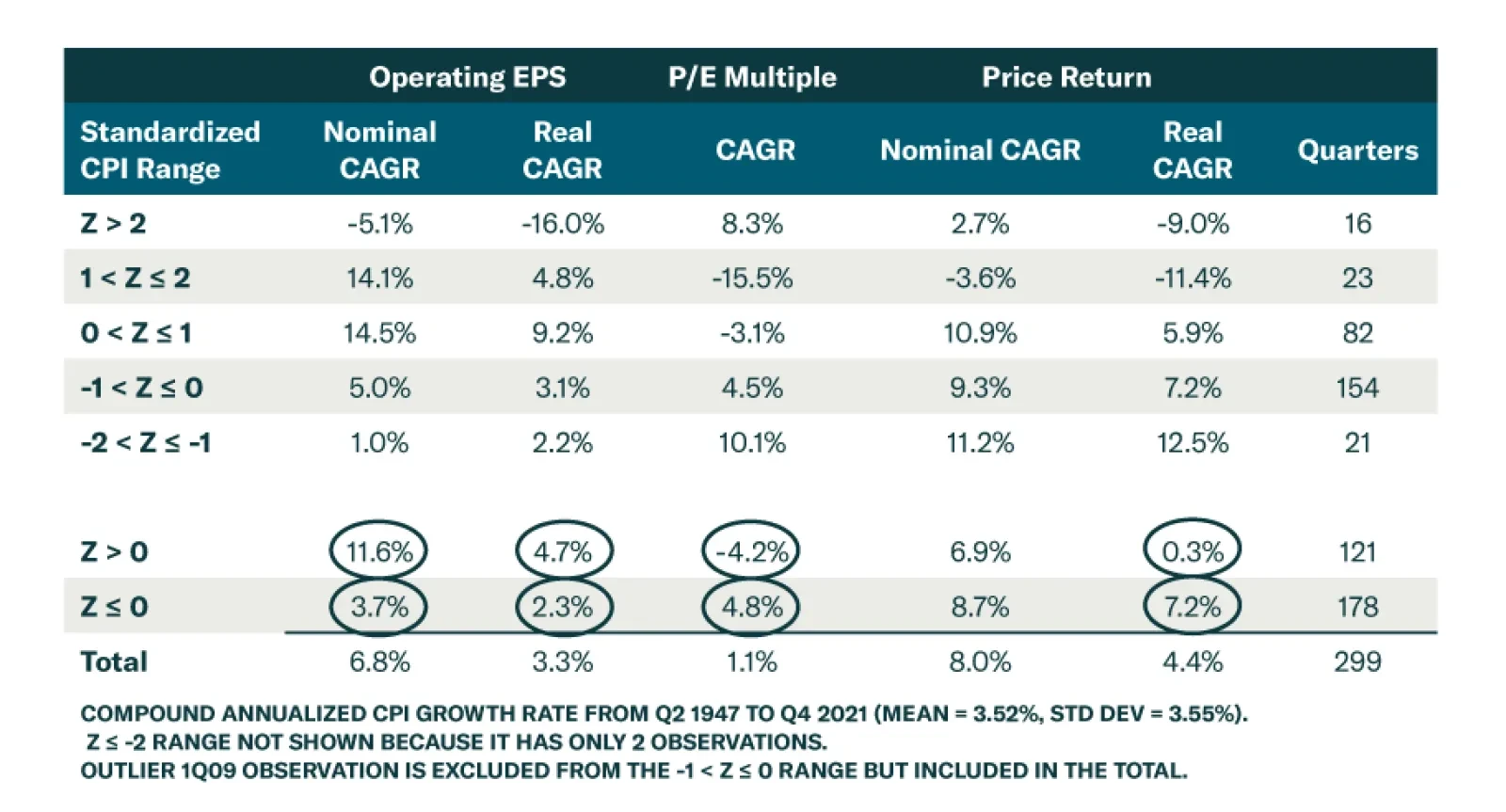

Bottom Line: The question of how to navigate an inflationary environment is likely to be with investors across 2022 and beyond. We continue to recommend overweighting equities over our cyclical 6-12-month timeframe, but risks are heightened and we will change course if conditions dictate. Feature With consumer prices rising at a clip not seen in over 40 years, inflation is a hot-button topic for anyone with even a passing interest in the US economy. The relentless series of upside inflation surprises have investors preoccupied with finding havens. To help get a handle on where to invest against varying inflation backdrops, we divided inflation into five regimes since the consumer price index (CPI) was launched in 1947: extreme inflation (an annualized quarter-over-quarter rate more than two standard deviations above its mean), high inflation (more than one but less than or equal to two standard deviations above the mean), moderate inflation (up to one standard deviation above the mean), moderately low inflation (one standard deviation below the mean up to the mean) and deflation (two standard deviations below the mean up to one standard deviation below the mean). Related Report US Investment StrategyThe Last Line Of Inflation Defense (Is Holding Fast) We reviewed the performance of S&P 500 operating earnings, earnings multiples and returns in each CPI regime to see how equities have responded to inflation over the last 75 years. We then reviewed the available total return data for Treasuries, investment-grade corporate bonds and high-yield corporate bonds and analyzed them alongside equity total returns. The empirical record enhances our confidence in earnings growth, but the S&P 500 currently trades at nearly 20 times forward four-quarter earnings, and it is especially vulnerable to de-rating, given that contracting valuations have been the driver of underperformance when inflation exceeds its mean. We find it hard to contemplate overweighting fixed income over the next year when nominal yields are so far below the rate of inflation. It may require a modest leap of faith to believe that equity multiples can maintain their cruising altitude, but the odds are very long that a 10-year Treasury note yielding 2.4% will protect its owner’s purchasing power when prices might rise by 3.5% to 4.5% over the next year. The positive real returns that Treasuries have delivered in high-inflation environments since 1984 were achieved over a lengthy stretch in which inflation compensation at the date of purchase repeatedly topped actual inflation to maturity. Today it appears as if ex-ante inflation compensation is likely to prove woefully inadequate and we are skeptical that bonds can live up to their historical return patterns. 75 Years Of Inflation Data Chart 1 shows 299 quarters of annualized inflation data in standard deviation increments since the CPI was constructed in 1947. The shape of the distribution bears out the notion that prices are sticky to the downside; the population mean is well above the median as the high-inflation right tail is longer and fatter than the deflationary left tail. Across the CPI’s entire history, inflation has averaged 3.52% on an annualized quarter-over-quarter basis with a standard deviation (“sigma”) of 3.55%. Based on those parameters, we define extremely high inflation as CPI increases above 10.62% (17 instances), high inflation as 7.08% to 10.62% (22 instances), moderately high inflation as 3.53% to 7.07% (82 instances), moderately low inflation as -0.02% to 3.52% (155 instances), disinflation as -3.57% to -0.03% (21 instances) and deflation as less than -3.57% (2 instances). Chart 1The Complete Annualized CPI Distribution

Inflation And Investing

Inflation And Investing

Inflation And Equities We examined movements in operating earnings, trailing multiples and closing prices for the S&P 500 in each of the six inflation regimes, though we discarded the outlier deflation bucket for insufficient data. In the extreme (greater-than-two-sigma) inflation scenario, S&P 500 earnings initially surged amidst the early postwar period’s pent-up demand explosion before going backwards in the Korean War inflation, the sharp 1973-75 recession and the Volcker double dip (Chart 2, dark solid line). An expanding P/E multiple (dashed line) helped to mitigate the blow from shrinking earnings, but equity investors endured sharp real declines (bottom panel, light solid line). Chart 2Extreme Inflation Squashes Earnings

Extreme Inflation Squashes Earnings

Extreme Inflation Squashes Earnings

The one-to-two-sigma high-inflation scenario is a mirror image of the extreme inflation scenario. Nominal earnings growth surged (Chart 3, top panel) and managed to hold up well in real terms (Chart 3, bottom panel), but the index’s multiple de-rated at a vicious 15.5% annualized rate, sticking investors with double-digit real losses. 70% of this regime played out from 1973 to 1982 and it also spanned some of 1990-91 and great recessions. The last two data points occurred in 2021, when flat multiples allowed equities to benefit from robust earnings growth, but previously melting multiples illustrate the peril for equities if monetary tightening induces a hard landing. Chart 3High Inflation: Surging Nominal Earnings, Fierce De-Rating