United States

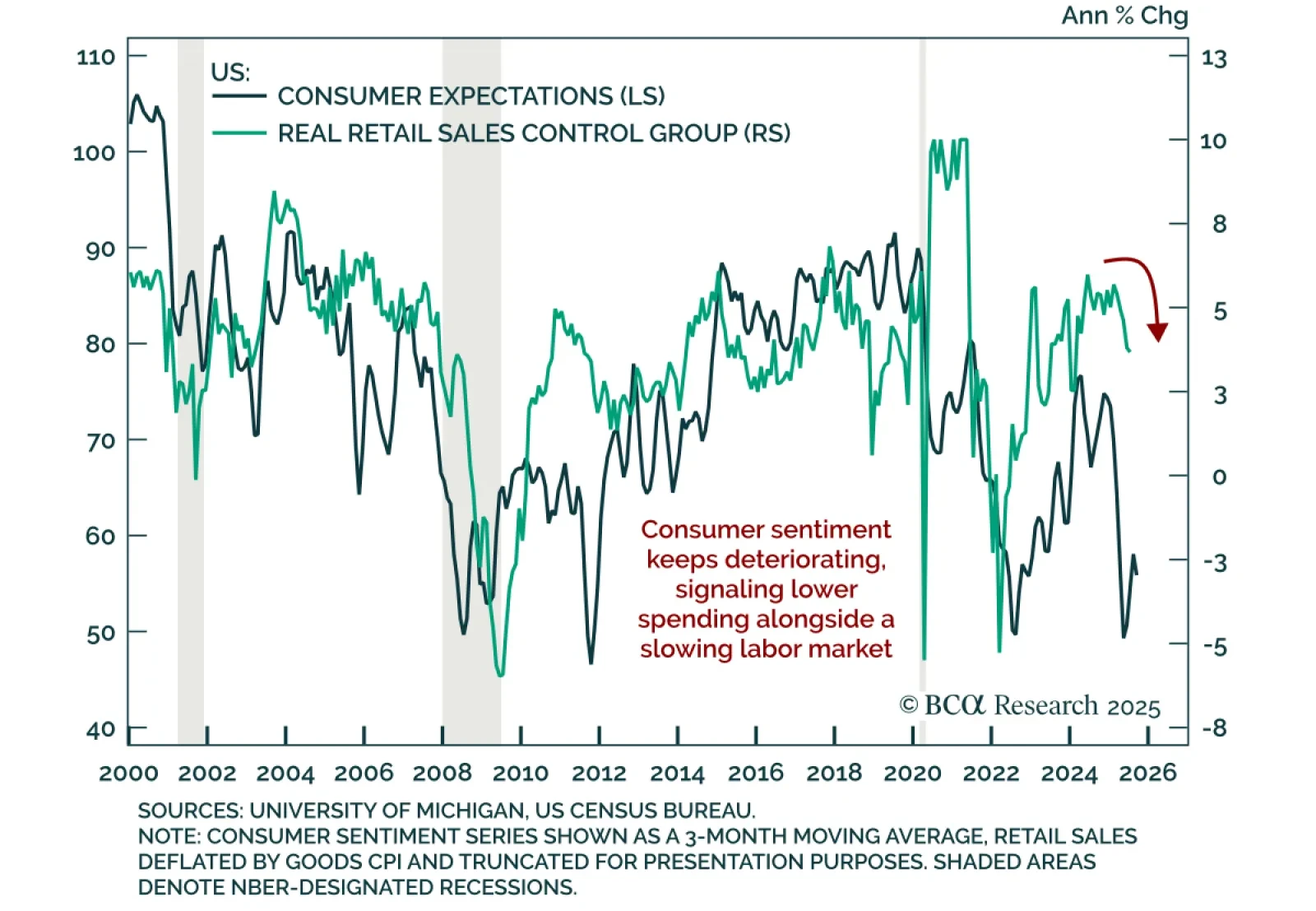

US consumer sentiment deteriorated in September, reinforcing signs of slowing consumption and supporting a defensive stance. The preliminary University of Michigan Consumer Sentiment Index dropped more than expected to 55.4 from 58.2, with declines in both…

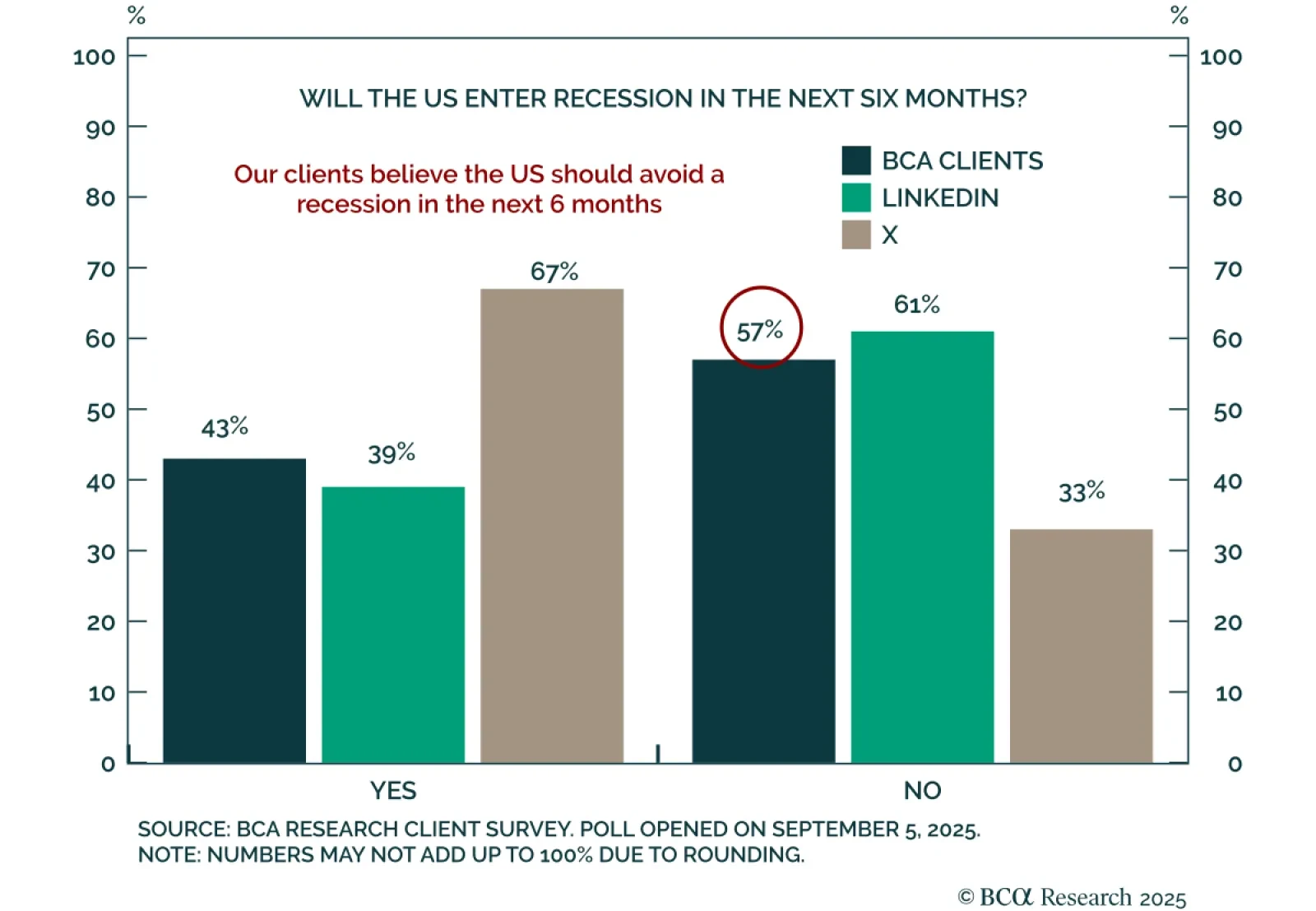

BCA clients are divided on whether the US economy is heading into a recession, but lean towards the view that it will be avoided. In the latest weekly poll on the Have Your Say section of BCA's website, 43% of respondents answered that the US will enter…

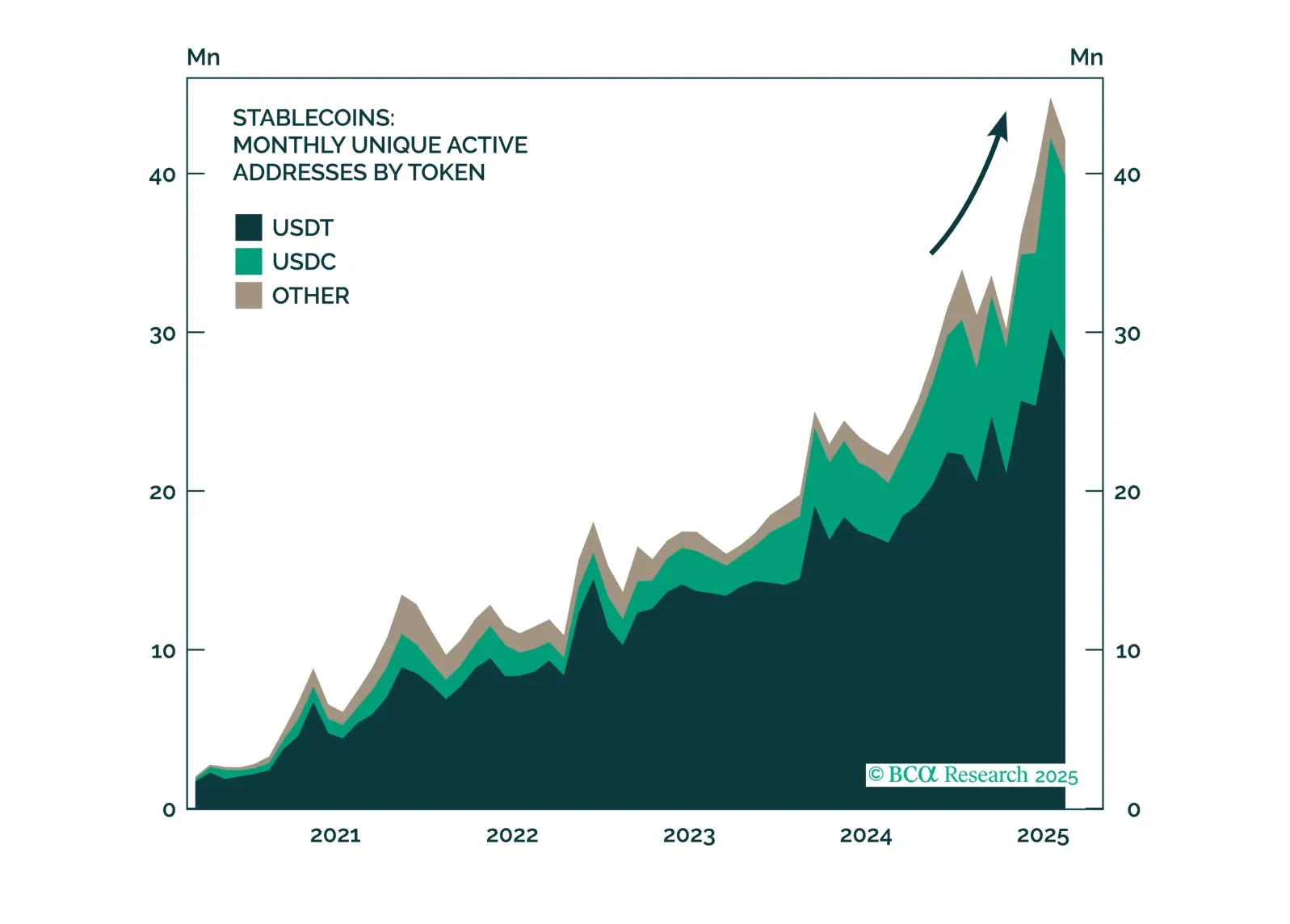

From Treasurys to tokenization, stablecoins are quietly becoming one of the most disruptive forces in global finance, with the power to compress yields, deepen dollar penetration, and shift the balance within crypto markets. Explore BCA’s latest insights on their growing impact.

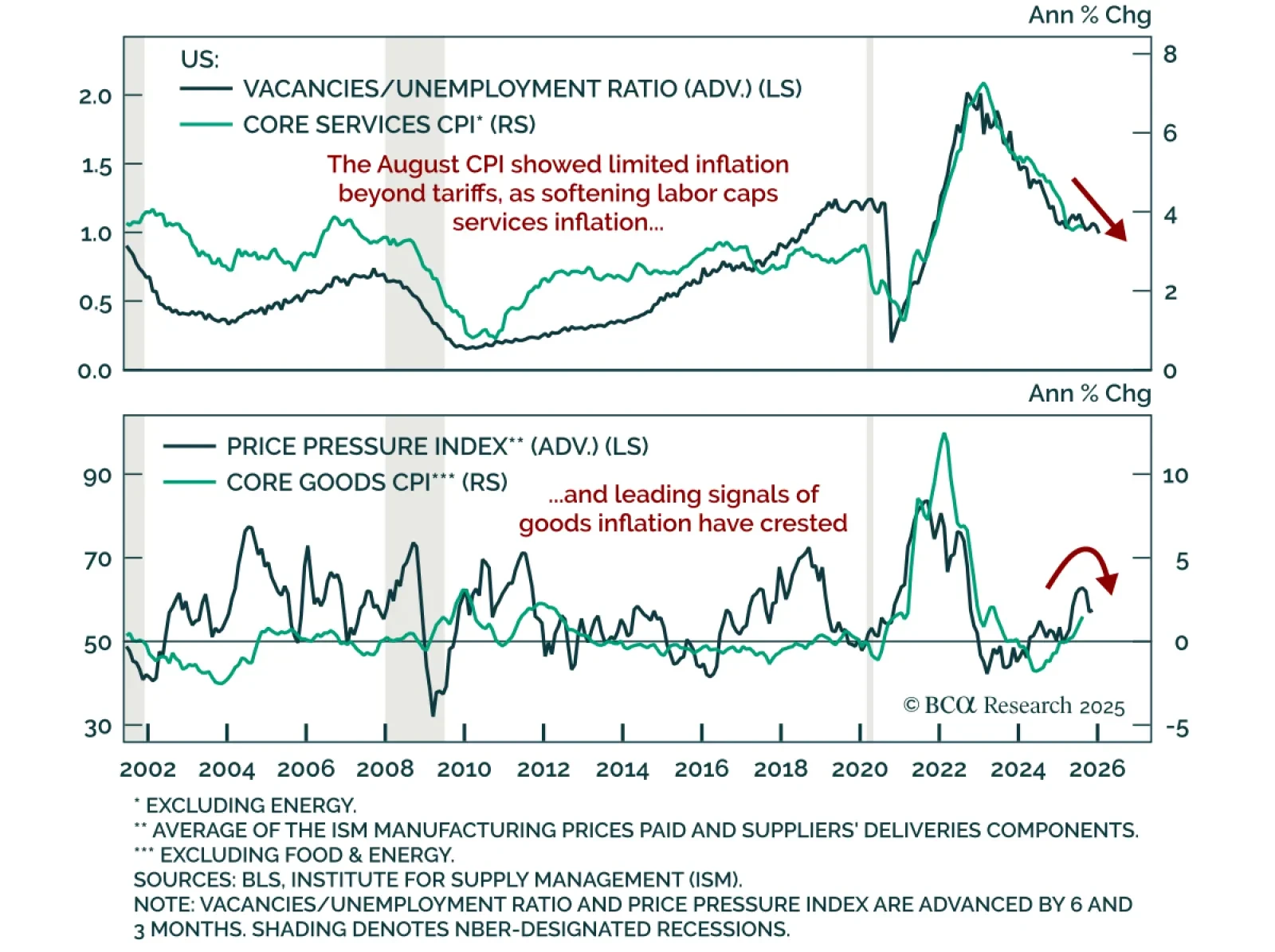

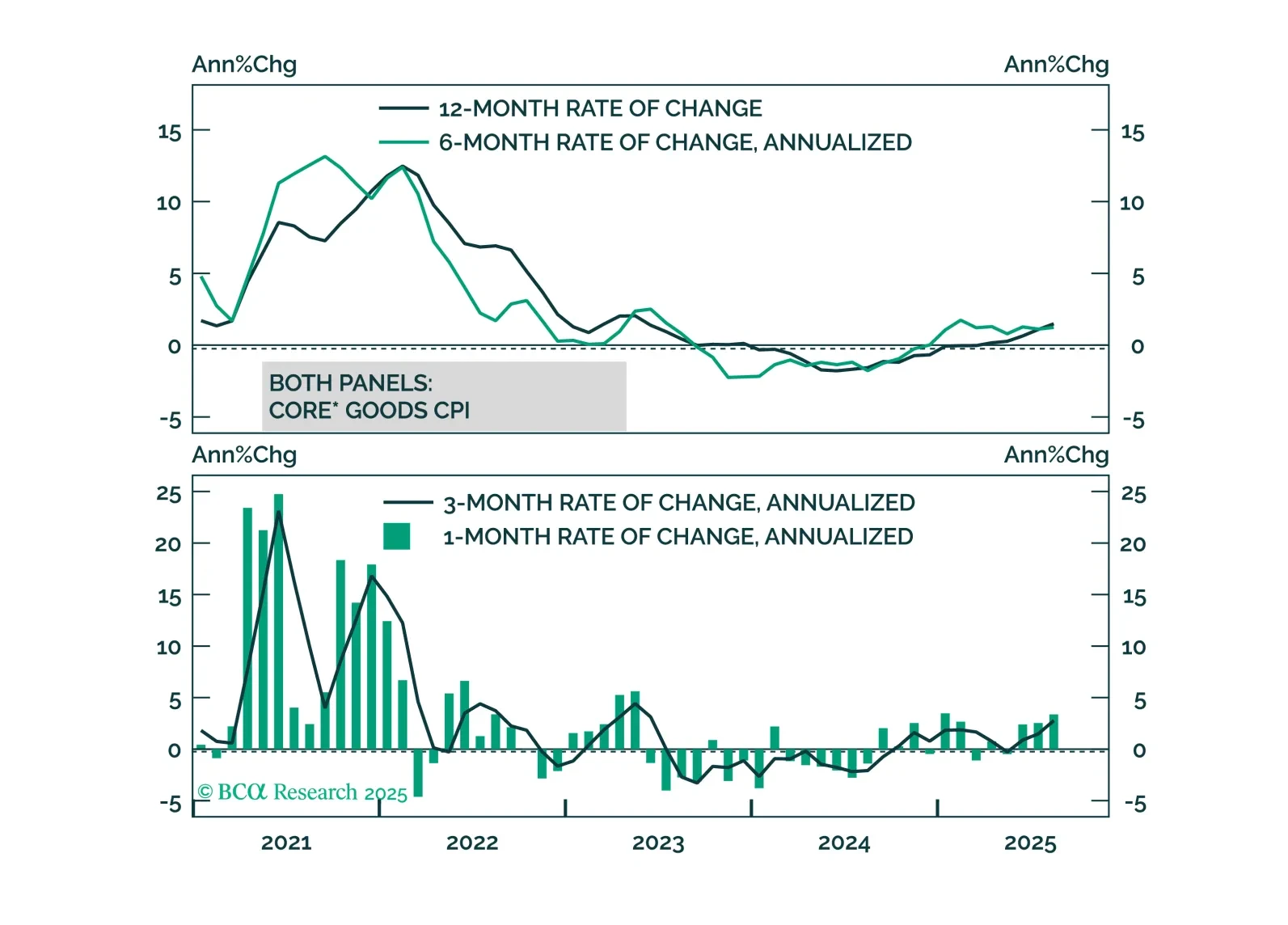

August US CPI was in line with expectations, reinforcing the case for Fed easing and a long-duration stance. Headline CPI rose 0.4% m/m (2.9% y/y), while core held at 0.3% m/m (3.1% y/y). Core goods inflation ticked up to 1.5% y/y from 1.1%, while services…

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

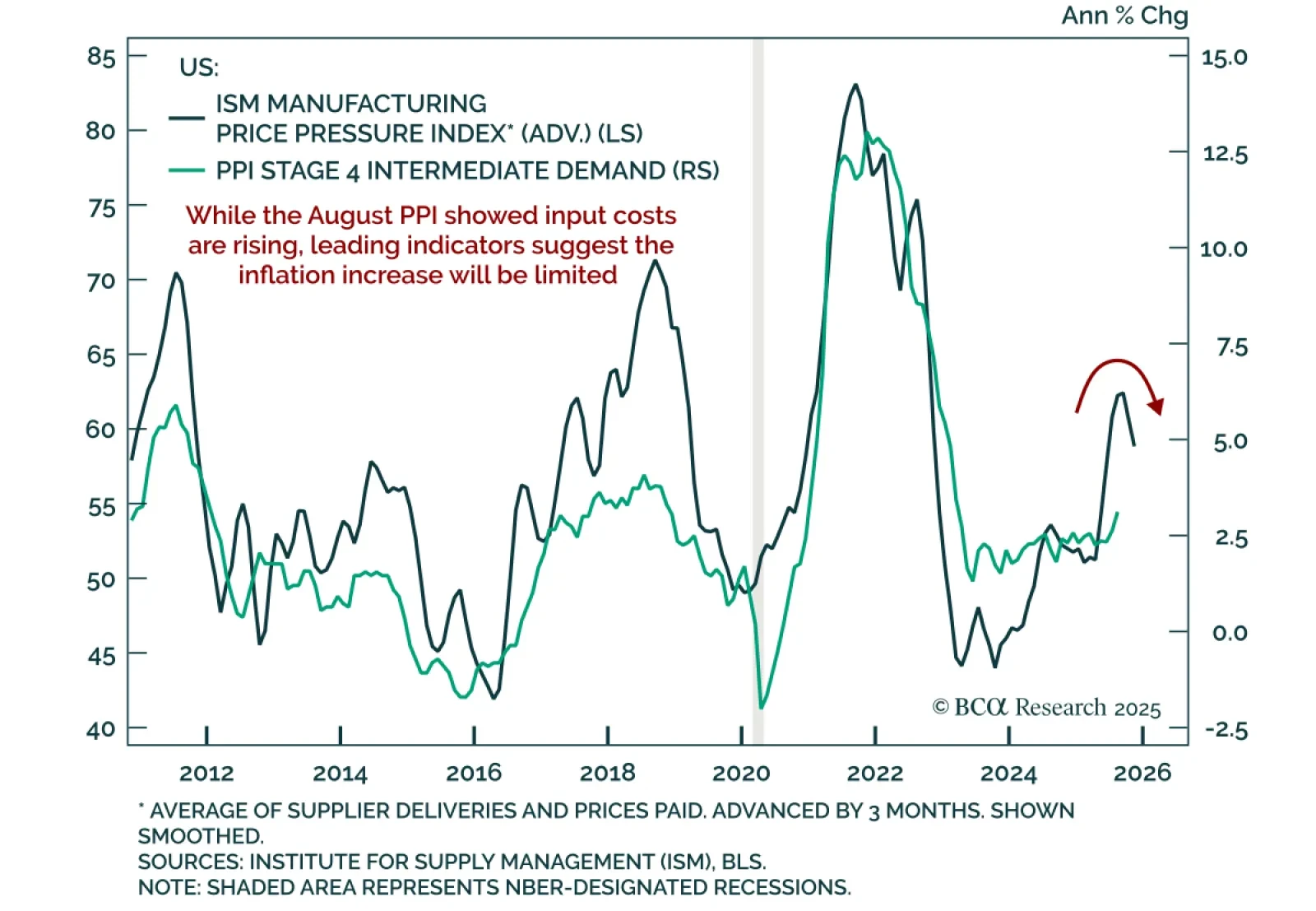

August PPI inflation cooled, reinforcing the case for Fed easing and long duration with steepeners. Headline PPI fell 0.1% m/m, bringing the annual rate down to 2.6% after July’s 0.7% gain. Core PPI (ex-food, energy, and trade) rose 0.3% m/m (2.8% y/y).…

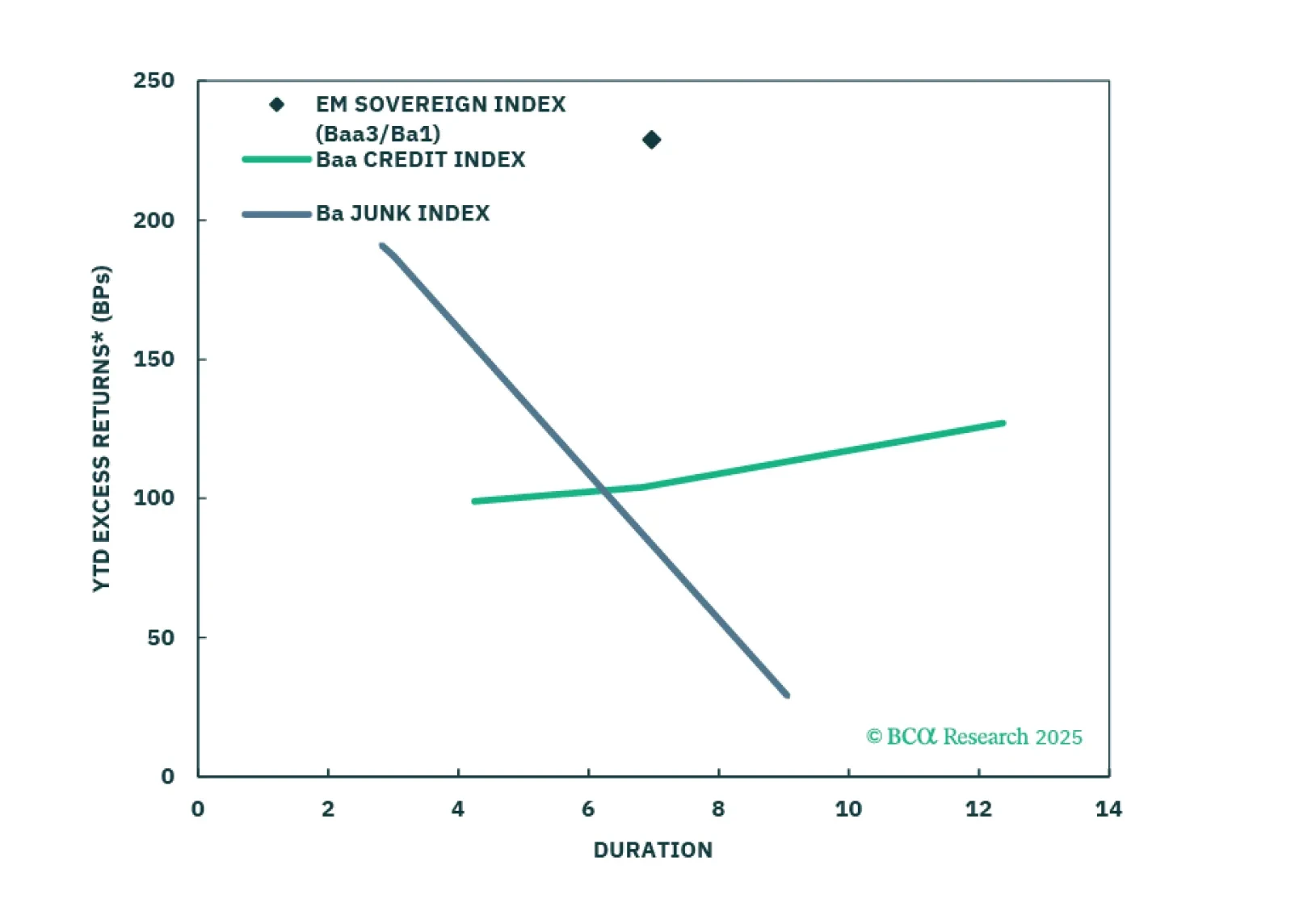

USD-denominated Emerging Market bonds have been outperforming US corporates for the past year. We don’t think the rally is exhausted yet.

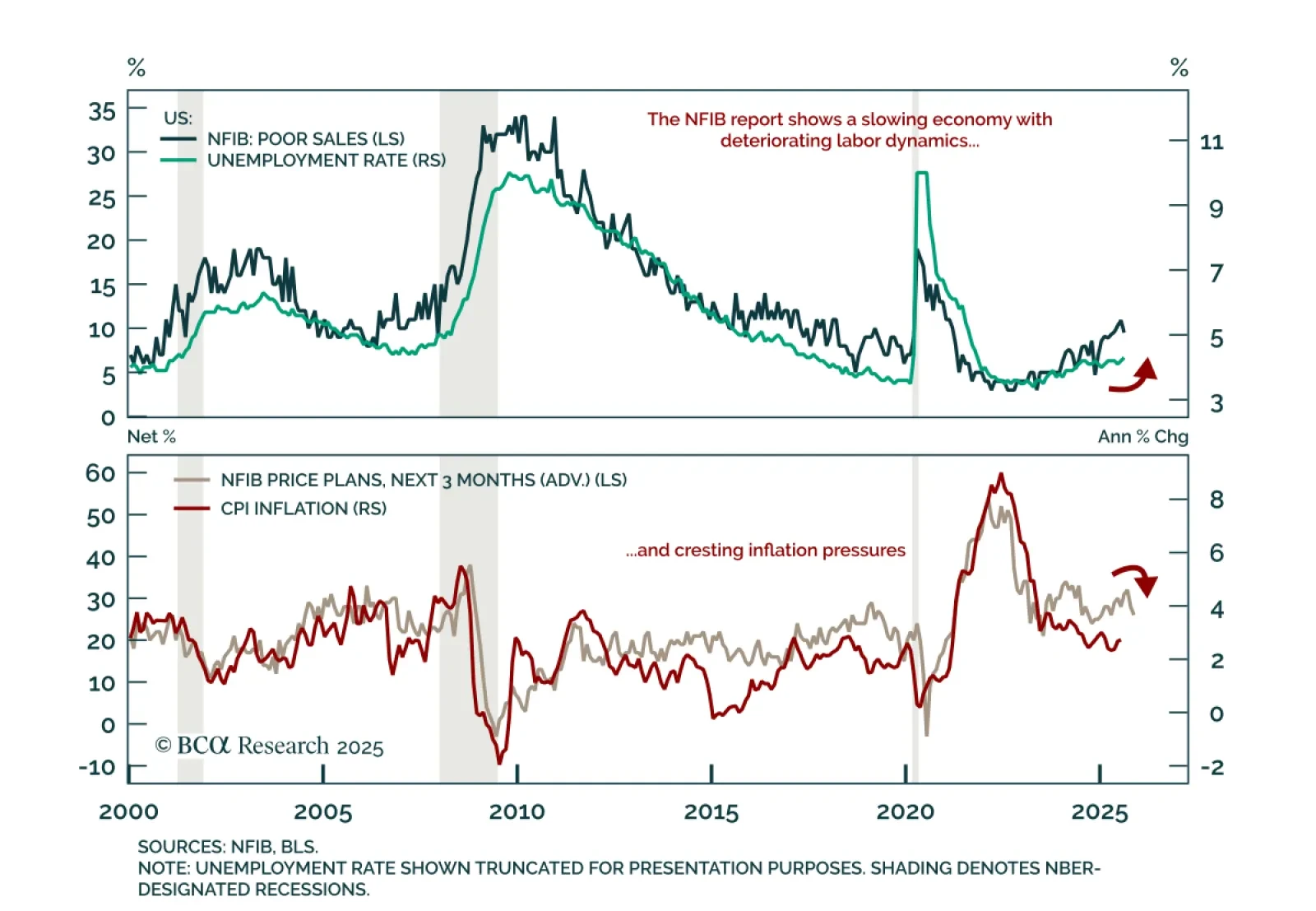

The August NFIB survey shows a fragile US economy with disinflationary signals and weak employment, supporting our defensive stance. The Small Business Optimism Index rose to 100.8 from 100.3, a six-month high, though still below December 2024 levels. Much of…

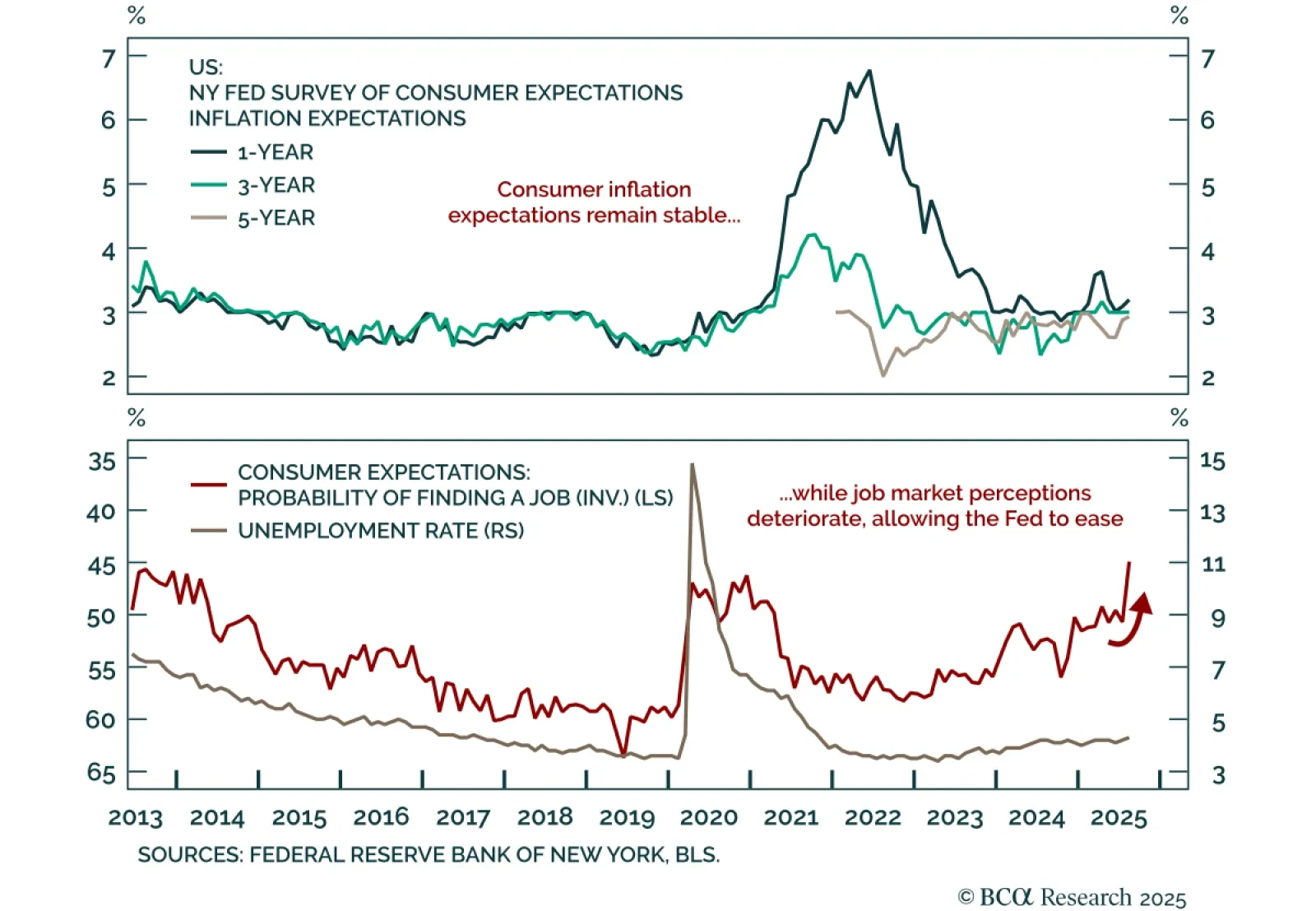

Stable long-term inflation expectations and weak labor perceptions support a defensive stance. The NY Fed Survey of Consumer Expectations showed 1-year inflation expectations ticking up to 3.2% in August, while the 3-year (3.0%) and 5-year (2.9%)…

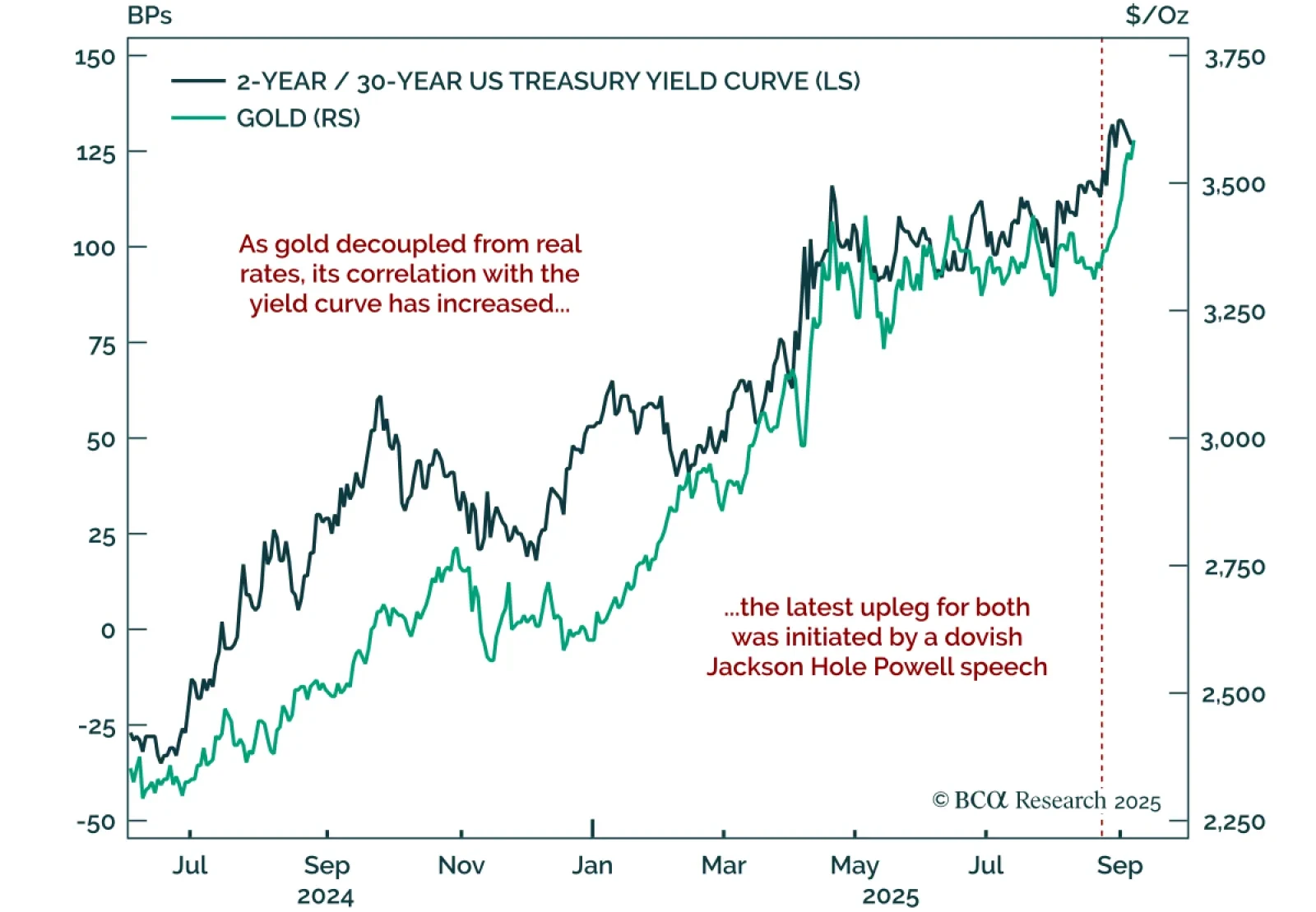

Gold and steepeners remain core trades, supported by structural shifts in markets and policy. Gold broke out of the consolidation range it had been in since April, supported by central-bank buying and heightened policy uncertainty. Moreover, the…