United States

The economy is slowing, but not collapsing, and monetary easing is imminent — a backdrop that will benefit equities. We remain strategically bullish, with a close eye on GenAI and resilient earnings, even amid numerous risks. However, we are tactically cautious, as seasonality, elevated valuations, and stretched technicals present near-term headwinds.

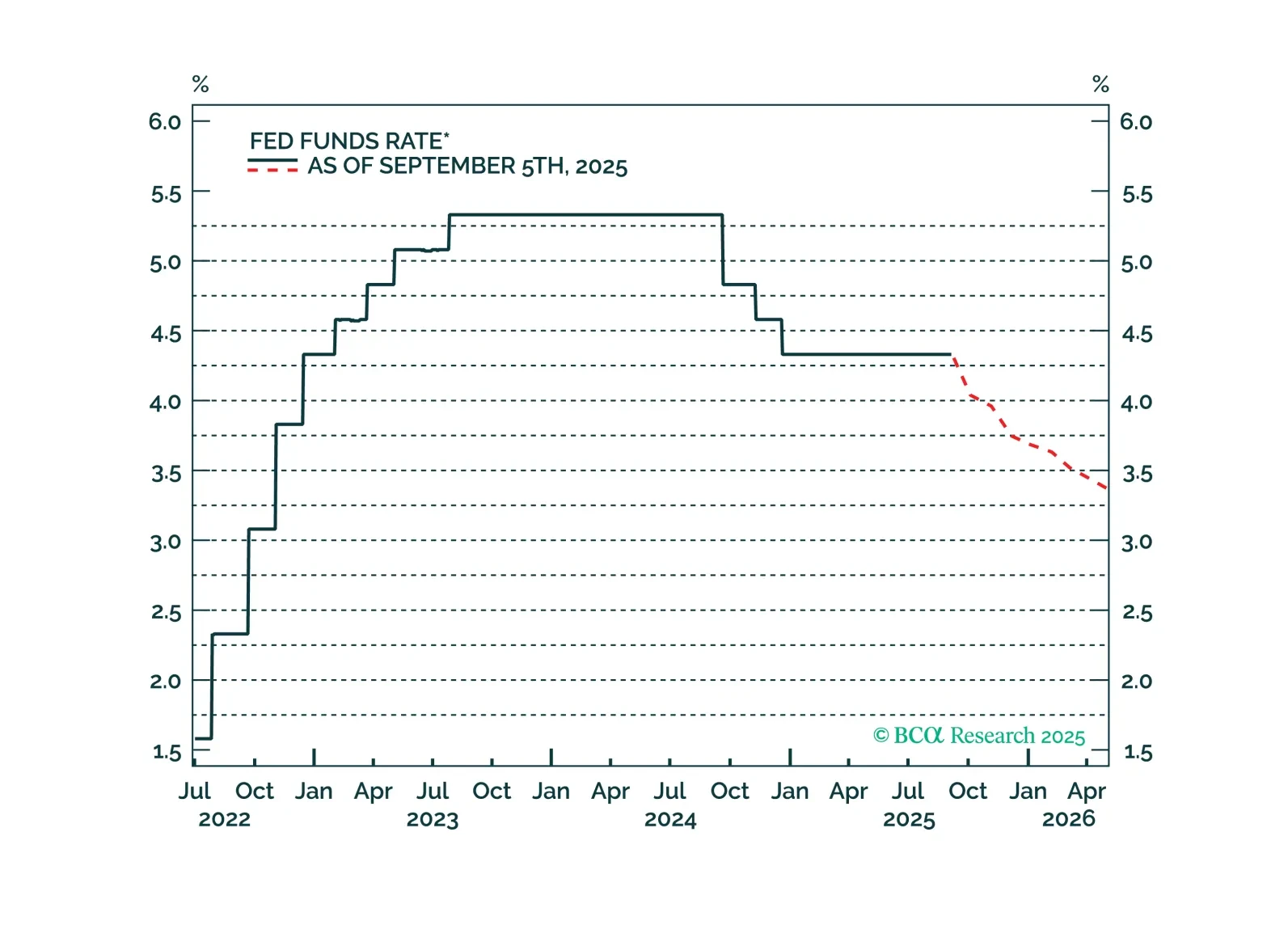

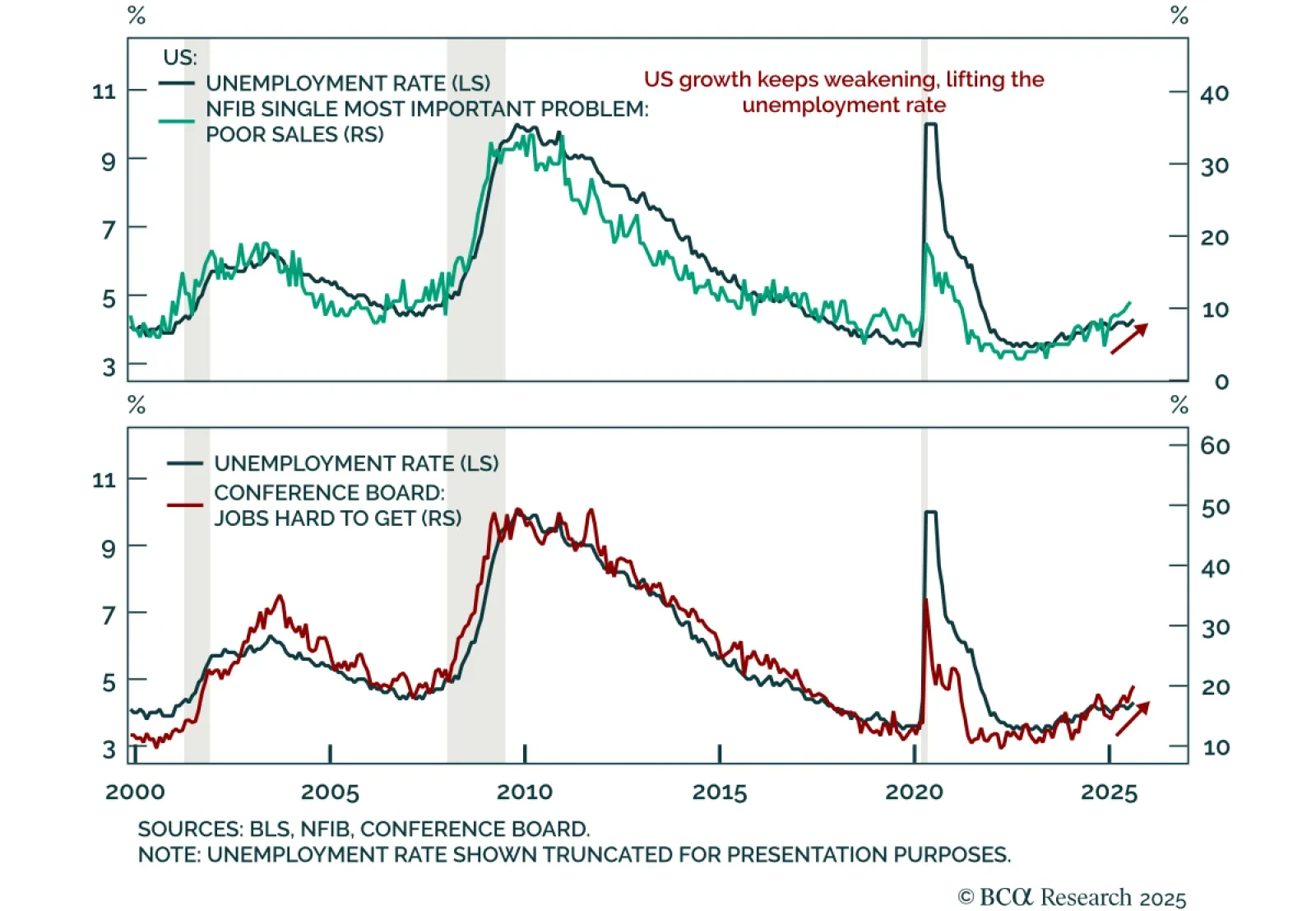

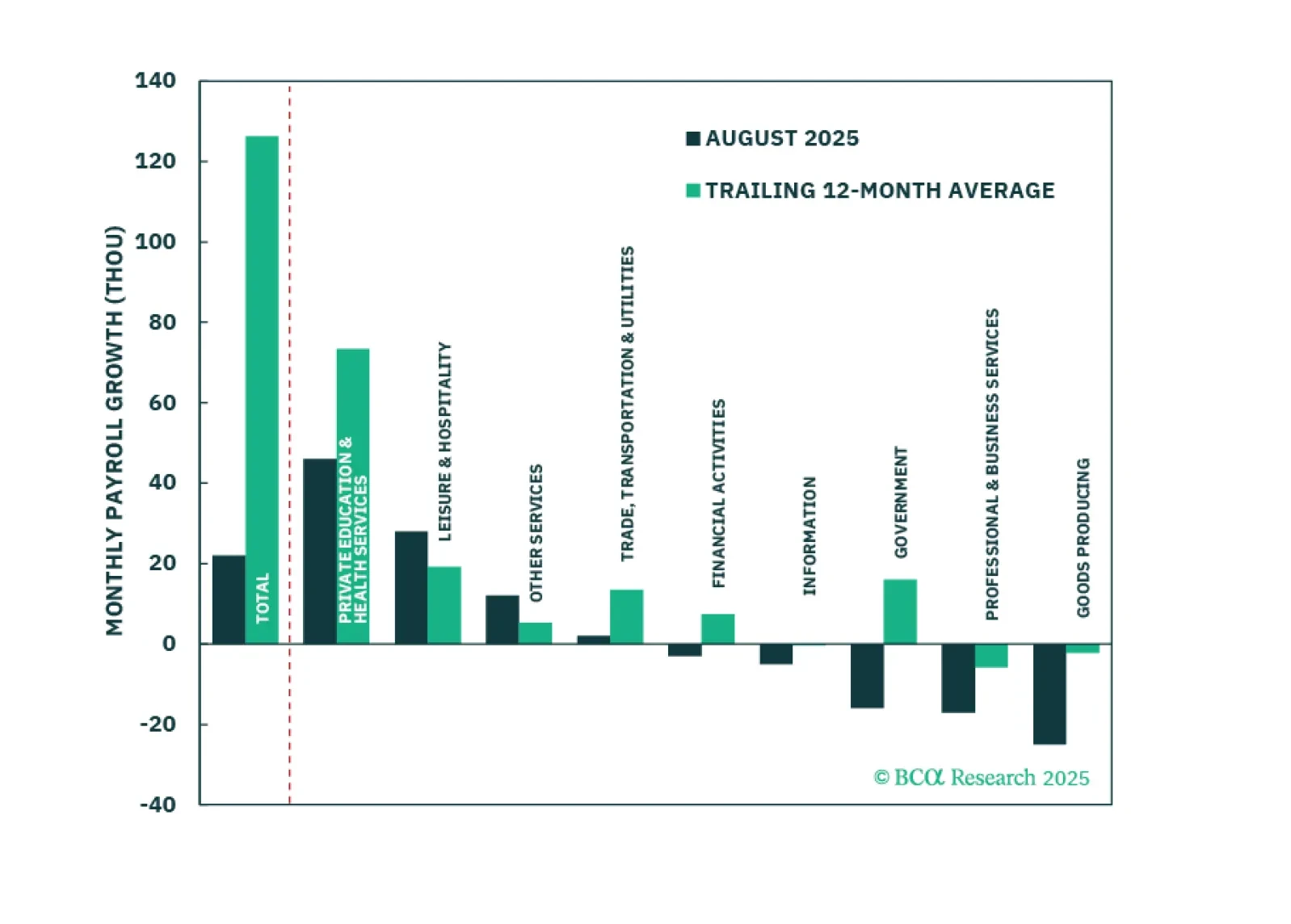

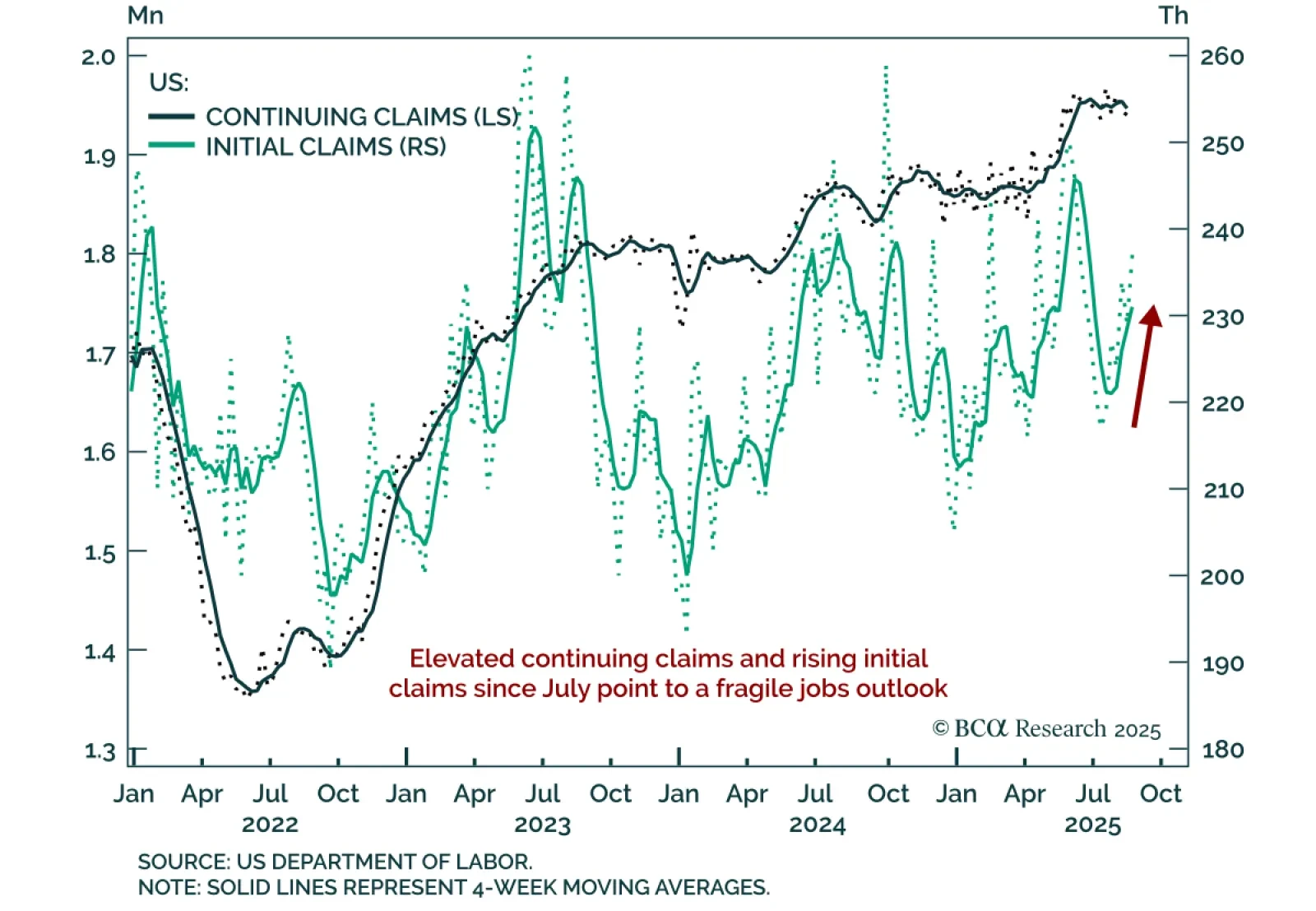

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

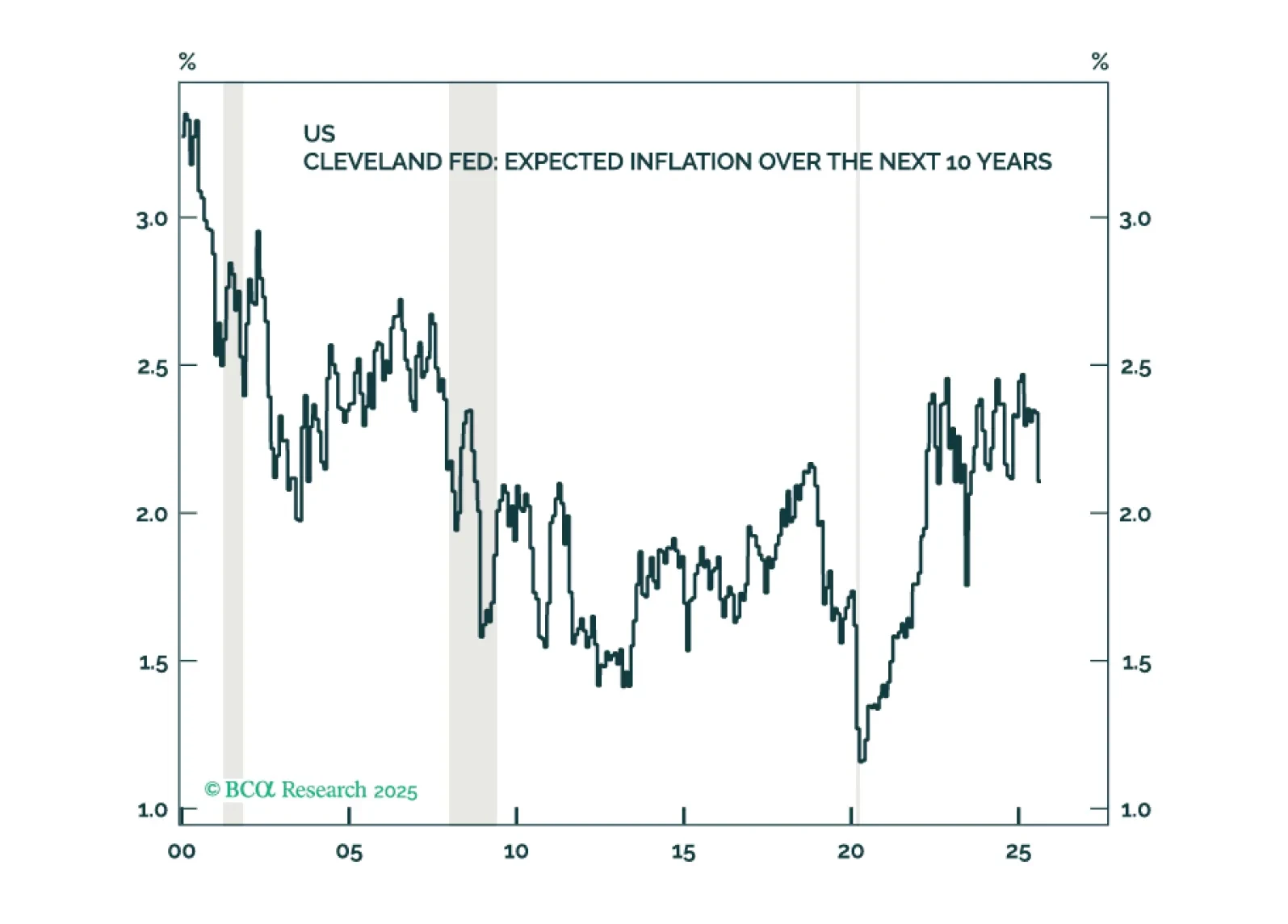

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

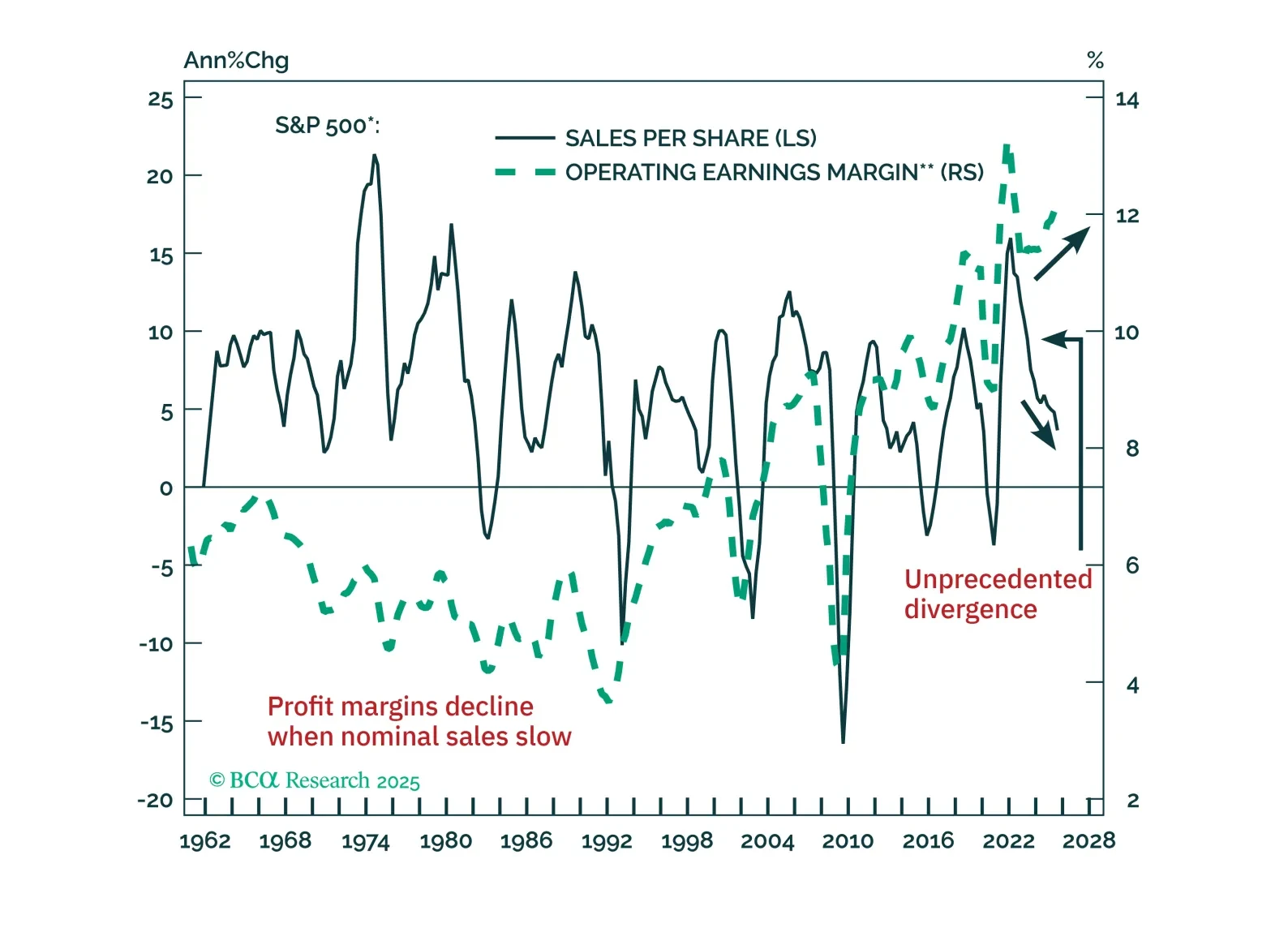

The resilience of US non-tech companies' profitability has not been driven by top-line growth but by falling costs, which safeguarded profit margins. Presently, risks in US stocks outweigh the potential rewards – margin sustainability is uncertain while equity valuations are very stretched.

Our Portfolio Allocation Summary for September 2025.