United States

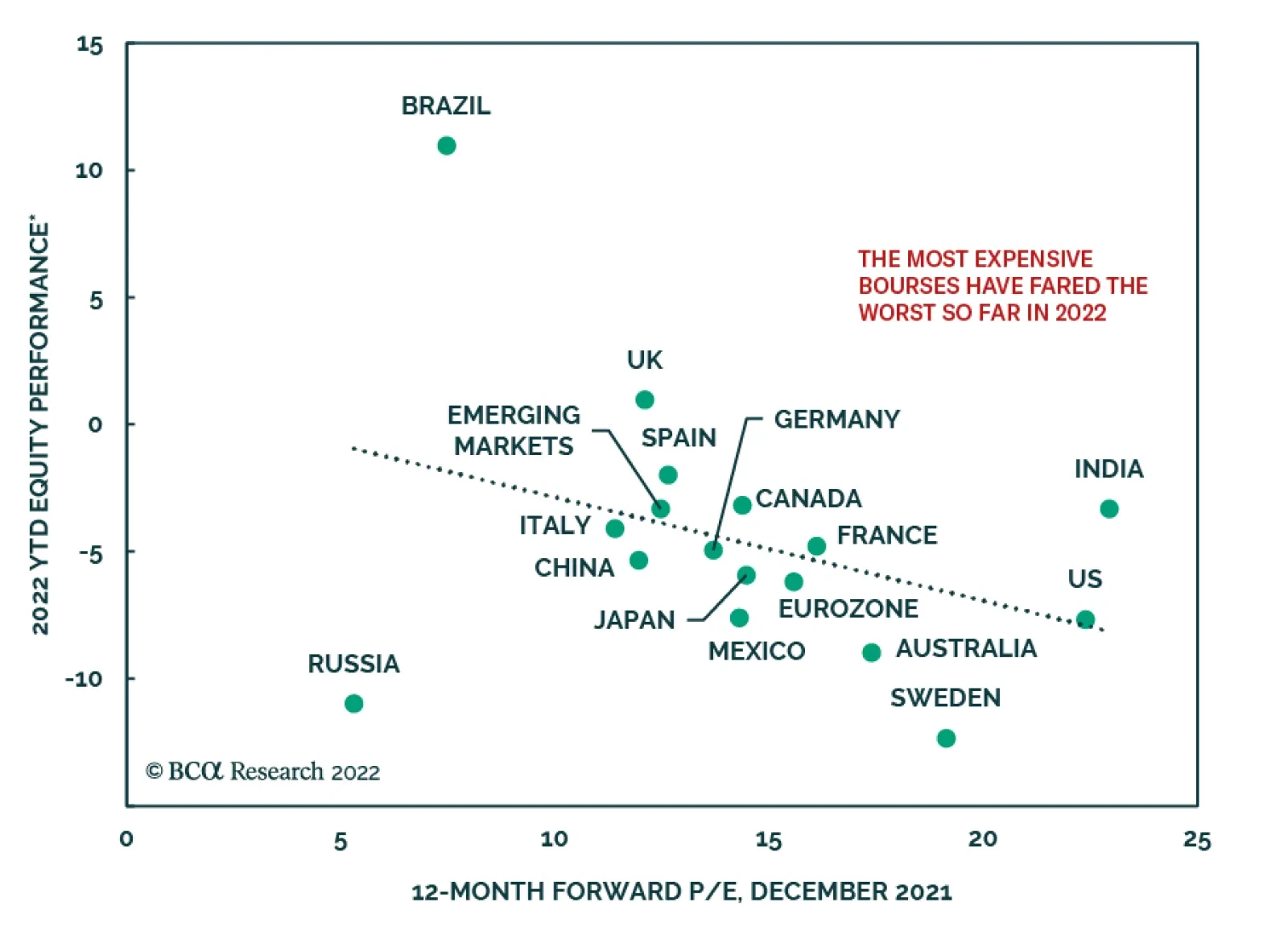

The climb up in government bond yields following the Fed’s late-2021 hawkish pivot is the trigger for the selloff in equity markets globally this month. However, the hit to equities has not been uniform across all global markets. In an insight last week, we…

Global equity markets whose valuations were most expensive going into this year have been hit hardest by the recent equity tumult (see Market Focus). Such has been the fate of US stocks: by the end of last week, the S&P 500 was down 7% so far this year,…

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Executive Summary The Software and Services Industry is undergoing a fundamental transformation in its business model catalyzed by a momentous migration of software applications to the cloud and broad-based digitization of the economy. This shift is accompanied by displacement of the traditional on-prem license and support model with a more lucrative cloud-based subscription model. While on-prem software sales are contracting, cloud revenue is growing in double digits. As a result, the industry enjoys spectacular margins and earnings growth. Its earnings have also proven to be resilient across the business cycle because software and IT services increase companies’ productivity in good times and bad. Rising rates are a headwind, but a temporary one. Margins Will Continue To Expand

Margins Are To Continue Expanding

Margins Are To Continue Expanding

Bottom Line: The Software and Services industry group is an all-weather industry with resilient earnings and strong growth throughout the business cycle. It is also in the epicenter of technological innovation: Migration to the cloud and digital transformation enhance the industry’s growth and profitability. We continue recommending both a tactical and a structural overweight. Feature Performance Technology stocks found themselves in the eye of this month’s market rout. After falling 19% from its peak, the NASDAQ is now firmly in correction territory. The Technology sector is down 11%, while the Software and Services industry group is down 10% (Chart 1). In the “Are We There Yet?” report published last week, we posited that it is not yet the right time to bottom fish: While the Technology sector appears oversold, macroeconomic headwinds from the imminent monetary tightening and a slowdown in demand for technology goods and services may prolong the pain. The interplay of valuations and fundamentals for the sector is not yet favorable. While we are underweight the Technology sector, thanks to our underweight positions in Semiconductors and Hardware and Equipment, we remain overweight Software and Services (S&S). In this report, we will conduct a “deep dive” into S&S and reevaluate our positioning (Table 1). Although S&S is down more than 10% from the peak, it has outperformed the S&P 500 by 88% since 2011 (Chart 2). The million-dollar question we will try to answer is whether this outperformance continues over the tactical and structural time horizons. Chart 1Software And Services Outperformed Other Tech Industries

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Chart 2S&S Outperformed The S&P 500 By 88% Over The Past 10 Years

S&S Outperformed The S&P 500 By 88% Over The Past 10 Years

S&S Outperformed The S&P 500 By 88% Over The Past 10 Years

Table 1Performance

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Sneak Preview: We maintain our overweight of the Software and Services sector thanks to positive market trends, the all-weather nature of the industry, and resilient earnings. Industry Group Composition The Software And Services Industry Group Is Top Heavy The S&P 500 Software and Services industry group is the largest in the Technology sector and is 48% of the sector market cap. The industry group is split between Software, which is about two-thirds of its market cap, and IT Services, which is one-third (Chart 3). Just like other technology industries, it is dominated by one of the FAANGs+M, Microsoft in this case, which makes up 42% of the industry group index weight. The top 10 constituents out of 36 comprise 80% of the industry’s weight (Table 2). During the current pullback, the S&S industry group has fallen by more than 10%, cushioned by the performance of its larger players. But this masks the pain of the smaller and less profitable constituents, which have fallen by more than 30% (Chart 4). Chart 3Software Dwarfs IT Services

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Chart 4Some Smaller Constituents Have Fallen More Than 15% YTD

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Table 2S&S Industry Is Dominated By A Handful Of Successful Companies

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

However, market dominance runs much deeper than just market capitalization: Microsoft, Adobe, Salesforce, and Oracle account for 87% of the Software Industry revenue, while Visa, Mastercard, Accenture, and PayPal generate 42% of the IT Services industry revenue. Larger industry players are also more profitable thanks to the high operating leverage the industry enjoys. Clearly, just a few companies drive sales and earnings growth, valuations, and performance. On the bright side, these are some of the most successful US technology companies, and their size is their competitive moat. We believe that the industry group is in “good hands.” Key Trends Cloud Migration Following the success of offshoring the US manufacturing base to China that allowed corporations to reduce labor costs, companies are now experimenting with outsourcing other key infrastructure elements. This time, however, the migration is happening to digital cloud platforms. Instead of investing in pricey servers and other hardware assets, corporations have the choice of going with Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), or Infrastructure-as-a-Service (IaaS) solutions offered by the tech titans. Not only are cloud solutions more cost-effective, but they also offer the convenience and flexibility to scale corporate hardware infrastructure by simply purchasing more or less computational power. COVID-19 lockdowns and the migration of the white-collar workforce towards remote work have motivated companies to transition their technology and operations to the cloud, and have acted as a catalyst for “digital offshoring.” Digital Transformation Digital transformation is in many ways similar to cloud migration. Essentially, it represents broader software penetration into the US economy. Whether it is a manufacturing production or customer relationship management process, wider adoption of software allows for a more efficient business solution via automation and process optimization. Airbnb and Uber are the poster children of digital transformation. While some industries have already undergone digital transformation, there are notable areas which lag behind. For instance, banks’ failure to modernize their digital infrastructure to speed up transactions and to increase overall user convenience has arguably led to the development of the crypto space as an alternative to the slow-evolving traditional financial institutions. The broader implication is that there are still major sectors in the economy that are yet to ramp up automation and increase efficiencies via digital transformation, meaning that there is a healthy demand pipeline for the tech companies. Types Of Software And Services Companies Software: Migration To The Cloud Is A Key Driver Of Growth In the past, classifying software companies was a relatively straightforward exercise: They were divided into system software vs. application software. System software included such categories as operating systems for PCs, and other hardware and database software. Application software covered Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Communications and Collaborations, etc. However, over time, the industry landscape has changed, first by the mergers that blurred the distinction across these lines, and lately, thanks to ubiquitous migration to the cloud model and digitization of the economy. Therefore, it is most practical to classify software companies by their type of business model, i.e., legacy license and support model, or cloud-based, or hybrid. Pure cloud-first: These companies derive 100% of their sales from the cloud model – Salesforce.com (CRM), ServiceNow (Now), and Twilio (TWLO) are among the biggest winners. Cloud/license hybrid: These are companies that derive 50%+ of their sales from the cloud, such as Microsoft (MSFT), Atlassian (TEAM), Autodesk (ADSK), and Adobe (ADBE). Legacy license and support model (aka On-Premises): Constellation Software (CSU), Citrix Systems (CTSX) – these companies are likely to struggle to grow organically. Types Of Cloud Application Services The cloud-based business model in turn can be classified under three different types of service: Software-as-a-Service (SaaS), Infrastructure-as-a-Service (IaaS), or Platform-as-a-Service (PaaS). Software-as-a-Service: Customers configure and access a web-based application operated by a SaaS provider over the internet. Salesforce.com, Workday (DAY), ServiceNow, and Oracle are some of the most established players. Infrastructure-as-a-Service: This service gives customers access to virtual storage and servers over the internet, enabling them to develop and run any application just as if it were running in their own data center. Amazon’s AWS, Microsoft’s Azure, and IBM are the key competitors in this space. Platform-as-a-Service: This service occupies a middle ground between SaaS and IaaS, i.e. between a full-fledged app that can be used “out-of-the-box” and a “raw server and storage” instance, making the customer responsible for installing and configuring its own “full stack.” PaaS offerings tend to be less standardized. Salesforce.com, Microsoft, and Oracle are the leaders. IDC projects the continued strength of this segment and expects it to grow at an annualized rate of 29.7% over the next five years. The following table from Microsoft presents a perfect explanation of the different software service models (Table 3). Table 3Differences In Cloud Computing Service Models

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

License And Support Vs. Cloud Subscription Model Growth Rates Broad-based migration to the cloud is shifting the industry’s revenue composition, with accelerating bifurcation between cloud and on-prem models: Cloud subscription revenue is replacing the traditional license and support model. As a result, legacy on-prem revenue has recently been contracting, and once the last of the legacy enterprise applications are retired, it will be fully replaced by cloud revenue. According to estimates by CFRA,1 the software industry grew by 4% in 2021, with a 22% year-on-year increase in cloud subscription revenue, which now constitutes 37% of total industry revenue, and a 3% decline in traditional software revenue. The surge in cloud growth is likely to continue, thanks to the accelerating pace of digital transformation. This trend is also promulgated by some of the largest players, such as Microsoft, whose cloud subscription revenue now constitutes more than half of the overall revenue and is an engine of growth in the software space. Strong cloud revenue growth is not just a function of recruiting new users but is also supported by the proliferation of new cloud apps and upgrades to the existing ones. Importantly, the cloud subscription model is also more profitable than the license model, whose EBITDA margins rarely exceed 40%. Cloud-based services take longer to become profitable but have much higher operating leverage: Once profitable, cloud and hybrid companies often have operating margins around 50-60%. Software is one of the most resilient technology industries, performing equally well in a growing economy and during downturns: Subscription pricing is sticky, and switching costs are high. As a result, companies, which derive a large share of their revenue from the cloud, have stable and predictable sales. Once clients are onboarded, cloud providers may also be able to exercise their pricing power. IT Services IT services is a smaller segment of the Software and Services industry group and is a hodge-podge of different companies that provide a wide range of services from IT consulting to FinTech. The following is a brief description of the key categories: IT Consulting: The S&P 500 IT Consulting companies are Accenture, Gartner, and Cognizant. Companies offer Professional advice in IT, management, HR, logistics, and many others. Since the pandemic, these companies’ key focus is on assisting their clients with digital transformation and improving companies’ operations. This industry is one of the key beneficiaries of accelerated migration to the cloud and has enjoyed exponential growth over the past decade. Its revenue stream is highly resilient, as even during economic downturns, clients are seeking advice on the best ways to navigate an uncertain market environment. Outsourcing: Companies such as ADP and Paychex provide HR and business services solutions for mid-sized and small companies. Their services cover payroll, benefits, retirement, and insurance services. This industry has been growing its sales and profits at a healthy clip over the past few years. Now it is focused on modernizing itself by moving its own operations to the cloud and deploying Artificial Intelligence to improve operations. These companies are also undergoing digital transformation and are moving towards the SaaS model. Financial Transaction Services: This is a FinTech industry that includes card and payment processors, such as Visa, Mastercard, and PayPal, and each of these players operates their own proprietary payment networks. Digital payments and the wide acceptance of e-commerce drive this space. Lately, these companies have been at the forefront of the adoption of digital currencies as viable payment options. Payment companies are among the earliest adopters of the cloud, and their business model is best described as Transaction-processing-as-a-service. These are highly profitable companies that consistently generate an operating margin above 60%. Key Industry Drivers Software Enhances Productivity And Improves Profitability Broadly speaking, the Software and Services industry group is considered a defensive holding owing to the resiliency of its earnings (Chart 5). Software enhances productivity: During economic downturns, it helps reduce costs, and during expansions, it helps overcome capacity constraints and labor shortages. While pandemic labor shortages and lockdowns produced a spike in productivity, more recently it has been falling, which has warranted a year-over-year increase in software investment (Chart 6). Chart 5S&S Earnings Are Resilient Across The Business Cycle

S&S Earnings Are Resilient Across The Business Cycle

S&S Earnings Are Resilient Across The Business Cycle

Chart 6Investing In Software Improves Productivity

Investing In Software Improves Productivity

Investing In Software Improves Productivity

Further, both labor shortages and rising wages are prompting companies to redesign their operations to contain costs and preserve margins. To do so, many are accelerating investments in Capex and automation, much of which is achieved through investment in software and IT services, replacing both labor and capital. According to CFRA, “software is no longer used to manage a means of production, but rather IS means of production .” Software-related Capex is not only garnering a larger slice of tech spending budgets but also of the overall Capex pie (Chart 7). Chart 7Share Of Software In Overall Capex Has Been Rising Steadily

Share Of Software In Overall Capex Has Been Rising Steadily

Share Of Software In Overall Capex Has Been Rising Steadily

Macroeconomic Backdrop Imminent Rate Hikes Tighter monetary policy and runaway inflation are at the fore of investors’ minds and, arguably, a cause of the current market rout. Software stocks have outperformed the other long-duration technology stocks. To gauge the reaction of S&S to the upcoming rate hike, we have repeated an exercise we conducted for the Technology sector last week – historical performance of the industry six months before and after the first rate hike (Chart 8). Clearly, industry returns fall two to three months before the first rate hike, but eventually recover once a new monetary regime is priced in. The year-to-date correction of the software stocks is textbook behavior. Chart 8S&S Underperforms Before The First Rate Hike

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Software And Services Is A Global Industry – Beware Of A Strong Dollar The Technology sector is one of the most global sectors in the S&P 500 and derives 40% of sales from abroad; similarly, Software and Services has a broad international footprint. As US rates trend higher, and the interest rate differential favors the US vs. other countries, the USD is likely to appreciate further. With a stronger dollar, products of US software firms are more expensive to foreigners, which may have a dampening effect on demand. The US firms’ profitability has also been hit by an unfavorable translation from foreign currency back to the USD. Historically, the path of the dollar and the returns of S&S were inversely correlated (Chart 9). Chart 9Historically, Stronger Dollar Has Been A Headwind For The Industry

Historically, Stronger Dollar Has Been A Headwind For The Industry

Historically, Stronger Dollar Has Been A Headwind For The Industry

The redeeming grace is that, as we mentioned before, software subscription revenue is sticky, and switching costs for customers are high. As such, we expect the adverse effect on demand to be minor. Fundamentals Sales Growth According to Grandview Research , the business software and services market is expected to grow at a compound annualized rate of 11.3% from 2021 to 2028. This strong growth is underpinned by the robust pace of enterprise application cloud migration and digital transformation, which see no end in sight. The street expects the Software and Services industry to grow on par with the Technology sector at just under 20% over the next 12 months, and growth is slowing off high levels. The pandemic has shifted forward some of the spending on software, as companies rushed to adjust to remote work. However, the industry continues to grow at a healthy clip (Chart 10). Chart 10Sales Growth Is Slowing

Sales Growth Is Slowing

Sales Growth Is Slowing

Labor Costs Are Contained For Now The S&S companies first and foremost rely on the talent and ingenuity of their workforce to deliver cutting-edge technological solutions. Wages are one of the largest expenses in the industry. Recent increases in salaries accompanied by labor shortages and “the great resignation” are bound to cut into the margins of these companies. So far, software and services companies have been able to counter the trend (Chart 11) by deploying creative solutions, offering their employees a wide range of perks, and throwing their net wide in search of talent by offering remote work. Chart 11Industry Labor Costs Have Been Contained

Industry Labor Costs Have Been Contained

Industry Labor Costs Have Been Contained

Resilient Earnings Growth For the reasons discussed above, S&S earnings growth is remarkably resilient and stable throughout the business cycle (Chart 12). Currently, earnings expectations of S&S over the next 12 months exceed growth expectations for both the Technology sector and the S&P 500. Over the next 12 months, S&S earnings are expected to grow at 14% compared to 8.6% for the S&P 500 (Table 4). Chart 12S&S EPS Growth Bests The Tech Sector And The S&P 500

S&S EPS Growth Bests The Tech Sector And The S&P 500

S&S EPS Growth Bests The Tech Sector And The S&P 500

Table 4Earnings Growth Vs. Valuations

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Despite the slowdown in sales growth and the pick-up in labor costs, EBITDA margins have exceeded the previous peak, and are projected to trend higher towards 40% over the course of the year (Chart 13). Expecting a growth slowdown, analysts have been revising earnings expectations down for S&S companies, but by now the downgrading process has run its course, and the bar is set low (Chart 14). Chart 13Margins Will Continue To Expand

Margins Will Continue To Expand

Margins Will Continue To Expand

Chart 14Downgrades Are Bottoming

Downgrades Are Bottoming

Downgrades Are Bottoming

Valuations Since the S&S industry group’s earnings are expected to grow faster than the earnings of the Tech sector and the S&P 500, it is not surprising that it trades with a 44% premium to the S&P 500 on a forward earnings basis – a steep mark-up. The current correction has taken some froth off the industry’s valuations , with multiples contracting by 3.9 points. Even after the correction, the sector appears overvalued (Chart 15). Adjusting for expected 12-month EPS growth, S&S appears more attractively valued and trades with a discount both to tech and the broad market (Table 4). It is also important to note that the industry group is home to a plethora of quite a few smaller companies, which tend to be more expensive and more volatile: Chart 16 plots companies’ forward earnings multiples against their weight in the industry group. Chart 15Valuations Are Still Dear...

Valuations Are Still Dear...

Valuations Are Still Dear...

Chart 16Significant Valuation Dispersion Among The Constituents

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Technicals Recently, the BCA Technical Indicator has moved into the oversold territory, indicating investor capitulation. This means that this bar is cleared, and from a technical standpoint alone, Software and Services is a buy (Chart 17). Chart 17... But Technicals Indicate That S&S Is Oversold

... But Technicals Indicate That S&S Is Oversold

... But Technicals Indicate That S&S Is Oversold

Investment Implications We are both tactically and structurally bullish on the Software and Services industry group. Tactically Bullish The Software and Services industry group is an all-weather industry with an unprecedented combination of both earnings resiliency and strong growth throughout the business cycle. It is also undergoing a fundamental transformation in its business model catalyzed by a ubiquitous shift in software applications to the cloud, accompanied by displacement of the traditional on-prem license and support model with a more lucrative subscription model. The industry is expected to grow earnings in double digits and expand margins, unhindered by rising labor costs. Rising rates are certainly a headwind, but hopefully a temporary one. Froth has come off valuations, and a new monetary regime is gradually getting priced in. According to the technical indicator, the sector is oversold. On balance, we have a positive outlook on the industry group (Table 5) and maintain our overweight position. Table 5Software And Services Scorecard

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Structurally Bullish Our long-held belief is that the broader push to the cloud, augmented reality, AI, cybersecurity, and autonomous driving, which are all software dependent, are not fads but are here to stay. Software and Services are at the epicenter of technological innovation and are home to some of the best American companies. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Footnotes 1 CFRA, Industry Surveys, Software, July 2021 Recommended Allocation

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Executive Summary The tensions between Russia and the West over Ukraine are boiling over, as the risk of a conflict escalates. Following Washington’s written response to Moscow’s demands, BCA’s Geopolitical Strategy team now assigns a 75% probability to a Russian invasion of its neighbor. Matt Gertken, the team’s Chief Strategist, sees only a 10% chance that Russia will aim to conquer the whole of Ukraine. European markets are vulnerable to a Russian retaliation, and so we recommend hedging exposure to Europe and cyclical assets until the situation clears up. The euro remains at risk as long as tensions fester. Who Is Most Vulnerable To A Russian Energy Embargo?

Protection Needed

Protection Needed

Bottom Line: Buy hedges such as short EUR/JPY and short EUR/CHF to protect portfolios against the risk of a conflict in Ukraine. The euro has more downside from here. Feature Handicapping The Risk Of War On Wednesday, after weeks of tense discussions, the US sent back its formal written response to Russia’s demands. Upon analysis of the situation, our geopolitical team concluded that the Biden administration offered no significant concessions. The US will not stop providing weapons to Ukraine, which, from Russia’s perspective, implies that its largest occidental neighbor could become “Russia’s Taiwan, i.e. a foreign-backed military enemy on its door step.” Matt Gertken, BCA’s Geopolitical Strategy team’s Chief Strategist, believes that the probability of a diplomatic solution has fallen to 25%, despite the joint statement made by Russia, Ukraine, France, and Germany on January 26, which reaffirms the ceasefire in the Donbass region of Ukraine. Any minor violation of the ceasefire’s terms by Ukraine will create an excuse for a Russian invasion. The nature of the eventual conflict will be crucial to the economic and market outlook for Europe. Matt argues that Europeans are hamstrung by their large dependence on Russian energy. Even switching to US LNG in case of a crisis this winter will not fill the full gap and cause major economic distress in Europe. As a result, European governments will try to avoid a war in order to limit sanctions so that Russia does not cut energy supply further. However, Europeans are also allied with the US, which will push for sanctions and which is not as afraid of the consequences of a conflict. Faced with this dichotomy, Matt argues that the most likely outcome is that Russia will ultimately concentrate on the Eastern Ukraine. He observes that “Russia, if waging war, will prefer to receive revenues from Europe, as long as Europe is still buying. Thus, Russia will keep its military aims limited so that Germany and other countries have a basis for watering down sanctions to keep the energy flowing and avoid a recession.” In terms of the breakdown of probabilities, he sees a 65% probability of a short conflict whereby the battle is to control Eastern Ukraine, a 10% probability of a Russian effort to conquer the entire country, and a 25% probability of a diplomatic solution. According to Matt, it is too soon to buy the dip. Even if the situation on the ground matches our base case scenario of a limited conflict, Russia will employ a shock-and-awe strategy, creating the first major conflict on European soil since World War II. This will surprise investors and cause a knee-jerk spike in European energy prices. It will produce downside in the euro and in the relative performance of European equities, especially as it could take a few weeks before it becomes clear whether Russian troops will permanently cross the Dnieper. Bottom Line: European markets should brace for some volatility caused by Ukrainian events in the coming weeks. BCA’s geopolitical strategy team assigns only a 25% probability to a diplomatic resolution to the current tensions, a 65% probability to a limited Russian incursion in Ukraine, and a 10% chance of a war for the entire Ukrainian nation. Economic Risks Chart 1A Large Energy Shock For A Recession

Protection Needed

Protection Needed

The economic implications of our base case scenario – a limited conflict – are restricted. As we showed three months ago, energy consumption only represents roughly 2% of European GDP. It would require a durable shock associated with a drawn-out conflict – the 10% probability scenario – to push up this ratio to the levels reached before the GFC, when energy prices were squeezing Europe (Chart 1). Nonetheless, markets will price in this probability as the conflict starts. Thus, understanding which economy is more vulnerable will help assess the risks to the market. The first metric to gauge vulnerability is the role of fossil fuels in the energy mix of European countries. In the event that a conflict causes an increase in energy prices, countries that rely more heavily on fossil fuel will experience a greater shock. On this front, pre-pandemic data from Eurostat shows that the Netherlands, Ireland, Poland, Greece, and Germany are the most exposed nations (Chart 2). By contrast, Sweden, Finland, France, and Denmark are the least exposed as a result of the role of nuclear or wind power generation in these countries. Chart 2Who depends Most On Fossil Fuel?

Protection Needed

Protection Needed

Another metric is the share of a nation’s energy needs fulfilled by imports (Chart 3). On this score, Belgium, Italy, Spain, Greece, and Portugal are the most vulnerable nations, whereas Sweden, the UK, Denmark, and Czechia are the least at risk. Chart 3Who Depends Most On Imported Energy?

Protection Needed

Protection Needed

We can also concentrate on the impact of the risk of a Russian embargo on energy shipments to Western Europe. Chart 4 shows that, when it comes to crude oil, Finland, Poland, Hungary, and, to a lesser extent, Czechia are most vulnerable, whereas Austria, Spain, and Ireland are the least at risk. With respect to natural gas, which is crucial to electricity generation, Czechia, Finland, and Hungary are the three most vulnerable countries, whereas Sweden, Austria, Ireland, and Denmark are not (Chart 5). Chart 4Who Depends Most On Russian Oil?

Protection Needed

Protection Needed

Chart 5Who Depends Most On Russian Natural Gas?

Protection Needed

Protection Needed

We may also combine all these measures and approximate the share of the total energy needs of European countries fulfilled by Russia. Our Vulnerability Index shows that the most exposed nation is by far Hungary, followed by Poland, Germany, Czechia, and Italy (Chart 6). This ranking helps explain why the German government’s support for Ukraine remains somewhat tepid, and why Italian businessmen still held a video call with Russian president Vladimir Putin as recently as last Wednesday. Chart 6Who Is Most Vulnerable To A Russian Energy Embargo?

Protection Needed

Protection Needed

Bottom Line: Hungary, Poland, Germany, Czechia, and Italy are the European nations most exposed to an energy crisis in the event of a drawn-out, all-out war in Ukraine, whereas Austria, Sweden, Denmark, Ireland, and the UK are the least exposed. This scenario carries only a 10% probability, but understanding its impact is important, since investors will have to adjust their expectations once a conflict begins in the Ukraine. The ECB Response The ECB response to a Ukrainian conflict will depend on the nature of the war. In our base case scenario involving a limited assault focused on Eastern Ukraine, the ECB will look at any energy shock and its impact on inflation as temporary. European wage gains remain limited (Chart 7), and the Governing Council will assume that any spike in energy prices will not last long enough to dislodge European inflation expectations. This picture will be very different if Russia tries to conquer Western Ukraine as well. While the potential energy embargo will most likely cause a European recession, it will also risk pushing up inflation expectations permanently. Because expectations are already close to the ECB’s objective (Chart 8), the ECB will respond by tightening policy, which many members of the GC will want. This action is likely to accentuate any recessionary pressures in Europe. Again, we cannot stress enough that this constitutes a tail risk and is not our base case scenario. Chart 7European Wage Growth Remains Tame

European Wage Growth Remains Tame

European Wage Growth Remains Tame

Chart 8Inflation Expectations Could Become Unmoored

Inflation Expectations Could Become Unmoored

Inflation Expectations Could Become Unmoored

Market Implications The Euro Three weeks ago, we wrote that the euro was not ready to bottom because the risks associated with a slowing Chinese economy, the continued economic impact of Omicron, and the volatility of the natural gas market were still too considerable. Chart 9Another Wave Of Euro Selling

Another Wave Of Euro Selling

Another Wave Of Euro Selling

This is even more true after last week’s Fed press conference, when FOMC Chair Jerome Powell did not contest the aggressive market pricing in the OIS curve. As a result, the window remains open in the near-term for interest rate differentials to move in a euro-bearish fashion (Chart 9). Ukraine adds another near-term threat to the euro. First, the run-up to an invasion, whether total or partial, will create a risk-off wave in global markets. Geopolitically driven sell-offs are most often associated with a rise in the counter-cyclical dollar, which is euro-bearish. The Swiss franc too would benefit against the euro. Moreover, Europe is much more exposed than the US to the economic consequences of a Ukrainian crisis. Obviously, our base case scenario implies a shorter and shallower sell-off than what would happen if Russia tried to conquer the whole of Ukraine. Nonetheless, a move below EUR/USD 1.10 now carries a greater than 40% probability. Bunds In our base case scenario of a limited Russian incursion in Ukraine, we should see a temporary dip in German yields driven by risk aversion. However, larger economic forces continue to point toward higher yields around the world, including in Germany. In our tail risk scenario, the German yield curve is likely to invert. ECB rate hikes will not be enough to push up 10-year yields, as markets will reflect that these increases will be temporary because of the associated recession. Instead, German 10-year yields will regress toward their 2021 lows of -0.55%. Equities Chart 10European Stocks Are Now Cheap

European Stocks Are Now Cheap

European Stocks Are Now Cheap

Since mid-December, European equities have been outperforming US equities on the back of rising yields. We expect European shares to continue to outperform US stocks over the remainder of the year. As we wrote two weeks ago, European stocks possess a more generous valuation cushion against higher yields than their US counterparts, especially now that forward multiples have fallen back to 15.4, their lowest levels since May 2020 (Chart 10). Moreover, the greater cyclicality of European stocks means that they will benefit from an eventual stabilization of the Chinese economy by the latter half of 2022. They also stand to gain from a gradual normalization of the terminal rate proxy over the coming years, which often coincides with an outperformance of value stocks over growth names. Despite this positive outlook, the Ukrainian crisis poses a considerable near-term risk, even in the base case scenario of a limited Russian military aim. The wave of risk aversion will hurt the euro, which arithmetically will weigh on the relative performance of European stocks in common currency terms. Moreover, the more pro-cyclical profile of European stocks will accentuate their vulnerability in a geopolitical crisis. However, the temporary nature of the risk-off wave means that the woes suffered by Europe will also be transitory. Under the tail risk scenario, European equities will not be capable of outperforming those of the US for many months because of the high recession risk that will engulf the region. High energy prices will destroy the profit margins of European companies, which will already suffer from a hit to their top line-growth. US equities will suffer too, but significantly less so. Chart 11European Cyclicals Are Exposed To A Crisis In Ukraine

European Cyclicals Are Exposed To A Crisis In Ukraine

European Cyclicals Are Exposed To A Crisis In Ukraine

Sector wise, a Ukrainian crisis will also short circuit the outperformance of European cyclicals over defensive equities. For now, European cyclicals have managed to generate alpha, despite the market correction (Chart 11), but the risk of a recession will affect this trend. Under our base case scenario, the underperformance will be short-lived, even if it proves severe; however, under the tail risk scenario, the cyclicals-to-defensives ratio will plunge toward the bottom of its historical range. Within defensive sectors, utilities will likely underperform, especially if the tail risk scenario comes to fruition. European governments will not allow utilities to pass on the full increase in natural gas prices to consumers, which will create a major compression in utilities’ profit margins. For cyclical names, consumer discretionary will bear the brunt of any sell-off. They are relatively pricey and the combination of the potential shock to household disposable income and rising risk aversion will prove to be lethal. The sales and profit margins of industrials will be under stress. However, this shock will be transitory if the Ukrainian crisis remains contained in our base-case scenario. Chart 12The Russian Exposure Of European Banks

Protection Needed

Protection Needed

Financials carry their own risk in the context of a drawn-out Ukrainian crisis. European banks have exposure to Russia equal to $106 billion, concentrated in France and Switzerland (Chart 12). In and of itself, this is small. However, if European nations impose large enough sanctions on Russia, not only will that country cut its energy shipments to Western Europe, but Russian firms will also likely default on their foreign obligations, emboldened by Russia’s robust FX reserves and balance of payments. In the context of a recession wherein the ECB also hikes rates, these defaults will add considerable stress to the European banking sector. Thus, under our tail risk scenario, financials could perform particularly poorly. In terms of the implications for countries, Germany is the most exposed of all the major European markets to a Ukrainian crisis because of its high energy dependence on Russia and fossil fuels. The recent underperformance of German equities when we correct for sectoral bias probably already reflects the recent rise in electricity costs in the country, which hurt German firms versus their European competitors (Chart 13). While we like the fundamentals of European small-cap stocks, we have remained on the sidelines because of the strong correlation between their relative performance and the trade-weighted euro (Chart 14). The risks surrounding Ukraine and their implications for both the euro and the European economy suggest it is still too dangerous to pull the trigger and overweight small-cap in Europe. However, if our base case scenario of a limited conflict comes true, then this will create the perfect opportunity to move into the European small-cap space. Chart 13German Suffers A Nat Gas Discount

German Suffers A Nat Gas Discount

German Suffers A Nat Gas Discount

Chart 14Small-Caps Need A Euro Bottom

Small-Caps Need A Euro Bottom

Small-Caps Need A Euro Bottom

Investment Implications Considering the probability distribution laid out by BCA’s Geopolitical Strategy team, whose base case scenario is a limited Russian incursion into Ukraine, we do not expect NATO countries to impose sanctions severe enough to force Russia to cut Western Europe’s energy supply. Nonetheless, the prospect of the most significant military conflict on European soil since World War II will have a significant impact on European asset prices, even if this effect is transitory. As a result, we still maintain our preference for cyclical equities in Europe and still expect European equities to outperform US stocks over the course of 2022. We also continue to anticipate that European stocks will outperform Bunds in 2022. Nonetheless, ahead of the conflict, we recommend investors buy some hedges, such as short EUR/CHF and EUR/JPY to protect against downside risk. Rapidly after the conflict begins, an opportunity to close those hedges will emerge. With respect to the euro, the combined stress from a hawkish Fed and Ukrainian risks means we will stay on the sidelines after having been stopped out of our long EUR/USD trade. If our base case of a limited conflict does come to fruition and Russia instead initiates a full invasion of Ukraine, we will shift our portfolio to a fully defensive stance. The euro could re-test parity or even drop below it. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations Closed Trades Currency Performance Fixed Income Performance Equity Performance

The Q4 US Employment Cost Index was somewhat mixed. It decelerated from 1.3% to 1.0% on a quarter-on-quarter basis – falling below the anticipated 1.2%. However, the annual rate accelerated to a two-decade high of 4% y/y from 3.7% in Q3. Elevated wage…

The signal from the US Q4 GDP release is that consumption remains a healthy component of the US economic expansion. The 3.3% q/q increase in personal consumption is above the average 2.5% q/q recorded over the 2015-2019 period. True, the positive consumption…

HighlightsThe current surge in US measured productivity looks very unlike what occurred in the mid-to-late 1990s. A detailed breakdown of labor productivity growth points to atypical labor market compositional effects – namely a significant decline in services employment – as being responsible for the apparent rise in productivity. In addition, technological disinflation, a major ingredient of the late 1990s “disinflationary boom”, is absent today.A cross-country comparison of the growth in output per worker during the pandemic can be mostly explained by differences in the fiscal response to the crisis. US output per worker surged compared to other countries, but the US fiscal response also generated a significant amount of excess income to support economic activity – unlike in the euro area, UK, and Japan.Micro-level arguments and some academic studies argue against the idea that work from home arrangements will ultimately be productivity-enhancing. Remote work makes it more difficult for firms to train the next generation of senior employees, which will raise the staffing risks for many businesses.While the long-term outlook for technologically-driven productivity growth is positive, projected commercialization timelines for several well-known technologies under development do not point to an imminent, inflation-offsetting boom in potential output.If inflation remains significantly above target after the pandemic is over, the Fed’s long-term interest rate projections may rise. US stocks would suffer potentially large losses in a scenario where 10-year US Treasury yields rise towards the potential growth rate of the economy. Investors should consider reducing their equity exposure if 5-year, 5-year forward US Treasury yields break above 2.5%. We do not expect that to occur this year, which for now justifies an overweight stance towards risky assets.Feature Chart II-1A Pandemic-Driven Productivity Surge?

A Pandemic-Driven Productivity Surge?

A Pandemic-Driven Productivity Surge?

The behavior of US labor productivity during the COVID-19 pandemic has raised several questions among investors. As defined by output per hour worked, US productivity accelerated significantly over the first six quarters of the COVID-19 pandemic, but then fell sharply in Q3 2021 (Chart II-1). While some market participants have questioned the cause of the recent decline, investors have generally been more interested in the question of whether the US is in the middle of a long-lasting productivity surge that will help alleviate inflationary pressure – akin to what occurred in the second half of the 1990s.In this report, we review the recent surge in US labor productivity in contrast to what occurred in the late-1990s, and then compare it with what has occurred globally. While we are not pessimistic about the pace of technological advancement and its potential to drive long-run productivity, we conclude that the US is not likely experiencing a sustained productivity boom driven by technological adoption during the pandemic. This underscores why investors should not expect a significant increase in potential output owing to the pandemic or its effects. It also highlights that, if elevated inflation in response to strongly positive output gaps were to occur over the coming few years, it would likely be met by significantly tighter fiscal or monetary policy.Today Versus The 1990s: Total Factor Productivity Versus Capital Intensity Chart II-2The Technologically-Driven US Productivity Surge In The 1990s Was A Major Macro Event

The Technologically-Driven US Productivity Surge In The 1990s Was A Major Macro Event

The Technologically-Driven US Productivity Surge In The 1990s Was A Major Macro Event

A technologically-driven surge in productivity growth in the second half of the 1990s was a highly significant macroeconomic event. Chart II-2 highlights that US labor productivity surged to over 3% from 1995 to 2000, alongside a significant deceleration in core PCE inflation and a sizeable acceleration in potential GDP growth.Given the acceleration in measured productivity during the pandemic, and the accompanying rapid adoption (or broader use) of technology, it is easy to see why some investors have questioned whether a 1990s-style productivity boom is underway. However, a detailed breakdown of the 2020 rise in labor productivity growth highlights substantial differences between the current environment and that of the late 1990s, which points instead to compositional effects as the main driver.Improvements in labor productivity can come from smarter workers, an increase in the amount of capital employed per worker, or from technological innovations and better working practices. The US Bureau of Labor Statistics provides a breakdown of the annual change in labor productivity that attempts to capture these three components:The contribution from shifts in labor composition: This measures the productivity impact of changes in the age, education, and gender structure of the labor force.The contribution from capital intensity: This measures the productivity impact of shifts in the amount of capital equipment available per worker.Total factor (or “multifactor”) productivity: This measures the changes in output per hour that cannot be accounted for by the above two factors. Thus, it includes the effects of technological changes, returns to scale, shifts in the allocation of resources, and other changes in operating procedures.Examining the 2020 rise in labor productivity growth along these three factors underscores key differences between the current environment and that of the late 1990s.The first point for investors to note is that the acceleration in labor productivity in 2020 occurred alongside a contraction in total factor productivity (TFP) growth, in contrast to the 1990s when TFP drove labor productivity (Chart II-3). The fact that TFP growth fell in 2020 means that the increase in labor productivity must have occurred either because of labor composition or capital intensity effects.In 2020, labor composition contributed somewhat to accelerating labor productivity, but that most of the increase was caused by a sharp increase in capital intensity. Some of the increase in overall capital intensity occurred because of an increase in the intensity of information processing equipment and intellectual property products (supporting the idea of an increase in pandemic-driven capital deployment), but this was outstripped by the contribution of “other” capital services (Chart II-4). Chart II-3Total Factor Productivity Collapsed In 2020, Unlike In The 1990s

Total Factor Productivity Collapsed In 2020, Unlike In The 1990s

Total Factor Productivity Collapsed In 2020, Unlike In The 1990s

Chart II-4The Surge In US Capital Intensity Reflects A Rapid Compositional Shift In The Labor Market

February 2022

February 2022

The concept of capital intensity refers to the amount of capital available per worker, but in practice it is measured as the ratio of the amount of capital used relative to the amount of labor hours used to produce output. Thus, a surge in capital intensity that is not accounted for by an increase in the amount of tech-related capital available to workers points to a rapid compositional shift in the economy from relatively low capital-intensive industries to relatively high-intensive industries.Under less extreme economic circumstances we would be more inclined to search for other potential causes of a rapid increase in measured capital intensity, but a shift in employment from less to more capital-intensive industries is exactly what has occurred during the pandemic. Services jobs tend to be much more labor-intensive than goods-producing jobs; Chart II-5 highlights that the former fell far more than the latter during the pandemic, in sharp contrast to what normally occurs during a recession (Chart II-6). This phenomenon is also reflected in a highly unusual decline in services spending compared with very strong goods spending relative to their pre-pandemic trend. Chart II-5Employment In Low Capital Intensity Services-Producing Industries Fell Far More Than Goods-Producing

Employment In Low Capital Intensity Services-Producing Industries Fell Far More Than Goods-Producing

Employment In Low Capital Intensity Services-Producing Industries Fell Far More Than Goods-Producing

Chart II-6The Sharp Decline In Services Jobs During The Pandemic Was Unprecedented

The Sharp Decline In Services Jobs During The Pandemic Was Unprecedented

The Sharp Decline In Services Jobs During The Pandemic Was Unprecedented

The takeaway for investors is that the nature of the pandemic and its unique impact on the economy has created the appearance of an acceleration in productivity, when in reality true productivity has fallen and the standard measure of productivity is being flattered by enormous changes in the composition of the labor market.Today Versus The 1990s: IT Investment, And Technological DisinflationThe trends in IT investment and prices highlight another major difference between the current environment and that of the late 1990s. Charts II-7 and II-8 highlight recent trends in comparison to those of the 1990s, with the following notable points: Chart II-7There Are Major Differences Between IT Investment And Prices Today Versus The 1990s

There Are Major Differences Between IT Investment And Prices Today Versus The 1990s

There Are Major Differences Between IT Investment And Prices Today Versus The 1990s

Chart II-8A One-Off Move

A One-Off Move

A One-Off Move

The recent pace of real investment in total IT does not point to the pandemic as a sustained source of productivity growth. Real investment in IT has already slowed significantly, in contrast to the 1990s when it accelerated on a sustained basis for years.IT investment as a % of GDP and of total plant and equipment spending has already stopped rising (or is now falling), exhibiting clear signs of a one-off shift and thus undermining the view that IT investment has significantly raised potential output.In pronounced contrast to the mid-1990s when IT equipment prices were collapsing, computing equipment inflation has recently risen into positive territory – to the highest levels recorded since the data became available in 1959.Higher prices for IT equipment clearly reflect, at least in part, pandemic-driven pressure on global supply chains and the production of semiconductors. So we do not expect sustained increases in the price of computing equipment. But the key point for investors is that a major ingredient of the late 1990s “disinflationary boom” is missing today.The US Versus The WorldWe have presented Chart II-9 in previous reports to highlight that there is certainly no evidence of a global productivity surge, using output per worker as a proxy for the standard measure of labor productivity (output per hour worked). Some investors have countered that the US is a more dynamic economy, and that a sustained productivity boom would be more apparent in the US prior to its emergence in other countries. Or simply that the US alone is experiencing a productivity boom that will help reduce very elevated US inflation, with strong implications for Fed policy. Chart II-9During The Pandemic, Cross-Country Changes In Real Output Per Worker…

February 2022

February 2022

Chart II-10…Are Mostly Explained By Different Fiscal Responses

February 2022

February 2022

Chart II-11High US Real Output Per Worker Also Reflects A Lagging Jobs Recovery Relative To Pre-Pandemic Levels

High US Real Output Per Worker Also Reflects A Lagging Jobs Recovery Relative To Pre-Pandemic Levels

High US Real Output Per Worker Also Reflects A Lagging Jobs Recovery Relative To Pre-Pandemic Levels

Charts II-10 and II-11 present a different cross-country comparison that reinforces the view that the US is not likely experiencing a long-lasting productivity surge that will help reduce inflation. Chart II-10 highlights that in the face of a significant decline in employment, US output was supported by a substantial amount of “excess income” – the cumulative amount of household disposable income earned over the course of the pandemic in excess of what would have been predicted based on the pre-pandemic trend.Other major DM economies (such as the UK and euro area) either saw negative excess income or a modestly positive amount (Japan), underscoring that the fiscal response to the pandemic in most advanced economies was aimed at stabilizing income rather than raising it. In combination with Chart II-11 – which highlights that the US labor market recovery has significantly lagged behind the European and Canadian economies in terms of returning to the pre-pandemic employment trend – this would appear to explain why the US has experienced stronger real output per worker than other countries. Chart II-12Given A Similar Fiscal Response, Would The US Have Canada's Job Recovery If It Had Less COVID Cases?

Given A Similar Fiscal Response, Would The US Have Canada's Job Recovery If It Had Less COVID Cases?

Given A Similar Fiscal Response, Would The US Have Canada's Job Recovery If It Had Less COVID Cases?

Canada stands out as the outlier compared with the US, in the sense that it’s growth in real output per worker has been much lower but Canadian fiscal policy created a similar amount of excess income. However, it may be the case that the Canadian experience highlights that the US labor market recovery is the outlier, which could imply that the surge in US labor productivity may in fact have inflationary rather than disinflationary consequences at the margin.We discussed the factors that we believe are driving the slow recovery in the US working-age population in our 2022 annual outlook report, and how they are strongly linked to the pandemic. However, Canada has also clearly been affected by COVID-19, and yet it has experienced a more significant recovery in jobs.Chart II-12 highlights that there has been one major difference between the US and Canada during the pandemic: a substantial gap in the burden of disease from COVID-19. This raises the question of whether Canada has outperformed the US in terms of its labor market recovery, despite a similarly impactful fiscal response, because of a smaller labor shortage stemming from long-term COVID symptoms.Over the past two years, there have been many reports about people who have recovered from COVID but who continue to experience some symptoms of the disease. The medical community has labeled this condition as post-acute sequelae of SARS-CoV-2 infection (PASC), colloquially referred to as “long COVID.” Chart II-13Long-COVID Might Help Explain The US’ Lagged Return To Pre-Pandemic Employment

February 2022

February 2022

The medical community’s understanding of long COVID is currently poor, and doctors do not know why some people get the condition or what treatment options are likely to be the most effective. Given this, it is possible that some reports of long COVID are, in fact, related to other conditions.But a recent research report from Brookings estimated that the US labor market may be missing 1.6 million workers because of long COVID’s effects (Chart II-13), which alone would account for 1 percentage point (or roughly 1/4th) of the growth in US real output per worker since the pandemic began. This circumstance would be inflationary rather than disinflationary on the margin, as it would imply that accelerating first and second quartile US wage growth may be sticky even as the pandemic recedes.Is Working From Home Positive For Productivity?We have noted above that the macro data argues against the idea of a sustained rise in US productivity stemming from the pandemic. A more micro-level perspective, one that examines the working-from-home (WFH) experience, also appears to support our case.It is true that surveys of employees highlight that their experience of WFH has been significantly better on average than workers expected and report their being more productive while working from home during the pandemic. Chart II-14 emphasizes that, based on the running surveys from Barrero, Bloom, and Davis (“BBD”), 60% of workers have conveyed better WFH outcomes relative to expectations, versus just 14% reporting worse outcomes. In addition, Chart II-15 clearly highlights that workers prefer at least some form of hybrid WFH arrangement, with just 22% of survey respondents reporting the desire to work from home either rarely or never. Chart II-14Remote Workers Have Reported Better Work-From-Home Outcomes Than What Was Expected

February 2022

February 2022

Chart II-15Remote Workers Clearly Prefer A Hybrid Work Model

February 2022

February 2022

However, worker preferences do not necessarily correlate with productivity gains, at least not to the same degree. Chart II-16 from the BBD surveys highlights that the share of workers reporting more efficiency while working from home is not as large as those reporting better outcomes relative to expectations, suggesting that employees are considering whether WFH arrangements are benefiting them personally when responding to their desired post-pandemic level of remote work. Chart II-17 also shows that employees working from home only spend a third of the time ordinarily allocated to commuting to working on their primary job; the rest is spent on childcare, leisure, home improvement, or working on a second job (which may or may not be a sustainable source of income). Chart II-16Less Than Half Of Workers Report Being More Efficient While Working Remotely

February 2022

February 2022

Chart II-17Only 1/3rd Of Time Saved Commuting Is Spent On Primary Employment

February 2022

February 2022

There is also some evidence from academic studies that indicates productivity fell during the pandemic for some remote workers. Michael Gibbs, Friederike Mengel, and Christoph Siemroth (2021) surveyed 10,000 professionals at a large Asian IT services company, and found that productivity declined because of a slight decline in average output and a rise in hours worked.1 Admittedly, elements of the study did point to some factors potentially impacting this decline in productivity that were more prominent in the earlier phase of the pandemic, specifically the issue of childcare (which would not likely be a drag on remote worker productivity in a post-pandemic environment).But it also noted that employees with a longer company tenure fared better, which in our view is an often overlooked element of remote work that points to less future productivity gains from WFH arrangements than may be recognized by investors. The outperformance of senior staff in a WFH environment is not particularly surprising: once employees have accrued significant experience, they spend less of their working time learning and more (or all) of their working time “doing.” It makes sense that employees who predominantly “platform” their existing experience may fare the same or better in a WFH arrangement, but it is highly questionable whether it is sustainable, because it makes it much more difficult for businesses to train the next generation of senior employees.The Gibbs, Mengel, and Siemroth study noted that higher communication and coordination costs featured prominently in their findings of reduced remote worker productivity. Importantly, they found that employees communicated with fewer individuals and business units, both inside and outside the firm, and received less coaching and one-to-one meetings with supervisors. While some firms may be able to mitigate these risks to the advancement and development of more junior staff while maintaining a hybrid on-site / WFH model, we suspect that many firms will fail to do so fully.Future Productivity: Pessimism Unwarranted, But No Inflation SalvationThe fact that the US is not likely in the middle of a pandemic-driven productivity boom does not mean that the outlook for productivity is poor. In fact, we would point to two factors that lead us to believe that productivity growth will be better in the future than it has been over the past decade:The pronounced consumer deleveraging phase that existed for several years following the global financial crisis is over, andThere are several identifiable technologies currently under development that are likely to have legitimate commercial applications and productivity-enhancing benefits in the futureOn the first point, we have contended in previous reports that the weak productivity growth observed during the first half of the last economic expansion was because of demand rather than supply-side factors. This notion is jarring for many investors, who are accustomed to think of productivity trends as being exclusively driven by supply-side phenomena. This is typically correct, in that the cyclical impact of fluctuating aggregate demand on measured productivity – particularly during and immediately after recessions – is usually temporary in nature.However, the 2008/2009 recession was highly atypical, in the sense that it was a household “balance sheet” recession rather than a normal “income” recession. This led to a prolonged period of US household deleveraging, below-average corporate sales growth, and poor growth in output per hour worked. In effect, the post-2008 deleveraging phase created a long-lasting, multi-year cyclical effect on measured productivity growth.In early-2009, pessimistic investors held to an understandable reason for why they doubted the sustainability of the economic recovery: there could be no meaningful labor market recovery if businesses expected several years of weak demand because of the likelihood of consumer deleveraging. In this respect, the post-2008 period served as an important natural experiment for macroeconomists and investors: we have learned that the response of firms to a durable but shallow economic recovery is, on the one hand, to hire additional workers, but, on the other hand, also to control wage and salary costs aggressively. Chart II-18Slow Productivity Growth Last Cycle Was A Demand Story, Not A Supply Story

February 2022

February 2022

Chart II-18 encapsulates the point that weak productivity during the last economic cycle was closely tied to US household deleveraging. The chart highlights that the decline in total factor productivity due to goods-producing industries – heavily concentrated in manufacturing – was much larger than for private services from 2007 to 2019. Since there was no technological slowdown that disproportionally impacted the manufacturing industry during the period, this clearly points to demand-side rather than supply-side factors as the main driver of the post-GFC productivity slowdown.On the second point about future productivity growth, Table II-1 outlines five well-known technologies that are in various stages of development and are likely to lead to significant applications at some point in the future: artificial intelligence, automated driving (a specific application of AI), quantum computing, augmented/virtual reality and human-machine interface, and CRISPR/gene editing. The table outlines the nature of potential future applications, as well as projections from McKinsey Global Institute about the most likely commercialization timeline. Table II-1Technological Advancement Is Ongoing. It Won’t Likely Help Fight Inflation Over The Next Few Years

February 2022

February 2022

A detailed analysis of each of these technologies is beyond the scope of this report, but Table II-1 underscores two key points for investors. The first is that further, technologically-driven productivity growth is not just possible, it is likely. It is clear what advancements will probably drive these productivity gains, and Table II-1 highlights only the most well-known technologies to which experts in the field would point to.The second point is that most major changes from these technologies are projected to occur beyond 2025, and, in many cases, beyond this decade. In the case of quantum computing, while it could potentially lead to an explosion of algorithmic power that would almost certainly have major commercial implications, it is even possible that this technology will initially subtract from total factor productivity growth before contributing positively. This is because of its potential to render much of the existing global internet security and privacy infrastructure useless, as highlighted by a NIST Cybersecurity White Paper last April:“Continued progress in the development of quantum computing foreshadows a particularly disruptive cryptographic transition. All widely used public-key cryptographic algorithms are theoretically vulnerable to attacks based on Shor’s algorithm, but the algorithm depends upon operations that can only be achieved by a large-scale quantum computer. Practical quantum computing, when available to cyber adversaries, will break the security of nearly all modern public-key cryptographic systems.”2Some experts believe that the preparation required to avoid this outcome may dwarf that of the millennium bug (“Y2K”) problem of the late-1990s,3 which cost roughly 1% of GDP to fix – and thus was clearly not productivity-enhancing.The bottom line for investors is that while the long-term outlook for technologically-driven productivity growth is bright, it is unlikely to save the US and/or global economies from elevated inflation over the next several years if output gaps in advanced economies rise to strongly positive levels in the wake of the pandemic.Investment ConclusionsOur analysis above has highlighted that the current surge in measured productivity looks very unlike what occurred in the mid-to-late 1990s, and that very atypical labor market compositional effects are likely responsible for the apparent rise in labor productivity. We have also highlighted that a cross-country comparison of the growth in output per worker during the pandemic can be mostly explained by differences in the fiscal response to the pandemic, and that there are micro-level arguments against the idea that work from home arrangements are productivity-enhancing. Finally, while the long-term outlook for technologically-driven productivity growth is positive, projected commercialization timelines for several well-known technologies under development do not point to an imminent, inflation-offsetting boom in potential output.While we believe that the COVID-19 pandemic will recede in importance this year, it is not yet over. As such, investors do not yet know how strong the output gap in the US and other advanced economies will be on average over the coming two to three years, or what the pace of consumer price inflation will look like in the face of strong aggregate demand but substantially lower (or no) pressure from the supply-side of the economy (as we expect). Chart II-19There Is A Lot Of Downside For Stocks If Bond Yields Rise To Potential Growth Rates

There Is A Lot Of Downside For Stocks If Bond Yields Rise To Potential Growth Rates

There Is A Lot Of Downside For Stocks If Bond Yields Rise To Potential Growth Rates

In a scenario in which aggregate demand remains strong next year and inflation remains above-target, even in the face of Fed tightening and a normalization in services/goods spending, we would expect to see significantly tighter fiscal or monetary policy. This is a scenario in which the secular stagnation narrative, which underpins the Fed’s low long-term interest rate projection, would likely be aggressively challenged by investors. Chart II-19 highlights that US equities would potentially suffer a 24% contraction in the forward P/E in a scenario in which the equity risk premium is in line with its historical average and 10-year US Treasury yields rise to the potential growth rate of the economy.We do not yet believe that a significant rise in long-term interest rate expectations will occur this year, meaning that investors should still be overweight stocks versus government bonds over the coming 6-12 months. But as we noted in last month’s report, we may recommend that investors reduce their equity exposure if 5-year, 5-year forward Treasury yields break above 2.5% (the FOMC’s long-run Fed funds rate projection), which we noted in Section 1 of our report is 50 basis points above current levels.Jonathan LaBerge, CFAVice PresidentThe Bank Credit AnalystFootnotes1 Michael Gibbs, Friederike Mengel, and Christoph Siemroth. “Work from Home & Productivity: Evidence from Personnel & Analytics Data.” Working Paper No. 2021-56. July 13, 2021. Pp. 1-30.2 William Barker, William Polk, and Murugiah Souppaya. “Getting Ready for Post-Quantum Cryptography: Exploring Challenges Associated with Adopting and Using Post-Quantum Cryptographic Algorithms.” National Institute of Standards and Technology, US Department of Commerce. April 28, 2021. Pp. 1-7.3 Jonathan Ruane, Andrew McAfee, and William Oliver. “Quantum Computing for Business Leaders.” Harvard Business Review, January-February 2022.

Highlights The combination of a temporarily negative domestic demand effect and a lingering domestic labor and global supply chain effect from the Omicron variant has increased the urgency for the Fed to raise interest rates. The central bank’s credibility has been significantly challenged over the past year by the extent of the rise in consumer prices, and it will move forward with a rate hike at its March meeting. We expect that the Fed funds rate will rise to 1% by the end of this year. The Fed’s asset purchase reductions will not have a direct impact on economic activity, but they could have an indirect effect by prompting a faster rise in US Treasury yields towards their fair value levels. The US 10-year yield could potentially rise to 2.3-2.4% at some point in the first half of the year, rather than by the end of 2022 as we previously expected. Part of the generalized rise in risk premia this month relates to the potential Russian invasion of Ukraine, but the sell-off in equity prices also appears to reflect an overall level of investor discomfort with rising interest rates. Rising long-maturity bond yields are being driven by the short end of the curve, which we see as a sign that the generalized selloff in the US equity market is uncalled for. Investors should buy the US stock market at current levels on a 6-12 month time horizon. It is too early to position aggressively towards China-sensitive commodities and global ex-US stocks, despite the recent pickup in our market-based growth indicator for China. We are more comfortable with a bullish view toward industrial metals in the latter half of 2022, and recommend that investors buy metals on any dips in prices. A Russian invasion of Ukraine has become a likely event, suggesting that investors need to decide now whether to reduce risky asset exposure. The invasion has not yet occurred as we go to press, but could happen at any moment. All told, we doubt that a minor invasion will have a lasting, full-year impact on financial markets, but investors should gird for a risk-off reaction over shorter-term time horizons. Omicron, The Supply-Side, And The Fed January was a poor month for the global equity market, which sold off 10% from its high at the beginning of the year. Chart I-1 highlights that in the US, the S&P 500 has now fallen below its 200-day moving average, in contrast to global ex-US stocks which have fared somewhat better in US$ terms. Equities have declined this month because of a combination of imminent Fed tightening and a geopolitical crisis, both of which we will discuss in detail below. On the pandemic front, the number of confirmed cases of COVID-19 has surged globally (Chart I-2), which is likely an underestimation of the total number of infections given capacity limits on testing in many countries. Panel 2 highlights that services PMIs fell sharply in January in several economies because of the Omicron wave, reflecting both renewed pandemic control measures in some countries as well as precautionary changes in behavior amongst consumers in countries where widespread “non-pharmaceutical interventions” (“NPIs”) were not reintroduced. Manufacturing PMIs, on the other hand, held up quite well, even in Europe where natural gas prices remain high. Chart I-1A Significant Correction In US Stock Prices

A Significant Correction In US Stock Prices

A Significant Correction In US Stock Prices

Chart I-2Omicron Is Impacting Services, Not Manufacturing

Omicron Is Impacting Services, Not Manufacturing

Omicron Is Impacting Services, Not Manufacturing

Some positive signs have emerged from the hospitalization data in advanced economies, as they appear to be pointing to a cresting wave of patients with COVID-19 both in hospitals overall and specifically in intensive care units (Chart I-3). The evolution of the pandemic remains highly uncertain, and the development of new variants continues to remain a risk. But incoming data on hospitalizations, the rapid increase in the number of vaccine booster doses administered in many advanced economies, and the sheer speed at which the disease has recently been spreading all point to a possible imminent peak in the impact of the Omicron variant on the demand side of the economy – at least in the developed world. However, Chart I-4 highlights that there is no sign yet of a waning impact of the pandemic on the supply side of the economy. The chart shows that rising European natural gas prices are having less of an impact on our supply-side pressure indicator, but that the indicator remains flat excluding this effect. We noted in last month’s report that the Omicron variant posed a significant risk of more frequent or longer lockdowns in China, because of the country’s zero-tolerance COVID policy and the inability of the Sinovac vaccine to provide any protection against contracting Omicron. Panel 2 of Chart I-4 highlights that shipping costs between China/East Asia and the west coast of the US have started to tick higher again, suggesting that the impact of ongoing lockdowns as well as mandatory quarantines and testing in key areas such as Shenzhen, Tianjin, Ningbo, and Xi’an may already be having an effect. Chart I-3Hospitalizations From Omicron Appear To Be Peaking

Hospitalizations From Omicron Appear To Be Peaking

Hospitalizations From Omicron Appear To Be Peaking

Chart I-4Pandemic-Related Supply-Side Pressures Remain Severe

Pandemic-Related Supply-Side Pressures Remain Severe

Pandemic-Related Supply-Side Pressures Remain Severe

From the Fed’s perspective, a combination of a temporarily negative domestic demand effect and a lingering domestic labor and global supply chain effect from the Omicron variant has increased the urgency to raise interest rates. The Fed’s credibility has been significantly challenged over the past year by the extent of the rise in consumer prices, which is being partially driven by demand (even if supply-chain factors are also materially boosting global goods prices). Chart I-5The Odds Of Extreme US Inflation Are Falling, But Inflation Will Still Be High This Year

The Odds Of Extreme US Inflation Are Falling, But Inflation Will Still Be High This Year

The Odds Of Extreme US Inflation Are Falling, But Inflation Will Still Be High This Year