United States

Highlights Industry Deep-dive Report: The Semiconductor and Semiconductor Equipment Industry (“Semis”) has had a fantastic run over the past 12 months. We have been overweight it since June and the trade is ahead of the market by 14%. In this deep-dive report into the sector, we aim to decipher the outlook for 2022. To do so, we review the supply chain, target markets, macroeconomic backdrop, and fundamentals. Production Model: Semiconductor production is divided among IC designers and manufacturers. This separation of design and manufacturing is called the fabless model, which has grown in prominence as the pace of innovation made it increasingly difficult for firms to manage both the capital intensity of manufacturing and the high levels of R&D spending for design. Designed In The US, Made In Asia: The entire semiconductor industry depends on the cooperation between two regions: North America that houses global leaders in designing the most sophisticated chips, and Asia which is home to companies that have the technology to manufacture them. Geopolitical risks: As a result, the Semis are in the crosshairs of rising tensions between China and the US with both countries seeking chips independence and pushing for onshoring. Conventional end-demand markets span the entire US economy but can be grouped into several main categories. Computing or data processing electronics is one of the largest markets, followed by Communications, Consumer Electronics, and Autos. Growth rates vary across segments. The novel markets for semis came on the back of emerging technologies, such as IoT, 5G, automation, AI, self-driving vehicles, and others, all of which require increasing chip sophistication. These markets present a tremendous long-term opportunity for the industry. Global semis sales grew at 25 percent in 2021. In 2022, market growth is expected to slow to 10 percent. Earnings growth has also been slowing. The industry is not immune to rising costs of raw materials, labor shortages, and supply-chain disruptions. While earnings growth is slowing, operating margins are set to expand over the next 12 months. Valuations are extended: The semis' earnings growth expectations are on par with the S&P 500, but trade with a 14% premium to forward multiple. The macroeconomic backdrop is unfavorable: Tighter monetary policy, slowing economic growth, and a slowdown in China, are headwinds for this hyper-cyclical industry. Investment Outlook: We conclude that we are bullish on the industry on a structural basis but are more ambivalent about its prospects over the next 3-6 months downgrading our portfolio overweight to an equal-weight.

Chart 9

Feature Performance The Semiconductors and Semiconductor Equipment industry (“Semis”) has received an unexpected boost during the pandemic: Lockdowns, coupled with helicopter cash drops, have spurred demand for durable goods, and foundries could not work fast enough to produce chips, direly needed by autos, consumer electronics, and computer manufacturers. Since the beginning of the pandemic, Semis have outperformed the S&P 500 by roughly 62%, and the Tech sector by just under 30% (Chart 1). Only this year, Semis are almost 20% ahead of the market (Table 1). This poses a question – can this outperformance continue in 2022, or will the economic growth slowdown and waning demand for goods end this superior run? Chart 1Shortages Boosted Performance Of Semis

Shortages Boosted Performance Of Semis

Shortages Boosted Performance Of Semis

Sneak Preview: While we believe in Semis as a multi-year structural theme, we recommend a tactical equal weight. We have been overweight Semis since June and the trade is ahead of the market by 14.5%. We are closing the overweight on the back of a strong run, rich valuations, slowing earnings growth, and an unfavorable macroeconomic backdrop. Table 1Semis Had A Strong Run Over The Past 12 Months

Semiconductors: Aren't They Fab?!

Semiconductors: Aren't They Fab?!

Semiconductor Primer What Are Semiconductors? I have a confession to make – I have always had only the fuzziest idea of what is inside my computer or under the hood of my car. Well, apparently, it is semis, aka chips, that are the brains of any electronic device that we come across in our daily life. I like the comparison of chips to modern-day bricks, serving a wide range of industries. The American Semiconductor Association (ASA) calls them a “marvel of modern technology,” which they truly are, being a foundation of modern life, packed with up to tens of billions of transistors on a piece of silicon the size of a quarter. Chips power not only our phones and vacuum cleaners, but also innovative medical devices, robots, and wireless internet. Semiconductors make all sectors of the US economy, from farming to manufacturing, more efficient. The number of applications of semis is innumerable, and recent shortages made all of us more aware of these, behind-the-scenes, engines of our daily life. The US Semis Brag Sheet The US semiconductor industry is the worldwide industry leader with about half of the global market share (47%) and sales of $208B in 2020.1 The industry employs over a quarter-million people and supports nearly 1.6 million additional US jobs. Semis are a top-five US export, with more than 80% of industry sales going to overseas customers. The US exported $49B in semiconductors in 2020. Rapid innovation has allowed the industry to produce exponentially more products at a lower cost, a principle known as Moore’s law. How Are Semiconductors Made? R&D is the first step in the production process. Firms involved in semiconductor design develop nanometer-scale integrated circuits that perform the critical tasks that make electronic devices work, such as connectivity to networks, computing, storage, and power management. Chip designers must use highly advanced electronic design automation (EDA) software and reusable architectural building blocks (“IP cores”) to do this task.2 The process requires significant investment: Developing a new chip can cost over 100M dollars and requires many years of work by hundreds of engineers. As chips have become increasingly complex, development costs have rapidly risen. Design is the part of the process that differentiates one type of chips from another and constitutes a competitive moat for the companies that design them. Design is chiefly knowledge- and skill-intensive, accounting for 65% of the total industry R&D and has the highest value-add of the entire production process. Manufacturing is a complex process. Once chips are designed, the process moves to production. Often the chip production starts with processing sand that contains a large amount of silicon. Sand is purified and melted into solid cylinders, that are then sliced into very thin silicon discs, polished to a flawless finish, called “blank wafer.” Wafers are then printed with intricated circuit designs, which are later divided into tiny individual semiconductors, called dies. Dies are later packaged into finished semiconductors that can be embedded into electronic devices. This process is summarized in Chart 2.

Chart 2

Cross-Border Supply Chains Types Of Semiconductor Production Companies The chip production process is usually divided between the three types of players that operate in the different segments of the supply chain. IC designing companies or fabless firms focus only on design and outsource fabrication to pure-play foundries and outsourced assembly and test (OSAT) firms. This segment of the value chain is dominated by the US firms such as Qualcomm, Broadcom, Nvidia, and AMD, which account for roughly 60% of all global fabless firm sales (Chart 3). Semiconductor manufacturing companies, aka foundries, receive orders from the IC designing companies and purchase raw materials and equipment to proceed in the chip manufacturing process. TSMC, Global Foundries, and United Microelectronics Corporation (UMC) are some of the largest and are located in Asia. The share of chips manufactured in China, South Korea, Southeast Asia, Taiwan, and other regions in East Asia has soared to 75% (Chart 4). Integrated Device Manufacturers (IDM) cover the entire production process from design to manufacturing. In terms of revenue, Samsung, Intel, and SK Hynix are the world’s three top IDM companies. Recently, there was a global push towards reintegration for geopolitical reasons (more about that later).

Chart 3

Chart 4

The fabless model, or separation of chip design and manufacturing, has grown along with the demand for semiconductors since the 1990s, as the pace of innovation made it increasingly difficult for many firms to manage both the capital intensity of manufacturing and the high levels of R&D spending for design. Since China joined the WTO in late 2001, global manufacturing offshoring switched to a higher gear with the semiconductor industry becoming a poster child for the movement. Except for Intel, which is the only US company that both designs and manufacturers chips, other US corporations completely outsourced their manufacturing to Asia. Designed In The US, Made In Asia As of 2020, the US market share of the global semiconductor market was 47% (Chart 5), dominated by fabless firms. Given the importance of semiconductor design in terms of value-added in the manufacturing process, the US must remain a leader in this stage of production. The US firms spend 17% of sales on R&D, more than any other country, to maintain a competitive edge (Chart 6). And this decisive advantage translates into a disproportionate share of industry revenue.

Chart 5

Chart 6

While specializing in chip design creates a competitive moat for the US semi companies, it also makes them vulnerable to supply-chain disruptions: At present only a little over 10% of all chips are manufactured in the US compared to 37% back in the ‘nineties (Chart 7), with the lion’s share of the most sophisticated chips manufactured in Asia. With the separation of design and manufacturing, the US, which is a leader in design, is falling behind as a location for manufacturing technology. As a result, the entire semiconductor industry depends on the cooperation between two regions: North America that houses global leaders in designing the most sophisticated chips, and Asia that is home to companies that have the technology to manufacture the most complex of chips. Both ends (design and manufacturing) of the semiconductor industry also have high barriers to entry due to the technology required to compete in the field, which creates a big problem since major geopolitical players now aim to break down existing supply-chains and to push their corporations towards domestic vertical integration.

Chart 7

Supply Chain Fragility The fragility of the semiconductor supply chains was best revealed during the pandemic-induced shutdown. With the global economy coming to a virtual hold, various industries had to cancel their semi orders, and foundries took some of the capacity offline. However, demand for goods rebounded unexpectedly and sharply, jump-started by global fiscal and monetary stimulus. It is important to note that a semiconductor manufacturing plant cannot be simply turned on after a period of inactivity. Not only does it require time to be brought back to life, but also the chip production itself is a month-long process. Semiconductor companies did their best during the lockdown to meet demand and even got an exemption from government-imposed lockdowns as “essential” businesses. The industry managed to increase production to address high demand, shipping more semiconductors every month than ever before by the middle of 2021 (Chart 8). However, chip shortages ensued, because supply, despite its best efforts, could not keep pace with the demand. Expanding semi manufacturing capacity was not an option: Building a fab and bringing it up to full capacity can take anywhere from 24 to 42 months at a price tag of anywhere from $1.7bn to $5.4bn, depending on the quality of the chips manufactured.3 Most industry analysts expect the shortage to linger into 2022.4 Chart 8The Industry Worked Hard To Meet Demand For Chips

The Industry Worked Hard To Meet Demand For Chips

The Industry Worked Hard To Meet Demand For Chips

Geopolitics Semiconductor Industry Is At The Epicenter Of Geopolitical Tensions The semi shortages also came within the broader context of the changing world order and the resulting competition for the key resource. As a result, governments around the globe took action to secure the key commodity for themselves and to establish its production on domestic soil. In the US, once semi-conductor shortages started crippling US manufacturing back in April 2021, President Biden held a semiconductor summit at the White House. In addition, he signed an executive order calling for a 100-day review of the US supply chains. In June, the US Senate passed the bipartisan US Innovation and Competition Act, which includes $52 billion in federal investments for semiconductors (building from the CHIPS for America Act announced in January). The House of Representatives excluded the $52 billion from its version of the bill but most of this semiconductor funding will likely be reinstated in the final compromise version of the bill. We expect the funding to help US-based firms, like Intel, as well as non-US firms, such as Taiwan Semiconductor, which is putting billions of dollars into its next-generation production plant in Arizona. And last, the administration agreed with Japan to cooperate on semiconductor development and supply chains.5 Moving east, the European Commission also expressed its concerns that the Old Continent was naïve to outsource chip manufacturing and now plans to double the EU’s share of global chip production from the current 10% to 20% by 2030 under its new Digital Compass plan which aims to boost “digital sovereignty” by funding various high-tech initiatives. In China, policymakers realized the importance of semis in 2013, and while China will not achieve full self-sufficiency anytime soon, ongoing US sanctions and political pressure will only accelerate the Middle Kingdom’s push for semiconductor supply independence. Already, the new five-year plan that was released this year, prioritizes technological innovation including in the semiconductor space. Japan and South Korea are also devoting state resources to the industry, and global policymakers are seeking ways to reduce dependency on Taiwan due to the risk of conflict over the long run. The broader implication of the global semiconductor production onshoring is two-fold. First, existing supply chains will come under pressure as nations will force their respective semiconductor companies to undergo a complete vertical integration, resulting in much steeper chip prices, unless governments come out with further extravagant subsidies. This transformation also implies higher demand for the output of semiconductor equipment manufacturers as nations are scrambling to build onshore manufacturing facilities. Target Markets Most industries are run on chips, but overall usage can be grouped into several key categories, such as Computers, Communications, Consumer Goods, Autos. These traditional markets account for most of the demand for chips. Conventional Chip Uses Computing aka Data Processing Electronics is one of the largest segments and comprises nearly one-third of all semiconductor usage. This segment represents the demand for chips used for personal computers, servers, and cloud storage. This is one of the fastest-growing categories, which SIA projects to grow at 21% per year6 (Chart 9). While this expected rate of growth is impressive, it is set to slow in the coming year as demand for personal computers is starting to decelerate (Chart 10). On the upside, annual growth in servers continues to rebound, with the year-on-year increase in global server shipments close to 15% (Chart 11).

Chart 9

Chart 10Demand For PCs Is Coming Off High Levels...

Demand For PCs Is Coming Off High Levels...

Demand For PCs Is Coming Off High Levels...

Chart 11While Demand For Servers Is On The Rise

While Demand For Servers Is On The Rise

While Demand For Servers Is On The Rise

Communications Electronics is the second largest chips market. These chips power wireless communications and are getting a boost from the rollout of 5G networks. This segment also benefits from the recently passed US Infrastructure Bill, which has funds earmarked for wireless communication. However, communications chips expect tepid growth of just 1% as the speed of the 5G rollout is disappointing, and many consumers are unwilling to upgrade their phones: Demand for smartphones has only recently turned up (Chart 12). Consumer Electronics is a segment that is expected to contract in the coming year as spending on consumer goods has already exceeded the pre-pandemic trend and has turned down (Chart 13). Chart 12Demand For Smart Phones Has Started To Pick Up

Demand For Smart Phones Has Started To Pick Up

Demand For Smart Phones Has Started To Pick Up

Chart 13Demand For Consumer Goods Is Waning

Demand For Consumer Goods Is Waning

Demand For Consumer Goods Is Waning

Automotive segment – Modern vehicles are increasingly reliant on chips for advanced brakes, steering systems, fuel efficiency, safety, and other features. So missing chips can easily stall production. While the segment is only 12% of the total, it has gotten the industry’s most negative rap. Auto manufacturers, for example, could experience a $61bn loss in revenue due to supply constraints in 2021.7 However, this segment is expected to grow in the high single digits due to significant pent-up demand for autos (Chart 14). Interestingly, EV makers that deploy the most sophisticated chips were somewhat spared from shortages, which afflicted mostly mainstream chip categories. Chart 14Auto Segment Is Expected To Grow Due To Pent-Up Demand For Cars

Auto Segment Is Expected To Grow Due To Pent-Up Demand For Cars

Auto Segment Is Expected To Grow Due To Pent-Up Demand For Cars

Chips Power The Fourth Industrial Revolution Besides these well-established markets, Semis are also intrinsically a play on every single emerging technology theme. Semiconductors are at the core of disruptive technologies and the fourth industrial revolution. Artificial Intelligence (AI) and Machine Learning (ML) rely heavily on computing power delivered by sophisticated chips to process massive datasets looking for insights. As AI becomes widely deployed in a wide range of industries, demand for powerful chips is bound to soar: The size of the AI chip market is forecast to increase eight-fold from an estimated $10.14bn in 2020 to $83.25bn by 2027.8 Internet of Things (IoT), or interconnectedness of electronics, is another source of demand for chips. However, to realize the full potential of this new-generation technology, processors, modems, and other communication infrastructure must be modernized. 5G adoption is starting to accelerate as new applications are being developed such as the metaverse, immersive gaming, and virtual reality. The higher data rates and lower latencies made possible by 5G are expected to be a driver of demand for advanced semiconductors. In a 2021 KPMG survey, 53% of semiconductor companies believe 5G will become a significant driver of revenue growth in one to two years, and 19% believe it could happen in less than a year.9 Automation: Be it self-driving cars or the installation of manufacturing assembly robots, both require semiconductors. Recent labor shortages and rising wages are another reason automation is to come to the fore: US manufacturers are a case in point, lagging their European and Asian counterparts in new robot installation and in dire need of catching up. While it’s true that automation does not bring an explosive demand shock like IoT and AI do, we would not underestimate the power of that structural force (Chart 15).

Chart 15

Fundamentals Sales Growth And Profitability According to the WSTS, the worldwide semiconductor market is expected to show an outstanding growth rate of 25 percent in 2021. The largest growth contributors are Memory with 37.1 percent, followed by Analog with 29.1 percent, and Logic with 26.2 percent. By 2022, the global semiconductor market growth is expected to slow and is projected to grow by 10.1 percent. Americas are expected to grow at 12% next year.10 These forecasts align rather well with bottom-up sales growth forecasts by street analysts at 10.8% (Chart 16), which exceed projected nominal GDP growth of 7.6% and expected sales growth of the S&P 500. This industry continues to be powered by pent-up demand, backlogs of orders, and adoption of brand-new technologies. Earnings growth has recently slowed (Chart 17). Semis is an R&D intense industry, especially for the fabless US companies, which continue to plow funds into research and design of chips to retain a competitive edge. After a pandemic hiatus, the industry now is starting to ramp up its Capex outlays (Chart 18). Chart 16Sales Growth Is To Stay Robust...

Sales Growth Is To Stay Robust...

Sales Growth Is To Stay Robust...

Chart 17But Earnings Growth Is Set To Decelerate

But Earnings Growth Is Set To Decelerate

But Earnings Growth Is Set To Decelerate

Recent labor shortages and rising wages have not bypassed highly educated segments of the labor market, cutting into the profitability of these high-tech labor-intensive businesses. And of course, this industry is not immune to rising costs of raw materials and supply-chain disruptions, albeit less so than many businesses further downstream in the value chain, such as Autos. Chart 18After Pandemic Hiatus, Capex Is On The Way Back

After Pandemic Hiatus, Capex Is On The Way Back

After Pandemic Hiatus, Capex Is On The Way Back

Chart 19Margins Are Expected To Expand Further

Margins Are Expected To Expand Further

Margins Are Expected To Expand Further

Despite all the production challenges, Semis is one of the few industries that are projected to further expand its margins in the coming year (Chart 19). However, just like many other industries, their pricing power is overextended (Chart 20) and is likely to mean revert, constraining companies to pass on higher costs of design, raw materials, and manufacturing to customers. Chart 20Pricing Power Is Extreme And Is Likely To Mean Revert

Pricing Power Is Extreme And Is Likely To Mean Revert

Pricing Power Is Extreme And Is Likely To Mean Revert

Valuations Semis is an industry whose earnings are expected to grow at 8% over the next 12 months, which is on par with the S&P 500. However, Semis are trading at 24x forward earnings, or with a 14% premium to the S&P 500 (21.3x) (Chart 21). Further, earnings growth is decelerating. It is hard to justify this valuation premium, especially in the context of imminent rate hikes. Of course, valuations may reflect the fact that demand for chips is still extremely strong both from conventional markets and nascent technology applications. The industry is also highly profitable, and margins are expected to expand in 2022. To break the tie, we will turn to the analysis of the macroeconomic backdrop in 2022 and whether it is going to be favorable for the industry. Chart 21Valuations Are Overextended

Valuations Are Overextended

Valuations Are Overextended

Macroeconomic Backdrop Semiconductor stocks as a group aren’t just highly sensitive to economic growth, they’re nearly immediately so, sniffing out economic rebounds and downturns before they become evident in broad market data. As a result, investors have to remain on their guard and be very nimble. Subtle shifts in the economic outlook can have a big impact on relative performance. At the moment, several macro trends constitute a headwind for the outperformance of the industry: Global bond yields are expected to rise due to the concerted action of Central Banks, dampening demand for chips, dragging down the sales growth of the Semis, and diminishing future cash flows (Chart 22). The US ISM Manufacturing index has peaked, while the ISM New Orders index is in a downward trend, suggesting an emerging decline in production and diminished demand for chips (Chart 23) Chinese growth is slowing and BCA Research’s house view is that a rebound is not likely until later in 2022. Chart 22Rising Bond Yields Will Be A Headwind For Semis

Rising Bond Yields Will Be A Headwind For Semis

Rising Bond Yields Will Be A Headwind For Semis

Chart 23Decline In The ISM New Orders Signal Less Demand For Semis

Decline In The ISM New Orders Signal Less Demand For Semis

Decline In The ISM New Orders Signal Less Demand For Semis

Therefore, we conclude that, while economic growth is to remain strong in 2022, and will provide a tailwind for many cyclical sectors, semiconductor growth is set to slow, and valuations are likely to compress as a reaction to rising bond yields. The macroeconomic outlook for the industry is contingent upon the direction of the interest rates and is sensitive to economic growth disappointments. In short, the macroeconomic backdrop is unfavorable. Investment Implications The semiconductor industry is positioned at the very core of the global economy. It is one of the key growth engines of the US economy, and one of its top exports. This is an industry highly geared to economic growth and exposed to a variety of emerging technology themes, such as 5G, self-driving vehicles, and the metaverse among many others. It is R&D and Capex intensive and sophisticated. We believe in Semis as a long-term structural theme. Tactically, we are concerned that in 2022 this industry may face macroeconomic headwinds being highly sensitive to slowing growth and rising rates, which are detrimental to the performance of this growth-oriented and cyclical sector. From a fundamental standpoint, sales and earnings growth are slowing and are on par with that of a broad market, yet Semis are trading with a premium to the S&P 500. Tactically, we are neutral on a sector, but structurally we are bullish. We recommend investors with longer holding horizons explore the following ETFs (Table 2), that are designed to capture Semis as an investment theme. Table 2Semis ETFs

Semiconductors: Aren't They Fab?!

Semiconductors: Aren't They Fab?!

Bottom Line In this deep-dive report on the Semiconductor industry, we review the supply chain, the key labor division between fabless chip designers and chips manufacturers, and the issues underpinning a recent push towards onshoring. We explore target markets and look at sales growth rates and fundamentals. We conclude that we are bullish on the industry on a structural basis but are more ambivalent about its prospects over the next 3-6 months downgrading our portfolio overweight to an equal-weight. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Footnotes 1 Semiconductor Industry Association (SIA) "2021 Industry Facts" May 19, 2021 2 Semiconductor Industry Association (SIA) "2021 STATE OF THE U.S. SEMICONDUCTOR INDUSTRY" 3 Global X "Putting the Chip Shortage into the Context of Long-Term Trends" May 24, 2021 4 Ibid 5 Ibid 6 Ibid 7 Bloomberg, “Chip Shortage: Taiwan, South Korea’s Manufacturing Lead Worries U.S., China” March 3, 2021 8 Ibid 9 Ibid 10 World Semiconductor Trade Statistics "Semiconductor Market Forecast Fall 2021" November 30, 2021 Recommended Allocation

Dear Client, Thank you for your continued readership and support this year. This is the last European Investment Strategy report for 2021. In this piece, we review ten charts covering important aspects of the European economy and capital markets. We will resume our regular publishing schedule on January 10th, 2022. The European Investment Strategy team wishes you and your loved ones a wonderful holiday season, and a healthy, happy, and prosperous new year. Best regards, Mathieu Savary Highlights European growth continues to face headwinds as it enters 2022. The ECB will be slow to remove more accommodation than what is implied by the end of the PEPP. Value stocks and Italian equities will enjoy a modest tailwind from rising Bund yields. The lower quality of European stocks creates a long-term headwind versus US benchmarks. The outperformance of European cyclicals relative to defensives will resume and financials will have greater upside. The relative performance of small-cap stocks will soon stabilize, but a weak euro will create a near-term risk. President Emmanuel Macron’s real contender is the center-right candidate Valerie Pécresse, not populists. Feature Chart 1: Wave Dynamics The current wave of COVID-19 infections continues to surge in Europe. As Chart 1 highlights, Austria and the Netherlands just witnessed intense waves that eclipsed those experienced earlier this year. However, these waves are already ebbing because of the containment measures implemented in recent weeks. In these two severely hit nations, hospitalization rates also increased significantly; however, they did not reach the degree experienced in France or the UK in the first half of 2021 (Chart 1, right panel). Chart 1Wave Dynamics

Wave Dynamics I

Wave Dynamics I

Chart 1Wave Dynamics

Wave Dynamics II

Wave Dynamics II

Europe will experience another test in the coming weeks as the highly contagious Omicron variant becomes the dominant COVID-19 strain. However, data from South Africa continues to suggest that this mutation is much less pathogenic than previous variants and will not place as much strain on the healthcare system as potential case counts would indicate. Nonetheless, it is too early to make this prognosis with great confidence. Importantly, even if a small proportion of infected people is hospitalized, a large enough a pool of infections could cause a rupture in the healthcare system. As a result, politicians will likely remain cautious until a larger share of the population receives its booster dose. Hence, Omicron still represents a near-term risk to economic activity, albeit one that will prove ephemeral. Chart 2: The Economy Is Not Out Of The Woods Yet European growth remains highly dependent on the fluctuations of the global economy because exports and capex account for a large share of the continent’s output. Consequently, global economic trends remain paramount when considering the European economic outlook. In the near-term, Europe continues to face headwinds beyond the uncertainty caused by the potential effects of the Omicron variant. Global economic activity, for instance, is likely to face some further near-term headwinds caused by the supply shock typified by elevated commodity prices and bottlenecks (Chart 2). Not only does this shock limit the ability of producers to procure important inputs, but it also increases the costs of production. Historically, this combination results in downward pressure on global manufacturing activity. Chart 2The Economy Is Not Out Of The Woods Yet

The Economy Is Not Out Of The Woods Yet I

The Economy Is Not Out Of The Woods Yet I

Chart 2The Economy Is Not Out Of The Woods Yet

The Economy Is Not Out Of The Woods Yet II

The Economy Is Not Out Of The Woods Yet II

The second problem remains the deceleration in the Chinese economy. Declining credit growth in China results in slower European exports, which also hurts the region’s PMI. The recent Central Economic Work Conference suggests that China is ready to inject more stimulus in its economy, which will help Europe. However, the beginning of 2022 will still witness the lagged impact of previous tightening in credit conditions on European economic indicators. Moreover, BCA’s China Investment Strategy team expects the stimulus to be modest at first and only grow in intensity later. It is unlikely to be as credit-heavy as in the past, which also means it will be less beneficial to Europe. Chart 3: A Careful ECB Last week, the European Central Bank aggressively upgraded its inflation forecast for 2022 and announced the end of the PEPP for March, however, it will increase temporarily the APP program to EUR40bn. Moreover, President Christine Lagarde remains steadfast that the Governing Council will not raise rates in 2022. Our Central Bank Monitor points to the need for tighter policy, yet the ECB continues to adopt a cautious tone, even if the Eurozone HICP inflation has reached 4%—the highest reading in thirteen years. First, the ECB still runs the risk of dislocation in the periphery, where Italian and Spanish spreads may easily explode if monetary accommodation is removed too quickly. Second, European inflationary pressures remain significantly narrower than they are in the US (Chart 3, left panel). Our Eurozone trimmed-mean CPI continues to linger well below core CPI readings, while in the US both measures track each other closely. Third, the decline in energy prices and the ebbing transportation bottlenecks mean that odds are growing that sequential inflation will soon experience an interim peak (Chart 3, right panel). Chart 3A Careful ECB

A Careful ECB I

A Careful ECB I

Chart 3A Careful ECB

A Careful ECB II

A Careful ECB II

This view of the ECB implies that German yields will not rise as much as US yields next year, which BCA’s US Bond Strategy team expects to reach 2.25% by the end of 2022. Moreover, the more tepid pace of the removal of accommodation and the implicit targeting of peripheral bond markets also warrant an overweight position in Italian bonds. Spreads will be volatile, but any move upward will be self-limiting because of their role in the ECB’s reaction function. As a result, investors should continue to pocket the additional income over German paper. Chart 4: A Murky Outlook For The Euro The market continues to test EUR/USD. Any breakdown below 1.1175 is likely to prompt a pronounced down leg toward 1.07-1.08, near the pandemic lows. The euro suffers from three handicaps. First, Europe’s economic links with China are greater than those of the US with China. Consequently, the Chinese economic deceleration hurts European rates of returns more than it hurts those in the US. Second, the acceleration of US inflation is inviting investors to reprice the path of the Fed’s policy rate, which accentuates the upside pressure on the dollar. Finally, the energy crisis is ramping up anew following Germany’s suspension of the approval of the Nord Stream 2 pipeline and the buildup of Russian troops on Ukraine’s borders. Surging European natural gas prices act as a powerful headwind for EUR/USD because they accentuate stagflation risks in the Eurozone (Chart 4, left panel). While these create downside pressures on the euro, the picture is more complex. Our Intermediate-Term Timing Model shows that EUR/USD is one-sigma oversold (Chart 4, right panel). Over the past 20 years, it was more depressed only in 2010 and in early 2015. Such a reading indicates that most of the bad news is already embedded in EUR/USD and that sentiment has become massively negative. Thus, we are not chasing the euro lower, even though we will respect our stop-loss at 1.1175 if it were triggered. Instead, we will look to buy the euro at lower levels in the first quarter of 2021. Chart 4A Murky Outlook For The Euro

A Murky Outlook For The Euro I

A Murky Outlook For The Euro I

Chart 4A Murky Outlook For The Euro

A Murky Outlook For The Euro II

A Murky Outlook For The Euro II

Chart 5: German Yields Are Key To Value Stocks And Italian Equities The performance of European value stocks relative to that of growth stocks continues to exhibit a close relationship with the evolution of German Bund yields (Chart 5, left panel). Value stocks are less sensitive than growth stocks to higher yields because they derive a smaller proportion of their intrinsic value from long-term deferred cash flows; which suffer more from rising discount factors than near-term cash flows. Moreover, value stocks overweight financials, whose profitability increases when yields rise. The same relationship exists between the performance of Italian equities relative to the Eurozone benchmark (Chart 5, right panel). This correlation holds because of Italy’s significant value bias and its large exposure to financials. Chart 5German Yields Are Key To Value Stocks And Italian Equities

German Yields Are Key To Value Stocks And Italian Equities I

German Yields Are Key To Value Stocks And Italian Equities I

Chart 5German Yields Are Key To Value Stocks And Italian Equities

German Yields Are Key To Value Stocks And Italian Equities II

German Yields Are Key To Value Stocks And Italian Equities II

Based on these observations, BCA’s view that German Bund yields will rise toward 0.25% is consistent with a modest outperformance of value and Italian equities in 2022. For a more robust outperformance by value and Italian stocks, the Chinese economy will have to re-accelerate clearly and the dollar will have to fall significantly. However, these two outcomes could take more time to materialize than our bond view. Chart 6: Europe’s Quality Deficit The gyrations in the performance of European equities relative to US stocks continue to be influenced by China’s economic fluctuations. The deterioration in various measures of China’s credit impulse remains consistent with further near-term underperformance of European equities (Chart 6, left panel). Moreover, if Omicron has a significant impact on consumer behavior (via personal choices or government measures), it will once again hurt spending on services and boost the appeal of growth stocks, which Europe underrepresents. These headwinds will not be long lasting. Europe has an opportunity to outperform next year if global yields rise. However, European equity markets continue to suffer from a potent long-term disadvantage relative to those of the US. American benchmarks are composed of higher quality stocks than European ones. As a result of greater market concentration, more innovative applications of research, and the development of greater moats, US stocks generate wider profits margins than European companies and have a higher utilization of their asset base. Consequently, US shares sport significantly higher RoEs and earnings growth than European large-cap names (Chart 6, right panel). Historically, the quality factor has been one of the top performers and is an important contributor to the current strength of growth equities. Thus, even if Europe’s day in the sun arrives before the middle of 2022, it will again be a temporary phenomenon. Chart 6Europe’s Quality Deficit

Europe's Quality Deficit I

Europe's Quality Deficit I

Chart 6Europe’s Quality Deficit

Europe's Quality Deficit II

Europe's Quality Deficit II

Chart 7: Will the Cyclicals Outperformance Resume? For most of 2021, European cyclicals equities have not performed as well against defensive stocks as many investors hoped. In fact, the relative performance of cyclicals is broadly flat since March. Going forward, cyclicals will resume their uptrend against defensive equities and even break out of their range of the past twenty years. From a technical perspective, cyclicals have expunged many of their excesses. By the spring, European cyclicals had become prohibitively expensive compared to their defensive counterparts (Chart 7, left panel). However, their overvaluation has now passed and medium-term momentum measures are not overbought anymore, which creates a much better entry point for cyclical equities. From a fundamental perspective, cyclicals will also enjoy rising yields after being hamstrung by Treasury yields that have moved sideways for more than nine months (Chart 7, right panel). Moreover, the eventual stabilization of the Chinese economy will create an additional tailwind for these stocks. Chart 7Will The Cyclicals Outperformance Resume?

Will the Cyclicals Outperformance Resume? I

Will the Cyclicals Outperformance Resume? I

Chart 7Will The Cyclicals Outperformance Resume?

Will the Cyclicals Outperformance Resume? II

Will the Cyclicals Outperformance Resume? II

The biggest risk to cyclical stocks lies in inflation expectations. Ten-year CPI swaps have stopped increasing despite rising inflation. As the yield curve flattens and long-term segments of the OIS curve invert, markets register their fears that the Fed might tighten too much over the next two years. In other words, markets continue to agonize over the effect of a very low perceived terminal rate. These worries may cause the CPI swaps to decline significantly as the Fed hikes rates next year, creating a headwind for cyclicals. Chart 8: Favor Financials Financials in general and banks in particular have outperformed the European benchmark this year. This trend will persist in 2020. More than the positive impact of higher yields on the profitability of financials justifies this view. One of the key drivers supporting our optimism toward this sector is the continued improvement in the balance-sheet health of the European banking sector (Chart 8, left panel). Capital adequacy ratios remain in an uptrend and NPLs continue to be well-behaved. Meanwhile, both the governments’ liquidity support during the pandemic and the nonfinancial sector’s cash buildup over the past 18 months limit the risk that a brisk rise in insolvencies would threaten the viability of the banking system. European bank lending is also likely to remain superior to that of the post-GFC years. Consumer confidence is still sturdy, despite the recent increase in COVID cases and the tax hike created by rapidly climbing energy prices (Chart 8, right panel). Companies also benefit from an environment of low real rates and limited fiscal austerity. Unsurprisingly, capex intentions are elevated, which should support credit demand from businesses going forward. Chart 8Favor Financials

Favor Financials I

Favor Financials I

Chart 8Favor Financials

Favor Financials II

Favor Financials II

These factors imply that the current large discount embedded in European financials’ valuations remains excessive (even if a smaller discount is still warranted). As long as peripheral spreads do not blow out durably, financials will have scope to outperform further. Banks should also beat insurance companies. Chart 9: Small-Caps Are Nearly There Despite a sideways move followed by a 4% dip, the performance of European small-cap stocks remains in a pronounced uptrend relative to large-cap equities. The recent bout of underperformance is likely to end soon, unless a recession is around the corner. Small-cap stocks are becoming oversold (Chart 9, left panel) and will benefit from their pronounced procyclicality, especially if the recent improvement in global economic surprises continues next year. Moreover, above-trend European growth as well as an ECB that will maintain accommodative monetary conditions will combine to prevent a significant widening in European high-yield spreads, particularly once natural gas prices are turned down after the winter. This process will also help small-cap equities. The biggest risk for the European small-caps’ relative performance is the currency market. The relative performance of small-cap names is still closely correlated to the euro (Chart 9, right panel). As a result, if EUR/USD were to falter in the coming weeks, the underperformance of small-cap stocks could deepen. At the very least, small-cap stocks would languish before resuming their uptrend later in the year. Chart 9Small-Caps Are Nearly There

Small-Caps Are Nearly There I

Small-Caps Are Nearly There I

Chart 9Small-Caps Are Nearly There

Small-Caps Are Nearly There II

Small-Caps Are Nearly There II

Chart 10: A Risk to Macron’s Second Term The emergence of the new populist candidate Éric Zemmour has galvanized the media in recent weeks. However, he is very unlikely to pose a credible threat to French President Emmanuel Macron, unlike center-right candidate Valerie Pécresse, who just won the Les Républicains (LR) primary. In a Special Report published conjointly with our geopolitical strategists last summer, we identified the emergence of a single candidate able to unite the center-right as one of the biggest risks to Macron. As Chart 10 shows, Pécresse has made a comeback in the polls and is now expected to face Macron in the second round. According to an Elabe poll conducted after her victory in the primary, if the second round of the elections were held now, she would beat Macron.

Chart 10

Chart 10

Will Pécresse manage to keep her momentum going until April 2022? First, she has to ensure the center-right remains united behind her. Up until the primaries, the center-right was divided. While she won the primary by a wide margin, her main opponent Éric Ciotti won the first round (25.6%), and Michel Barnier as well as Xavier Bertrand came close behind, with 23.9% and 22.7% respectively. Second, Pécresse must work hard to prevent voters from succumbing to the siren songs of Zemmour and Marine Le Pen, or to lean toward former Prime Minister Phillippe Edouard, a declared supporter of Macron. Investors should ignore Le Pen and Eric Zemmour. The real threat to Macron lies in Valerie Pécresse’s ability to keep the center-right united under her banner. Considering that the center-left does not represent an option and that the far-right is entangled in a tug-of-war, there is a high probability that Pécresse will reach the second round. Footnotes Tactical Recommendations

Europe In Charts

Europe In Charts

Cyclical Recommendations

Europe In Charts

Europe In Charts

Structural Recommendations

Europe In Charts

Europe In Charts

Closed Trades Currency Performance Fixed Income Performance Equity Performance

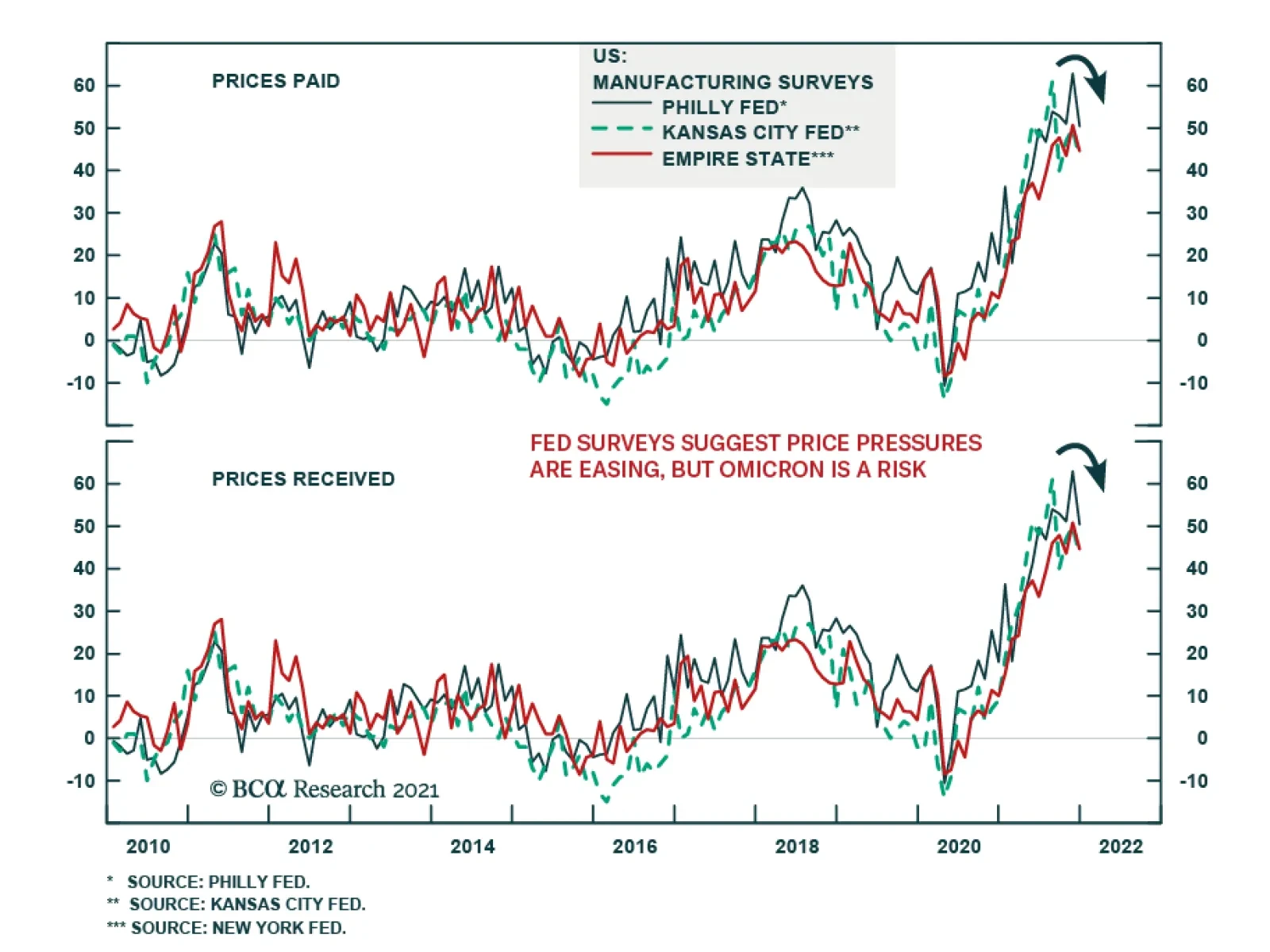

The December Philly Fed Manufacturing Business Outlook survey provides some preliminary suggestions that the supply-side crunch is moderating. Both the current conditions and forward-looking prices paid and prices received series declined (albeit to still…

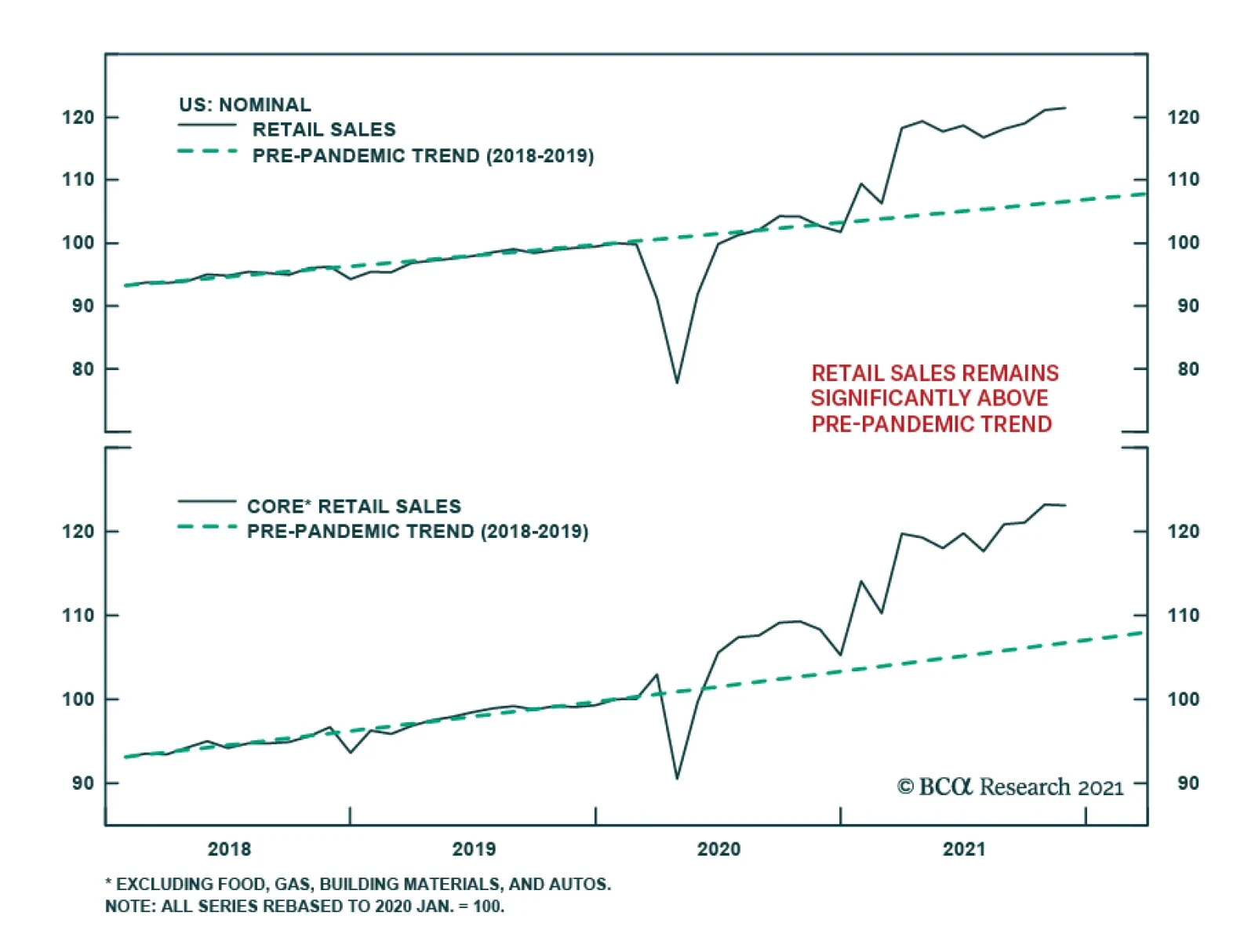

The US retail sales report surprised to the downside in November. Overall retail sales growth decelerated sharply from 1.8% m/m to 0.3% and fell below the anticipated 0.8%. Similarly, retail sales growth excluding autos and gas slowed to 0.2% m/m from 1.6%.…

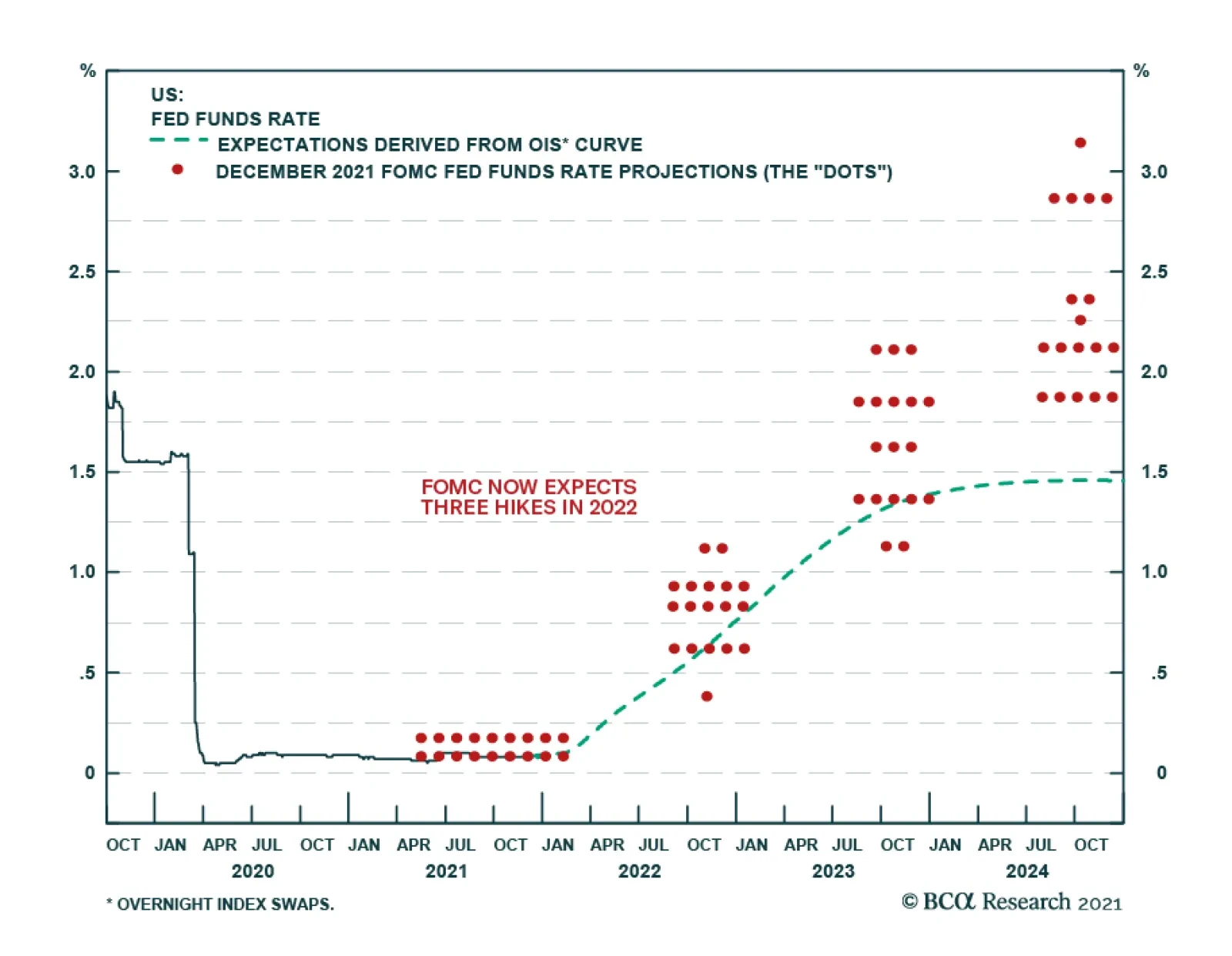

The FOMC delivered a hawkish message on Wednesday. As expected, the central bank doubled the pace of asset purchase tapering, in effect bringing forward the end of the program to mid-March. Moreover, the median forecast for the fed funds rate now calls for 3…

Image

Almost two years ago, the Fed and other Central Banks (CBs) flooded the market with liquidity in an attempt to help the global economy and the financial sector to battle the pandemic. One of the unintended consequences of the said liquidity flood was a rally in the most speculative parts of the US equity market, such as small caps growth technology stocks, which are akin to lottery tickets and attract a disproportionate share of retail flows. Today, the situation could not be any different with more CBs tightening policy, the Fed discussing an accelerated taper program, and the market pricing in three rate hikes in 2022. Consequently, investors are now shedding their exposure to the most speculative assets with BTC, ARKK, and small caps growth being in an outright bear market. Given that we are still in the early innings of the tightening cycle, things are likely to get worse before they get better. Bottom Line: As global growth decelerates over the coming quarters, the Fed will be the final nail into the retail-heavy speculative assets’ coffin (see chart).

Highlights Our three strategic themes over the long run: (1) great power rivalry (2) hypo-globalization (3) populism and nationalism. The implications are inflationary over the long run. Nations that gear up for potential conflict and expand the social safety net to appease popular discontent will consume a lot of resources. Our three key views for 2022: (1) China’s reversion to autocracy (2) America’s policy insularity (3) petro-state leverage. The implications are mostly but not entirely inflationary: China will ease policy, the US will pass more stimulus, and energy supply may suffer major disruptions. Stay long gold, neutral US dollar, short renminbi, and short Taiwanese dollar. Stay tactically long global large caps and defensives. Buy aerospace/defense and cyber-security stocks. Go long Japanese and Mexican equities – both are tied to the US in an era of great power rivalry. Feature Chart 1US Resilience

US Resilience

US Resilience

Global investors have not yet found a substitute for the United States. Despite a bout of exuberance around cyclical non-US assets at the beginning of 2021, the year draws to a close with King Dollar rallying, US equities rising to 61% of global equity capitalization, and the US 30-year Treasury yield unfazed by inflation fears (Chart 1). American outperformance is only partly explained by its handling of the lingering Covid-19 pandemic. The US population was clearly less restricted by the virus (Chart 2). But more to the point, the US stimulated its economy by 25% of GDP over the course of the crisis, while the average across major countries was 13% of GDP. Americans are still more eager to go outdoors and the government has been less stringent in preventing them (Chart 3).

Chart 2

Chart 3Social Restrictions Short Of Lockdown

Social Restrictions Short Of Lockdown

Social Restrictions Short Of Lockdown

Going forward, the pandemic should decline in relevance, though it is still possible that a vaccine-resistant mutation will arise that is deadlier for younger people, causing a new round of the crisis. The rotation into assets outside the US will be cautious. Across the world, monetary and credit growth peaked and rolled over this year, after the extraordinary effusion of stimulus to offset the social lockdowns of 2020 (Chart 4). Government budget deficits started to normalize while central banks began winding down emergency lending and bond-buying. More widespread and significant policy normalization will get under way in 2022 in the face of high core inflation. Tightening will favor the US dollar, especially if global growth disappoints expectations. Chart 4Waning Monetary And Credit Stimulus

Waning Monetary And Credit Stimulus

Waning Monetary And Credit Stimulus

Chart 5Global Growth Stabilization

Global Growth Stabilization

Global Growth Stabilization

Global manufacturing activity fell off its peak, especially in China, where authorities tightened monetary, fiscal, and regulatory policy aggressively to prevent asset bubbles from blowing up (Chart 5). Now China is easing policy on the margin, which should shore up activity ahead of an important Communist Party reshuffle in fall 2022. The rest of the world’s manufacturing activity is expected to continue expanding in 2022, albeit less rapidly. This trend cuts against US outperformance but still faces a range of hurdles, beginning with China. In this context, we outline three geopolitical themes for the long run as well as three key views for the coming 12 months. Our title, “The Gathering Storm,” refers to the strategic challenge that China and Russia pose to the United States, which is attempting to form a balance-of-power coalition to contain these autocratic rivals. This is the central global geopolitical dynamic in 2022 and it is ultimately inflationary. Three Strategic Themes For The Long Run The international system will remain unstable in the coming years. Global multipolarity – or the existence of multiple, competing poles of political power – is the chief destabilizing factor. This is the first of our three strategic themes that will persist next year and beyond (Table 1). Our key views for 2022, discussed below, flow from these three strategic themes. Table 1Strategic Themes For 2022 And Beyond

2022 Key Views: The Gathering Storm

2022 Key Views: The Gathering Storm

1. Great Power Rivalry Multipolarity – or great power rivalry – can be illustrated by the falling share of US economic clout relative to the rest of the world, including but not limited to strategic rivals like China. The US’s decline is often exaggerated but the picture is clear if one looks at the combined geopolitical influence of the US and its closest allies to that of the EU, China, and Russia (Chart 6).

Chart 6

China’s rise is the most destabilizing factor because it comes with economic, military, and technological prowess that could someday rival the US for global supremacy. China’s GDP has surpassed that of the US in purchasing power terms and will do so in nominal terms in around five years (Chart 7).

Chart 7

True, China’s potential growth is slowing and Chinese financial instability will be a recurring theme. But that very fact is driving Beijing to try to convert the past 40 years of economic success into broader strategic security. Chart 8America's Global Role Persists (If Lessened)

America's Global Role Persists (If Lessened)

America's Global Role Persists (If Lessened)

Since China is capable of creating an alternative political order in Asia Pacific, and ultimately globally, the United States is reacting. It is penalizing China’s economy and seeking to refurbish alliances in pursuit of a containment policy. The American reaction to the loss of influence has been unpredictable, contradictory, and occasionally belligerent. New isolationist impulses have emerged among an angry populace in reaction to gratuitous wars abroad and de-industrialization. These impulses appeared in both the Obama and Trump administrations. The Biden administration is attempting to manage these impulses while also reinforcing America’s global role. The pandemic-era stimulus has enabled the US to maintain its massive trade deficit and aggressive defense spending. But US defense spending is declining relative to the US and global economy over time, encouraging rival nations to carve out spheres of influence in their own neighborhoods (Chart 8). Russia’s overall geopolitical power has declined but it punches above its weight in military affairs and energy markets, a fact which is vividly on display in Ukraine as we go to press. The result is to exacerbate differences in the trans-Atlantic alliance between the US and the European Union, particularly Germany. The EU’s attempt to act as an independent great power is another sign of multipolarity, as well as the UK’s decision to distance itself from the continent and strengthen the Anglo-American alliance. If the US and EU do not manage their differences over how to handle Russia, China, and Iran then the trans-Atlantic relationship will weaken and great power rivalry will become even more dangerous. 2. Hypo-Globalization The second strategic theme is hypo-globalization, in which the ancient process of globalization continues but falls short of its twenty-first century potential, given advances in technology and governance that should erode geographic and national boundaries. Hypo-globalization is the opposite of the “hyper-globalization” of the 1990s-2000s, when historic barriers to the free movement of people, goods, and capital seemed to collapse overnight. Chart 9From 'Hyper-Globalization' To Hypo-Globalization

From 'Hyper-Globalization' To Hypo-Globalization

From 'Hyper-Globalization' To Hypo-Globalization

The volume of global trade relative to industrial production peaked with the Great Recession in 2008-10 and has declined slowly but surely ever since (Chart 9). Many developed markets suffered the unwinding of private debt bubbles, while emerging economies suffered the unwinding of trade manufacturing. Periods of declining trade intensity – trade relative to global growth – suggest that nations are turning inward, distrustful of interdependency, and that the frictions and costs of trade are rising due to protectionism and mercantilism. Over the past two hundred years globalization intensified when a broad international peace was agreed (such as in 1815) and a leading imperial nation was capable of enforcing law and order on the seas (such as the British empire). Globalization fell back during times of “hegemonic instability,” when the peace settlement decayed while strategic and naval competition eroded the global trading system. Today a similar process is unfolding, with the 1945 peace decaying and the US facing the revival of Russia and China as regional empires capable of denying others access to their coastlines and strategic approaches (Chart 10).1 Chart 10Hypo-Globalization And Hegemonic Instability

Hypo-Globalization And Hegemonic Instability

Hypo-Globalization And Hegemonic Instability

Chart 11Hypo-Globalization: Temporary Trade Rebound

Hypo-Globalization: Temporary Trade Rebound

Hypo-Globalization: Temporary Trade Rebound

No doubt global trade is rebounding amid the stimulus-fueled recovery from Covid-19. But the upside for globalization will be limited by the negative geopolitical environment (Chart 11). Today governments are not behaving as if they will embark on a new era of ever-freer movement and ever-deepening international linkages. They are increasingly fearful of each other’s strategic intentions and using fiscal resources to increase economic self-sufficiency. The result is regionalization rather than globalization. Chinese and Russian attempts to revise the world order, and the US’s attempt to contain them, encourages regionalization. For example, the trade war between the US and China is morphing into a broader competition that limits cooperation to a few select areas, despite a change of administration in the United States. The further consolidation of President Xi Jinping’s strongman rule will exacerbate this dynamic of distrust and economic divorce. Emerging Asia and emerging Europe live on the fault lines of this shift from globalization to regionalism, with various risks and opportunities. Generally we are bullish EM Asia and bearish EM Europe. 3. Populism And Nationalism A third strategic theme consists of populism and nationalism, or anti-establishment political sentiment in general. These forces will flare up in various forms across the world in 2022 and beyond. Even as unemployment declines, the rise in food and fuel inflation will make it difficult for low wage earners to make ends meet. The “misery index,” which combines unemployment and inflation, spiked during the pandemic and today stands at 10.8% in the US and 11.4% in the EMU, up from 5.2% and 8.1% before the pandemic, respectively (Chart 12). Large budget deficits and trade deficits, especially in the US and UK, feed into this inflationary environment. Most of the major developed markets have elected new governments since the pandemic, with the notable exception of France and Spain. Thus they have recapitalized their political systems and allowed voters to vent some frustration. These governments now have some time to try to mitigate inflation before the next election. Hence policy continuity is not immediately in jeopardy, which reduces uncertainty for investors. By contrast, many of the emerging economies face higher inflation, weak growth, and are either coming upon elections or have undemocratic political systems. Either way the result will be a failure to address household grievances promptly. The misery index is trending upward and governments are continually forced to provide larger budget deficits to shore up growth, fanning inflation (Chart 13). Chart 12DM: Political Risk High But New Governments In Place

DM: Political Risk High But New Governments In Place

DM: Political Risk High But New Governments In Place

Chart 13EM: Political Risk High But Governments Not Recapitalized

EM: Political Risk High But Governments Not Recapitalized

EM: Political Risk High But Governments Not Recapitalized

Chart 14EM Populism/Nationalism Threatens Negative Surprises In 2022

EM Populism/Nationalism Threatens Negative Surprises In 2022

EM Populism/Nationalism Threatens Negative Surprises In 2022

Just as social and political unrest erupted after the Great Recession, notably in the so-called “Arab Spring,” so will new movements destabilize various emerging markets in the wake of Covid-19. Regime instability and failure can lead to big changes in policies, large waves of emigration, wars, and other risks that impact markets. The risks are especially high unless and until Chinese imports revive. Investors should be on the lookout for buying opportunities in emerging markets once the bad news is fully priced. National and local elections in Brazil, India, South Korea, the Philippines, and Turkey will serve as market catalysts, with bad news likely to precede good news (Chart 14). Bottom Line: These three themes – great power rivalry, hypo-globalization, and populism/nationalism – are inflationary in theory, though their impact will vary based on specific events. Multipolarity means that governments will boost industrial and defense spending to gear up for international competition. Hypo-globalization means countries will attempt to put growth on a more reliable domestic foundation rather than accept dependency on an unreliable international scene, thus constraining supplies from abroad. Populism and nationalism will lead to a range of unorthodox policies, such as belligerence abroad or extravagant social spending at home. Of course, the inflationary bias of these themes can be upset if they manifest in ways that harm growth and/or inflation expectations, which is possible. But the general drift will be an inflationary policy setting. Inflation may subside in 2022 only to reemerge as a risk later. Three Key Views For 2022 Within this broader context, our three key views for 2022 are as follows: 1. China’s Reversion To Autocracy As President Xi Jinping leads China further down the road of strongman rule and centralization, the country faces a historic confluence of internal and external risks. This was our top view in 2021 and the same dynamic continues in 2022. The difference is that in 2021 the risk was excessive policy tightening whereas this coming year the risk is insufficient policy easing. Chart 15China Eases Fiscal Policy To Secure Recovery In 2022

China Eases Fiscal Policy To Secure Recovery In 2022

China Eases Fiscal Policy To Secure Recovery In 2022

China’s economy is witnessing a secular slowdown, a deterioration in governance, property market turmoil, and a rise in protectionism abroad. The long decline in corporate debt growth points to the structural slowdown. Animal spirits will not improve in 2022 so government spending will be necessary to try to shore up overall growth. The Politburo signaled that it will ease fiscal policy at the Central Economic Work Conference in early December, a vindication of our 2021 view. Neither the combined fiscal-and-credit impulse nor overall activity, indicated by the Li Keqiang Index, have shown the slightest uptick yet (Chart 15). Typically it takes six-to-nine months for policy easing to translate to an improvement in real economic activity. The first half of the year may still bring economic disappointments. But policymakers are adjusting to avoid a crash. Policy will grow increasingly accommodative as necessary in the first half of 2022. The key political constraint is the Communist Party’s all-important political reshuffle, the twentieth national party congress, to be held in fall 2022 (usually October). While Xi may not want the economy to surge in 2022, he cannot afford to let it go bust. The experience of previous party congresses shows that there is often a policy-driven increase in bank loans and fixed investment. Current conditions are so negative as to ensure that the government will provide at least some support, for instance by taking a “moderately proactive approach” to infrastructure investment (Chart 16). Otherwise a collapse of confidence would weaken Xi’s faction and give the opposition faction a chance to shore up its position within the Communist Party. Chart 16China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

Party congresses happen every five years but the ten-year congresses, such as in 2022, are the most important for the country’s overall political leadership. The party congresses in 1992, 2002, and 2012 were instrumental in transferring power from one leader to the next, even though the transfer of power was never formalized. Back in 2017 Xi arranged to stay in power indefinitely but now he needs to clinch the deal, lest any unforeseen threat emerge from at home or abroad. Xi’s success in converting the Communist Party from “consensus rule” to his own “personal rule” will be measurable by his success in stacking the Politburo and Politburo Standing Committee with factional allies. He will also promote his faction across the Central Committee so as to shape the next generations of party leaders and leave his imprint on policy long after his departure. The government will be extremely sensitive to any hint of dissent or resistance and will move aggressively to quash it. Investors should not be surprised to see high-level sackings of public officials or private magnates and a steady stream of scandals and revelations that gain prominence in western media. The environment is also ripe for strange and unexpected incidents that reveal political differences beneath the veneer of unity in China: defections, protests, riots, terrorist acts, or foreign interference. Most incidents will be snuffed out quickly but investors should be wary of “black swans” from China in 2022. Chinese government policies will not be business friendly in 2022 aside from piecemeal fiscal easing. Everything Beijing does will be bent around securing Xi’s supremacy at all levels. Domestic politics will take precedence over economic concerns, especially over the interests of private businesses and foreign investors, as is clear when it comes to managing financial distress in the property sector. Negative regulatory surprises and arbitrary crackdowns on various industrial sectors will continue, though Beijing will do everything in its power to prevent the property bust from triggering contagion across the economic system. This will probably work, though the dam may burst after the party congress. Relations with the US and the West will remain poor, as the democracies cannot afford to endorse what they see as Xi’s power grab, the resurrection of a Maoist cult of personality, and the betrayal of past promises of cooperation and engagement. America’s midterm election politics will not be conducive to any broad thaw in US-China relations. While China will focus on domestic politics, its foreign policy actions will still prove relatively hawkish. Clashes with neighbors may be instigated by China to warn away any interference or by neighbors to try to embarrass Xi Jinping. The South and East China Seas are still ripe for territorial disputes to flare. Border conflicts with India are also possible. Taiwan remains the epicenter of global geopolitical risk. A fourth Taiwan Strait Crisis looms as China increases its military warnings to Taiwan not to attempt anything resembling independence (Chart 17A). China may use saber-rattling, economic sanctions, cyber war, disinformation, and other “gray zone” tactics to undermine the ruling party ahead of Taiwan’s midterm elections in November 2022 and presidential elections in January 2024. A full-scale invasion cannot be ruled out but is unlikely in the short run, as China still has non-military options to try to arrange a change of policy in Taiwan.

Chart 17

Chart 17BMarket-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

Market-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

Market-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

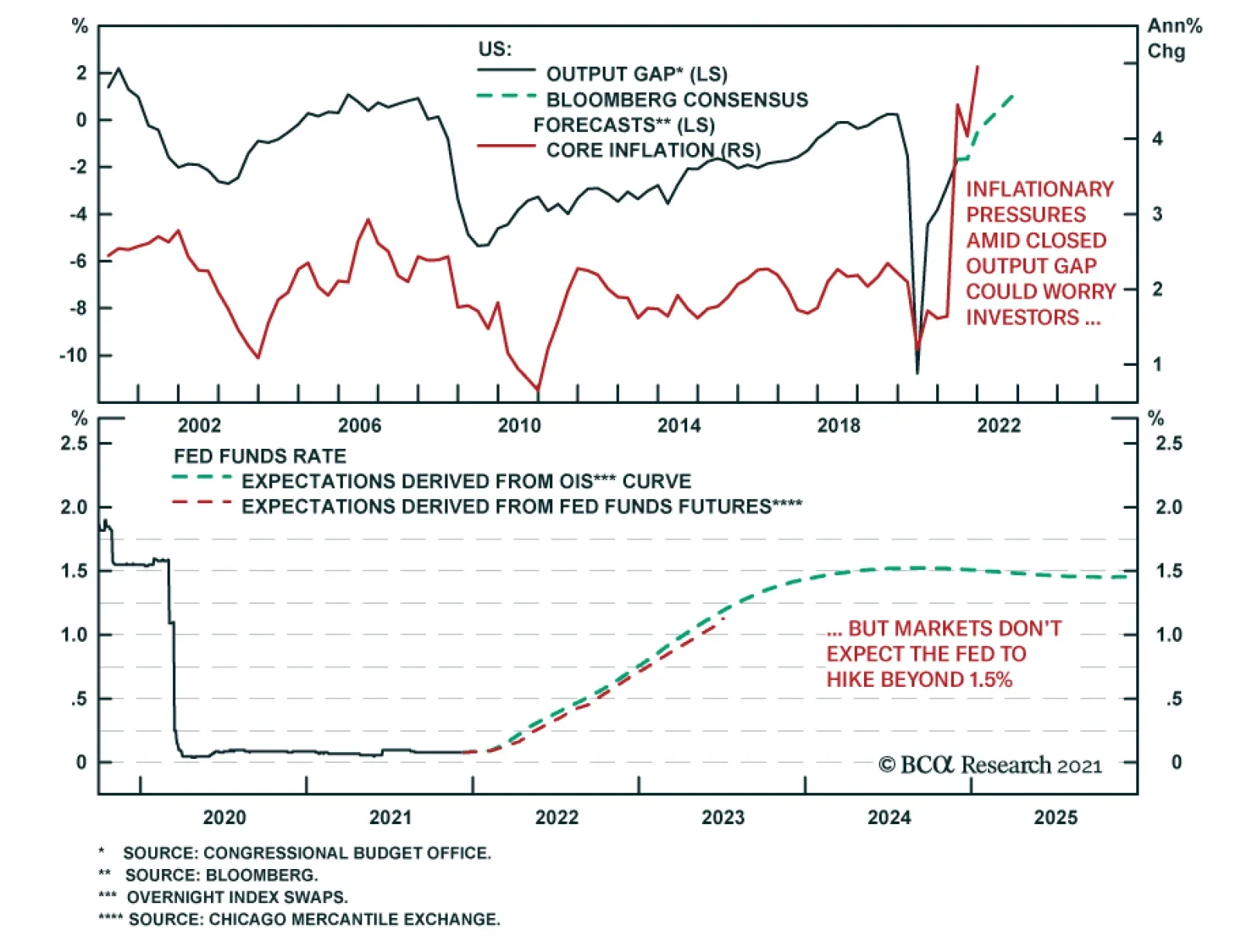

China has not yet responded to the US’s deployment of a small number of troops in Taiwan or to recent diplomatic overtures or arms sales. It could stage a major show of force against Taiwan to help consolidate power at home. China also has an interest in demonstrating to US allies and partners that their populations and economies will suffer if they side with Washington in any contingency. Given China’s historic confluence of risks, it is too soon for global investors to load up on cheap Chinese equities. Volatility will remain high. Weak animal spirits, limited policy easing, high levels of policy uncertainty, regulatory risk, ongoing trade tensions, and geopolitical risks suggest that investors should remain on the sidelines, and that a large risk premium can persist throughout 2022. Our market-based geopolitical risk indicators for both China and Taiwan are still trending upwards (Chart 17B). Global investors should capitalize on China’s policy easing indirectly by investing in commodities, cyclical equity sectors, and select emerging markets. 2. America’s Policy Insularity Our second view for 2022 centers on the United States, which will focus on domestic politics and will thus react or overreact to the many global challenges it faces. The US faces the first midterm election after the chaotic and contested 2020 presidential election. Political polarization remains at historically high levels, meaning that social unrest could flare up again and major domestic terrorist incidents cannot be ruled out. So far the Biden administration has focused on the domestic scene: mitigating the pandemic and rebooting the economy. Biden’s signature “Build Back Better” bill, $1.75 trillion investment in social programs, has passed the House of Representatives but not the Senate. The spike in inflation has shaken moderate Democratic senators who are now delaying the bill. We expect it to pass, since tax hikes were dropped, but our conviction is low (65% subjective odds), as a single defection would derail the bill. The implication would be inflationary since it would mark a sizable increase in government spending at a time when the output gap is already virtually closed. Spending would likely be much larger than the Congressional Budget Office estimate, shown in Chart 18, because the bill contains various gimmicks and hard-to-implement expiration clauses. Equity markets may not sell if the bill fails, since more fiscal stimulus would put pressure on the Federal Reserve to hike rates faster.

Chart 18

Chart 19

Whether the bill passes or fails, Biden’s legislative agenda will be frozen thereafter. He will have to resort to executive powers and foreign policy to lift his approval rating and court the median voter ahead of the midterm elections. Currently Democrats are lined up to lose the House and probably also the Senate, where a single seat would cost them their majority (Chart 19). The Senate is still in play so Biden will be averse to taking big risks. For the same reason, Biden’s foreign policy goal will be to stave off various bubbling crises. Restoring the Iranian nuclear deal was his priority but Russia has now forced its way to the top of the agenda by threatening a partial reinvasion of Ukraine. In this context Biden will not have room for maneuver with China. Congress will be hawkish on China ahead of the midterms, and Xi Jinping will be reviving autocracy, so Biden will not be able to improve relations much. Biden’s domestic policy could fuel inflation, while his domestic-focused foreign policy will embolden strategic rivals, which increases geopolitical risks. 3. Petro-State Leverage A surge in gasoline prices at the pump ahead of the election would be disastrous for a Democratic Party that is already in disarray over inflation (Chart 20). Biden has already demonstrated that he can coordinate an international release of strategic oil reserves this year. Oil and natural gas producers gain leverage when the global economy rebounds, commodity prices rise, and supply/demand balances tighten. The frequency of global conflicts, especially those involving petro-states, tend to rise and fall in line with oil prices (Chart 21). Chart 20Inflation Constrains Biden Ahead Of Midterms

Inflation Constrains Biden Ahead Of Midterms

Inflation Constrains Biden Ahead Of Midterms

Chart 21

Both Russia and Iran are vulnerable to social unrest at home and foreign strategic pressure abroad. Both have long-running conflicts with the US and West that are heating up for fundamental reasons, such as Russia’s fear of western influence in the former Soviet Union and Iran’s nuclear program. Both countries are demanding that the US make strategic concessions to atone for the Trump administration’s aggressive policies: selling lethal weapons to Ukraine and imposing “maximum pressure” sanctions on Iran. Biden is not capable of making credible long-term agreements since he could lose office as soon as 2025 and the next president could reverse whatever he agrees. But he must try to de-escalate these conflicts or else he faces energy shortages or price shocks, which would raise the odds of stagflation ahead of the election. The path of least resistance for Biden is to lift the sanctions on Iran to prevent an escalation of the secret war in the Middle East. If this unilateral concession should convince Iran to pause its nuclear activities before achieving breakout uranium enrichment capability, then Biden would reduce the odds of a military showdown erupting across the region. Opposition Republicans would accuse him of weakness but public opinion polls show that few Americans consider Iran a major threat. The problem is that this logic held throughout 2021 and yet Biden did not ease the sanctions. Given Iran’s nuclear progress and the US’s reliance on sanctions, we see a 40% chance of a military confrontation with Iran over the coming years. With regard to Ukraine, an American failure to give concessions to Russia will probably result in a partial reinvasion of Ukraine (50% subjective odds). This in turn will force the US and EU to impose sanctions on Russia, leading to a squeeze of natural gas prices in Europe and eventually price pressures in global energy markets. If Biden grants Russia’s main demands, he will avoid a larger war or energy shock but will make the US vulnerable to future blackmail. He will also demoralize Taiwan and other US partners who lack mutual defense treaties. But he may gain Russian cooperation on Iran. If Biden gives concessions to both Russia and Iran, his party will face criticism in the midterms but it will be far less vulnerable than if an energy shock occurs. This is the path of least resistance for Biden in 2022. It means that the petro-states may lose their leverage after using it, given that risk premiums would fall on Biden’s concessions. Of course, if energy shocks happen, Europe and China will suffer more than the US, which is relatively energy independent. For this reason Brussels and Beijing will try to keep diplomacy alive as long as possible. Enforcement of US sanctions on Iran may weaken, reducing Iran’s urgency to come into compliance. Germany may prevent a hardline threat of sanctions against Russia, reducing Russia’s fear of consequences. Again, petro-states have the leverage. Therefore investors should guard against geopolitically induced energy price spikes or shocks in 2022. What if other commodity producers, such as Saudi Arabia, crank up production and sink oil prices? This could happen. Yet the Saudis prefer elevated oil prices due to the host of national challenges they face in reforming their economy. If the US eases sanctions on Iran then the Saudis may make this decision. Thus downside energy price shocks are possible too. The takeaway is energy price volatility but for the most part we see the risk as lying to the upside. Investment Takeaways Traditional geopolitical risk, which focuses on war and conflict, is measurable and has slipped since 2015, although it has not broken down from the general uptrend since 2000. We expect the secular trend to be reaffirmed and for geopolitical risk to resume its rise due to the strategic themes and key views outlined above. The correlation of geopolitical risk with financial assets is debatable – namely because some geopolitical risks push up oil and commodity prices at the expense of the dollar, while others cause a safe-haven rally into the dollar (Chart 22). Global economic policy uncertainty is also measurable. It is in a secular uptrend since the 2008 financial crisis. Here the correlation with the US dollar and relative equity performance is stronger, which makes sense. This trend should also pick up going forward, which is at least not negative for the dollar and relative US equity performance (Chart 23). Chart 22Geopolitical Risk Will Rise, Market Impacts Variable

Geopolitical Risk Will Rise, Market Impacts Variable

Geopolitical Risk Will Rise, Market Impacts Variable

Chart 23Economic Policy Uncertainty Will Rise, Not Bad For US Assets

Economic Policy Uncertainty Will Rise, Not Bad For US Assets

Economic Policy Uncertainty Will Rise, Not Bad For US Assets