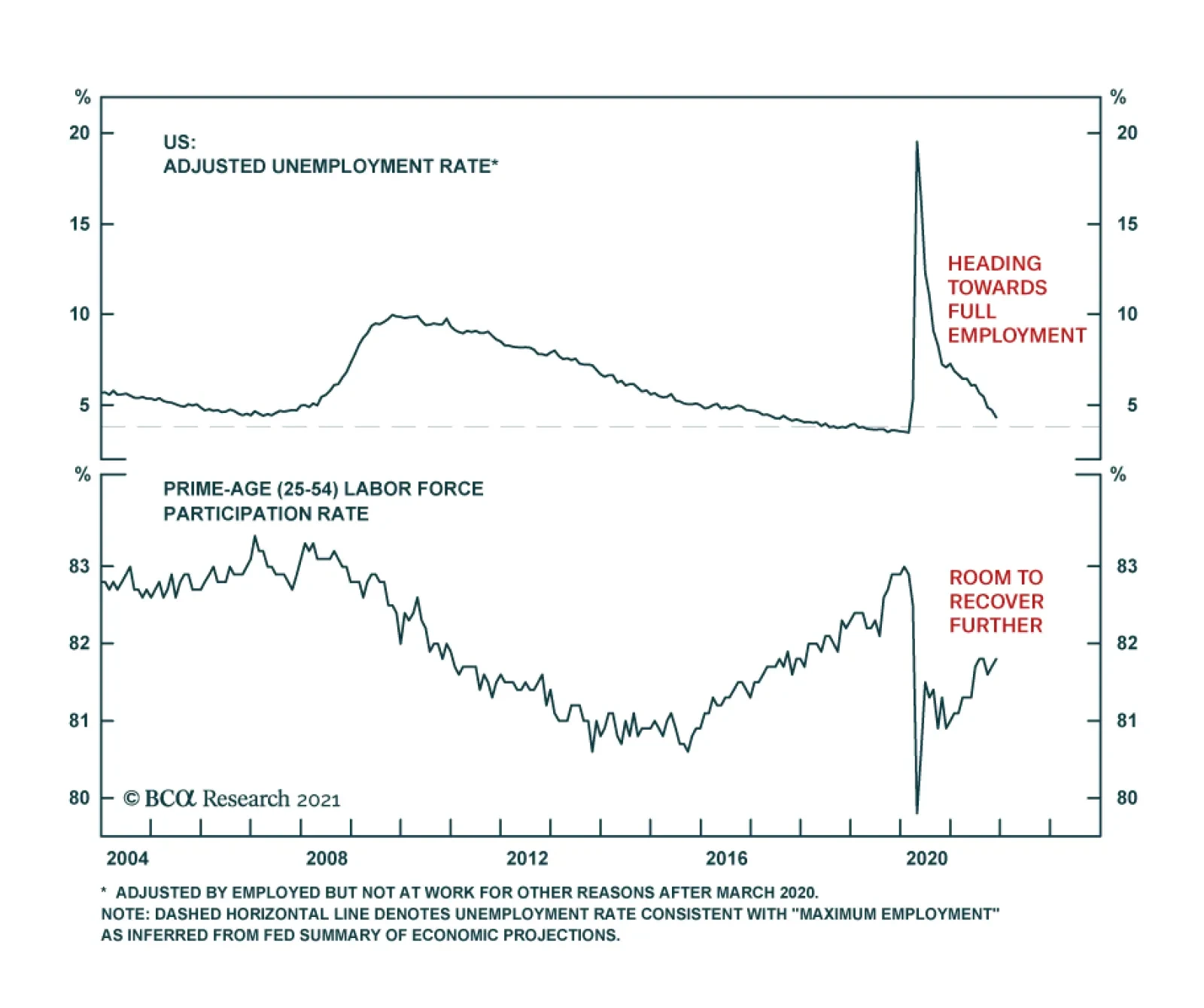

United States

Results of the establishment survey in the US employment report suggest that the labor market recovery experienced a setback in November. Nonfarm payroll gains slowed to 210 thousand following the prior month’s upwardly revised 546 thousand, and below…

BCA Research’s Global Asset Allocation service recommends that at a time of uncertainty like this, investors should dial down risk a little (with an overweight in cash not in government bonds) but maintain their long-term allocations to risk assets such as…

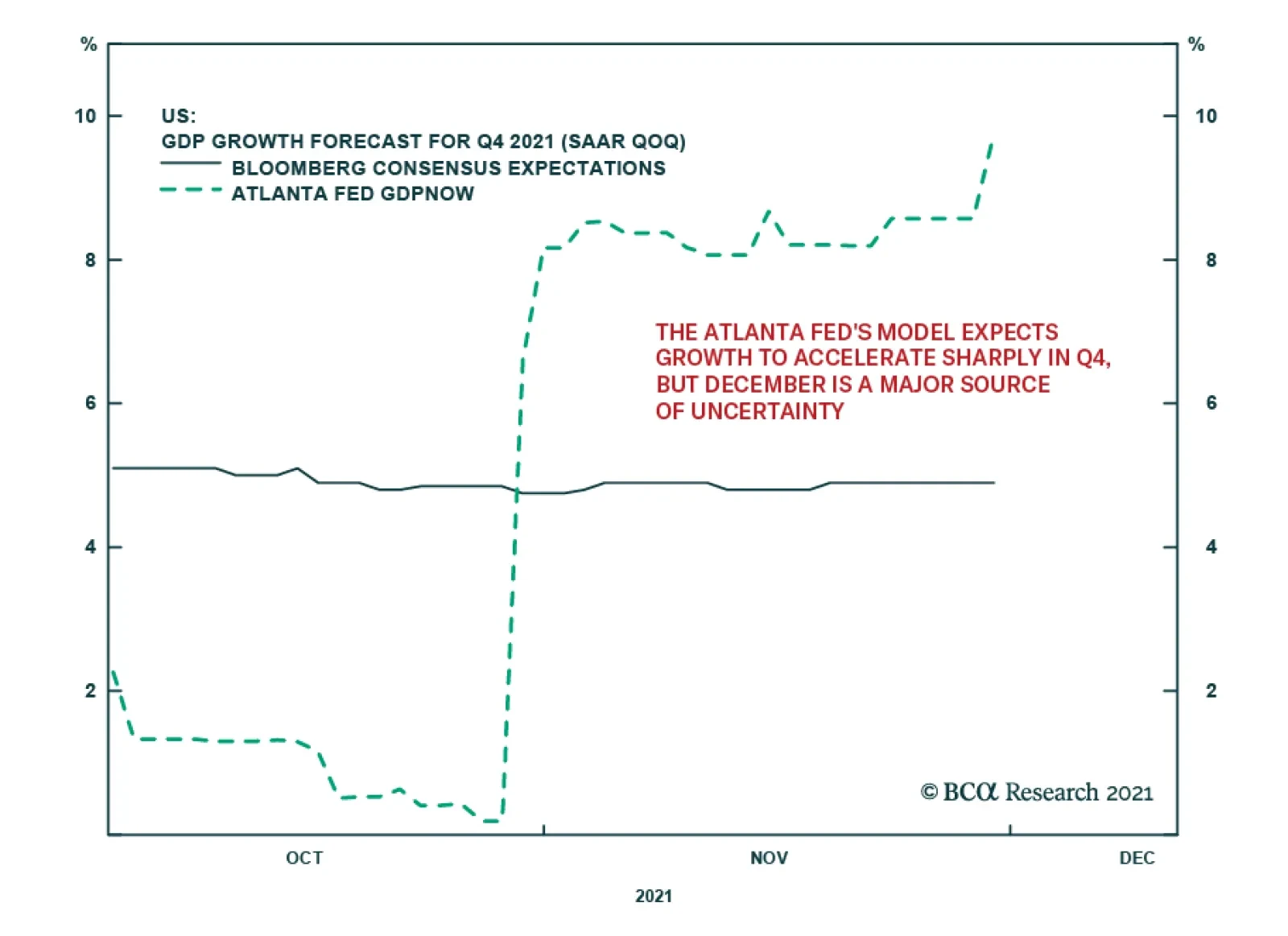

The Atlanta Fed’s GDPNow model is sending an upbeat signal about the US economy. Its estimates of Q4 GDP growth have been consistently revised up over the past month. The model’s latest output now predicts real GDP growth in the fourth quarter will be 9.7% –…

Halloween Not Over Yet

Halloween Not Over Yet

The Omicron variant is a “known unknown” we fretted about even while the economic reopening was unfolding: Being prepared for multiple viral mutations is part of learning how to live with Covid. The market did not take the news of a new variant in a stride. At this point, little is known about the strain, its virulence, immuno-evasion, and pathogenicity. Uncertainty begets volatility: The VIX shot up more than 50% last Friday on the back of the virus scare. Investors have swiftly rotated from the "Reopening" basket back to the “Covid winners,” i.e., Growth and Technology stocks. Treasuries spiked as investors rushed to safety. However, market turbulence per se is of little concern for long-term investors. To gain clarity on Omicron’s effect on the markets, we will be watching the rate of hospitalizations in South Africa and the median age and vaccination status of people with severe infections. On a policy front, we will watch the response of the “zero-tolerance countries,” such as China, Israel, and Australia, and how widespread border closures and lockdowns are. And then, to add insult to injury, the Fed announced its plans for an accelerated pace of tapering. This news has clashed with investors’ fears of the variant and new lockdowns, and a hope for a compassionate and patient Fed. Equities have pulled back, indicating that the aggressive Fed response to inflation is not priced-in and that investors fear that tightening will choke off economic growth. Despite recent developments, our base case is still intact – growth returning to trend, supply chains normalizing, and inflation shifting lower. Omicron and a more aggressive Fed are unlikely to derail the economic recovery for the following reasons. First, global lockdowns are no longer palatable to the general public. Second, even if vaccine effectiveness is compromised, unlike in 2020, there are several drugs available, which significantly improve outcomes of even the most severe cases, regardless of the variant. Third, if virulency and severity are inversely correlated, we are hoping for a mild variant. Last, the Fed still has the flexibility to alter its response if Omicron presents a severe public health threat. Bottom Line: Covid introduced permanent uncertainty in the markets and has become “a known unknown.” For downside protection, we recommend a barbell approach to portfolio construction outlined in the September 13 "Barbell Portfolio: Safety First" Strategy Report.

Fed Chair Jerome Powell’s comments during Tuesday’s congressional testimony mark a hawkish shift in Fed policy. Specifically, Powell noted that an earlier conclusion to the asset purchase program may be appropriate – making it likely that the pace of taper…

BCA Research’s US Bond Strategy service recommends that investors remain overweight spread product versus Treasuries in US bond portfolios. Spreads will tighten back down to their recent lows giving investors an opportunity to reduce exposure sometime next…

Despite the risk-off mood in financial markets, the dollar has been depreciating following news of the emergence of the omicron variant. It weakened on Friday and after a brief respite on Monday, it continued to decline on Tuesday amid fresh concerns about…

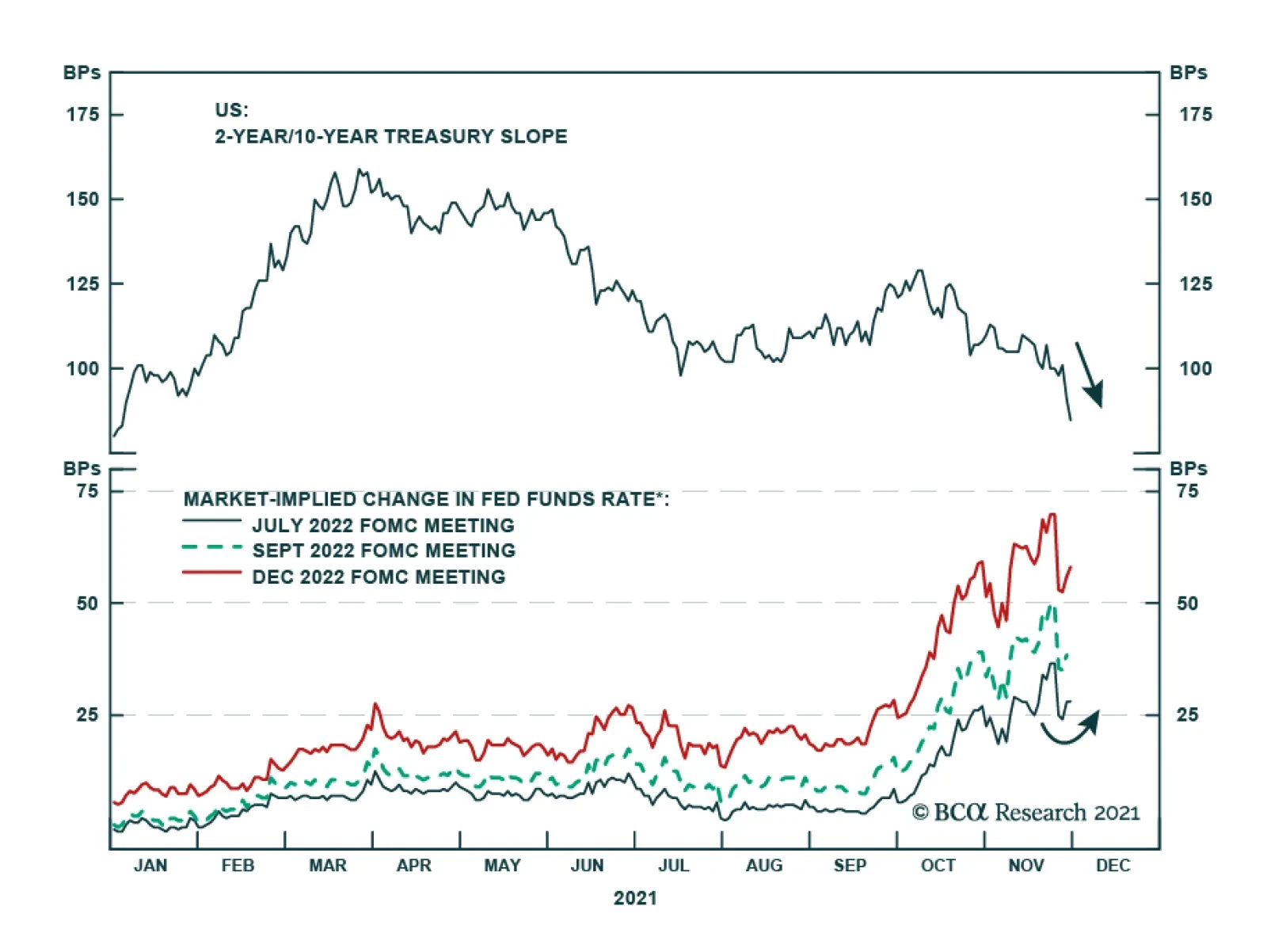

Highlights Fed: Until more is learned about the omicron variant, our base case view remains that the Fed will lift rates later than what is currently priced in the market. We think a September or December 2022 liftoff date is reasonable. Treasuries: Our main Treasury curve investment recommendations: below-benchmark portfolio duration and 2/10 curve steepeners, are not that sensitive to the timing of Fed liftoff. Both positions should be profitable whether the first rate hike occurs in June 2022 or December 2022. Corporates: Investors should remain overweight spread product versus Treasuries in US bond portfolios, maintaining a preference for high-yield corporates over investment grade. The recent bout of spread widening caused by expectations of more restrictive monetary policy and news about the omicron variant will reverse in the coming months. MBS: Agency MBS are unattractive relative to other US spread products, and current MBS valuations may understate the future pace of mortgage refi activity. Remain underweight Agency MBS within US bond portfolios. Feature Chart 1Curve Flattening Is Overdone

Curve Flattening Is Overdone

Curve Flattening Is Overdone

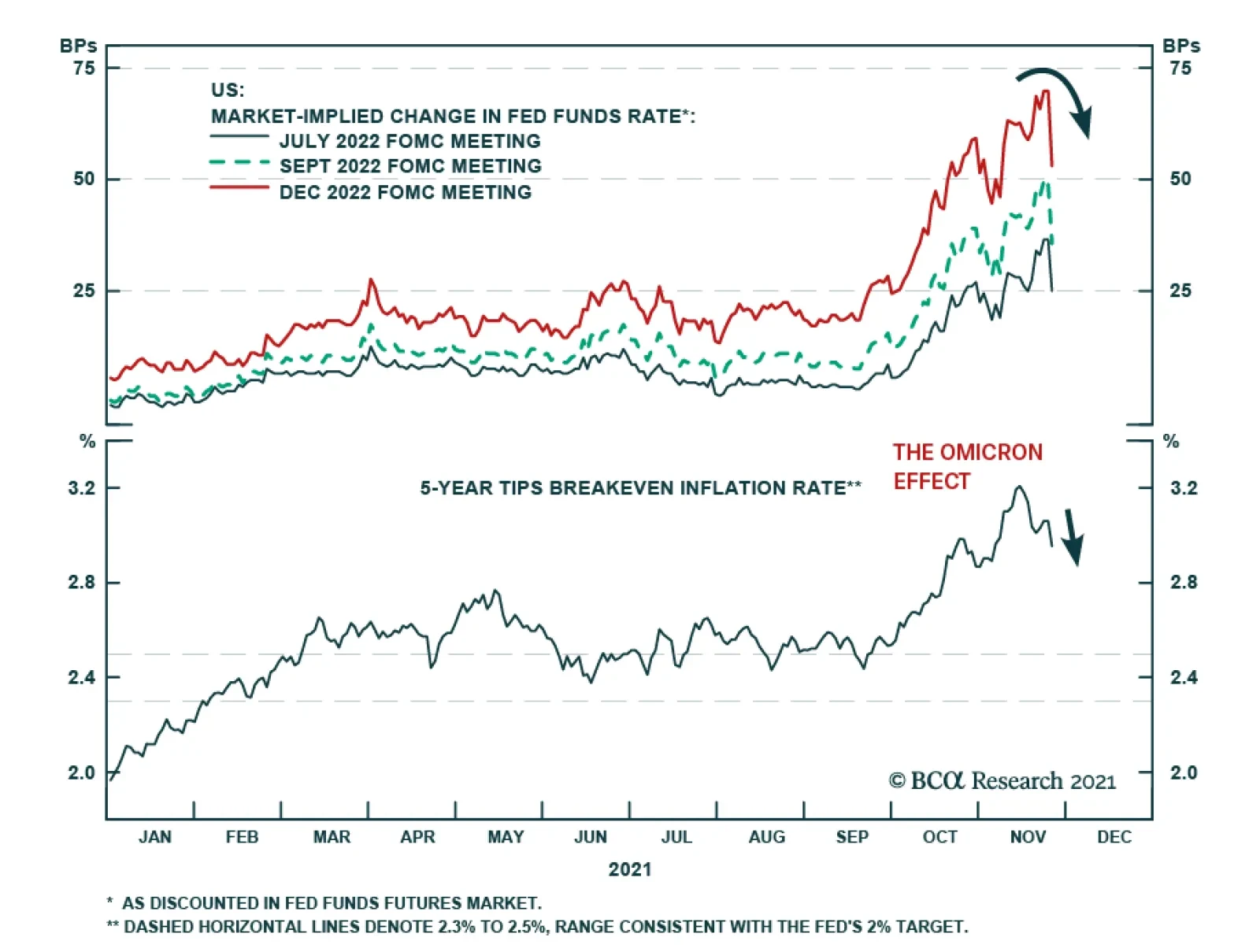

Up until Friday, the bear-flattening of the Treasury curve was a well-established trend, one that even accelerated early last week before revelations about the new omicron COVID variant sent yields sharply lower (Chart 1). Large swings in expectations about the timing of Fed liftoff have been responsible for the recent volatility in Treasury yields. Back in September, the market was priced for no rate hikes at all until 2023. Just two months later we find the fed fund futures market pricing Fed liftoff in July 2022 with 75% odds of three rate hikes before the end of next year (Chart 2A). At one point early last week the market was priced for Fed liftoff in June 2022, with 32% chance of liftoff in March 2022 (Chart 2B). Chart 2ALiftoff Expectations: H2 2022

Liftoff Expectations: H2 2022

Liftoff Expectations: H2 2022

Chart 2BLiftoff Expectations: H1 2022

Liftoff Expectations: H1 2022

Liftoff Expectations: H1 2022

Pre-Omicron Market Moves June and March liftoff dates came into play early last week because of mounting evidence that the Fed is considering accelerating the pace of its asset purchase tapering. As it stands now, the current pace of tapering gets net asset purchases to zero by June of next year. Given the Fed’s stated preference for lifting rates only after tapering is finished, the current pace means that Fed liftoff is only possible in H2 2022 or later. However, if the pace of tapering is increased it would make earlier liftoff dates possible. It was speculation about an announcement of accelerated tapering at the December FOMC meeting that caused the market to bring June and March 2022 liftoff dates into play last week. Speculation about an accelerated taper really got going after an interview by San Francisco Fed President Mary Daly. Daly is widely regarded as one of the most dovish members of the FOMC, and indeed in last week’s report we highlighted her November 16th speech that called for patience in the face of high inflation.1 But last week, Daly said in an interview that “if things continue to do what they’ve been doing, then I would completely support an accelerated pace of tapering.”2 With one of the most dovish FOMC members seemingly on board, we see a good chance that the committee will announce an accelerated taper at the next meeting. As of today, we’d put the odds of an accelerated taper announcement in December at 50%, with still one more CPI report and one more employment report that will tip the scales in one direction or the other before the Fed meets. An accelerated taper doesn’t necessarily mean that the Fed will move toward earlier rate hikes, it simply gives the committee the option to hike sooner if inflation remains stubbornly high. In fact, we’ve been expecting a later liftoff date (December 2022) on the view that inflationary pressures will wane between now and the middle of next year. We continue to think that a September 2022 or December 2022 liftoff date is the most likely outcome, as we expect that falling inflation during the next six months will allow the Fed to focus more on the employment side of its mandate. However, if inflation doesn’t fall as we expect, then the Fed may move more quickly. The Impact Of The Omicron Variant Chart 3Households Have Ample Savings

Households Have Ample Savings

Households Have Ample Savings

Friday’s revelation that a new COVID variant (the omicron variant) has been identified sent yields lower and caused the market to push out its liftoff expectations. As of today, available evidence suggests that the omicron variant will out-compete the delta variant and quickly become the world’s dominant COVID strain. There is some evidence to suggest that current vaccines will offer less protection against omicron. However, it is still unknown whether the omicron variant causes more (or less) severe illness than prior strains. Even in a severe scenario where the new strain leads to the re-imposition of lockdown measures, we are puzzled by Friday’s bond market moves. The market seems to be saying that a prolonged pandemic will be deflationary and lead to a later Fed liftoff date. We aren’t so sure that’s the case. US households continue to enjoy a large buffer of accumulated savings compared to the pre-COVID trend (Chart 3) and they have ample room to increase consumer debt (Chart 3, bottom panel). This suggests that aggregate demand will stay well supported next year, even in the face of greater pandemic concerns. The re-imposition of lockdown measures, however, will hamper the supply side of the economy and prolong the economy’s issues with supply chain bottlenecks and labor shortages. It will also prevent consumers from shifting demand away from over-heating goods sectors and towards services. All of this will only keep inflation higher for longer, a development that could actually encourage the Fed to act more quickly. Bottom Line: Until more is learned about the omicron variant, our base case view remains that the Fed will lift rates later than what is currently priced in the market. We think a September or December 2022 liftoff date is reasonable. However, if inflation refuses to fall during the next 3-6 months there is a risk that the Fed will be tempted to move earlier. The Treasury Market Implications Of Earlier Liftoff Tables 1A – 1C show expected 12-month returns for different Treasury maturities. Each table assumes that the market moves to fully price-in a specific expected path for the fed funds rate during the 12-month investment horizon.

Chart

Chart

Chart

The scenario presented in Table 1A assumes that the Fed starts to lift rates in June 2022. It then proceeds with rate increases at a pace of 100 bps per year before the fed funds rate levels-off at 2.08%, 8 bps above the lower-end of a 2.0% - 2.25% target range.3 The scenarios presented in Tables 1B and 1C use the same rate hike pace and terminal rate as in Table 1A. However, we vary the expected liftoff dates. Table 1B assumes that liftoff occurs at the September 2022 FOMC meeting and Table 1C assumes that liftoff occurs at the December 2022 FOMC meeting. The first big conclusion we draw is that expected Treasury returns are negative for most maturities in all three scenarios. This justifies sticking with below-benchmark portfolio duration. Second, expected returns are better at the short-end of the curve (2yr) than at the long-end (10yr) in all three scenarios. This justifies sticking with our recommended 2/10 yield curve steepener. Specifically, we advise clients to buy the 2-year note versus a duration-matched barbell consisting of cash and the 10-year note. Finally, the 20-year bond continues to offer greater expected returns than the 10-year and 30-year maturities. We view this as an attractive carry trade opportunity and advise clients to buy the 20-year bond versus a duration-matched barbell consisting of the 10-year note and 30-year bond. Bottom Line: Our main Treasury curve investment recommendations: below-benchmark portfolio duration and 2/10 curve steepeners, are not that sensitive to the timing of Fed liftoff. Both positions should be profitable whether the first rate hike occurs in June 2022 or December 2022. Corporate Spreads: Just A Tremor, Not The Big One Chart 4IG Spreads Troughed In September

IG Spreads Troughed In September

IG Spreads Troughed In September

Corporate bond spreads had already been widening before Friday’s news sent them even higher (Chart 4). Prior to Friday, the most likely reason for spread widening was a concern about a quicker pace of Fed tightening. As we highlighted in last week’s report, corporate balance sheet health is sublime and all signs point to default risk remaining low for some time.4 In fact, up until Friday, investment grade corporates were performing worse than high-yield as spreads widened. This suggests that the widening had more to do with perceptions of monetary accommodation than with perceptions of default risk. Then, on Friday, spreads widened sharply and high-yield underperformed investment grade. This is consistent with the market pricing-in an increase in expected default risk due to the emergence of the omicron variant. Our view is that the recent bout of spread widening will reverse in the near-term. Spreads will tighten back down to their recent lows giving investors an opportunity to reduce exposure sometime next year. We posit three possible scenarios: In the first scenario, the omicron COVID variant turns out to be less economically impactful than the recent delta strain. In this case, the recent spike in default expectations will reverse and inflation will moderate during the next six months as pandemic fears recede. In this scenario, the Fed will be able to wait until September or December 2022 – when its “maximum employment” target will be met – before lifting rates. Spreads will tighten on expectations of more accommodative monetary policy. Chart 5Pace Of Curve Flattening Will Moderate

Pace Of Curve Flattening Will Moderate

Pace Of Curve Flattening Will Moderate

In the second scenario, the omicron COVID variant turns out to be inflationary. US consumer demand is not curbed significantly, but supply chains remain under pressure and labor shortages persist. This will encourage the Fed to move more quickly, possibly lifting rates as early as June. However, even this scenario would only see the 3-year/10-year Treasury slope dip below 50 bps in March of next year (Chart 5). Our prior research has shown that excess corporate bond returns tend to be strong when the 3-year/10-year Treasury slope is above 50 bps, as this suggests a highly accommodative monetary environment.5 We would likely see another period of spread tightening between now and March, even in this worst-case scenario for corporate spreads. The final possible scenario is one where the omicron COVID variant turns out to be deflationary. Growth and inflation both slow and the Fed significantly delays tightening, possibly into 2023. Given the robust health of corporate balance sheets, this scenario would be excellent for corporate bond returns. The deflationary shock would have to be very severe, much worse than the delta wave, to push the default rate meaningfully higher. Further, a shift toward more accommodative Fed policy would lengthen the runway for strong corporate bond returns. That is, it would be some time before the 3-year/10-year slope dips below 50 bps. Bottom Line: Investors should remain overweight spread product versus Treasuries in US bond portfolios, maintaining a preference for high-yield corporates over investment grade. The recent bout of spread widening caused by expectations of more restrictive monetary policy and news about the omicron variant will reverse in the coming months. Investors will be able to reduce cyclical corporate bond exposure at more attractive levels sometime next year. Stay Negative On Agency MBS We have been recommending an underweight allocation to Agency MBS in US bond portfolios for quite some time, and that is not likely to change anytime soon. Since the March 23rd 2020 peak in credit spreads, conventional 30-year Agency MBS have outperformed a duration-matched position in Treasuries by 0.59% while Aaa and Aa-rated corporate bonds have outperformed by 16% and 15%, respectively (Chart 6). MBS performance has been particularly poor since the spring. A big reason why is that MBS spreads did not adequately compensate investors for the magnitude of mortgage refinancings. Chart 7 shows that the compensation for prepayment risk embedded in MBS spreads (the option cost) plunged in mid-2020 as interest rates were cut to zero and mortgage refis spiked. In fact, the option cost embedded in MBS spreads was the lowest it had been in several years (Chart 7, panel 2), signaling that the market was priced for a big drop in refi activity. However, that big drop in refi activity never materialized. The MBA Refinance Index has remained elevated in 2021 (Chart 7, bottom panel), despite the back-up in bond yields. Chart 6MBS Returns Have Lagged Corporates

MBS Returns Have Lagged Corporates

MBS Returns Have Lagged Corporates

Chart 7Option Cost Must Rise

Option Cost Must Rise

Option Cost Must Rise

An increase in cash-out refinancings is a big reason for the stickiness in refi activity this year. Home prices have been on a tear and households have an increasing incentive to tap the equity in their homes (Chart 8). Freddie Mac recently noted an increase in both the share of refinancings that are for “cash-out” and the aggregate dollars of equity that borrowers are extracting from their homes.6 They also noted, however, that the amount of equity extraction as a percent of property values has trended down. This suggests that this trend toward cash-out refinancings is not yet exhausted. In fact, we expect refi activity will remain elevated during the next 6-12 months, even as bond yields move modestly higher. Chart 8Households Can Tap Their Home Equity

Households Can Tap Their Home Equity

Households Can Tap Their Home Equity

Against this back-drop, our sense is that the compensation for prepayment risk embedded in MBS spreads remains too low. But, even if we assume that the MBS option cost is exactly right, it still wouldn’t make Agency MBS look attractive compared to alternative investments. The option-adjusted spread (OAS) offered by conventional 30-year Agency MBS is below the OAS offered by Aaa and Aa-rated corporate bonds (Chart 9). It is only slightly above the OAS offered by Agency CMBS and Aaa-rated consumer ABS. Chart 9OAS Differentials

OAS Differentials

OAS Differentials

Bottom Line: Agency MBS are unattractive relative to other US spread products, and current MBS valuations may understate the future pace of mortgage refi activity. Remain underweight Agency MBS within US bond portfolios. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “The Fed’s Inflation Problem”, dated November 23, 2021. 2 https://news.yahoo.com/san-francisco-fed-mary-daly-certainly-see-a-case-for-speeding-up-taper-142328227.html 3 The effective fed funds rate currently trades 8 bps above the lower-end of its target range, and we assume that this will continue to be the case. 4 Please see US Bond Strategy Weekly Report, “The Fed’s Inflation Problem”, dated November 23, 2021. 5 Please see US Bond Strategy Weekly Report, “Expected Returns In Corporate Bonds”, dated September 21, 2021. 6 http://www.freddiemac.com/research/insight/20211029_refinance_trends.page Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

The emergence of the omicron variant has prompted financial markets to dial back Fed rate hike expectations. Similarly, TIPS breakeven inflation rates fell on Friday. However, our bias is that the omicron variant poses an upside risk to inflation and…

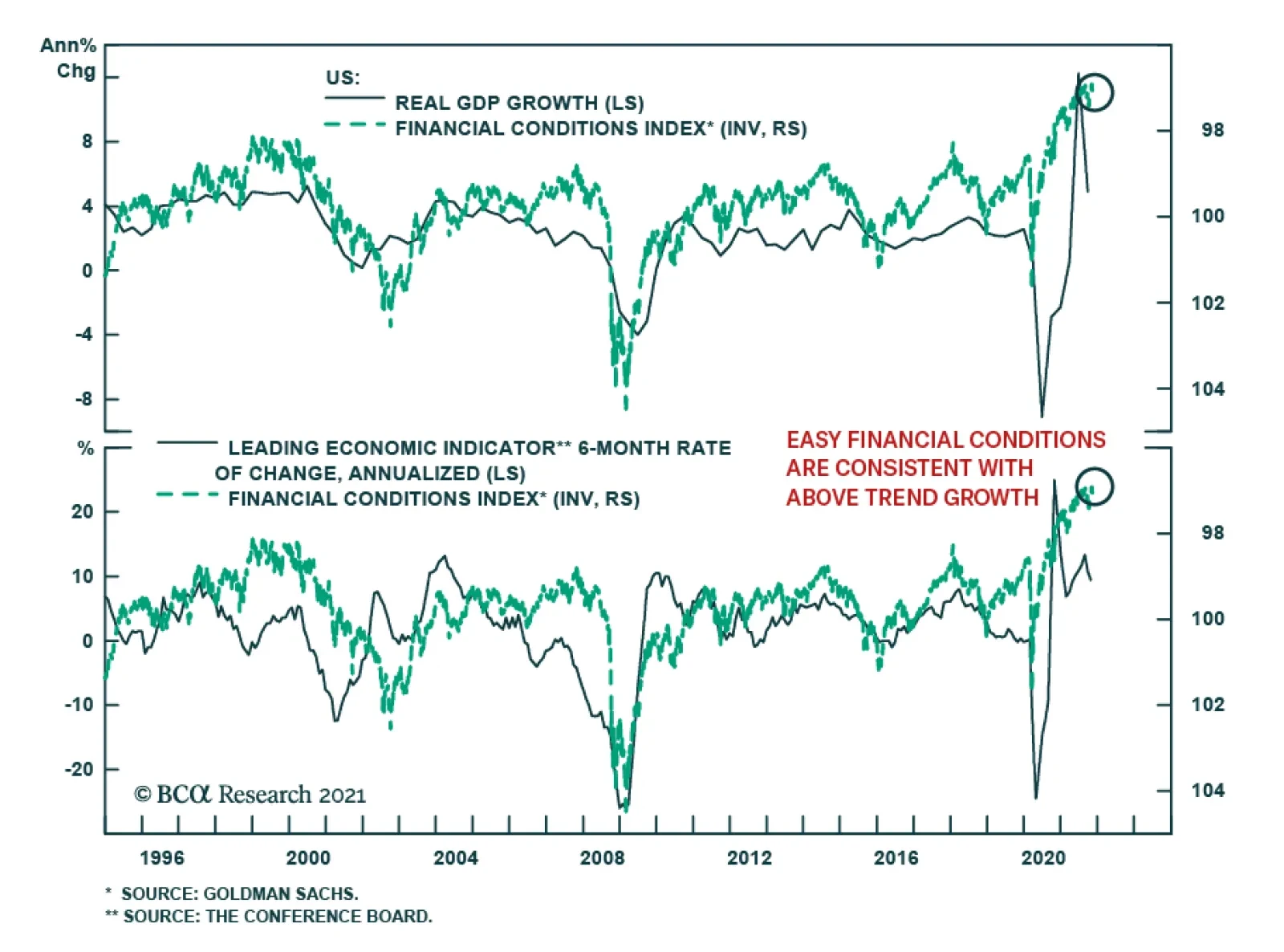

According to the Goldman Sachs Index, US financial conditions are extremely easy. The index, which takes into account the value of the dollar, interest rates, and equity prices, is near its loosest level ever. Easy financial conditions are conducive for…