United States

BCA Research’s US Investment Strategy service expects tax changes to deal the bull a glancing blow rather than a knockout punch. Based on the relative favoritism the US tax code bestows upon a particular activity, or the disparate way it treats domestic…

Highlights Investors are caught in the crosscurrents of inconsistent economic data and contradictory trends, which obscure the answer to the most important questions of the day: What will be the direction and rate of change of yields? The answer will dictate which US equity sectors and styles are to do well (Chart 1). In this report, we aim to cut through the noise and organize all the considerations and the economic data into two neat buckets: “lower for longer” vs “rates are about to rise”. “Rates Are About To Rise” vs “Lower For Longer” Arguments Fed Talk: Fed Chair Jay Powell’s Jackson Hole speech all but promised to start tapering in the coming months. However, this speech had many caveats, leaving the Fed with substantial latitude for the timing of the decision. Covid-19 Variants: The Covid-19 Delta variant is cresting, and it is unlikely that its transmission is a threat to global growth. However, Delta is the third prominent Covid-19 variant, and more vaccine-resistant variants may emerge, disrupting recovery, and derailing all plans for monetary tightening. Unemployment Rate: The unemployment rate has come down to 5.2% in August. There are also labor shortages. However, August payroll disappointed. African American unemployment remains at 8.8%. Inflation: Inflation has been running hot of late. Supply chain disruptions and upward pressure on wages perpetuate price increases. However, much of the inflation spike observed over the past several months was due to the base effect, which is rolling over. Economic Growth: The US economy is in good health: Pent-up demand for goods and services remains strong, manufacturing is booming. However, US economic data has been disappointing recently and most of the economic indicators have turned. GDP growth estimates have been downgraded. The Consumer Is Healthy But In A Bad Mood: Consumers have money to spend, and demand remains high. However, stimulus spending has peaked, which may dent consumer spending. The consumer confidence reading has slumped to a six-month low. It is apparent from this analysis that predicting the timing of tapering is close to impossible, as too much depends on the September employment report, the future rate of Covid-19 infections, potential emergence of variants, and the further patterns of inflation and supply disruption. Investment Implications: Barbell Approach To Portfolio Construction Considering the level of uncertainty in the markets, we recommend a barbell approach for portfolio construction, i.e., having an overweight in the portfolio to sectors that outperform when rates go up, such as Financials, and selected Cyclicals, and have overweights to parts of the market that benefit from “lower for longer” such as Growth, Technology, and Health Care. Feature The “easy” phase of the recovery, “the tide that lifts all boats”, supported by a torrent of ultra-easy monetary and fiscal stimulus is in the rearview mirror, leaving investors to guess the timing of Fed tapering and its implications for the different segments of the stock market. While the US equity market defies gravity, volatility is likely to make a comeback this fall thanks to near-term economic uncertainty, interest-rate uncertainty, and Covid risk (Chart 2). Chart 1Barbell Portfolio: Choose Outperformers From Each Regime

Barbell Portfolio Or Safety First

Barbell Portfolio Or Safety First

Chart 2Policy Uncertainty Is On The Rise

Policy Uncertainty Is On The Rise

Policy Uncertainty Is On The Rise

Investors are caught in the crosscurrents of inconsistent economic data and contradictory trends, which obscure the answer to the most important questions of the day: When will the Fed start tapering and where will the Treasury rates end the year? The direction and rate of change in yields will dictate which US equity sectors and styles are to do well: Growth or Value, Small or Large, Cyclicals or Defensives. The Fed has stated clearly that it has twin goals: To target average inflation and a low rate of unemployment. Yet, there is a lot of uncertainty around how long the Fed will tolerate “transitory inflation”, and what the target rate for unemployment might be. The “bad news is good news” theme is gaining prominence. Disappointing economic data points to a slowdown in recovery, which is certainly bad news. Yet, slower growth is likely to translate into a slowdown in employment gains, delaying the commencement of tapering, keeping rates rises at bay, and supporting equity prices. This sounds simple enough except for the worst-case scenario being stagflation, whereby growth slowdown is accompanied by rampant inflation, which would leave the Fed with no choice but to tighten monetary policy even if it constricts flagging growth. In this report, we aim to cut through the noise and organize all the considerations and the economic data into two neat buckets: “lower for longer” vs “rates are about to rise”. We also propose a barbell portfolio allocation for downside protection as it is not yet clear which of the possible scenarios will materialize. We are overweight Growth, Technology, Health Care, Financials, Industrials, and Consumer Services. Economic Crosscurrents Fed Speak Rates Are About To Rise The Fed has broadcasted its plans for tapering well in advance, and Fed Chair Jay Powell’s Jackson Hole speech all but promised to start tapering bond buying in the coming months. Lower For Longer Uncertain timetable: Chairman Powell’s speech had many caveats for tapering, leaving the Fed with substantial latitude for the timing of the decision. Further, Chairman Powell explicitly separated the decision to taper from the timing of the first rate hike, which is conditioned on full employment being “a long way off”. Further, tapering is tightening when it becomes a signal on the Fed’s monetary policy – the Fed went out of its way to reassure the markets that this is not the case. Covid-19 Variants Rates Are About To Rise Delta variant infections have peaked: There are early signs that the Covid-19 Delta variant is cresting (Chart 3). Around 75% of the US population has had at least one vaccine shot. Vaccinated persons are less likely to end up in a hospital even if infected. Covid-19 won’t disappear, but US consumers and businesses are learning how to live with it. Hence, worries about Covid are unlikely to keep the Fed on hold for much longer. We, too, are sanguine about the risk that Delta variant transmission is a threat to global growth. Chart 3The Covid-19 Delta Variant Is Cresting

The Covid-19 Delta Variant Is Cresting

The Covid-19 Delta Variant Is Cresting

Lower For Longer New mutations are likely: Delta is the third prominent Covid-19 variant, and more vaccine-resistant variants may emerge, disrupting recovery, and derailing all plans for monetary tightening. Also, while the spread of the Delta variant is unlikely to trigger another lockdown, consumers may curtail their activities out of fear of infection, adversely affecting demand for goods and services, and stalling recovery. There are some signs that the new wave of Delta variant infections has dented consumer spending. Delta may also be behind the disappointing August jobs report, which could be a harbinger of a slowdown in employment gains. Unemployment Rate Rates Are About To Rise Unemployment rate is falling swiftly: The unemployment rate has come down to 5.2% in August. BCA estimates that at 750,000 average monthly job gains, the pre-pandemic level of unemployment can be reached in the summer of 2022, with the first rate hike in December 2022, which is somewhat earlier than consensus – the futures market is pricing in January 2023. Labor shortages: Companies are still struggling to fill job openings: There are 10.9 million job openings but only 8.5 million job seekers (Chart 4). Shortage of labor puts upward pressure on wages and increases companies’ costs, driving up inflation. Chart 4There Are More Job Openings Then Job Seekers

There Are More Job Openings Then Job Seekers

There Are More Job Openings Then Job Seekers

Lower For Longer Disappointing jobs report: August payrolls grew only by 235,000. This low number may have resulted from the Delta hit to service industries. Next month’s report will be a decisive data point for the Fed’s tapering timing decision. Are there fundamental issues behind this number, such as Covid fears, flagging recovery, or skills mismatch between workers and jobs available? The African American unemployment rate remains elevated at 8.8%, which is still 2.8% above the pre-pandemic level (compared to the 5.2% total unemployment rate, which is only 1.7% above the 2020 pre-pandemic level), (Chart 5). The Fed is focused not only on the overall level of unemployment but also on an equitable unemployment rate across racial groups. Chart 5The African American Unemployment Rate Remains Elevated

The African American Unemployment Rate Remains Elevated

The African American Unemployment Rate Remains Elevated

Inflation Rates Are About To Rise Inflation is here to stay: Inflation has been running hot of late. The US consumer price index rose by 5.3% yoy in both June and July—a spike the Fed calls transitory. BCA agrees but believes that over the longer term, inflation will be higher than the pre-pandemic average. The Fed is coming close to admitting that inflation is becoming a problem and has been around longer than was initially expected. Supply chain disruptions are still rampant: There are significant backlogs of goods (Chart 6), and shipping costs have soared in recent months: Container freight costs have increased nearly five-fold from pre-pandemic levels. It will take time for supply chains to normalize, with most industry participants expecting the situation to improve only in 2022. Supply chain disruptions drive up inflation and, unless progress is made, lead to stagflation. Companies continue raising prices: Pricing power remains at an all-time high, with 45% of companies planning to pass surging labor and supply costs on to consumers. This leads to broadening of inflation across categories, with even trimmed mean inflation indicators significantly overshooting 2% (Chart 7). Chart 6US Manufacturers Have Work Cut Out For Them

US Manufacturers Have Work Cut Out For Them

US Manufacturers Have Work Cut Out For Them

Chart 7Trimmed Mean Inflation Is Overshooting 2%

Trimmed Mean Inflation Is Overshooting 2%

Trimmed Mean Inflation Is Overshooting 2%

Lower For Longer: Inflation is transitory: Much of the inflation spike observed over the past several months was due to the base effect, which is rolling over. The consumer categories where prices have risen fastest are services most affected by the pandemic, such as airline tickets and hotels – these prices remain at pre-pandemic levels. Other elevated prices are due to supply disruptions, such as cars and durable goods – these readings are stickier and will go away only once supply chains normalize. Further, while 45% of companies intend to raise prices, the Corporate Pricing Power Indicator has turned, which may suggest that the vicious cycle of inflation may come to a halt (Chart 8). And lastly, divergence between CPI and PPI inflation, indicates that PPI will come down in the near future (Chart 9). Chart 8Corporate Pricing Power Has Reached Its Limit

Corporate Pricing Power Has Reached Its Limit

Corporate Pricing Power Has Reached Its Limit

Chart 9Divergence Between PPI And CPI Has To Close

Divergence Between PPI And CPI Has To Close

Divergence Between PPI And CPI Has To Close

Economic Growth Rates Are About To Rise US economy is in good health: GDP growth expectations are 6.3% for this year and about 4.3% in 2022. Pent-up demand for goods and services remains strong. ISM PMI Orders components are on the rise. Inventories are depleted and need to be replenished, offering further support for industrial activity in the US (Chart 10A). Philly Fed survey shows that about 40% of respondents plan to increase their capex expenditure (Chart 10B). Strong manufacturing activity is likely to translate into further robust employment gains. Chart 10AAre At All Time Low And Need To Be Replenished

Are At All Time Low And Need To Be Replenished

Are At All Time Low And Need To Be Replenished

Chart 10BCapex Intentions Are On The Rise

Capex Intentions Are On The Rise

Capex Intentions Are On The Rise

Lower For Longer: US economic data has been disappointing recently: Much of the good economic news has been priced in, and the Citigroup Economic Surprise Index is negative. Most of the economic indicators have turned, confirming that the surge in growth has run its course and the macroeconomic environment is normalizing. GDP growth estimates have been downgraded (Chart 11). The Conference Board Economic Indicator has turned, confirming that the US economy is in a slowdown stage of the business cycle (Chart 12). Prolonged friction of supply bottlenecks and transportation disruption may put the brakes on economic growth. Chart 11GDP Growth Estimates Downgraded

GDP Growth Estimates Downgraded

GDP Growth Estimates Downgraded

Chart 12US Economy Is Slowing

US Economy Is Slowing

US Economy Is Slowing

Consumer Is Healthy But In A Bad Mood Rates Are About To Rise Consumers have money to spend: There is still about $2 trillion in excess savings, and considering backlogs of orders across industries, pent-up demand remains high. Lower For Longer Fiscal Tightening: Stimulus spending has peaked. Supplemental federal unemployment benefits of $300 a week expired as of Sept. 6. This may dent consumer spending unless millions of unemployed rejoin the labor force. The rub is in the fact that, with an extra $300 per week, 48% of workers were making more money not working than while employed, according to a recent paper published by the JPMorgan Chase & Co. Institute. Consumer mood has soured: Consumer confidence has slumped to a six-month low of 114 from 125 a month earlier (Chart 13). Many consumers have also postponed durable goods and house purchases discouraged by soaring prices and low inventories (Chart 14). Consumers are also worried about rising prices and expect inflation to exceed 6.5% within 12 months. Chart 13Consumer Mood Has Soured

Consumer Mood Has Soured

Consumer Mood Has Soured

Chart 14Soaring Prices And Low Inventories Discourage Purchases

Soaring Prices And Low Inventories Discourage Purchases

Soaring Prices And Low Inventories Discourage Purchases

Investment Implications It is apparent from this analysis that predicting the timing of tapering is close to impossible, as too much depends on the September employment report, the future rate of Covid-19 infections, the potential emergence of variants, and the further patterns of inflation and supply disruption. How do different assets react to rate hikes? In case the “Lower for Longer” scenario dominates, Growth and Defensives will outperform. Specifically, sectors like Consumer Staples, Health Care, Communications, and Technology will thrive in this environment (Chart 15). If rates start rising, we expect Value, Small Caps, and Cyclicals to outperform, specifically, Financials, Consumer Discretionary, and Industrials. Chart 15Barbell Portfolio: Choose Outperformers From Each Regime

Barbell Portfolio Or Safety First

Barbell Portfolio Or Safety First

US Equity Sector Strategy Positioning We recommend pursuing a barbell approach to portfolio construction: A mix of Growth sectors that benefit from low rates, and economically sensitive Cyclicals, which are geared to higher growth and rising rates. Rates Are About To Rise We are overweight cyclicals in our portfolio in case the economy keeps growing apace, US consumers prove to be undeterred by fears of Covid-19 variant(s), and market expectations shift towards imminent tapering. We are overweight Consumer Services and Industrials. Lower for longer We have been overweight Growth, Technology, and Media & Entertainment in our portfolio since June 2021. While the rates outlook remains uncertain and “lower for longer” is a realistic scenario, we will stick to this positioning while Covid variants are lurking, and growth slowing. For the same reason, we are also overweight Health Care (defensive growth). Underweights We are underweight Consumer Staples, Utilities, and Telecom as these sectors are bond proxies, and at this point it is unlikely that rates will move much lower from here. Our base case is stable or higher. We are also underweight Materials, and Metal & Mining specifically, as this sector is exposed to a Chinese growth slowdown, which suppresses demand for industrial metals. Changes in Positioning Upgrade Financials to an overweight from equal weight. Financials thrive in an environment of rising rates and a steepening yield curve when tapering arrives. From a broader investment perspective, Financials and Banks are cheap, trading at 14x and 12.2x forward earnings respectively. Further, commitment to returning cash to shareholders will benefit investors with a long-term investment horizon. We stay neutral on Insurance as the magnitude of the fallout from Hurricane Ida is still unknown, but it is already clear that payouts will be sizeable. Downgrade Energy to equal-weight from overweight. Although energy, in principle, should do well in the environment of rising rates, we don’t see much upside to this investment. Crude oil has come off its recent highs, with Brent trading at $73 a barrel compared to $76 at the beginning of August. Although demand will continue to recover and supply is somewhat constrained by the OPEC 2.0 agreement, our energy strategists see limited upside to oil prices over the next 12 months, with a forecast of Brent to average $73 a barrel in 2022 (Chart 16). Chart 16Limited Upside For Oil For The Next Year

Limited Upside For Oil For The Next Year

Limited Upside For Oil For The Next Year

Bottom Line The Fed has been clear in communicating that we are drawing closer and closer to the doom day of tapering, yet there are so many countertrends in the market that it is not clear which will dominate and how soon tapering will commence. Our working assumption is that it starts in December 2021 / January 2022. Considering that markets are forward-looking, repositioning for tapering may start in advance, but there is also a danger of being too early if economic growth, inflation, and employment gains surprise on the downside and tapering is delayed. Considering the level of uncertainty in the markets, we recommend a barbell approach to portfolio construction, i.e., having an overweight in the portfolio to sectors that outperform when rates go up, such as Financials and Cyclicals, and have overweights to parts of the market that benefit from “lower for longer” such as Growth, Technology, and Health Care. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Recommended Allocation

Highlights Economy – A partial undoing of 2017’s Tax Cuts and Jobs Act is in the works as Congress takes up the Biden Administration’s infrastructure agenda: A modest increase in the marginal corporate tax rate to help fund infrastructure investment is being discussed on Capitol Hill. We do not expect the ultimate agreement will meaningfully impact output. Markets – Equities appear to have taken little note of the tax-hike debate, and there are worries that investors are being overly complacent about the potential implications: Earnings estimates do not seem to reflect the impact of higher taxes on companies’ bottom lines. Based on the proposals that are reportedly being discussed, however, we think the impact on S&P 500 earnings will be modest. Strategy – A tax hike alone does not justify broad asset allocation shifts, though adjusting positions within equity portfolios could have promise: The effects from a marginal rate increase will be felt most strongly at the individual stock level, based on differences in effective tax rates. Feature We have shown that bear markets (light red shading) and recessions (gray shading) tend to coincide, while stocks generally march higher during economic expansions (Chart 1). We have also shown that the S&P 500 performs considerably better when monetary policy is easy (the fed funds rate is below our estimate of equilibrium) than when it is tight (fed funds exceeds our equilibrium estimate). While an investor could do a lot worse than mechanically tie his/her equity positioning to the state of the business cycle and/or the monetary policy cycle, it is not easy to recognize the onset of a recession in real time or accurately assess the equilibrium fed funds rate. We are confident, however, that a recession will not occur in time to sour the twelve-month outlook unless a vaccine-resistant strain of COVID emerges and that monetary policy is at least a couple years from turning restrictive. Chart 1Bear Markets Coincide With Recessions

Bear Markets Coincide With Recessions

Bear Markets Coincide With Recessions

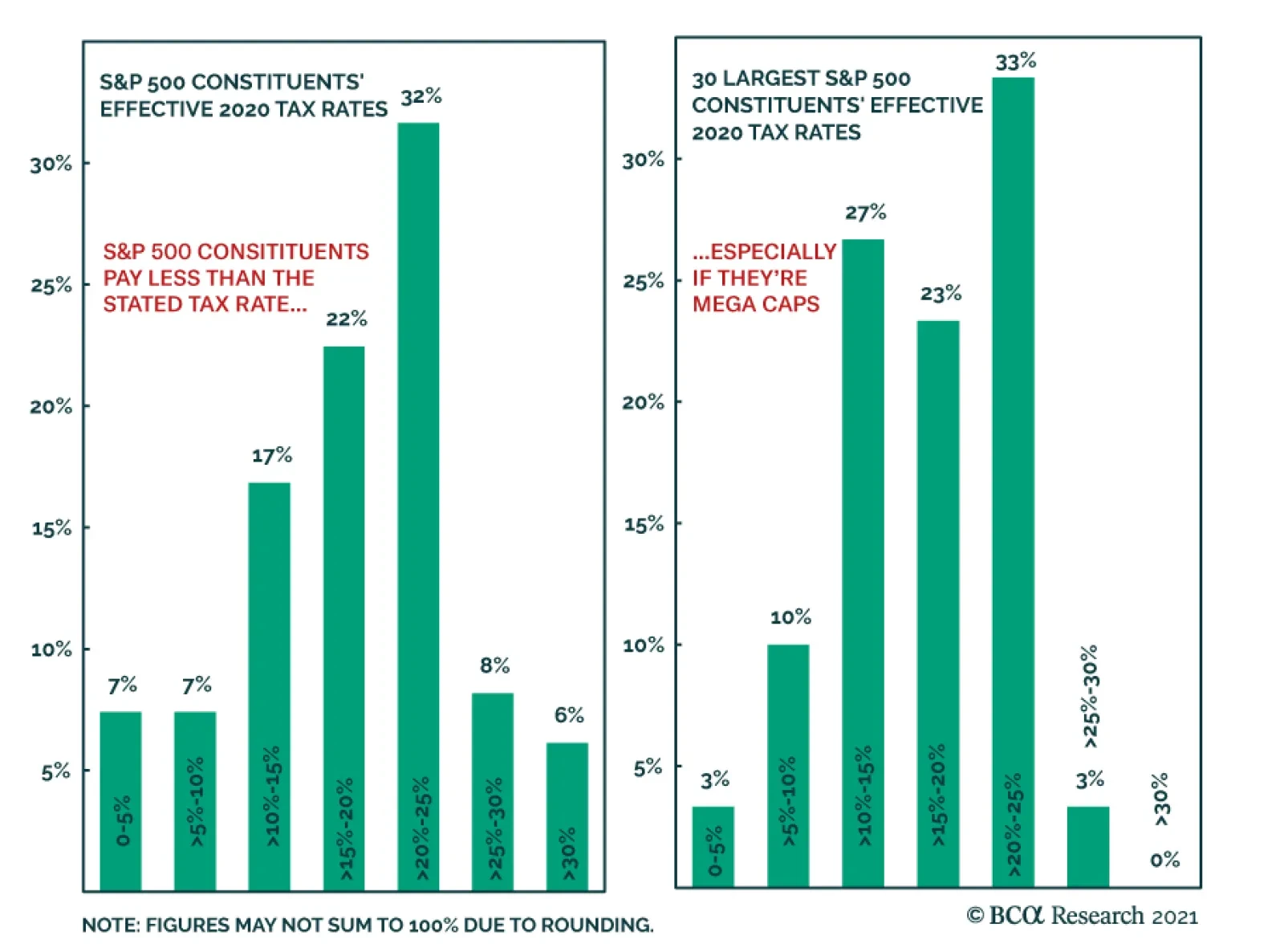

There is more to asset allocation than monetary policy settings and the state of the business cycle, but they currently call for a default equity overweight in multi-asset portfolios. Per our process, an investor must have a very good reason for overriding that default. A blow to earnings from a corporate tax hike that has not been discounted could provide that reason, especially when valuations are extremely elevated. Although it is difficult to know exactly what markets are discounting at any given moment, it seems clear that equity analysts have not put a great deal of effort into estimating the impact of a tax hike on the earnings of the companies in their coverage universe. The good news is that our base-case scenario suggests that the tax changes most likely to make it through Congress will deal the bull a glancing blow rather than a knockout punch. We estimate that a statutory increase in the corporate tax rate from 21% to 25% would clip S&P 500 earnings by about 5%. Against a backdrop of unusually conservative four-quarter earnings expectations, the lagged effects of extraordinarily accommodative monetary and fiscal support, and a paucity of alternatives, the equity bull market appears to be capable of weathering a modest tax hike. The Gap Between Marginal And Effective Tax Rates The byzantine nature of the United States tax code creates myriad opportunities for the spectrum of companies subject to its provisions. Tailored tax advice is a thriving cottage industry that employs hundreds of thousands of well-paid accountants, attorneys and specialists in structuring transactions to minimize clients’ outlays. The upshot of the various incentives embedded in the code is that the marginal tax rate – the tax owed on an additional dollar of earnings – may diverge from the effective tax rate – the share of an entity's aggregate earnings that are paid in taxes. Based on the relative favoritism the code bestows upon a particular activity, or the disparate way it treats domestic and foreign operations, effective tax rates can vary widely at the industry level. Of the 392 S&P 500 constituents that owed income tax in their last full year of operations, 60% had an all-in effective tax rate that fell below the 21% statutory federal rate.1 After allowing for state and local income tax levies, the distribution of effective rates shows that a considerable majority of companies manage to pay less than the marginal rate (Chart 2A). The potential for reducing the effective rate is directly related to a company’s size (presumably because the biggest companies are most likely to have multinational activities): the 30 largest tax-paying constituents, accounting for over one-half of the index's tax-paying market-cap, were even more adept at staying below the all-in marginal rate (Chart 2B). Chart 2AS&P 500 Constituents Pay Less Than The Stated Tax Rate ...

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Chart 2B... Especially If They're Mega-Caps

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Will Higher Corporate Taxes Spell The End Of The Bull Market?

If every S&P 500 constituent’s effective tax rate equaled the marginal tax rate, an increase to 25% from 21% would result in a 5.1% decrease in S&P 500 earnings, as net income would fall from 79 cents of every dollar of pre-tax income to 75 cents. The income decline would be permanent, assuming no further tax-rate changes, and would merit an equivalent decline in the index. Changes in long-run fundamental prospects are not reflected instantaneously in stock prices, however, and it is uncertain just when the market would account for it. There are additionally some near-term buffers to declines in forward four-quarter estimates that might mask any drag from a tax hike. If A Long-Term Tree Falls, Will It Make A Sound? The future is unknowable, but we have at least a puncher’s chance of anticipating what’s to come over short segments like a quarter or a year. The ecosystem of publicly held companies largely operates within that one-to-four-quarter timeframe: companies report quarterly results, as do asset managers, and nearly everyone professionally involved with public equities is subject to compensation structures with annual performance incentives. A share of stock may entitle its owner to a proportional share of earnings in perpetuity, but the next four quarters loom large in the market’s calculus, even to the point of obscuring nearly everything that may come after them. It follows, then, that surprises affecting the outlook for the next year may muffle the market’s reaction to tax negotiations on Capitol Hill. We repeat that consensus analyst expectations for the coming four quarters are modest relative to history and the current macroeconomic backdrop. Now that the second quarter is in the books, analysts are calling for a slight earnings retrenchment, with earnings falling nearly 7% in the third quarter before rising 4% and 1% in the next two quarters, respectively, to settle in the first quarter of 2022 at a level 2% below the quarter just ended. They are not projected to top last quarter’s high-water mark until the second quarter of 2022 (Table 1). Table 1A Low Bar

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Will Higher Corporate Taxes Spell The End Of The Bull Market?

It is possible that earnings will grow that slowly – the pandemic is not over, corporate profit margins may narrow if companies are unable to raise prices enough to cover their rising input costs, fiscal support for the economy is waning, and financial conditions may tighten as the Fed dials back monetary accommodation at the margin – but it would be unlikely on two counts. First, it would counter the empirical record. Earnings have tended to grow, quarter-on-quarter, during expansions (Chart 3). Chart 3That's Why They're Called Expansions

That's Why They're Called Expansions

That's Why They're Called Expansions

Second, it would fly in the face of the red-hot macroeconomic backdrop. The lagged effects of extraordinarily accommodative monetary and fiscal policy settings have real US GDP poised to grow at a pace well above its long-run potential trend through the end of 2022. The equity market is indifferent to quarterly GDP releases, which come out every 63 trading days with a one-month lag and are subject to two revisions that arrive after 21-session intervals, but trailing four-quarter GDP is highly correlated with trailing four-quarter sales (Chart 4, top) and earnings per share (Chart 4, bottom). We of course prefer forward-looking models to backward-looking data but the persistence of economic cycles, especially as they have lengthened across the postwar era, confers some useful predictive properties on trailing data. Chart 4GDP Growth Influences Revenue And Earnings Growth

GDP Growth Influences Revenue And Earnings Growth

GDP Growth Influences Revenue And Earnings Growth

Earnings are a function of revenues (units times price per unit) and margins (per-unit profitability) and robust GDP growth would seem to be tied only loosely to the latter. Over the last three decades, however, growth in S&P 500 earnings per share has been as correlated with GDP growth as growth in revenue per share. Margins are already elevated (Chart 5) and rising cost pressures threaten to squeeze them unless companies can pass on costs to their customers, but the volume pickup embedded in potent real GDP growth will mitigate some of the downward pressure. Chart 5Elevated For Longer?

Elevated For Longer?

Elevated For Longer?

We will have to wait and see how much pricing power companies have, as it will probably take several months before a clear picture begins to emerge. If they can make price hikes stick, margins will hold up, earnings will keep rising and the S&P 500 should power through the meager year-end 2021 and 2022 targets offered by a panel of buy- and sell-side strategists in last week’s Barron’s. We think it is plausible that households, flush with found money from pandemic fiscal transfers and/or financial and housing market appreciation, may prove to be relatively price-insensitive until they work down their windfalls. Vibrant demand could push companies to increase capacity, boosting hiring and capex, stoking more demand in a self-reinforcing post-pandemic honeymoon. The boom would not go on forever, but such a scenario would yield more upside for financial markets and the economy than the increasingly wary consensus projects. Revisiting Lower Fifth Avenue’s Retail Corridor To landlords’ chagrin, businesses’ real estate costs are a source of margin relief. We returned to lower Fifth Avenue to update our retail rental survey and found that little changed between Memorial Day and Labor Day. Two storefronts that were vacant at the end of May have since been rented by pandemic winners Tonal (interactive home gyms) and Hoka (high-performance running shoes), filling two corner locations in the northern half of the corridor (Figure 1). Four storefronts that were occupied by apparel retailers on our last tour – Gap, Gap Kids and Gap Body, and Rigby & Peller, a specialty purveyor of lingerie and swimwear – are vacant now (Figure 2). The net two-store decline has reduced the retail occupancy rate on Fifth Avenue between 14th Street and 23rd Street to 60% from 63%. Figure 1Fifth Avenue Storefronts, 19th Street To 23rd Street

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Figure 2Fifth Avenue Storefronts, 14th Street To 19th Street

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Will Higher Corporate Taxes Spell The End Of The Bull Market?

According to the Real Estate Board of New York (REBNY), average and median asking rents along the corridor have fallen by 3% and 21%, respectively, since Fall 2020. The excess of storefront supply over demand is a modest inflation corrective in an economy in which the partial release of pent-up demand has exceeded the uneven restoration of supply across several categories. REBNY’s semi-annual rental research survey left no doubt that retail tenants have the upper hand in Gotham and we’d suspect that office tenants do as well. The current market offers tenants ample availability and reduced leasing costs. Some firms recently capitalized on the conditions[,] … includ[ing] [upscale British furniture] retailer … Timothy Oulton [which leased over 7,000 square feet of space across three levels at 20th and Broadway, a block east of Fifth Avenue]. Additionally, an array of smaller service-oriented retailers such as dry cleaners, dance studios and barber shops are locking in favorable terms or shifting to better locations.2 Investment Implications The investment implications of the equity market’s seeming nonchalance regarding looming corporate tax hikes will probably be most keenly felt at the sector, sub-industry or individual stock level. Though we do not see meaningful asset allocation consequences, the disparity in effective tax rates at the sector level (Table 2) hints at disparities across sub-industries and individual stocks. With input from equity analysts, it should be possible to assemble baskets of stocks based on their sensitivity to a higher marginal income tax rate. Table 2One Size Does Not Fit All

Will Higher Corporate Taxes Spell The End Of The Bull Market?

Will Higher Corporate Taxes Spell The End Of The Bull Market?

As Barron’s September 6th Fall Investment Outlook feature highlighted, buy-side CIOs and sell-side strategists have adopted a measured tone. Year-end 2021 S&P 500 targets hover around the index’s current level and top-down 2022 projections offer no more than grudging upside. Tightening margins are a leading fundamental concern, along with rising inflation pressures, and elevated valuations contribute to the sense of unease. A chorus of “This won’t end well” intonations suggests that stocks may have a wall of worry to scale before the spoilsport consensus can claim validation. Regarding inflation concerns, asset allocators should bear in mind that stocks are an inflation hedge relative to cash and bonds. They should also recognize that high inflation does not derail equities; tight monetary policy in response to high inflation, which involves higher interest rates as part of a deliberate effort to throttle an overheating economy, derails equities. Investors conditioned to a predictably rapid Fed response may view this as a distinction without a difference. Per our house view that the fed funds liftoff date is over a year away and the sustained series of rate hikes required to tighten policy is well more than another year out, however, TINA's influence may become even more pronounced before this bull market ends. We remain vigilant, but we think it is too early to head for cover. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 The term “all-in” recognizes that US corporations uniformly incur tax liabilities at the state level in addition to their federal obligations. The average marginal 2021 state income tax rate is 6.6%. 2 REBNY_Manhattan_Retail_Spring_2021.pdf

As central banks pare back their asset purchases, the process will have the effect of slowing the decline in the stock of bonds that the private sector needs to hold relative to when the central bank was buying bonds more aggressively. This dynamic suggests…

The US August producer price index (PPI) report was somewhat mixed. The year-over-year rate accelerated to a record high of 8.3% from July’s 7.8%. However, PPI slowed on a month-over-month basis to 0.7% from 1.0%. The continued acceleration in annual PPI…

Congress’ passage of the American Families Act is a keystone of the President Biden’s legislative agenda. However, to pay for the additional spending, Democrats will seek to levy more taxes on corporations and higher-income earners. The Biden Administration is aiming to raise the corporate tax rate from 21% to 28%, bringing it halfway back to the 35% level that prevailed prior to the Trump tax cuts. Joe Manchin, a key swing voter in the Senate, has indicated a preference for 25%. PredictIt, a popular betting site, assigns 31% odds to no tax hike. Among bettors forecasting higher tax rates, the median estimate is around 25% (Chart 1). BCA’s Geopolitical team thinks that corporate taxes will rise more than current market expectations suggest. Chart 1

Only Death And Taxes…

Only Death And Taxes…

Meanwhile, analyst estimates do not appear to reflect the prospect of higher taxes. However, even under President Biden’s baseline scenario of 28% tax rate, higher tax rates will cut earnings-per-share for S&P 500 companies by about 5% in 2022. Given that earnings are expected to rise by 9% next year, this would leave earnings growth in a positive territory, but just about (BCA Research - Five Risks We Are Monitoring). That’s concerning, given that earnings—particularly earnings estimates—have been driving the S&P 500 higher. The market, however, hasn’t even begun to consider the potential impact (Chart 2). Chart 2

CHART 2

CHART 2

Bottom Line: Corporate taxes are slated for a rise, yet the market has not yet priced this in. Even base case scenario tax hike to 28% is bound to reduce earnings growth by 5%, and have an adverse effect on the US equity market returns.

The share of market capitalization of equities within portfolios is elevated by historical standards. The threat now is that this elevated level could trigger a rebalancing of flows away from equities in favor of bonds, especially among institutional…

Highlights The US Climate Prediction Center gives ~ 70% odds another La Niña will form in the August – October interval and will continue through winter 2021-22. This will be a second-year La Niña if it forms, and will raise the odds of a repeat of last winter's cold weather in the Northern Hemisphere.1 Europe's natural-gas inventory build ahead of the coming winter remains erratic, particularly as Russian flows via Ukraine to the EU have been reduced this year. Russia's Nord Stream 2 could be online by November, but inventories will still be low. China, Japan, South Korea and India – the four top LNG consumers in Asia – took in 155 Bcf of the fuel in June. A colder-than-normal winter would boost demand. Higher prices are likely in Europe and Asia (Chart of the Week). US storage levels will be lower going into winter, as power generation demand remains stout, and the lingering effects from Hurricane Ida reduce supplies available for inventory injections. Despite spot prices trading ~ $1.30/MMBtu above last winter's highs – currently ~ $4.60/MMBtu – we are going long 1Q22 NYMEX $5.00/MMBtu natgas calls vs short NYMEX $5.50/MMBtu natgas calls expecting even higher prices. Feature Last winter's La Niña was a doozy. It brought extreme cold to Asia, North America and Europe, which pulled natural gas storage levels sharply lower and drove prices sharply higher as the Chart of the Week shows. Natgas storage in the US and Europe will be tight going into this winter (Chart 2). Europe's La Niña lingered a while into Spring, keeping temps low and space-heating demand high, which delayed the start of re-building inventory for the coming winter. In the US, cold temps in the Midwest hampered production, boosted demand and caused inventory to draw hard. Chart of the WeekA Return Of La Niña Could Boost Global Natgas Prices

A Return Of La Niña Could Boost Global Natgas Prices

A Return Of La Niña Could Boost Global Natgas Prices

Chart 2Europe, US Gas Stocks Will Be Tight This Winter

NatGas: Winter Is Coming

NatGas: Winter Is Coming

Summer in the US also produced strong natgas demand, particularly out West, as power generators eschewed coal in favor of gas to meet stronger air-conditioning demand. This is partly due to the closing of coal-fired units, leaving more of the load to be picked up by gas-fired generation (Chart 3). The EIA estimates natgas consumption in July was up ~ 4 Bcf/d to just under 76 Bcf/d. Hurricane Ida took ~ 1 bcf/d of demand out of the market, which was less than the ~ 2 Bcf/d hit to US Gulf supply resulting from the storm. As a result, prices were pushed higher at the margin. Chart 3Generators Prefer Gas To Coal

NatGas: Winter Is Coming

NatGas: Winter Is Coming

US natgas exports (pipeline and LNG) also were strong, at 18.2 Bcf/d in July (Chart 4). We expect US LNG exports, in particular, to resume growth as the world recovers from the COVID-19 pandemic (Chart 5). This strong demand and exports, coupled with slightly lower supply from the Lower 48 states – estimated at ~ 98 Bcf/d by the EIA for July (Chart 6) – pushed prices up by 18% from June to July, "the largest month-on-month percentage change for June to July since 2012, when the price increased 20.3%" according to the EIA. Chart 4US Natgas Exports Remain Strong

US Natgas Exports Remain Strong

US Natgas Exports Remain Strong

Chart 5US LNG Exports Will Resume Growth

NatGas: Winter Is Coming

NatGas: Winter Is Coming

Chart 6US Lower 48 Natgas Production Recovering

US Lower 48 Natgas Production Recovering

US Lower 48 Natgas Production Recovering

Elsewhere in the Americas, Brazil has been a strong bid for US LNG – accounting for 32.3 Bcf of demand in June – as hydroelectric generation flags due to the prolonged drought in the country. In Asia, demand for LNG remains strong, with the four top consumers – China, Japan, South Korea, and India – taking in 155 Bcf in June, according to the EIA. Gas Infrastructure Ex-US Remains Challenged A combination of extreme cold weather in Northeast Asia, and a lack of gas storage infrastructure in Asia generally, along with shipping constraints and supply issues at LNG export facilities, led to the Asian natural gas price spike in mid-January.2 Very cold weather in Northeast Asia, drove up LNG demand during the winter months. In China, LNG imports for the month of January rose by ~ 53% y-o-y (Chart 7).3 The increase in imports from Asia coincided with issues at major export plants in Australia, Norway and Qatar during that period. Chart 7China's US LNG Exports Surged Last Winter, And Remain Stout Over The Summer

NatGas: Winter Is Coming

NatGas: Winter Is Coming

Substantially higher JKM (Japan-Korea Marker) prices incentivized US exporters to divert LNG cargoes from Europe to Asia last winter. The longer roundtrip times to deliver LNG from the US to Asia – instead of Europe – resulted in a reduction of shipping capacity, which ended up compounding market tightness in Europe. Europe dealt with the switch by drawing ~ 18 bcm more from their storage vs. the previous year, across the November to January period. Countries in Asia - most notably Japan – however, do not have robust natural gas storage facilities, further contributing to price volatility, especially in extreme weather events. These storage constraints remain in place going into the coming winter. In addition, there is a high probability the global weather pattern responsible for the cold spells around the globe that triggered price spikes in key markets globally – i.e., a second La Niña event – will return. A Second-Year La Niña Event The price spikes and logistical challenges of last winter were the result of atmospheric circulation anomalies that were bolstered by a La Niña event that began in mid-2020.4 The La Niña is characterized by colder sea-surface temperatures that develops over the Pacific equator, which displaces atmospheric and wind circulation and leads to colder temperatures in the Northern Hemisphere (Map 1). Map 1La Niña Raises The Odds Of Colder Temps

NatGas: Winter Is Coming

NatGas: Winter Is Coming

The IEA notes last winter started off without any exceptional deviations from an average early winter, but as the new year opened "natural gas markets experienced severe supply-demand tensions in the opening weeks of 2021, with extremely cold temperature episodes sending spot prices to record levels."5 In its most recent ENSO update, the US Climate Prediction Center raised the odds of another La Niña event for this winter to 70% this month. If similar conditions to those of the 2020-21 winter emerge, US and European inventories could be stretched even thinner than last year, as space-heating demand competes with industrial and commercial demand resulting from the economic recovery. Global Natgas Supplies Will Stay Tight JKM prices and TTF (Dutch Title Transfer Facility) prices are likely to remain elevated going into winter, as seen in the Chart of the Week. Fundamentals have kept markets tight so far. Uncertain Russian supply to Europe will raise the price of the European gas index (TTF). This, along with strong Asian demand, particularly from China, will keep JKM prices high (Chart 8). The global economic recovery is the main short-term driver of higher natgas demand, with China leading the way. For the longer-term, natural gas is considered as the ideal transition fuel to green energy, as it emits less carbon than other fossil fuels. For this reason, demand is expected to grow by 3.4% per annum until 2035, and reach peak consumption later than other fossil fuels, according to McKinsey.6 Chart 8BCAs Brent Forecast Points To Higher JKM Prices

BCAs Brent Forecast Points To Higher JKM Prices

BCAs Brent Forecast Points To Higher JKM Prices

Spillovers from the European natural gas market impact Asian markets, as was demonstrated last winter. Russian supply to Europe – where inventories are at their lowest level in a decade – has dropped over the last few months. This could either be the result of Russia's attempts to support its case for finishing Nord Stream 2 and getting it running as soon as possible, or because it is physically unable to supply natural gas.7 A fire at a condensate plant in Siberia at the beginning of August supports the latter conjecture. The reduced supply from Russia, comes at a time when EU carbon permit prices have been consistently breaking records, making the cost of natural gas competitive compared to more heavy carbon emitting fossil fuels – e.g., coal and oil – despite record breaking prices. With Europe beginning the winter season with significantly lower stock levels vs. previous years, TTF prices will remain volatile. This, and strong demand from China, will support JKM prices. Investment Implications Natural gas prices are elevated, with spot NYMEX futures trading ~ $1.30/MMBtu above last winter's highs – currently ~ $4.60/MMBtu. Our analysis indicates prices are justifiably high, and could – with the slightest unexpected news – move sharply higher. Because natgas is, at the end of the day, a weather market, we favor low-cost/low-risk exposures. In the current market, we recommend going long 1Q22 NYMEX $5.00/MMBtu natgas calls vs short NYMEX $5.50/MMBtu natgas calls expecting even higher prices. This is the trade we recommended on 8 April 2021, at a lower level, which was stopped out on 12 August 2021 with a gain of 188%. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish Earlier this week, Saudi Aramco lowered its official selling price (OSP) by more than was expected – lowering its premium to the regional benchmark to $1.30/bbl from $1.70/bbl – in what media reports based on interviews with oil traders suggest is an attempt to win back customers electing not to take volumes under long-term contracts. This is a marginal adjustment by Aramco, but still significant, as it shows the company will continue to defend its market share. Pricing to Northwest Europe and the US markets is unchanged. Aramco's majority shareholder, the Kingdom of Saudi Arabia (KSA), is the putative leader of OPEC 2.0 (aka, OPEC+) along with Russia. The producer coalition is in the process of returning 400k b/d to the market every month until it has restored the 5.8mm b/d of production it took off the market to support prices during the COVID-19 pandemic. We expect Brent crude oil prices to average $70/bbl in 2H21, $73/bbl in 2022 and $80/bbl in 2023. Base Metals: Bullish Political uncertainty in Guinea caused aluminum prices to rise to more than a 10-year high this week (Chart 9). A coup in the world’s second largest exporter of bauxite – the main ore source for aluminum – began on Sunday, rattling aluminum markets. While iron ore prices rebounded primarily on the record value of Chinese imports in August, the coup in Guinea – which has the highest level of iron ore reserves – could have also raised questions about supply certainty. This will contribute to iron-ore price volatility. However, we do not believe the coup will impact the supply of commodities as much as markets are factoring, as coup leaders in commodity-exporting countries typically want to keep their source of income intact and functioning. Precious Metals: Bullish Gold settled at a one-month high last Friday, when the US Bureau of Labor Statistics released the August jobs report. The rise in payrolls data was well below analysts’ estimates, and was the lowest gain in seven months. The yellow metal rose on this news as the weak employment data eased fears about Fed tapering, and refocused markets on COVID-19 and the delta variant. Since then, however, the yellow metal has not been able to consolidate gains. After falling to a more than one-month low on Friday, the US dollar rose on Tuesday, weighing on gold prices (Chart 10). Chart 9

Aluminum Prices Recovering

Aluminum Prices Recovering

Chart 10

Weaker USD Supports Gold

Weaker USD Supports Gold

Footnotes 1 Please see the US Climate Prediction Center's ENSO: Recent Evolution, Current Status and Predictions report published on September 6, 2021. 2 Please see Asia LNG Price Spike: Perfect Storm or Structural Failure? Published by Oxford Institute for Energy Studies. 3 Since China LNG import data were reported as a combined January and February value in 2020, we halved the combined value to get the January 2020 amount. 4 Please see The 2020/21 Extremely Cold Winter in China Influenced by the Synergistic Effect of La Niña and Warm Arctic by Zheng, F., and Coauthors (2021), published in Advances in Atmospheric Sciences. 5 Please see the IEA's Gas Market Report, Q2-2021 published in April 2021. 6 Please see Global gas outlook to 2050 | McKinsey on February 26, 2021. 7 Please see ICIS Analyst View: Gazprom’s inability to supply or unwillingness to deliver? published on August 13, 2021. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

August payroll grew only by 235,000 jobs, which is way below 750 thousand expected by the market, and a million jobs that were created both in June and July. This disappointing number is confounding. Companies are still struggling to fill job openings: There are 10.9 million job openings but 8.5 million workers looking for a job (Chart 1). Of nearly 25 million jobs lost since January 2020, only about half have been restored and filled. Wages in August increased by 4.3% year-over-year, which is consistent with labor shortages that put upward pressure on wages. Chart 1Plenty Of Job Openings To Fill

Plenty Of Job Openings To Fill

Plenty Of Job Openings To Fill

What is behind this conundrum? A low jobs number may have resulted from a Delta hit to the service industries both in terms of availability of jobs and the number of applicants: According to Indeed, over 15% of unemployed workers are not looking for a job because of covid fears (Chart 2). Hope is that Delta infections are cresting, and these workers will return to the job market, along with those who have care responsibilities. Also, jobs data is volatile, and revisions are common. In short, we are not worried: the August job report is an aberration, and September numbers will be better. Chart 2Americans Are Not Desperate To Find Work

Labor Shortages Vs A Disappointing Jobs Report

Labor Shortages Vs A Disappointing Jobs Report

Chart 3African American Employment Is Elevated

African American Employment Is Elevated

African American Employment Is Elevated

Will a good September report bring tapering forward? It depends. The unemployment rate stands at 5.2%, while African American unemployment stands at 8.8%, which is 1.7% and 2.7% above the pre-pandemic levels respectively. If in September African American unemployment does not budge and remains elevated, it will most likely delay tapering as Fed is focused not only on the overall level of unemployment but also on an equitable unemployment rate across racial groups (Chart 3). Bottom Line: Next month’s report will be a decisive data point for a Fed’s tapering timing decision, with the focus on unemployment rates disparities across racial groups.

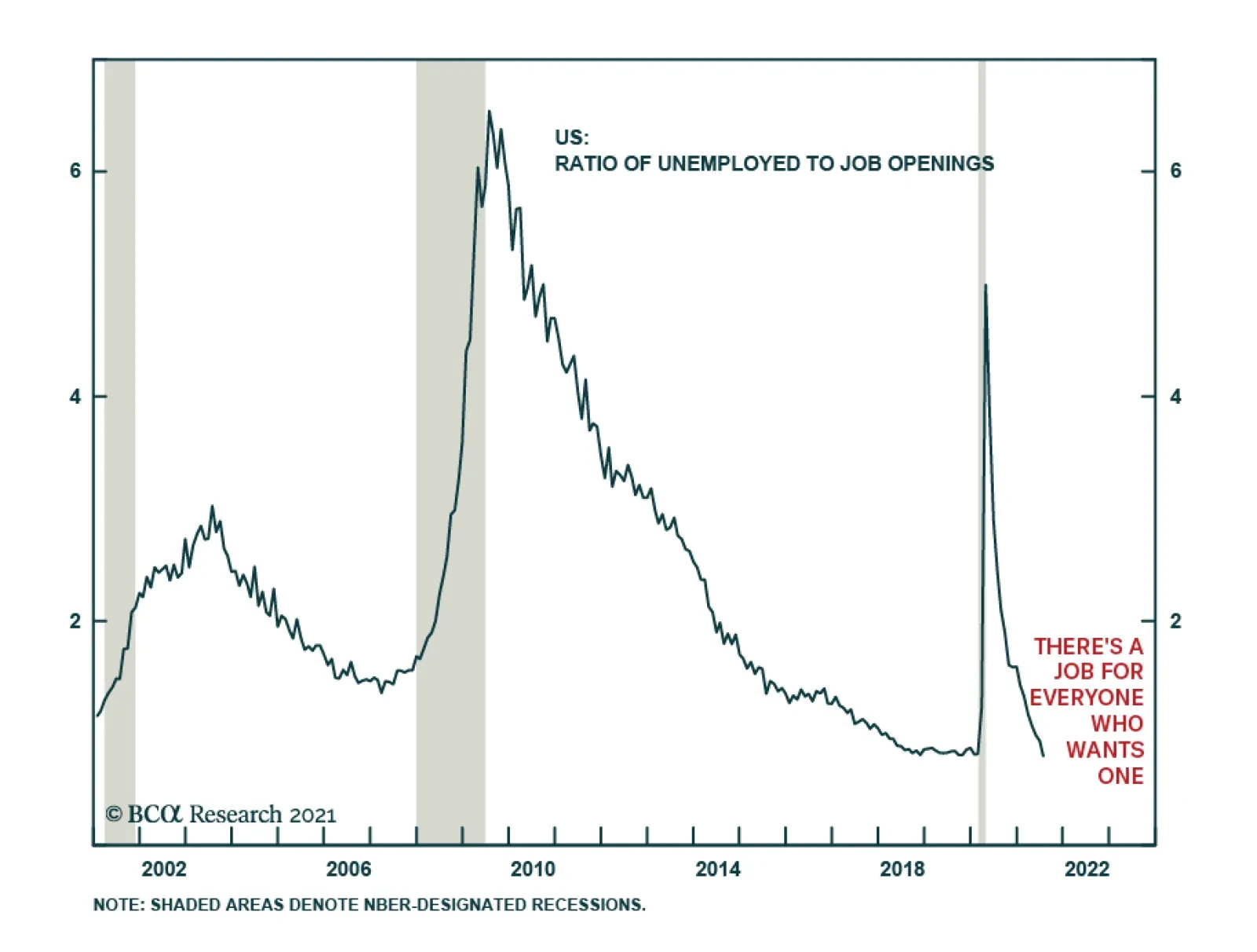

The JOLTS survey for July showed that US labor demand remains extremely strong. The number of job openings reached a new series high of 10.9 million following June's 10.2 million, and handedly beat expectations of 10.0 million. The accommodation & food…