United States

Highlights Economic policy uncertainty is rising in the US and will generate volatility this fall. But by the end of the year the result should be more fiscal reflation. Biden’s approval rating is now “underwater” – net negative – but this was expected. Unless he suffers another black eye, he can still shepherd his two big bills through Congress by year’s end. Public support for Biden’s tax hikes is weak. Some tax hikes are likely but aggressive hikes are now off the table. The midterm elections were already likely to produce a Republican win in the House. History supports this consensus. But the Senate is still an open game. The presidential election outlook is only marginally affected, at most, by the messy Afghanistan pullout. Value stocks are re-testing their low point against growth stocks. We do not expect them to break down when Congress is about to pass historic new spending increases. Feature Economic policy uncertainty is reviving in the US and set to increase this fall. This is true in absolute terms and relative to global uncertainty, even at a time when China’s sweeping regulatory crackdown is generating a lot of global uncertainty (Chart 1). Chart 1US Relative Policy Uncertainty Reviving

US Relative Policy Uncertainty Reviving

US Relative Policy Uncertainty Reviving

Chart 2Policy Uncertainty Breakdown

Policy Uncertainty Breakdown

Policy Uncertainty Breakdown

The latest increase in the policy uncertainty index is largely driven by rising uncertainty over future government spending (Chart 2, panel 2) and expiring tax provisions (Chart 2, panel 3), more so than by public sentiment reflected in the mainstream media or even the inflation debate. The looming budget battle this fall will have major implications for taxes and spending and will lift the uncertainty indicators regarding sentiment and consumer prices. Volatility will ensue in the coming months. But by the end of the year, Congress will have passed at least one, likely two, new laws that will increase government fiscal support for the economy and dispel deflationary tail risks. The lingering pandemic will if anything help concentrate lawmakers’ minds on passing more stimulus. Therefore we expect US equities and cyclical sectors to grind higher. The passage of these bills will mark the high point in policy reflation, after which clouds will loom on the horizon in 2022. Biden’s Net Negative Approval Rating President Biden’s job approval rating is now officially “underwater” – more people disapprove of his leadership than approve (Table 1). This is raising serious doubts about his ability to shepherd legislation through Congress this fall. However, these doubts are overrated. Table 1Biden’s Net Approval Is Officially Negative

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Biden’s approval has mostly fallen due to his mishandling of the US military’s withdrawal from Afghanistan – which most Americans agree was necessary, however much they deplored the commander-in-chief’s handling of it. Therefore Biden’s approval rating will not fall much farther – at least not until he suffers another black eye. Until that happens, Biden’s approval will stabilize in the range of Obama’s and above Trump’s. The reason is that he retains a solid political base of support – and his political base is larger than President Trump’s, so his general approval will stay higher. Indeed his approval is still stronger than Obama’s among Democrats (Charts 3A and 3B). This is counterintuitive since Obama was a charismatic, young, and progressive Democrat. The reason is that Democrats are still very cognizant and fearful of the alternative: President Trump. This anti-Trump tailwind will help Biden for some time. Support among Democrats is critical for maintaining party discipline in passing the reconciliation bill this fall. It is also important for the midterm elections. Chart 3ABiden’s Job Approval Collapses

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 3BBiden’s Approval Holding Up Among Democrats

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

On specific issues, Biden is weaker than Obama on foreign policy and than Trump on the economy (Charts 4A and 4B). The economy will remain the central concern, notwithstanding Afghanistan, and on this front Biden should stabilize or improve. However, other foreign policy issues could rise to the fore and hurt him at any time given today’s fraught geopolitical environment. Chart 4ABiden’s Falling Approval On Economy

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 4BBiden’s Falling Approval On Foreign Policy

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

We say Biden’s score on the economy will improve because consumer confidence will rebound once the Delta variant of COVID-19 subsides (Chart 5). Both manufacturing and service sectors are performing better than when Biden was elected and employment is holding up in both sectors. The new orders-to-inventories measures suggest the service sector will continue to improve (Chart 6). The headline unemployment rate has dropped to 5.2%. Chart 5Consumer Confidence Should Support Biden

Consumer Confidence Should Support Biden

Consumer Confidence Should Support Biden

Chart 6PMIs Also Offer Some Support For Biden

PMIs Also Offer Some Support For Biden

PMIs Also Offer Some Support For Biden

Given the above, Biden still has enough clout to steer his signature legislation through Congress this fall, albeit with major modifications to his unwieldy $3.5 trillion American Families Plan. Moderate Democratic Senator Joe Manchin of West Virginia has called for a pause in new big spending legislation, but a close look at his words shows that he does not oppose the bill, he merely wants to water it down, which is not a change from his earlier position.1 He speaks for other moderates. The left-wing faction led by Senator Bernie Sanders of Vermont will make counter-threats yet ultimately has no choice other than to support the most progressive social legislation in recent memory. The bill will be watered down. Could this watering down process result in a total jettison of the Democrats’ proposed tax hikes? The Wall Street Journal reports that congressional support for tax hikes is losing steam.2 While aggressive tax hikes are off the table, we highly doubt that all tax hikes will be removed. Financial markets have not responded much to the threat of higher taxes. Small business owners, who are most sensitive to the risk of new taxes and regulation imposed by Democrats, have not shown much concern for either issue this year – they are much more worried about inflation (Chart 7). We assume the equity market would rally if tax hikes were dropped but we do not think this is likely to happen. Americans support higher taxes – but only Democrats are enthusiastic about across-the-board hikes on individuals, corporations, and capital gains. Polls show that 59% of independent voters, not to mention Democrats, support higher taxes on high-income earners, although the proposed 28% corporate is increasingly likely to be cut down (Chart 8). This is the fundamental reason for investors to expect Democrats to band together in the eleventh hour and include tax hikes in their reconciliation bill. If nothing else, a partial reversal of President Trump’s Tax Cut and Jobs Act will be necessary to give a veneer of affordability to Biden’s giant spending bill to get it past Senate moderates. Chart 7Business Will Worry About Tax Hikes When (If) They Pass

Business Will Worry About Tax Hikes When (If) They Pass

Business Will Worry About Tax Hikes When (If) They Pass

Chart 8Look Out: Americans Support Higher Taxes

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

The impact of Biden’s corporate tax hike is expected to be a 5%-8% one-off hit to corporate earnings, according to our Global Investment Strategy. The impact could be less than that but the combination of popular opinion and the Democratic Party’s need to finance their social agenda suggests that investors should plan for the worst, which in this case is not that bad – key tax rates will still be lower than they were under President Obama. The chief risk to Biden’s legislation is that passing the bipartisan infrastructure bill (80% subjective odds) consumes so much political capital that there is not enough left for Biden’s reconciliation bill (50%-65% subjective odds, depending on circumstances). This is possible. Congressional Democrat leaders want to tie these two bills together but most likely the quick success of infrastructure, which is more popular than social welfare, will lead Democrats to conclude that a bird in the hand is worth two in the bush. They will pass infrastructure on less-than-perfect assurances from Senate moderates that they will support reconciliation. Then a separate battle over reconciliation will ensue, in which Biden must cajole the left-wing and moderate factions of his party into a “yea” vote while Republicans obstruct. The second major risk to Biden’s legislation – and the macro backdrop – comes if he mismanages foreign policy more generally, such as with the looming crisis over Iran. A foreign policy failure beyond Afghanistan could cause permanent damage to his political capital. And yet Democrats would be even more desperate for a legislative victory then, as they would face a wipeout in the midterm elections if they had no legislative victories and two foreign policy humiliations. In other words, Biden is nowhere near so unpopular that moderate Democrats will abandon his signature legislative agenda and condemn their party and his administration to a heavy defeat in 2022. Bottom Line: Biden’s legislation will pass, including some tax hikes. The revised magnitude of tax hikes will not be known until later this fall when the Senate and House start producing legislative text. Policy uncertainty and equity volatility will trend upward this fall but the end-game is more reflationary policy, which should keep equities grinding higher at least through Christmas. Midterm Elections: The Best Case For Democrats Is Not Good Enough Are Republicans more likely to take Congress now that Biden’s approval is underwater? How would this impact the policy and macroeconomic outlook? While Republicans are highly likely to retake the House of Representatives, the Senate is still slightly tipped for the Democrats. Biden would have to fail to pass legislation or commit another major policy mistake to give Republicans full control of Congress, although this outcome is slightly favored in online betting markets. The House currently consists of 220 Democrats and 212 Republicans. There is always some fluctuation in the exact numbers. Three vacancies should be filled in November’s special elections, which could bring the count to 222 Democrats and 213 Republicans.3 With 218 votes needed to pass legislation on an absolute majority vote, Democrats can only afford to lose three votes at present. This is an extremely tight margin and shows that this fall’s reconciliation bill is at risk in the House as well as the Senate. In the midterm elections, Republicans only need to take five-to-six seats to regain the majority (218). This is easy on paper: the average seat gain for the opposition in midterm House elections is 35. Biden’s latest approval rating puts Democrats in line to lose 37 seats based on history. The opposition typically makes gains in the midterm because it is fired up whereas the presidential party is complacent. In addition Republicans are expected to gain two seats (possibly as many as four) via gerrymandering in 2022. True, Democrats have some underrated supports in 2022. In all probability the pandemic will be waning while the economy will be waxing. Biden will likely have passed at least a bipartisan infrastructure deal. The divisions within Republican ranks over Trumpism will also persist, which may or may not increase Democratic turnout and vote-switching from suburban Republicans. Hence it is reasonable to ask whether Democrats could surprise to the upside and retain the House. Online betting markets put the probability at 29%, and these odds make sense to us. The historical record helps to define what kind of events might alter the outlook for the midterms. Table 2 shows the midterm elections in which the presidential party performed best (the opposition party disappointed the historical norm). The following points are salient: Table 2Best-Case Outcomes For Presidential Party In Midterm Elections

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

There are only two cases in which the presidential party gained seats (Clinton 1998, Bush 2002) and three cases in which they only lost a few seats (Kennedy 1962, Reagan 1986, arguably Bush 1990). The Democratic victory of 1998 occurred at the top of an economic boom while the Republican victory of 2002 occurred one year after the 9/11 terrorist attacks. Neither is likely to be replicated for Democrats in 2022. Republicans’ mild losses in 1990 occurred just after Iraq invaded Kuwait. Republican’s mild losses in 1986 occurred despite a big legislative victory (tax reform). If either of the last two scenarios played out for Democrats in 2022, Democrats would likely lose the House by a whisker. Only if the Democrats’ 1962 scenario played out would Democrats retain the House in 2022, and only by a single seat. Yet the 1962 election occurred in the midst of the Cuban Missile Crisis! The takeaway is that a foreign policy crisis could help Democrats pare their losses in the midterms if Biden is deemed to have handled the crisis adroitly. But even then the ruling party would likely lose the House judging by history. Needless to say these are just historical examples. They also show that Democratic fortunes could turn around drastically between now and next fall (e.g. Kennedy went from a recession and the Bay of Pigs fiasco to gaining his party seats). The Senate outlook is less straightforward. Biden’s approval rating suggests a loss of four seats for Democrats based on the historical pattern. But the same pattern suggested Republicans would lose four seats in 2018 and instead they gained two. Our quantitative Senate election model, which we update every week in the Appendix, still tips the Democrats to gain one seat (a 51-49 majority) or at least retain their de facto one seat majority (50-50). Chart 9Presidential Vetoes In History

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

What are the macroeconomic implications? A Republican House and Democratic White House would play “constitutional hardball,” just as occurred from 2011-14, given that the country is still at historically peak levels of political polarization.4 There are likely to be critical differences between 2011 and 2023 – populism has fundamentally weakened support for fiscal austerity – but the most likely result is gridlock and deadlock. Republicans will not be able to slash spending or cut taxes as Biden will have the presidential veto, but Democrats will not be able to increase spending or hike taxes (Chart 9). The problem for Biden would be the need to avoid a national default when and if the Republicans insist on spending cuts to raise the debt ceiling. The looming debt ceiling showdown this fall will increase uncertainty and volatility but ultimately Democrats have the votes to avoid a default. That would not necessarily be the case if Republicans controlled the House. And this time around Republicans could be driven to impeach the president, for whatever reason, in retaliation for President Trump’s impeachment in 2019. This situation obviously cannot be ruled out, even though it would be virtually impossible for the Senate to convict. At the same time, some bipartisanship could occur, as it did under Trump following the 2018 midterms. Anti-trust legislation and immigration reform are the two most important policy areas to watch on this front. Republican gains in Congress would marginally weaken the Democrats’ hold on the White House in 2024, though we continue to believe that Democrats are favored. American voters are likely to be better off in November 2024 than they were in November 2020, amid a pandemic, recession, and nationwide social unrest. Our quantitative model tips Democrats with 308 electoral votes (Appendix). Professor Allan Lichtman’s “13 Keys” to the presidency – a nearly flawless prediction system since 1984 – currently suggest that the Democrats only have three keys turned against them. They would need to see six or more in order to lose the White House (Table 3). Obviously the long-term status of the economy will be a critical factor (Chart 10). Table 3Lichtman’s Keys To The Presidency (Updated Sept 2021)

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 10Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Bringing it all together, US fiscal policy has taken a more proactive turn but it is still likely to freeze after this fall. It will be hard to pass major budget bills in 2022 ahead of the election and gridlock is the likeliest outcome, making 2025 the next realistic chance for major fiscal changes. The immediate implication is that Biden and Democratic leaders will have to disconnect the bipartisan infrastructure bill from the partisan social welfare reconciliation bill this autumn. This will require a major concession from House Speaker Nancy Pelosi. Otherwise both bills could collapse and with them the Democratic Party’s fortunes. Biden and moderate Democrats that face competitive races in 2022 will demand a quick victory before moving onto the less popular part. Investment Takeaways Value stocks are re-testing their cycle lows against growth stocks (Chart 11). The Delta variant and global growth jitters continue to weigh on this trade. Chart 11S&P Value Re-Tests Lows Versus Growth

S&P Value Re-Tests Lows Versus Growth

S&P Value Re-Tests Lows Versus Growth

The S&P 500’s “Big Five” are rallying and outperforming the other 495 companies once again (Chart 12). Chart 12S&P 5 Recovery Versus 495

S&P 5 Recovery Versus 495

S&P 5 Recovery Versus 495

We expect politically induced volatility throughout the fall but we also expect it to be resolved in new and reflationary legislation. Signs that Biden’s legislation will pass should enable cyclical sectors and value stocks to recover, though the pandemic, global growth, and Chinese stability may prevent them from outperforming defensive sectors and growth stocks. A new set of hurdles will face markets if Republicans regain the House and halt fiscal easing from 2022-24. However, they will not be rewarded by voters if they create a fiscal or economic crisis, implying that the proactive fiscal turn in public opinion will prevail over the long run. If Biden’s legislation fails then it suggests that US fiscal policy is dysfunctional even under single-party control. This would heighten the deflationary tail risk and force us to reassess our macro and policy outlook. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1USPS Trade Table

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A2Political Risk Matrix

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart A1Presidential Election Model

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart A2Senate Election Model

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A3Political Capital Index

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4APolitical Capital: White House And Congress

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4BPolitical Capital: Household And Business Sentiment

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4CPolitical Capital: The Economy And Markets

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Footnotes 1 See Senator Joe Manchin, “Why I Won’t Support Spending Another $3.5 Trillion,” Wall Street Journal, September 2, 2021, wsj.com. 2 Richard Rubin, “Progressives’ Tax-The-Rich Dreams Fade As Democrats Struggle For Votes,” Wall Street Journal, September 5, 2021, wsj.com. 3 The three special House elections are: Florida’s 20th District, previously Democratic held; Ohio’s 11th District, previously Democratic held; Ohio’s 15th District, previously Republican held. 4 See Mark V. Tushnet, “Constitutional Hardball,” John Marshall Legal Review 37 (2004), pp. 523-53, scholarship.law.georgetown.edu.

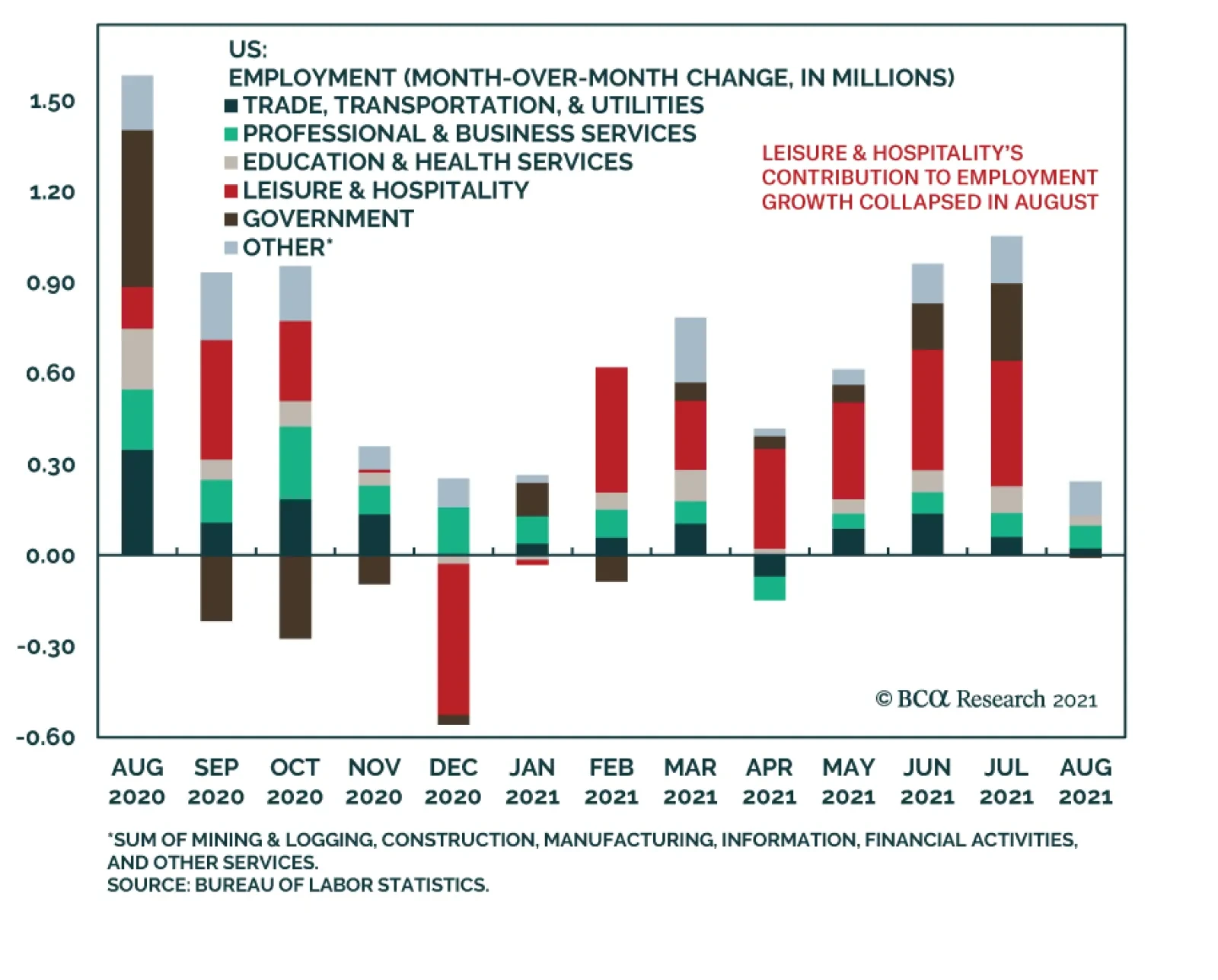

Highlights Chart 1Employment Growth Will Rebound

Employment Growth Will Rebound

Employment Growth Will Rebound

August’s weak employment growth reflects the surge of Delta variant COVID cases in the United States. This is evidenced by the fact that Leisure & Hospitality sector payrolls held flat in August after having grown by 415k in July and 397k in June (Chart 1). While Delta could still be a drag on employment growth for another month or two, there is mounting evidence that the daily new case count is close to its peak. Leisure & Hospitality employment growth will regain its prior pace as new Delta cases trend down. This will lead to a resumption of strong monthly payroll reports (500k – 1000k) as we head into the new year. For monetary policy, we calculate that average monthly nonfarm payroll growth of 414k will be sufficient for the Fed to start rate hikes before the end of 2022 (bottom panel). We anticipate that this threshold will easily be met. The Treasury curve will bear-flatten as employment growth improves and the market prices-in an earlier start and quicker pace of Fed rate hikes. Investors should maintain below-benchmark portfolio duration and stay short the 5-year Treasury note versus a duration-matched 2/10 barbell. Feature Table 1Recommended Portfolio Specification

The Delta Drag

The Delta Drag

Table 2Fixed Income Sector Performance

The Delta Drag

The Delta Drag

Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds underperformed the duration-equivalent Treasury index by 5 basis points in August, dragging year-to-date excess returns down to +166 bps. The combination of above-trend economic growth and accommodative monetary policy supports continued positive excess returns for spread product versus Treasuries. At 91 bps, the 3-year/10-year Treasury slope remains steep. This is a strong signal that monetary conditions are accommodative. But despite the positive macro back-drop, investment grade valuations are extremely tight (Chart 2). A recent report looked at what different combinations of Treasury slope and corporate spreads have historically signaled for corporate bond excess returns.1 It shows that tight corporate spreads only correlate with negative excess returns once the 3-year/10-year Treasury slope is below 50 bps. Though we retain a positive view of spread product as a whole, better value can be found outside of the investment grade corporate sector. Specifically, we recommend that investors shift into high-yield corporates, municipal bonds and USD-denominated Emerging Market sovereigns and corporates. We also advise investors to favor long-maturity corporate bonds and those corporate sectors with elevated Duration-Times-Spread.2 Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Delta Drag

The Delta Drag

Table 3BCorporate Sector Risk Vs. Reward*

The Delta Drag

The Delta Drag

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 66 basis points in August, bringing year-to-date excess returns up to +502 bps. A recent report looked at the default expectations that are currently priced into the junk index and considered whether they are likely to be met.3 If we demand an excess spread of 100 bps and assume a 40% recovery rate on defaulted debt, then the High-Yield index embeds an expected default rate of 3.0% (Chart 3). Using a model of the 12-month trailing speculative grade default rate that is based on gross corporate leverage (pre-tax profits over total debt) and C&I lending standards, we estimate that the 12-month default rate will fall to between 2.3% and 2.8%, below what the market currently discounts. Notably, the corporate default rate is tracking at an annualized rate of roughly 1.7% through the first seven months of the year, well below the estimate generated by our macro model. Another recent report looked at the incremental spread pick-up investors can earn by moving out of investment grade corporates and into junk.4 It concluded that the extra spread available in high-yield is worth grabbing and that B-rated bonds look particularly attractive in risk-adjusted terms. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 3 basis points in August, dragging year-to-date excess returns down to -67 bps. The nominal spread between conventional 30-year MBS and equivalent-duration Treasuries tightened 4 bps in August. The spread is wide compared to recent history, but it remains tight compared to the pace of mortgage refinancings (Chart 4). The conventional 30-year MBS option-adjusted spread (OAS) widened 2 bps in August (panel 2), and it is now starting to look attractive compared to other similarly risky spread sectors. The conventional 30-year MBS OAS sits at 38 bps, below the 56 bps offered by Aa-rated corporate bonds but above the 20 bps offered by Aaa-rated consumer ABS and the 35 bps offered by Agency CMBS. In a recent report we looked at MBS performance and valuation across the coupon stack.5 We noted that the higher convexity of high-coupon MBS makes them likely to outperform lower-coupon MBS in a rising yield environment. Higher coupon MBS also have greater OAS than lower coupons. This makes the high-coupon MBS more likely to outperform in a flat bond yield environment as well. Given our view that bond yields will be higher in 6-12 months, we recommend favoring high coupons (4%, 4.5%) over low coupons (2%, 2.5%, 3%) within an overall underweight allocation to Agency MBS. Government-Related: Neutral Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 27 basis points in August, bringing year-to-date excess returns up to +84 bps (Chart 5). Sovereign debt outperformed duration-equivalent Treasuries by 122 bps in August, bringing year-to-date excess returns up to +7 bps. Foreign Agencies outperformed the Treasury benchmark by 8 bps on the month, bringing year-to-date excess returns up to +44 bps. Local Authority bonds outperformed by 9 bps in August, bringing year-to-date excess returns up to +382 bps. Domestic Agency bonds outperformed by 3 bps, bringing year-to-date excess returns up to +30 bps. Supranationals outperformed by 5 bps, bringing year-to-date excess returns up to +31 bps. USD-denominated Emerging Market (EM) Sovereign bonds outperformed US corporates in August and relative valuation between the two sectors is starting to equalize (panel 4). That said, we retain a preference for EM sovereigns over US corporates, particularly the bonds of Russia, Mexico, Saudi Arabia, UAE and Qatar where value remains attractive. A recent report looked at valuation within the investment grade USD-denominated EM corporate space.6 It found that EM corporates are attractively priced relative to US corporate bonds across the entire investment grade credit spectrum. It also found that EM corporates are attractive relative to EM sovereigns within the A and Baa credit tiers. EM sovereigns have the edge in the Aa credit tier. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 9 basis points in August, dragging year-to-date excess returns down to +262 bps (before adjusting for the tax advantage). The economic and policy back-drop remains favorable for municipal bond performance. Trailing 4-quarter net state & local government savings were already positive through the end of Q1 2021 and they received another significant boost in Q2 as funds from the American Rescue Plan were doled out (Chart 6). With state & local government balance sheets in such good shape, we are comfortable moving down in quality within municipal bonds. A move down in quality is especially compelling because of tight Aaa muni valuations relative to Treasuries (top panel). Valuation is more compelling in the lower investment grade credit tiers, especially at the long-end of the curve.7 GO munis in the 12-17 year maturity bucket offer a 5% breakeven tax rate versus corporates with the same credit rating and duration. 12-17 year Revenue munis actually offer a before-tax yield pick-up (panel 2). Finally, high-yield muni spreads are reasonably attractive relative to high-yield corporates, offering a breakeven tax rate of 23% (panel 4). But despite the attractive spread, we recommend only a neutral allocation to high-yield munis versus high-yield corporates as the deep negative convexity of high-yield munis makes them susceptible to extension risk if bond yields rise. Treasury Curve: Buy 2/10 Barbell Versus 5-Year Bullet Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury yields moved higher in August, with the 5-year and 7-year maturities bearing the brunt of the sell-off. The 2-year/10-year Treasury slope steepened 5 bps to end the month at 110 bps. The 5-year/30-year slope flattened 5 bps to end the month at 115 bps. We expect bond yields to be higher in 6-12 months, but we also anticipate that the next significant move higher in bond yields will coincide with curve flattening, not steepening. At 1.93%, the 5-year/5-year forward Treasury yield is not that far below our target fair value range of 2% - 2.25%. In a recent report, we demonstrated that yield curve steepening only occurs when either the Fed is cutting rates or the 5-year/5-year forward yield rises.8 This means that the 2/10 Treasury curve is more likely to flatten than steepen during the next 6-12 months, even as bond yields move higher. Similarly, we observe that the overnight index swap (OIS) curve is priced for the fed funds rate to be 0.21% in one year’s time and 1.47% in five years (Chart 7). The latter rate has 146 bps of upside if it converges all the way back to its 2018 high, but this pales in comparison to the 265 bps of upside in the 12-month forward rate. The yield curve will flatten as the 12-month forward OIS rate converges with the 5-year forward rate (panel 3). Investors should position in yield curve flatteners on a 6-12 month horizon. Specifically, we recommend shorting the 5-year bullet versus a duration-matched 2/10 barbell. TIPS: Neutral Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS performed in line with the duration-equivalent nominal Treasury index in August, leaving year-to-date excess returns unchanged at +578 bps. The 10-year and 5-year/5-year forward TIPS breakeven inflation rates both fell by 7 bps in August. At 2.37%, the 10-year TIPS breakeven inflation rate is near the middle of the 2.3% to 2.5% range that is consistent with inflation expectations being well anchored around the Fed’s target (Chart 8). Meanwhile, at 2.21%, the 5-year/5-year forward TIPS breakeven inflation rate is only just below target (panel 3). With long-dated inflation expectations close to the Fed’s target levels, we see limited upside on a 6-12 month investment horizon. We also see the cost of short-maturity inflation protection falling during the next few months as realized inflation continues to moderate from its current extremely high level. This will lead to some modest steepening of the inflation curve (bottom panel). While the inflation curve has some room to steepen, we don’t see it returning to positive territory. An inverted inflation curve is simply more consistent with the Fed’s Average Inflation Target than a positively sloped one. This is because the Fed’s new framework calls for it to attack its inflation target from above rather than from below. ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 3 basis points in August, bringing year-to-date excess returns up to +40 bps. Aaa-rated ABS outperformed by 2 bps on the month, bringing year-to-date excess returns up to +30 bps. Non-Aaa ABS outperformed by 4 bps, bringing year-to-date excess returns up to +92 bps. The stimulus from last year’s CARES Act led to a significant increase in household savings when individual checks were mailed in April 2020. That excess savings has still not been spent and the most recent round of stimulus checks has only added to the stockpile (Chart 9). The extraordinarily large stock of household savings means that the collateral quality of consumer ABS is also extraordinarily high. Indeed, many households have been using their windfalls to pay down consumer debt (bottom panel). Investors should remain overweight consumer ABS and should also take advantage of the high quality of household balance sheets by moving down the quality spectrum. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 6 basis points in August, bringing year-to-date excess returns up to +193 bps. Aaa Non-Agency CMBS outperformed Treasuries by 10 bps in August, bringing year-to-date excess returns up to +92 bps. Non-Aaa Non-Agency CMBS underperformed Treasuries by 9 bps on the month, dragging year-to-date excess returns down to +529 bps (Chart 10). Though returns have been strong and spreads remain attractive, particularly for lower-rated CMBS, we continue to recommend only a neutral allocation to the sector because of the structurally challenging environment for commercial real estate. Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 4 basis points in August, bringing year-to-date excess returns up to +91 bps. The average index option-adjusted spread held flat on the month. It currently sits at 35 bps (bottom panel). Though Agency CMBS spreads have recovered to well below pre-COVID levels, they still look attractive compared to other similarly risky spread products. Stay overweight. Ryan Swift US Bond Strategist rswift@bcaresearch.com Appendix A: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 12 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 12 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Delta Drag

The Delta Drag

Appendix B: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Footnotes 1 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 2 For ideas on how to increase the average spread of a US bond portfolio please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 3 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 4 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 5 Please see US Bond Strategy Weekly Report, “A New Conundrum”, dated April 20, 2021. 6 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 7 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 8 Please see US Bond Strategy / Global Fixed Income Strategy Weekly Report, “A Bump On The Road To Recovery”, dated July 27, 2021.

Foreword Today we are publishing a charts-only report focused on the S&P 500, Cyclicals/Defensives, Growth/Value, and Small/Large. Many of the charts are self-explanatory; to some we have added a short commentary. The charts cover macro, valuations, fundamentals, technicals, and the uses of cash. Our goal is to equip you with all the data you need to make investment decisions along these style dimensions. We also include performance, valuations, and earnings growth expectations tables for all styles, sectors, industry groups, and industries (GICS 1, 2 and 3). We hope you will find this publication useful. We alternate between Style and Sector chart packs updates on a bi-monthly basis. Overarching Investment Themes Macro Is bad news good news again? Investors are caught in crosscurrents of worries and deteriorating economic data. The Citigroup Economic Surprise index is in negative territory (Chart 1) – yet the US equity market defies gravity. The bad news is good news again, as it gives the Fed cover to keep a loose monetary policy for longer. Tapering: The Fed has broadcast its plans for tapering well in advance, and Fed Chair Jay Powell’s Jackson Hole speech, with its many caveats and uncertain timetable, produced a muted reaction from financial markets. However, investors exhaled with relief, when Powell explicitly separated the decision to taper from the timing of the first rate hike, conditioned on full employment, which is “a long way off”. Covid-19 Delta variant has caught investors off guard: "What does not kill us, mutates and tries again”. While a new wave of infections has dented consumer activity, there are early signs that it is cresting (Chart 2). Delta scare was a key reason for the underperformance of consumer services and cyclical stocks over the summer. Once fears of Delta subside, these groups will bounce back. Chart 1US Economic Data Disappoints

US Economic Data Disappoints

US Economic Data Disappoints

Chart 2Delta Infections Are Cresting

Delta Infections Are Cresting

Delta Infections Are Cresting

Supply chain disruptions are still rampant: Shipping costs have soared again in recent months: After falling below 10 this summer, the number of anchored containers ships waiting to offload in the West Coast ports has spiked again to 40, a level last seen in January 2021. Container freight costs have increased nearly five-fold from pre-pandemic levels (Chart 3). There are also significant backlogs of goods (Chart 4), and inventories have been drawn down to all-time low. It will take time for supply chains to normalize, with most industry participants expecting the situation to improve only in 2022. Chart 3Transportation Costs Have Surged

Transportation Costs Have Surged

Transportation Costs Have Surged

Chart 4Supply Chain Bottlenecks Are Not Abating

Supply Chain Bottlenecks Are Not Abating

Supply Chain Bottlenecks Are Not Abating

Labor shortages: : Companies are still struggling to fill job openings: There are 10 million job openings to slightly over eight million job seekers (Chart 5). That puts upward pressure on wages and increases companies’ costs. Disappointing jobs report: It is confounding, given strong demand for workers, that August payroll grew only by 235,000 jobs. While this low number may have resulted from the Delta hit to service industries, jobs data is volatile, and revisions are common. Next month's report will be a decisive data point for the Fed’s tapering timing decision. Chart 5Plenty Of Job Openings To Fill

Plenty of Job Openings To Fill

Plenty of Job Openings To Fill

Chart 6Inflation Is Broadening

Inflation Is Broadening

Inflation Is Broadening

Companies continue rising prices: Good news for corporate America is that its pricing power remains high, with 45% of companies planning on passing surging labor and supply costs on to consumers. This leads to a broadening of inflation across categories, with even trimmed means significantly overshooting 2% (Chart 6). While pricing power protects against significant margin compression, former peak margins are elusive. Consumer mood has soured: Consumers are well-aware of rising prices and expect inflation to exceed 6.5% within 12 months - high inflation is becoming embedded into consumer behavior and may become a self-fulfilling prophecy. The consumer confidence reading has slumped to a six-month low of 114 from 125 a month earlier. Many consumers have also postponed durable goods and house purchases discouraged by soaring prices and low inventories (Chart 7). Quality balance sheets outperformed: The wall of worries has resulted in strong balance sheet equities outperforming weak ones. This is also consistent with the classical performance of assets during the slowdown stage of the business cycle (Chart 8). Chart 7Consumer Are Discouraged By Prices And Shortages Of Inventory

Consumer Are Discouraged By Prices And Shortages Of Inventory

Consumer Are Discouraged By Prices And Shortages Of Inventory

Chart 8Strong Balance Sheet Companies Outperformed During The Slowdown

Strong Balance Sheet Companies Outperformed During The Slowdown

Strong Balance Sheet Companies Outperformed During The Slowdown

Valuations and Profitability Q2-2021 earnings season was remarkable both in terms of growth delivered (96% yoy%), and earnings surprise (88%). Earnings have grown at a 14% compound rate since 2019: Chart 9Earnings Growth Is Returning To Trend

US Equity Chart Pack

US Equity Chart Pack

Now earnings have returned to trend, and we expect normalization of growth. Analysts expect flat QoQ growth for the next three quarters. These are timid expectations; barring a black swan event, earnings growth is likely to surprise on the upside (Chart 9). Earnings growth will provide the necessary impetus for the US equity markets to move higher, with the driver of returns shifting from multiple expansion to earnings growth and cash disbursements to shareholders. Valuations remain elevated with the S&P 500 trading at 21x forward earnings. However, this level of valuations is more of a speed limit for future gains as opposed to a harbinger of a bear market. Sentiment Buy the dip investor mentality prevails. The S&P 500 has not had a 10% correction for nearly a year. This can be explained by FOMO (fear of missing out), and $2 trillion in excess savings in the US: cash that many retail investors aim to park in US equities. Retail flows into domestic equities have been exceptionally strong (Chart 10). Uses of Cash Share buybacks and other shareholder-friendly activities are on the rise again and are expected to gain steam this year and next. S&P 500 buybacks have increased from $120B reported two months ago to nearly $180B – impressive. This is another driver of returns in addition to earnings growth (Chart 11). Chart 10Retail Investors Buy On Dips

Retail Investors Buy On Dips

Retail Investors Buy On Dips

Chart 11Buybacks Are A Driver Of Returns

Buybacks Are A Driver Of Returns

Buybacks Are A Driver Of Returns

Investment Implications Low for longer: Fed’s dovish stance, Delta scare, and deteriorating economic growth data suggest that rates are likely to remain “low for longer”, and tapering may be postponed till January 2022. S&P 500: We expect US equities to perform well into the balance of the year on the back of an easy fiscal and monetary policy and steady earnings growth. Growth vs Value: Economic growth continues to slow, the Delta variant is still at the forefront of investor worries, and the Fed is dovish: Interest-rate sensitive stocks, such as Growth and Technology sector will continue outperforming. Cyclicals vs Defensives: We expect consumer cyclicals to start performing again once the onset of Delta dissipates, and more people are willing to travel and eat out. We believe that this is imminent and we are watching Delta stats closely. We also believe that parts of the Industrial sector most exposed to restocking of inventories, infrastructure, and construction will perform strongly. Small vs Large: Small is an “out of the gate” asset class, which tends to surge at the first whiff of recovery. Recently, Small started outperforming on the news that the number of new Delta cases is rolling over. Small is cheap relative to Large, and most of the earnings downgrades are already in the price. We are getting more constructive on this asset class. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com S&P 500 Chart 12Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 13Profitability

Profitability

Profitability

Chart 14Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 15Uses Of Cash

Uses Of Cash

Uses Of Cash

Cyclicals Vs Defensives Chart 16Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 17Profitability

Profitability

Profitability

Chart 18Valuation And Technicals

Valuation And Technicals

Valuation And Technicals

Chart 19Uses Of Cash

Uses Of Cash

Uses Of Cash

Growth Vs Value Chart 20Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 21Profitability

Profitability

Profitability

Chart 22Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Small Vs Large Chart 23Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 24Profitability

Profitability

Profitability

Chart 25Valuations And Technicals

Valuations and Technicals

Valuations and Technicals

Chart 26Uses Of Cash

Uses Of Cash

Uses Of Cash

Recommended Allocation . Footnotes

Highlights A trio of ECB hawks raised the prospect of an ECB taper. In the past, the current set of economic conditions in the Euro Area would have prompted the ECB to tighten policy. A potential economic deceleration this fall, the transitory nature of the Eurozone’s inflation spike, and the level of inflation expectation in the region limit the ECB’s ability to taper this week. We expect a one-off return to the pre-Q2 2021 level of asset purchases couched in a very dovish forward guidance. Peripheral bonds and European corporate bonds will outperform German and other core European paper. Stay long European curve steepeners, while buying US curve flatteners. Overweight German Bunds versus US Treasury Notes, on a USD-hedged basis. European productivity will remain structurally hampered compared to that of the US. US real bond yields will rise relative to Europe. Feature Last week, a chorus of ECB Governing Council members raised the idea among investors that the central bank may soon begin to taper its asset purchases, which prompted Bund yields to hit -0.35% on Wednesday. Robert Holzmann of Austria, Klaas Knot of the Netherlands, and Jens Weidmann of Germany all suggested that monetary conditions were too accommodative for the Eurozone and that the ECB needed to remedy this problem. The complaints of this hawkish trio reflect the current environment. In August, the Eurozone HICP reached a 3% annual rate while the preliminary estimate for core CPI clicked in at 1.6%. Meanwhile, July PPI rose to 12.1%. Such robust inflation readings are at odds with the low level of interest rates in the Eurozone, where the yields on European IG credit and 10-year Italian BTPs average a paltry 0.45% (Chart 1). Beyond the level of inflation, its broad geographic nature is an additional source of concern. Headline CPI is accelerating across all the bloc’s nations, and it stands above 2% in 82% of the members’ states. Historically, this kind of inflationary backdrop resulted in either higher interest rates or some tapering of asset purchases, especially when economic activity was also improving in the Eurozone (Chart 2). Chart 1A Gap For The Hawks

A Gap For The Hawks

A Gap For The Hawks

Chart 2In The Past, The ECB Would Have Tightened

In The Past, The ECB Would Have Tightened

In The Past, The ECB Would Have Tightened

Will the ECB listen to its most hawkish members and follow its past script? We do not believe that the Governing Council is about to start a sustained period of decreased bond buying, even if a return to the pre-Q2 2021 pace of buying is likely this fall. Thus, a dovish taper is the most likely outcome of this week’s meeting. The ECB’s Three Constraints The outlook for growth, the temporary nature of the current spike in European inflation, and the low-level of Euro Area inflation expectations limit the ECB’s ability to remove monetary accommodation. First, European economic growth is at its apex and will decelerate over the next six months. Currently, domestic activity as approximated by the Services PMI stands at near a 15-year high of almost 60. Moreover, despite the spike in COVD-19 cases linked to the Delta variant, mobility remains very robust. If anything, the decline in cases in Spain and France should lead to further improvement in mobility (Chart 3). Nonetheless, the recent fall in consumer confidence and the recent US experience, which the European economy usually follows, point to a deceleration in the Services PMI. The case for a decline in manufacturing activity is more pronounced. The European manufacturing sector responds strongly to the fluctuation of the global industrial sector. US consumer spending on durable goods is 21% above its pre-pandemic trend and is beginning to weaken as pent-up demand for such products has been satiated and households shift their spending back toward services. Moreover, the Chinese credit cycle, which leads the Eurozone Manufacturing PMI by nine months, indicates a greater deceleration in the coming quarters, because European exports to China will slow (Chart 4, top and middle panels). In response to these two forces, Europe will not diverge from the deterioration in our Global Activity Nowcast (Chart 4, bottom panel). Chart 3So Far, No Delta Impact

So Far, No Delta Impact

So Far, No Delta Impact

Chart 4The Coming Manufacturing Slowdown

The Coming Manufacturing Slowdown

The Coming Manufacturing Slowdown

Chart 5Abnormal Goods Inflation

Abnormal Goods Inflation

Abnormal Goods Inflation

Second, most evidence still suggests that the current inflation increase will be temporary, despite its violence. To begin with, the spike in inflation remains consigned to the goods sectors, while services inflation stands at 1.1%, in line with the experience of the past 10 years (Chart 5). Even within goods prices, the spike in CPI is limited to sectors facing bottlenecks or linked closely to commodity and shipping prices. As Chart 6 illustrates, the categories experiencing abnormal inflation are directly related to higher energy prices, cars, complex machinery, hotels, and fresh food. Meanwhile, underlying inflation as estimated by our trimmed-mean CPI measure is bottoming, but remains at a very low 0.2% annual rate (Chart 7). Chart 6Inflation Remains A Commodity and Bottleneck Story

The ECB Taper Dilemma

The ECB Taper Dilemma

In the same vein, the surge in Selling Price Expectations of the European Commission Business Survey is a function of commodity inflation (Chart 8). In other words, companies feel they can increase their selling prices, because natural resource prices have spiked. However, inflation across many commodities is currently peaking, which suggests that Selling Price Expectations will soon do so as well. Moreover, this process indicates that headline inflation should hit its summit by year end, because Selling Price Expectations are a coincident indicator of inflation (Chart 8, bottom panel). Chart 7Narrow Inflation

Narrow Inflation

Narrow Inflation

Chart 8Rising Selling Prices And Commodities

Rising Selling Prices And Commodities

Rising Selling Prices And Commodities

A wage-inflation spiral also remains far away. Historically, rapidly accelerating wage growth marked periods of elevated inflation. Despite current fears, such a development is not taking place in the Eurozone. For the whole bloc, negotiated wages are growing at a modest 1.7% annual rate (Chart 9). Even in Germany, negotiated wages are only increasing at the same rate. While some labor shortages have been reported, total hours worked remain below the equilibrium level based on the Euro Area demographic profile (Chart 9, bottom panel). Furthermore, the past ten years reveal that labor shortages only caused stronger salary growth with a multi-year delay. Third, the market doubts the credibility of the ECB when it comes to achieving a 2% inflation target. So far, survey-based inflation expectations remain below 2% at all tenors (Chart 10, top panel). The same is true of market-based measures, which are still lower than the levels that prevailed before the sovereign debt crisis of the past decade (Chart 10, bottom panel). Chart 9No Wages/Inflation Spiral

No Wages/Inflation Spiral

No Wages/Inflation Spiral

Chart 10The ECB's Inflation Mandate Is Not Yet Credible

The ECB's Inflation Mandate Is Not Yet Credible

The ECB's Inflation Mandate Is Not Yet Credible

Bottom Line: Risks to growth over the winter, the transitory nature of the recent inflation shock, and inflation expectations that remain significantly below target are constraints limitating the ability of the ECB to announce a true tapering of its asset purchases this Thursday. A Dovish Taper? Considering the current set of conditions prevailing in the Eurozone, we expect the ECB to announce a return to the pace of asset purchases that existed prior to Q2 2021. However, the Governing Council (GC) will go out of its way to issue clear forward guidance that strongly indicates this is not the beginning of a taper campaign. Instead, the GC will hint at the transmutation of a large proportion of the PEPP monthly buying into the PSPP after March 2022. The inflation target change enacted at the conclusion of the ECB’s strategy review in July limits the central bank’s ability to go back to its old rule book and tighten policy at the first hint of inflation. First, the ECB must believe that inflation will overshoot 2% on a durable basis, which will necessitate an upgrade to its long-term inflation forecast above the target. Too many members of the GC do not share this view, which makes it unlikely that inflation forecasts will rise this much this week. Moreover, inflation expectations are also too low to warn of a meaningful change in the behavior of European economic agents, especially if the current spike in inflation proves to be transitory. Another problem for the ECB is the Fed. If the ECB were to announce a durable tapering of its asset purchase this week, it would be doing so ahead of the Fed. The GC fears that this action would put considerable upward pressure on EUR/USD, which would create a grave deflationary tendency in the Eurozone (Chart 11). Despite these shackles, the ECB will also acknowledge that the current emergency pace of asset purchases is no longer warranted. Starting Q2 2021, the ECB increased its average monthly purchase from EUR80 billion in the August 2020 to March 2021 period, to EUR95 billion since April 2021 (Chart 12). However, these increased purchases followed a 0.1% GDP contraction in Q1 in the wake of a spike in COVID-19 cases and deaths, which prompted a large reduction in mobility. Moreover, the larger bond buying also followed large increases in bond yields across the main economies of the continent, a rise which, if it had been left unchecked, would have exacerbated the economic malaise. Chart 11The ECB Fears A Strong Euro

The ECB Fears A Strong Euro

The ECB Fears A Strong Euro

Chart 12Normalizing Purchases

The ECB Taper Dilemma

The ECB Taper Dilemma

None of these factors are still present. The increasing level of vaccination has dulled the economic impact of the third wave of infection. The economy is expanding robustly and, even if it slows in the months ahead, growth will remain well above trend. Crucially, financial conditions are much more generous than in the first half of the year, with a euro that trades 4% below its January peak and with yields in the bloc’s four largest economies 25 to 45 basis points below their spring peaks. Bottom Line: In response to the aforementioned crosscurrents, we anticipate the ECB to announce a return of its monthly asset purchases to the level that prevailed in the August 2020 to March 2021 period. However, the GC will also clearly indicate, as it did last March, that this policy shift is a one-off, and that investors must not anticipate any further curtailment of asset purchases over the next six months. To reinforce this guidance, we expect the ECB’s inflation forecast to show a return of HICP below 2% by the end of 2023. The GC might also hint at the roll-over of the PEPP program into the PSPP after March 2022. Investment Implications An ECB that conducts a dovish taper on Thursday will support our main fixed-income themes in Europe. First, it will remain a tailwind behind an overweight position in peripheral government bonds versus German bonds. The combination of continued purchases of EUR80 billion a month of bonds over the foreseeable future, above-trend growth, and the fiscal risk mutualization from the NGEU and REACT EU programs means that investors can continue to safely pocket the yield premium offered by BTPs and BONOs. Moreover, our geopolitical strategists expect a left-wing coalition to govern Germany after the September 26 election, which will limit the pressures to tighten budgets in the periphery over the coming years. Chart 13European Corporates Remain Attractive

European Corporates Remain Attractive

European Corporates Remain Attractive

Second, continued liquidity injections by the ECB are also consistent with a preference for European corporate credit over government securities, especially in Germany, France, and the Netherlands. European breakeven spreads for IG and high-yield debts are in the 18th and 13th percentile rank, respectively (Chart 13). Easy monetary conditions and above-trend growth will facilitate further yield-seeking behavior in the Eurozone. This process will allow these securities to offer continued excess returns over at least the next six months. Third, we hold on to our box trade of being long Eurozone curve steepeners and long US curve flatteners. In our base case scenario, the Fed will soon indicate the beginning of its tapering campaign and will be on track to raise rates by early 2023, while the ECB will still conduct a very easy monetary policy. In this context, the US yield curve will flatten relative to the European one, driven by a more rapid increase at the short end of the curve. Chart 14Still Favor Bunds Over T-Notes

The ECB Taper Dilemma

The ECB Taper Dilemma

Finally, in a global bond portfolio, it still makes sense to overweight German Bunds (hedged into USD) relative to US Treasury Notes. Bunds display a significantly lower yield beta than their US counterparts, which creates an attractive defensive feature in an environment in which global yields are likely to rise. Moreover, as the model in Chart 14 highlights, the US/German 10-year yield spread is roughly 50bps below an equilibrium estimate based on relative inflation, unemployment and policy rates, and the size of the Fed and ECB balance sheets. US inflation is likely to remain perkier than that of Europe over the coming quarters, and the US unemployment rate will decline faster as well. Additionally, in the unlikely scenario that the Fed declines to taper its purchases this year, but the ECB does, inflation expectations will rise in the US relative to the Euro Area, which will put upward pressure on yield spreads. Bottom Line: A dovish ECB taper, whereby the GC executes a one-off adjustment in asset purchases with an easy forward guidance, will support our overweight in peripheral government bonds relative to bunds, our preference for European corporate credit relative to government paper, our Europe / US box trade, and BCA’s underweight in Treasurys relative to Bunds. Europe’s Productivity Deficit Is Not Over Compared to the US, GDP growth in the Eurozone has been trending lower since the introduction of the euro in 1999. While a weaker demographic profile has hurt Europe, so has slower productivity growth. Going forward, the gap between European and US productivity growth will somewhat narrow compared to last decade, but it will still favor the US. The cross-Atlantic gap in output per hour growth between has a cyclical and a structural component. The cyclical element is set to ebb. Last decade, the Eurozone suffered a double-dip recession, as the European sovereign debt crisis raged. As a result, capex and debt accumulation in Europe lagged that of the US, which hurt demand and, thus, output-per-hour worked (Chart 15, top panel). Going forward, the European debt crisis has been addressed, the ECB has demonstrated its willingness to do “whatever it takes” to support the monetary union and both the European Commission and the German government have thrown their full weight behind the integrity of Europe, even if it means bailing out their profligate southern neighbors. Despite this positive, some structural headwinds will continue to handicap European productivity. Since 2000, total factor productivity in the major Euro Area economies has lagged that of the US (Chart 15, bottom panel). Many factors suggest this will not change: Chart 15Europe’s Productivity Deficit

The ECB Taper Dilemma

The ECB Taper Dilemma

The Eurozone’s big four economies continue to linger well behind the US in terms of ICT investment, which in recent decades has been a crucial driver of productivity. R&D represents a significantly lower share of GDP in the Eurozone than it does in the US (Chart 16). More investment in intangible assets has been linked to higher productivity growth. Additionally, Ortega-Argilés et al. have shown that EU companies do not convert R&D into productivity gains as well as US businesses do, because they generate lower return on investments.1 Confirming this insight, an empirical study using microdata on R&D spending for EU and US firms highlights that both R&D intensity and productivity are lower for EU firms than for their US counterparts.2 For a 10% increase in R&D intensity, US businesses generated a 2.7% increase in productivity, while EU firms enjoyed a much smaller 1% gain. The gap is larger for high-tech companies, where the same rise in R&D intensity produced a 3.3% productivity gain in the US, but only a 1.2% one in the EU. The European economy remains much more fragmented than that of the US, and the greater prevalence of small firms in the Euro Area results in a less efficient use of the human and capital stocks. Finally, the low rate of investments in recent years has caused the European capital stock to age faster than that of the US. An older pool of assets is further away from the technological frontier and thus weighs on TFP and overall labor productivity (Chart 17). Chart 16Lagging European R&D

The ECB Taper Dilemma

The ECB Taper Dilemma

Chart 17The Ageing European Capital Stock

The Ageing European Capital Stock

The Ageing European Capital Stock

Notwithstanding cyclical fluctuations related to the global debt cycle, the Eurozone profit margins and RoEs will not converge meaningfully toward US levels on a structural basis because of this productivity problem. Europe’s lower industry concentration ratios, lower markups, and greater share of output absorbed by wages will only accentuate this problem. Chart 18TIPS Yields Vs Real Bunds

TIPS Yields Vs Real Bunds

TIPS Yields Vs Real Bunds

As a result of the lower trend growth rate caused by lower productivity and its inferior return on invested capital, Europe’s R-Star is unlikely to catch up meaningfully to US levels. Consequently, the gap between US and Germany real rates will remain wide and will drive the increase in US yields relative to those of Germany, as the Fed begins to tighten policy while the ECB stands pat (Chart 18). Bottom Line: Europe’s productivity deficit is not the only consequence of last decade’s sovereign debt crisis. Thus, the Euro Area’s potential GDP growth and return on invested capital will lingers behind those of the US. As a corollary, the Eurozone’s R-star is well below that of the US. Hence, we expect higher real rates to drive the increase in US yields over Germany as the Fed tightens policy ahead of the ECB. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Footnotes 1R. Ortega-Argilés, M. Piva, and M. Vivarelli, “The Transatlantic Productivity Gap: Is R&D the Main Culprit?,” Canadian Journal of Economics 47.4 (2014), pp. 1342-71. 2D. Castellani, M. Piva, T. Schubert, and M. Vivarelli, “The Productivity Impact of R&D Investment: A Comparison between the EU and the US,” IZA Discussion Papers 9937 (2016). Tactical Recommendations

The ECB Taper Dilemma

The ECB Taper Dilemma

Cyclical Recommendations

The ECB Taper Dilemma

The ECB Taper Dilemma

Structural Recommendations

The ECB Taper Dilemma

The ECB Taper Dilemma

Closed Trades

The ECB Taper Dilemma

The ECB Taper Dilemma

Currency Performance Fixed Income Performance Equity Performance

Highlights Economy – Goldilocks remains our base-case macro backdrop for the next twelve months: The transitory inflation narrative is still intact, despite persistently high consumer price increases, suggesting that the economy will not overheat. The Delta wave has roiled many communities, but COVID is unlikely to spark a growth outage unless a vaccine-resistant variant emerges. Markets – Above-trend growth and extraordinarily accommodative monetary policy is a sweet spot for risk assets: As long as the Fed’s novel policy of adding monetary stimulus to an economy growing way above trend doesn’t give rise to unnervingly high inflation, the combination will be conducive to continued equity and credit outperformance. Strategy – Continue to overweight risk assets within multi-asset portfolios: There’s more to investment returns than the state of the business, credit and monetary policy cycles but they make a powerful case against turning defensive in the near term. Feature We had several virtual meetings with clients in August and inflation, the Fed and the growth outlook were frequently recurring themes. In this week’s report, we share some of the most common questions, along with our take on them, so that all clients can see what we’ve been discussing with their peers. In the interest of space, we confine the discussion to our base-case scenarios, but future outcomes appear to be even more uncertain than they normally are against a backdrop of unprecedented policy settings. We advise investors to remain vigilant and be prepared to hold positions for shorter-than-usual durations in the event circumstances change. Inflation prints remain high, pressuring the Fed’s transitory narrative. What will happen to markets if investors reject it? Chart 1Losing Steam?

Losing Steam?

Losing Steam?

Inflation prints do remain high, with headline CPI rising 0.5% month-over-month and 5.3% year-over-year in July and core CPI rising 0.3% and 4.2%. Both series modestly exceeded expectations, though they recorded their smallest sequential gains since February and their year-over-year increases came in just below the peaks recorded in June (Chart 1). It is possible that consumer price increases have begun to decelerate though it will take more data to confirm the existence of a new trend. Reports of continued bottlenecks driven by component shortages, transport challenges and the Delta infection wave suggest that even if the factors that have pushed inflation higher are beginning to abate, they may linger in some form for longer than initially expected. The transitory narrative remains intact, however. Drilling into the components of the elevated core CPI reveals that a handful of categories that have been particularly impacted by the pandemic are exerting outsized influence over the index. When we published the initial version of Table 1 in late May, nine categories powered April’s reported core inflation. This time there are eight, as the five shaded components have come off the boil and the four components shown in an indented font have newly begun to run hot. Table 1Temporary Irritants

Discussing Inflation, Growth And Market Implications

Discussing Inflation, Growth And Market Implications

Excepting historically volatile recreational services and water, sewer and trash services, which have been increasing in price far faster than other goods and services for a while, the hot categories’ moves have been extreme relative to their own history. Unless their spaces have undergone lasting structural changes, we expect their two-plus standard deviation moves will not be sustained. The biggest outliers, lodging and new vehicles, can be explained entirely by the pandemic and once hotels are able to return to full capacity and an end to the semiconductor shortage allows automakers to resume normal production levels, they will come back to earth. The turnover among the outliers supports the transitory narrative, as price spikes in categories that have long lagged the overall basket, like airfares and used cars, or have experienced long deflationary skids, like furniture and bedding, appear to have been fleeting. Chart 2Back To The Early Nineties

Back To The Early Nineties

Back To The Early Nineties

Markets would experience considerable disruption if investors became convinced that elevated inflation readings were not transitory. Bond yields would rise sharply; the dollar would weaken, stoking further price increases; and the technology sector would come under pressure, threatening the S&P 500. Worst of all, the Fed would be forced to begin hiking the fed funds rate sooner than expected, on its way to setting it at a higher terminal level than expected, sending rates higher across all maturities and weighing on equities generally. The sizable potential market impacts have us monitoring inflation closely, even if the inflation debate won’t likely be resolved until we have several more monthly data points. So you’re watching inflation closely, but you’re not all that worried about it? That’s the gist of it, yes. We’re watchful but not worried. Part of the reason that respective year-over-year core and headline CPI prints over 4% and 5% give everyone such a start is that inflation hasn’t been so high since the beginning of the nineties (Chart 2). But the structural factors that have helped keep inflation in check for decades didn’t suddenly disappear when the pandemic arrived. While BCA’s house view holds that investors are complacent about inflation’s longer-run trajectory, we expect that it will take a few years for prices to move sustainably higher. Table 2Inflation Checklist

Discussing Inflation, Growth And Market Implications

Discussing Inflation, Growth And Market Implications

We developed our inflation checklist to keep tabs on when inflation is poised to rise enough to impact monetary policy and provoke a market inflection. We check the same three boxes that we have in our previous reviews: Labor demand is still red-hot, year-over-year changes in marquee inflation indexes are still well above the Fed’s target and BCA’s pipeline inflation indicator remains very elevated (Table 2). Wages have not yet broken out in response to the worker shortage, however (Chart 3), and it is as if idle workers are abstaining from working rather than using their leverage to command higher wages. The more refined trimmed-mean measures of the CPI and the PCE Index remain relatively well behaved (Chart 4). Chart 3Wages Have Risen, But They Haven't Broken Out Yet

Wages Have Risen, But They Haven't Broken Out Yet

Wages Have Risen, But They Haven't Broken Out Yet

Chart 4More Refined Inflation Measures Continue To Lag Their Marquee Peers

More Refined Inflation Measures Continue To Lag Their Marquee Peers

More Refined Inflation Measures Continue To Lag Their Marquee Peers

Even if our pipeline inflation indicator has crested, it remains at an extremely high level consistent with above-target consumer price gains (Chart 5). As measured by the DXY Index, the dollar has twice bounced convincingly off support at 90 this year, helping to keep imports from adding fuel to the fire. Core consumer prices in the Eurozone and China are only rising a little more than 1% annually in any event, so the two largest economies outside the US are not yet exporting inflation stateside (Chart 6). Chart 5Inflation Pressures May Finally Be Easing

Inflation Pressures May Finally Be Easing

Inflation Pressures May Finally Be Easing

Chart 6Eurozone Prices Are Rising, But They're Not Yet Elevated

Eurozone Prices Are Rising, But They're Not Yet Elevated

Eurozone Prices Are Rising, But They're Not Yet Elevated

If we had to pick just one indicator to determine whether inflation will become problematic, it would be the shape of the inflation expectations curve. High inflation becomes self-sustaining when economic actors – workers, businesses, consumers and lenders – begin to expect it will persist into the future and change their behavior to align with their expectations. When inflation is expected to be high over the long term, individual workers or their unions insist on higher wages to maintain purchasing power, businesses at all points of the supply chain demand higher prices to protect their margins, consumers accelerate their big-ticket purchase decisions to get the most bang for their buck and lenders require higher nominal pro forma returns. The resulting feedback loops help inflation become entrenched in the same way that expectations of falling prices have paved the way for a deflationary mindset to grip Japan. As long as investors (Table 3) and households (Chart 7) expect inflation to decelerate from the short term to the intermediate term, and again from the intermediate term to the long term, the inflation genie has not gotten out of the bottle. Table 3Investors' Inflation Expectations Curve Is Inverted, ...

Discussing Inflation, Growth And Market Implications

Discussing Inflation, Growth And Market Implications

Chart 7... And So Is Consumers'

... And So Is Consumers'

... And So Is Consumers'