United States

In this Sector Insight report, we come back to the issue of “how much inflation is too much” for equities. The short answer is – equities don’t mind inflation as long as the Fed does not mind it either. Chart 1 shows historical analysis of forward SPX returns (both real and nominal) using different inflation ranges as a starting point. Empirically, CPI prints of below 3% do not weigh on market performance. However, once inflation rises above the 3-4% range, it causes a notable slowdown in returns, and above the 4% mark, it results into negative expected forward returns. Chart 2 is a scatterplot of trailing PE multiples vs core CPI prints. This chart confirms our initial conclusion that an inflation sweet spot for the equity market is around 2-3% core CPI range: this is the range where equity multiples expand the most. It is also clear from the chart that any higher core CPI values become a headwind for equities. The implication is that the negative forward expected return that we showed on Chart 1 comes from the multiple contraction. Chart 1Moderate Inflation Does Not Have An Adverse Effect On The Performance Of Equities

How Much Is Too Much?

How Much Is Too Much?

Chart 2High Levels Of Inflation Are Associated With Multiple Contraction

How Much Is Too Much?

How Much Is Too Much?

Equities are a real asset, and rising inflation does not have a negative effect on the earnings, as most companies are able to pass cost increases to their customers, and strong earnings growth translates into robust equity returns. Inflation is a concern for equity investors only from one angle: higher inflation may provoke the Fed to raise rates, and higher rates do have an adverse effect on the performance of equities. Bottom Line: Our view remains that inflation surge was transitory, but we do believe that the inflation will stay elevated for a while. Yet, if it does not exceed the 3% mark, there will be no negative repercussions for equities if the Fed stays patient.

Highlights US Treasuries: US Treasury yields are rising once again, in response to typical drivers – less dovish Fed commentary and upside growth surprises. The spread of the Delta variant in the US represents a potential near-term roadblock to additional yield increases, but the recent slowing of new cases in the UK and Europe is a positive sign that the US can see a similar result and avoid a major economic hit. Stay below-benchmark on US duration exposure. UK: The Bank of England is starting to prepare the markets for less accommodative monetary policy, with the UK economy holding up well as its Delta variant surge is losing momentum. UK Gilt yields are vulnerable to a hawkish repricing with only 48bps of rate hikes discounted by the end of 2024. Stay below-benchmark on UK duration exposure, and downgrade Gilts to underweight in global bond portfolios. A New Turning Point For Global Bond Yields? After seeing steady declines since the peak in late March that took the yield down to an intraday 2021 low of 1.13% last week, the 10-year US Treasury experienced a rebound back to 1.30% in a span of just three days. Yields in typically “high-beta” countries like Canada and Australia also saw significant increases. There were two main triggers for the pickup in US yields. Firstly, a speech from Fed Vice-Chair Richard Clarida was interpreted hawkishly, as he stated that he expects the conditions necessary for the Fed to begin lifting rates would be met by the end of 2022. Secondly, a better-than-expected July employment report confirmed the strength of the US labor market already evident in booming demand indicators like job openings. A third potential cause of the trough in yields can be found outside the US in the increasingly positive news on the spread of the Delta variant coming out of the UK. We would argue that the more relevant turning point for global bond yields in 2021 was not the late March peak in the US, but the mid-May peak in non-US developed market yields. The 10-year UK Gilt yield reached its 2021 apex on May 13, just as the spread of the Delta variant was starting to push UK COVID-19 case numbers sharply higher – despite the high vaccination rate in that country (Chart of the Week). This raised the fears that the “reopening boom” could stall, not only in the UK but other major economies, at a time when global growth momentum was already starting to cool off from the overheated pace in the first half of the year. Chart of the WeekThe "Delta Rally" In Bond Markets Is Fading

The 'Delta Rally' In Bond Markets Is Fading

The 'Delta Rally' In Bond Markets Is Fading

The Delta variant wave continues to wash over the US, although primarily in regions with lower vaccination rates. There was little sign of any impact from the variant in the July US jobs data with just over one million new jobs added (including revisions to prior months) and the unemployment rate falling one-half of a percentage point to 5.4%, the lowest level since March 2020 (Chart 2). However, we will need to see more economic data from July and August to confirm that this latest wave is not having a material impact on the broad US economy beyond the regions with lower vaccination rates. New COVID-19 cases in the UK peaked in mid-July, and are rolling over in continental Europe, with relatively low hospitalization rates – a hopeful sign that the US Delta spread could also soon begin to lose momentum. We continue to believe that steady improvements in the US labor market will be the driver of higher US bond yields over at least the next 6-12 months, as falling unemployment will embolden the Fed to begin tapering asset purchases and, eventually, begin rate hikes towards the end of 2022. The technical backdrop for Treasuries has become less of a headwind to higher yields, with the 10-year yield falling back to its 200-day moving average and speculators closing a lot of short positioning in Treasury futures (Chart 3). If the US can follow the more positive news from across the Atlantic with regards to the spread of the Delta variant, this would remove another impediment to higher US bond yields. Chart 2Steady Progress Towards The Fed's Employment Goals

Steady Progress Towards The Fed's Employment Goals

Steady Progress Towards The Fed's Employment Goals

Bottom Line: US Treasury yields are rising once again, in response to typical drivers – less dovish Fed commentary and upside growth surprises. Chart 3Technical Backdrop Less Of A Headwind To Higher US Yields

Technical Backdrop Less Of A Headwind To Higher US Yields

Technical Backdrop Less Of A Headwind To Higher US Yields

The surge in Delta variant cases represents a potential near-term roadblock to additional yield increases, but the recent slowing of new cases in the UK and Europe may be a positive sign that the US will avoid a major economic hit. Stay below-benchmark on US duration exposure. A Gilt-Bearish Shift In Tone From The Bank Of England Chart 4Pressures Building On The BoE To Dial Back Stimulus

Pressures Building On The BoE To Dial Back Stimulus

Pressures Building On The BoE To Dial Back Stimulus

BCA Research’s Global Fixed Income Strategy has had the UK on “downgrade watch” over the past few months. Improving growth momentum and recovering inflation have raised the risks of a more hawkish turn by the Bank of England (BoE), as evidenced by the elevated reading from our UK Central Bank Monitor (Chart 4). At the same time, the spread of the Delta variant injected a note of caution into an otherwise positive UK economic story. We now think it is time to move from “downgrade watch” to a full downgrade of our current neutral stance on UK Gilts. The BoE left its policy settings unchanged at last week’s policy meeting, but did provide strong indications that some removal of monetary accommodation would soon be necessary. The central bank noted that the UK economy was recovering from the pandemic shock at a faster-than-expected pace. In the August Monetary Policy Report (MPR) also released last week, the BoE maintained its 2021 real GDP growth forecast at 7.25% while slightly raising its 2022 growth estimate to 6%. UK GDP is now projected to fully recover to the pre-COVID level by the end of 2021. More importantly, the projections for the unemployment rate were lowered substantially. The central bank no longer expects much of an impact on unemployment when the UK government’s job-protecting furlough scheme expires in September. The BoE now expects unemployment to peak at 5.1% in Q3/2021 (Chart 5), a big change from the 6% projection in the May MPR, with the central bank noting that job vacancies are already back to pre-pandemic levels. The unemployment rate is projected to reach 4.25% in both 2022 and 2023. Chart 5Major Changes To The BoE's Forecasts

Major Changes To The BoE's Forecasts

Major Changes To The BoE's Forecasts

The BoE baseline forecast now calls for UK headline CPI inflation to see a temporary surge to 4% in Q4/2021 – a significant change from the 2.5% peak in inflation projected in the May MPR - before returning back to close to 2% over the next two years. Yet the minutes of last week’s policy meeting noted that the medium-term risks surrounding inflation were “two-way”, a message that sounds a bit more concerning compared to the benign 2022/23 inflation projections. The BoE is now running the risk of underestimating how long the UK inflation uptrend can persist and force increases in interest rates – perhaps beginning as soon as mid-2022 – given the multiple factors that are pushing up inflation. A modest growth hit from the Delta variant The daily number of new cases has fallen by nearly one-half since the peak on July 20th, according to the Oxford University data (Chart 6). Hospitalizations are also rolling over at a peak that would be one-quarter the size of the January peak. If these trends continue, this latest wave of COVID will not have a lasting negative impact on the economy that would dampen inflation pressures. The modest dip in the UK manufacturing and services PMIs in June and July, when cases were rising, supports this conclusion. Accelerating wage growth UK job vacancies are now higher than the pre-pandemic peak, while the BoE’s Agents’ Survey of companies reports an increasing number of firms reporting recruitment difficulties across a broader range of industries (Chart 7). The job market frictions are similar to the dynamics currently at play in the US, where labor demand is booming but firms have struggled to fill openings because government pandemic support programs have dampened labor market participation. Chart 6The Biggest Threat To The Dovish BoE Stance

The Biggest Threat To The Dovish BoE Stance

The Biggest Threat To The Dovish BoE Stance

Chart 7Good Help Is Hard To Find In The UK

Good Help Is Hard To Find In The UK

Good Help Is Hard To Find In The UK

The BoE noted in the August MPR that its forecasts include the impact of labor market frictions that have temporarily raised the medium-term equilibrium rate of unemployment during the pandemic, resulting in a surge in wage growth. However, this effect is expected to fade as the economy normalizes and government support programs expire. For example, the BoE estimates that the UK government’s job retention “furlough” scheme, which pays a reduced wage to workers who cannot work because of COVID economic restrictions and which expires in September, has acted to dampen measured wage growth over the past year. At the same time, compositional effects, with pandemic job losses being skewed towards lower-paying roles, have had a far greater impact in lifting wage growth. The BoE estimates that the “underlying” pace of wage growth, excluding pandemic effects, is only 3.3% compared to the reported 7.2%, but is expected to rise towards 4.5% in Q3 as the labor market recovers. Yet if the employment frictions do not fade as rapidly as the BoE expects, perhaps due to persistent skills mismatches for existing job openings, then the inflationary pressures emanating from the UK jobs market may cause UK inflation to stay elevated for longer than the BoE is projecting. Continued recovery from the initial COVID shock Chart 8Recovering From The COVID Recession

Recovering From The COVID Recession

Recovering From The COVID Recession

The BoE now expects UK real GDP to return to its pre-pandemic level in Q4 of this year (Chart 8). Much of the recovery in activity seen so far has been in services as pandemic restrictions have been lifted. Looking forward, consumer spending will be boosted by improving growth momentum in employment and incomes, further underpinned by a high levels of household savings accumulated during the pandemic. Business investment is also expected recover, given the robust reading from the BoE Agents’ Survey of investment intentions (bottom panel). The twin engines of consumption and investment will be enough to keep the UK economy growing at an above-trend pace in 2022, even with a modest expected drag from fiscal policy, which should help maintain some of the current cyclical inflationary pressures. Rising house prices UK house prices are experiencing another sharp uptick, with the Nationwide index up 10.3% year-over-year in Q2 (Chart 9). Demand for homes has been boosted by the UK government’s holiday on stamp duty, or housing transaction taxes, which began last year as a form of pandemic economic support. Housing transactions spiked in June as demand surged ahead of the expiry of the stamp duty holiday last month, and some payback is likely in the near-term. Yet UK housing demand has also been supported by the same factors boosting house prices in most developed economies - low interest rates, high household savings available for down payments and the increased need for space for those choosing to work from home. UK house price inflation thus could remain higher for longer than the BoE expects. Chart 9Is This House Price Surge 'Transitory' Or Policy Driven?

Is This House Price Surge 'Transitory' Or Policy Driven?

Is This House Price Surge 'Transitory' Or Policy Driven?

Supply Chain Bottlenecks The BoE noted in the August MPR that overall UK import prices have risen faster than expected, especially with the British pound higher on a year-over-year basis. UK firms have faced rising input costs because of disruption to global supply chains from the pandemic. For example, the annual growth rate of import prices for manufactured components rose by 12.1% in May, a sharp contrast to the -5.4% deflation of consumer goods prices (Chart 10). The BoE projects UK overall import price inflation to turn negative in 2022 and 2023, a big part of its slowing inflation forecast. Some decrease is inevitable as price momentum in oil and other commodities cools from overheated levels seen in 2021. However, supply chain disruptions are a global phenomenon already persisting for longer than expected in other countries and could linger into 2022 if global growth stays above trend - potentially causing UK import price inflation to once again exceed the BoE’s expectations. Summing it all up, the pressure is clearly building on the BoE to dial back the massive monetary easing put in place last year in response to the pandemic. Not only is the economy now recovering far more rapidly than the BoE had been projecting, with inflation set to peak at a higher level, but there are other indications that monetary conditions may now be too loose like accelerating house prices. There are numerous upside risks to the BoE’s benign post-2021 inflation forecasts, especially with the central bank also projecting the UK to have a positive output gap in 2022 and 2023 (Chart 11). Chart 10BoE Betting On Waning Global Supply Bottlenecks

BoE Betting On Waning Global Supply Bottlenecks

BoE Betting On Waning Global Supply Bottlenecks

Markets are not expecting much from the BoE in terms of interest rate increases. While the UK overnight index swap (OIS) curve is now discounting an initial 25bp rate hike in August 2022, only one other 25bp increase is expected by the end of 2024 (Table 1). Chart 11Domestic Price Pressures On The Rise

Domestic Price Pressures On The Rise

Domestic Price Pressures On The Rise

The BoE has not been a very active central bank since the 2008 financial crisis, never raising the Bank Rate above 0.75% over that time, thus the markets now seem conditioned to think that the BoE will continue to do very little in the future. Table 1Markets Expect The BoE To Hike Before The Fed

The UK Leads The Way

The UK Leads The Way

Chart 12Markets Expect Persistent Negative UK Real Rates

The UK Leads The Way

The UK Leads The Way

That is evident when you look at longer-dated OIS rates compared to forward inflation rates from the UK CPI swap curve. The combined message from those markets is that the BoE is expected to maintain deeply negative real interest rates for at least the next decade, a major reason why the UK has persistently negative real bond yields (Chart 12). A lower equilibrium real interest rate (i.e. “r-star”) is consistent with the declining trend in the OECD’s estimate of UK potential real GDP growth over the past 20 years (Chart 13). Yet it is a stretch to think that the neutral UK real interest rate is now negative, especially given how rapidly UK growth and inflation have snapped back from the 2020 COVID recession. UK interest rate markets are highly vulnerable to any hawkish shift by the BoE – and outcome that the current growth and inflation dynamics suggest is increasingly likely over the next 6-12 months. The BoE has already started to process of dialing back monetary accommodation by slowing the pace of asset purchases in its quantitative easing (QE) program (Chart 14). While no decision on additional tapering was made last week, the BoE did dedicate three pages of the August MPR to a detailed discussion on how the future size of the BoE’s balance sheet would likely be reduced if the BoE were to begin raising interest rates. There has also been some political pressure on the UK to dial back QE, with the Chair of the Economic Affairs Committee in the UK House of Lords saying that the BoE was “addicted” to QE last month. BoE Governor Andrew Bailey has previously stated that he viewed QE as a regular part of a central banker’s toolkit, to be used opportunistically during periods of deep economic or financial market stress. That made sense in 2020 during the height of the pandemic, but is no longer the case now. Chart 13UK R-Star Is Still Positive

UK R-Star Is Still Positive

UK R-Star Is Still Positive

We anticipate that the BoE will end the current QE program sometime in the next six months, with an initial 25bp rate hike occurring sometime in mid-2022. Chart 14UK QE: Expect More Tapering

UK QE: Expect More Tapering

UK QE: Expect More Tapering

This would be a faster pace of tapering, with a quicker liftoff, than the Fed, although we expect the Fed to eventually raise rates by more than the BoE in the next interest rate cycle. Investment Conclusions Given our expectation that the BoE is starting to prepare the markets for an unwind of its pandemic policy settings, we come to the following fixed income and currency investment conclusions (Chart 15): Chart 15Summarizing Our UK Fixed Income Recommendations

Summarizing Our UK Fixed Income Recommendations

Summarizing Our UK Fixed Income Recommendations

Chart 16A More Hawkish BoE Would Benefit The Pound

A More Hawkish BoE Would Benefit The Pound

A More Hawkish BoE Would Benefit The Pound

Duration: Maintain a below-benchmark duration stance within dedicated UK bond portfolios, with too few rate hikes discounted Country Allocation: Downgrade UK Gilts to underweight in global bond portfolios Yield Curve: On a tactical (0-6 months) basis, the UK Gilt curve may re-steepen as UK and global growth stays resilient, but a more hawkish BoE will eventually result in a flatter Gilt curve Inflation-Linked: Inflation breakevens on UK index-linked Gilts are already quite elevated and are overvalued on our fair value models, while real yields are at deeply negative levels that are conditioned on a continually dovish BoE – a combination that suggests an underweight stance on UK linkers is appropriate. Corporate Credit: Stay neutral on a tactical basis, as solid UK growth will offset the impact of a shift to a less dovish BoE. Currency: Our currency strategists are positive on the British pound - which is undervalued on their models (Chart 16) - over the medium-term, with the BoE seemingly on a path to begin tightening monetary policy sooner than the ECB and perhaps even the Fed. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The UK Leads The Way

The UK Leads The Way

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

The NFIB survey suggests that small business owners are losing confidence in the economic outlook. The headline index fell to 99.7 in July, disappointing expectations it would remain broadly unchanged near the prior month’s 102.5. Notably, six of the index’s…

According to BCA Research’s US Bond Strategy service, the Fed is preparing the markets for a taper announcement in Q4. Several Fed governors and regional presidents made media appearances last week, each one presenting a timeline that sets up a tapering…

Highlights Fed: The Fed is preparing markets for a taper announcement in Q4 of this year. But we don’t see asset purchase tapering as a catalyst for higher bond yields. Rather, bond yields will move higher as the employment data continue to come in hot. Job growth will be strong enough to reach the Fed’s definition of maximum employment by the end of 2022, and the fed funds rate will rise more quickly than is implied by current market expectations. Duration: The 10-year Treasury yield will reach a range of 2% to 2.25% by the time the Fed is ready to lift rates, near the end of 2022. Strong employment data will catalyze the next significant jump in bond yields, but this may not happen until Q4 of this year. The spread of the delta COVID variant could limit the pace of hiring during the next month or two, and bond market positioning may need to turn more bullish before yields can rise. Labor Market: After July’s strong employment report, we calculate that average monthly nonfarm payroll growth of 431k is required to reach the Fed’s “maximum employment” liftoff criteria by the end of 2022. Feature Chart 1A Tapering Announcement Is Coming

A Tapering Announcement Is Coming

A Tapering Announcement Is Coming

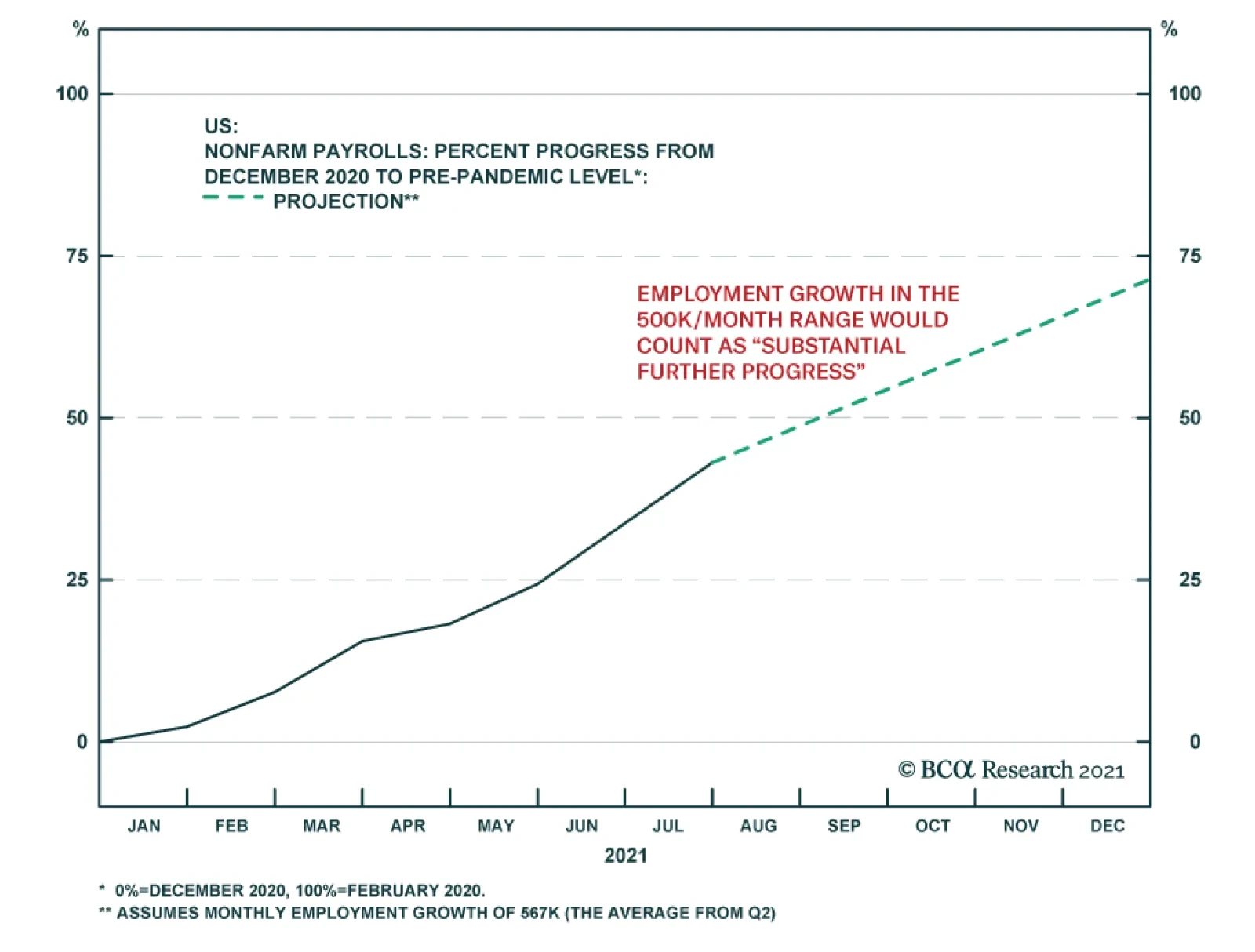

It’s finally time to talk about tapering. Several Fed governors and regional presidents made media appearances last week, each one presenting a timeline that sets up a tapering announcement before the end of this year. Federal Reserve Governor Christopher Waller: I think you could be ready to do an announcement by September. That depends on what the next two jobs reports do. If they come in as strong as the last one, then I think you have made the progress you need. If they don’t, then I think you are probably going to have to push things back a couple of months.1 St Louis Fed President James Bullard: I don’t think that we need to continue with these purchases now that we’ve got new risks on the horizon and possibly inflation risks on the horizon. […] What I think we should do here is start sooner and go faster and get finished by the end of the first quarter of next year. We don’t really need the purchases anymore.2 Dallas Fed President Robert Kaplan: As long as we continue to make progress in July (jobs) numbers and in August jobs numbers, I think we’d be better off to start adjusting these purchases soon. Doing so gradually, over a time frame of plus or minus about eight months, will help give ourselves as much flexibility as possible to be patient and be flexible on the fed funds rate.3 Fed Governor Lael Brainard presented the most detailed description of what it will take for the Fed to start paring its asset purchases.4 Since December, the Fed’s criteria for tapering has been “substantial further progress” toward its employment and price stability goals. In December, nonfarm payrolls were about 10 million below pre-pandemic levels (Chart 2A). In her speech, which was given prior to the release of July’s jobs report, Brainard noted that if employment grows at the same rate in Q3 as it did in Q2, then “about two-thirds of the outstanding job losses as of December 2020” would be made up by the end of 2021. That figure rose to 71% after July’s strong jobs number (Chart 2B). Chart 2AConditions For Tapering

Conditions For Tapering

Conditions For Tapering

Chart 2BDefining "Substantial Further Progress"

Defining "Substantial Further Progress"

Defining "Substantial Further Progress"

In other words, as long as employment growth stays solid – in the 500k/month range – then the Fed will be well over 50% of the way toward its maximum employment goal by the end of this year. This would certainly count as “substantial further progress”. Our expectation is that Q3 jobs growth will be strong enough for the Fed to make an official taper announcement in Q4, with the actual tapering starting in January 2022.5 There is an outside chance that the Fed will rush to start tapering earlier, but only if long-dated inflation expectations rise to well above the Fed’s target range (Chart 2A, bottom panel). As for market impact, we don’t expect the tapering announcement to move markets all that much. First, we mainly care about asset purchase tapering because it could signal that the Fed intends to move more quickly toward rate hikes (Chart 1). This is the concern that prompted the 2013 taper tantrum. This time around, however, the Fed has tied liftoff to explicit employment and inflation criteria. This forward guidance significantly weakens the signaling power of any tapering announcement. Second, surveys indicate that market participants already anticipate that tapering will start in early-2022 (Tables 1A & 1B). In other words, a Q4 taper announcement shouldn’t be that much of a shock to expectations. Table 1ASurvey Of Market Participants Expected Fed Timeline

Talking About Tapering

Talking About Tapering

Table 1BSurvey Of Primary Dealers Expected Fed Timeline

Talking About Tapering

Talking About Tapering

Interestingly, Fed Vice-Chair Richard Clarida did manage to shock markets with his speech last week, but only because he went further than just a discussion of tapering. Specifically, Clarida articulated his expected timeline for lifting interest rates: Chart 3Median FOMC Forecasts

Median FOMC Forecasts

Median FOMC Forecasts

While, as Chair Powell indicated last week, we are clearly a ways away from considering raising interest rates and this is certainly not something on the radar screen right now, if the outlook for inflation and outlook for unemployment I summarized earlier turn out to be the actual outcomes for inflation and unemployment realized over the forecast horizon, then I believe that these three necessary conditions for raising the target range for the federal funds rate will have been met by year-end 2022.6 What are the economic forecasts that Clarida says would meet the conditions for liftoff by the end of 2022? It turns out that they are very close to the FOMC’s median projections (Chart 3). The Fed’s forecast calls for 3% core PCE inflation in 2021, falling to 2.1% in 2022 and 2023. The Fed also sees the unemployment rate falling to 4.5% by the end of this year, 3.8% by the end of 2022 and 3.5% by the end of 2023. Clarida said that he views this forecast as consistent with overall employment returning to its pre-pandemic levels by the end of 2022. We think Clarida’s expected timeline is reasonable. The Appendix at the end of this report presents different scenarios for when the Fed’s “maximum employment” liftoff condition might be met. We estimate that average monthly nonfarm payroll growth of 431k will get us to maximum employment by the end of 2022, in time for early-2023 liftoff. At least so far, monthly nonfarm payroll growth is tracking well above the 431k threshold. If we compare our (and Clarida’s) forecast to market prices, we conclude that market rate expectations are too low. The overnight index swap curve is priced for Fed liftoff in January 2023 but for not even three 25 basis point rate hikes in total by the end of 2023 (Chart 4). This seems too low if the Fed’s liftoff criteria are in fact met by the end of 2022, as is our expectation. Chart 4Rate Expectations

Rate Expectations

Rate Expectations

Bottom Line: The Fed is preparing markets for a taper announcement in Q4 of this year. But we don’t see asset purchase tapering as a catalyst for higher bond yields. Rather, bond yields will move higher as the employment data continue to come in hot. Job growth will be strong enough to reach the Fed’s definition of maximum employment by the end of 2022, and the fed funds rate will rise more quickly than is implied by current market expectations. Timing The Move Higher In Yields Our expectation for a return to maximum employment by the end of 2022 implies that bond yields will be significantly higher by then. Specifically, we expect that both the 5-year/5-year forward Treasury yield and the 10-year Treasury yield will be in a range between 2% and 2.25% by the time of the first rate hike (Chart 5). The 2% to 2.25% range is consistent with survey estimates of the long-run neutral fed funds rate. But a big question remains over the timing of the next move higher in yields. Are bond yields poised to jump higher immediately? Or will they remain low for the next few months and move up only in 2022? Our sense is that the catalyst for the next significant jump in bond yields will be surprisingly strong employment data. There is widespread consensus that inflation will be close to the Fed’s target (if not higher) by the end of 2022, but recent concerns about labor supply have increased the uncertainty around employment projections. Ultimately, we think that labor supply constraints will ease and that the unemployment rate will catch up to levels implied by different labor demand indicators (Chart 6). However, this may not happen during the next month or two. Chart 5A Target For Long-Dated Yields

A Target For Long-Dated Yields

A Target For Long-Dated Yields

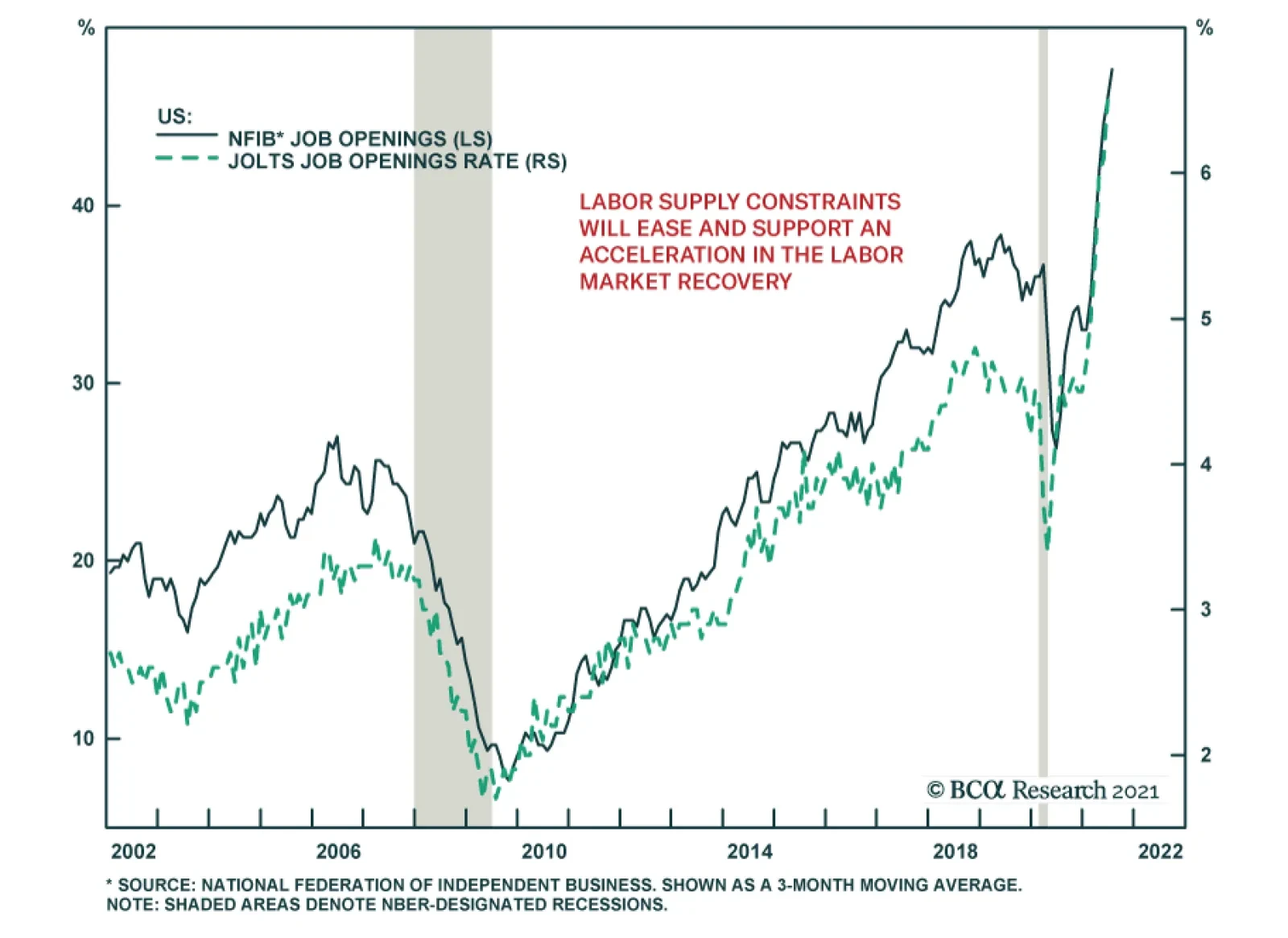

Chart 6Labor Demand Is Strong

Labor Demand Is Strong

Labor Demand Is Strong

The spread of the Delta coronavirus variant has just started to ramp up in the United States (Chart 7). The UK’s experience with the variant shows that vaccination significantly limits the number of hospitalizations and suggests that economic lockdowns can be avoided. However, it took about one month for the UK’s new case count to peak once the variant started spreading. A similar roadmap could lead to hiring delays in the US during the next month or two, at least until the new case count starts to fall and concerns abate. From a market technical perspective, we also note that bond market positioning remains significantly net short and that bond market sentiment is less bullish than is often the case at major inflection points (Chart 8). This is not the ideal technical set-up for a large immediate jump in bond yields. Chart 7Delta Is A Near-Term Risk To Hiring

Delta Is A Near-Term Risk To Hiring

Delta Is A Near-Term Risk To Hiring

Chart 8Positioning & Sentiment

Positioning & Sentiment

Positioning & Sentiment

Bottom Line: The 10-year Treasury yield will reach a range of 2% to 2.25% by the time the Fed is ready to lift rates, near the end of 2022. Strong employment data will catalyze the next significant jump in bond yields, but this may not happen until Q4 of this year. The spread of the delta COVID variant could limit the pace of hiring during the next month or two, and bond market positioning may need to turn more bullish before yields can rise. Appendix: How Far From “Maximum Employment” And Fed Liftoff? Chart A1Defining “Maximum Employment”

Defining "Maximum Employment"

Defining "Maximum Employment"

The Federal Reserve has promised that the funds rate will stay pinned at zero until the labor market returns to “maximum employment”. The Fed has not provided explicit guidance on the definition of “maximum employment”, but we deduce that “maximum employment” means that the Fed wants to see the U3 unemployment rate within a range consistent with its estimates of the natural rate of unemployment, currently 3.5% to 4.5%, and that it wants to see a more or less complete recovery of the labor force participation rate back to February 2020 levels (Chart A1). Alternatively, we can infer definitions of “maximum employment” from the New York Fed’s Surveys of Primary Dealers and Market Participants. These surveys ask respondents what they think the unemployment and labor force participation rates will be at the time of Fed liftoff. Currently, the median respondent from the Survey of Market Participants expects an unemployment rate of 3.5% and a participation rate of 63%. The median respondent from the Survey of Primary Dealers expects an unemployment rate of 3.7% and a participation rate of 63%. Tables A1-A4 present the average monthly nonfarm payroll growth required to reach different combinations of unemployment rate and participation rate by specific future dates. For example, if we use the definition of “maximum employment” from the Survey of Market Participants, then we need to see average monthly nonfarm payroll growth of +431k in order to hit “maximum employment” by the end of 2022. Table A1Average Monthly Nonfarm Payroll Growth Required For The Unemployment To Reach 4.5% By The Given Date

Talking About Tapering

Talking About Tapering

Table A2Average Monthly Nonfarm Payroll Growth Required For The Unemployment To Reach 4% By The Given Date

Talking About Tapering

Talking About Tapering

Table A3Average Monthly Nonfarm Payroll Growth Required For The Unemployment To Reach 3.5% By The Given Date

Talking About Tapering

Talking About Tapering

Table A4Average Monthly Nonfarm Payroll Growth Required To Reach “Maximum Employment” As Defined By Survey Respondents

Talking About Tapering

Talking About Tapering

Chart A2 presents recent monthly nonfarm payroll growth along with target levels based on the Survey of Market Participants’ definition of “maximum employment”. This chart is to help us track progress toward specific liftoff dates. For example, if monthly nonfarm payroll growth continues to print at the same level as last month, then we could anticipate a Fed rate hike by June 2022. Table A2Tracking Toward Fed Liftoff

Tracking Toward Fed Liftoff

Tracking Toward Fed Liftoff

We will continue to track these charts and tables in the coming months, and will publish updates after the release of each monthly employment report. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 https://www.bloomberg.com/news/articles/2021-08-02/waller-says-strong-job-reports-may-warrant-september-taper-call?sref=Ij5V3tFi 2 https://www.stlouisfed.org/from-the-president/video-appearances/2021/bullard-washington-post-inflation-tapering 3 https://www.reuters.com/business/finance/exclusive-feds-kaplan-wants-bond-buying-taper-start-soon-be-gradual-2021-08-04/ 4 https://www.federalreserve.gov/newsevents/speech/brainard20210730a.htm 5 Please see US Bond Strategy / Global Fixed Income Strategy Special Report, “A Central Bank Timeline For The Next Two Years”, dated June 1, 2021. 6 https://www.federalreserve.gov/newsevents/speech/clarida20210804a.htm Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

Since 2007, US growth stocks have outperformed value by more than 350%. This marked a significant shift versus the prior seven years during which US value stocks outperformed growth by nearly 50%. Moreover, the episodes during which value outperformed growth…

BCA Research’s Global Investment Strategy service believes online retailers (AMZN), payment processing companies (V, MA, PYPL, SQ), and social media companies (FB, SNAP) are likely to experience headwinds over the next 12 months as life returns to normal…

Foreword Today we are publishing a charts-only report focused on the S&P 500 and its sectors. Many of the charts are self-explanatory; to some we have added a short commentary. As with the styles Chart Pack, published a month ago, the sector charts cover macro, valuations, fundamentals, technicals, and the uses of cash. Our goal is to equip you with all the data you need to underpin sector allocation decisions. We also include performance, valuations, and earnings growth expectations tables for all the styles, sectors, industry groups, and industries (GICS 1, 2 and 3). We hope you will find this publication useful. We plan to update it monthly, alternating sector and style coverage. Overarching Investment Themes Macro Economic surprise index is flagging while Q2-21 earnings surprises are unprecedented. Much of the good economic news has been priced in and the Citigroup Economic Surprise Index is hovering around zero (Chart 1A). Most of the economic indicators have turned, confirming that the surge in growth has run its course and the macroeconomic environment is normalizing. Covid-19 fears are resurfacing: The spread of the Delta variant is unlikely to trigger another lockdown, but consumers may curtail their activities out of fear of infection, adversely affecting demand for goods and services. However, for now, we are sanguine about this risk. Investors expect inflation to roll over: Investors’ inflation fears are dissipating, attested by the falling 5Y/5Y inflation breakevens (Chart 1B). Indeed, it appears that the debate on the persistence of inflation has been won by the “inflation is transitory” camp. Yet, we won’t be surprised if inflation surprises on the upside (no pun intended). Chart 1AGood Economic News Has Been Priced In

Good Economic News Has Been Priced In

Good Economic News Has Been Priced In

Chart 1BMost Investors Are Now Convinced That Inflation Will Be Transitory

Most Investors Are Now Convinced That Inflation Will Be Transitory

Most Investors Are Now Convinced That Inflation Will Be Transitory

Labor shortages are starting to dissipate: On the labor front, companies are still struggling to fill job openings. However, there are signs that the labor market is healing, with more and more workers interested in returning to the labor force (Chart 2). Inventories will be replenished, spurring investment: Post-pandemic economic recovery is still plagued by the mismatch between supply and demand. Supply-chain disruptions and shortages fail to meet pent-up demand of consumers eager to spend “helicopter drop cash” and accumulated savings. As a result, inventories have been drawn down, chipping away 1.1% from GDP growth. In fact, they are at all-time lows: Non-farm inventories to final sales have dropped lower than they were during the GFC (Chart 3). Low inventories will have to be replenished, resulting in further gains in investment and providing a boost to industrial activity going forward. Chart 2More Workers Are Interested In Returning To The Labor Force

US Equity Chart Pack

US Equity Chart Pack

Demand for services will continue to exceed demand for goods: Last, but not least, consumers have money to spend but are shifting away from goods and toward services and experiences. Consumer expenditure on goods is above trend and has recently turned down, while spending on services is still below pre-pandemic levels, and rebound is still running its course (Chart 4). Chart 3Inventories Are At All Time Low

Inventories Are At All Time Low

Inventories Are At All Time Low

Chart 4Real Spending On Services Is At PrePandemic Levels: Room For Further Rebound

Real Spending On Services Is At PrePandemic Levels: Room For Further Rebound

Real Spending On Services Is At PrePandemic Levels: Room For Further Rebound

Valuations And Profitability The US stock market remains expensive: The S&P 500 is trading more than two standard deviations above the long-term average. However, there are pockets of reasonably priced, albeit unloved, stocks within the S&P 500: Telecom (11x forward earnings), Health Care (17x), Energy (14x), and Financials (14x). Earnings continue to crush expectations: While equities are expensive, they are redeemed by the strong showing of earnings and sales growth reported for Q2-2021. The scale of earnings beats relative to analyst expectations is spectacular: Running at nearly 20%, or more than two standard deviations above the historical average (Chart 5). Chart 5Earnings Surprises Are Unprecedented

US Equity Chart Pack

US Equity Chart Pack

Earnings growth is normalizing: Earnings have increased 90% over the lackluster Q2, 2020. Compared to Q2-2019 as a baseline quarter, earnings are up 22%, pointing to normalization going forward. Earnings growth will become a tailwind for the outperformance of equities into the balance of the year and will help the S&P 500 to grow into its big valuation “shoes”. Margins are expanding despite inflation: Many sectors are able to grow earnings and recover margins despite increases in costs of raw materials and labor, thanks to their strong pricing power, i.e., ability to pass on higher input costs to their customers (Chart 6A). Sectors with the highest pricing power are: Communications Services, Consumer Discretionary, Industrials, Energy and Materials. They are the best inflation hedges. Chart 6ACompanies' Profitability Is Improving To Pre-Pandemic Levels

Companies' Profitability Is Improving To Pre-Pandemic Levels

Companies' Profitability Is Improving To Pre-Pandemic Levels

Uses Of Cash Cash to be disbursed to shareholders: Share buybacks and other shareholder-friendly activities are on the rise again and are expected to gain steam this year and next. This is supported both by strong earnings growth, healthy balance sheets, and regulatory headwinds to any potential M&A activity due to the anti-trust stance of the current administration Capex is about to make a comeback: Capex is still lagging across most sectors. A pickup in capex will signal that the post-pandemic recovery is firmly on track, and companies are comfortable investing in future growth. However, there are early signs that that is about to change. Philly Fed survey shows that over 40% of respondents are planning to increase their capex expenditure (Chart 6B). Chart 6BCapex Increases Are On The Way

Capex Increases Are On The Way

Capex Increases Are On The Way

Investment Implications Overweight sectors and industry groups exposed to consumer services spending (airlines, hotels, leisure) and be selective about consumer goods and retailing industry groups: Real PCE for goods has turned down toward the trend line. Exceptions are areas of the market with well-publicized shortages such as Autos and Parts. Overweight Industrials – US manufacturing has limited capacity, onshoring is a new trend, inventories need to be replenished, and capex intentions are on the rise. Overweight Health Care – growth slowdown favors this defensive sector, which also benefits from a backlog of demand for medical procedures and services. Reflation trade is out of the picture, now that inflation fears have abated and the Delta variant preoccupies investors. For that, we still favor Growth over Value. Yet, we watch this allocation closely, to time rotation once Covid-19 fears dissipate, rates pick up and inflation surprises on the upside. With valuations high, and forward returns expectations lackluster, we favor sectors likely to delivery healthy cash yield: Financials, Health Care, Energy, and Technology. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com S&P 500 Chart 7Macroeconomic Backdrop And Earnings Surprise

Macroeconomic Backdrop And Earnings Surprise

Macroeconomic Backdrop And Earnings Surprise

Chart 8Profitability

Profitability

Profitability

Chart 9Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 10Uses Of Cash

Uses Of Cash

Uses Of Cash

Communication Services Chart 11Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 12Profitability

Profitability

Profitability

Chart 13Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 14Uses Of Cash

Uses Of Cash

Uses Of Cash

Consumer Discretionary Chart 15Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 16Profitability

Profitability

Profitability

Chart 17Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 18Uses Of Cash

Uses Of Cash

Uses Of Cash

Consumer Staples Chart 19Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 20Profitability

Profitability

Profitability

Chart 21Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 22Uses Of Cash

Uses Of Cash

Uses Of Cash

Energy Chart 23Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 24Profitability

Profitability

Profitability

Chart 25Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 26Uses Of Cash

Uses Of Cash

Uses Of Cash

Financials Chart 27Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 28Profitability

Profitability

Profitability

Chart 29Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 30Uses Of Cash

Uses Of Cash

Uses Of Cash

Health Care Chart 31Health Care: Sector vs Industry Groups

Health Care: Sector vs Industry Groups

Health Care: Sector vs Industry Groups

Chart 32Profitability

Profitability

Profitability

Chart 33Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 34Uses Of Cash

Uses Of Cash

Uses Of Cash

Industrials Chart 35Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 36Profitability

Profitability

Profitability

Chart 37Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 38Uses Of Cash

Uses Of Cash

Uses Of Cash

Information Technology Chart 39Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 40Profitability

Profitability

Profitability

Chart 41Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 42Uses Of Cash

Uses Of Cash

Uses Of Cash

Materials Chart 43Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 44Profitability

Profitability

Profitability

Chart 45Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 46Uses Of Cash

Uses Of Cash

Uses Of Cash

Real Estate Chart 47Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 48Profitability

Profitability

Profitability

Chart 49Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 50Uses Of Cash

Uses Of Cash

Uses Of Cash

Utilities Chart 51Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 52Profitability

Profitability

Profitability

Chart 53Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 54Uses Of Cash

Uses Of Cash

Uses Of Cash

Table 1Performance

US Equity Chart Pack

US Equity Chart Pack

Table 2Valuations And Forward Earnings Growth

US Equity Chart Pack

US Equity Chart Pack

Recommended Allocation Footnotes

Highlights Economy – A range of economic and fundamental indicators are at such high levels that deceleration is inevitable: US growth will peak any day if it hasn’t done so already. Markets – Financial markets typically pay closer heed to direction than level: All else equal, we prefer direction to level as well, but levels are likely to remain elevated for a while even as deceleration takes hold, and investors should take that into account when assessing the outlook. Strategy – Remain overweight equities and credit in multi-asset portfolios: Risk assets are likely to continue to generate positive excess returns over Treasuries and cash despite moderating growth. Feature COVID-19’s arrival ushered in a wave of extremes in monetary and fiscal policy measures, economic data and financial markets. Everywhere investors look, data series are at unusually outlying levels. Inflation pressures are more intense than they have been in decades, as measured by consumer price indexes and a range of business surveys. Household net worth has advanced at its fastest-ever five-quarter pace despite the record setback that began the pandemic, S&P 500 earnings growth has demolished analyst expectations over the last five quarters, the federal government has injected a head-spinning amount of fiscal stimulus into the economy and the Fed has done all it seemingly could to cushion the pandemic’s economic blow. Much of the growth has resulted from Herculean stimulus measures that cannot be maintained on a rate-of-change basis. The slowdown in fiscal and monetary thrust implies that economic growth, along with several other series that are viewed as significant financial market drivers, will soon peak if they haven’t already. The looming deceleration has kindled a recurring debate among BCA researchers: What matters most for financial markets, level or direction? The answer to the most challenging questions in markets and economics is often “it depends,” and that’s the way we view the level-versus-direction debate. We’d position a portfolio based on direction if key series were just breaking above or below trend levels with robust momentum, but it’s a more nuanced decision when they are slowing from exceedingly high levels and a modestly decelerating pace should have them still sitting well above trend this time next year. Our view, then, is that the interaction between level and direction will drive markets going forward. Given that we have cited a range of levels in support of our bullish stance, however, it is prudent to ask how good might be too good for reliably mean-reverting series. We therefore examine the empirical record of how S&P 500 returns have interacted with the level and direction of the unemployment rate, earnings-per-share growth, and interest rates. We conclude that the humble level matters as well as the more celebrated rate of change and that deceleration will not spell the end of the equity bull market. The Unemployment Rate We used the unemployment rate as a proxy for the impact of macroeconomic changes on S&P 500 returns. While the unemployment rate is quite variable from month to month, it tends to follow a clear pattern over longer periods of time, rising very rapidly to cyclical peaks before meandering its way to cyclical troughs. Over the series’ 73-year history, there have been eleven complete rising phases and it is currently in its eleventh declining phase (Chart 1). Owing to unemployment’s established pattern – it takes the elevator up and the stairs down, flipping equity indexes’ pattern on its head – the eleven rising phases have spanned 30% of the nearly 900 months while the falling phases currently total 70% of them. Chart 1Unemployment Takes The Elevator Up And The Stairs Down

Unemployment Takes The Elevator Up And The Stairs Down

Unemployment Takes The Elevator Up And The Stairs Down

A simple compilation of one-month forward S&P 500 returns based on the level of the unemployment rate has a clear theme – stocks do well when the rate is at least one standard deviation above the mean (about 7.4% or higher) and poorly when it is one or more standard deviations below it (about 4.2% or lower) (Chart 2, left side). A compilation based on the month-to-month direction of the unemployment rate – up, down or unchanged – also favors rising unemployment, though it is unclear what investors should conclude from the fact that rising and falling both outperform unchanged (Chart 2, right side). Chart 2The S&P 500 Is Sensitive To Anticipated Turns In Unemployment

Level Or Direction?

Level Or Direction?

We think the analysis is much improved if the unemployment rate is combined with its direction as indicated by the cycle phase. The interaction of level and phase provides more information than the simple message that high unemployment is good for equities and low unemployment is bad. Applying the rising or falling unemployment rate phase to the ranges shown in Chart 2, we find that direction matters quite a lot within four of the five ranges, where the annualized return differs by thirteen to sixteen percentage points based on the underlying trend (Table 1). Table 1Level And Direction Tell The Most Compelling Story

Level Or Direction?

Level Or Direction?

Equities are just coming off their bottom, on balance, when the unemployment rate exceeds a standard deviation above its mean and is still rising. Direction is everything when the rate is below its mean (5.8%). When it’s falling, there’s plenty of money to be made in an expanding economy before the Fed has designs on removing the punch bowl, though once the rate is a standard deviation below the mean (4.2% or lower), the equity top is near. Once the unemployment rate rises off the bottom, even though it’s still at an unusually low level, the equity tide has already begun to go out. Losses are in store until the rate gets back above the mean, signaling future improvement. Chart 3Up, Up And Away

Up, Up And Away

Up, Up And Away

It is important to recognize that we can only demarcate the unemployment rate’s phases in retrospect. There is no telling with certainty in real time how far a nascent trend will go. We do expect, however, in line with every FOMC voter, that the unemployment rate is likely to approach the vicinity of last cycle’s lows before the current phase ends. If that expectation is realized, there is a stretch of downward movement ahead (a good chunk of the 1.7% standard deviation, though July claimed 50 basis points of it) that has empirically been quite favorable for the S&P 500. The speed with which it covers the ground from here to 4% or below is unknown. Given the tremendous pent-up demand for labor, as evidenced by a record high job openings rate (Chart 3), the unemployment rate may come down much faster than it normally does. The level-and-direction analysis makes it clear that 5.9% and falling has provided an auspicious backdrop for equity investors, and the Fed’s more relaxed reaction function may allow the economy to run a little hotter than it normally would once unemployment falls below its natural rate. All in all, the empirical record of the relationship between the unemployment rate and equities suggests that stocks have room to run while the labor market improves. Earnings The unemployment rate may not be too low for equities to continue to rally, but is earnings growth too good for stocks’ own good? It doesn’t appear to be, given the historical interaction between forward one-quarter S&P 500 performance and the speed and acceleration of growth in trailing four-quarter earnings. We use trailing earnings because they exhibit extended trends that highly variable sequential changes in single-quarter data do not. Since 1948, trailing four-quarter operating earnings have experienced eleven complete double-digit declines from cycle peaks and eleven complete earnings growth phases, while beginning a new growth phase in the first quarter (Chart 4). Chart 4Steady Growth With Occasional Hiccups

Steady Growth With Occasional Hiccups

Steady Growth With Occasional Hiccups

The chart shows that four-quarter earnings have grown in a pattern that features extended growth phases punctuated by concentrated declines that are occasionally severe. This pattern is the mirror image of the unemployment rate’s and S&P 500 earnings have been in a growth phase three out of every four quarters on the way to an annualized growth rate of 6.4%. Since P/E multiples are a mean-reverting series, stocks need to grow earnings to rise over time, but there is little difference in lagged S&P 500 returns when earnings are in growth or contraction mode (Chart 5). The disparity widens within each broad phase when we considered the growth rates – deceleration has been better for stock prices than acceleration within expansion phases, while a slowing rate of decline has been a tremendous catalyst when earnings are in a contraction phase. Chart 5More Money Is Made From Terrible To Bad Than From Good To Great

Level Or Direction?

Level Or Direction?

To explore S&P 500 index performance during acceleration and deceleration phases within growth ranges, we repeated the unemployment rate analysis. The return disparities for different earnings ranges were not nearly as clear cut as they were for different unemployment ranges, but acceleration was good for near-term equity returns in the middle of the earnings growth distribution, while deceleration trumped acceleration at growth rates plus or minus three quarters of a standard deviation from the mean (Table 2). Table 2Headed Out Of The Earnings Sweet Spot

Level Or Direction?

Level Or Direction?

The muddled empirical record does not point to a clear path for S&P 500 returns over the next few quarters. We assign a very low probability to a recession over the next year, virtually ensuring that the growth phase that began last quarter will continue. If actual earnings turn out to be somewhat close to the current consensus expectation, however, all subsequent quarters in this growth phase will be decelerating, and deceleration within growth phases (Table 2, circled three outcomes) has previously yielded below-average price returns. Trailing four-quarter earnings growth appears sustainable over the next year, however, and history is hardly sounding an alarm. Interest Rates We have already examined the relationship between moves in real 10-year Treasury yields and equity performance in a dedicated Special Report.1 The executive summary is that the level of real rates has exerted a greater influence on S&P 500 returns than their direction. The empirical evidence suggests that stocks generally outperform when real rates are rising, though they hit a wall once the real 10-yield exceeds estimated potential real GDP growth. They also underperform at the other extreme, as extremely negative real rates tend to be associated with dire economic conditions, but potentially frightening weakness is not a feature of today’s negative real-rate backdrop. Per the potential-GDP-rule-of-thumb, the nominal 10-year Treasury yield that would begin to crimp economic activity is around 4.5-5%, assuming potential GDP growth of 1.75-2% and annual inflation with a central tendency near 3%. It is very difficult to see the 10-year yield exceeding one-half of that threshold level in the next twelve months. Though a yield backup to 2% or above over the next year would likely have significant implications for relative returns within the S&P 500, we do not think it would spell the end of the equity rally. The bottom line, then, is that we do not believe that interest rates are at a level that makes equities especially vulnerable. Price-earnings multiples may well contract if real rates rise in line with our expectations, but we expect that earnings and earnings estimates would rise enough to offset the de-rating pressure. Investment Implications Mean reversion is a bedrock investment concept, and it helps explain why the level of variables that impact equity returns can be deceiving. When key variables reach extremes, the potential of an abrupt reversal increases. Financial markets are additionally forward discounting mechanisms and the rate of change – a variable’s “second derivative” – may offer more insight into its future path than its existing position. It is easy to see why investors typically favor direction over level when looking ahead. Level does not always take a back seat to direction, however, and we think a consideration of how level and direction interact is important when assessing the current landscape. Economic growth will surely slow from double or triple its long-run trend level, earnings will surely stop beating estimates by three or four times the maximum magnitude of the previous 32 quarters, nonfarm payrolls won’t expand by 900,000 every single month (though they may for much of the rest of this year) and a range of other variables won’t keep setting records. But deceleration from record highs will not necessarily spell the end of the rallies in risk assets. While important variables remain at elevated levels, equities and credit are likely to continue to generate excess returns. Extraordinary monetary and fiscal accommodation, combined with remarkably swift and successful action to blunt the threat of COVID-19, have carried financial markets for the last year-plus and we don’t think they’re finished yet. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see the September 24, 2018 US Investment Strategy Special Report, "When Will Higher Rates Hurt Stocks?", available at usis.bcaresearch.com.

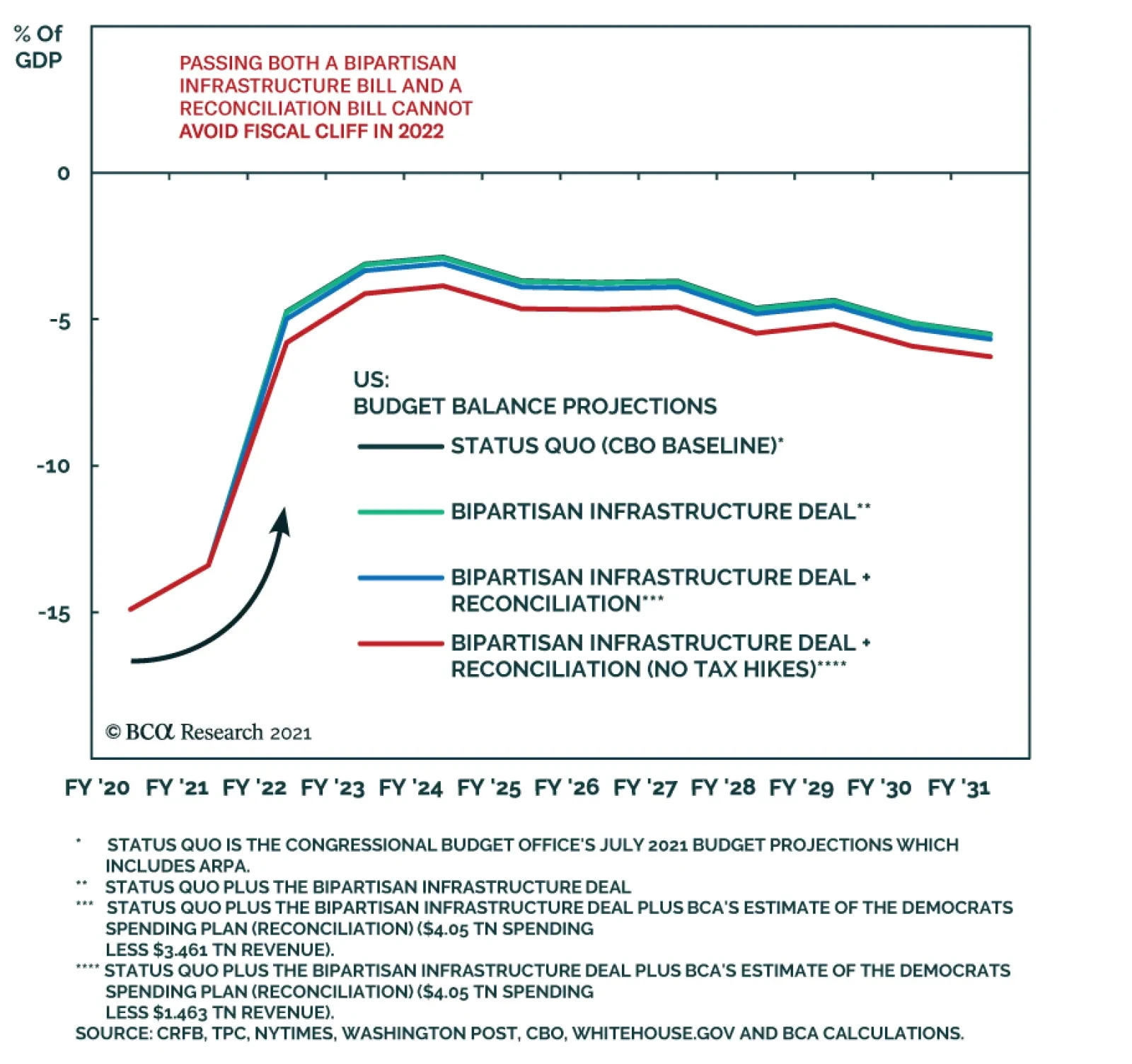

BCA Research’s Geopolitical Strategy service expects the Biden administration to pass a bipartisan infrastructure deal – as well as a large spending bill by Christmas. Ten Republicans are now slated to join 50 Democrats in the Senate to pass a $1 trillion…