United States

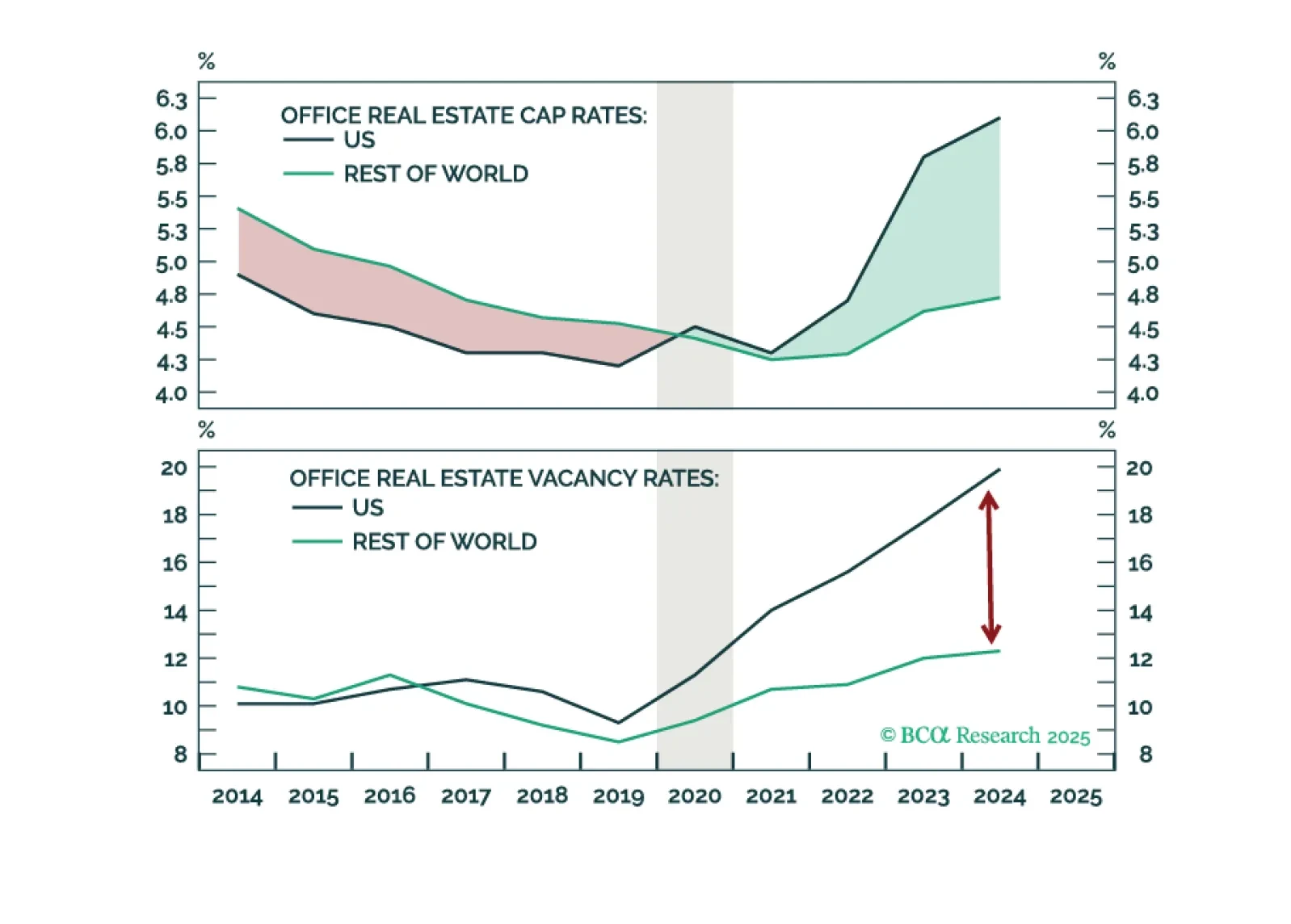

Asset prices reflect expectations—but US Office Real Estate expectations are too pessimistic. We present the case for why strong fundamentals will drive performance, despite macro risks.

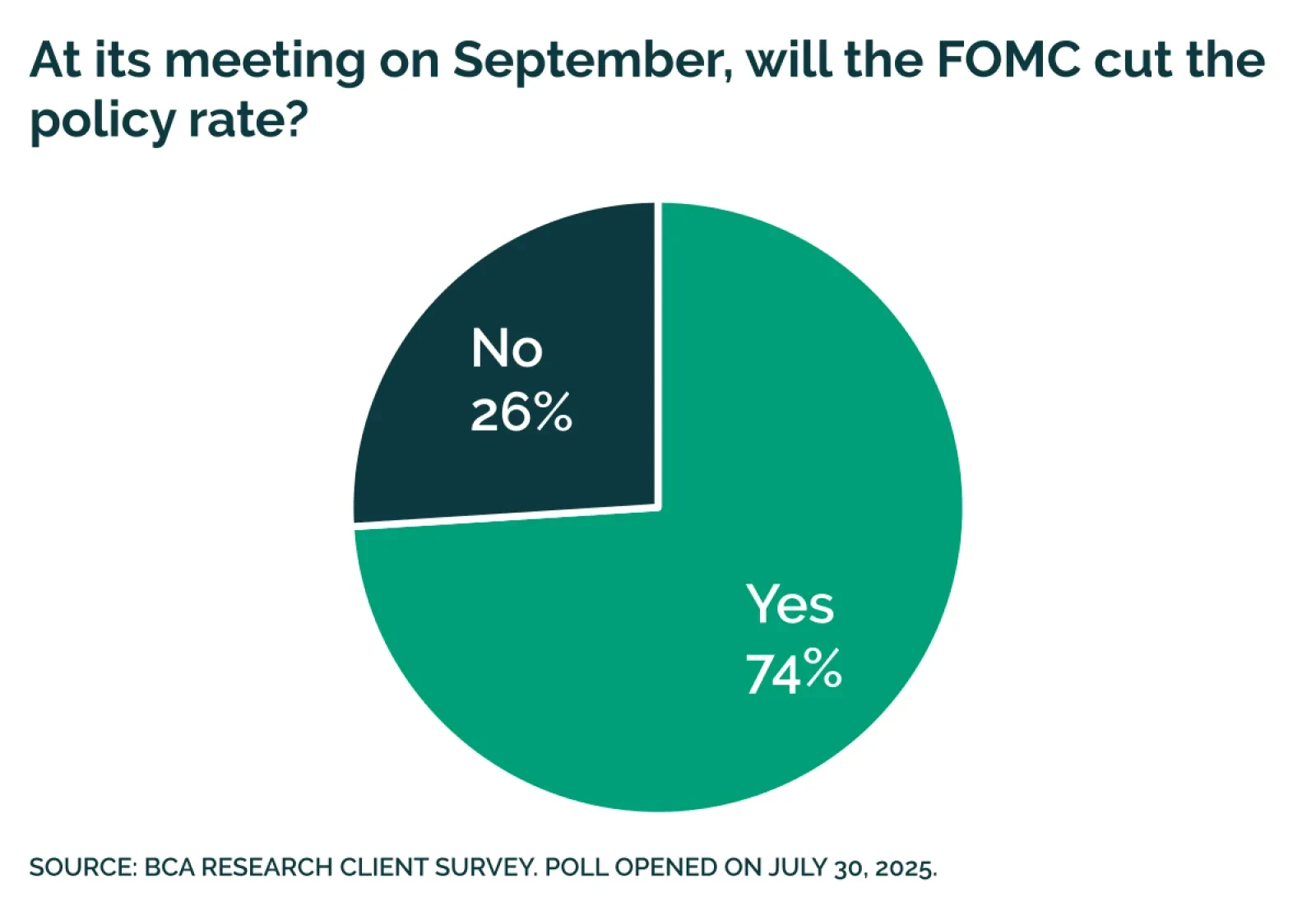

BCA clients see lower odds of a Fed rate cut on September 17 than the markets. In the latest weekly poll on the Have Your Say section of BCA's website, only 74% of respondents expect a cut, with 26% forecasting no cut. This compares with an 88%…

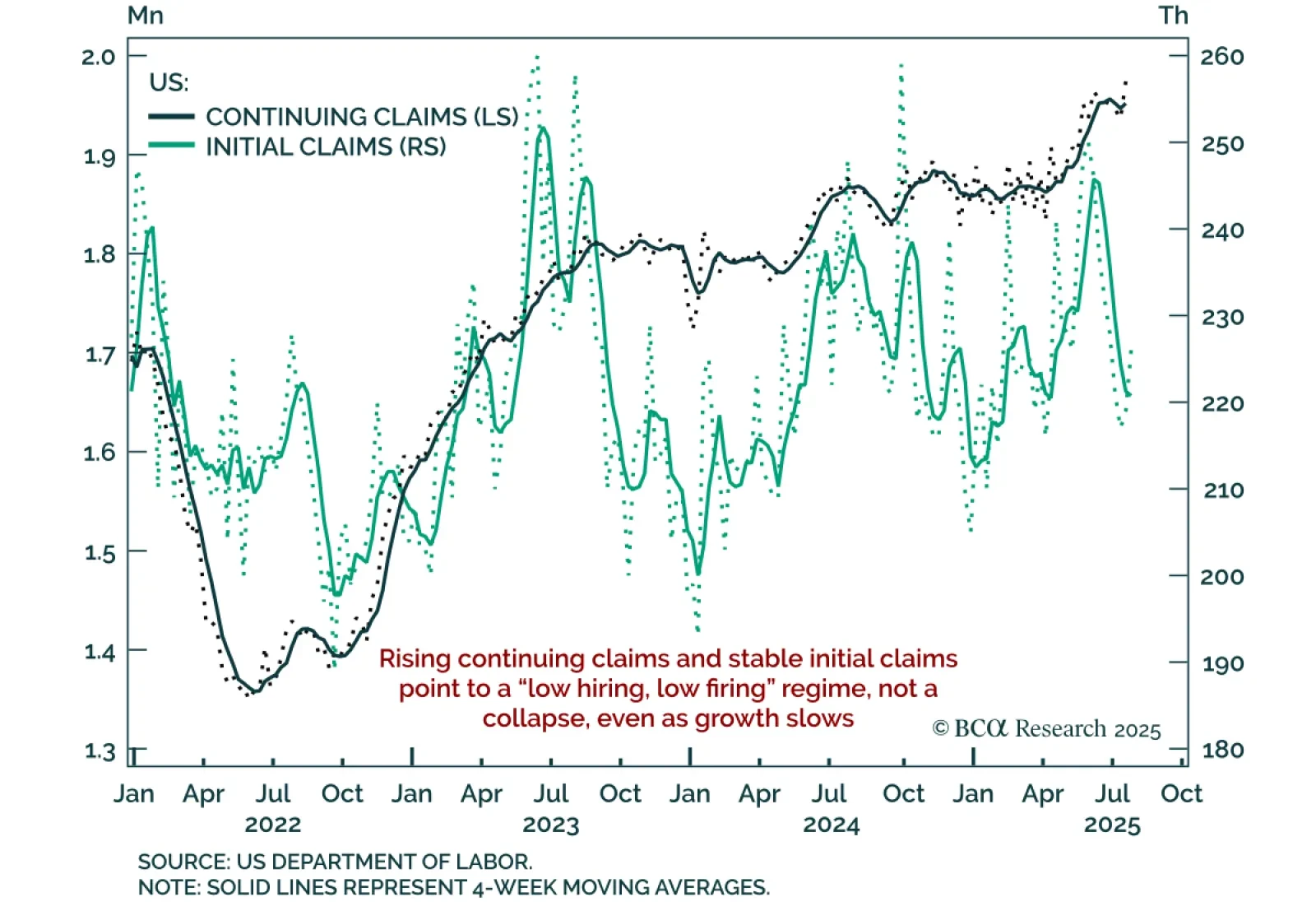

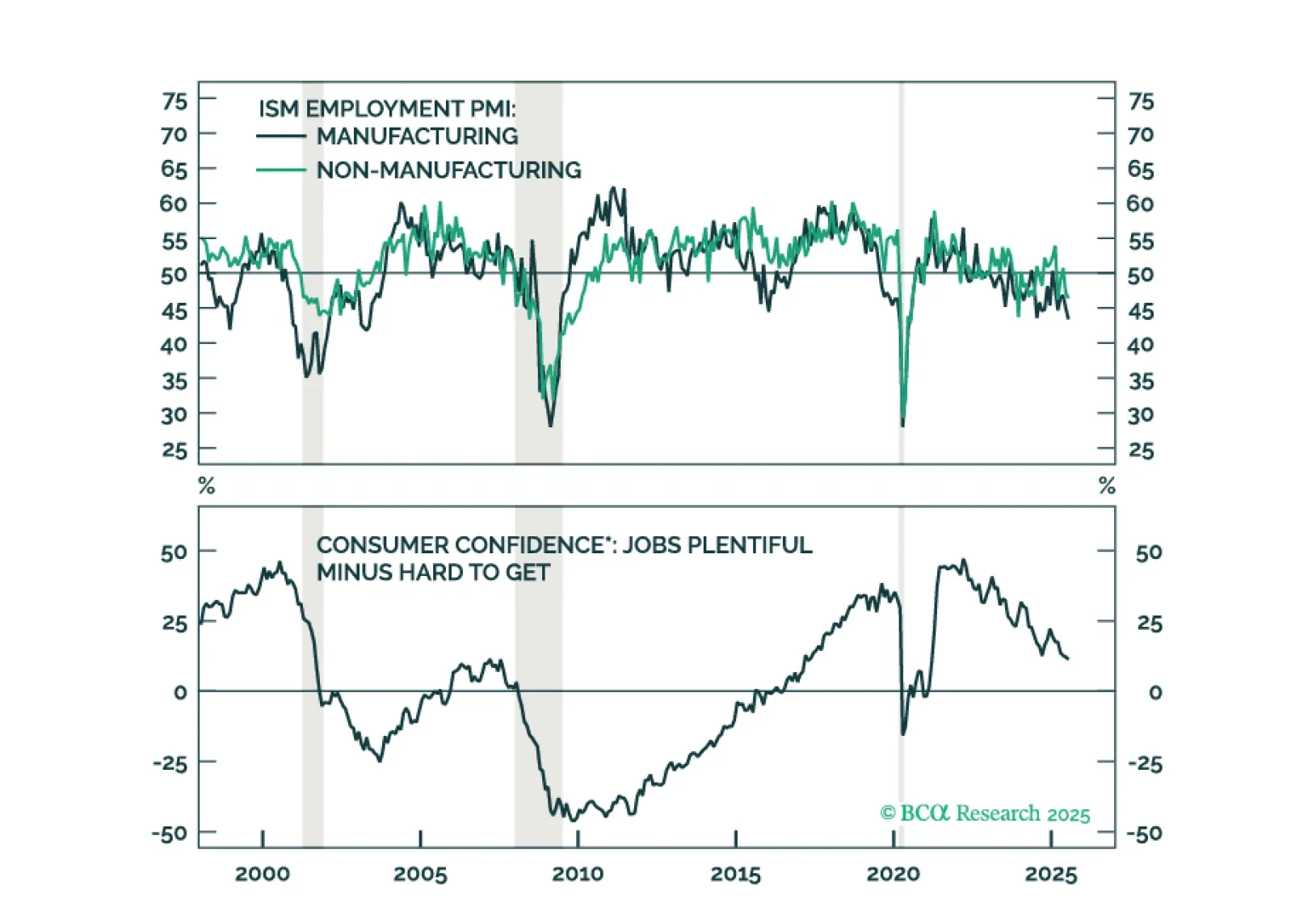

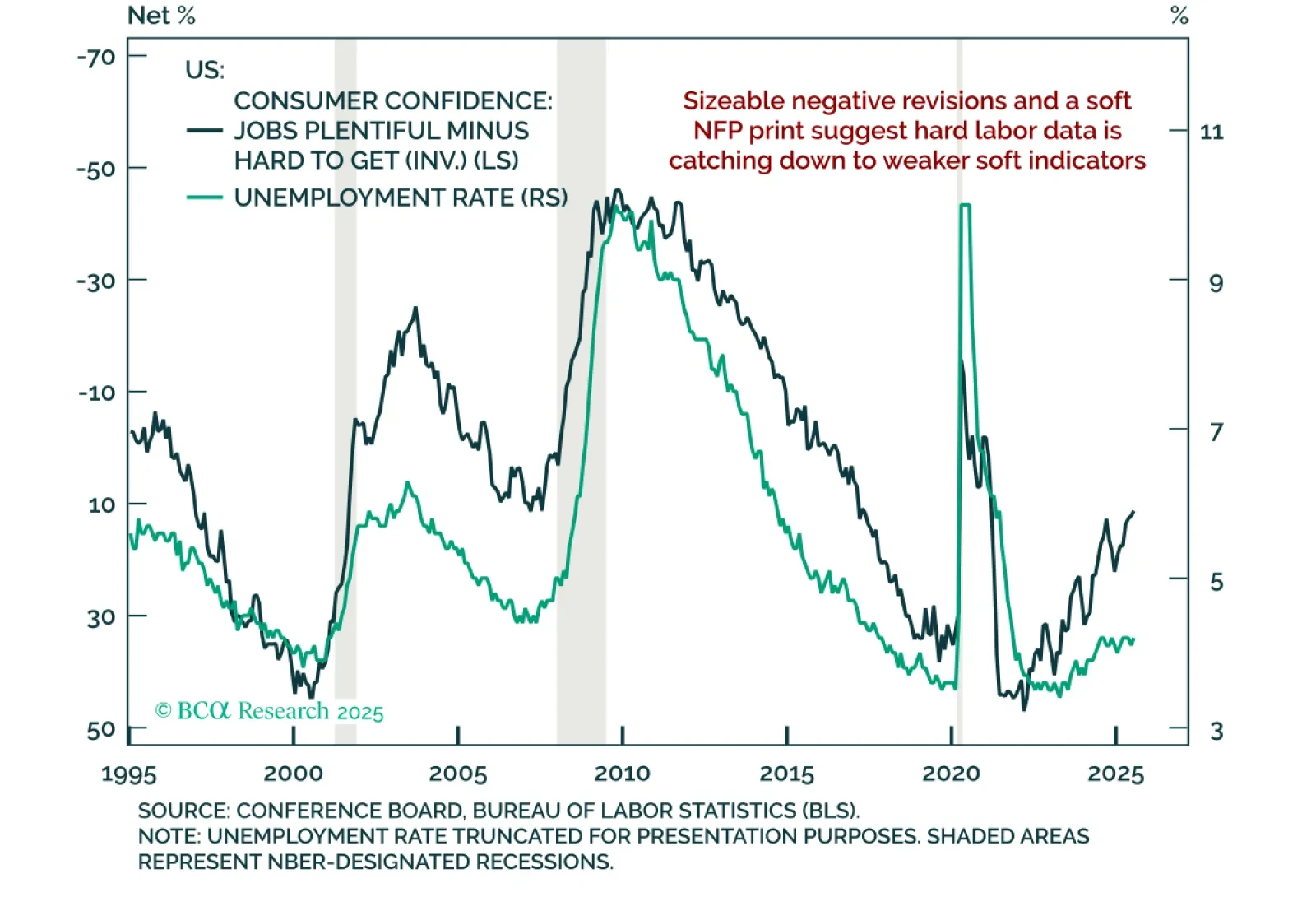

Rising continuing claims and slower job creation reinforce labor market softening, supporting a defensive stance. Continuing claims climbed to a post-COVID high of 1.974m, while initial claims held steady at 226k. Weekly claims data were closely watched…

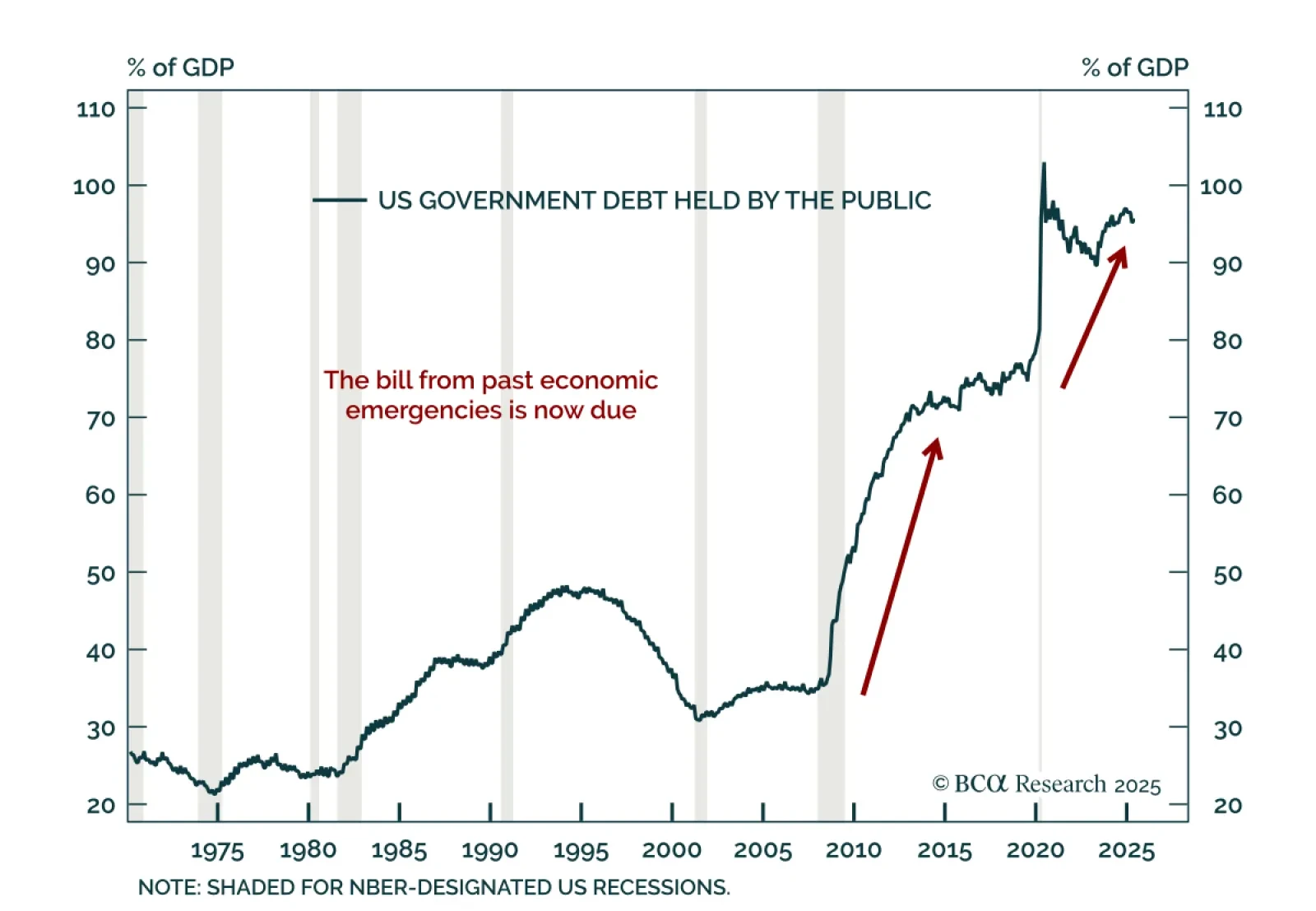

Our Bank Credit Analyst strategists argue that a US fiscal crisis should be treated as a base case over the next decade, not a tail risk. The ballooning US budget deficit reflects higher interest rates, demographic pressures, and the lingering effects of past…

Our Portfolio Allocation Summary for August 2025.

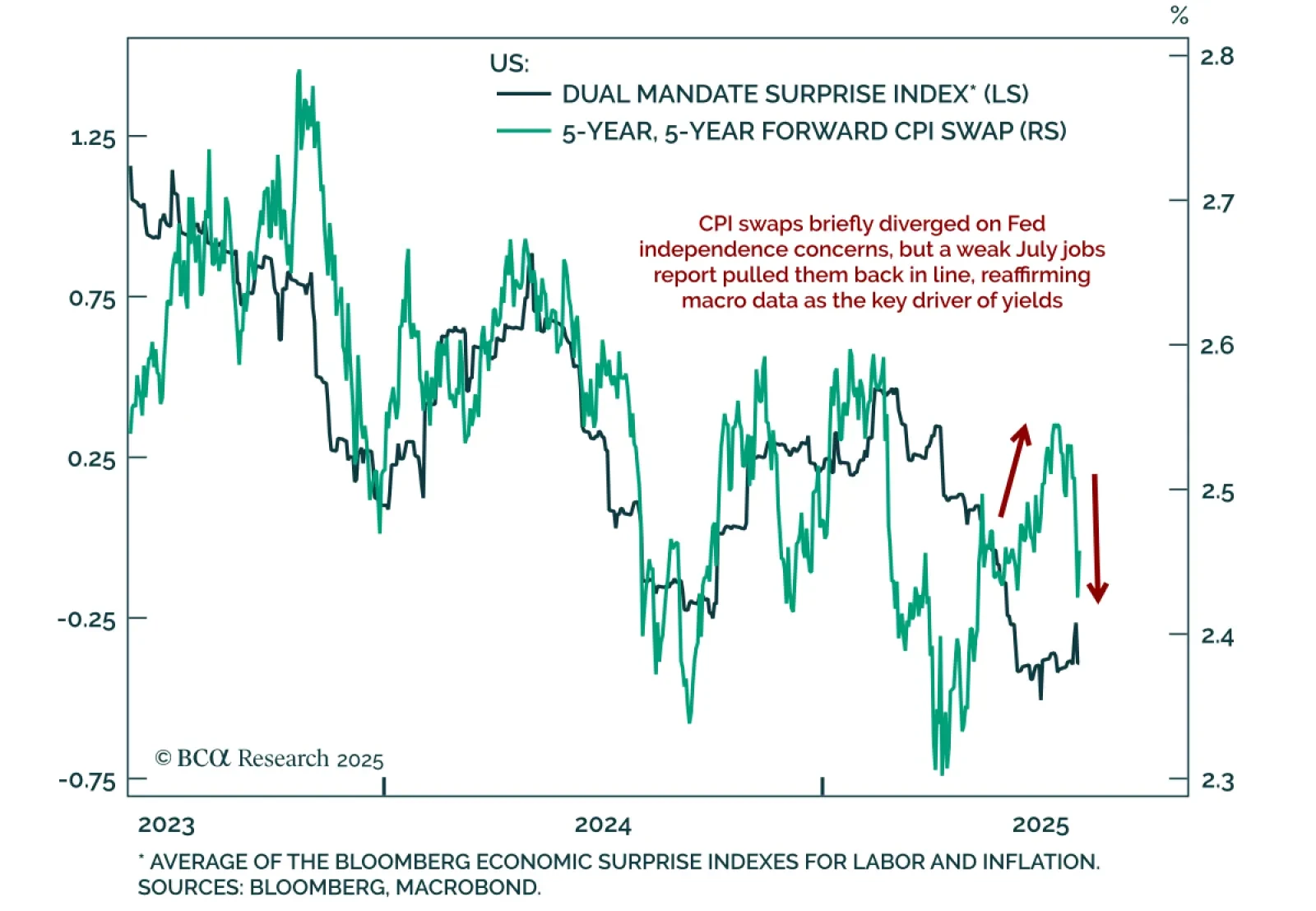

While the early resignation of Fed Gov. Kugler opened the door for a politically aligned nominee, yields will ultimately be determined by the economic outlook. Her departure triggered a further intraday DXY drop, as markets reacted to the prospect of a…

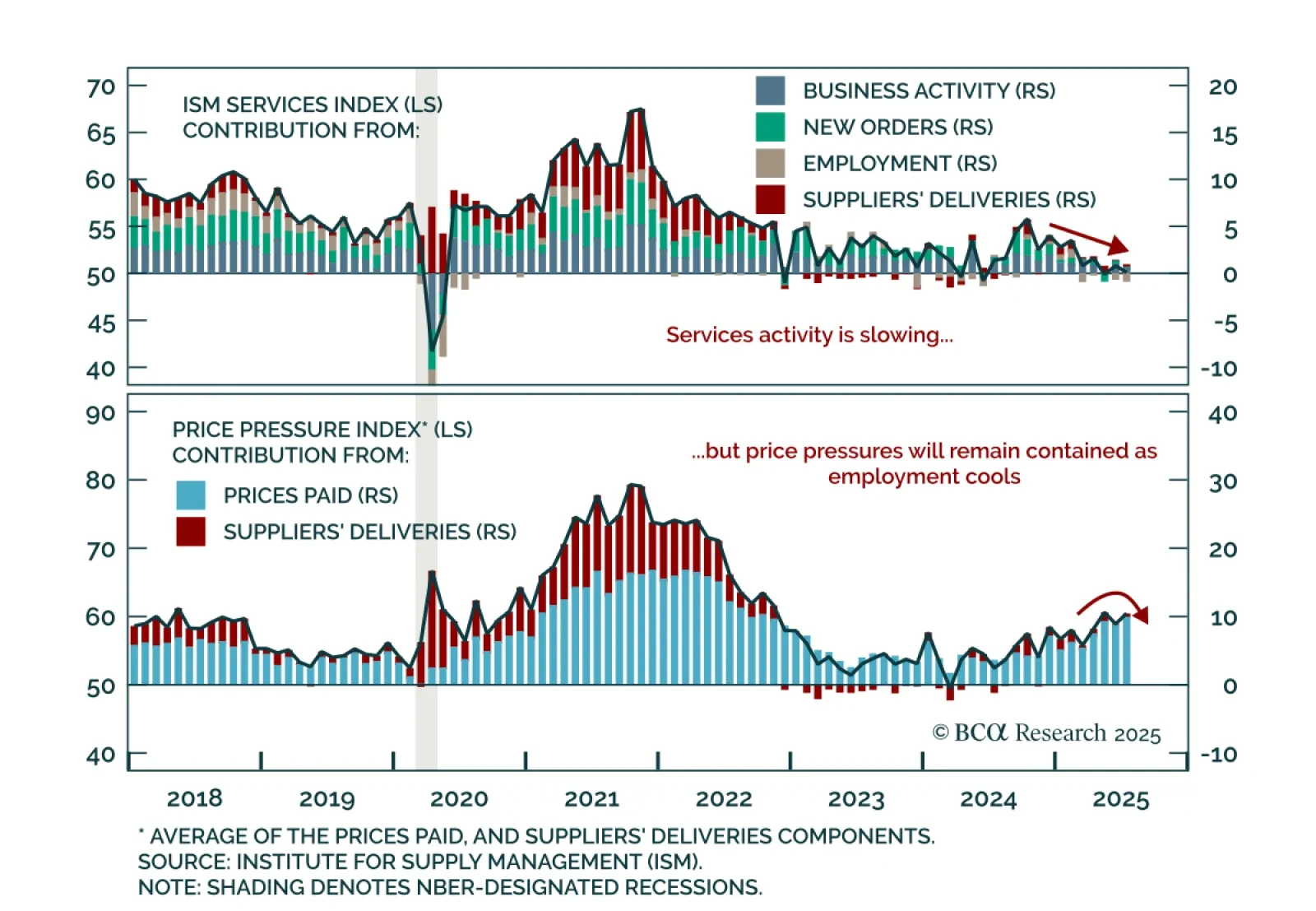

The July ISM Services report showed a stagflationary impulse, but soft labor momentum reinforces the view that price pressures remain contained. The headline index fell to 50.1 from 50.8, missing expectations. New orders softened to 50.3, while employment…

We maintain our 12-month US recession probability at 60%. However, until the “whites of the recession’s eyes” are more clearly visible, we would refrain from moving to a fully defensive stance.

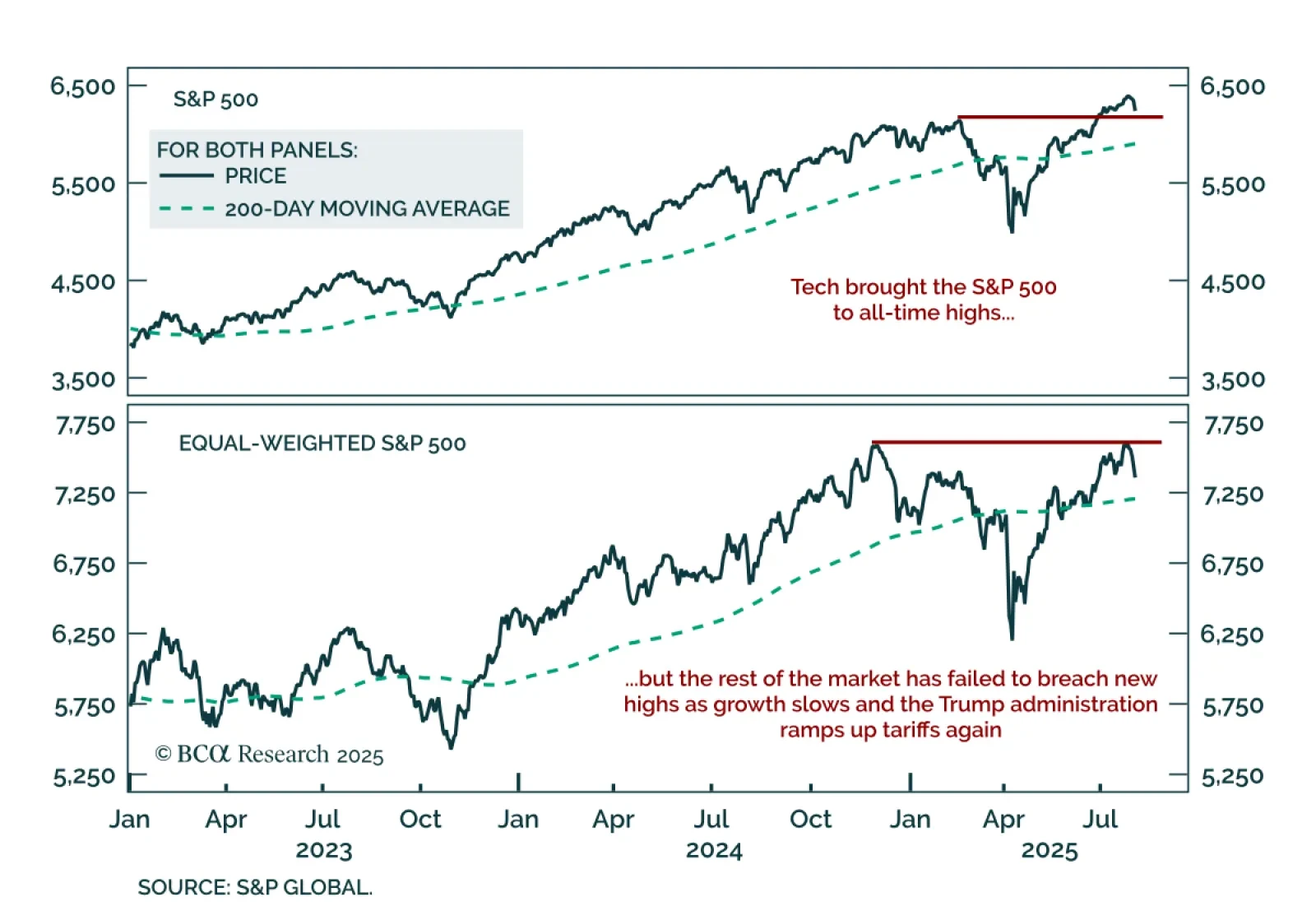

Did The S&P 500 Actually Make New Highs?

…

The July employment report revealed large downward revisions and slowing payroll growth, reinforcing our defensive stance. Nonfarm payrolls rose just 73k, and prior months were revised down by 258k, bringing the 3-month average to 35k, well below the…