United States

BCA Research’s Global Investment strategists recently highlighted that there are several compelling factors behind a weaker dollar narrative. For one, the US dollar usually weakens when growth momentum rotates from the US to the rest of the world. This is…

According to BCA Research’s US Bond Strategy service, investors should position in yield curve flatteners on a 6-12 month horizon. The Treasury curve bull-flattened in July. Bond yields were down across the curve, but by much more at the long end. The…

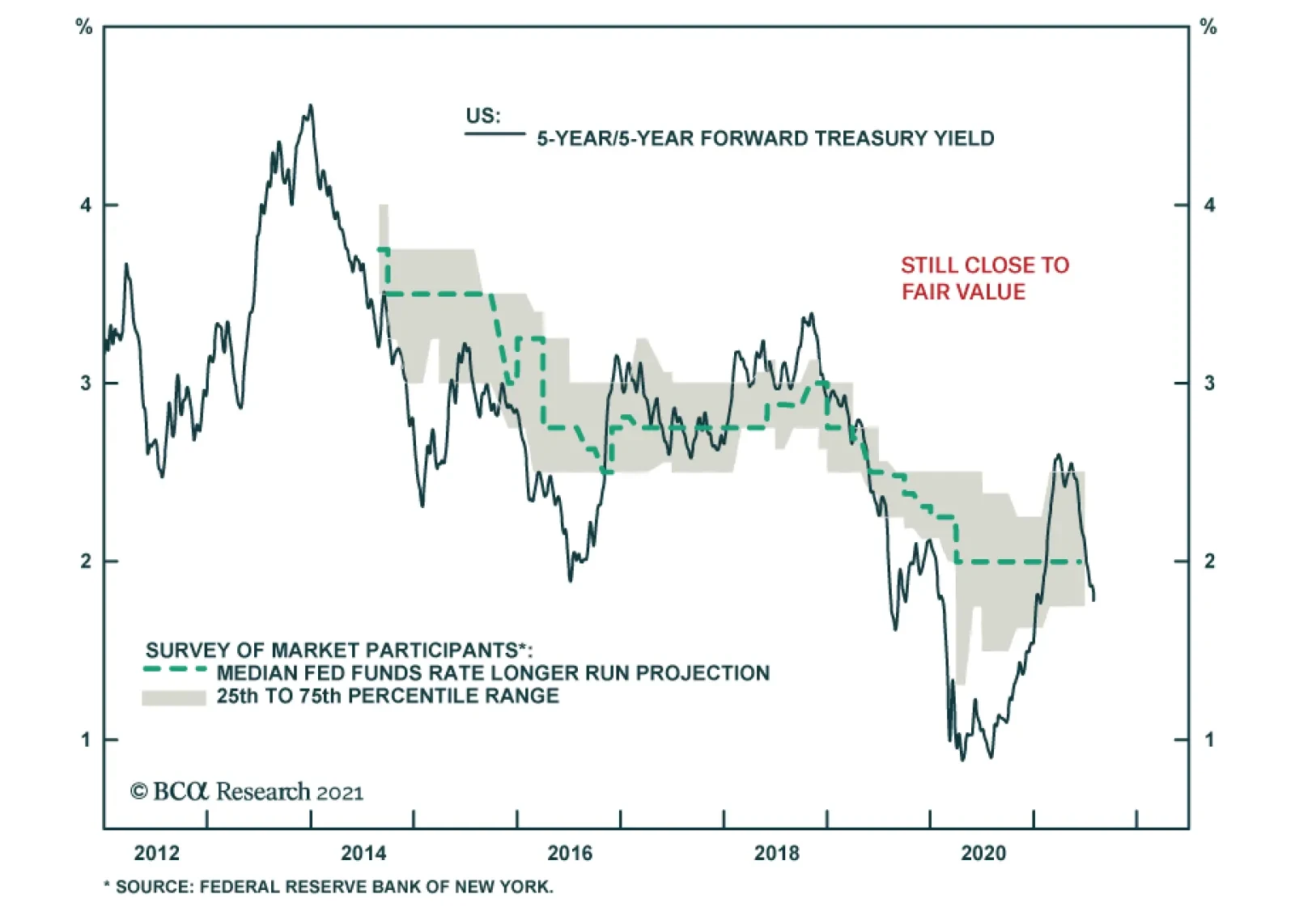

Highlights Chart 1Still Close To Fair Value

Still Close To Fair Value

Still Close To Fair Value

Treasury yields fell significantly in July, particularly at the long end of the curve. We continue to view this move as an overreaction to mediocre economic data that will be reversed this fall when labor supply constraints ease and employment surprises to the upside. It’s important to note, however, that despite the drop in long-dated yields the 5-year/5-year forward Treasury yield remains within the bounds of its 1.75% to 2.5% fair value range (Chart 1). That is, shorter-maturity Treasury yields have much more upside than long-dated yields on a 6-12 month investment horizon. We expect the next big move in bonds to be a bear-flattening of the yield curve as the market prices in a Fed rate hike cycle that we see starting near the end of 2022. Investors should position for that outcome today by keeping portfolio duration low and by entering yield curve flatteners. Feature Table 1Recommended Portfolio Specification

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

Table 2Fixed Income Sector Performance

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds underperformed the duration-equivalent Treasury index by 37 basis points in July, dragging year-to-date excess returns down to +172 bps. The combination of above-trend economic growth and accommodative monetary policy supports continued positive excess returns for spread product versus Treasuries. At 89 bps, the 3-year/10-year Treasury slope remains steep. This is a strong signal that monetary conditions are accommodative. But despite the positive macro back-drop, investment grade valuations are extremely tight (Chart 2). A recent report looked at what different combinations of Treasury slope and corporate spreads have historically signaled about corporate bond excess returns.1 It shows that tight corporate spreads only correlate with negative excess returns once the 3-year/10-year Treasury slope is below 50 bps. Though we retain a positive view of spread product as a whole, better value can be found outside of the investment grade corporate sector. Specifically, we recommend that investors shift into high-yield corporates, municipal bonds and USD-denominated EM sovereigns and corporates. We also advise investors to favor long-maturity corporate bonds and those corporate sectors with elevated Duration-Times-Spread.2 Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

Table 3BCorporate Sector Risk Vs. Reward*

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield underperformed the duration-equivalent Treasury index by 34 basis points in July, dragging year-to-date excess returns down to +433 bps. A recent report looked at the default expectations that are currently priced into the junk index and considered whether they are likely to be met.3 If we demand an excess spread of 100 bps and assume a 40% recovery rate on defaulted debt, then the High-Yield index embeds an expected default rate of 3.2% (Chart 3). Using a model of the 12-month trailing speculative grade default rate that is based on gross corporate leverage (pre-tax profits over total debt) and C&I lending standards, we estimate that the 12-month default rate will fall to between 2.3% and 2.8%, below what the market currently discounts. Notably, the corporate default rate is tracking at an annualized rate of roughly 1.6% through the first six months of the year, well below the estimate generated by our macro model. Another recent report looked at the incremental spread pick-up investors can earn by moving out of investment grade corporates and into junk.4 It concluded that the extra spread available in high-yield is worth grabbing and that B-rated bonds look particularly attractive in risk-adjusted terms. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 19 basis points in July, dragging year-to-date excess returns down to -64 bps. The nominal spread between conventional 30-year MBS and equivalent-duration Treasuries widened 8 bps in July. The spread is wide compared to recent history, but it remains tight compared to the pace of mortgage refinancings (Chart 4). The conventional 30-year MBS option-adjusted spread (OAS) widened 3 bps in July (panel 3), and it is now starting to look more competitive compared to other similarly risky spread sectors. The conventional 30-year MBS OAS sits at 36 bps, below the 54 bps offered by Aa-rated corporate bonds but above the 20 bps offered by Aaa-rated consumer ABS and the 34 bps offered by Agency CMBS. In a recent report we looked at MBS performance and valuation across the coupon stack.5 We noted that the higher convexity of high-coupon MBS makes them likely to outperform lower-coupon MBS in a rising yield environment. Higher coupon MBS also have greater OAS than lower coupons. This makes the high-coupon MBS more likely to outperform in a flat bond yield environment as well. Given our view that bond yields will be higher in 6-12 months, we recommend favoring high coupons (4%, 4.5%) over low coupons (2%, 2.5%, 3%) within an overall underweight allocation to Agency MBS. Government-Related: Neutral Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related Index underperformed the duration-equivalent Treasury index by 34 basis points in July, dragging year-to-date excess returns down to +57 bps (Chart 5). Sovereign debt underperformed duration-equivalent Treasuries by 149 bps in July, dragging year-to-date excess returns down to -113 bps. Foreign Agencies underperformed the Treasury benchmark by 11 bps on the month, dragging year-to-date excess returns down to +35 bps. Local Authority bonds underperformed by 19 bps in July, dragging year-to-date excess returns down to +372 bps. Domestic Agency bonds outperformed by 2 bps, bringing year-to-date excess returns up to +28 bps. Supranationals performed in line with Treasuries in July, year-to-date excess returns held flat at +26 bps. USD-denominated Emerging Market (EM) Sovereign bonds continue to offer an attractive spread pick-up versus investment grade US corporate bonds with the same credit rating and duration. Attractive countries include: Qatar, UAE, Saudi Arabia, Mexico and Russia. A recent report looked at valuation within the investment grade USD-denominated EM corporate space.6 It found that EM corporates are attractively priced relative to US corporate bonds across the entire investment grade credit spectrum. It also found that EM corporates are attractive relative to EM sovereigns within the A and Baa credit tiers. EM sovereigns have the edge in the Aa credit tier. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 37 basis points in July, dragging year-to-date excess returns down to +271 bps (before adjusting for the tax advantage). The economic and policy back-drop is favorable for municipal bond performance. Trailing 4-quarter net state & local government savings were already positive through the end of Q1 2021 and they received another significant boost in Q2 as funds from the American Rescue Plan were doled out (Chart 6). With state & local government balance sheets in such good shape, we are comfortable moving down in quality within municipal bonds. A move down in quality is especially compelling because of tight Aaa muni valuations relative to Treasuries (top panel). Valuation is more compelling in the lower investment grade credit tiers, especially at the long-end of the curve.7 GO munis in the 12-17 year maturity bucket offer a 10% breakeven tax rate versus corporates with the same credit rating and duration. The breakeven tax rate for Revenue munis is just 2% (panel 2). Finally, high-yield muni spreads are reasonably attractive relative to high-yield corporates, offering a breakeven tax rate of 25% (panel 4). But despite the attractive spread, we recommend only a neutral allocation to high-yield munis versus high-yield corporates as the deep negative convexity of high-yield munis makes them susceptible to extension risk if bond yields rise. Treasury Curve: Buy 2/10 Barbell Versus 5-Year Bullet Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve bull-flattened in July. Bond yields were down across the curve, but by much more at the long end. The 2-year/10-year slope flattened 15 bps to end the month at 105 bps. The 5-year/30-year slope steepened 1 bp to end the month at 120 bps. While we expect the recent decline in bond yields to reverse during the next 6-12 months, we do not think this reversal will coincide with a re-steepening of the 2/10 yield curve. We noted on the first page of this report that the 5-year/5-year forward Treasury yield remains close to its fair value range. Last week’s report demonstrated that yield curve steepening only occurs when either the Fed is cutting rates or the 5-year/5-year forward yield rises.8 This means that the 2/10 Treasury curve is more likely to flatten than steepen during the next 6-12 months, even as bond yields move higher. Similarly, we observe that the overnight index swap (OIS) curve is priced for the fed funds rate to be 0.17% in one year’s time and 1.36% in five years (Chart 7). While the latter rate has 157 bps of upside if it converges all the way back to its 2018 high, this pales in comparison to the 269 bps of upside in the 12-month forward rate. The yield curve will flatten as the 12-month forward OIS rate converges with the 5-year forward rate (panel 3). Investors should position in yield curve flatteners on a 6-12 month horizon. Specifically, we recommend shorting the 5-year bullet versus a duration-matched 2/10 barbell. TIPS: Neutral Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 112 basis points in July, bringing year-to-date excess returns up to +578 bps. The 10-year and 5-year/5-year forward TIPS breakeven inflation rates rose by 9 bps and 8 bps, respectively, on the month. At 2.43%, the 10-year TIPS breakeven inflation rate is near the middle of the 2.3% to 2.5% range that is consistent with inflation expectations being well anchored around the Fed’s target (Chart 8). Meanwhile, at 2.26%, the 5-year/5-year forward TIPS breakeven inflation rate is just below target (panel 3). With long-dated inflation expectations close to the Fed’s target levels, we see limited upside on a 6-12 month investment horizon. We also see the cost of short-maturity inflation protection falling during the next few months as realized inflation moderates from its extremely high level. This will lead to some modest steepening of the inflation curve (bottom panel). While the inflation curve has some room to steepen, we don’t see it returning to positive territory. An inverted inflation curve is simply more consistent with the Fed’s Average Inflation Target than a positively sloped one. This is because the Fed’s new framework calls for it to attack its inflation target from above rather than from below. ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

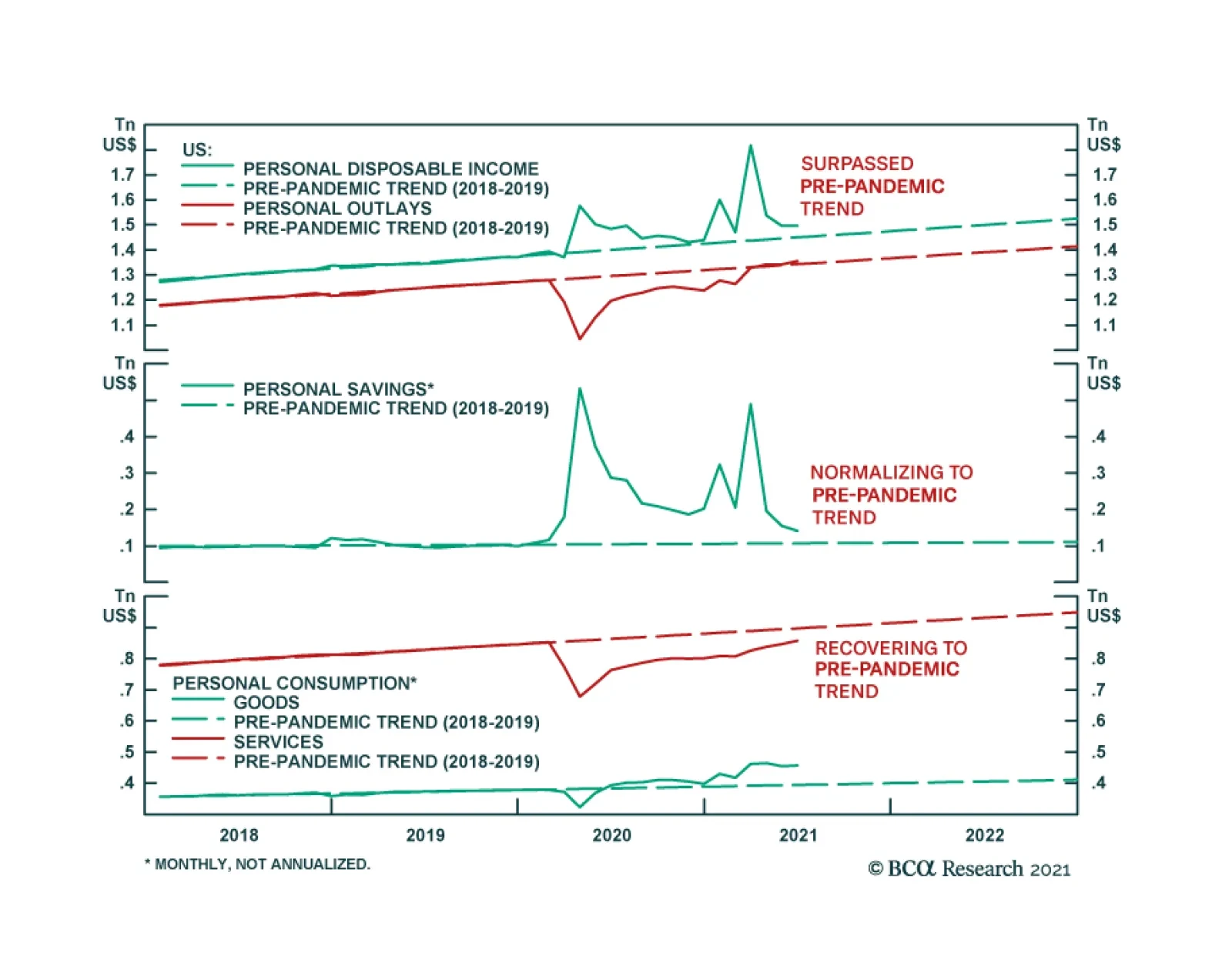

Asset-Backed Securities underperformed the duration-equivalent Treasury index by 2 basis points in July, dragging year-to-date excess returns down to +37 bps. Aaa-rated ABS underperformed by 3 bps on the month, dragging year-to-date excess returns down to +28 bps. Non-Aaa ABS outperformed by 4 bps, bringing year-to-date excess returns up to +88 bps. The stimulus from last year’s CARES act led to a significant increase in household savings when individual checks were mailed in April 2020. That excess savings has still not been spent and the most recent round of stimulus checks has only added to the stockpile, pushing the savings rate higher yet again (Chart 9). The extraordinarily large stock of household savings means that the collateral quality of consumer ABS is also extraordinarily high. Indeed, many households have been using their windfalls to pay down consumer debt (bottom panel). Investors should remain overweight consumer ABS and should also take advantage of the high quality of household balance sheets by moving down the quality spectrum. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 3 basis points in July, bringing year-to-date excess returns up to +187 bps. Aaa Non-Agency CMBS performed in-line with Treasuries in July, keeping year-to-date excess returns steady at +82 bps. Non-Aaa Non-Agency CMBS outperformed Treasuries by 16 bps on the month, bringing year-to-date excess returns up to +539 bps (Chart 10). Though returns have been strong and spreads remain attractive, particularly for lower-rated CMBS, we continue to recommend only a neutral allocation to the sector because of the structurally challenging environment for commercial real estate. Agency CMBS: Overweight Agency CMBS underperformed the duration-equivalent Treasury index by 28 basis points in July, dragging year-to-date excess returns down to +87 bps. The average index option-adjusted spread widened 5 bps on the month and it currently sits at 34 bps (bottom panel). Though Agency CMBS spreads have recovered to well below pre-COVID levels, they still look attractive compared to other similarly risky spread products. Stay overweight. Appendix A: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of July 30TH, 2021)

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of July 30TH, 2021)

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 26 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 26 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

Appendix B: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of July 30TH, 2021)

It’s Time For Bear-Flatteners

It’s Time For Bear-Flatteners

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 2 For ideas on how to increase the average spread of a US bond portfolio please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 3 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 4 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 5 Please see US Bond Strategy Weekly Report, “A New Conundrum”, dated April 20, 2021. 6 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 7 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 8 Please see US Bond Strategy / Global Fixed Income Strategy Weekly Report, “A Bump On The Road To Recovery”, dated July 27, 2021.

Dear Client, This week, in lieu of our regular report, I am sending you a special report written by my colleague Jonathan LaBerge, chief strategist of our flagship The Bank Credit Analyst service. Jonathan argues that investors should see social media as a technological innovation that harms productivity. While Jonathan concedes that social media was not the main driver of policy uncertainty and political risk over the past decade, he makes a good case that it plays an aggravating role. He warns that social media and political polarization still pose risks to the macroeconomic outlook in the coming years, while also highlighting idiosyncratic risks threatening social media stocks. We trust that you will find this report insightful. We will resume regular publication next week. All very best, Matt Gertken Vice President Geopolitical Strategy US Political Strategy BCA Research Highlights Investors should view social media as a technological innovation with negative productivity growth. Social media has contributed to policy mistakes – such as fiscal austerity and protectionism – that have acted as shocks to aggregate demand over the past 15 years. The cyclical component of productivity was long lasting in nature during the last economic expansion. Forces that negatively impact economic growth but do not change the factors of production necessarily reduce measured productivity, and repeated policy mistakes strongly contributed to the slow growth profile of the last economic cycle. Political polarization in a rapidly changing world is the root cause of these policy shocks, but social media likely facilitated and magnified them. The risks of additional mistakes from populism remain present, even before considering other risks to society from social media: a reduction in mental health among young social media users, and the role that social media has played in spreading misinformation. A potential revival in protectionist sentiment is a risk to a constructive cyclical view that we will be closely monitoring over the coming 12-24 months. Investors with concentrated positions in social media stocks should be aware of the potential idiosyncratic risks facing these companies from the public’s impression of the impact of social media on society – especially if social media companies come to be widely associated with political gridlock, the polarization of society, and failed economic policies (as already appears to be the case). Feature Investors should view social media as a technological innovation with negative productivity growth. Social media has contributed to policy mistakes – such as fiscal austerity and protectionism – that have acted as shocks to aggregate demand over the past 15 years. Political polarization in a rapidly changing world is the root cause of these policy shocks, but social media likely facilitated and magnified them. While the risk of premature fiscal consolidation appears low today compared to the 2010-14 period, the pandemic and its aftermath could force the Biden administration or Congressional Democrats toward protectionist or otherwise populist actions over the coming year in the lead up to the 2022 mid-term elections. The midterms, for their part, are expected to bring gridlock back into US politics, which could remove fiscal options should the economy backslide. Frequent shocks during the last economic expansion reinforced the narrative of secular stagnation. In the coming years, any additional policy shocks following a return to economic normality will again be seen by both investors and the Fed as strong justification for low interest rates – despite the case for cyclically and structurally higher bond yields. In addition, investors with concentrated positions in social media companies should take seriously the long-term idiosyncratic risks facing these stocks. These risks stem from the public’s impression of the impact of social media on society, particularly if social media comes to be widely associated with political gridlock, the polarization of society, and failed economic policies. A Brief History Of Social Media The earliest social networking websites date back to the late 1990s, but the most influential social media platforms, such as Facebook and Twitter, originated in the mid-2000s. Prior to the advent of modern-day smartphones, user access to platforms such as Facebook and Twitter was limited to the websites of these platforms (desktop access). Following the release of the first iPhone in June 2007, however, mobile social media applications became available, allowing users much more convenient access to these platforms. Charts 1 and 2 highlight the impact that smartphones have had on the spread of social media, especially since the release of the iPhone 3G in 2008. In 2006, Facebook had roughly 12 million monthly active users; by 2009, this number had climbed to 360 million, growing to over 600 million the year after. Twitter, by contrast, grew somewhat later, reaching 100 million monthly active users in Q3 2011. Social media usage is more common among those who are younger, but Chart 3 highlights that usage has risen over time for all age groups. As of Q1 2021, 81% of Americans aged 30-49 reported using at least one social media website, compared to 73% of those aged 50-64 and 45% of those aged 65 and over. Chart 4 highlights that the usage of Twitter skews in particular toward the young, and that, by contrast, Facebook and YouTube are the social media platforms of choice among older Americans. Chart 1Facebook: Monthly Active Users

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

Chart 2Twitter: Monthly Active Users Worldwide

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

Chart 3A Sizeable Majority Of US Adults Regularly Use Social Media

A Sizeable Majority Of US Adults Regularly Use Social Media

A Sizeable Majority Of US Adults Regularly Use Social Media

Chart 4Older Americans Use Facebook Far More Than Twitter

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

As a final point documenting the development and significance of social media, Chart 5 highlights that more Americans now report consuming news often (roughly once per day) from a smartphone, computer, or tablet other than from television. Radio and print have been completely eclipsed as sources of frequent news. The major news publications themselves are often promoted through social media, but the rise of the Internet has weighed heavily on the journalism industry. Social media has, for better and for worse, enabled the rapid proliferation of alternative news, citizen journalism, rumor, conspiracy theories, and foreign disinformation. Chart 5Social Media Has Changed The Way People Consume News

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Link Between Social Media And Post-GFC Austerity Following the 2008-2009 global financial crisis (GFC), there have been at least five deeply impactful non-monetary shocks to the US and global economies that have contributed to the disconnection between growth and interest rates: A prolonged period of US household deleveraging from 2008-2014 The Euro Area sovereign debt crisis Fiscal austerity in the US, UK, and Euro Area from 2010 – 2012/2014 The US dollar / oil price shock of 2014 The rise of populist economic policies, such as the UK decision to leave the European Union, and the US-initiated trade war of 2018-2019. Among these shocks to growth, social media has had a clear impact on two of them. In the case of austerity in the aftermath of the Great Recession, a sharp rise in fiscal conservatism in 2009 and 2010, emblematized by the rise of the US Tea Party, profoundly affected the 2010 US midterm elections. It is not surprising that there was a fiscally conservative backlash following the crisis: the US budget deficit and debt-to-GDP ratio soared after the economy collapsed and the government enacted fiscal stimulus to bail out the banking system. And midterm elections in the US often lead to significant gains for the opposition party However, Tea Party supporters rapidly took up a new means of communicating to mobilize politically, and there is evidence that this contributed to their electoral success. Chart 6 illustrates that the number of tweets with the Tea Party hashtag rose significantly in 2010 in the lead-up to the election, which saw the Republican Party take control of the House of Representatives as well as the victory of several Tea Party-endorsed politicians. Table 1 highlights that Tea Party candidates, who rode the wave of fiscal conservatism, significantly outperformed Democrats and non-Tea Party Republicans in the use of Twitter during the 2010 campaign, underscoring that social media use was a factor aiding outreach to voters. Chart 6Tea Party Supporters Rapidly Adopted Social Media To Mobilize Politically

Tea Party Supporters Rapidly Adopted Social Media To Mobilize Politically

Tea Party Supporters Rapidly Adopted Social Media To Mobilize Politically

Table 1Tea Party Candidates Significantly Outperformed In Their Use Of Social Media

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

And while it is more difficult to analyze the use and impact of Facebook by Tea Party candidates and supporters owing to inherent differences in the structure of the Facebook platform, interviews with core organizers of both the Tea Party and Occupy Wall Street movements have noted that activists in these ideologically opposed groups viewed Facebook as the most important social networking service for their political activities.1 Under normal circumstances, we agree that fiscal policy should be symmetric, with reduced fiscal support during economic expansions following fiscal easing during recessions. But in the context of multi-year household deleveraging, the fiscal drag that occurred in following the 2010 midterm elections was clearly a policy mistake. This mistake occurred partially under full Democratic control of government and especially under a gridlocked Congress after 2010. Chart 7 highlights that the contribution to growth from government spending turned sharpy negative in 2010 and continued to subtract from growth for some time thereafter. In addition, panel of Chart 7 highlights that the US economic policy uncertainty index rose in 2010 after falling during the first year of the recovery, reaching a new high in 2011 during the Tea Party-inspired debt ceiling crisis. Chart 7The Fiscal Drag That Followed The 2010 Midterm Elections Was A Clear Policy Mistake

The Fiscal Drag That Followed The 2010 Midterm Elections Was A Clear Policy Mistake

The Fiscal Drag That Followed The 2010 Midterm Elections Was A Clear Policy Mistake

In addition to the negative impact of government spending on economic growth, this extreme uncertainty very likely damaged confidence in the economic recovery, contributing to the subpar pace of growth in the first half of the last economic expansion. Chart 8 highlights the weak evolution in real per capita GDP from 2009-2019 compared with previous economic cycles, which was caused by a prolonged household balance sheet recovery process that was made worse by policy mistakes. To be sure, the UK and the EU did not have a Tea Party, and yet political elites imposed fiscal austerity. It is also the case that President Obama was the first president to embrace social media as a political and public relations tool. So it cannot be said that either social media or the Republican Party are uniquely to blame for the policy mistakes of that era. But US fiscal policy would have been considerably looser in the 2010s if not for the Tea Party backlash, which was partly enabled by social media. Too tight of fiscal policy in turn fed populism and produced additional policy mistakes down the road. Chart 8Policy Mistakes Significantly Contributed To Last Cycle's Subpar Growth Profile

Policy Mistakes Significantly Contributed To Last Cycle's Subpar Growth Profile

Policy Mistakes Significantly Contributed To Last Cycle's Subpar Growth Profile

From Fiscal Drag To Populism While social media is clearly not the root cause of the recent rise of populist policies, it has had a hand in bringing them about – in both a direct and indirect manner. The indirect link between social media use and the rise in populist policies has mainly occurred through the highly successful use of social media by international terrorist organizations (chiefly ISIL) and its impact on sentiment toward immigration in several developed market economies. Chart 9 highlights that public concerns about immigration and race in the UK began to rise sharply in 2012, in lockstep with both the rise in UK immigrants from EU accession countries and a series of events: the Syrian refugee crisis, the establishment and reign of the Islamic State, and three major terrorist attacks in European countries for which ISIL claimed responsibility. Given that the main argument for “Brexit” was for the UK to regain control over its immigration policies, these events almost certainly increased UK public support for withdrawing from the EU. In other words, it is not clear that Brexit would have occurred (at least at that moment in time) without these events given the narrow margin of victory for the “leave” campaign. The absence of social media would not have prevented the rise of ISIL, as that occurred in response to the US’s precipitous withdrawal from Iraq. The inevitable rise of ISIL would still have generated a backlash against immigration. Moreover, fiscal austerity in the UK and EU also fed other grievances that supported the Brexit movement. But social media accelerated and amplified the entire process. Chart 10 presents fairly strong evidence that Brexit weakened UK economic performance relative to the Euro Area prior to the pandemic, with the exception of the 2018-2019 period. In this period Euro Area manufacturing underperformed during the Trump administration’s trade war as a result of its comparatively higher exposure to automobile production and its stronger ties to China. Panel 2 highlights that GBP-EUR fell sharply in advance of the referendum, and remains comparatively weak today. Chart 9Terrorism And Immigration Likely Contributed To Brexit

Terrorism And Immigration Likely Contributed To Brexit

Terrorism And Immigration Likely Contributed To Brexit

Chart 10Brexit Weakened UK Economic Performance Prior To The Pandemic

Brexit Weakened UK Economic Performance Prior To The Pandemic

Brexit Weakened UK Economic Performance Prior To The Pandemic

Turning to the US, Donald Trump’s election as US President in 2016 was aided by both the direct and indirect effects of social media. In terms of indirect effects, Trump benefited from similar concerns over immigration and terrorism that caused the UK to leave the EU: Chart 11 highlights that terrorism and foreign policy were second and third on the list of concerns of registered voters in mid-2016, and Chart 12 highlights that voters regarded Trump as the better candidate to defend the US against future terrorist attacks. Chart 11Terrorism Ranked Highly As An Issue In The 2016 US Election

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

Chart 12Voters Regarded Trump As Better Equipped To Defend Against Terrorism

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

Trump’s election; and the enactment of populist policies under his administration, were directly aided by Trump’s active use of social media (mainly Twitter) to boost his candidacy. Chart 13 highlights that there were an average of 15-20 tweets per day from Trump’s Twitter account from 2013-2015, and 80% of those tweets occurred before he announced his candidacy for president in June 2015. This strongly underscores that Trump mainly used Twitter to lay the groundwork for his candidacy as an unconventional political outsider rather than as a campaign tool itself, which distinguishes his use of social media from that of other politicians. In other words, new technology disrupted the “good old boys’ club” of traditional media and elite politics. Chart 13Trump Used Twitter To Lay The Groundwork For His Candidacy

Trump Used Twitter To Lay The Groundwork For His Candidacy

Trump Used Twitter To Lay The Groundwork For His Candidacy

Chart 14The Trump Tax Cuts A Huge Rise In Corporate Earnings

The Trump Tax Cuts A Huge Rise In Corporate Earnings

The Trump Tax Cuts A Huge Rise In Corporate Earnings

Some policies of the Trump administration were positive for financial markets, and it is fair to say that Trump fired up animal spirits to some extent: Chart 14 highlights that the Tax Cuts and Jobs Act caused a significant rise in stock market earnings per share. But the Trump tax cuts were a conventional policy pushed mostly by the Congressional leadership of the Republican Party, and they did not meaningfully boost economic growth. Chart 15 highlights that, while the US ISM manufacturing index rose sharply in the first year of Trump’s administration, an uptrend was already underway prior to the election as a result of a significant improvement in Chinese credit growth and a recovery in oil prices after the devastating collapse that took place in 2014-2015. Chart 15But The Tax Cuts Did Not Do Much To Boost Growth

But The Tax Cuts Did Not Do Much To Boost Growth

But The Tax Cuts Did Not Do Much To Boost Growth

Similarly, Chart 15 highlights that the Trump trade war does not bear the full responsibility of the significant slowdown in growth in 2019, as China’s credit impulse decelerated significantly between the passage of the Tax Cuts and Jobs Act and the onset of the trade war because Chinese policymakers turned to address domestic concerns. But Chart 16 highlights that the aggressive imposition of tariffs, especially between the US and China, caused an explosion in trade uncertainty even when measured on an equally-weighted basis (i.e., when overweighting trade uncertainty, in countries other than the US and China), which undoubtedly weighed on the global economy and contributed to a very significant slowdown in US jobs growth in 2019 (panel 2). Moreover, Chinese policymakers responded to the trade onslaught by deleveraging, which weighed on the global economy; and consolidating their grip on power at home. In essence, Trump was a political outsider who utilized social media to bypass the traditional media and make his case to the American people. Other factors contributed to his surprising victory, not the least of which was the austerity-induced, slow-growth recovery in key swing states. While US policy was already shifting to be more confrontational toward China, the Trump administration was more belligerent in its use of tariffs than previous administrations. The trade war thus qualifies as another policy shock that was facilitated by the existence of social media. Chart 16The Trade War Caused An Explosion In Global Trade Uncertainty

The Trade War Caused An Explosion In Global Trade Uncertainty

The Trade War Caused An Explosion In Global Trade Uncertainty

Viewing Social Media As A Negative Productivity-Innovation A rise in fiscal conservatism leading to misguided austerity, the UK’s decision to leave the European Union, and the Trump administration’s trade war have represented significant non-monetary shocks to both the US and global economies over the past 12 years. These shocks strongly contributed to the subpar growth profile of the last economic expansion, as demonstrated above. Given the above, it is reasonable for investors to view social media as a technological innovation with negative productivity growth, given that it has facilitated policy mistakes during the last economic expansion. Chart 17 underscores this point, by highlighting that multi-factor productivity growth has been extremely weak in the post-GFC environment. While productivity is usually driven by supply-side factors over the longer term, it has a cyclical component to it – and in the case of the last economic expansion, the cyclical component was long lasting in nature. Any forces negatively impacting economic growth that do not change the factors of production necessarily reduce measured productivity; it is for this reason that measured productivity declines during recessions; and policy mistakes negatively impact productivity growth. Chart 17Policy Mistakes, Partially Enabled By Social Media, Reduced Productivity During The Last Expansion

Policy Mistakes, Partially Enabled By Social Media, Reduced Productivity During The Last Expansion

Policy Mistakes, Partially Enabled By Social Media, Reduced Productivity During The Last Expansion

Chart 18State & Local Government Finances Are In Much Better Shape Today

State & Local Government Finances Are In Much Better Shape Today

State & Local Government Finances Are In Much Better Shape Today

The Risk Of Aggressive Austerity Seems Low Today… Fiscal austerity in the early phase of the last economic cycle was the first social media-linked shock that we identified, but the risk of aggressive austerity appears low today. Much of the fiscal drag that occurred in the aftermath of the global financial crisis happened because of insufficient financial support to state and local governments – and the subsequent refusal by Congress to authorize more aid. But Chart 18 highlights that state and local government finances have already meaningfully recovered, on the back of bipartisan stimulus in 2020, while the American Rescue Plan provides significant additional funding. While it is true that US fiscal policy is set to detract from growth over the coming 6-12 months, this will merely reflect the unwinding of fiscal aid that had aimed to support household income temporarily lost, as a result of a drastic reduction in services spending. As we noted in last month’s report,2 goods spending will likely slow as fiscal thrust turns to fiscal drag, but services spending will improve meaningfully – aided not just by a post-pandemic normalization in economic activity, but also by the deployment of some of the sizable excess savings that US households have accumulated over the past year. Fiscal drag will also occur outside of the US next year. For example, the IMF is forecasting a two percentage point increase in the Euro Area’s cyclically-adjusted primary budget balance, which would represent the largest annual increase over the past two decades. But here too the reduction in government spending will reflect the end of pandemic-related income support, and is likely to occur alongside a positive private-sector services impulse. During the worst of the Euro Area sovereign debt crisis, the impact of austerity was especially acute because it was persistent, and it occurred while the output gap was still large in several Euro Area economies. Chart 19 highlights that Euro Area fiscal consolidation from 2010-2013 was negatively correlated with economic activity during that period, and Chart 20 highlights that, with the potential exception of Spain, this austerity does not appear to have led to subsequently stronger rates of growth. Chart 19Euro Area Austerity Lowered Growth During The Consolidation Phase…

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

Chart 20…And Did Not Seem To Subsequently Raise Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

This experiment in austerity led the IMF to conclude that fiscal multipliers are indeed large during periods of substantial economic slack, constrained monetary policy, and synchronized fiscal adjustment across numerous economies.3 Similarly, attitudes about austerity have shifted among policymakers globally in the wake of the populist backlash. Given this, despite the significant increase in government debt levels that has occurred as a result of the pandemic, we strongly doubt that advanced economies will attempt to engage in additional austerity prematurely, i.e., before unemployment rates have returned close-to steady-state levels. …But The Risk Of Protectionism And Other Populist Measures Looms Large The role that social media has played at magnifying populist policies should be concerning for investors, especially given that there has been a rising trend towards populism over the past 20 years. In a recent paper, Funke, Schularick, and Trebesch have compiled a cross-country database on populism dating back to 1900, defining populist leaders as those who employ a political strategy focusing on the conflict between “the people” and “the elites.” Chart 21 highlights that the number of populist governments worldwide has risen significantly since the 1980s and 1990s, and Chart 22 highlights that the economic performance of countries with populist leaders is clearly negative. Chart 21Populism Has Been On The Rise For The Past 30 Years

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The authors found that countries’ real GDP growth underperformed by approximately one percentage point per year after a populist leader comes to power, relative to both the country’s own long-term growth rate and relative to the prevailing level of global growth. To control for the potential causal link between economic growth and the rise of populist leaders, Chart 23 highlights the results of a synthetic control method employed by the authors that generates a similar conclusion to the unconditional averages shown in Chart 22: populist economic policies are significantly negative for real economic growth. Chart 22Populist Leaders Are Clearly Growth Killers Even After…

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

Chart 23… Controlling For The Odds That Weak Growth Leads To Populism

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

The Social Media Magnification Effect: Austerity, Populism, And Slower Growth

This is especially concerning given that wealth and income inequality, perhaps the single most important structural cause of rising populism and political polarization, is nearly as elevated as it was in the 1920s and 1930s (Chart 24). This trend, at least in the US, has been exacerbated by a decline in public trust of mainstream media among independents and Republicans that began in the early 2000s and helped to fuel the public’s adoption of alternative news and social media. The decline in trust clearly accelerated as a result of erroneous reporting on what turned out to be nonexistent weapons of mass destruction in Iraq and other controversies of the Bush administration. Chart 21 showed that the rise in populism has also yet to abate, suggesting that social media has the potential to continue to amplify policy mistakes for the foreseeable future. Chart 24Inequality: The Most Important Structural Cause Of Populism And Polarization

Inequality: The Most Important Structural Cause Of Populism And Polarization

Inequality: The Most Important Structural Cause Of Populism And Polarization

It is not yet clear what economic mistakes will occur under the Biden administration, but investors should not rule out the possibility of policies that are harmful for growth. The likely passage of a bipartisan infrastructure bill or a partisan reconciliation bill in the second half of this year will most likely be the final word on fiscal policy until at least 2025,4 underscoring that active fiscal austerity is not likely a major risk to investors. Spending levels will probably freeze after 2022: Republicans will not be able to slash spending, and Democrats will not be able to hike spending or taxes, if Republicans win at least one chamber of Congress in the midterms (as is likely). Biden has preserved the most significant of Trump’s protectionist policies by maintaining US import tariffs against China, and the lesson from the Tea Party’s surge following the global financial crisis is that major political shifts, magnified by social media, can manifest themselves as policy with the potential to impact economic activity within a two-year window. Attitudes toward China have shifted negatively around the world because of deindustrialization and now the pandemic.5 White collar workers in DM countries have clearly fared better during lockdowns than those of lower-income households. This has created extremely fertile ground for a revival in populist sentiment, which could force the Biden administration or Congressional Democrats toward protectionist or otherwise populist actions over the coming year, in the lead up to the 2022 mid-term elections. Investment Conclusions In this report, we have documented the historical link between social media, populism, and policy mistakes during the last economic expansion. It is clear that neither social media nor even populism is solely responsible for all mistakes – the UK’s and EU’s ill-judged foray into austerity was driven by elites. Furthermore, we have not addressed in this report the impact of populism on actions of emerging markets, such as China and Russia, whose own behavior has dealt disinflationary blows to the global economy. Nevertheless, populism is a potent force that clearly has the power to harness new technology and deliver shocks to the global economy and financial markets. The risks of additional mistakes from populism are still present, and that is even before considering other risks to society from social media: a reduction in mental health among young social media users, and the role that social media has played in spreading misinformation – contributing to the vaccine hesitancy in some DM countries that we discussed in Section 1 of our report. Two investment conclusions emerge from our analysis. First, we noted in our April report that there is a chance that investor expectations for the natural rate of interest (“R-star”) will rise once the economy normalizes post-pandemic, but that this will likely not occur as long as investors continue to believe in the narrative of secular stagnation. Despite the fact that the past decade’s shocks occurred against the backdrop of persistent household deleveraging (which has ended in the US), these shocks reinforced that narrative, and any additional policy shocks following a return to economic normality will again be seen by both investors and the Fed as strong justification for low interest rates. Thus, while the rapid closure of output gaps in advanced economies over the coming year argues for both cyclically and structurally higher bond yields, a revival in protectionist sentiment is a risk to this view that we will be closely monitoring over the coming 12-24 months. Second, for tech investors, the bipartisan shift in public sentiment to become more critical of social media companies is gradually becoming a real risk, potentially affecting user growth. Based solely on Facebook, Twitter, Pinterest, and Snapchat, social media companies do not account for a very significant share of the overall equity market (Chart 25), suggesting that the impact of a negative shift in sentiment toward social media companies would not be an overly significant event for equity investors in general. Chart 25 highlights that the share of social media companies as a percent of the broad tech sector rises if Google is included; YouTube accounts for less than 15% of Google’s total advertising revenue, however, suggesting modest additional exposure beyond the solid line in Chart 25. Chart 25The Underperformance Of Social Media Would Not Excessively Weigh On The Broad Market

The Underperformance Of Social Media Would Not Excessively Weigh On The Broad Market

The Underperformance Of Social Media Would Not Excessively Weigh On The Broad Market

Still, investors with concentrated positions in social media stocks should be aware of the potential idiosyncratic risks facing social media companies as a result of the public’s impression of the impact of social media on society. If social media companies come to be widely associated with political gridlock, the polarization of society, and failed economic policies (as already appears to be the case), then the fundamental performance of these stocks is likely to be quite poor regardless of whether or not tech companies ultimately enjoy a relatively friendly regulatory environment under the Biden administration. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 Grassroots Organizing in the Digital Age: Considering Values and Technology in Tea Party and Occupy Wall Street by Agarwal, Barthel, Rost, Borning, Bennett, and Johnson, Information, Communication & Society, 2014. 2 Please see The Bank Credit Analyst “July 2021,” dated June 24, 2021, available at bca.bcaresearch.com 3 “Are We Underestimating Short-Term Fiscal Multipliers?”,IMF World Economic Outlook, October 2012 4 Please see US Political Strategy Outlook "Third Quarter Outlook 2021: Game Time," dated June 30, 2021, available at usps.bcaresearch.com 5 “Unfavorable Views of China Reach Historic Highs in Many Countries,” PEW Research Center, October 2020.

Highlights The countertrend yield rally is near its end. Despite the deteriorating Chinese credit impulse, the outlook for global growth remains robust. An ample global liquidity backdrop, an inventory restocking cycle, and an upbeat capex outlook will increase aggregate demand and global capacity utilization. In this context, safe-haven bonds have sufficiently rallied. German yields will rise too, because the European yield curve will steepen. European banks will benefit from this trend. Investors should buy European momentum stocks and sell growth stocks. Investors should favor industrial equities and Sweden. Feature On April 12 of this year, we warned that a countertrend rally in bonds was increasingly likely. The decline in the Chinese credit impulse and the increasingly oversold state of Treasuries created the perfect conditions to generate disappointments in a lopsided market. As a corollary, we grew worried about our equity positioning, which calls for a large exposure to pro-cyclical stocks. Consequently, we recommended investors hedge this portfolio bias with some defensive bets. On July 20, Treasury yields fell to as low as 1.13%. Did this level mark the end of the Treasury rally? The bulk of the decline is behind us, and investors with a 12- to 18-month investment horizon should resume shortening portfolio duration. In Europe too, German yields are likely to trend higher. As a result, European financials and momentum stocks should generate significant outperformance in the coming quarters. Industrial equities are also set to shine, which will benefit the Swedish market, our favorite. Should I Stay Or Should I Go? The near-term outlook for Treasuries is currently more complex than it was in April, when forces lined up neatly to warn of an imminent pullback in yields. Technical indicators show that the oversold conditions that prevailed this spring have mostly cleared up. In April, the BCA Composite Technical Indicator for Treasuries reached its most oversold level in more than 20 years, which provided a very reliable buy signal (Chart 1). Now that the 10-year yield has reclaimed its 40-week moving average, the technical indicator is back to neutral. Normally, when bonds are in a cyclical bear market, which is BCA’s House View, the indicator rarely dips significantly into overbought territory. Meanwhile, the Marketvane Bullish Sentiment survey stands at 60%, which indicates that bonds are once again favored by many newsletters, traders, and investors. Chinese credit growth continues to send a bond-bullish signal (Chart 2). Slowing credit growth could hurt Chinese capex, which in turn has the potential to slow the demand for capital at the global level. This risk could still decrease global yields. Chart 1Bonds Are Not Oversold Anymore...

Bonds Are Not Oversold Anymore...

Bonds Are Not Oversold Anymore...

Chart 2...But China Still Consistutes A Risk

...But China Still Consistutes A Risk

...But China Still Consistutes A Risk

Chart 3A Synchronous Global Upswing

A Synchronous Global Upswing

A Synchronous Global Upswing

The global economic recovery remains sufficiently broad-based to compensate for the risk of a Chinese slowdown. Our Global Synchronicity Indicator shows that manufacturing PMIs among the world’s major economies are all expanding (Chart 3), which usually elevates yields. This is especially important today, because the far-reaching and generalized nature of the current recovery gives more scope to the global economy to withstand a Chinese economic deceleration. Bottom Line: The variables that called for lower yields in early April are currently sending a mixed message. “Go!” The Global Business Cycle Responds Outside of China’s TSF impulse, most economic variables point toward higher yields. Chart 4Financial Liquidity Lifts The Business Cycle

Financial Liquidity Lifts The Business Cycle

Financial Liquidity Lifts The Business Cycle

Global liquidity conditions remain consistent with higher growth and thus also with rising global interest rates. BCA’s US Financial Liquidity Index still stands near record highs and confirms that the Global Leading Economic Indicator (LEI) will remain at elevated levels (Chart 4). As a result, we expect the current fall in the Global LEI Diffusion Index to be short lived. Any softening in global growth, therefore, will prove to be transitory. Markets are forward looking. The recent decline in yields anticipated the deceleration in the Global LEI. Long-term rates will also increase before the LEI firms anew. Excess money growth tells a similar story. Historically, an expansion of the global money supply in excess of the demand for credit sends a strong signal that global economic activity is well supported by reflationary policies. It forecasts above-trend industrial production growth, robust international trade and rising global export prices. Currently, excess money growth in the US, Eurozone and Japan has overtaken its post-GFC high and is consistent with higher US and German yields (Chart 5). Global capacity utilization also points toward higher yields. Our US Composite Capacity Utilization indicator is back in the neutral zone after a steep decline in 2020. Furthermore, US industrial capacity utilization is currently back above its structural trend. Most importantly, capacity utilization should be evaluated at the global level. Even when slower-growing economies such as the Euro Area and Japan are included, global capacity utilization is improving enough to be consistent with rising yields (Chart 6). Chart 5Excess Money Points To Higher Yields

Excess Money Points To Higher Yields

Excess Money Points To Higher Yields

Chart 6Rising CAPU Lifts Yields

Rising CAPU Lifts Yields

Rising CAPU Lifts Yields

Capacity utilization should climb higher in the coming quarters as the world experiences an inventory re-stocking cycle. The US, with its rich data, provides a good example. The sales-to-inventory ratio is at an extremely elevated level and is climbing very rapidly (Chart 7). Meanwhile, the level of inventories is still 1% below its pre-pandemic peak, while GDP overtook it previous high in the second quarter, and business sales are 11% above their 2018 high. The recent rise in inflation highlights the inability of companies to fulfil demand for their goods and services and, consequently, the need to restock. Hence, we expect companies to increase their inventory spending, which will add to demand and to capacity utilization as the adjustment process takes place. Capex will also lift capacity utilization and put upward pressure on yields. US capex intentions are rising swiftly as firms are unable to meet demand (Chart 8, top panel). Our Japanese Capex Indicator reiterates this message, while the European Commission’s Investment Surveys are also recovering (Chart 8 bottom panels). Historically, capex intentions are an excellent, leading indicator of actual investments, hence, the recent poor capex numbers will not last. Chart 7Restocking Ahead!

Restocking Ahead!

Restocking Ahead!

Chart 8Climbing Capex Intentions Everywhere

Climbing Capex Intentions Everywhere

Climbing Capex Intentions Everywhere

Greater global cash flow growth is also consistent with higher capex. The growth in EBITDA among global companies has bottomed, and it is currently around 14%. Incidentally, this suggests that capex among quoted firms around the world should expand in the second half of the year by a similar amount (Chart 9). Ultimately, robust cash flows finance expansion plans and also send a strong signal to corporate boards that the environment is ripe for investment spending. Already, capital goods orders are strengthening, which confirms the signal from both the capex surveys and profits. This strength portends very strong private capex numbers in the coming quarters and thus, a greater level of demand in the economy (Chart 10). Chart 9Rising Cash Flows Lead To Higher Capex

Rising Cash Flows Lead To Higher Capex

Rising Cash Flows Lead To Higher Capex

Chart 10Strong Global Orders

Strong Global Orders

Strong Global Orders

Public infrastructure plans will create the final boost to global capex. $550 billion of the Biden administration’s infrastructure plan is getting close to bipartisan approval, and the budget reconciliation process might still result in an even bigger package before yearend. In Europe, the EUR800 billion NGEU plan that has been approved by all the EU’s national parliaments also includes large infrastructure spending envelopes to deploy over the coming five years. This context suggests that yields are unlikely to decline much further from current levels, since the oversold conditions that prevailed in March have been purged. Chart 11 shows that specific events are needed to prompt a greater 90-trading day collapse in yields than the one just registered. In 2019 and 2020, the Fed was cutting rates. Today, it is gearing up to raise them. In 2010 and 2011, the European sovereign debt crisis was hurting global growth and creating massive deflationary risks. In 2015, China was mired in deep deflation and devalued the RMB, which exported these negative pressures around the world and lowered yields. By late 2018, the yield curve was moving toward an inversion, which signaled that monetary policy was too tight. Today, none of these conditions are present and, consequently, the odds of a greater decline in yields are low. Chart 11Yields Have Moved Enough

Yields Have Moved Enough

Yields Have Moved Enough

Bottom Line: The broad-based nature of the global recovery will limit the decline in yields. Global liquidity conditions remain extremely accommodative, global capacity utilization is improving, and inventories and capex spending will add to demand in the coming quarters. In this context, the recent decline in yields corrected this spring’s oversold condition in the bond market sufficiently. Investment Implications Bonds Investors with an investment horizon of more than six months should reduce their portfolio duration and remove hedges protecting against higher yields. The low in Treasury yields is likely to stay around 1.1%. The exact timing of the rebound is imprecise, and yields could churn for a brief period and retest their recent lows, but the balance of risks points toward a much greater probability of higher yields in the coming six to twelve months, and a limited probability of significantly lower yields from current levels. In fact, the CRB-to-gold ratio, often shown by BCA’s US bond strategists, clearly favors higher yields (Chart 12). Higher yields are not inconsistent with BCA’s view that the current inflation spike is transitory. TIPS yields are at a record low. As global growth recovers and the Fed moves closer to removing some accommodation, real yields will increase (Chart 13, top panel). Meanwhile, 5-year/5-year forward inflation breakeven rates remain well below the 2.5%-to-3% zone that prevailed prior to 2014, when long-term inflation expectations were still well anchored (Chart 13, bottom panel). The Fed is actively aiming to push this inflation expectation measure higher. Chart 12The CRB/Gold Ratio Points To Higher Yields

The CRB/Gold Ratio Points To Higher Yields

The CRB/Gold Ratio Points To Higher Yields

Chart 13TIPS Yields Will Rise

TIPS Yields Will Rise

TIPS Yields Will Rise

Chart 14The European Yield Curve Will Steepen

The European Yield Curve Will Steepen

The European Yield Curve Will Steepen

German yields have some upside too, even if the ECB will lag well behind the Fed in terms of both ending its QE program and lifting interest rates. The ECB policy rate mostly anchors the short end of the curve, and the large European excess savings warrant lower Bund yields than those of T-Note. However, the nominal and real terminal rates embedded in the German curve remain lower than at the apex of the European sovereign debt crisis and are extremely low compared to the US. As a result, the European yield curve will steepen, which is confirmed by the comparative strength of the earnings revisions of Europe’s cyclical equity sectors (Chart 14). Equities An environment in which yields rise again should favor financials, industrials, and momentum stocks at the expense of growth stocks. In Europe, banks and financials will be the prime beneficiaries of higher yields. Historically, higher German Bund yields are associated with an outperformance of banks relative to the broad market, because a steeper yield curve boosts net interest margins (Chart 15). European banks also have scope for some re-rating. There is little case to significantly upgrade the sectors’ expected long-term profitability significantly, considering that the European economy remains replete with an excessively large capital stock. Nonetheless, at a price-to-book ratio of 0.6 or 55% below that of US banks and 67% below the European broad market, European banks are also priced as risky investments. However, European NPLs have declined significantly, and the public sector support during the pandemic will limit how high NPLs can rise (Chart 16, top panel). Moreover, European banks are much better capitalized than they once were, which further decreases their riskiness (Chart 16). Additionally, the ECB has allowed banks to pay dividends again. Finally, the fiscal risk sharing created by the NGEU funds and continued bond purchases by the ECB will cap the upside for peripheral yield spreads, which will limit the odds of the emergence of the kind of doom-loop that once plagued the European banking system. UK bank stocks look particularly attractive. Chart 15European Banks Have Upside

European Banks Have Upside

European Banks Have Upside

Chart 16Less Risky

Less Risky

Less Risky

The massive underperformance of European momentum stocks relative to growth stocks is also likely to reverse (Chart 17). As Chart 18 shows, momentum stocks currently trade at an exceptionally large discount to both growth stocks and the European broad market. Most importantly, momentum equities tend to outperform growth stocks in the wake of a rise in German yields (Chart 19). This sensitivity to yields is currently accentuated by the sector bias of momentum stocks. Relative to growth stocks, momentum equities greatest overweights are financials, industrials and materials (Table 1), three sectors that thrive on higher interest rates. Meanwhile, their largest relative underweights are consumer staples and healthcare, two sectors with strong defensive characteristics that benefit from lower yields. Chart 17Bomned Out Momentum Stocks...

Bomned Out Momentum Stocks...

Bomned Out Momentum Stocks...

Chart 18...Have Become Very Cheap

...Have Become Very Cheap

...Have Become Very Cheap

Chart 19Momentum Stocks Outperform When Yields Rise

Momentum Stocks Outperform When Yields Rise

Momentum Stocks Outperform When Yields Rise

Table 1Sector Biases: Momentum Vs Growth Stocks

The Ageing Bond Rally

The Ageing Bond Rally

Chart 20The Capex Outlook Favors Industrials

The Capex Outlook Favors Industrials

The Capex Outlook Favors Industrials

Finally, we recommend investors move more aggressively into industrial equities. Industrials are the best-placed sector to benefit from the rise in global capex and the excess money supply growth. As Chart 20 highlights, even if the rate of growth of global capital goods orders decelerates, industrials should outperform the European broad market as long as the rate of growth remains positive. Nonetheless, the sector’s outperformance could moderate because it has become more expensive than the broad market. However, a stronger profitability compensates for this negative. As a corollary, we continue to favor Swedish equities because of their 38% weight in industrials and 27% allocation to financials. Moreover, their superior return on equity and profit margins, as well as the EUR/SEK’s downside potential, add to Sweden’s allure. The largest risk for industrials remains the slowdown in the Chinese credit impulse. However, the upbeat picture for DM capex and inventory growth counters this negative side. We continue to recommend some hedges against this risk. When it comes to our Sweden overweight, we still advise selling Norway, a position that has worked out well. We also still like selling consumer discretionary equities / long European telecoms to protect portfolios against a greater-than-anticipated global slowdown. Bottom Line: Global safe-haven yields are unlikely to decline significantly from current levels. Instead, they will rise meaningfully in the coming quarters, even in Germany. Consequently, investors with an investment horizon greater than six months should curtail their portfolio duration once again. Higher yields will also benefit European bank equities. We also recommend investors buy European momentum stocks and sell growth stocks. Finally, European industrials are set to shine compared to the rest of the European market, which will give a fillip to Swedish stocks, our favored European market. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Currency Performance Currency Performance

The Ageing Bond Rally

The Ageing Bond Rally

Fixed Income Performance Government Bonds

The Ageing Bond Rally

The Ageing Bond Rally

Corporate Bonds

The Ageing Bond Rally

The Ageing Bond Rally

Equity Performance Major Stock Indices

The Ageing Bond Rally

The Ageing Bond Rally

Geographic Performance

The Ageing Bond Rally

The Ageing Bond Rally

Sector Performance

The Ageing Bond Rally

The Ageing Bond Rally

Highlights Economy – The Fed remains unperturbed about inflation, even as it continues to surprise to the upside: At his latest press conference, Chair Powell repeated the mantra that the spike in inflation will prove to be temporary. The shape of the inflation expectations curve supports the Fed’s view and the key expectations boxes of our inflation checklist remain unchecked. Markets – The decline in Treasury yields indicates that investors aren’t too worried about it, either: Although inflation data have continued to surprise to the upside, investors and the broader public seem to have moved on after the release of the March and April numbers. Inflation agita is not gone for good, but it may remain dormant until the fall. Strategy – The economic and policy backdrops remain favorable for risk assets and we remain overweight equities and spread product: Stop us if you’ve heard this one before, but risk assets will continue to generate positive excess returns over Treasuries and cash unless the Delta variant disrupts activity. Feature What a difference ten weeks make. When we rolled out our checklist on May 24th, inflation was Topic A for BCA clients and Google searchers, but it has been coming up less in our meetings and the internet queries are half of what they were (Chart 1). Inflation is a critical element of bond and currency markets, however, and it can have significant implications when it diverges from market expectations. Its currently elevated level and the novelty and uncertainty of the Fed’s revised approach to it ensure that it will intermittently command the spotlight. Chart 1Oh, Never Mind

Oh, Never Mind

Oh, Never Mind

Down the road, we think it has a good chance to break above a range that investors and policymakers are comfortable with, and we will review our inflation checklist every month or two to keep clients apprised of its course. We have checked the same three boxes that we did six weeks ago and the story from the charts underlying them is unchanged. Inflation remains well above 2% year-over-year and it will stay there for the foreseeable future. The Fed is nowhere close to deploying its tools to guide it back down to its stated target, however, so it presents no danger to the potent post-pandemic expansion, and households’ and businesses’ mindsets do not appear to have changed in any way that would presage a self-reinforcing dynamic that would feed an inflation spiral. If inflation isn’t going to become problematic any time soon, overheating is not a pressing risk over our twelve-month investment timeframe. If we are correct that the new Delta-powered wave of COVID infections will not strain the health care system’s capacity or spark an unsettling pickup in fatalities, we won’t need to increase our probability of a growth shortfall. From an investment strategy perspective, diminishing probabilities of too-hot and too-cold tail outcomes support continued risk-friendly positioning. The Goldilocks outcome of strong growth backed by ultra-accommodative monetary policy should allow risk assets to continue generating positive excess returns over Treasuries and cash over the next twelve months. Updating The Inflation Checklist Table 1Inflation Checklist

Resolute

Resolute

As mentioned above, we have checked the same three boxes on our inflation checklist that we did in late May and late June (Table 1). The labor market story remains unchanged: employer demand is at all-time highs as measured by the Job Openings components of the NFIB and JOLTS surveys (Chart 2). Labor supply has not risen to meet it, however, as a range of factors, including reduced caregiver availability (for children and adults), reluctance to risk infection and generous unemployment insurance benefits, converge to limit the number of job seekers. Though record demand and limited supply would be expected to lead to much higher prices, wage growth has remained contained (Chart 3), especially in the more refined series that adjust for composition effects or include benefits (Chart 3, bottom two panels). Chart 2Help Wanted

Help Wanted

Help Wanted

Chart 3Wage Growth Has Remained In Check

Wage Growth Has Remained In Check

Wage Growth Has Remained In Check

Year-over-year increases in core CPI and the core PCE price index have continued to accelerate (Chart 4, solid lines). They seem to have lost their ability to shock after April, however, as inflation expectations have taken little note of them and Google “inflation” searches have come off the boil. Investors apparently accept the Fed’s contention that the base inflation readings are being distorted by price moves in spaces that have been especially impacted by the pandemic and subsequent component shortages. Though the Fed's explanation may seem awfully convenient, its read is supported by the much more modest moves in the trimmed-mean CPI and PCE indexes (Chart 4, dashed lines). Chart 4Inflation Is Not Quite As Bad As It May Seem ...

Inflation Is Not Quite As Bad As It May Seem ...

Inflation Is Not Quite As Bad As It May Seem ...

We continue to check the inflation pipeline box as our Pipeline Inflation Pressure Index is still pointing steeply higher (Chart 5). With components like the CRB’s Raw Industrials Index showing no sign of letting up, pipeline pressures will not just go away. The dollar’s recovery is limiting inflation pressure from the import channel, though inflation is comparatively muted in both the euro zone (Chart 6, top panel) and China (Chart 6, bottom panel) in any event. Chart 5... But Its Got Legs

... But Its Got Legs

... But Its Got Legs

Chart 6Global Pressures Are Mild For Now

Global Pressures Are Mild For Now

Global Pressures Are Mild For Now

Chart 7Markets Are Looking Through Temporary Inflation Pressures ...

Markets Are Looking Through Temporary Inflation Pressures ...

Markets Are Looking Through Temporary Inflation Pressures ...

Chart 8... And So Are Consumers

... And So Are Consumers

... And So Are Consumers

We continue to view inflation expectations as the key to a meaningful inflection. If households, businesses and investors begin to anticipate a much higher rate of inflation over the longer term, they will change their behavior in ways that will cause their expectations to become self-fulfilling. We are therefore especially focused on the inflation expectations curve and have been relieved to see that market measures (Chart 7) and surveys (Chart 8) indicate that investors and other economic participants believe that an elevated rate of consumer price increases will not persist beyond the next year or two. As Table 2 illustrates, the inverted TIPS and CPI swaps expectations curves project a significant decline in inflation from the near term to the intermediate and long term. Table 2The Inflation Expectations Curve Is Solidly Inverted

Resolute

Resolute