United States

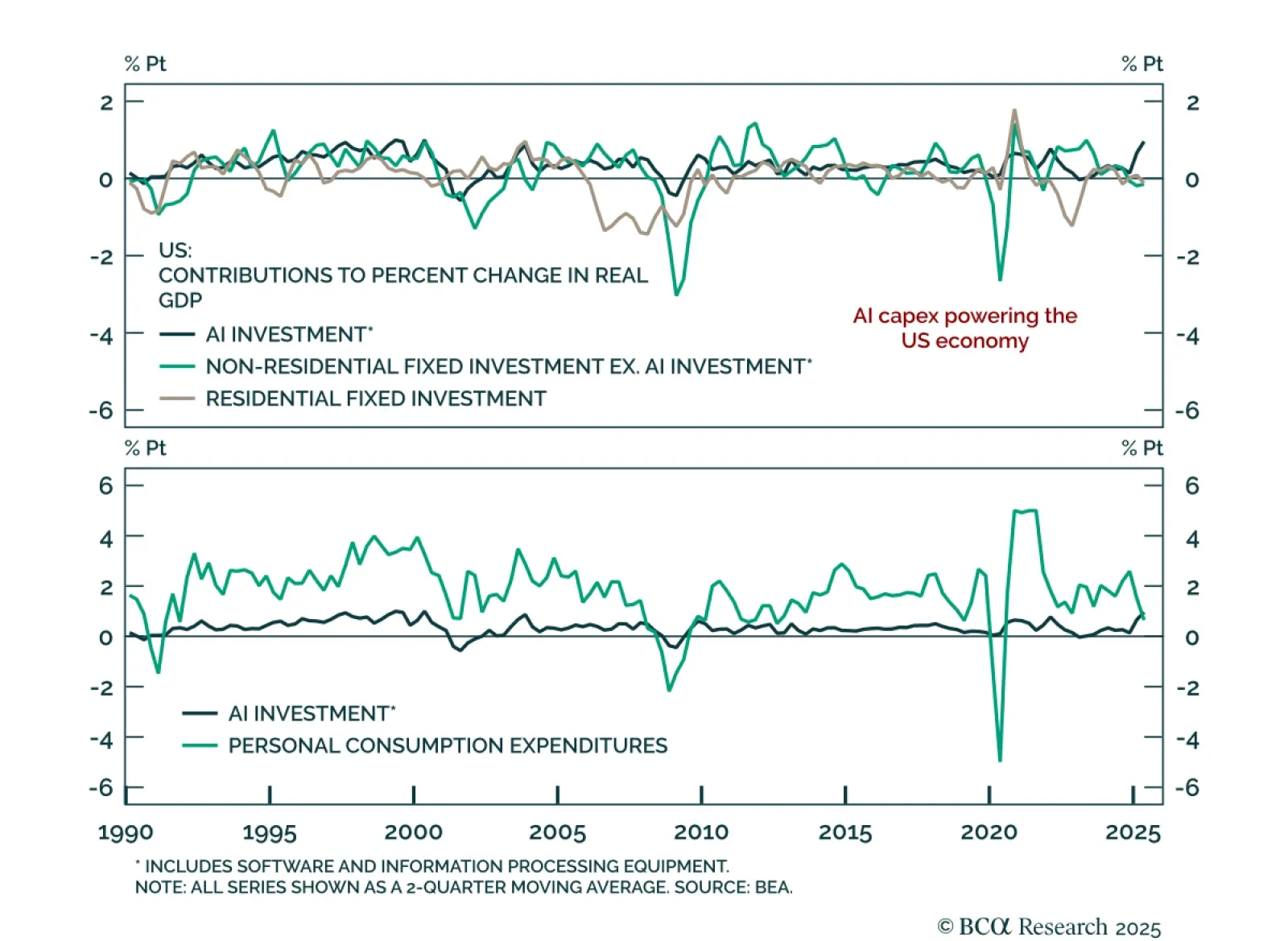

AI capex has emerged as the dominant driver of US growth in 2025, reshaping both macro dynamics and equity strategy. Our Chart Of The Week comes from Juan Correa, Chief Strategist for Global Asset Allocation.Over the first half of the year, AI-related…

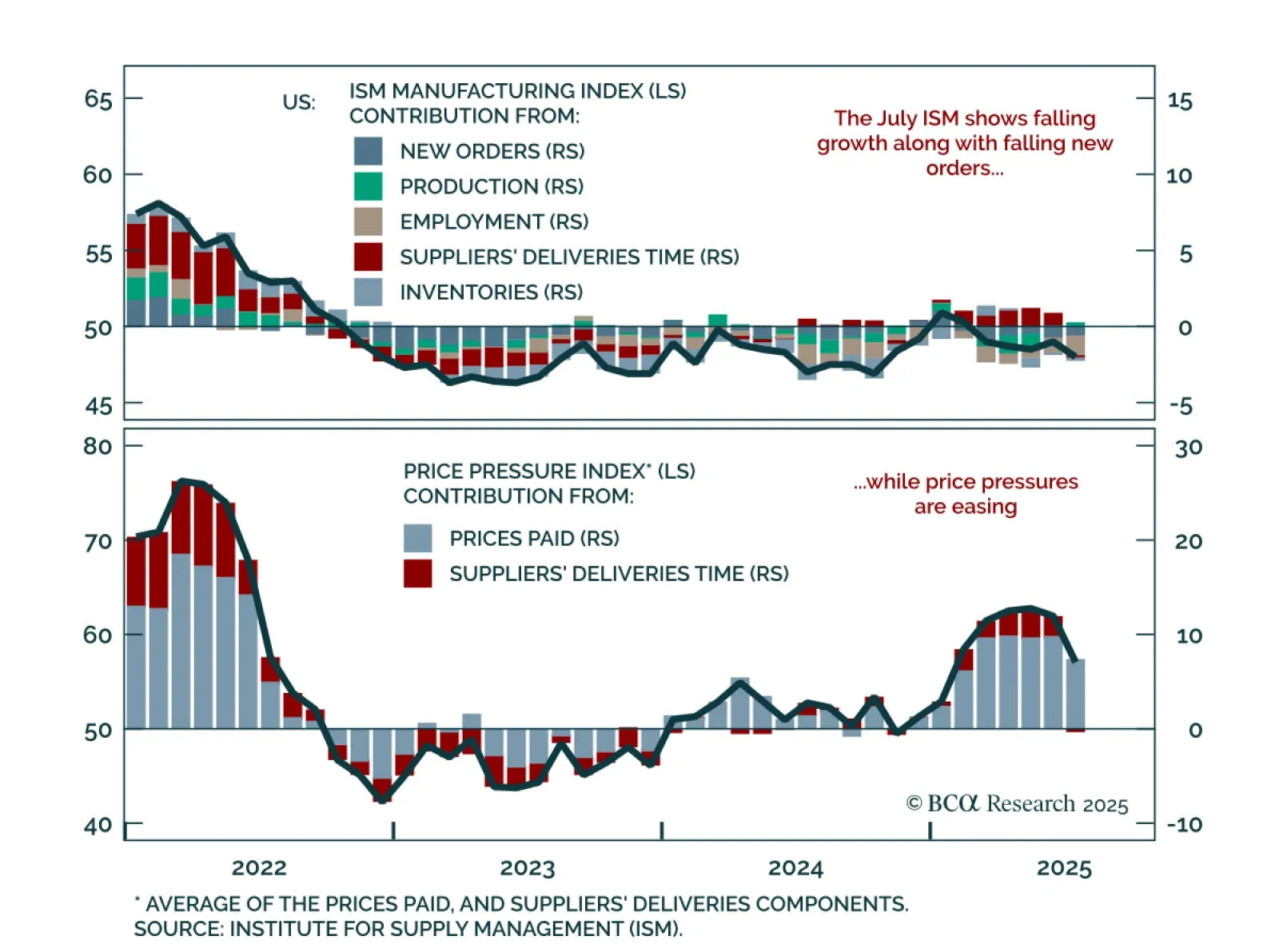

The July ISM Manufacturing miss shows weakening growth and decelerating inflation, reinforcing our long-duration stance. The index fell to 48.0 from 49.0, with only the production component contributing positively. New orders remain weak, and the drop in…

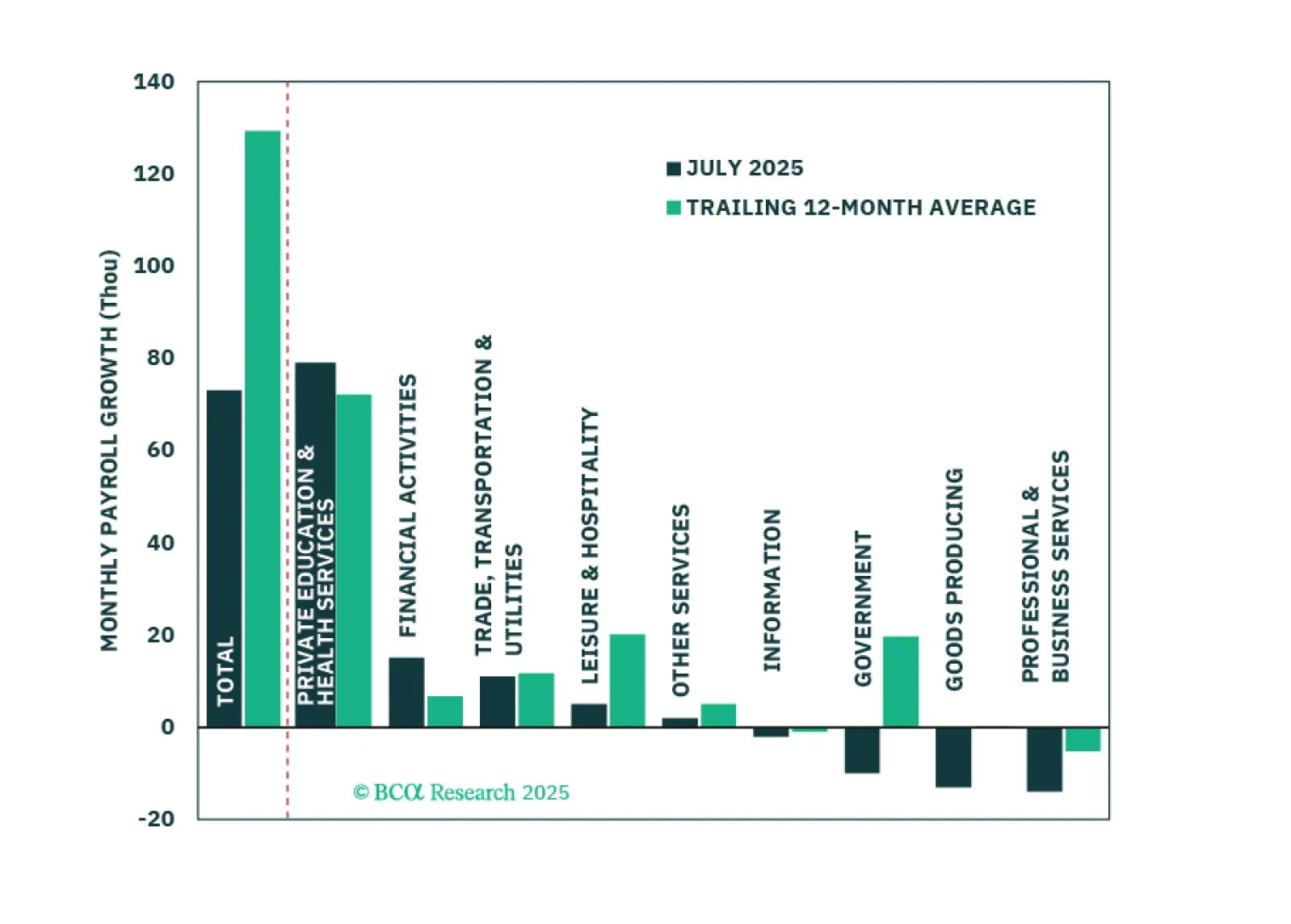

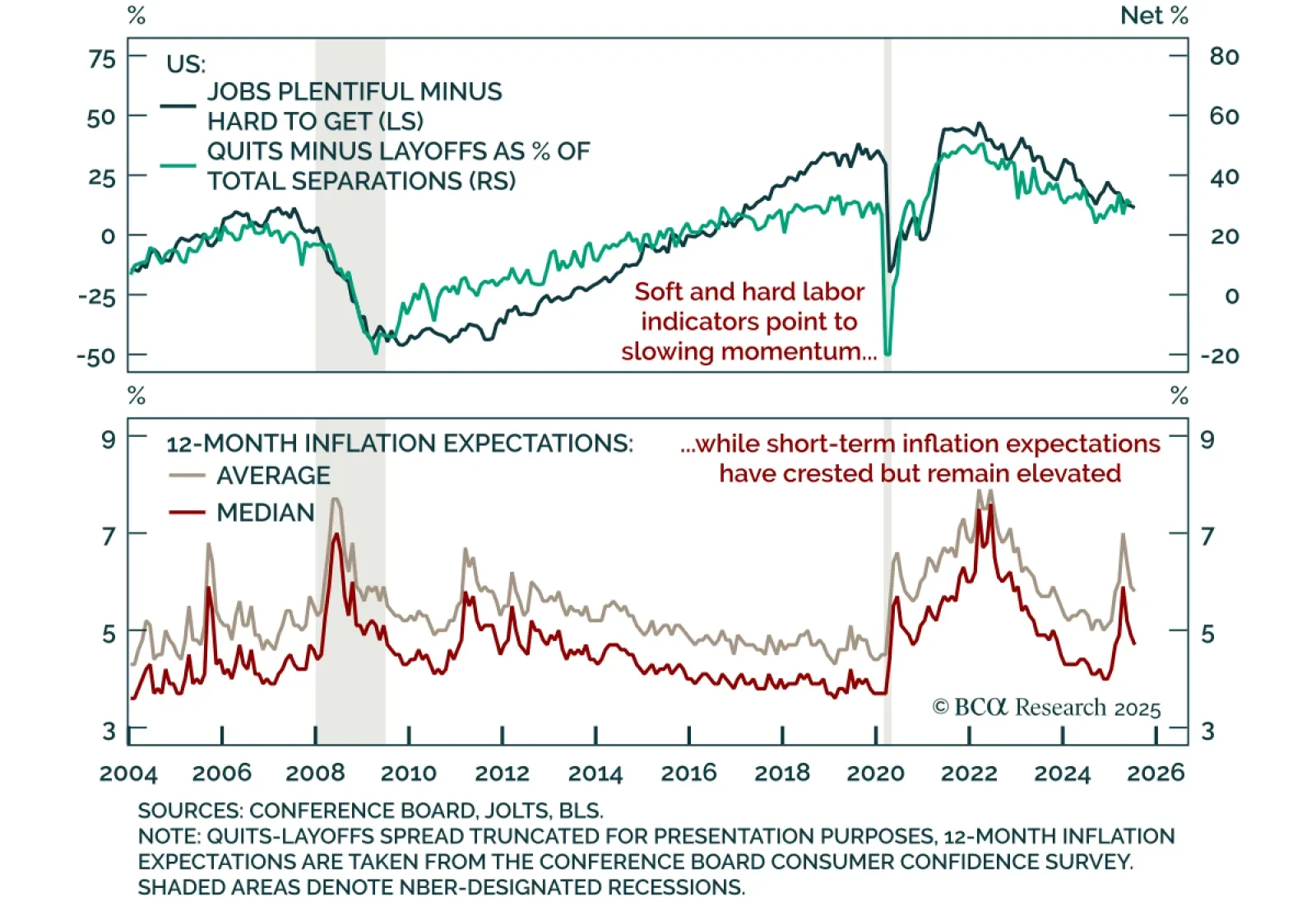

Economic activity and hiring cooled significantly in the first half of the year. The most important question for investors is whether this signals an imminent increase in labor market slack.

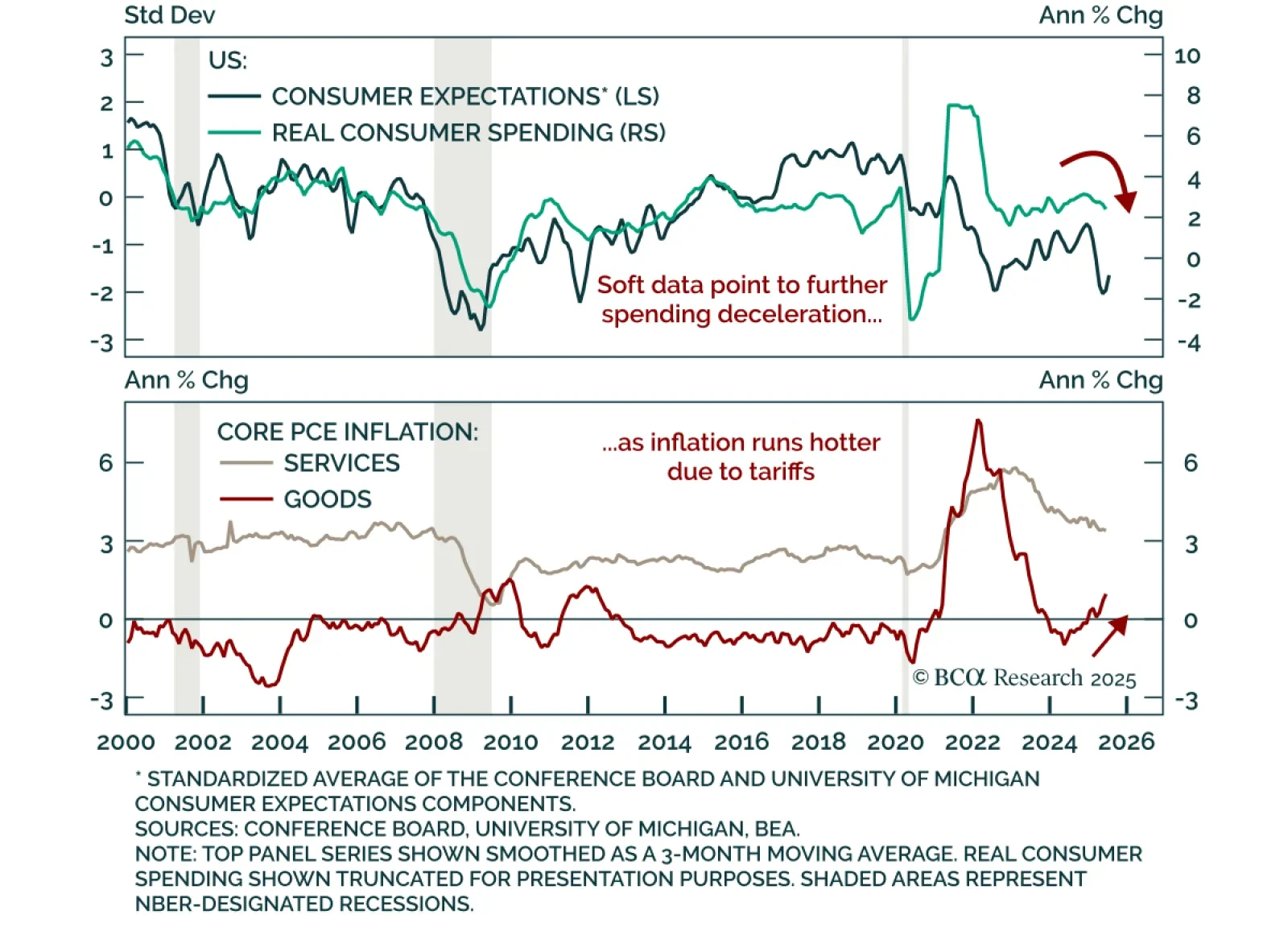

June US income and spending shows softening demand and rising goods inflation pressure, reinforcing our long-duration stance. Real personal spending only rose 0.1% m/m, in line with expectations. Personal income increased 0.3% m/m, but real income…

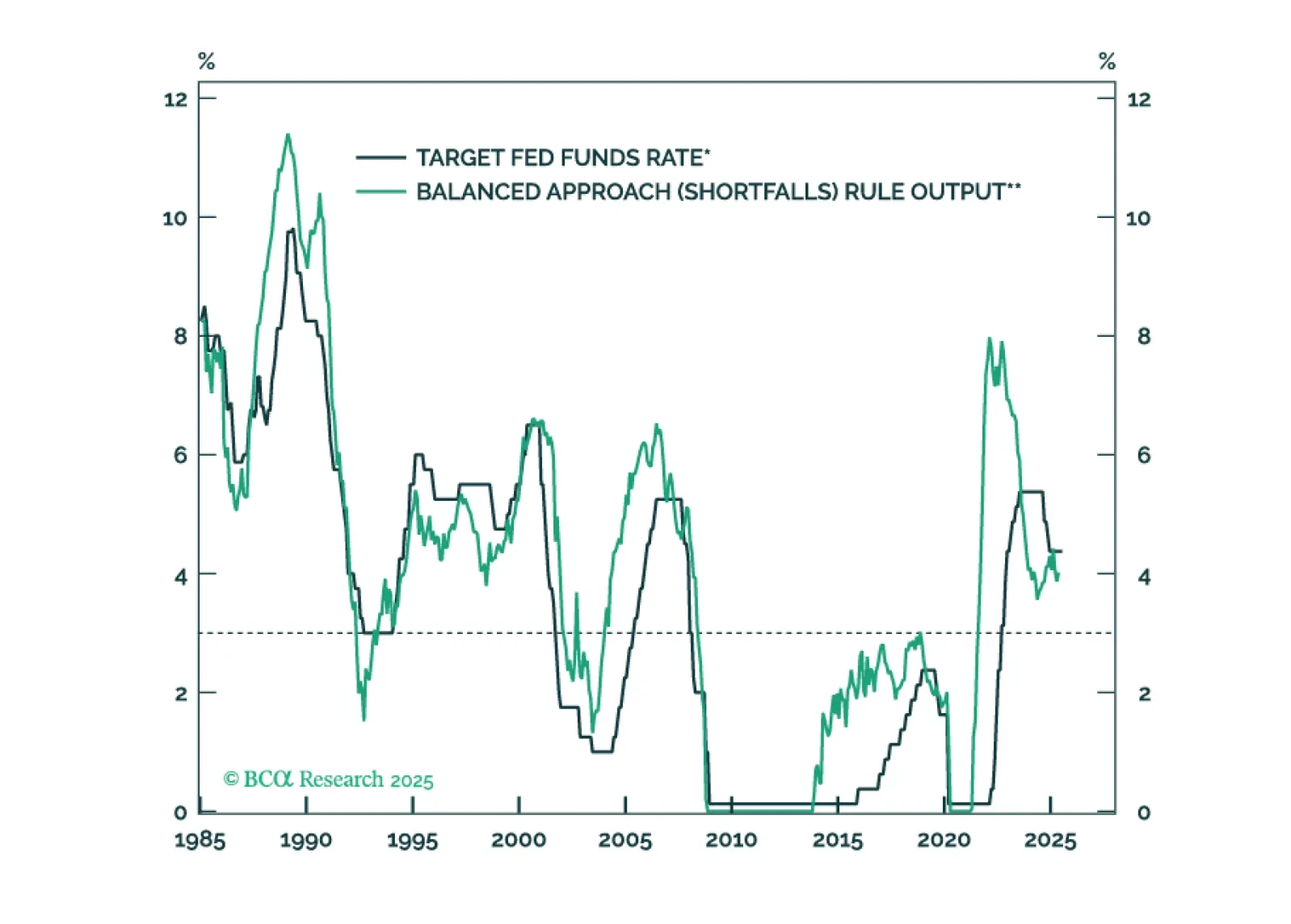

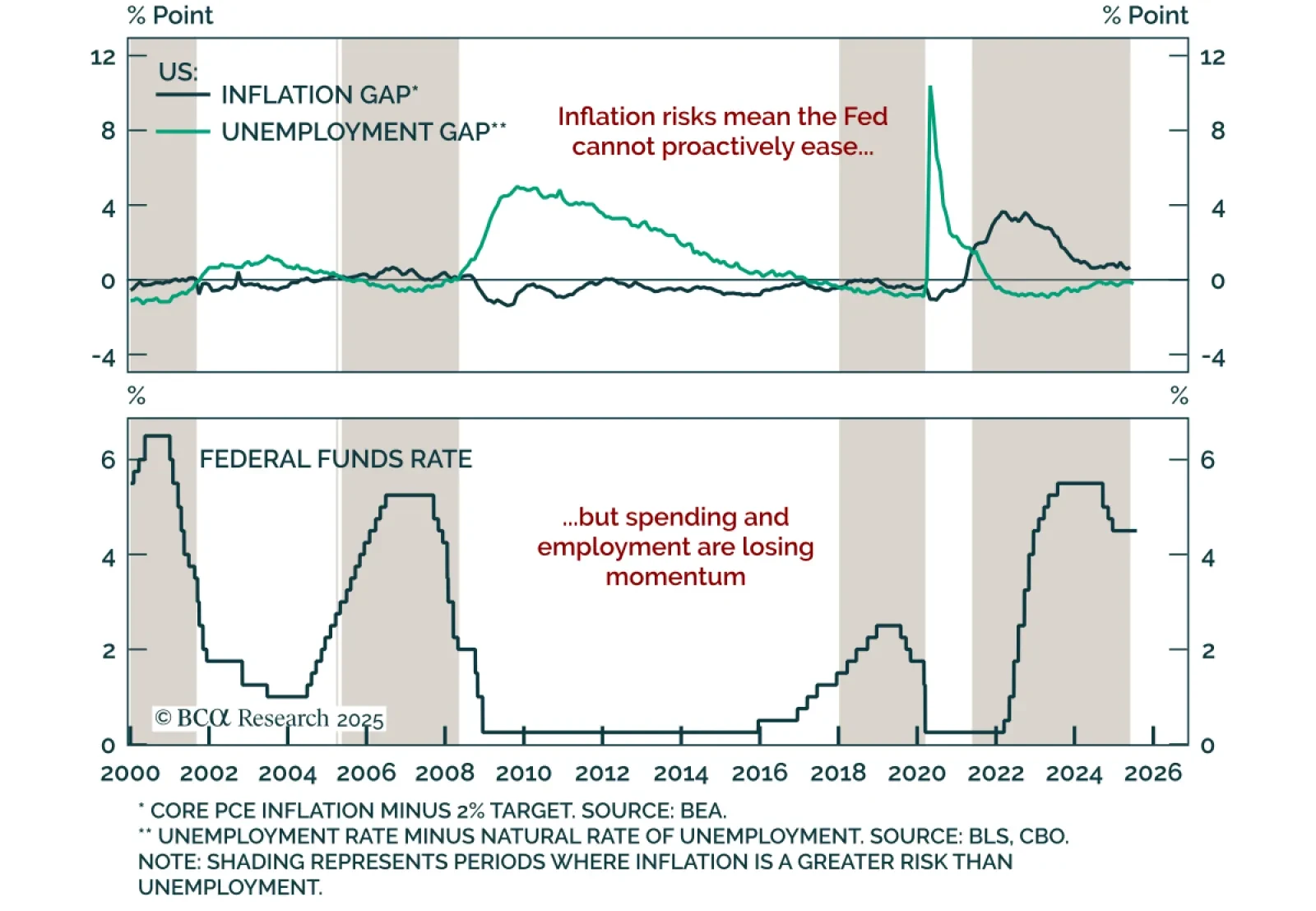

The Fed will keep rates on hold until the unemployment rate forces its hand.

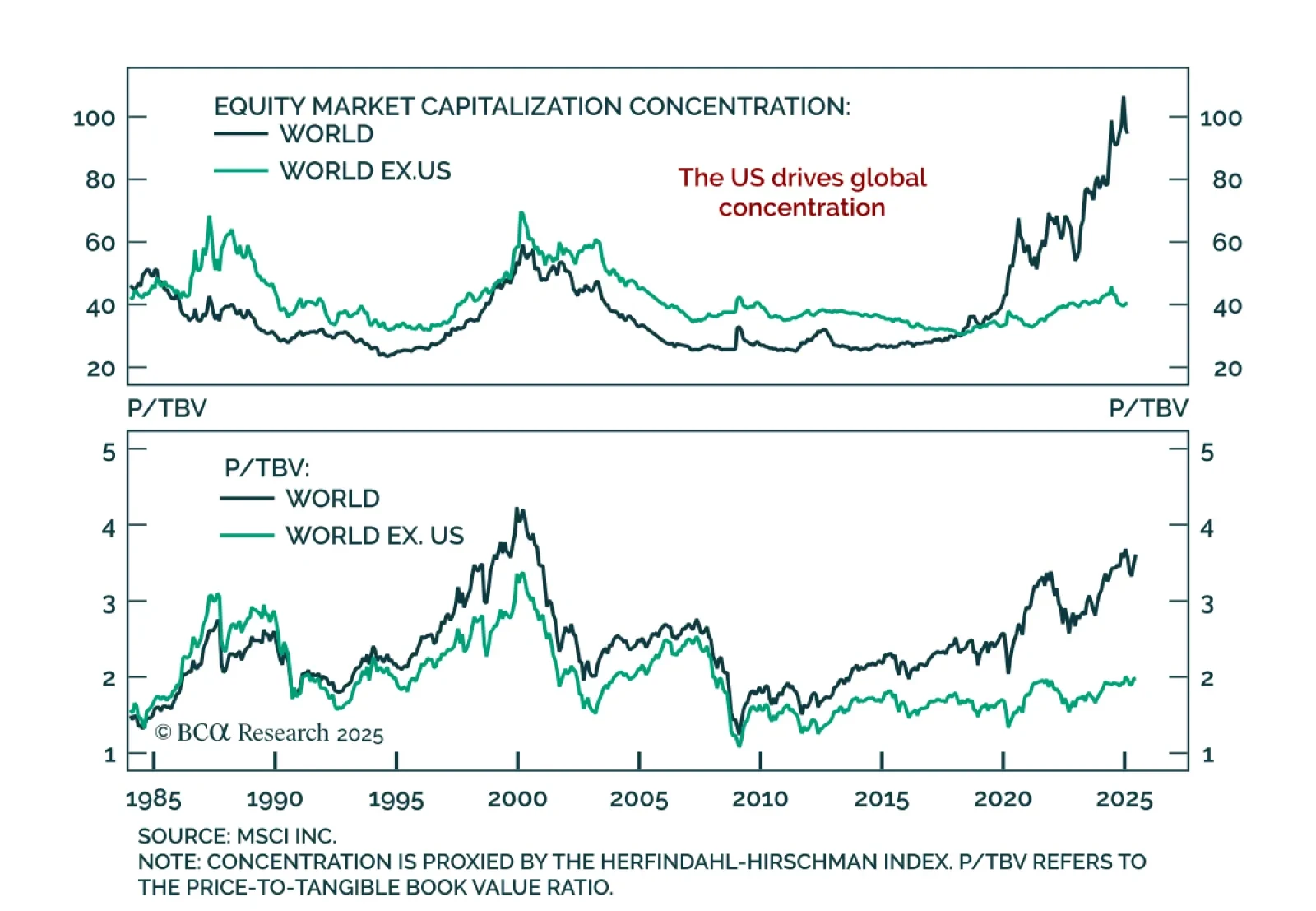

Our Global Asset Allocation strategists argue that equity market concentration is not a meaningful risk factor and does not help forecast returns. Cross-sectional concentration reflects index size, with smaller indices typically appearing more concentrated.…

Q2 US GDP beat expectations at 3.0% annualized, but the underlying data confirm that growth momentum is fading, reinforcing our defensive stance. Consumption rebounded, but disappointed at 1.4%. The quarter was heavily distorted by trade dynamics: firms…

The Fed held rates steady for a fifth straight meeting, with a divided FOMC and resilient growth keeping policy on hold, supporting our long-duration stance. The target range remains at 4.25%–4.50%, with the statement reflecting only a modest downgrade to the…

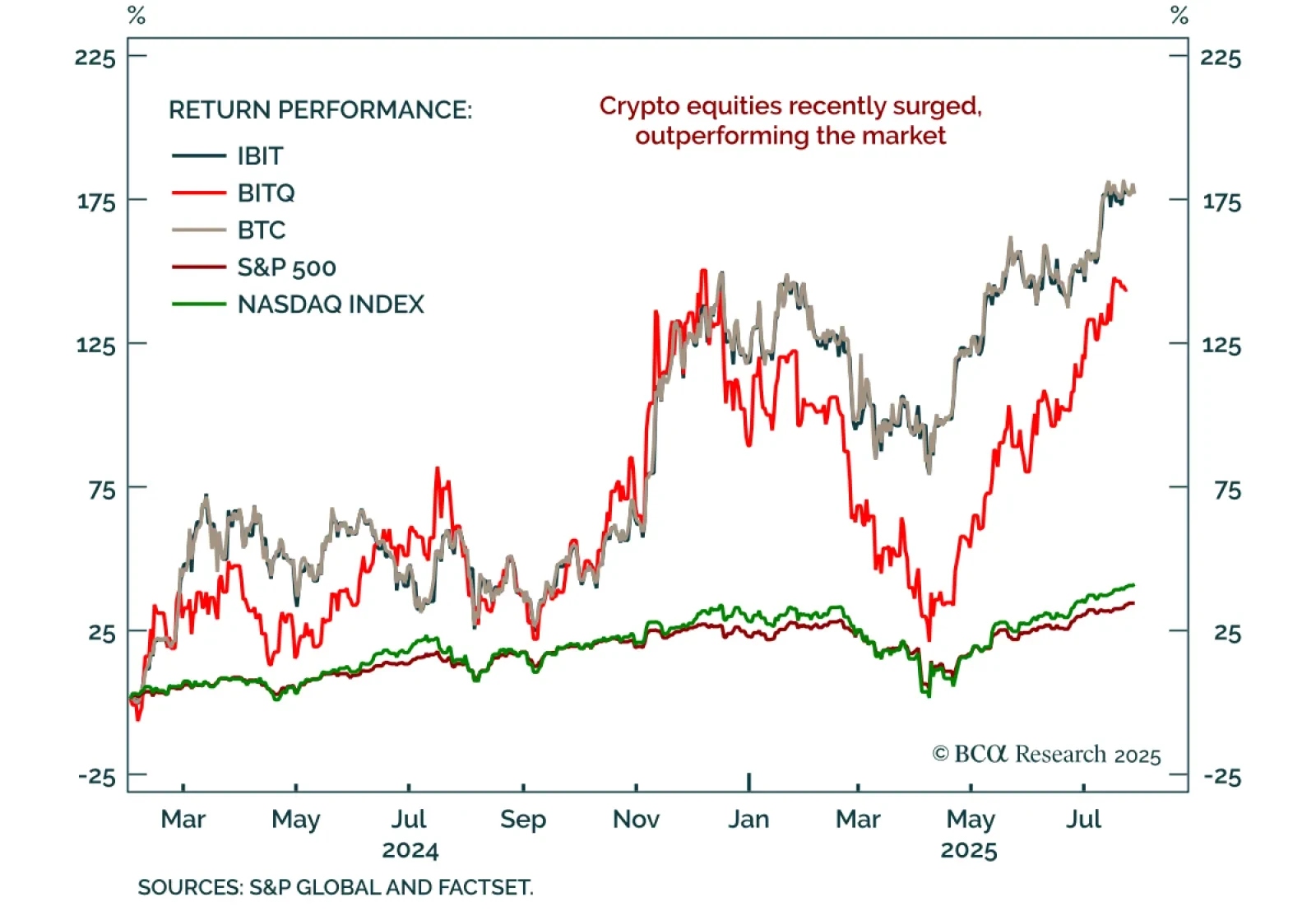

Our US Equity strategists recommend building long-term exposure to crypto equities through diversified ETFs, using pullbacks as entry points. The GENIUS Act establishes a regulatory framework for digital assets, setting the stage for accelerated crypto…

The July Conference Board Consumer Confidence report showed improved expectations but weaker current conditions, reinforcing our defensive stance and preference for downside protection. The headline index rose to 97.2 from a revised 95.2 on the back of better…