United States

Highlights The Auto and Components industry group is in the middle of a momentous transition to electric and autonomous-vehicle manufacturing thanks to technological advances in battery storage, AI, and radars. The entire EV cohort will benefit from government support for decarbonization, the preferences of millennials for green tech, and cutting-edge technological innovation. Further, the price of gas has recently nearly doubled, average US vehicles are more than 12 years old, while most US consumers came out of recession unscathed. Is this the time for consumers to upgrade to EVs? Legacy Automakers are to be primary beneficiaries of the theme: Higher earnings and greater economic visibility regarding EV transition should lead to further rerating of the industry group. These carmakers are also turning into Growth stocks as an expected surge in earnings is far in the future. Tesla has already had an amazing run. Even though it is 30% down from its peak, it remains expensive, and much of the growth expectations are already baked into the price. We recommend staying neutral on Tesla as it is a “cult” stock and a surge “to the moon” is not out of question. Ecosystem: The surge in EV capex and R&D spending will give a boost to the entire supply chain, which consists of chip manufacturers, battery and lidar R&D, part manufacturers, and charging networks. Many of these companies are still small. An ETF may be the best way to capture these names. Existing EV themed ETFs may not be perfect: Many have holdings that are way too broad and over-diversified, most invest outside of the US. Yet, these are the convenient vehicles to capture the theme and provide exposure to the entire EV cohort. Some of the best-known ETFs are ARKQ, DRIV, IDRV, and KARS. We believe that the EV/AV theme will outperform the US equity market over the 3-12 months horizon. Overweighting EV is also consistent with our call to rotate into Growth as higher rates and the pick up in inflation appear to be priced in. Feature Auto And Components Industry Delivers Historical Technological Advances The auto industry is undergoing a monumental shift towards electric vehicles (EV) and autonomous driving thanks to technological advances in battery storage, AI, and radars. Transition to EV is happening at a fast pace: According to IEA, the number of EVs on the road increased from about 17,000 vehicles in 2010 to 7.9 million in 2019. Autonomous vehicles (AV) are still in a testing stage, but most automakers promise to put them on the road within the next decade. LMC Automotive forecasts that that by 2031, EVs will reach 17 million units, while AVs will approach one million in 2025. Investors are cheering on this transition: The MSCI USA Auto and Components sector has outperformed MSCI USA by over 300% (408% vs. 90%) since the pandemic trough in March 2020. The EV-themed ETF DRIV outperformed by 95%. In this Special Report we provide an overview of the EV and AV industries and their emerging ecosystem. It is structured as following: First, we discuss the tailwind for transitioning towards EV. Second, we identify the key players in the EVs and AVs space. Third, we look at ways that investors can best get exposure to the EV theme and provide an investment outlook for the space. EV Tailwinds: Biden Administration Pushes Toward “Clean Tech”, Millennials Cheer The Biden administration’s push toward decarbonization of the economy will further accelerate transition towards EVs with a host of fiscal, infrastructure, and executive actions, such as tax credits, scrappage incentives, and government purchases. The White House’s $1.7-2.3 trillion infrastructure bill – which is highly likely to pass by the end of the year with green initiatives intact – includes a $15 billion buildout of 500,000 charging stations (there are currently only 27,000 in operation). Executive action by President Biden has also tightened fuel-economy standards. Individual states like California have committed to zero-emission standards by 2030. Add this to the emerging preferences of millennials for clean tech, and fully electric vehicles are expected to account for 33% of all US auto sales by 2030. Of course, there are EV adoption challenges: EV batteries remain expensive, adding approximately $10,000 to the price of a vehicle. Charging infrastructure is sparse, while EVs have relatively limited driving ranges and long charging times. But even these obstacles will be resolved sooner rather then later. According to Cathie Wood, CEO and CIO of the ARK (thematic) ETFs, EVs will approach sticker parity with gas-powered cars as soon as 2023. And there are a number of new entrants developing charging networks. Even driving ranges are increasing with Lucid promising 500 miles per charge (Chart 1). Key Players In The US Market Tesla: Enormous Potential But Competition Is Catching Up Tesla is a pioneer of battery electric vehicles (BEV), rewarded with sky-high valuations and deep pockets. Its stock had a spectacular run, rising ten-fold in two years, getting ahead of itself: It is down 30% from its January peak. So what is the bull case for Tesla that justifies the multiples, and may be considered a catalyst for future outperformance? After all, manufacturing of EVs is likely to become a highly competitive and low-margin business. Tesla has four unique advantages that constitute its competitive “moat”: An extensive supercharger network in the US and worldwide. Its push towards increased vertical integration into capabilities such as battery manufacturing and other key enabling technologies would allow it to maintain a technological edge over competition, as well as protect the company against any potential supply-chain disruptions. A mobility ecosystem, especially of data and network, turning the car into “mobile real estate”, powered by the cloud and fueled ultimately by thousands of exabytes of data. A host of auxiliary businesses: Energy, insurance, mobility/rideshare, network services and third-party battery supply. However, despite its tremendous long-term potential, Tesla has only recently become profitable (Chart 2). Further, we can’t discount a possibility that Tesla’s dominance may come to an end. Not only are Ford and GM gearing up their EV operations, but also European and Asian vehicle manufacturers such as VW, BMW, Hyundai, and Toyota present a significant competitive threat. Further, Chinese EVs, such as NIO, Geely, BYD, and XPEV, could erode Tesla’s market share in the Chinese market. Chart 1EV Will Reach Price Parity With ICE In 2023

EV Revolution

EV Revolution

Chart 2Tesla Has Only Recently Become Profitable

Tesla Has Only Recently Become Profitable

Tesla Has Only Recently Become Profitable

Ford And GM Are Firmly Committed To EV Legacy automakers, such as Ford and GM, have no choice but to move aggressively into the EV space in order to survive the imminent regulatory push in Europe and the US to eliminate fossil-fuel cars. Also succeeding in the EV space is necessary to stave off competition from Tesla and other EV and legacy automakers (Chart 3). Recently, GM announced that it would accelerate its EV timeline and develop 30 new EV models by 2025, transitioning to 100% EV by 2035. It is targeting global EV sales of more than 1 million by 2025. On the heels of that announcement, Ford pledged to become all electric in Europe by 2030. The company anticipates that 40% of its global vehicle volume will be fully electric by 2030. Chart 3GM And Ford Need to Stave Off Competition From Tesla

GM And Ford Need to Stave Off Competition From Tesla

GM And Ford Need to Stave Off Competition From Tesla

The transition to EV is a major endeavor for all legacy automakers but, if successful, they will reap significant rewards by means of higher sales and profits as EVs become increasingly more popular. They will also emerge as prime competitors of Tesla. Waymo (Alphabet) Alphabet’s Waymo launched its first autonomous ride-hailing network in Arizona but will need time and significant resources to scale nationally. The company is also developing both local and long-haul AV networks to transport goods. So far the company has not been profitable, struggling to commercialize the product efficiently. New EV Players There is a host of newcomers into the EV/AV space in the US. Furthest down the path in the light-vehicle market are Lucid, Fisker, and Electrameccanica (Solo). Workhorse Group, and the controversial Nikola are most established in the truck space. There are also EV recreational vehicle makers such as Canoe and Green Power Motors. EV/Autonomous Vehicles Ecosystem There is a brand new ecosystem developing around EVs, with suppliers providing batteries, radars, and charging stations. The industry is highly fragmented, and most smaller suppliers on the cutting edge of technological innovation are too small to be part of any index just yet or are not even public yet. Batteries The recently IPO’d QuantumScape has developed a breakthrough technology for a battery that charges in just 15 minutes. The company has received significant investment from VW. Solid Power is its newest competitor, still privately owned. Romeo Power develops batteries for big trucks, buses, and construction equipment. And XL Fleet supports EV conversions for commercial vehicles. Lidars Companies like Luminar and Velodyne use Lidar technology to improve the 3-D “vision” of the self-driving cars. These ventures demand large investments into capex and R&D, but present significant future revenue opportunities to the winners. Waymo (Alphabet) relies on Lidar technology for its fleet of AV vehicles. Charging Networks There are also a few companies focused on developing private charging networks, overcoming the main obstacle on the path to EV adoption – the need for ubiquitous availability of charging stations: ChargePoint, EVBox and Volta. Chipmakers All these vehicles are powered by chips produced by Nvidia, Qualcomm, Micron, and other semiconductor manufacturers, and technological improvements taking place in this industry are literally exponential. It is not clear yet which of these entrants are here to stay and, in a way, the EV and AV industry should remind investors of biotech: Each of these companies requires only a small allocation as part of an EV basket in order to capture the 100-bagger future winners. Where Do You Find The EV/AV Theme In Equity Indices? EV Companies And Suppliers Are Spread Across A Multitude Of Sectors This may sound like a silly question. The answer is seemingly obvious: In the Auto and Components Industry Group. However, there is a whole host of companies that are part of the ecosystem that are neither in the S&P 500/MSCI USA nor in the Auto and Components industry group. Nvidia, Micron, and Qualcomm are chipmakers assigned to the Technology sector. Alphabet’s self-driving business unit, Waymo, sits within Communications Services. Velodyne (recently added to the Russell 2000), Luminar, Quantumscape, and XL Fleet are small caps. There are also a number of special purpose acquisition companies (SPACs) that are in the process of merging with EV companies (Lucid, Faraday, ChargePoint, etc.). Auto And Components Industry Group Is Dwarfed By Tesla Moreover, a key issue with Auto and Components GICS2 is that it is dominated by a few large companies: Ford, GM, and Tesla account for 90% of the segment by market cap. The rest is divided among several autoparts manufacturers. Moreover, despite generating sales equal to only a quarter of the sales of GM or Ford (in 2020 $31 billion vs $122 billion for GM and $116 billion for Ford), Tesla alone represents roughly 3/4 of the industry group by market cap, being five times larger than Chrysler and GM combined (Chart 4). In terms of market share, Ford and GM account for 6% and 9% of global auto sales respectively, while Tesla barely even registers on a radar at 0.8%. Tesla’s dominant position holds this industry group hostage to its price performance (Chart 5). Chart 4Tesla Dominates Auto & Components Industry Group

EV Revolution

EV Revolution

Chart 5Performance Of Auto Industry Is Held Hostage By Tesla

EV Revolution

EV Revolution

Therefore, it is more effective to pursue the EV theme via a more balanced and diversified custom stock basket or ETF. Having said that, because of the size of the three largest automakers, we rely on MSCI USA Auto and Components industry group as a proxy for the EV/AV investment theme for analytical purposes. EV ETFs Are Mushrooming Recently there appeared a number of ETFs powered by EV/AV themes, cutting across GICS, such as ARKQ, IDRV, KARS, and DRIV. The ETFs BATT and LIT narrowly focus on EV batteries. These ETFs contain a wide range of companies cutting across industries (See Appendix for details) Excluding the broader-themed ARKQ (Autonomous Technology and Robotics), the DRIV ETF is the most widely traded. This ETF contains all the same companies as the MSCI USA Auto and Parts industry group, but also covers the entire EV/AV supply chain from miners to companies manufacturing opto-electronic components like IIVI. DRIV contains 77 names, and ranges from giants like Tesla and Microsoft to the tiny Plug Power. It is a global ETF and includes names like Nio, VW, and Toyota. Not a single name exceeds 4% weight. DRIV is 67% correlated with MSCI USA Auto and Components, and is generally less volatile, as it is more diversified across a variety of sectors (Table 1). Table 1EV/AV ETFs

EV Revolution

EV Revolution

Key Revenue Drivers Reopening Trade And Global Growth Acceleration The Automobiles and Components industry group is a classic early cyclical, highly geared to economic growth, outperforming during the recovery stage of the business cycle. Global reopening has resulted in a sharp global growth acceleration and benefited US automakers’ sales at home and abroad. Indeed, total vehicle sales in the US have already exceeded pre-pandemic levels. The question is whether this surge may continue with a backdrop of a growth slowdown (albeit off high levels) and how fast supply-chain disruptions will be resolved. Consumers Are Flush With Cash Most vehicles are sold to consumers, whose sentiment and financial wellbeing are the key industry drivers. Ubiquitous vaccination and economy-wide reopening is increasing employment in the lower-paid cohorts most affected by lockdowns. Expiration of unemployment benefits and school reopening will see millions more returning to work this fall. Anticipating a surge in employment, consumer confidence has started to rebound, albeit off low levels. The most recent $1.9 trillion fiscal stimulus package with its $1,400 checks cut directly to consumers, bodes well for US auto sales. For many vehicles, this amount may be sufficient for a down-payment. Personal savings have increased by roughly $1.5 trillion from the January 2020 trough, and disposable income has increased by 6%. Coupled with low interest rates and an improvement in banks’ willingness to lend, US consumers are in an excellent shape to upgrade their vehicles (Charts 6 & 7). Chart 6Demand For Auto Loans Has Picked Up

Demand For Auto Loans Has Picked Up

Demand For Auto Loans Has Picked Up

Chart 7Lending Standards for Auto Loans Eased Up

Lending Standards for Auto Loans Eased Up

Lending Standards for Auto Loans Eased Up

However, plans to buy a new car have declined recently due to car shortages and a spike in prices. Supply Chain Disruptions Hurt Demand For Vehicles Pandemic has brought about unique challenges: Global pent-up demand and COVID-induced supply-chain disruptions led to a mismatch between supply and demand and resulted in sharp price acceleration across a wide range of goods. US automakers have been hit hard by the global chip shortage, resulting in plant shutdowns and lower output in some cases. Shortages of lithium, a key component of EV batteries, led to its price doubling. Transportation networks are also choked up, and delivery costs are up more than 30%. While these post-pandemic difficulties are transitory in nature, prices of vehicles spiked, making it the most volatile component of the latest CPI reading, with prices in May rising 16% YoY (Chart 8). Higher price tags and half-empty car lots at dealerships are dampening consumers’ intentions to upgrade their vehicles, despite their present financial wellbeing (Chart 9). Chart 8Prices Of Cars Surged

Prices Of Cars Surged

Prices Of Cars Surged

Chart 9Supply Disruption Dampened Demand For Vehicles

Supply Disruption Dampened Demand For Vehicles

Supply Disruption Dampened Demand For Vehicles

According to IHS Markit, the average age of vehicles on US roadways rose to a record 12.1 years last year, as lofty prices and improved quality prompted owners to hold on to their cars for longer. The average price for a new vehicle is $38,000, which is expensive for most Americans. However, there are early signs that supply disruptions are starting to dissipate: Production of motor vehicles rose 6.7% in May compared with a 5.7% decrease a month earlier. Once vehicle prices stabilize, or even correct, sales are likely to rebound. EV also enjoy a unique tailwind: The price of gasoline has doubled since the beginning of the year, making electric vehicles a more attractive proposition than gas-guzzling alternatives. Weaker Dollar Boosts Foreign Sales USD has weakened by 8% since the beginning of the pandemic. This bodes well for the US auto and parts manufacturers who derive about 1/3 of revenues from outside the US. A weaker USD not only stimulates demand by making vehicles cheaper for foreign buyers but will also benefit manufacturers' income statements via a currency-translation effect (Chart 10). Chart 10Weaker Dollar Boosts Foreign Sales

Weaker Dollar Boosts Foreign Sales

Weaker Dollar Boosts Foreign Sales

Profitability Of Automakers Belt-tightening Of 2020 Is Unsustainable Margin compression has been a problem for the industry group for a while as a race to enhance existing vehicles and transition to EV has been weighing on profitability (Chart 11). However, in 2020, despite a dip in sales volume, US automakers were able to successfully manage margins, by reducing R&D expenses, capex, and labor costs, and by halting increases in dividends and buybacks, and enjoying lower prices of industrial metals. Maintaining this new lean cost structure is hardly sustainable. Chart 11Margins Are Under Pressure

Margins Are Under Pressure

Margins Are Under Pressure

R&D And Capex Will Rise As Technological Innovation Demands Capital Outlays R&D and capex are likely to increase for the entire group. Legacy automakers are forced to operate on two distinct timelines by managing and investing in the immediate conventional vehicle production cycle, while concurrently preparing for the longer-term transition to a world of vehicle electrification and autonomous driving. Development of EVs requires deep pockets and substantial investments into both capex and R&D, which have been steadily rising (Charts 12 & 13). Chart 12R&D Expense Is Bound To Increase…

R&D Expense Is Bound To Increase…

R&D Expense Is Bound To Increase…

Chart 13… As Is Capex

EV Revolution

EV Revolution

Case in point, GM has recently announced a $35 billion investment into EV and AV, an increase of 75% from its initial pledge, an amount exceeding its gas and diesel investment. Not to be outdone, Ford has copied the move, pledging $30 billion on EV vehicle development, including battery development, by 2025. This is an increase of more than 35% over the $22 billion previously pledged. Clearly, commitment to EV siphons resources away from other businesses, and put pressures on automakers to keep up with competitors. Yet the market applauded these announcements by bidding up shares of both companies, implicitly saying that EV spending will lead to better future cashflows. Thus transition to EV moves auto stocks from the Value into the Growth camp, making the group more sensitive to interest rates. Runaway Cost Of Raw Materials Is Stabilizing Metals such as steel, iron, and aluminum comprise over 75% of the content of the car. The price of metals is particularly important to EV manufacturers as the body of an EV contains five times more steel than regular vehicles. In 2020 gross margin benefited from a dip in prices of industrial metals. However, the recent economic recovery has led to a rebound in the prices of commodities, with the GSCI Industrial Metals Index rising by more than 70% off the bottom and reaching 2010 levels (Chart 14). There are early signs that prices are stabilizing: The price of steel is down by 20%, copper by 13%, and aluminum by 6%, from their respective peaks (Chart 15). Chart 14Price Of Industrial Metals Have Spiked...

Price Of Industrial Metals Have Spiked...

Price Of Industrial Metals Have Spiked...

Chart 15...But There Are Early Signs Of Correction

...But There Are Early Signs Of Correction

...But There Are Early Signs Of Correction

High Operating Leverage Of Auto Manufacturers Amplified Earnings Growth Automakers and suppliers have high fixed-cost manufacturing facilities. As a result, their operating leverage is high, i.e., increases in sales are translated into even greater increases in profits. As 2021 sales are expected to rise, earnings will also continue to rebound, reaching or even exceeding pre-pandemic levels. Looking ahead, we expect earnings growth to decelerate as sales are likely to normalize while EV transitioning costs will continue to rise (Chart 16). However, eventually, EV investment will translate into higher sales volumes: Once new technology infrastructure is in place, the long-term profitability of the industry group will improve. Chart 16Earnings Are Rebounding To Pre-pandemic Levels

Earnings Are Rebounding To Pre-pandemic Levels

Earnings Are Rebounding To Pre-pandemic Levels

Valuations: Significant Dispersion Within Industry Group The auto and parts industry has been underperforming the market since February 2020, with valuations coming down significantly. Looking under the hood, we observe a pronounced bifurcation between Tesla and other stocks (Table 2). Table 2Tesla Is Still Expensive, Ford and GM Are Cheap

EV Revolution

EV Revolution

Tesla trades at an eye-watering 596x earnings (which is an improvement from 1,300x back in January) and 16.3x sales multiple. The company has enormous long-term potential, but over the short term it needs to grow into its valuations, as it has effectively “borrowed” returns from the future. Yet investors need to keep in mind that Tesla is a cult stock, and has a strong retail following: Continuation of an irrational speculative bubble is within the realm of possibility. Therefore, a neutral allocation to Tesla will be prudent. Legacy automakers and suppliers are still cheap despite a strong run off their market lows. Forward 12-month PE is in the single/low-double digit range. Low valuations indicate that there is still an overhang of uncertainty over the economic recovery and potential profitability of legacy car manufacturers and suppliers, along with lingering doubts about the success of the group in the EV space. However, there is a lot of room for long-term rerating once there is greater visibility (Chart 17). Chart 17With Tesla Down 30% From Peak, Industry Group Looks Cheaper

With Tesla Down 30% From Peak, Industry Group Looks Cheaper

With Tesla Down 30% From Peak, Industry Group Looks Cheaper

Investment Outlook We have a positive 3-12-month outlook for the investment performance of the EV theme: The entire EV cohort will benefit from government support for decarbonization, the preference of millennials for green tech, and cutting-edge technological innovation. American vehicles are getting old, and consumers have financial resources to purchase new cars. Supply disruptions are gradually dissipating. Gasoline is getting expensive, but EV/ICE parity is near. Investing in automakers and suppliers, which are turning into growth companies with longer duration of cash flows, is also aligned with our thesis of rotating into Growth as rates have stabilized and the pick up in inflation has been priced in. Legacy Automakers are to be primary beneficiaries of the theme. Both Ford and GM are relatively inexpensive. Higher earnings and improved visibility on the success of EV transition should lead to further rerating. Tesla is also a quintessential growth company. However, unlike legacy automakers, it has already had an amazing run. Even though it is down from its peak, it remains expensive, and much of the positive expectations are already baked into price. We recommend staying neutral on Tesla as it is a “cult” stock and a surge “to the moon” is not out of the question. Ecosystem Surge in EV capex and R&D spending will have positive spill-over effect on EV ecosystem suppliers. These are small cap stocks and creating a well-diversified basket of names in battery, radar, chips and software will help capture returns of the long-term winners. Existing EV-themed ETFs may not be perfect: Many have holdings that are way too broad and over diversified, most invest outside of the US. Yet, these are convenient vehicles to capture the theme and provide exposure to the entire EV value chain, including emerging industry players. Bottom Line: The auto industry is undergoing a major technological disruption. This process is expensive and perilous yet presents an enormous future earnings growth opportunity. The ingredients for success are in place: Proliferation of new technologies, government support, changing consumer preferences, and surging US economy. This tide will lift all boats: Legacy and EV-only auto manufacturers and suppliers as well as EV ecosystem players. We are bullish on the sector on a 3-12 months investment horizon. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Appendix Table A1EV/AV ETF Summary

EV Revolution

EV Revolution

Recommended Allocation

EV Revolution

EV Revolution

Highlights Economy – We agree with the Fed’s judgment that sky-high inflation readings will not last: Used-car prices won’t go up forever and neither will airline fares or hotel accommodations. Supply bottlenecks affecting the prices of a wide range of goods will eventually ease. Markets – If growth is too strong for a recession but not so strong that it forces the Fed to induce a recession, equities and spread product will outperform Treasuries: Uncertainty surrounds the post-pandemic economy, but our base case is that the US will be able to grow well above trend in 2021 and 2022 without triggering uncomfortably high inflation. Strategy – Investors should remain at least equal weight risk assets in multi-asset portfolios: A strong-growth, easy-policy backdrop is good for equities and credit and investors should maintain exposure to them in balanced portfolios. Feature The unprecedented nature of the current economic backdrop, in which a global pandemic causes the US to idle large swaths of the economy, inject previously unimaginable amounts of aid to households and businesses to help them withstand its ravages, then attempt to restart the idled elements more than a year later, allows a lot of room for interpretation. One can see just about whatever one wants to see in the incoming flow of data as it is highly uncertain how long it will take the many individual engines to hum after their switches are flipped back to ON from OFF. Investors are charged with getting ahead of moves in forward-looking markets, however, and want to know now what awaits around the bend. Amidst the flow of often contradictory data points, we strive to maintain our focus on the broad overarching trend. We continue to find the Goldilocks-and-the-Two-Tails framework helpful in keeping our eye on the ball (Figure 1). Our base case remains that the just-right strong-growth/accommodative-monetary-policy backdrop will remain in place for the balance of our three-to-twelve-month cyclical investment time frame. COVID-19’s apparent retreat in the US1 leads us to believe that the too-cold left-tail outcome, characterized by disappointingly slow growth, is increasingly unlikely (Chart 1). Figure 1Goldilocks And The Two Tails

Checking In With The Inflation Checklist

Checking In With The Inflation Checklist

Chart 1The Pace Has Slowed, But A Lot Of Americans Are Already Vaccinated

The Pace Has Slowed, But A Lot Of Americans Are Already Vaccinated

The Pace Has Slowed, But A Lot Of Americans Are Already Vaccinated

Table 1Inflation Checklist

Checking In With The Inflation Checklist

Checking In With The Inflation Checklist

The right-tail outcome in which the economy overheats looks more probable and it is our primary concern. Overheating would bring uncomfortably high rates of consumer price inflation and we devote this week’s report to a review of our inflation checklist (Table 1). The checklist is not meant to identify the moment that inflation becomes a mortal threat to the expansion. We will not sound the alarm and adjust our asset allocation recommendations the instant that a pre-determined number of boxes are checked; it is simply meant to provide us with a systematic framework for assessing its movements and their implications for financial markets and the economy. Labor Market Indicators Chart 2Wages Are Not Yet A Hot Spot

Wages Are Not Yet A Hot Spot

Wages Are Not Yet A Hot Spot

The executive summary of last week’s examination of the labor market is that we expect the factors constraining supply will ease considerably by the fall as the services sector fully reopens, in-person learning resumes for all K through 12 students and federal supplements to unemployment insurance benefits expire. Demand for workers remains robust, with the JOLTS job openings rate and the NFIB survey’s unfilled job openings series making new highs. The combination of potent demand and constrained supply is not producing wage inflation, however. The Atlanta Fed’s wage tracker, which follows the same set of employees over time, has rolled over and is now nearly a full point below its post-GFC peak (Chart 2, middle panel); the employment cost index, which also adjusts for changes in labor force composition, is rising but remains near the bottom of its pre-GFC range (Chart 2, bottom panel); and the less-sophisticated average hourly earnings series has dipped below 2% (Chart 2, top panel). Price Indexes Checking the Marquee Indexes box was a no-brainer after the core CPI and core PCE price index made new multi-year highs in May. The question going forward is whether the surge in consumer prices is a one-off or a harbinger of a lasting change. We remain in the one-off camp with the Fed, figuring that the bottlenecks that have pushed month-over-month gains in the price indexes to multi-decade highs are a function of trying to ramp up production to more normal levels after a year-plus interruption. The trimmed-mean measures of core CPI and PCE send a much less worrisome message and suggest that once the bottlenecks driving outlier price increases are resolved, the marquee measures will settle down as well (Chart 3). Chart 3Trimmed-Mean Price Indexes Are Still Well Behaved

Trimmed-Mean Price Indexes Are Still Well Behaved

Trimmed-Mean Price Indexes Are Still Well Behaved

Pipeline Pressures BCA’s pipeline inflation pressure index did not let up in May (Chart 4, top panel), indicating that components like the CRB Raw Industrials Index are still pushing higher, reinforcing our Commodity and Energy Strategy team’s view that several years of tepid investment have left base metals and energy markets with supply deficits that will push prices higher into the intermediate term. The DXY index tested multi-year support at 90 but is holding above it for now (Chart 4, bottom panel), staving off the increase in import prices that could result from a technical breakdown in the dollar. There is also little direct inflation pressure coming from overseas, as consumer prices in the Eurozone and China, the two biggest economies outside of the US, remain contained (Chart 5). Chart 4Pipeline Pressures Have Not Eased, But The Dollar Staved Off An Inflationary Breakdown

Pipeline Pressures Have Not Eased, But The Dollar Staved Off An Inflationary Breakdown

Pipeline Pressures Have Not Eased, But The Dollar Staved Off An Inflationary Breakdown

Chart 5China And The Eurozone Aren't Exporting Inflation Pressures To The US Yet

China And The Eurozone Aren't Exporting Inflation Pressures To The US Yet

China And The Eurozone Aren't Exporting Inflation Pressures To The US Yet

Inflation Expectations Chart 6Markets Still Expect The Rate Of Inflation To Slow Over Time

Markets Still Expect The Rate Of Inflation To Slow Over Time

Markets Still Expect The Rate Of Inflation To Slow Over Time

The inflation expectations curve as derived from market-based measures remains inverted, indicating that investors agree with the Fed’s transitory inflation assessment. The message is the same as it was last month when we showed the TIPS break-even and CPI swap rates for the 2-to-5- and 5-to-10-year periods, though there have been some adjustments across the segments. The 2-to-5-year segment has become more inverted (Chart 6, top and third panels), which is to say that investors expect a larger drop-off in inflation in years three, four and five versus years one and two, while the 5-to-10-year segment has become less inverted (Chart 6, second and bottom panels). The curves still point to declining long-term inflation after a near-term spike, however, as inflation is projected to fall in years 3 to 5 and then hold steady (TIPS) or rise slightly (CPI swaps) in years 6 to 10 (Table 2). We find market-based measures to be more insightful than survey measures, but we were encouraged to see the University of Michigan consumer survey data follow the same pattern. The median 1-year inflation expectation, at 4% (down 60 basis points (“bps”) from May), was 120 bps above the median 5-year inflation expectation of 2.8% (down 20 bps from May’s reading). The New York Fed’s April Survey of Market Participants had 5-year-on-5-year CPI inflation rising, albeit at a modest level that demonstrated market professionals’ inflation expectations remain well anchored. The respondents’ median forecast for the annual rate of inflation from April 2026 through March 2031 was 2.2%, slightly above their 2.1% median forecast from April 2021 through March 2026. Table 2Investors Agree That Inflation Will Be Transitory

Checking In With The Inflation Checklist

Checking In With The Inflation Checklist

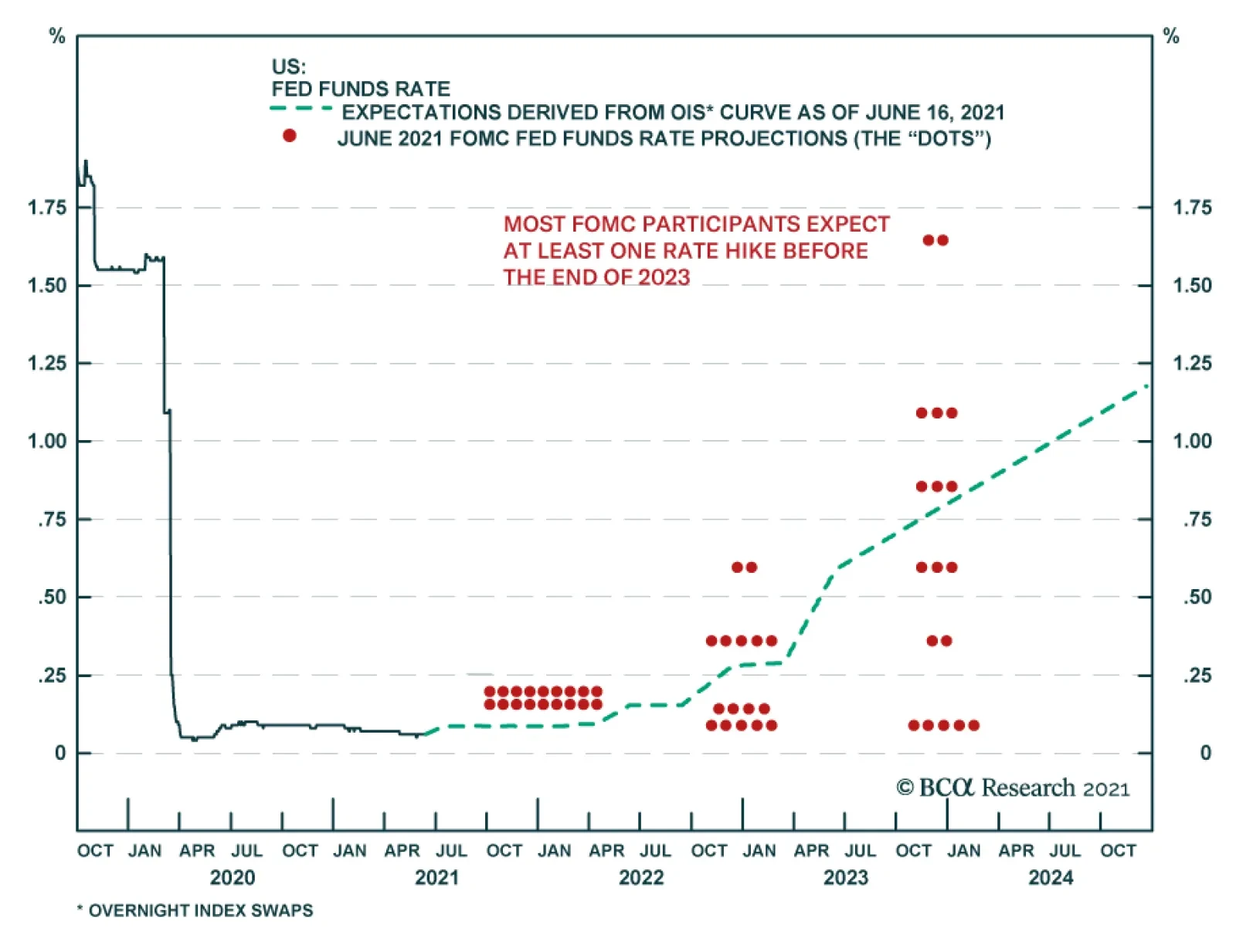

The Fed’s Reaction Function The June FOMC meeting accorded with our expectations. The post-meeting statement acknowledged the economy’s improvement as waning infections and an effective vaccination campaign have pushed the pandemic off of center stage. Meeting participants pulled their median liftoff date expectation into 2023 from 2024, aligning “the dots” more closely with financial markets and our own late-2022 view (Chart 7). They also significantly raised their 2021 inflation expectations from March, which had been trampled by the April and May CPI and PCE index releases. Chart 7Much Ado About A Modest Tweak

Much Ado About A Modest Tweak

Much Ado About A Modest Tweak

We were therefore surprised that the meeting produced so much excitement in financial markets. Treasuries gyrated, with yields soaring across all maturities Wednesday afternoon before long-dated issues unwound most of their backup (the 10-year note) or made new multi-month lows (the 30-year bond) in Thursday’s session. Yields at the short end of the curve stayed higher as the bond market moved its liftoff date expectations forward, with the net result that the Treasury curve flattened. The dollar popped, precious metals were hammered, and the NASDAQ rose while banks took a hit. We included the Fed reaction function items in our inflation checklist as a way of highlighting that the high-inflation end game will proceed once fed funds rate hikes are directed at containing it. When we introduced the checklist last month, we wrote that we would only check the Fed boxes in the event that Fed speakers begin to telegraph a change of direction or if the dots indicated that the bias toward accommodative policy was shifting. We do not think last week’s recognition that the March Summary of Economic Projections (SEP) had gone stale in the wake of subsequent data releases constitutes a change in the Fed’s accommodative stance. As a Wall Street Journal editorial lamenting that bias (and the administration’s ambitious spending plans) put it,2 Which of the following doesn’t fit with the others? A) 7% GDP growth in 2021. B) 5% and 3.8% year-over-year increases in CPI and core CPI, respectively. C) 4.5% unemployment by year-end, on its way to 3.8% at year-end 2022. D) A near-zero fed funds rate for two more years. As long as the Fed finds a way for D) to coexist with A), C) and whatever B) turns out to be over the ensuing months as transitory inflation pressures abate, there will be no need to check our reaction function boxes. Investors won’t have any need to get overweight benchmark duration to position for a cyclical rally in Treasuries, either. Why Bother? Our US Bond Strategy colleagues have noted that the inflation-related criteria for hiking rates have been met. Year-over-year PCE inflation is above 2% and with the SEP’s median headline and core projections for 2021 PCE inflation at 3.4% and 3%, respectively, it is on track to exceed 2% for some time. If the Fed abides by the specific guidance it has repeatedly outlined, the beginning of the next rate-hiking cycle will depend on the state of the labor market. An investor who wants to position for the cyclical inflection in Treasury yields will be best served by anticipating the path of nonfarm payrolls. We will continue to keep tabs on our inflation checklist, however, because inflation is an important tail risk. We are asked about it in every meeting and it is a hot topic in the general media as well. If households, businesses and investors were to become convinced that a new worrisome inflation regime had begun, financial markets and the economy would be roiled. Even though such a scenario lies outside of our base case, we will track it and think about how to navigate it on the general principle that we would rather be ready than have to get ready. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 The 7-day averages of new cases and deaths have fallen all the way to their late March 2020 levels. 2https://www.wsj.com/articles/no-inflation-worries-at-the-fed-11623883322 Accessed June 17, 2021.

Dear Client, Next week, instead of our regular report, we will be sending you a Special Report from BCA Research’s MacroQuant tactical global asset allocation team. Titled “MacroQuant: A Quantitative Solution For Forecasting Macro-Driven Financial Trends,” this white paper will discuss the purpose, coverage, and methodology of the MacroQuant model. I hope you will find the report insightful. We will be back the following week with the GIS Quarterly Strategy Outlook, where we will explore the major trends that are set to drive financial markets for the rest of 2021 and beyond. We will also be holding a webcast on Thursday, July 8 at 10:00 AM EDT (3:00 PM BST, 4:00 PM CEST, 10:00 PM HKT) to discuss the outlook. Best regards, Peter Berezin Chief Global Strategist Highlights Although the Fed delivered a hawkish surprise on Wednesday, monetary policy is likely to remain highly accommodative for the foreseeable future. We continue to see high US inflation as a long-term risk rather than a short-term problem. Outside of a few industries, wage inflation remains well contained. In those industries suffering from labor shortages, the expiration of emergency unemployment benefits, increased immigration, and the opening up of schools should replenish labor supply. Bottlenecks in the global supply chain are starting to ease. Many key input prices have already rolled over, suggesting that producer price inflation has peaked and is heading down. A slowdown in Chinese credit growth could weigh on metals prices during the summer months, which would further temper inflationary pressures. We are downgrading our view on US TIPS from overweight to neutral. Owning bank shares is a cheaper inflation hedge. Look Who’s Talking The Fed jolted markets on Wednesday after the FOMC signaled it may raise rates twice in 2023. Back in March, the Fed projected no hikes until 2024 (Chart 1). Chart 1Fed Forecasts Converge Toward Market Expectations

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Seven of 18 committee members expected lift-off as early as 2022, up from four in March. Only five participants expected the Fed to start raising rates in 2024 or later, down from 11 previously. The Fed acknowledged recent upward inflation surprises by lifting its forecast of core PCE inflation to 3.4% for 2021 compared with the March projection of 2.4%. These forecast revisions bring the Fed closer to market expectations, although the latter are proving to be a moving target. Going into the FOMC meeting, the OIS curve was pricing in 85 bps of rate tightening by the end of 2023. At present, the market is pricing in about 105 bps of tightening. At his press conference, Chair Powell acknowledged that FOMC members had discussed scaling back asset purchases. “You can think of this meeting as the ‘talking about talking about’ meeting,” he said. A rate hike in 2023 would imply the start of tapering early next year. The key question for investors is whether this week’s FOMC meeting marks the first of many hawkish surprises from the Fed. We do not think it does. As Chair Powell himself noted, the dot-plot is “not a great forecaster of future rate moves,” before adding that “Lift-off is well into the future.” Ultimately, a major monetary tightening cycle would require that inflation remain stubbornly high. As we discuss below, while there are good reasons to think that the US economy will eventually overheat, the current bout of inflation is indeed likely to be “transitory.” This implies that bond yields are unlikely to rise into restrictive territory anytime soon, which should provide continued support to stocks. Inflation: A Long-Term Risk Rather Than A Short-Term Problem Chart 2Globalization Plateaued More Than A Decade Ago

Globalization Plateaued More Than A Decade Ago

Globalization Plateaued More Than A Decade Ago

There are plenty of reasons to worry that US inflation will eventually move persistently higher. As we discussed in a recent report, many of the structural factors that have suppressed inflation over the past 40 years are reversing direction: Globalization is in retreat: The ratio of global trade-to-manufacturing output has been flat for over a decade (Chart 2). Looking out, the ratio could even decline as more companies shift production back home in order to gain greater control over unruly global supply chains. Baby boomers are leaving the labor force en masse. As a group, baby boomers control more than half of US wealth (Chart 3). They will continue to run down their wealth once they retire. However, since they will no longer be working, they will no longer contribute to national output. Continued spending against a backdrop of diminished production could be inflationary. Chart 3Baby Boomers Have Accumulated A Lot Of Wealth

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

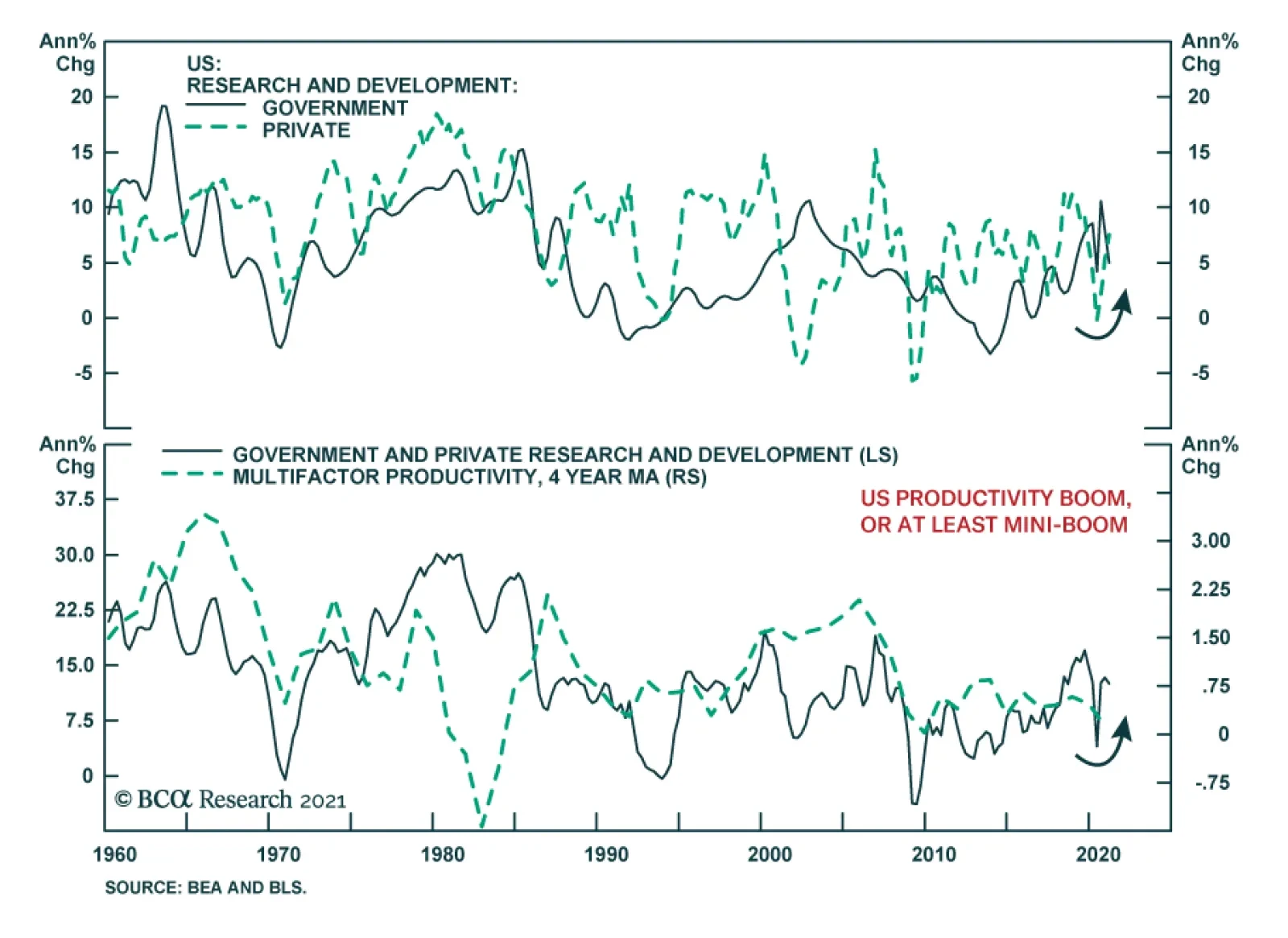

Despite a pandemic-induced bounce, underlying productivity growth remains disappointing (Chart 4). Slow productivity growth could cause aggregate supply to fall short of aggregate demand. Social stability is in peril, as exemplified by the recent dramatic increase in the US homicide rate. In the past, social instability and higher inflation have gone hand in hand (Chart 5). Chart 4Trend Productivity Growth Has Been Disappointing

Trend Productivity Growth Has Been Disappointing

Trend Productivity Growth Has Been Disappointing

Chart 5Historically, Social Unrest And Higher Inflation Move In Lock-Step

Historically, Social Unrest And Higher Inflation Move In Lock-Step

Historically, Social Unrest And Higher Inflation Move In Lock-Step

Perhaps most importantly, policymakers are aiming to run the economy hot. A tight labor market will lift wage growth (Chart 6). Not only could higher wage growth push up inflation through the usual “cost-push” channel, but by boosting labor’s share of income, a tight labor market could spur aggregate demand. Despite these structural inflationary forces, history suggests that it will take a while – perhaps another two-to-four years – for the US economy to overheat to the point that persistently higher inflation becomes a serious risk. Consider the case of the 1960s. While the labor market reached its full employment level in 1962, it was not until 1966 – when the unemployment rate was a full two percentage points below NAIRU – that inflation finally took off (Chart 7). Chart 6A Tight Labor Market Eventually Bolsters Wages

A Tight Labor Market Eventually Bolsters Wages

A Tight Labor Market Eventually Bolsters Wages

Chart 7Inflation Started Accelerating Quickly Only When Unemployment Reached Very Low Levels In The 1960s

Inflation Started Accelerating Quickly Only When Unemployment Reached Very Low Levels In The 1960s

Inflation Started Accelerating Quickly Only When Unemployment Reached Very Low Levels In The 1960s

In May, 4.4% fewer Americans were employed than in January 2020 (Chart 8). The employment-to-population ratio for prime-aged workers stood at 77.1%, 3.4 percentage points below its pre-pandemic level (Chart 9). Chart 8US Employment Still More Than 4% Below Pre-Pandemic Levels

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Chart 9Prime-Age Employment-To-Population Ratio Remains Below Pre-Pandemic Levels

Prime-Age Employment-To-Population Ratio Remains Below Pre-Pandemic Levels

Prime-Age Employment-To-Population Ratio Remains Below Pre-Pandemic Levels

A Labor Market Puzzle Admittedly, if one were to ask most companies if they were finding it easy to hire suitable workers, one would hear a resounding “no.” According to the National Federation of Independent Business (NFIB), 48% of firms reported difficulty in filling vacant positions in May, the highest share in the 46-year history of the survey (Chart 10). Chart 10US Labor Market Shortages (I)

US Labor Market Shortages (I)

US Labor Market Shortages (I)

Chart 11US Labor Market Shortages (II)

US Labor Market Shortages (II)

US Labor Market Shortages (II)

Nationwide, the job openings rate reached a record high of 6% in April, up from 4.5% in January 2020. The share of workers quitting their jobs voluntarily – a measure of worker confidence – also hit a record of 2.7% (Chart 11). How can we reconcile the apparent tightness in the labor market with the fact that employment is still well below where it was at the outset of the pandemic? Four explanations stand out. First, unemployment benefits remain extremely generous. For most low-wage workers, benefits exceed the pay they received while employed. It is not surprising that labor shortages have been most pronounced in sectors such as leisure and hospitality where average wages are relatively low (Chart 12). The good news for struggling firms is that the disincentive to working will largely evaporate by September when enhanced unemployment benefits expire. Chart 12Labor Scarcity Prevalent In Low-Wage Sectors

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Chart 13School Closures Have Curbed Labor Supply

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Second, lingering fears of the virus and ongoing school closures continue to depress labor force participation. Chart 13 shows that participation rates have recovered less for mothers with young children than for other demographic groups. This problem will also fade away by the fall when schools reopen. Third, the number of foreign workers coming to the US fell dramatically during the pandemic. State Department data show that visas dropped by 88% in the nine months between April and December of last year compared to the same period in 2019 (Chart 14). President Biden revoked President Trump’s visa ban in February, which should pave the way for renewed migration to the US. Chart 14US Migrant Worker Supply Is Depressed

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Chart 15The Pandemic Accelerated Early Retirement

The Pandemic Accelerated Early Retirement

The Pandemic Accelerated Early Retirement

Fourth, about 1.5 million more workers retired during the pandemic than one would have expected based on the pre-pandemic trend (Chart 15). Most of these workers were near retirement age anyway. Thus, there will likely be a decline in new retirements over the next couple of years before the baby boomer exodus described earlier in this report resumes in earnest. Other Input Prices Set To Ease Just as labor shortages in a number of industries will ease later this year, some of the bottlenecks gripping the global supply chain should also diminish. The prices of various key inputs – ranging from lumber, steel, soybeans, corn, to DRAM prices – have rolled over (Chart 16). This suggests that producer price inflation for manufactured goods, which hit a multi-decade high of 13.5% in May – has peaked and is heading lower. Chart 16Input Prices Have Rolled Over

Input Prices Have Rolled Over

Input Prices Have Rolled Over

The jump in prices largely reflected one-off pandemic effects. For example, rental car companies, desperate to raise cash at the start of the pandemic, liquidated part of their fleets. Now that the US economy is reopening, they have found themselves short of vehicles. With fewer rental vehicles hitting the used car market, households flush with cash, and new vehicle production constrained by the global semiconductor shortage, both new and used car prices have soared. Vehicle prices have essentially moved sideways since the mid-1990s (Chart 17). Thus, it is doubtful that the recent surge in prices represents a structural break. More likely, prices will come down as supply increases. According to a recent report from Goldman Sachs, auto production schedules already imply an almost complete return to January output levels in June. Chart 17Vehicle Prices Have Essentially Moved Sideways Since The Mid-1990s

Vehicle Prices Have Essentially Moved Sideways Since The Mid-1990s

Vehicle Prices Have Essentially Moved Sideways Since The Mid-1990s

Chart 18Rebounding Pandemic-Affected Services Prices Are Pushing Up Overall CPI

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

As Chart 18 shows, more than half of the increase in consumer prices in April and May can be explained by higher vehicle prices, along with a rebound in pandemic-affected service prices (airfares, hotels, and event admissions). Outside those sectors, the level of the CPI remains below its pre-pandemic trend (Chart 19). Chart 19Unwinding Of "Base Effects"

Unwinding Of "Base Effects"

Unwinding Of "Base Effects"

Chart 20"Supercore" Inflation Measures Remain Well Contained

"Supercore" Inflation Measures Remain Well Contained

"Supercore" Inflation Measures Remain Well Contained

More refined measures of underlying inflation such as the trimmed-mean CPI, median CPI, and sticky price CPI are all running well below their official core CPI counterpart (Chart 20). While certain components of the CPI basket, such as residential rental payments, are likely to exhibit higher inflation in the months ahead, others such as vehicle and food prices will see lower inflation, and perhaps even outright deflation. Slower Chinese Credit Growth Should Temper Commodity Inflation Chart 21Chinese Credit Growth And Metal Prices Move Together

Chinese Credit Growth And Metal Prices Move Together

Chinese Credit Growth And Metal Prices Move Together

Chinese credit growth and base metals prices are strongly correlated (Chart 21). We do not expect the Chinese authorities to embark on a new deleveraging campaign. Credit growth has already fallen back to 11%, which is close to the prior bottom reached in late-2018. Nevertheless, to the extent that changes in Chinese credit growth affect commodity prices with a lag of about six months, metals prices could struggle to maintain altitude over the summer months. China’s plan to release metal reserves into the market could further dampen prices. We remain short the global copper ETF (COPX) relative to the global energy ETF (IXC) in our trade recommendations. The trade is up 18.4% since we initiated on May 27, 2021. We will close this trade if it reaches our profit target of 30%. Bank Shares Are A Better Hedge Against Inflation Than TIPS We have been overweight TIPS in our view matrix. However, with 5-year/5-year forward breakevens trading near pre-pandemic levels, any near-term upside for inflation expectations is limited (Chart 22). As such, we are downgrading TIPS from overweight to neutral in our fixed-income recommendations. Investors looking to hedge inflation risk should consider bank shares. Our baseline view is that the 10-year Treasury yield will rise to about 1.9% by the end of the year. If inflation fails to come down as fast as we anticipate, bond yields would increase even more than that. Chart 23 shows that banks almost always outperform the S&P 500 when bond yields are rising. Chart 22Limited Near-Term Upside For Inflation Expectations

Limited Near-Term Upside For Inflation Expectations

Limited Near-Term Upside For Inflation Expectations

Chart 23Bank Shares Thrive in A Rising Yield Environment

Bank Shares Thrive in A Rising Yield Environment

Bank Shares Thrive in A Rising Yield Environment

Banks are also cheap. US banks trade at 12.2-times forward earnings compared with 21.9-times for the S&P 500. Non-US banks trade at 10-times forward earnings compared to 16.4-times for the MSCI ACW ex-US index. Finally, we like gold as a long-term inflation hedge. We would go long gold in our structural trade recommendations if the price were to fall to $1700/ounce. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Global Investment Strategy View Matrix

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Special Trade Recommendations

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Current MacroQuant Model Scores

Don’t Sweat US Inflation…Just Yet

Don’t Sweat US Inflation…Just Yet

Highlights China’s Communist Party has overcome a range of challenges over the past 100 years, performed especially well over the past 42 years, but the macro and geopolitical outlook is darkening. The “East Asian miracle” phase of Chinese growth has ended. Potential GDP growth is slowing and it will be harder for Beijing to maintain financial and sociopolitical stability. The Communist Party has shifted the basis of its legitimacy from rapid growth to quality of life and nationalist foreign policy. The latter, however, will undermine the former by stirring up foreign protectionism. In the near term, global investors should favor developed market equities over China/EM equities. But they should favor China and Hong Kong stocks over Taiwanese stocks given significant geopolitical risk over the Taiwan Strait. Structurally, favor the US dollar and euro over the renminbi. Feature Ten years ago, in the lead up to the Communist Party’s 90th anniversary, I wrote a report called “China and the End of the Deng Dynasty,” referring to Deng Xiaoping, the Chinese Communist Party’s great pro-market reformer.1 The argument rested on three points: the end of the export-manufacturing economic model, an increasingly assertive foreign policy, and the revival of Maoist nationalism. After ten years the report holds up reasonably well but it did not venture to forecast what precisely would come next. In reality it is the rule of the Communist Party, and not the leader of any one man, that fits into China’s history of dynastic cycles. As the party celebrates a hundred years since its founding on July 23, 1921, it is necessary to pause and reflect on what the party has achieved over the past century and what the current Xi Jinping era implies for the country’s next 100 years. Single-Party Rule Can Bring Economic Success. Communism Cannot. Regime type does not preclude wealth. Countries can prosper regardless of whether they are ruled by one person, one party, or many parties. The richest countries in the world grew rich over centuries in which their governments evolved from monarchy to democracy and sometimes back again. Even today several of the world’s wealthy democracies are better described as republics or oligarchies. Chart 1China Outperformed Communism But Not Liberal Democracy

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

The rule of one person, or autocracy, is not necessarily bad for economic growth. For every Kim Il Sung of North Korea there is a Lee Kuan Yew of Singapore. But authority based on a single person often expires with that person and rarely survives his grandchild. In China, Chairman Mao Zedong’s death occasioned a power struggle. Deng Xiaoping’s attempts to step down led to popular unrest that threatened the Communist Party’s rule on two separate occasions in the 1980s. The rule of a single party is thought to be more sustainable. Japan and Singapore are effectively single-party states and the wealthiest countries in Asia. They are democracies with leadership rotation and a popular voice in national affairs. And yet South Korea’s boom times occurred under single-party military rule. The same goes for the renegade province of Taiwan. Only around the time these two reached about $11,000-$14,000 GDP per capita did they evolve into multi-party democracies – though their wealth grew rapidly in the wake of that transition. China and soon Vietnam will test whether non-democratic, single-party rule can persist beyond the middle-income economic status that brought about democratic transition in Taiwan (Chart 1). Vietnam and Taiwan are the closest communist and non-communist governing systems, respectively, to mainland China. Insofar as China and Vietnam succeed at catching up with Taiwan it will be for reasons other than Marxist-Leninist ideology. Most communist systems have failed. At the height of international communism in the twentieth century there were 44 states ruled by communist parties; today there are five. China and Vietnam are the rare examples of communist states that not only survived the Soviet Union’s fall but also unleashed market forces and prospered (Chart 2). North Korea survived in squalor; Cuba’s experience is mixed. States that close off their economies do not have a good record of generating wealth. Closed economies lack competition and investment, struggle with stagflation, and often succumb to corruption and political strife. Openness seems to be a more diagnostic variable than government type or ideology, given the prosperity of democratic Japan and non-democratic China. Has the CPC performed better than other communist regimes? Arguably. It performs better than Vietnam but worse than Cuba on critical measures like infant mortality rates and life expectancy. Has it performed better than comparable non-communist regimes? Not really, though it is fast approaching Taiwan in all of these measures (Chart 3). Chart 2Communist States Get Rich By Compromising Their Communism

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Chart 3China Catching Up To Cuba On Basic Wellbeing

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

What can be said for certain is that, since China’s 1979 reform and opening up, the CPC has avoided many errors and catastrophes. It survived the 1980s, 1990s, and 2000s without succumbing to international isolation, internal divisions, or economic crisis. It has drastically increased its share of global power (Table 1). Contrast this global ascent with the litany of mistakes and crises in the US since the year 2000. The CPC also managed the past decade relatively well despite the Chinese financial turmoil of 2015-16, the US trade war of 2018-19, and the COVID-19 pandemic. However, these events hint at greater challenges to come. China’s transition to a consumer-oriented economy has hardly begun. The struggle to manage systemic financial risk is intensifying today at risk to growth and stability (Chart 4). The trade war is simmering despite the Phase One trade deal and the change of party in the White House. And it is too soon to draw conclusions about the impact of the global pandemic, though China suppressed the virus more rapidly than other countries and led the world into recovery. Table 1China’s Global Rise After ‘Reform And Opening Up’

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Chart 4China To Keep Struggling With Financial Instability

China To Keep Struggling With Financial Instability

China To Keep Struggling With Financial Instability

Judging by the points above, there are two significant risks on the horizon. First, the CPC’s revival of neo-Maoist ideology, particularly the new economic mantra of self-reliance and “dual circulation” (import substitution), poses the risk of closing the economy and undermining productivity.2 Second, China’s sliding back into the rule of a single person – after the “consensus rule” that prevailed after Deng Xiaoping – increases the risk of unpredictable decision-making and a succession crisis whenever General Secretary Xi Jinping steps down. The party’s internal logic holds that China’s economic and geopolitical challenges are so enormous as to require a strongman leader at the helm of a single-party and centralized state. But because of the traditional problems with one-man rule, there is no guarantee that the country will remain as stable as it has been over the past 42 years. Slowing Growth Drives Clash With Foreign Powers Every major East Asian economy has enjoyed a “miracle” phase of growth – and every one of them has seen this phase come to an end. Now it is China’s turn. The country’s potential GDP growth is slowing as the population peaks, the labor force shrinks, wages rise, and companies outsource production to cheaper neighbors (Charts 5A & 5B). The Communist Party is attempting to reverse the collapse in the fertility rate by shifting from its historic “one Child policy,” which sharply reduced births. It shifted to a two-child policy in 2016 and a three-child policy in 2021 but the results have not been encouraging over the past five years. Chart 5AChina’s Demographic Decline Accelerating

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Chart 5BChina’s Demographic Decline Accelerating

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

In the best case China’s growth will follow the trajectory of Taiwan and South Korea, which implies at most a 6% yearly growth rate over the next decade (Chart 6). This is not too slow but it will induce financial instability as well as hardship for overly indebted households, firms, and local governments. Chart 6China's Growth Rates Will Converge With Taiwan, South Korea

China's Growth Rates Will Converge With Taiwan, South Korea

China's Growth Rates Will Converge With Taiwan, South Korea

The Communist Party’s legitimacy was not originally based on rapid economic growth but it came to be seen that way over the roaring decades of the 1980s through the 2000s. Thus when the Great Recession struck the party had to shift the party’s base of legitimacy. The new focus became quality of life, as marked by the Xi administration’s ongoing initiatives to cut back on corruption, pollution, poverty, credit excesses, and industrial overcapacity while increasing spending on health, education, and society (Chart 7). Chart 7China’s Fiscal Burdens Will Rise On Social Welfare Needs

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

The party’s efforts to improve standards of living and consumer safety also coincided with an increase in propaganda, censorship, and repression to foreclose political dissent. The country falls far short in global governance indicators (Chart 8). Chart 8China Lags In Governance, Rule Of Law

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

A second major new source of party legitimacy is nationalist foreign policy. China adopted a “more assertive” foreign and trade policy in the mid-2000s as its import dependencies ballooned. It helped that the US was distracted with wars of choice and financial crises. After the Great Recession the CPC’s foreign policy nationalism became a tool of generating domestic popular support amid slower economic growth. This was apparent in the clashes with Japan and other countries in the East and South China Seas in the early 2010s, in territorial disputes with India throughout the past decade, in political spats with Norway and most recently Australia, and in military showdowns over the Korean peninsula (2015-16) and today the Taiwan Strait (Chart 9). Chart 9Proxy Wars A Real Risk In China’s Periphery

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

If China were primarily focused on foreign policy and global strategy then it would not provoke multiple neighbors on opposite sides of its territory at the same time. This is a good way to motivate the formation of a global balance-of-power coalition that can constrain China in the coming years. But China’s outward assertiveness is not driven primarily by foreign policy considerations. It is driven by the secular economic slowdown at home and the need to use nationalism to drum up domestic support. This is why China seems indifferent to offending multiple countries at once (like India and Australia) as well as more distant trade partners whom it “should be” courting rather than offending (like Europe). Such assertive foreign policy threatens to undermine quality of life, namely by provoking international protectionism and sanctions on trade and investment. The US is galvanizing a coalition of democracies to put pressure on China over its trade practices and human rights. The Asian allies are mostly in step with the US because they fear China’s growing clout. The European states do not have as much to fear from China’s military but they do fear China’s state-backed industry and technological rise. Europe’s elites also worry about anti-establishment political movements just like American elites and therefore are trying to win back the hearts and minds of the working class through a more proactive use of fiscal and industrial policy. This entails a more assertive trade policy. China has so far not adapted to the potential for a unified front among the democracies, other than through rhetoric. Thus the international horizon is darkening even as China’s growth rates shift downward. China’s Geopolitical Outlook Is Dimming China’s government has overcome a range of challenges and crises. The country takes an ever larger role in global trade despite its falling share of global population because of its productivity and competitiveness. The drop in China’s outward direct investment is tied to the global pandemic and may not mark a top, given that the country will still run substantial current account surpluses for the foreseeable future and will need to recycle these into natural resources and foreign production (Chart 10). However, the limited adoption of the renminbi as a reserve currency in the face of this formidable commercial power reveals the world’s reservations about Beijing’s ability to maintain macroeconomic stability, good governance, and peaceful foreign relations. Chart 10China's Rise Continues

China's Rise Continues

China's Rise Continues

Chart 11China's Policy Uncertainty: A Structural Uptrend

China's Policy Uncertainty: A Structural Uptrend

China's Policy Uncertainty: A Structural Uptrend

China is not in a position to alter the course of national policy dramatically prior to the Communist Party’s twentieth national congress in 2022. The Xi administration is focused on normalizing monetary and fiscal policy and heading off any sociopolitical disturbances prior to that critical event, in which General Secretary Xi Jinping, who was originally slated to step down at this time according to the old rules, may be anointed the overarching “chairman” position that Mao Zedong once held. The seventh generation of Chinese leaders will be promoted at this five-year rotation of the Central Committee and will further consolidate the Xi administration’s grip. It will also cement the party’s rotation back to leaders who have ideological educations, as opposed to the norm in the 1990s and early 2000s of promoting leaders with technocratic skills and scientific educations.3 This does not mean that President Xi will refuse to hold a summit with US President Biden in the coming months nor does it mean that US-China strategic and economic dialogue will remain defunct. But it does mean that Beijing is unlikely to make any major course correction until after the 2022 reshuffle – and even then a course correction is unlikely. China has taken its current path because the Communist Party fears the sociopolitical consequences of relinquishing economic control just as potential growth slows. The new ruling philosophy holds that the Soviet Union fell because of Mikhail Gorbachev’s glasnost and perestroika, not because openness and restructuring came too late. Moreover it is far from clear that the US, Europe, and other democratic allies will apply such significant and sustained pressure as to force China to change its overall strategy. America is still internally divided and its foreign policy incoherent; the EU remains reactive and risk-averse. China has a well-established set of strategic goals for 2035 and 2049, the 100th anniversary of the People’s Republic, and the broad outlines will not be abandoned. The implication is that tensions with the US and China’s Asian neighbors will persist. Rising policy uncertainty is a secular trend that will pick back up sooner rather than later (Chart 11), to the detriment of a stable and predictable investment environment. Chart 12Chinese Government’s Net Worth High But Hidden Liabilities Pose Risks

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Monetary and fiscal dovishness and a continued debt buildup are the obvious and necessary solutions to China’s combination of falling growth potential, rising social liabilities, the need to maintain the rapid military buildup in the face of geopolitical challenges. Sovereign countries can amass vast debts if they own their own debt and keep nominal growth above average bond yields. China’s government has a very favorable balance sheet when national assets are taken into consideration as well as liabilities, according to the IMF (Chart 12). On the other hand, China’s government is having to assume a lot of hidden liabilities from inefficient state-owned companies and local governments. In the short run there are major systemic financial risks even though in the long run Beijing will be able to increase its borrowing and bail out failing entities in order to maintain stability, just like Japan, the US, and Europe have had to do. The question for China is whether the social and political system will be able to handle major crises as well as the US and Europe have done, which is not that well. Investment Takeaways The rule of a single party is not a bar to economic success – but the rule of a single person is a liability due to the problem of succession. Marxism-Leninism is terrible for productivity unless it is compromised to allow for markets to operate, as in China and Vietnam. States that close their economies to the outside world usually atrophy. There is no compelling evidence that China’s Communist Party has performed better than a non-communist alternative would have done, given the province of Taiwan’s superior performance on most economic indicators. Since 1979, the Communist Party has avoided catastrophic errors. It has capitalized on domestic economic potential and a favorable international environment. Now, in the 2020s, both of these factors are changing for the worse. China’s “miracle” phase of growth has expired, as it did for other East Asian states before it. The maturation of the economy and slowdown of potential GDP have forced the Communist Party to shift the base of its political legitimacy to something other than rapid income growth: namely, quality of life and nationalist foreign policy. An aggressive foreign policy works against quality of life by provoking protectionism from foreign powers, particularly the United States, which is capable of leading a coalition of states to pressure China. The Communist Party’s policy trajectory is unlikely to change much through the twentieth national party congress in 2022. After that, a major course correction to improve relations with the West is conceivable, though we would not bet on it. Between 2021 and China’s 2035 and 2049 milestones, the Communist Party must navigate between rising socioeconomic pressures at home and rising geopolitical pressures abroad. An economic or political breakdown at home, or a total breakdown in relations with the US, could lead to proxy wars in China’s periphery, including but not limited to the Taiwan Strait. For now, global investors should favor the euro and US dollar over the renminbi (Chart 13). Chart 13Prefer The Dollar And Euro To The Renminbi

Prefer The Dollar And Euro To The Renminbi

Prefer The Dollar And Euro To The Renminbi

Mainland investors should favor government bonds relative to stocks. Chinese stocks hit a major peak earlier this year and the government’s seizure of control over the tech sector is taking a toll. Investors should prefer developed market equities relative to Chinese equities until China’s current phase of policy tightening ends and there is at least a temporary improvement in relations with the United States. But investors should also prefer Chinese and Hong Kong stocks relative to Taiwanese due to the high risk of a diplomatic crisis and the tail risk of a war. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 The report concluded, “the emerging trends suggest a likely break from Deng's position toward heavier state intervention in the economy, more contentious relationships with neighbors, and a Party that rules primarily through ideology and social control.” Co-written with Jennifer Richmond, "China and the End of the Deng Dynasty," Stratfor, April 19, 2011, worldview.stratfor.com. 2 The Xi administration’s new concept of “dual circulation” entails that state policy will encourage the domestic economy whereas the international economy will play a secondary role. This is a reversal of the outward and trade-oriented economic model under Deng Xiaoping. See “Xi: China’s economy has potential to maintain long-term stable development,” November 4, 2020, news.cgtn.com. 3 See Willy Wo-Lap Lam, "China’s Seventh-Generation Leadership Emerges onto the Stage," Jamestown Foundation, China Brief 19:7, April 9, 2019, Jamestown.org.

Based on the reaction of financial markets, Wednesday’s FOMC meeting produced an unquestionably hawkish surprise for financial markets. US Treasuries sold off, the US dollar strengthened, and gold fell. However, equity moves were significantly more muted. The…

Highlights Oil demand expectations remain high. Realized demand continues to disappoint. This means OPEC 2.0's production-management strategy – i.e., keeping the level of supply below demand – will continue to dictate oil-price levels. US producers will remain focused on consolidation via M&A and on returning capital to shareholders, in line with the Kingdom of Saudi Arabia's (KSA) expectation. Going forward, shale producers will focus on protecting and growing profit margins. The durability of OPEC 2.0's tactical advantage arising from its enormous spare capacity – ~ 7mm b/d – is difficult to gauge: Tightening global oil markets now in anticipation of Iran's return as a bona fide exporter benefits producers globally, and could accelerate the return of US shales if that return is delayed or re-opening boosts demand more than expected. We are raising our average Brent forecast for 2021 to $66.50 vs. $63/bbl earlier, with 2H21 prices averaging $70/bbl. We are moving our 2022 and 2023 forecasts up slightly to $74 and $81/bbl (Chart of the Week). WTI will trade $2-$3/bbl lower. We remain long the S&P GSCI Dynamic Roll Index ETF (COMT) and the S&P GSCI, expecting tight supply-demand balances to further steepen backwardations in forward curves. Feature While the forecasted rebound in global oil demand continues to drive expectations for higher prices, it is the production discipline of OPEC 2.0 and capital discipline imposed on US shale producers that has and will continue to super-charge the recovery of prices. Continued monetary accommodation and fiscal stimulus notwithstanding, realized global oil demand has mostly flatlined at ~ 96mm b/d following its surge in February, as uncertainty over COVID-19 containment keeps governments hesitant about reopening their economies too quickly. Stronger demand in Asia, led by China, has been offset by weaker demand in India and Japan, where COVID-19 remains a deterrent to re-opening and recovery. The recovery in DM demand generally stalled over this period even as vaccine availability increased (Chart 2). Chart of the WeekOPEC 2.0 Comfortable With Higher Prices

Balance Of Risks Tilts To Higher Oil Prices

Balance Of Risks Tilts To Higher Oil Prices

Chart 2Global Demand Recovery Stalled

Balance Of Risks Tilts To Higher Oil Prices

Balance Of Risks Tilts To Higher Oil Prices