United States

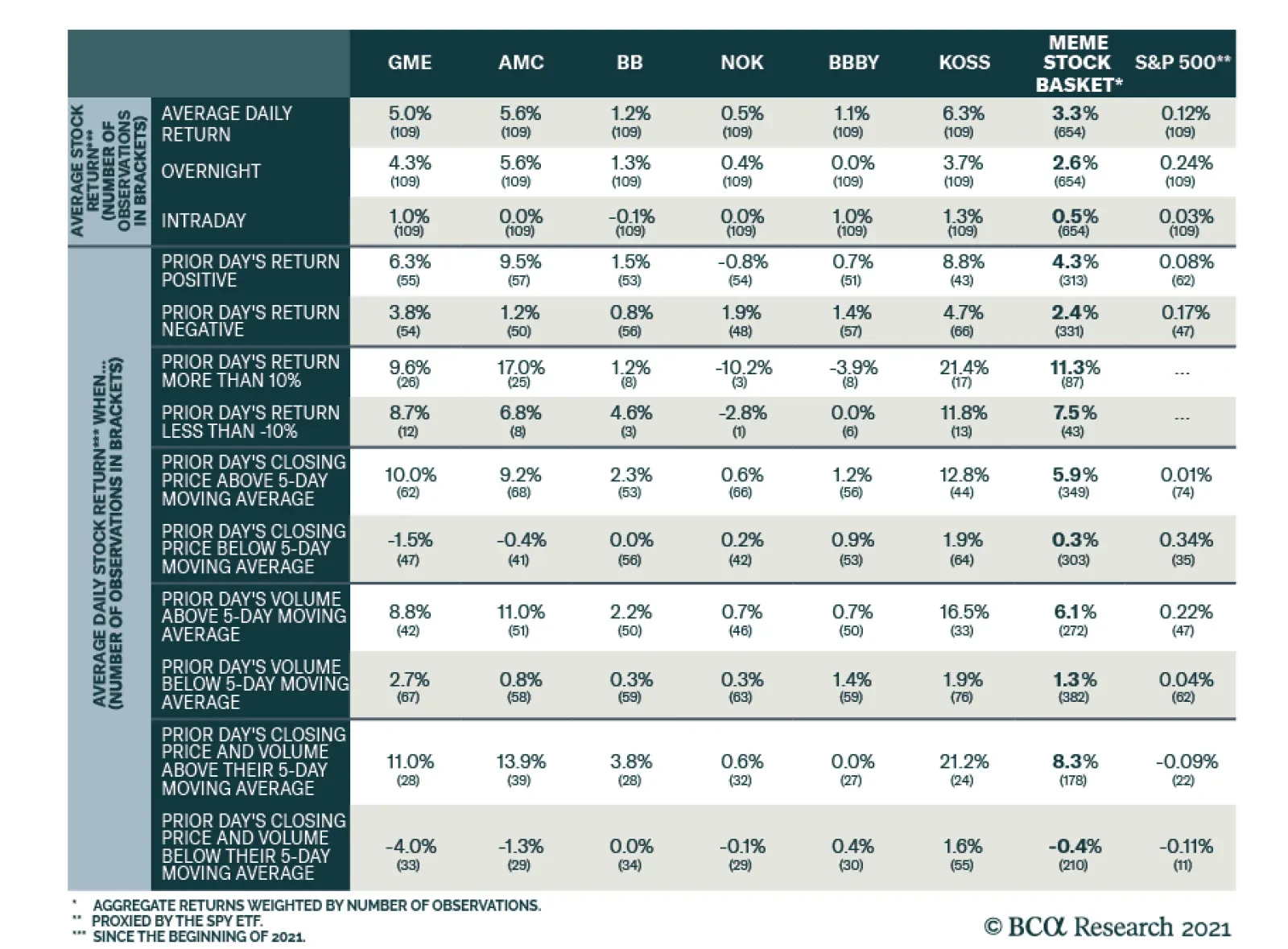

According to BCA Research’s Global Investment Strategy service, the meme stock mania is unlikely to die down anytime soon. If one were so inclined, how should one trade meme stocks? A few observations stand out from an analysis of the six popular meme…

Friday’s preliminary University of Michigan Consumer Sentiment survey for June indicates that consumer confidence is improving. The headline measure jumped to 86.4 from 82.9, exceeding the 84.2 anticipated by the consensus. This improvement was led by a…

On the surface, Thursday’s market behavior was somewhat counterintuitive. US Treasury yields declined despite a red-hot CPI report that showed headline and core surging to 30- and 29-year highs, respectively. The decline in real yields more than offset the…

Highlights Geopolitical risk is trickling back into financial markets. China’s fiscal-and-credit impulse collapsed again. The Global Economic Policy Uncertainty Index is ticking back up after the sharp drop from 2020. All of our proprietary GeoRisk Indicators are elevated or rising. Geopolitical risk often rises during bull markets – the Geopolitical Risk Index can even spike without triggering a bear market or recession. Nevertheless a rise in geopolitical risk is positive for the US dollar, which happens to stand at a critical technical point. The macroeconomic backdrop for the dollar is becoming less bearish given China’s impending slowdown. President Biden’s trip to Europe and summit with Russian President Vladimir Putin will underscore a foreign policy of forming a democratic alliance to confront Russia and China, confirming the secular trend of rising geopolitical risk. Shift to a defensive tactical position. Feature Back in March 2017 we wrote a report, “Donald Trump Is Who We Thought He Was,” in which we reaffirmed our 2016 view that President Trump would succeed in steering the US in the direction of fiscal largesse and trade protectionism. Now it is time for us to do the same with President Biden. Our forecast for Biden rested on the same points: the US would pursue fiscal profligacy and mercantilist trade policy. The recognition of a consistent national policy despite extreme partisan divisions is a testament to the usefulness of macro analysis and the geopolitical method. Trump stole the Democrats’ thunder with his anti-austerity and anti-free trade message. Biden stole it back. It was the median voter in the Rust Belt who was calling the shots all along (after all, Biden would still have won the election without Arizona and Georgia). We did make some qualifications, of course. Biden would maintain a hawkish line on China and Russia but he would reject Trump’s aggressive foreign and trade policy when it came to US allies.1 Biden would restore President Obama’s policy on Iran and immigration but not Russia, where there would be no “diplomatic reset.” And Biden’s fiscal profligacy, unlike Trump’s, would come with tax hikes on corporations and the wealthy … even though they would fall far short of offsetting the new spending. This is what brings us to this week’s report: New developments are confirming this view of the Biden administration. Geopolitical Risk And Bull Markets Chart 1Global Geopolitical Risk And The Dollar

Global Geopolitical Risk And The Dollar

Global Geopolitical Risk And The Dollar

In recent weeks Biden has adopted a hawkish policy on China, lowered tensions with Europe, and sought to restore President Obama’s policy of détente with Iran. The jury is still out on relations with Russia – Biden will meet with Putin on June 16 – but we do not expect a 2009-style “reset” that increases engagement. Still, it is too soon to declare a “Biden doctrine” of foreign policy because Biden has not yet faced a major foreign crisis. A major test is coming soon. Biden’s decision to double down on hawkish policy toward China will bring ramifications. His possible deal with Iran faces a range of enemies, including within Iran. His reduction in tensions with Russia is not settled yet. While the specific source and timing of his first major foreign policy crisis is impossible predict, structural tensions are rebuilding. An aggregate of our 13 market-based GeoRisk indicators suggests that global political risk is skyrocketing once again. A sharp spike in the indicator, which is happening now, usually correlates with a dollar rally (Chart 1). This indicator is mean-reverting since it measures the deviation of emerging market currencies, or developed market equity markets, from underlying macroeconomic fundamentals. The implication is positive for the dollar, although the correlation is not always positive. Looking at both the DXY’s level and its rate of change shows periods when the global risk indicator fell yet the dollar stayed strong – and vice versa. The big increase in the indicator over the past week stems mostly from Germany, South Korea, Brazil, and Australia, though all 13 of the indicators are now either elevated or rising, including the China/Taiwan indicators. Some of the increase is due to base effects. As global exports recover, currencies and equities that we monitor are staying weaker than one would expect. This causes the relevant BCA GeoRisk indicator to rise. Base effects from the weak economy in June 2020 will fall out in coming weeks. But the aggregate shows that all of the indicators are either high or rising and, on a country by country level, they are now in established uptrends even aside from base effects. Chart 2Global Policy Uncertainty Revives

Global Policy Uncertainty Revives

Global Policy Uncertainty Revives

Meanwhile the global Economic Policy Uncertainty Index is recovering across the world after the drop in uncertainty following the COVID-19 crisis (Chart 2). Policy uncertainty is also linked to the dollar and this indicator shows that it is rising on a secular basis. The Geopolitical Risk Index, maintained by Matteo Iacoviello and a group of academics affiliated with the Policy Uncertainty Index, is also in a secular uptrend, although cyclically it has not recovered from the post-COVID drop-off. It is sensitive to traditional, war-linked geopolitical risk as reported in newspapers. By contrast our proprietary indicators are sensitive to market perceptions of any kind of risk, not just political, both domestic and international. A comparison of the Geopolitical Risk Index with the S&P 500 over the past century shows that a geopolitical crisis may occur at the beginning of a business cycle but it may not be linked with a recession or bear market. Risk can rise, even extravagantly, during economic expansions without causing major pullbacks. But a crisis event certainly can trigger a recession or bear market, particularly if it is tied to the global oil supply, as in the early 1970s, 1980s, and 1990s (Chart 3). Chart 3Secular Rise In Geopolitical Risk Soon To Reassert Itself

Secular Rise In Geopolitical Risk Soon To Reassert Itself

Secular Rise In Geopolitical Risk Soon To Reassert Itself

While geopolitical risk is normally positive for the dollar, the macroeconomic backdrop is negative. The dollar’s attempt to recover earlier this year faltered. This underlying cyclical bearish dollar trend is due to global economic recovery – which will continue – and extravagant American monetary expansion and budget deficits. This is why we have preferred gold – it is a hedge against both geopolitical risk and inflation expectations. Tactically this year we have refrained from betting against the dollar except when building up some safe-haven positions like Japanese yen. Over the medium and long term we expect geopolitical risk to put a floor under the greenback. The bottom line is that the US dollar is at a critical technical crossroads where it could break out or break down. Macro factors suggest a breakdown but the recovery of global policy uncertainty and geopolitical risk suggests the opposite. We remain neutral. A final quantitative indicator of the recovery of geopolitical risk is the performance of global aerospace and defense stocks (Chart 4). Defense shares are rising in absolute and relative terms. Chart 4Another Sign Of Geopolitical Risk: Defense Stocks Outperform As Virus Ebbs And Military Spending Surges

Another Sign Of Geopolitical Risk: Defense Stocks Outperform As Virus Ebbs And Military Spending Surges

Another Sign Of Geopolitical Risk: Defense Stocks Outperform As Virus Ebbs And Military Spending Surges

Can The WWII Peace Be Prolonged? Qualitative assessments of geopolitical risk are necessary to explain why risk is on a secular upswing – why drops in the quantitative indicators are temporary and the troughs keep getting higher. Great nations are returning to aggressive competition after a period of relative peace and prosperity. Over the past two decades Russia and China took advantage of America’s preoccupations with the Middle East, the financial crisis, and domestic partisanship in order to build up their global influence. The result is a world in which authority is contested. The current crisis is not merely about the end of the post-Cold War international order. It is much scarier than that. It is about the decay of the post-WWII international order and the return of the centuries-long struggle for global supremacy among Great Powers. The US and European political establishments fear the collapse of the WWII settlement in the face of eroding legitimacy at home and rising challenges from abroad. The 1945 peace settlement gave rise to both a Cold War and a diplomatic system, including the United Nations Security Council, for resolving differences among the great powers. It also gave rise to European integration and various institutions of American “liberal hegemony.” It is this system of managing great power struggle, and not the post-Cold War system of American domination, that lies in danger of unraveling. This is evident from the following points: American preeminence only lasted fifteen years, or at best until the 2008 Georgia war and global financial crisis. The US has been an incoherent wild card for at least 13 years now, almost as long as it was said to be the global empire. Russian antagonism with the West never really ended. In retrospect the 1990s were a hiatus rather than a conclusion of this conflict. China’s geopolitical rise has thawed the frozen conflicts in Asia from the 1940s-50s – i.e. the Chinese civil war, the Hong Kong and Taiwan Strait predicaments, the Korean conflict, Japanese pacifism, and regional battles for political influence and territory. Europe’s inward focus and difficulty projecting power have been a constant, as has its tendency to act as a constraint on America. Only now is Europe getting closer to full independence (which helped trigger Brexit). Geopolitical pressures will remain historically elevated for the foreseeable future because the underlying problem is whether great power struggle can be contained and major wars can be prevented. Specifically the question is whether the US can accommodate China’s rise – and whether China can continue to channel its domestic ambitions into productive uses (i.e. not attempts to create a Greater Chinese and then East Asian empire). The Great Recession killed off the “East Asia miracle” phase of China’s growth. Potential GDP is declining, which undermines social stability and threatens the Communist Party’s legitimacy. The renminbi is on a downtrend that began with the Xi Jinping era. The sharp rally during the COVID crisis is over, as both domestic and international pressures are rising again (Chart 5). Chart 5Biden Administration Review Of China Policy: More China Bashing

Biden Administration Review Of China Policy: More China Bashing

Biden Administration Review Of China Policy: More China Bashing

While the data for China’s domestic labor protests is limited in extent, we can use it as a proxy for domestic instability in lieu of official statistics that were tellingly discontinued back in 2005. The slowdown in credit growth and the cyclical sectors of the economy suggest that domestic political risk is underrated in the lead up to the 2022 leadership rotation (Chart 6). Chart 6China's Domestic Political Risk Will Rise

China's Domestic Political Risk Will Rise

China's Domestic Political Risk Will Rise

Chart 7Steer Clear Of Taiwan Strait

Steer Clear Of Taiwan Strait

Steer Clear Of Taiwan Strait

The increasing focus on China’s access to key industrial and technological inputs, the tensions over the Taiwan Strait, and the formation of a Russo-Chinese bloc that is excluded from the West all suggest that the risk to global stability is grave and historic. It is reminiscent of the global power struggles of the seventeenth through early twentieth centuries. The outperformance of Taiwanese equities from 2019-20 reflects strong global demand for advanced semiconductors but the global response to this geopolitical bottleneck is to boost production at home and replace Taiwan. Therefore Taiwan’s comparative advantage will erode even as geopolitical risk rises (Chart 7). The drop in geopolitical tensions during COVID-19 is over, as highlighted above. With the US, EU, and other countries launching probes into whether the virus emerged from a laboratory leak in China – contrary to what their publics were told last year – it is likely that a period of national recriminations has begun. There is a substantial risk of nationalism, xenophobia, and jingoism emerging along with new sources of instability. An Alliance Of Democracies The Biden administration’s attempt to restore liberal hegemony across the world requires a period of alliance refurbishment with the Europeans. That is the purpose of his current trip to the UK, Belgium, and Switzerland. But diplomacy only goes so far. The structural factor that has changed is the willingness of the West to utilize government in the economic sphere, i.e. fiscal proactivity. Infrastructure spending and industrial policy, at the service of national security as well as demand-side stimulus, are the order of the day. This revolution in economic policy – a return to Big Government in the West – poses a threat to the authoritarian powers, which have benefited in recent decades by using central strategic planning to take advantage of the West’s democratic and laissez-faire governance. If the West restores a degree of central government – and central coordination via NATO and other institutions – then Beijing and Moscow will face greater pressure on their economies and fewer strategic options. About 16 American allies fall short of the 2% of GDP target for annual defense spending – ranging from Italy to Canada to Germany to Japan. However, recent trends show that defense spending did indeed increase during the Trump administration (Chart 8). Chart 8NATO Boosts Defense Spending

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

The European Union as a whole has added $50 billion to the annual total over the past five years. A discernible rise in defense spending is taking place even in Germany (Chart 9). The same point could be made for Japan, which is significantly boosting defense spending (as a share of output) after decades of saying it would do so without following through. A major reason for the American political establishment’s rejection of President Trump was the risk he posed to the trans-Atlantic alliance. A decline in NATO and US-EU ties would dramatically undermine European security and ultimately American security. Hence Biden is adopting the Trump administration’s hawkish approach to trade with China but winding down the trade war with Europe (Chart 10). Chart 9Europe Spending More On Guns

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

Chart 10US Ends Trade War With Europe?

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

A multilateral deal aimed at setting a floor in global corporate taxes rates is intended to prevent the US and Europe from undercutting each other – and to ensure governments have sufficient funding to maintain social spending and reduce income inequality (Chart 11). Inequality is seen as having vitiated sociopolitical stability and trust in government in the democracies. Chart 11‘Global’ Corporate Tax Deal Shows Return Of Big Government, Attempt To Reduce Inequality In The West

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

Risks To Biden’s Diplomacy It is possible that Biden’s attempt to restore US alliances will go nowhere over the course of his four-year term in office. The Europeans may well remain risk averse despite their initial signals of willingness to work with Biden to tackle China’s and Russia’s challenges to the western system. The Germans flatly rejected both Biden and Trump on the Nord Stream II natural gas pipeline linkage with Russia, which is virtually complete and which strengthens the foundation of Russo-German engagement (more on this below). The US’s lack of international reliability – given the potential of another partisan reversal in four years – makes it very hard for countries to make any sacrifices on behalf of US initiatives. The US’s profound domestic divisions have only slightly abated since the crises of 2020 and could easily flare up again. A major outbreak of domestic instability could distract Biden from the foreign policy game.2 However, American incapacity is a risk, not our base case, over the coming years. We expect the US economic stimulus to stabilize the country enough that the internal political crisis will be contained and the US will continue to play a global role. The “Civil War Lite” has mostly concluded, excepting one or two aftershocks, and the US is entering into a “Reconstruction Lite” era. The implication is negative for China and Russia, as they will now have to confront an America that, if not wholly unified, is at least recovering. Congress’s impending passage of the Innovation and Competition Act – notably through regular legislative order and bipartisan compromise – is case in point. The Senate has already passed this approximately $250 billion smorgasbord of industrial policy, supply chain resilience, and alliance refurbishment. It will allot around $50 billion to the domestic semiconductor industry almost immediately as well as $17 billion to DARPA, $81 billion for federal research and development through the National Science Foundation, which includes $29 billion for education in science, technology, engineering, and mathematics, and other initiatives (Table 1). Table 1Peak Polarization: US Congress Passes Bipartisan ‘Innovation And Competition Act’ To Counter China

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

With the combination of foreign competition, the political establishment’s need to distract from domestic divisions, and the benefit of debt monetization courtesy of the Federal Reserve, the US is likely to achieve some notable successes in pushing back against China and Russia. On the diplomatic front, the US will meet with some success because the European and Asian allies do not wish to see the US embrace nationalism and isolationism. They have their own interests in deterring Russia and China. Lack Of Engagement With Russia Russian leadership has dealt with the country’s structural weaknesses by adopting aggressive foreign policy. At some point either the weaknesses or the foreign policy will create a crisis that will undermine the current regime – after all, Russia has greatly lagged the West in economic development and quality of life (Chart 12). But President Putin has been successful at improving the country’s wealth and status from its miserably low base in the 1990s and this has preserved sociopolitical stability so far. Chart 12Russia's Domestic Political Risk

Russia's Domestic Political Risk

Russia's Domestic Political Risk

It is debatable whether US policy toward Russia ever really changed under President Trump, but there has certainly not been a change in strategy from Russia. Thus investors should expect US-Russia antagonism to continue after Biden’s summit with Putin even if there is an ostensible improvement. The fundamental purpose of Putin’s strategy has been to salvage the Russian empire after the Soviet collapse, ensure that all world powers recognize Russia’s veto power over major global policies and initiatives, and establish a strong strategic position for the coming decades as Russia’s demographic decline takes its toll. A key component of the strategy has been to increase economic self-sufficiency and reduce exposure to US sanctions. Since the invasion of Ukraine in 2014, Putin has rapidly increased Russia’s foreign exchange reserves so as to buffer against shocks (Chart 13). Chart 13Russia Fortified Against US Sanctions

Russia Fortified Against US Sanctions

Russia Fortified Against US Sanctions

Putin has also reduced Russia’s reliance on the US dollar to about 22% (Chart 14), primarily by substituting the euro and gold. Russia will not be willing or able to purge US dollars from its system entirely but it has been able to limit America’s ability to hurt Russia by constricting access to dollars and the dollar-based global financial architecture. Russian Finance Minister Anton Siluanov highlighted this process ahead of the Biden-Putin summit by declaring that the National Wealth Fund will divest of its remaining $40 billion of its US dollar holdings. Chart 14Russia Diversifies From USD

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

In general this year, Russia is highlighting its various advantages: its resilience against US sanctions, its ability to re-invade Ukraine, its ability to escalate its military presence in Belarus and the Black Sea, and its ability to conduct or condone cyberattacks on vital American food and fuel supplies (Chart 15). Meanwhile the US is suffering from deep political divisions at home and strategic incoherence abroad and these are only starting to be mended by domestic economic stimulus and alliance refurbishment. Chart 15Cyber Security Stocks Recover

Cyber Security Stocks Recover

Cyber Security Stocks Recover

Europe’s risk-aversion when it comes to strategic confrontation with Russia, and the lack of stability in US-Russia relations, means that investors should not chase Russian currency or financial assets amid the cyclical commodity rally. Investors should also expect risk premiums to remain high in developing European economies relative to their developed counterparts. This is true despite the fact that developed market Europe’s outperformance relative to emerging Europe recently peaked and rolled over. From a technical perspective this outperformance looks to subside but geopolitical tensions can easily escalate in the near term, particularly in advance of the Russian and German elections in September (Chart 16). Chart 16Developed Markets In Europe Will Outperform Emerging Europe Unless Russian Geopolitical Risk Abates

Developed Markets In Europe Will Outperform Emerging Europe Unless Russian Geopolitical Risk Abates

Developed Markets In Europe Will Outperform Emerging Europe Unless Russian Geopolitical Risk Abates

Developed Europe trades in line with EUR-RUB and these pair trades all correspond closely to geopolitical tensions with Russia (Chart 17). A notable exception is the UK, whose stock market looks attractive relative to eastern Europe and is much more secure from any geopolitical crisis in this region (Chart 17, bottom panel). The pound is particularly attractive against the Czech koruna, as Russo-Czech tensions have heated up in advance of October’s legislative election there (Chart 18). Chart 17Long UK Versus Eastern Europe

Long UK Versus Eastern Europe

Long UK Versus Eastern Europe

Chart 18Long GBP Versus CZK

Long GBP Versus CZK

Long GBP Versus CZK

Meanwhile Russia and China have grown closer together out of strategic necessity. Germany’s Election And Stance Toward Russia Germany’s position on Russia is now critical. The decision to complete the Nord Stream II pipeline against American wishes either means that the Biden administration can be safely ignored – since it prizes multilateralism and alliances above all things and is therefore toothless when opposed – or it means that German will aim to compensate the Americans in some other area of strategic concern. Washington is clearly attempting to rally the Germans to its side with regard to putting pressure on China over its trade practices and human rights. This could be the avenue for the US and Germany to tighten their bond despite the new milestone in German-Russia relations. The US may call on Germany to stand up for eastern Europe against Russian aggression but on that front Berlin will continue to disappoint. It has no desire to be drawn into a new Cold War given that the last one resulted in the partition of Germany. The implication is negative for China on one hand and eastern Europe on the other. Germany’s federal election on September 26 will be important because it will determine who will succeed Chancellor Angela Merkel, both in Germany and on the European and global stage. The ruling Christian Democratic Union (CDU) is hoping to ride Merkel’s coattails to another term in charge of the government. But they are likely to rule alongside the Greens, who have surged in opinion polls in recent years. The state election in Saxony-Anhalt over the weekend saw the CDU win 37% of the popular vote, better than any recent result, while Germany’s second major party, the Social Democrats, continued their decline (Table 2). The far-right Alternative for Germany won 21% of the vote, a downshift from 2016, while the Greens won 6% of the vote, a slight improvement from 2016. All parties underperformed opinion polling except the CDU (Chart 19). Table 2Saxony-Anhalt Election Results

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

Chart 19Germany: Conservatives Outperform In Final State Election Before Federal Vote, But Face Challenges

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

Chart 20Germany: Greens Will Outperform in 2021 Vote

Germany: Greens Will Outperform in 2021 Vote

Germany: Greens Will Outperform in 2021 Vote

The implication is still not excellent for the CDU. Saxony-Anhalt is a middling German state, a CDU stronghold, and a state with a popular CDU leader. So it is not representative of the national campaign ahead of September. The latest nationwide opinion polling puts the CDU at around 25% support. They are neck-and-neck with the Greens. The country’s left- and right-leaning ideological blocs are also evenly balanced in opinion polls (Chart 20). A potential concern for the CDU is that the Free Democratic Party is ticking up in national polls, which gives them the potential to steal conservative votes. Betting markets are manifestly underrating the chance that Annalena Baerbock and the Greens take over the chancellorship (Charts 21A and 21B). We still give a subjective 35% chance that the Greens will lead the next German government without the CDU, a 30% that the Greens will lead with the CDU, and a 25% chance that the CDU retains power but forms a coalition with the Greens. A coalition government would moderate the Greens’ ambitious agenda of raising taxes on carbon emissions, wealth, the financial sector, and Big Tech. The CDU has already shifted in a pro-environmental, fiscally proactive direction. Chart 21AGerman Greens Will Recover

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

Chart 21BGerman Greens Still Underrated

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

No matter what the German election will support fiscal spending and European solidarity, which is positive for the euro and regional equities over the next 12 to 24 months. However, the Greens would pursue a more confrontational stance toward Russia, a petro-state whose special relations with the German establishment have impeded the transition to carbon neutrality. Latin America’s Troubles A final aspect of Biden’s agenda deserves some attention: immigration and the Mexican border. Obviously this one of the areas where Biden starkly differs from Trump, unlike on Europe and China, as mentioned above. Vice President Kamala Harris recently came back from a trip to Guatemala and Mexico that received negative media attention. Harris has been put in charge of managing the border crisis, the surge in immigrant arrivals over 2020-21, both to give her some foreign policy experience and to manage the public outcry. Despite telling immigrants explicitly “Do not come,” Harris has no power to deter the influx at a time when the US economy is fired up on historic economic stimulus and the Democratic Party has cut back on all manner of border and immigration enforcement. From a macro perspective the real story is the collapse of political and geopolitical risk in Mexico. From 2016-20 Mexico faced a protectionist onslaught from the Trump administration and then a left-wing supermajority in Congress. But these structural risks have dissipated with the USMCA trade deal and the inability of President Andrés Manuel López Obrador to follow through with anti-market reforms, as we highlighted in reports in October and April. The midterm election deprived the ruling MORENA party of its single-party majority in the Chamber of Deputies, the lower house of the legislature (Chart 22). AMLO is now politically constrained – he will not be able to revive state control over the energy and power sectors. Chart 22Mexican Midterm Election Constrained Left-Wing Populism, Political Risk

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

Chart 23Buy Mexico (And Canada) On US Stimulus

Buy Mexico (And Canada) On US Stimulus

Buy Mexico (And Canada) On US Stimulus

American monetary and fiscal stimulus, and the supply-chain shift away from China, also provide tailwinds for Mexico. In short, the Mexican election adds the final piece to one of our key themes stemming from the Biden administration, US populism, and US-China tensions: favor Mexico and Canada (Chart 23). A further implication is that Mexico should outperform Brazil in the equity space. Brazil is closely linked to China’s credit cycle and metals prices, which are slated to turn down as a result of Chinese policy tightening. Mexico is linked to the US economy and oil prices (Chart 24). While our trade stopped out at -5% last week we still favor the underlying view. Brazilian political risk and unsustainable debt dynamics will continue to weigh on the currency and equities until political change is cemented in the 2022 election and the new government is then forced by financial market riots into undertaking structural reforms. Chart 24Brazil's Troubles Not Truly Over - Mexico Will Outperform

Brazil's Troubles Not Truly Over - Mexico Will Outperform

Brazil's Troubles Not Truly Over - Mexico Will Outperform

Elsewhere in Latin America, the rise of a militant left-wing populist to the presidency in a contested election in Peru, and the ongoing social unrest in Colombia and Chile, are less significant than the abrupt slowdown in China’s credit growth (Charts 25A and 25B). According to our COVID-19 Social Stability Index, investors should favor Mexico. Turkey, the Philippines, South Africa, Colombia, and Brazil are the most likely to see substantial social instability according to this ranking system (Table 3). Chart 25AMexico To Outperform Latin America

Mexico To Outperform Latin America

Mexico To Outperform Latin America

Chart 25BChina’s Slowdown Will Hit South America

China's Slowdown Will Hit South America

China's Slowdown Will Hit South America

Table 3Post-COVID Emerging Market Social Unrest Only Just Beginning

Joe Biden Is Who We Thought He Was

Joe Biden Is Who We Thought He Was

Investment Takeaways Close long emerging markets relative to developed markets for a loss of 6.8% – this is a strategic trade that we will revisit but it faces challenges in the near term due to China’s slowdown (Chart 26). Go long Mexican equities relative to emerging markets on a strategic time frame. Our long Mexico / short Brazil trade hit the stop loss at 5% but the technical profile and investment thesis are still sound over the short and medium term. Chart 26China Slowdown, Geopolitical Risk Will Weigh On Emerging Markets

China Slowdown, Geopolitical Risk Will Weigh On Emerging Markets

China Slowdown, Geopolitical Risk Will Weigh On Emerging Markets

Chart 27Relative Uncertainty And Safe Havens

Relative Uncertainty And Safe Havens

Relative Uncertainty And Safe Havens

China’s sharp fiscal-and-credit slowdown suggests that investors should reduce risk exposure, take a defensive tactical positioning, and wait for China’s policy tightening to be priced before buying risky assets. Our geopolitical method suggests the dollar will rise, while macro fundamentals are becoming less dollar-bearish due to China. We are neutral for now and will reassess for our third quarter forecast later this month. If US policy uncertainty falls relative to global uncertainty then the EUR-USD will also fall and safe-haven assets like Swiss bonds will gain a bid (Chart 27). Gold is an excellent haven amid medium-term geopolitical and inflation risks but we recommend closing our long silver trade for a gain of 4.5%. Disfavor emerging Europe relative to developed Europe, where heavy discounts can persist due to geopolitical risk premiums. We will reassess after the Russian Duma election in September. Go long GBP-CZK. Close the Euro “laggards” trade. Go long an equal-weighted basket of euros and US dollars relative to the Chinese renminbi. Short the TWD-USD on a strategic basis. Prefer South Korea to Taiwan – while the semiconductor splurge favors Taiwan, investors should diversify away from the island that lies at the epicenter of global geopolitical risk. Close long defense relative to cyber stocks for a gain of 9.8%. This was a geopolitical “back to work” trade but the cyber rebound is now significant enough to warrant closing this trade. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Trump’s policy toward Russia is an excellent example of geopolitical constraints. Despite any personal preferences in favor of closer ties with Russia, Trump and his administration ultimately reaffirmed Article 5 of NATO, authorized the sale of lethal weapons to Ukraine, and deployed US troops to Poland and the Czech Republic. 2 As just one example, given the controversial and contested US election of 2020, it is possible that a major terrorist attack could occur. Neither wing of America’s ideological fringes has a monopoly on fanaticism and violence. Meanwhile foreign powers stand to benefit from US civil strife. A truly disruptive sequence of events in the US in the coming years could lead to greater political instability in the US and a period in which global powers would be able to do what they want without having to deal with Biden’s attempt to regroup with Europe and restore some semblance of a global police force. The US would fall behind in foreign affairs, leaving power vacuums in various regions that would see new sources of political and geopolitical risk crop up. Then the US would struggle to catch up, with another set of destabilizing consequences.

The US May consumer price index (CPI) report produced an upside surprise. The headline number jumped to 5.0% y/y – the largest increase since August 2008 – while core CPI accelerated to a 29-year high of 3.8% y/y. Meanwhile, headline and core inflation…

The yields continue being range bound, creating an environment more favorable for companies which derive majority of their earnings further in the future. In addition, earnings growth has peaked and is slowing down, making growth stocks more attractive at times when earnings growth is becoming a little harder to find. These two factors support our thesis that it’s time to revisit growth stocks. Looking at growth names in the context of the business cycle is also instructive. The chart below shows relative performance of different S&P 500 styles during various stages of the business cycle. Historically, growth shines best during periods of slowdown, as it is one of the safer styles. Bottom Line: Investors should add growth exposure to their portfolio.

Has The Rotation Begun?

Has The Rotation Begun?

According to BCA Research’s US Political Strategy service, the Fed’s independence from politics is limited. President Biden has the potential to reshape the Fed’s Board of Governors through three personnel picks, two of which are due by January 2022. While…

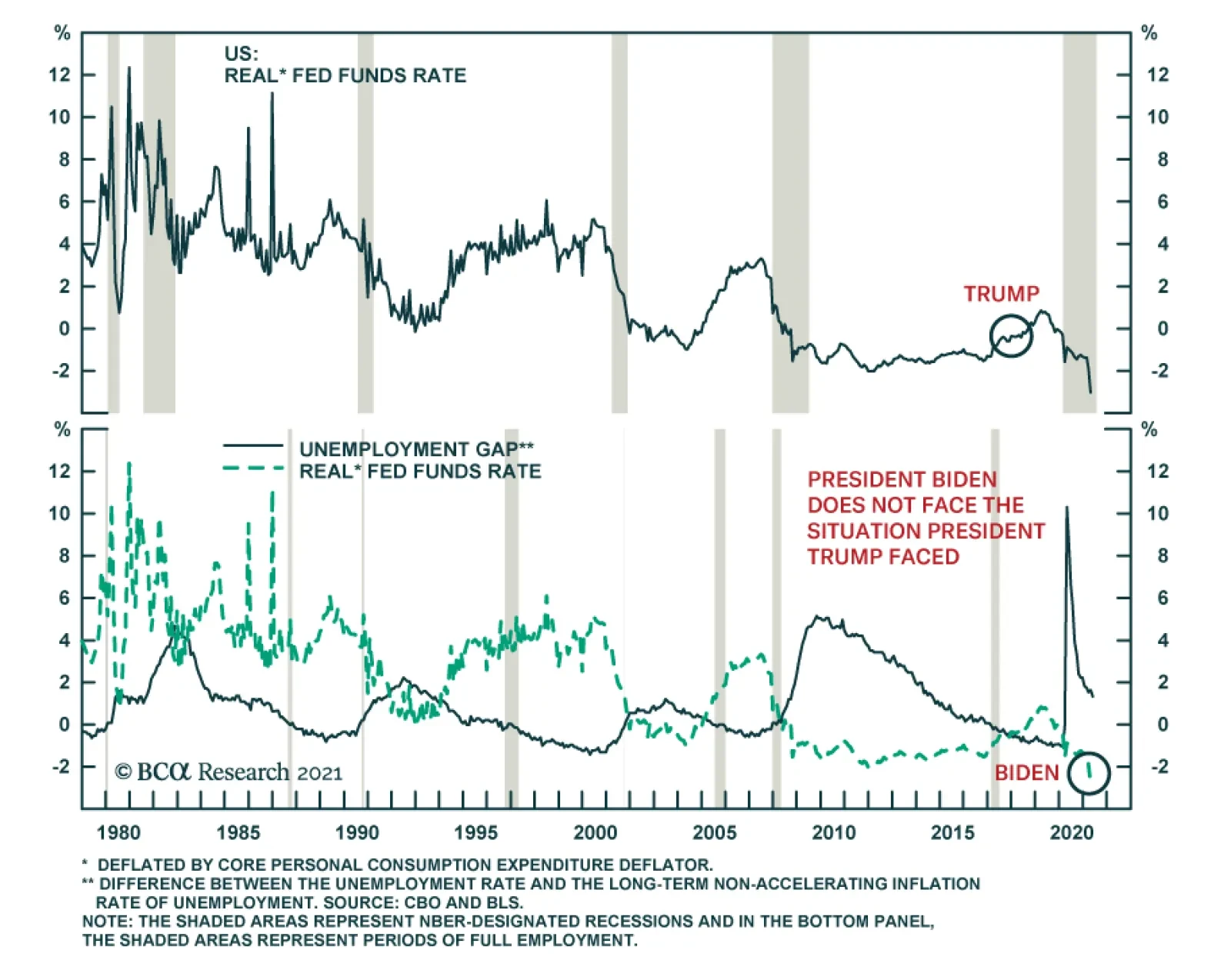

Highlights The Fed’s independence from politics is illusory. President Biden has the potential to reshape the Fed’s Board of Governors through three personnel picks, two of which are due by January 2022. While monetary policy could only get marginally more dovish, the Democratic Party’s goals would be furthered by new appointments. If Biden retains Powell then he is convinced that Powell is fully committed to today’s ultra-dovish monetary policy strategy. If he does not, then the new Fed chair will be still more dovish. Nevertheless the excessive expansion of the US money supply is reminiscent of the Arthur Burns era and suggests that any Fed chair faces a sea of troubles from 2022-26. For now stay long TIPS, infrastructure plays, cyclicals, and value stocks. Feature I do not recall a single instance where somebody in the political realm said, “We need to raise rates, they’re too low.” -Alan Greenspan, CNBC, October 18, 2018 Just before the 2020 election I held a call with a client in New York and the question arose of whether the expected winner, then candidate Joe Biden, would reappoint Federal Reserve Chairman Jerome Powell when his term expired on January 31, 2022. I argued that the odds of Biden keeping Powell in place were higher than one might think. After all, Powell reversed his stance on rate hikes in the winter of 2018-19 and then oversaw the Fed’s adoption of a new monetary policy strategy that deliberately targets an inflation overshoot. Powell would be a reliable dove for a president who would seek economic recovery above all things. The client drily responded, “There is no way that is going to happen.” We still do not know what President Biden will decide with seven months before the decision is due. Personnel appointments are a matter of information and intelligence, not political or macroeconomic analysis. From a macro point of view all that can be said is that Biden does not face the situation President Trump faced: Biden has entered early in the business cycle, under a new, ultra-easy average inflation targeting regime at the Fed. Trump entered in the middle of a business cycle, while the Fed was hiking rates (Chart 1). Chart 1Biden's and Powell's Context

Biden's and Powell's Context

Biden's and Powell's Context

Almost any new Fed chair will be largely constrained by the policy consensus on the Federal Open Market Committee (FOMC). Biden is an establishment player whose appointments so far suggest that he is unlikely to nominate a maverick capable of bucking the entire FOMC. But personalities can still make a difference at critical junctures. Nobody should be surprised if Biden opts to replace Powell with a candidate who is marginally more committed to keeping rates lower for longer. Investors should bet on dovish surprises for three reasons. First, the Fed as an institution has reached a consensus on its current policy framework, which is geared toward an inflation overshoot. Second, Powell may wish to retain his job. Third, the aforementioned client could be right and Biden may replace Powell with a more fervent proponent of ultra-easy policy. The takeaway is bullish for the time being. The Dependency Of Central Banks Central banks are part of the political bureaucracy of the nation state. Insofar as they achieve policy autonomy, or independence, it is at the forbearance of the executive or legislative branch. The ability to contain personal influences shows institutional maturity but institutions can never be fully independent. Fiscal policy is controlled by the ruling party, which will legislate in its interest. The “political business cycle” is an empirical phenomenon in which policymakers attempt to manipulate fiscal policy ahead of elections either to help or hurt the incumbent. A “political monetary cycle” also exists but its prevalence is debatable. It is more widely observed in developing countries.1 Politics in the developed world are more democratic and institutionalized so central banks have achieved considerable autonomy. In many cases their independence is enshrined in law, although the legal basis is often questionable and exaggerated.2 Not only are there checks and balances but they are reinforced by asynchronous cycles between the institutions. Term limits constrict politicians as much as or more so than monetary policymakers. Federal Reserve chairmen William McChesney Martin, Arthur F. Burns, and Jerome H. Powell were not immune to political influence but were able in their own ways to “wait out” the tenure of manipulative presidents Lyndon B. Johnson, Richard M. Nixon, and Donald J. Trump. Still, the latter examples highlight that developed markets cannot claim to be purely rationalist in their conduct of monetary policy. President Trump publicly asked, “Who is our bigger enemy, Jay Powell or Chairman Xi?” Yet this was mild compared to the treatment that Nixon gave Burns and especially that Johnson gave Martin. Johnson physically shoved Martin around a private room demanding policy easing and accused him of not caring about the lives of young American soldiers dying in Vietnam. Martin held his ground and hiked rates in 1966 despite the war.3 Arthur Burns was subjected to a relentless campaign of public and private verbal abuse by Nixon and his staffers. Nixon was convinced that he lost the 1960 election because of overly tight Fed policies and was determined not to let it happen again in 1972. Greenspan kept rates low during the Iraq war and inflated the housing bubble. Plenty of unsavory examples of political influence and interference can be drawn from other developed markets.4 All governments and monetary systems are built and run by humans and therefore fallible. Even aside from individuals and anecdotes, structural forms of central bank manipulation within the developed world include: (1) Debt accommodation: Central banks face an inexorable pressure to provide liquidity to governments running irresponsible fiscal deficits. The consequences if they refused could be devastating (Chart 2). Chart 2The Fed's Biggest Political Constraint: Debt

The Fed's Biggest Political Constraint: Debt

The Fed's Biggest Political Constraint: Debt

(2) Appointments: Presidents and executives appoint and remove leaders. In the US, the tendency for members of the Board of Governors to resign often gives the president substantial influence even aside from picking the Fed chairman, who can indeed be removed at will.5 (3) Bureaucracy: Administrative structures exert a powerful influence over the personnel, policy frameworks, and behavior of central bank leadership and staff. The candidates for top positions are heavily filtered – and once they achieve high office, their options are constrained.6 Today’s Federal Reserve supports these three points: it is highly accommodative toward the US’s soaring federal debt and its leadership consists of a tight coterie of experts and academics who share a robust consensus regarding the appropriate theory and practice of monetary policy. The outstanding question stems from item number two, appointments, where President Biden has the opportunity to influence the Fed’s board. But the third point mostly controls the available personnel. Still, the choice of the Fed chair could prove decisive under unforeseen circumstances. Historical accounts of the Fed show that the chairman exerts substantial influence over monetary policy decisions.7 Most investors know from experience that individuals and leaders can still exert an outsized influence at critical junctures. For example, premature monetary tightening occurred with negative consequences in the US in 1937, Japan in 2000, and Europe in 2011. Investors are safest to bet on institutions rather than individuals. But the choice of the Fed chair can hardly be ignored. The current context features an extraordinary expansion of the money supply, and “excess money supply,” comparable only to the inflationary 1970s (Chart 3). The Fed chair in the coming years faces an unstable and difficult sea of troubles to navigate. Chart 3Excess Money Supply Unseen In Modern Memory

Excess Money Supply Unseen In Modern Memory

Excess Money Supply Unseen In Modern Memory

Fed Chairs Care About Their Careers But Not Midterm Elections Political influence over monetary policy is measurable. A substantial body of academic literature reveals not only the above structural political factors but also that ideological affiliation – i.e. the political party whose president appointed the Fed chair – influences interest rates. So do elections and the career interests of Fed chairmen. Consider the following findings: Abrams and Iossifov show evidence of abnormally expansionary monetary policy if the president and the chair are affiliated with the same political party.8 Gamber and Hakes show evidence of a lowered federal funds rate if the Fed chair stands for reappointment in the two years following a national election – i.e. Fed chairmen accommodate political pressures in the latter part of term to increase odds of reappointment.9 Dentler shows that while the Fed funds rate does not fall in advance of elections to help presidents in general, it is found to fall when the Fed chair and president have the same partisan affiliation, especially when the Fed chair’s reappointment is looming. Also the Fed funds rate is abnormally high before elections if the Fed chair hails from the opposite party of the incumbent president.10 Dentler shows specifically that Fed chair career motivations matter. If you omit career considerations, then it is not so much partisan affiliation as partisan opposition that can influence monetary policy. In effect, there is a potential increase in policy rate before elections. Dentler calls this a “reverse political monetary policy cycle.”11 In essence, a Fed chair is more likely to lean into his partisan affiliation as an incumbent president seeks reelection. It is hard to prove this behavior is partisan because it conforms with the idea of a staunchly independent central bank. Now let us look at the data first hand. In the following analysis we focus on the nominal Fed funds rate alongside (1) the headline consumer price index and (2) an implied policy rate following a simple Taylor Rule using potential GDP, the core PCE deflator, and the unemployment rate.12 We chose the nominal Fed funds rate and headline consumer price index because they should provide an indication of how the US president and public perceived interest rates and inflation. These factors are critical for the president’s decisions as to whether to reappoint or replace sitting Fed chairmen. However, we also use the Taylor Rule as a proxy for the correct or appropriate policy rate at the time, recognizing that headline CPI is insufficient. We observe the following: Burns worked closely with President Nixon and his tenure has always been controversial. The simple evidence shown here suggests that he accommodated Nixon in 1972 but did not accommodate President Ford’s bid for the presidency in 1976. He might have stayed easy a bit longer than necessary in 1977 ahead of President Carter’s decision on whether to reappoint him (Chart 4). Chart 4AArthur Burns As Fed Chair

Arthur Burns As Fed Chair

Arthur Burns As Fed Chair

Chart 4BArthur Burns As Fed Chair

Arthur Burns As Fed Chair

Arthur Burns As Fed Chair

Miller’s tenure was marred by stagflation. He did not accommodate the Democrats during the 1978 midterm election and probably could not have done so. Carter promoted him to Treasury Secretary as a way of removing him from the Fed chair. The episode is a reminder that the president can remove the Fed chair – as the best constitutional studies show – but he may need to get creative about how to do it to avoid a political storm (Chart 5). Volcker may have accommodated Carter somewhat but not entirely in 1980. His actions are debatable around Reagan’s election in 1984. But Volcker laid inflation low and his reappointment by Reagan in 1983 makes sense in the context of that triumph (Chart 6). Chart 5William Miller As Fed Chair

William Miller As Fed Chair

William Miller As Fed Chair

Chart 6Paul Volcker As Fed Chair

Paul Volcker As Fed Chair

Paul Volcker As Fed Chair

Greenspan cannot really be said to have accommodated Bush in 1992 though rates fell. He cracked down on inflation regardless of the 1994 midterm election, which turned out badly for President Clinton and the Democrats. But Clinton did not hold it against him – inflation had been brought down without a recession. Greenspan was tame during Clinton’s reelection bid in 1996 despite rising inflation – he hiked rates immediately thereafter. Clinton reappointed him in the midst of a rate-hike cycle justified by rising inflation, regardless of any risk to the Democratic bid in the 2000 election (Chart 7). Chart 7AAlan Greenspan As Fed Chair

Alan Greenspan As Fed Chair

Alan Greenspan As Fed Chair

Chart 7BAlan Greenspan As Fed Chair

Alan Greenspan As Fed Chair

Alan Greenspan As Fed Chair

Bernanke’s tenure was dominated by the subprime mortgage crisis and Great Recession. He cannot be said to have accommodated the Republicans in 2008, though they were doomed anyway. President Obama’s decision to reappoint him in 2009 was a clear example of an urgent need to maintain policy continuity. Obama announced his replacement in 2013, after the crisis had passed (Chart 8). Chart 8ABen Bernanke As Fed Chair

Ben Bernanke As Fed Chair

Ben Bernanke As Fed Chair

Chart 8BBen Bernanke As Fed Chair

Ben Bernanke As Fed Chair

Ben Bernanke As Fed Chair

Yellen’s decision to pause hiking interest rates in 2016 is debatable and can be said to have accommodated the Democratic Party that year. She was replaced by President Trump in the midst of a rate-hike cycle justified by conditions (Chart 9). Powell hiked rates four times in 2018 despite the onset of a trade war with China. Powell cannot be said to have accommodated the Republicans in the 2018 midterm election. His behavior in 2020 was dominated by the COVID-19 crisis (Chart 10). Chart 9Janet Yellen As Fed Chair

Janet Yellen As Fed Chair

Janet Yellen As Fed Chair

Chart 10Jerome Powell As Fed Chair

Jerome Powell As Fed Chair

Jerome Powell As Fed Chair

The point is not to claim that politics is the driving factor behind monetary policy but rather to observe the cruxes in which personal and political motivations are at least mixed with technocratic and institutional decisions. Incidentally our observations largely corroborate the relevant academic literature. If there is one solid rule that emerges from this analysis, it is that Fed chairmen and chairwomen do not accommodate midterm elections. There are no exceptions in the data shown here. If anything they are more hawkish. At the same time, it is true (though sometimes exaggerated) that rate hikes tend to be put on pause during presidential election years. And this tendency is observable not only during times in which a crisis makes rate hikes impossible. Furthermore a close examination of these charts supports the contention that Fed chairs tend to avoid or delay rate hikes prior to the president’s decision whether to reappoint them. There are exceptions but the charts do not disconfirm the hypothesis, which is intuitive because it fits with the central banker’s self-interest. Biden Faces Zero Risk From A New Chair Or Some Risk From Powell A flat application of the rules of thumb in the previous section would suggest that Powell will push for easier policy than necessary ahead of Biden’s decision whether to reappoint him. It would also suggest that, if reappointed, Powell will not make any special accommodation for the Democrats in the critical 2022 midterms or in 2023. Obviously the reality might work out differently this time. But it is legitimate to suggest that retaining Powell poses a risk to the Democrats’ control of the economy ahead of the 2024 elections, even though we know we will get hate mail for saying it. Investors should not assume that there is a powerful norm in favor of the president’s retaining the sitting Fed chair in the name of continuity and “doing no harm.” The modern period of the Federal Reserve begins with the Fed-Treasury Accord in 1951. There have been seven changes of the Fed chair since that time and three of them occurred because of a change of political party in the White House (Martin to Burns, Burns to Miller/Volcker, and Yellen to Powell). While President Obama retained Bernanke, the reappointment came in early 2009, in the midst of a historic crisis. Biden has much greater flexibility than that today. And while Clinton retained Greenspan, the above analysis suggests that Democrats may warn Biden against doing the same. Most importantly Biden is president at a period of peak polarization in the US, when most of his Democratic Party and the US political establishment believe that democracy itself is at risk of dying at the hands of the Trumpist populism that is overtaking the Republican Party. If this is the view then even marginal risks to Democratic election prospects over the next four years should not be willingly taken. Biden’s dilemma can be illustrated easily by game theory. If he retains Powell he runs some risk of a hawkish surprise, however small, whereas if he replaces Powell he can avoid that risk. Powell regains some individual discretion if he is reappointed and therefore a hawkish surprise cannot be ruled out. The game theory implies that Biden will opt to remove Powell, but obviously that is up to Biden. Note that there is no stable equilibrium as Powell’s decision is shown as data-dependent and indifferent to the outcome (which may not truly be the case) (Diagram 1). Diagram 1Game Theory: Will The President Reappoint The Fed Chair?

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Biden must also choose a replacement for Vice Chair Richard Clarida, whose term expires in January 2022. Later, in June 2023, John Williams’s tenure on the board will expire (Diagram 2). With three new appointments Biden would be able to remake the board both slightly more dovish and considerably more diverse. Diversity and inclusiveness in top government positions are key aspects of Biden’s and the Democrats’ overall agenda. Diagram 2Biden Could Replace At Least Three Fed Governors

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

The history of the Fed shows that leaders tend to be captured by the institution. Powell is fully absorbed into the new Fed consensus and his personal legacy depends on executing the new ultra-dovish monetary policy strategy that he himself ushered into being. While Modern Monetary Theory (MMT) has made great strides, it is not easy for Biden to get a true believer confirmed in the Senate. In this sense, it does not matter whether Biden replaces Powell – the result will be largely the same and in line with the Fed’s current policy framework. We have a lot of sympathy with this argument. It emphasizes the checks and balances on the individual policymaker, which is the method we use to analyze US politics. The Fed has given very explicit criteria for lifting rates off the zero lower bound that are tied to specific economic outcomes. They have removed a lot of the discretion from that decision. Anyone qualified to take up the Fed chair would understand that it would be very risky to deviate from that specific guidance: the Fed would lose a lot of credibility. It would have to be a very non-mainstream pick to do that. That is not likely to happen. But again – personalities can matter at inflection points. Some would argue that Biden will not be able to find any credible candidates who can pass Senate confirmation and still be significantly more dovish than Powell (the Senate being divided equally between the two parties). However, Lael Brainard, Raphael Bostic, and Neel Kashkari are all Fed insiders who would be likely to pass the Senate and marginally more dovish than Powell, albeit supporters of the current policy framework. They would also advance the diversity agenda in different ways. They are more likely nominees than other potential candidates (Table 1). Table 1Potential Successors To Powell As Fed Chair

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Note that the focus on inclusiveness is not only about personnel but also about the inclusiveness of the economy and hence it could affect monetary policy decisions. Inclusiveness as well as climate change and inequality are concerns outside of the Fed’s official mandate, where monetary policy will have a limited effect, but any influence of these issues whatsoever would point to dovish surprises. Biden can advance this agenda without legislative change through appointments. Investment Takeaways The Fed chair appointment is a misleading win-win situation for markets. If Biden retains Powell, it is because Powell has proved thoroughly committed to the Fed’s new ultra-dovish monetary policy strategy, whereas if Biden replaces him, the replacement will be ultra-dovish. However, this win-win is misleading because beyond the near term the Fed will have to normalize policy. The Fed will ultimately remain data-dependent and the rapid closing of the output gap combined with a historic increase in excess money supply will push up inflation and require Fed responses regardless of the future chairman or chairwoman (Chart 11). Our US Bond Strategist Ryan Swift emphasizes that the Fed’s policy framework is very explicit. In order to normalize policy it needs to see inflation above the 2% target, the economy at maximum employment, and a convincing inflation overshoot (Table 2). The first goal is already met, with 12-month PCE inflation above target. An inflation overshoot will necessarily follow from the first goal combined with the second goal. Therefore the focal point for investors should be the second goal, “maximum employment,” i.e. the unemployment rate and labor participation rate (Chart 12). Positive data surprises on the employment front will accelerate the time frame. Chart 11Output Gap To Close Rapidly

Output Gap To Close Rapidly

Output Gap To Close Rapidly

Table 2Checklist For Fed Liftoff

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Chart 12Charting The Checklist For Fed Liftoff

Charting The Checklist For Fed Liftoff

Charting The Checklist For Fed Liftoff

For now we remain long TIPS relative to duration-matched nominal Treasuries in expectation of dovish policy surprises. We may modify this trade in the near future. The upside is limited now that ten-year breakevens and five-year/five-year forward breakevens have reached the point where they are consistent with the Fed’s goal of well-anchored inflation expectations. But the above analysis supports this trade. Of course, the Fed’s actions should be taken into context with fiscal policy as well as external events and the US dollar. In the near term we continue to advise a cautious approach given that the US dollar is resting at a critical juncture, around 90 on the DXY. If the dollar breaks down beneath this level then it could fall substantially further. From a macro perspective this is what we would expect given the standing of budget deficit and real interest rates. Today’s historic combination of loose fiscal, loose monetary policy is dollar-bearish (Chart 13). The implication is positive for equities, especially cyclical and value sectors, so we maintain our current positioning. Chart 13Loose Monetary, Loose Fiscal Policy Threaten The Dollar

Loose Monetary, Loose Fiscal Policy Threaten The Dollar

Loose Monetary, Loose Fiscal Policy Threaten The Dollar

Our sister Geopolitical Strategy highlights China among other foreign policy challenges to the bearish dollar view and global risk appetite. This summer should provide some clarity on whether global policy uncertainty will rise and reinforce the dollar’s floor (Chart 14). Chart 14Geopolitical Risk And Policy Uncertainty Put Floor Under Dollar?

Geopolitical Risk And Policy Uncertainty Put Floor Under Dollar?

Geopolitical Risk And Policy Uncertainty Put Floor Under Dollar?

Biden is still highly likely to pass an infrastructure bill this year (80% subjective odds). Any failure of bipartisan talks with Republicans will simply result in an all-Democratic bill via budget reconciliation. West Virginia Senator Joe Manchin will not prevent the passage of a bipartisan infrastructure bill and/or Biden’s next reconciliation bill (the American Jobs Plan). Manchin’s current tensions with the Democratic caucus center on the so-called “For The People” voting rights bill and the Senate filibuster, not the question of infrastructure and corporate tax hikes. Indeed Manchin may be forced to accept a higher corporate tax rate than his preferred 25% if he wants to make peace with his party. It is not inconceivable that he could defect from his party – the Republicans lost a 50-seat majority in the Senate this way as recently as 2001. But we have long argued that Manchin will support Biden’s signature legislative achievement. The market may be temporarily disappointed by stimulus hiccups but we view the infrastructure bill as a “buy the rumor, sell the news” dynamic for US cyclicals. While a fiscal policy weak spot will develop late in 2021 and early 2022, after the American Rescue Plan Act’s provisions expire but before new funds arrive from the American Jobs Plan, nevertheless the recovery of the private economy both at home and abroad should provide a bridge. The implication of the above analysis is to stay invested in the stock market and maintain a constructive outlook over the cyclical (12-month) time horizon while exercising near-term caution due to the dollar and geopolitical risk. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1USPS Trade Table

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Table A2Political Risk Matrix

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Table A3Political Capital Index

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Table A4APolitical Capital: White House And Congress

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Table A4BPolitical Capital: Household And Business Sentiment

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Table A4CPolitical Capital: The Economy And Markets

Will Biden Re-Appoint Powell? Does It Matter?

Will Biden Re-Appoint Powell? Does It Matter?

Footnotes 1 For political monetary cycles see Edward N. Gamber and David R. Hakes, “The Federal Reserve’s response to aggregate demand and aggregate supply shocks: Evidence of a partisan political cycle,” Southern Economic Journal 63:3 (1997), 680-91. For developed versus developing market political monetary cycles, see S. Alpanda and A. Honig, “The impact of central bank independence on political monetary cycles in advanced and developing nations,” Journal of Money, Credit and Banking 41:7 (2009), 1365-1389. 2 In the US, the Fed’s independence rests on dubious constitutional and legal supports but is nevertheless well-established in legal and political practice. See Peter Conti-Brown, “The Institutions of Federal Reserve Independence,” Yale Journal on Regulation 32 (2015), 257-310. 3 Lawrence Bauer and Alex Faseruk, “Understanding Political Pressures, Monetary Policy, and the Independence of the Federal Reserve in the United States from 1960-2019,” Journal of Management Policy and Practice 21:3 (2020), 41-63. 4 Kuttner and Posen (2007) demonstrate that financial markets respond to newsworthy developments with central bankers across the developed world. See footnote 7 below. 5 See Conti-Brown, footnote 2 above. See also Kelly H. Chang, Appointing Central Bankers: The Politics of Monetary Policy in the United States and European Union (Cambridge: CUP, 2003). 6 See Alexander W. Salter and Daniel J. Smith, “Political economists or political economists? The role of political environments in the formation of Fed policy under Burns, Greenspan, and Bernanke,” The Quarterly Review of Economics and Finance 71 (2019), 1-13. 7 See Dentler, 241. See also Ellen E. Mead, “The FOMC: Preferences, Voting, and Consensus,” Federal Reserve Bank of St. Louis Reivew 87:2 (2005), 93-101; Kenneth N. Kuttner and Adam S. Posen, “Do Markets Care Who Chairs the Central Bank?” National Bureau of Economic Research, Working Paper 13101 (May 2007), nber.org. 8 B. A. Abrams and P. Iossifov, “Does the Fed contribute to a political business cycle?” Public Choice 129 (2006), 249-62. 9 Gamber and Hakes, “The Taylor rule and the appointment cycle of the chairperson of the Federal Reserve,” Journal of Economics and Business 58 (2006), 55-66. 10 Alexander Dentler, “Did the Fed raise interest rates before elections?” Public Choice 181 (2019), 239-73. 11 Dentler, 259, characterizes the Fed chairs as follows: “We believe that Martin was more susceptible to political infuences than his colleagues, but he never worked in opposition to a president in our sample period. Neither did Arthur Burns; however, we find him to be a moderating force with respect to ideological biases, though he appears to have been vulnerable to threats regarding his career. We find Volcker to respond more strongly than most other chairs to ideological motives and career incentives. Greenspan, on the other hand, did not fall prey to biased behavior that characterizes the other chairs. Bernanke’s tenure is probably the most difficult to interpret.” 12 Real Potential GDP Growth + Core PCE Deflator + 0.5 * (Core PCE Deflator – 2% Target) - 0.5 * (Unemployment Rate – NAIRU). We prefer real potential GDP to estimates of the real neutral rate because it is simpler and more transparent.

Highlights Bond Market Performance: Government bonds in the developed economies are currently trapped in ranges, consolidating the sharp upward moves seen in the first quarter of 2021. This is only a pause in the broader cyclical uptrend, however, with central banks under increasing pressure to turn less dovish amid surging inflation and tightening labor markets. Oversold USTs: Technical indicators of yield/price momentum and investor sentiment/positioning suggest that US Treasuries are oversold. Working off this condition can take another 2-3 months, based on an analysis of past oversold episodes. Beyond that, higher yields loom with the Fed starting to prepare the markets for a taper in 2022. Stay underweight Treasuries in global bond portfolios on a cyclical basis. RBA Checklist: Only one of the five components of our “RBA Checklist” – designed to measure the pressures that would force the Reserve Bank of Australia to turn less dovish – is flashing such a signal. We are upgrading our recommended allocation for Australian government bonds to overweight on a tactical (0-6 months) investment horizon. Feature Dear Client, Next week, in lieu of our regularly weekly report, I will be hosting a webcast on Tuesday, June 15 where I will discuss the outlook for global fixed income markets in the second half of 2021. Following that, we will be jointly publishing our bi-annual Global Central Bank Monitor Chartbook with our colleagues at BCA Research Foreign Exchange Strategy on Friday, June 18th. We will return to our regular publishing schedule on Tuesday, June 29th. Best Regards, Rob Robis Chart of the WeekA Tale Of Two Quarters

A Summer Nap For Global Bond Yields

A Summer Nap For Global Bond Yields

The performance of government bond markets in the developed world so far in 2021 has been a tale of two quarters. In Q1, yields were rising steadily on the back of upside surprises in global growth and emerging signs of the biggest inflation upturn seen in nearly a generation. The Bloomberg Barclays Global Treasury index delivered a total return of -2.7% (hedged into US dollars) during the quarter, with no country escaping losses (Chart of the Week). The biggest declines were seen in the UK (-7.5%) the US (-4.3%), with the smallest losses occurring in Japan (-0.3%) and Italy (-0.7%). Chart 2Lower Vol Means High Yielders Outperform Low Yielders

Lower Vol Means High Yielders Outperform Low Yielders

Lower Vol Means High Yielders Outperform Low Yielders

Q2 has been a different story, however. Yields have retreated somewhat from the year-to-date peaks seen at the end of Q1, leading to positive returns so far in Q2 in the UK (+0.8), the US (+1.2%) and Australia (+1.1%). The laggards are the low yielding euro area markets, most notably Italy (-0.7%) and France (-0.9%), that have seen yields move higher on the back of accelerating European growth. The Q2 returns look very much like a carry-driven market, with higher-yielding markets outperforming lower-yielding ones. That trend can persist if the current backdrop of low market volatility persists (Chart 2), although this calm will eventually be broken by a shift towards less dovish monetary policies. Some countries will make that shift at a faster pace than others, leading to relative value opportunities for bond investors in the latter half of 2021. This week, we discuss one such opportunity – Australia versus the US. US Treasuries: Oversold & Trendless – For Now After reaching a 2021 intraday high of 1.77% back on March 30, the benchmark 10-year US Treasury yield has traded in a narrow 15bp range between 1.55% and 1.70%. From a fundamental perspective, US yields are lacking direction because inflation expectations have already made a major upward adjustment to the more inflationary backdrop, but real yields have remained depressed by the continued dovish messaging from the Fed – for now - with regards to the timing of tapering or future rate hikes. From a technical perspective, however, the sideways pattern for US Treasury yields is also consistent for a market that trying to work off an oversold condition. Most of the technical indicators for the US Treasury market that we monitor regularly were at or close to the most bearish/oversold extremes seen since 2000 (Chart 3): Chart 3US Treasuries Are Working Off An Oversold Condition

US Treasuries Are Working Off An Oversold Condition

US Treasuries Are Working Off An Oversold Condition

The 10-year Treasury yield is 39bps above its 200-day moving average, but that gap was as high as 84bps on March 19; The 26-week total return of the 10-year Treasury is -4.7%, after reaching a low of -8.8% on March 19; The JP Morgan client survey of bond managers and traders shows some of the largest underweight duration positioning in the 19-year history of the series; The Market Vane index of sentiment for Treasuries is in the bottom half of the range that has prevailed since 2000; The CFTC data on positioning in 10-year Treasury futures is the only one of our indicators that is not signaling an oversold market, with a small net long position of +3% (scaled by open interest). The overall message of these indicators suggests that price momentum and positioning reached such a bearish extreme by mid-March that some pullback in Treasury yields was inevitable. However, a look back at past periods when Treasuries became heavily oversold since the turn of the century shows that the duration and magnitude of such a pullback is highly variable – anywhere from two months to ten months. The main determining factors are the trends in economic growth and inflation in the US, and the Fed’s expected policy response to both. To show this, we conducted a simple study, updating work we first presented in a 2018 report.1 We looked at “oversold episodes” since 2000, which began when the 10-year Treasury yield was trading at least 50bps above its 200-day moving average. We then defined the end of the oversold episode as simply the point when the 10-year Treasury yield subsequently converged back to its 200-day moving average. We then looked at the length of the episode (in days), and the change in bond yields, for each oversold episode. There were nine such episodes since the year 2000, not counting the current one which has not yet ended. In Table 1, we rank the episodes by the number of days it took to complete each one, based on our simple moving average rule. We also show the change in both the 10-year Treasury yield and its 200-day moving average during each episode, to show how the convergence between the two unfolds. Table 1A Look At Prior Episodes Of An Oversold Treasury Market

A Summer Nap For Global Bond Yields

A Summer Nap For Global Bond Yields

To describe the US economic backdrop during each episode, we looked at the change in the ISM manufacturing index and core PCE inflation during those oversold periods. We also show changes in two important determinants of the level of Treasury yields: inflation expectations using 10-year TIPS breakeven rates, and Fed rate hike expectations using our 12-month Fed discounter which measures the expected change in interest rates - one year ahead - priced into the US overnight index swap (OIS) curve. At the bottom of the table, we show the average for all nine oversold episodes, as well as the averages for the episodes were the ISM was rising and where core PCE inflation was rising. Chart 4US Treasury Market Oversold Episodes: 2003-2007

US Treasury Market Oversold Episodes: 2003-2007

US Treasury Market Oversold Episodes: 2003-2007

There are a few messages gleaned from the results in Table 1: The longest correction of an oversold Treasury market since 2000 took place between February 2018 and December 2018, when 305 days passed before the 10-year yield fell back to its 200-day moving average; The shortest correction was between June 2007 and August 2007, where only 52 days elapsed; Treasury yields typically decline during oversold periods, with two notable exceptions: 2018 and 2013/14, which were also the two longest episodes; During all of the oversold periods, markets reduced the amount of expected Fed tightening by an average of 26bps. However, that was entirely concentrated in four of the nine episodes - including three of the four shortest episodes – and is typically associated with a decline in inflation expectations. Growth momentum appears to be a bigger factor than inflation momentum in determining the length of an oversold episode, with longer episodes typically occurring alongside a rising ISM index, and vice versa. The notable exception was the longest episode in 2018, where the ISM declined by six points, although the bulk of that decline occurred in a single month at the end of the period (November 2018). For the more visually oriented, we present the time series for all the data in Table 1, shaded for the oversold periods, in Chart 4 (for the 2003-2007 period), Chart 5 (2008-2012), Chart 6 (2013-2017) and Chart 7 (2018 to today). We’ve added one additional variable – our Fed Monitor, designed to signal the need for tighter or looser US monetary policy – in the bottom panel of each of those charts. Chart 5US Treasury Market Oversold Episodes: 2008-2012

US Treasury Market Oversold Episodes: 2008-2012

US Treasury Market Oversold Episodes: 2008-2012

Chart 6US Treasury Market Oversold Episodes: 2013-2017

US Treasury Market Oversold Episodes: 2013-2017

US Treasury Market Oversold Episodes: 2013-2017

Chart 7US Treasury Market Oversold Episodes: 2018 To Today

US Treasury Market Oversold Episodes: 2018 To Today

US Treasury Market Oversold Episodes: 2018 To Today

What does this look back tell us about looking ahead? The current episode, at only 105 days old, is still 62 days “younger” than the average oversold period, and 76 days “younger” than the average period where core inflation was rising. This would put the end of the current episode sometime in August. The ISM is essentially unchanged over the current episode so far, making it difficult to draw conclusions based on growth momentum – although the longest episode in 2018 shows that yields can trade sideways for a long time, even in the absence of a big slowing of growth, if the Fed is in a rate hiking cycle. However, the current episode differs dramatically from others in this analysis on two critical fronts. Core inflation has surged 1.6 percentage points since the oversold period began in February, far more than any other episode, while the gap between a rapidly increasing Fed Monitor and a flat 12-month Fed Discounter is also unique among post-2000 oversold periods. In other words, the Treasury market is still vulnerable to a repricing of Fed tightening expectations, especially with positioning and sentiment measures like the Market Vane survey and net futures positioning not yet at fully bearish extremes. Bottom Line: The current oversold condition in the US Treasury market can take another 2-3 months to unwind, based on an analysis of past oversold episodes. Beyond that, higher yields loom with the Fed starting to prepare the markets for a taper in 2022. Stay underweight Treasuries in global bond portfolios on a cyclical basis. RBA Checklist Update: No Case For A Hawkish Turn Yet Australia has been one of the top performing government bond markets within the developed economies, as discussed earlier. This performance has occurred even with strong acceleration of both Australian economic momentum and market-based inflation expectations (Chart 8). Despite our RBA Monitor flashing pressure on the RBA to tighten, and the Australian OIS curve already discounting 48bps of rate hikes over the next two years, Australian bond yields have remained very well behaved during the “calm” second quarter for global fixed income. Chart 8RBA Policies Limiting Rise In Bond Yields

RBA Policies Limiting Rise In Bond Yields

RBA Policies Limiting Rise In Bond Yields

Chart 9RBA Stimulus Takes Many Forms