United States

The 10-year US Treasury yield has been range bound between 1.5% and 1.7% for the past three months despite fireworks in the US economic data, from CPI readings to unemployment beats. The fact that the bond market has refused to budge no matter how positive US data got, confirms our view that all the good news has already been priced in. Citigroup US economic surprise index (CESI) is hovering around zero, which corroborates the same message. Given a tight positive correlation (0.44) between CESI and UST10Y, and the fact that growth is peaking, it is unlikely that the bond market will enter another aggressive sell-off phase (see chart). The implication for equities is that long-duration growth equities, beaten down by rising yields, may stage a come back, especially once inflation data makes a clear ∩-turn on a year-over-year basis. Bottom Line: Bond market is likely to remain calm over the next three to six months, and it’s time to revisit beaten down growth names. Stay tuned for future research on the topic.

Time to Revisit Growth Names

Time to Revisit Growth Names

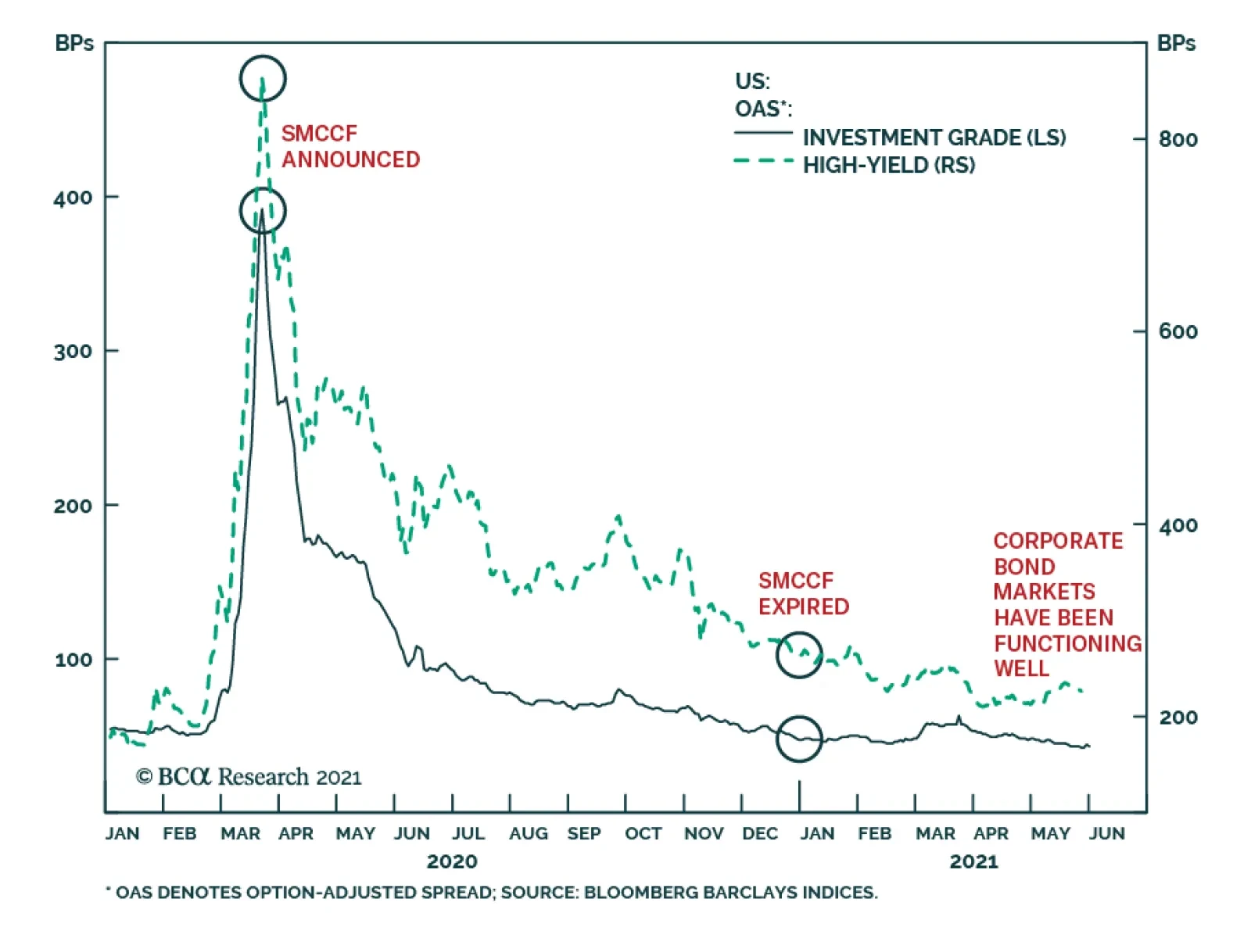

On Wednesday, the Fed announced plans to begin selling its corporate debt holdings from the Secondary Market Corporate Credit Facility (SMCCF) – an emergency lending facility initiated amid liquidity concerns in March last year. The wind-down will begin with…

Tactically Bearish, Cyclically Bullish

Tactically Bearish, Cyclically Bullish

In today’s Sector Insight report, we take the opportunity to summarize our views on the US equity market return expectations across different investment horizons. And by doing so help clients reconcile our views with the other BCA publications. Currently, US Equity Strategy is cyclically (6 to 12 months investment horizon) bullish on the prospects of the broad equity market. The reasons for that are numerous: Pent up demand does not show signs of waning, supply chain bottlenecks are yet to be resolved, and stimulus checks and excess savings are yet to be spend. All of the above is to contribute to robust earnings growth which we expect to surprise on the upside, just like during Q1-2021 earnings season. Looking ahead we do not anticipate a recession but only a modest slowdown in a current fast pace of economic growth. This business cycle bull market rally has not run its course. Having said that, we believe that in the near term the market is ripe for a correction. It is fully valued, if not outright expensive: nearly 50% of all industries have PEs ranking in top 10 percentile of their ten-year history. There is simply not much valuation cushion left to absorb any negative shocks. More specifically, there are two major risks that can serve as a catalyst for a selloff: 1) Fed may surprise the market with hawkish rhetoric if jobs data exceeds expectations or inflation exhibits a staying power; 2) China growth deceleration surprises further on the downside. And these are just the known risks. Further, we are mindful of the SPX risk/reward profile over the next 3-6 months. The market expects EPS NTM of $196 and if we assume an optimistic 22x forward P/E multiple, this equates to SPX target of 4,312 over the next 3-6 months. This is a 3% upside from the current level of 4200. Deploying new capital at these levels of valuations and with a limited upside is like picking up pennies in front of a steamroller. Our recommendation is to raise dry powder by taking profits from some of the recent winners like industrials and basic materials, and redeploying capital during the next market pullback which would provide a more favorable risk/return profile. Bottom Line: We remain cyclically bullish on the prospects of the broad equity market, but are keeping our guard up in the near-term.

Highlights Political and corporate climate activism will increase the cost of developing the resources required to produce and deliver energy going forward – e.g., oil and gas wells; pipelines; copper mines, and refineries. Over the short run, the fastest way for investor-owned companies (IOCs) to address accelerated reductions in CO2 emissions imposed by courts and boards is to walk away from the assets producing them, which could be disruptive over the medium term. Longer term, state-owned companies (SOCs) not facing the constraints of IOCs likely will be required to provide an increasing share of the resources needed to produce and distribute energy. The real difficulty will come in the medium term. Capex for critical metals like copper languishes, just as the call on these metals steadily increases over the next 30 years (Chart of the Week). The evolution to a low-carbon future has not been thought through at the global policy level. A real strategy must address underinvestment in base metals and incentivize the development of technology via a carbon tax – not emissions trading schemes – so firms can innovate to avoid it. We remain long energy and metals exposures.1 Feature And you may ask yourself, "Well … how did I get here?" David Byrne, Once In A Lifetime Energy markets – broadly defined – are radically transforming from week to week. The latest iteration of these markets' evolution is catalyzed by climate activists, who are finding increasing success in court and on corporate boards – sometimes backed by major institutional investors – and forcing oil and gas producers to accelerate CO2 emission-reduction programs.2 Climate activists' arguments are finding increasing purchase because they have merit: Years of stiff-arming investors seeking clarity on the oil and gas producers' decarbonization agendas, coupled with a pronounced failure to provide returns in excess of their cost of capital, have given activists all of the ammo needed to argue their points. Chart of the WeekCall On Metals For Energy Will Increase

A Perfect Energy Storm On The Way

A Perfect Energy Storm On The Way

This activism is not limited to the courts or boardrooms. Voters in democratic societies with contested elections also are seeking redress for failures of their governments to effectively channel mineral wealth back into society on an equitable basis, and to protect their environments and the habitats of indigenous populations. This voter activism is especially apparent in Chile and Peru, where elections and constitutional conventions likely will result in higher taxes and royalties on metals IOCs operating in these states, which will increase production costs and ultimately be passed on to consumers.3 These states account for ~ 40% of world copper output. IOCs Walk Away Earlier this week, Exxon walked away from an early-stage offshore oil development project in Ghana.4 This followed the unfavorable court rulings and boardroom setbacks experienced by Royal Dutch Shell, Chevron and Exxon recently (referenced in fn. 2). While the company had no comment on its abrupt departure, its action shows how IOCs can exercise their option to put a project back to its host government, thus illustrating one of the most readily available alternatives for energy IOCs to meet court- or board-mandated CO2 emissions targets. If these investments qualify as write-offs, the burden will be borne by taxpayers. As climate activism increases, state-owned companies (SOCs) not facing the constraints of IOCs likely will be required to provide an increasing share of the resources – particularly oil and gas – needed to produce and distribute energy going forward. This is not an unalloyed benefit, as the SOCs still face stranded-asset risks, if they invest in longer-lived assets that are obviated by a successful renewables + grid buildout globally. That is a cost that will have to be compensated, when the SOCs work up their capex allocations. Still, if legal and investor activism significantly accelerates IOCs' capex reductions in oil and gas projects, the SOCs – particularly those in OPEC 2.0 – will be able to expand their position as the dominant supplier in the global oil market, and could perhaps increase their influence on price levels and forward-curve dynamics (Chart 2).5 Chart 2OPEC 2.0s Could Expand If Investor Activism Increases

OPEC 2.0s Could Expand If Investor Activism Increases

OPEC 2.0s Could Expand If Investor Activism Increases

Higher Call On Metals At present, there is a lot of talk about the need to invest in renewable electricity generation and the grid structure supporting it, but very little in the way of planning for this transition. Other than repeated assertions of its necessity, little is being said regarding how exactly this strategy will be executed given the magnitude of the supply increase in metals required. Nowhere is this more apparent than in the refined copper market, which has been in a physical deficit – i.e., production minus consumption is negative – for the last 6 years (Chart 3). Physical copper markets in China, which consumes more than 50% of refined output, remain extremely tight, as can be seen in the ongoing weakness of treating charges and refining charges (TC/RC) for the past year (Chart 4). These charges are inversely correlated to prices – when TC/RCs are low, it means there is surplus refining capacity for copper – unrefined metal is scarce, which drives down demand for these services. Chart 3Coppers Physical Deficit Likely Persist

Coppers Physical Deficit Likely Persist

Coppers Physical Deficit Likely Persist

Chart 4Chinas Refined Copper Supply Remains Tight

Chinas Refined Copper Supply Remains Tight

Chinas Refined Copper Supply Remains Tight

Theoretically, high prices will incentivize higher levels of production. However, after the last decade’s ill-timed investment in new mine discoveries and expansions, mining companies have become more wary with their investments, and are using earnings to pay dividends and reduce debt. This leads us to believe that mining companies will not invest in new mine discoveries but will use capital expenditure to expand brownfield projects to meet rising demand. In the last decade, as copper demand rose, capex for copper rose from 2010-2012, and fell from 2013-2016 (Chart 5). During this time, the copper ore grade was on a declining trend. This implies that the new copper brought online was being mined from lower-grade ore, due to the expansion of existing projects(Chart 6). Chart 5Copper Capex Growth Remains Weak

A Perfect Energy Storm On The Way

A Perfect Energy Storm On The Way

Chart 6Copper Ore-Quality Declines Persist Through Capex Cycle

A Perfect Energy Storm On The Way

A Perfect Energy Storm On The Way

Capex directed at keeping ore production above consumption will not be sufficient to avoid major depletions of ore supplies beginning in 2024, according to Wood Mackenzie. The consultancy foresees a cumulative deficit of ~ 16mm MT by 2040. Plugging this gap will require $325-$500 billion of investment in the copper mining sector.6 The Case For A Carbon Tax The low-carbon future remains something of a will-o'-the-wisp – seen off in the future but not really developed in the present. Most striking in discussions of the low-carbon transition is the assumption of resource availability – particularly bases metals –in, e.g., the IEA's Net Zero by 2050, A Roadmap for the Global Energy Sector, published last month. In the IEA's document, further investment in hydrocarbons is not required beyond 2025. The copper, aluminum, steel, etc., required to build the generation and supporting grid infrastructure will be available and callable as needed to build all the renewable generation the world requires. The document is agnostic between carbon trading and carbon taxes as a way to price carbon and incentivize the technology that would allow firms and households to avoid a direct cost on carbon. A real strategy must address the fact that most of the world will continue to rely on fossil fuels for decades, as development goals are pursued. Underinvestment in base metals and its implications for the buildout of generation and grids has to be a priority if these assets are to be built. Given the 5-10-year lead times base metals mines require to come online, it is obvious that beyond the middle of this decade, the physical reality of demand exceeding supply will assert itself. A good start would be a global effort to impose and collect carbon taxes uniformly across states.7 This would need to be augmented with a carbon club, which restricts admission and trading privileges to those states adopting such a scheme. Harmonizing the multiple emissions trading schemes worldwide will be a decades-long effort that is unlikely to succeed. Such schemes also can be gamed by larger players, producing pricing distortions. A hard and fast tax that is enforced in all of the members of such a carbon club would immediately focus attention on the technology required to avoid paying it – mobilizing capital, innovation and entrepreneurial drive to make it a reality. This would support carbon-capture, use and storage technologies as well, thus extending the life of existing energy resources as the next generation of metals-based resources is built out. In addition, a carbon tax raises revenue for governments, which can be used for a variety of public policies, including reducing other taxes to reduce the overall burden of taxation. Lastly, a tax eliminates the potential for short-term price volatility in the pricing of carbon – as long as households and firms know what confronts them they can plan around it. Tax revenues also can be used to reduce the regressive nature of such levies. Investment Implications The lack of a coherent policy framework that addresses the very real constraints on the transition to a low-carbon economy makes the likelihood of a volatile, years-long evolution foreordained. We believe this will create numerous investment opportunities as underinvestment in hydrocarbons and base metals production predisposes oil, natural gas and base metals prices to move higher in the face of strong and rising demand. We remain long commodity index exposure – the S&P GSCI and GSCI Commodity Dynamic Roll Strategy ETF (COMT), which is optimized to take advantage of the most backwardated commodity forward curves in the index. These positions were up 5.3% and 7.2% since inception on December 7, 2017 and March 12, 2021, respectively, at Tuesday's close. We also remain long the MSCI Global Metals & Mining Producers ETF (PICK), which is up 33.9% since it was put on December 10, 2020. Expecting continued volatility in metals – copper in particular – we will look for opportunities to re-establish positions in COMEX/CME Copper after being stopped out with gains. A trailing stop was elected on our long Dec21 copper position established September 10, 2020, which was closed out with a 48.2% gain on May 21, 2021. Our long calendar 2022 vs short calendar 2023 COMEX copper backwardation trade established April 22, 2021, was closed out on May 20, 2021, leaving us with a return of 305%. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish OPEC 2.0 offered no surprises to markets this week, as it remained committed to returning just over 2mm b/d of production to the market over the May-July period, 70% of which comes from the Kingdom of Saudi Arabia (KSA), according to Platts. While Iran's return to the market is not a given in OPEC 2.0's geometry, we have given better than even odds it will return to the market beginning in 3Q21 and restore most of the 1.4mm b/d not being produced at present to the market over the course of the following year. OPEC itself expects demand to increase 6mm b/d this year, somewhat above our expectation of 5.3mm b/d. Stronger demand could raise Brent prices above our average $63/bbl forecast for this year (Chart 7). Brent was trading above $71/bbl as we went to press. Base Metals: Bullish BHP declared operations at its Escondida and Spence mines were running at normal rates despite a strike by some 200 operations specialists. BHP is employing so-called substitute workers to conduct operation, according to reuters.com, which also reported separate unions at both mines are considering strike actions in the near future. Precious Metals: Bullish The Fed’s reluctance to increase nominal interest rates despite indications of higher inflation will reduce real rates, which will support higher gold prices (Chart 8). We agree with our colleagues at BCA Research's US Bond Strategy that the Fed is waiting for the US labor market to reach levels consistent with its assessment of maximum employment before it makes its initial rate hike in this interest-rate cycle. Subsequent rate changes, however, will be based on realized inflation and inflation expectations. In our opinion, the Fed is following this ultra-accommodative monetary policy approach to break the US liquidity trap, brought about by a rise in precautionary savings due to the pandemic. In addition, we continue to expect USD weakness, which also will support gold and precious metals prices. We remain long gold, expecting prices to clear $2,000/oz this year. Ags/Softs: Neutral Corn prices fell more than 2% Wednesday, following the release of USDA estimates showing 95% of the corn crop was planted by 31 May 2021, well over the 87% five-year average. This was in line with expectations. However, the Department's assessment that 76% of the crop was in good-to-excellent condition exceeded market expectations. Chart 7

By 2023 Brent Trades to $80/bbl

By 2023 Brent Trades to $80/bbl

Chart 8

Gold Prices Going Up

Gold Prices Going Up

Footnotes 1 Please see Trade Tables below. 2 Please see OPEC, Russia seen gaining more power with Shell Dutch ruling and EXCLUSIVE BlackRock backs 3 dissidents to shake up Exxon board -sources published by reuters.com June 1, 2021 and May 25, 2021. 3 Please see Chile's govt in shock loss as voters pick independents to draft constitution published by reuters.com May 17, 2021, and Peru’s elite in panic at prospect of hard-left victory in presidential election published by ft.com June 1, 2021. Peru has seen significant capital flight on the back of these fears. See also Results from Chile’s May 2021 elections published by IHS Markit May 21, 2021 re a higher likelihood of tax increases for the mining sector. The risk of nationalization is de minimis, according to IHS. 4 Please see Exxon walks away from stake in deepwater Ghana block published by worldoil.com June 1, 2021. 5 Please see OPEC 2.0's Production Strategy In Focus, which we published on May 20, 2021, for a recap our how we model OPEC 2.0's strategy. It is available at ces.bcaresearch.com. 6 Please see Will a lack of supply growth come back to bite the copper industry?, published by Wood Mackenzie on March 23, 2021. 7 Please see The Challenges and Prospects for Carbon Pricing in Europe published by the Oxford Institute for Energy Studies last month for a discussion of carbon taxes vs. emissions trading schemes. Investment Views and Themes Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way

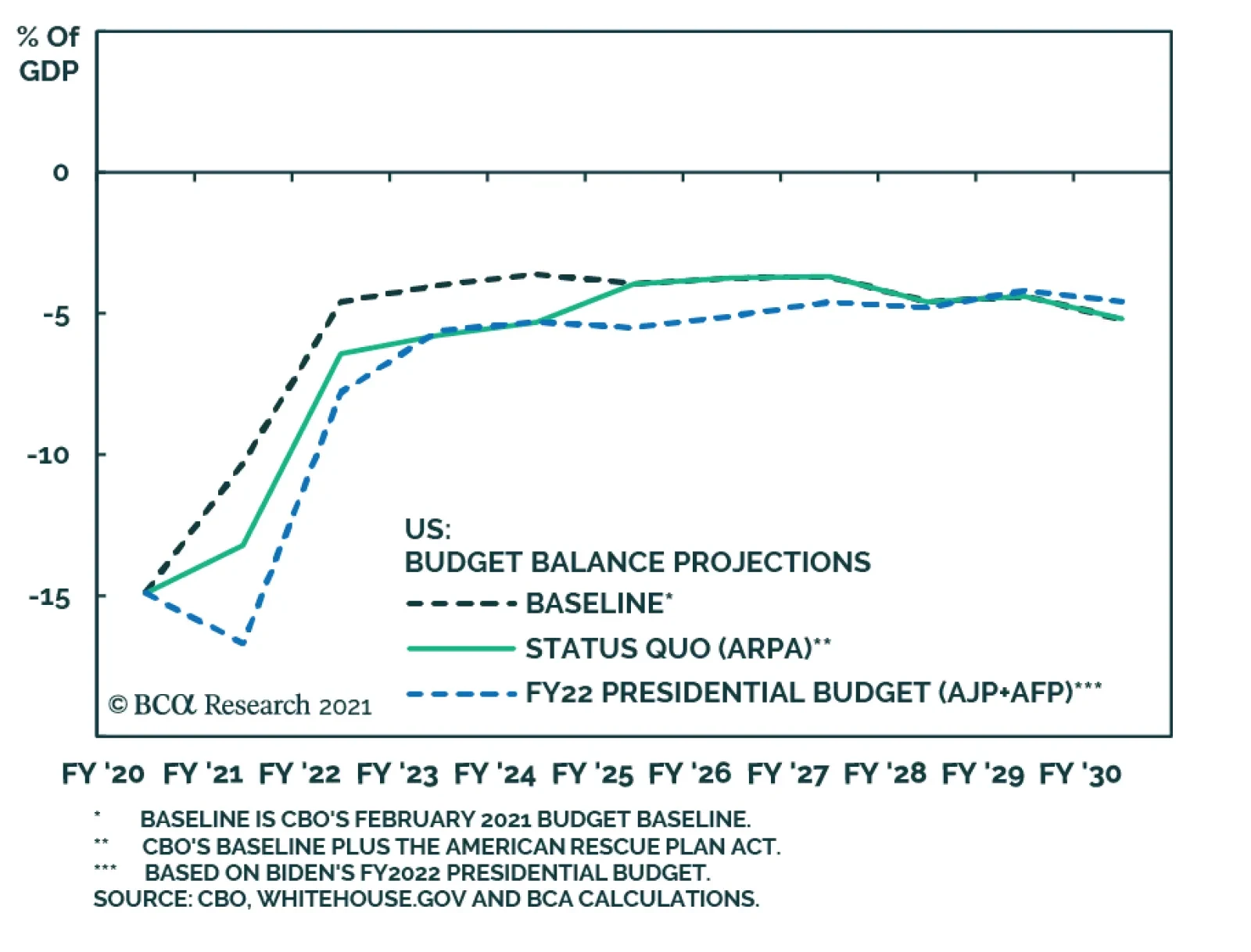

BCA Research’s US Political Strategy service concludes that the looming “fiscal cliff” is probably overrated from an economic point of view even though it may contribute to a pullback in the stock market. The FY2022 presidential budget, which assumes that…

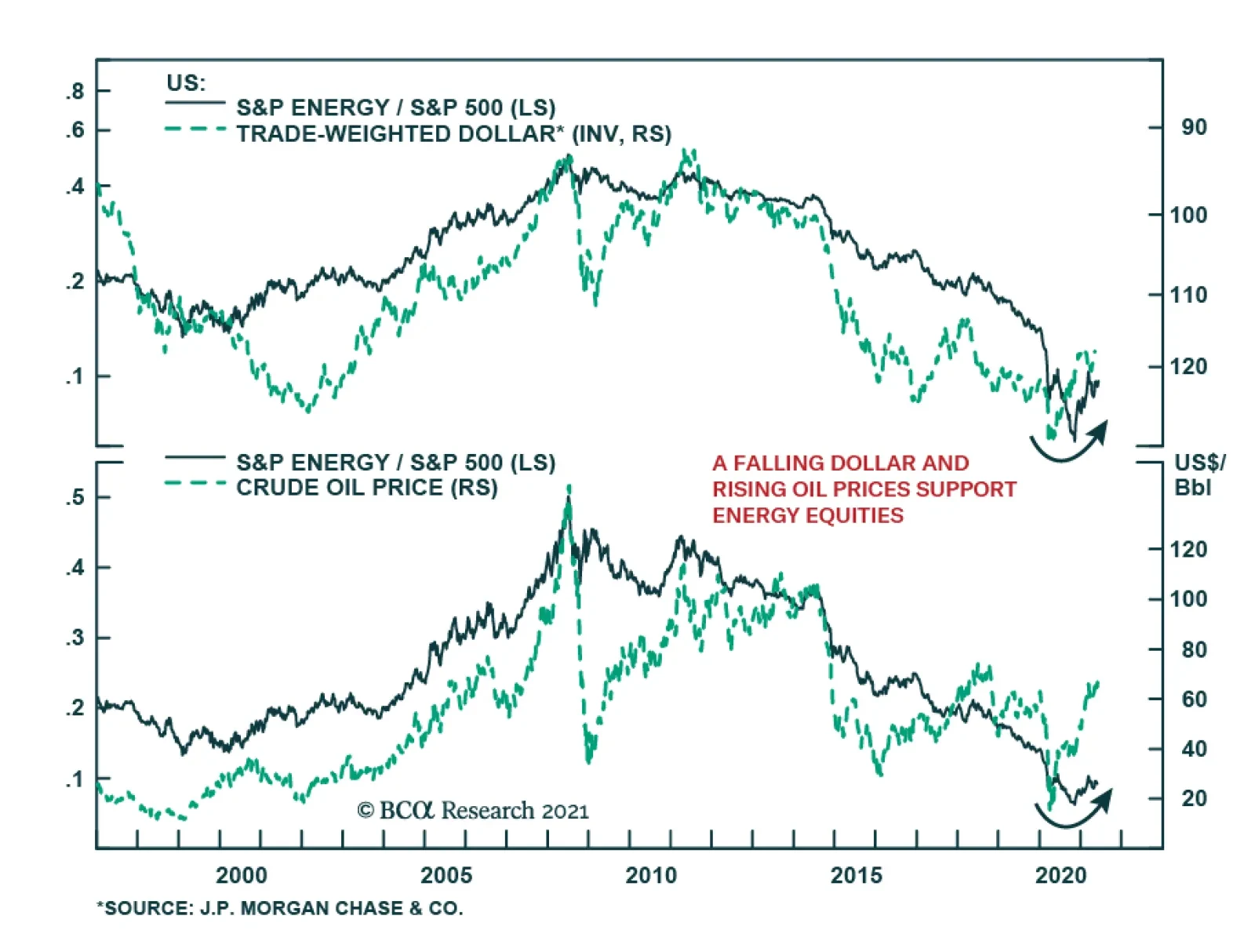

US Energy stocks have been on a tear. The S&P 500 Energy sector is up more than 40% so far this year, outperforming the broad index by roughly 30 percentage points. On Tuesday alone – a generally uneventful day in US equities – energy stocks gained nearly…

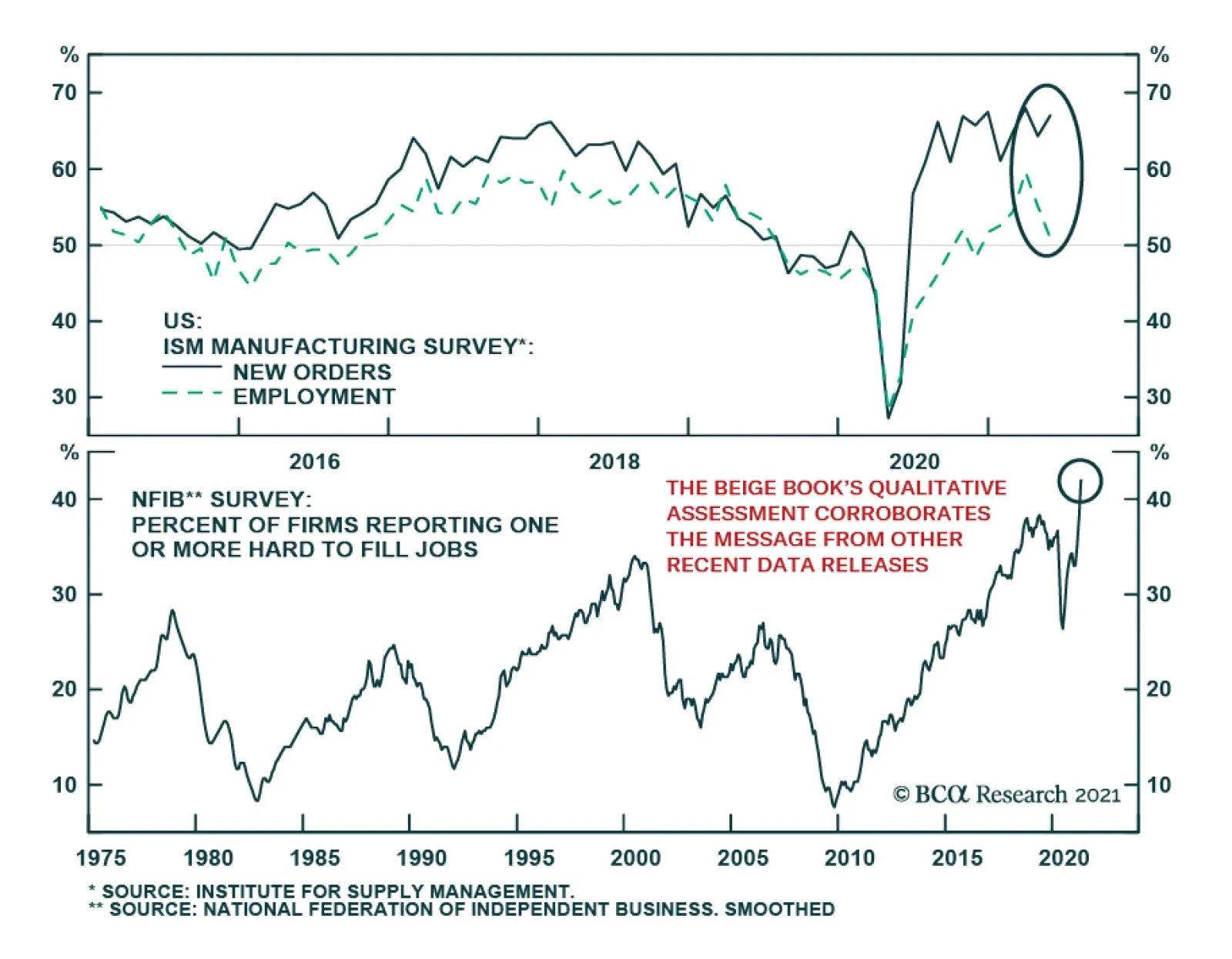

The Federal Reserve’s May Beige Book, released on Wednesday, noted that US economic activity accelerated in the early April to late May period. The reversal of some COVID-19 restrictions was especially beneficial for consumer spending on leisure and…

Highlights President Biden’s FY2022 budget largely confirms consensus views of the economy – which means that it overrates the government’s tax-collecting powers and underrates its fiscal profligacy. The US fiscal thrust will turn negative as the budget deficit contracts in the coming years but the private economic recovery looks robust and positive government spending surprises will mitigate the fiscal cliff. The Biden administration may attempt to pass its capital gains tax hike in the next budget reconciliation bill and make it retroactive to 2021. We doubt this will occur but investors will need to book some profits to be on the safe side. Big Tech still faces a “slow boil” when it comes to government regulation. Stay long materials and infrastructure relative to tech. We were stopped out of our long energy large caps trade. The energy sector is still a beneficiary of a strong macro backdrop for oil and commodities. Close our long municipal bonds trade for a gain of 2%. Feature President Biden’s budget proposal for fiscal 2022 is a confirmation of macro policy trends that the market is well aware of and has already priced. The presidential budget, released on May 27, is a symbolic document. Congress controls the purse strings and congressional dynamics will work out differently from what the White House intends. Still, the budget is significant for highlighting the administration’s big spending preferences and the critical structural theme: the return of Big Government. That is not to say that Biden will fail to overcome various checks and balances with regard to his major legislative priorities, the American Jobs Plan (AJP) and American Families Plan (AFP). Biden’s measurable political capital is still moderate-to-strong. His popular approval remains above 50% and slightly improved in the latest opinion surveys (Chart 1). It should stay above the halfway line as the economy recovers. Chart 1ABiden’s Approval Rating Holding Up

Forget Biden's Budget

Forget Biden's Budget

Chart 1BBiden’s Approval Rating Holding Up

Forget Biden's Budget

Forget Biden's Budget

Consumer confidence improved again in May, on the back of what promises to be a rollicking disease-free summer for households. Political polarization continued to abate in the wake of the contested 2020 election. It may be hitting resistance levels (we expect polarization to remain elevated despite dropping off from Trump-era peaks) but the market implications will only become relevant after Biden’s legislative agenda grinds to a halt following the passage of his second reconciliation bill. Polarization will revive around September with the debt ceiling and the 2022 budget appropriations process and ahead of the 2022 midterm elections, which have a subjective 75% chance of gridlocking Congress. But that time has not yet come and Biden is still capable of signing one or two major bills into law. New data on government spending underscores the big government trend. Fiscal thrust – in this case the unadjusted change in the budget deficit – grew substantially in the first quarter of 2021 relative to the fourth quarter of 2020. It went from 4.6% of GDP in Q4 to 13.1% of GDP in Q1, an increase of 8.5%. The budget deficit will contract in the coming years, a headwind for the economy, but not too dangerous of a headwind as long as the private economy continues to recover, as it should. Real wages are growing at a steady pace, leaping up from a 1.9% growth rate in November to 11.7% in April. What is more notable is the continued decline in consumer loan delinquencies from 1.8% to 1.7% in the first quarter – i.e. flat and marginally declining. It is impressive that the US suffered a recession without considerable consumer or business bankruptcies or delinquencies. When government support ends – when the moratorium on home evictions expires this month and unemployment insurance dries up in September 6 – it will be critical to watch for an increase in distress to determine if the Fed will become more or less inclined to taper asset purchases, the preliminary to raising interest rates. Given that the pandemic caused the recession, and that the pandemic is ebbing on the back of vaccinations, our base case is that the private economy will recover even as government support declines. Most of the good news of the US recovery and government stimulus is priced into the market. Investors will now focus on the Federal Reserve and the passage of Biden’s two big bills. We agree with the BCA House View that the Fed will deliver dovish surprises despite the improving economy as it cannot afford to renege on its new monetary policy strategy but must convince the market that it remains dedicated to an inflation overshoot. Biden’s Budget In A Few Simple Charts Biden’s first presidential budget projects a sea change in US government spending, a “normalization” in US government taxation (reversal of President Trump’s tax cuts), and an economy whose underlying conditions remain the same despite the policy sea change. In reality the economy will respond to the sea change in policy. Real economic growth is projected to slow from 5.2% this calendar year to 4.3% in 2022 and then to settle at around 2% through 2031 (Chart 2). This is in line with forecasts from the Congressional Budget Office and consensus expectations of potential GDP growth. Productivity and labor force growth, which make up potential GDP, are hard to predict. We would note that the Biden administration has drastically cut back on immigration law enforcement. It will be hard to dislodge the Democrats in 2024 given that the economy will be robust and the Republican Party is divided. Therefore immigration policy will not undergo a substantial tightening at least through 2028, though bipartisan immigration reform is possible after 2022 and would marginally tighten inflows. Chart 2Presidential Budget Growth Rate Assumption

Forget Biden's Budget

Forget Biden's Budget

Meanwhile a substantial increase in federal funding for infrastructure, research and development, and STEM education could improve productivity later in the decade, if only on a cyclical rather than structural basis. In other words the administration is not too optimistic regarding growth assumptions even though it assumes higher growth than the Fed or CBO. Inflation is expected to peak at 2.3% in 2025 and continue at that rate throughout the decade (Chart 3). We will not enter into the inflation debate here. Suffice it to say that the risk lies to the upside despite the above points regarding potential growth. Republican voters have abandoned any semblance of fiscal austerity, as signified by President Trump’s success, while the Democrats under Biden are flirting with modern monetary theory. The Fed has adopted a new monetary policy that is aimed at fighting deflationary tail risks at all costs. The budget deficit and trade deficit are ballooning and the US dollar is weakening. The US has fundamentally shifted trade policy, at least with regard to China, which is pushing up input costs. Chinese and global demographics imply a falling ratio of workers to dependents, which implies a secular rise in wages. Chart 3Presidential Budget Inflation Assumption

Forget Biden's Budget

Forget Biden's Budget

In terms of taxing and spending, the presidential budget is overly optimistic about the ability of the federal government to maintain policy orthodoxy. Budgetary receipts are expected to rise on Biden’s tax hikes and the expiration of the Trump tax cuts in 2025. This is exaggerated, since Biden has already said he will accept a corporate tax hike half as large as that in the budget (25% instead of 28%). It is true that finding the votes to extend the Trump tax cuts will be politically difficult and the expiration date arrives at the beginning of a new administration in a non-election year when some fiscal tightening is manageable. But the projection that spending will stay stable at less than 25% of GDP despite Biden’s “Great Society”-style spending is infeasible (Chart 4). Chart 4Presidential Budget Tax-And-Spend Assumptions

Forget Biden's Budget

Forget Biden's Budget

Major spending cuts are far less likely in the foreseeable future than they were back in 2011, when the Budget Control Act was passed. True, Republicans will rediscover their fiscal rectitude in the opposition. But in a social environment of populism and anti-austerity they will either fail to obtain full control of Congress or they will fail to execute deep spending cuts. The party’s political base is now the working class so it will have to rethink cuts to entitlements (mandatory spending), just as it is already rethinking its commitment to corporate tax cuts. Democrats will not cut mandatory or non-defense discretionary spending and will oppose any Republican efforts aggressively (Chart 5). Chart 5Presidential Budget Mandatory Versus Discretionary Spending

Forget Biden's Budget

Forget Biden's Budget

While the presidential budget envisions stable defense spending, the truth is that the one area where Republicans are likely to succeed in influencing fiscal policy substantially lies in defense, which will grow. The US is phasing out its “small wars” and focusing on struggle among the Great Powers. Biden anticipates that defense spending will be flat while non-defense rises sharply but this is unlikely to occur. Regardless of Biden’s specific budget, the US is engaged in the largest government spending since the 1940s and yet there is neither a Great Depression nor a World War II taking place. However, this extravagant peacetime spending looks less extravagant when one considers that there are some historical parallels to the 1930s-40s. There have been two major economic shocks over the past 13 years and there is an emerging cold war with China. The US public has taken a populist turn, the political establishment is determined to provide more largesse to win back the hearts and minds of the people, and the defense and intelligence establishment are well aware of the rising security threats from China and Russia. Federal spending will persistently surprise to the upside while tax hikes could be stymied as early as the 2022 midterm elections. The result is a larger-than-expected budget deficit. The implication for the short-to-medium term is higher inflation and a weaker US dollar. But soaring geopolitical conflict and China’s structural slowdown will eventually put a floor under the dollar. Fiscal Thrust And Budget Deficit Projections Financial markets are already pretty well aware of these trends. The FY2022 presidential budget, which assumes that Biden’s entire legislative agenda passes Congress, does not project a budget deficit that is very different from a back-of-the-envelope “Status Quo” scenario, which assumes that the American Jobs and Families Plans do not pass (Chart 6). Chart 6Presidential Budget Deficit Scenario Alongside Previous Scenarios

Forget Biden's Budget

Forget Biden's Budget

Of course, the AJP, at least, is likely to pass. If a bipartisan deal is struck this week or shortly thereafter then full passage is possible by the end of July. The Democrats would then spend the entire fall legislative session crafting a bill that combines some of the remaining portions of the AJP with the high-priority parts of the AFP into a single budget reconciliation bill that would be likely to pass by Christmas or early 2022. Nevertheless Biden’s budget reveals that there is not much distance in budget deficit projections with regard to the AFP (Chart 7). Even though the price tag of the AFP is huge, at $1.8 trillion, the truth is that it will be watered down in negotiation and it will also be accompanied by at least some tax hikes. Thus the market already has most of the information it needs regarding US budget deficit projections. Everything else depends on events in the private economy and external sector. The good news of the US budget deficit blowout is largely priced. Future upward surprises in the deficit, which we expect, serve to mitigate the contraction in the budget deficit, i.e. to reduce the negative fiscal thrust that drags on the economy as stimulus wanes. In other words the looming “fiscal cliff” is probably overrated from an economic point of view even though it may contribute to a pullback in the stock market. Chart 7Small Difference Between Biden’s Two Plans

Forget Biden's Budget

Forget Biden's Budget

Changes In The Post-Infrastructure Agenda After Biden passes his infrastructure plan (the AJP), whether via bipartisanship or reconciliation, the AFP presents a much tougher political slog in Congress. The revised AFP promises to be a Frankenstein monster of social spending – a new “Alphabet Soup” of government programs including affordable child care, elderly care, universal pre-kindergarten schooling, subsidized community college, and paid leave. It will have to be pared back somewhat to appease moderate Democratic senators. The administration has tried to pitch the new social spending as “human infrastructure,” since infrastructure is more popular than welfare, but while Democrats accept this rhetorical gimmick, a majority of independent voters (along with opposition Republicans) apparently do not (Chart 8). Still the AFP could very well pass before the midterm on the condition that Biden signs the AJP this summer. We stick with our 50/50 odds for now. Chart 8Much Tougher Slog On Social Spending Bill

Forget Biden's Budget

Forget Biden's Budget

The presidential budget introduced a new risk regarding the impending capital gains tax hike: the possibility that it will be enacted retroactively, taking effect in 2021, rather than in 2022 or thereafter as expected. The administration proposes to raise the long-term capital gains rate to 39.6%, which, combined with the Obamacare surtax of 3.8% would result in a 43.4% rate on capital gains for investors making over $1 million. A compromise will be necessary but the top rate could still end up above 32%. If Biden completes a bipartisan infrastructure deal this summer then he is much more likely to get this and other individual tax hikes into the reconciliation bill at the end of this year. Retroactivity is possible but it would be bad politics ahead of the midterm election. Therefore we stick with our view that individual tax hikes will take effect in 2023 if at all. But from a prudential perspective, investors will have to book some gains to prepare for negative tax surprises and that suggests near-term profit taking could weigh on the stock market (Chart 9). Chart 9A Retroactive Capital Gains Tax?

A Retroactive Capital Gains Tax?

A Retroactive Capital Gains Tax?

Since Biden is guaranteed to get a lot of spending through two or three reconciliation bills (one already passed), he will not get much when it comes to regular appropriations. We are more likely to see the GOP refuse to cooperate on budgetary appropriations. This could lead to a debt ceiling crisis and government shutdown at the end of this year or early next year; hence the aforementioned return of polarization. However, these events will play out very differently from 2011-13. The GOP must tread carefully as they are already divided among pro-Trump and anti-Trump factions and will suffer even worse in public support if they induce a shutdown. A government shutdown would not be market negative in an already highly stimulated economy but it could jeopardize Republican odds in 2022, thus marginally increasing the risk of upward surprises in Democrats’ tax-and-spend policies. Congress is also moving forward on a raft of other legislative proposals, highlighted in Table 1. Most of these proposals will fall short of the bipartisan support necessary to get the required 60 votes in the Senate. The most promising bills involve efforts to resurrect US industrial policy, research and development, technological leadership (particularly in semiconductors), supply chain resilience, and domestic manufacturing. Anything that aims to coordinate the two parties in the face of geopolitical competition with China is likely to pass, as we have highlighted in our sister Geopolitical Strategy service. The result, as mentioned above, is likely to be a cyclical uptick in productivity (we will not speculate here on whether the structural downtrend will be broken). Table 1Pending Legislation In Congress Under Biden

Forget Biden's Budget

Forget Biden's Budget

The Slow Boil Of Tech Regulation In a recent report on the Biden administration’s regulatory threat to the tech sector we argued that while popular opinion and government interest were creating a “slow boil” for Big Tech, nevertheless the reflationary macroeconomic backdrop posed a much larger short-term risk. We stand by this view especially in light of recent developments. In particular, legislative priorities, gridlock in all key agencies, slow movement in the Department of Justice’s staffing, an evenly divided Senate, and a recent Supreme Court judgement against the Federal Trade Commission all lend confirmation to our thesis, at least for now. To elaborate: A bipartisan consensus in public opinion holds that Big Tech needs tougher regulation (Chart 10) and this consensus grew substantially over the controversial 2020 political cycle. However, not all surveys show strong majorities in favor of regulation, even if they show strong majorities are skeptical of Big Tech’s influence. And Republicans and Democrats disagree on the aims of regulation, with Republicans averse to “content moderation,” or ideological censorship, and Democrats eager to retain their advantage in political fundraising from Silicon Valley. Any bill requiring 60 votes in the Senate would be an opportunity for Republicans to demand that their speech and press rights be preserved, which would be a poison pill for Democrats. The lack of cooperation on the proposed commission to investigate the January 6 riot at the US Capitol highlights the inability to bridge the ideological gap. Chart 10Bipartisan Consensus On Tech Regulation

Forget Biden's Budget

Forget Biden's Budget

Most of the Democrats’ political capital will be spent on passing the infrastructure bill and the next budget reconciliation bill. There is limited space for other legislation, aside from the strategic competition with China. Minnesota Senator Amy Klobuchar’s anti-trust efforts, including parts of the Competition and Antitrust Enforcement Reform Act, have some chance of passage. She has proposed steps that Republicans can agree on, such as increasing fees on big mergers to fund anti-trust agencies, preventing anti-competitive pricing, and protecting whistleblowers. Her main bill avoids the debate over censorship and arguably preserves the almighty “consumer welfare” standard for determining where harm has occurred and government intervention may be necessary. Republican Senator Mike Lee of Utah has said some positive things about the bill and argues that it would not replace consumer welfare (though not all Republicans will agree and the judicial system will separately defend the consumer welfare standard). Regulatory reform is far more effective when backed by a new legislative overhaul. For example, reform of Section 230 of the Communications Decency Act becomes more difficult without new legislation. Regulation via the executive branch can be important but requires focus from the president and a strong consensus in key positions in the bureaucracy. Democrats must confirm two nominations to the Federal Communications Commission, which is currently deadlocked, in order to achieve a partisan majority and make headway on policy priorities (Table 2). Cybersecurity, net neutrality, and overseeing broadband internet expansion will compete with any regulatory probes into Big Tech. The Senate will also have to confirm two nominations for the Federal Trade Commission, which is also deadlocked at the moment (Table 3). One of these, for anti-trust scholar Lina Khan, a critic of Big Tech, is in process. Yet the FTC has possibly lost some of its bite after a Supreme Court ruling in April (AMG Capital v. FTC) determined that the agency cannot seek monetary relief under one of its most frequently used legal authorities (Section 13b of the Federal Trade Commmission Act). The FTC will thus lose some ability to impose penalties, particularly in consumer protection cases. Facebook is already attempting to use this ruling to dismiss the FTC’s case against it, which could result in a forced sale of popular subsidiaries WhatsApp and Instagram. Table 2Balance Of Power On The FCC

Forget Biden's Budget

Forget Biden's Budget

Table 3Balance Of Power On The FTC

Forget Biden's Budget

Forget Biden's Budget

As for the Department of Justice, while Biden’s appointments have all been confirmed, the anti-trust division is bogged down by ethics concerns since several officials would have to recuse themselves in cases against Big Tech due to their previous work representing plaintiffs against Big Tech. The bottom line is that Big Tech is in the hot seat after the various controversies of the pandemic and 2016-2020 elections, just as Big Banks faced tougher regulation in the wake of the subprime mortgage crisis. Both public and government willingness to prosecute and regulate Big Tech have gone up, creating a permanently higher level of regulatory risk. Yet government focus and capability are lacking in the short run. Investment Takeaways Most of the major reflation trades have taken a pause in recent weeks, as expected. The stock-to-bond ratio has stalled, the cyclicals to defensives ratio has peaked twice, and TIPS have lost momentum relative to duration-matched nominal treasuries. The big five tech firms’ shares have tentatively arrested their fall relative to the other 495 companies on the S&P500. It is not clear if they will break down further but the above analysis suggests that they will. We are sticking with our long materials / short tech trade (Chart 11). Chart 11Long Materials Versus Technology

Long Materials Versus Technology

Long Materials Versus Technology

Investors should stay invested, maintain pro-cyclical trades, favor value stocks relative to growth stocks, but avoid taking on large new risks in the current environment. The post-vaccine rally has lost steam but the overall macro backdrop remains favorable as the global economy recovers. We are closing our long municipal bonds trade for a gain of 2.3%. Our large cap energy trade has stopped out at -5% with small caps outperforming in the face of regulatory and ESG headwinds for the supermajors. Biden’s regulatory risk to energy small caps has been outweighed by the macro context but will become relevant at some point. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Jesse Anak Kuri Associate Editor jesse.Kuri@bcaresearch.com Appendix Table A1USPS Trade Table

Forget Biden's Budget

Forget Biden's Budget

Table A2Political Risk Matrix

Forget Biden's Budget

Forget Biden's Budget

Table A3Political Capital Index

Forget Biden's Budget

Forget Biden's Budget

Table A4APolitical Capital: White House And Congress

Forget Biden's Budget

Forget Biden's Budget

Table A4BPolitical Capital: Household And Business Sentiment

Forget Biden's Budget

Forget Biden's Budget

Table A4CPolitical Capital: The Economy And Markets

Forget Biden's Budget

Forget Biden's Budget

In yesterday’s Special Report, we initiated a long S&P oil & gas exploration & production / short S&P metals & mining market neutral trade as a way to capitalize on the China/DM growth differential on a 6 to 12-month time horizon. This trade is also a way to express our view that crude oil will likely outperform copper going forward. While we outlined the demand side of the story in the Special Report, today we touch on relative supply dynamics. Ultimately, supply of crude oil and copper is dictated by how much companies invest in capex. It allows them to dig up more commodities in the future, thus increasing supply and lowering commodity prices. The chart below illustrates this relationship for copper and crude producers and highlights that on a relative basis, copper producers’ capex meaningfully outpaced the one of oil producers (relative capex shown inverted). In short, that means that not only relative demand dynamics are a major headwind for the copper/crude oil price ratio, but the supply side of the story will also be a drag. Bottom Line: We reiterate our newly established long S&P oil & gas exploration & production / short S&P metals & mining pair trade. For more details on the rationale behind the trade, please refer to yesterday’s Special Report.

More Reasons To Like Our New Intra-commodity Pair Trade

More Reasons To Like Our New Intra-commodity Pair Trade

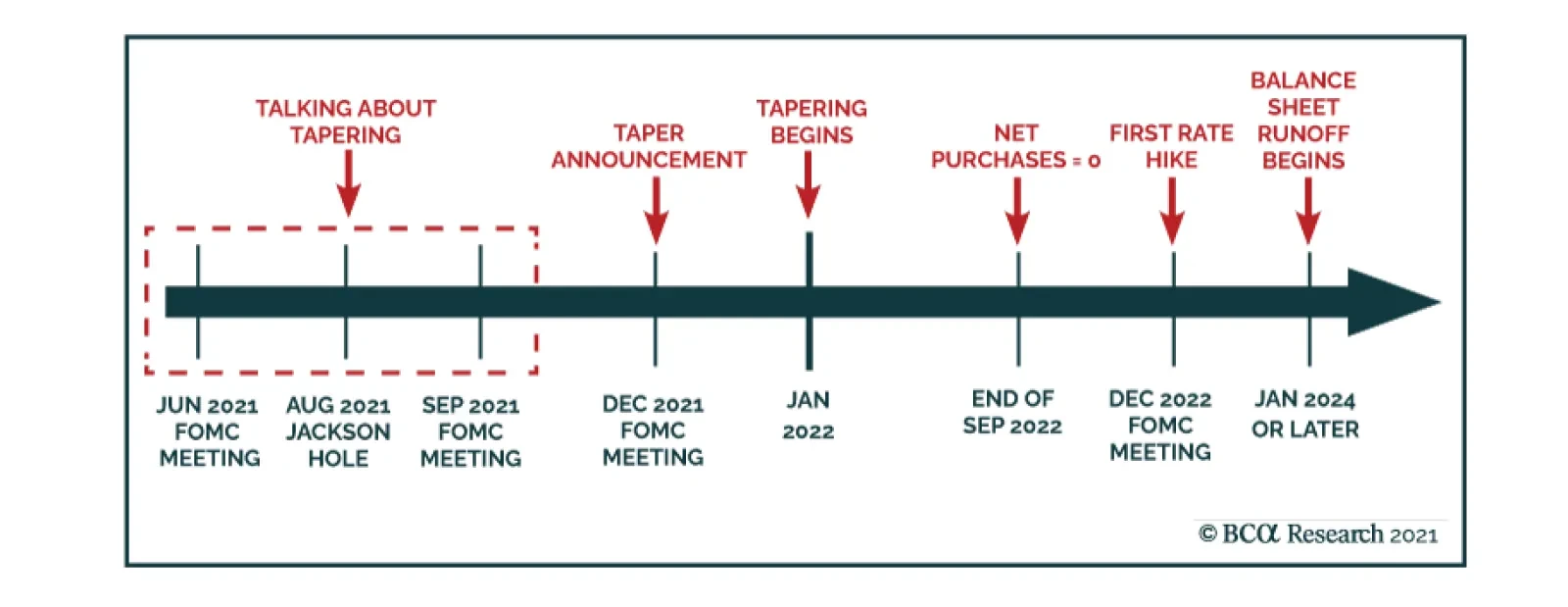

BCA Research’s Global Fixed Income Strategy and US Bond Strategy services conclude that investors should maintain below-benchmark portfolio duration in US fixed income portfolios. According to their anticipated timeline for when the Federal…