United States

Highlights President Biden has called for the US intelligence community to investigate the origins of COVID-19 and one of Biden’s top diplomats has stated the obvious: the era of “engagement” with China is over. This clinches our long-held view that any Democratic president would be a hawk like President Trump. The US-China conflict – and global geopolitical risk – will revive and undermine global risk appetite. China faces a confluence of geopolitical and macroeconomic challenges, suggesting that its equity underperformance will continue. Domestic Chinese investors should stay long government bonds. Foreign investors should sell into the bond rally to reduce exposure to any future sanctions. The impending agreement of a global minimum corporate tax rate has limited concrete implications that are not already known but it symbolizes the return of Big Government in the western world. Our updated GeoRisk Indicators are available in the Appendix, as well as our monthly geopolitical calendar. Feature In our quarterly webcast, “Geopolitics And Bull Markets,” we argued that geopolitical themes matter to investors when they have a demonstrable relationship with the macroeconomic backdrop. When geopolitics and macro are synchronized, a simple yet powerful investment thesis can be discerned. The US war on terror, Russia’s resurgence, the EU debt crisis, and Brexit each provided cases in which a geopolitically informed macro view was both accessible and actionable at an early stage. Investors generally did well if they sold the relevant country’s currency and disfavored its equities on a relative basis. Chart 1China's Decade Of Troubles

China's Decade Of Troubles

China's Decade Of Troubles

Of course, the market takeaway is not always so clear. When geopolitics and macroeconomics are desynchronized, the trick is to determine which framework will prevail over the financial markets and for how long. Sometimes the market moves to its own rhythm. The goal is not to trade on geopolitics but rather to invest with geopolitics. One of our key views for this year – headwinds for China – is an example of synchronization. Two weeks ago we discussed China’s macroeconomic challenge. In this report we discuss China’s foreign policy challenge: geopolitical pressure from the US and its allies. In particular we address President Biden’s call for a deeper intelligence dive into the origins of COVID-19. The takeaway is negative for China’s currency and risk assets. The Great Recession dealt a painful blow to the Chinese version of the East Asian economic miracle. By 2015, China’s financial turmoil and currency devaluation should have convinced even bullish investors to keep their distance from Chinese stocks and the renminbi. If investors stuck with this bearish view despite the post-2016 rally, on fear of trade war, they were rewarded in 2018-19. Only with China’s containment of COVID-19 and large economic stimulus in 2020 has CNY-USD threatened to break out (Chart 1). We expect the renminbi to weaken anew, especially once the Fed begins to taper asset purchases. Our cyclical view is still bullish but US-China relations are unstable so we remain tactically defensive. Forget Biden’s China Review, He’s A Hawk Chinese financial markets face a host of challenges this year, despite the positive factors for China’s manufacturing sector amid the global recovery. At home these challenges consist of a structural economic slowdown, a withdrawal of policy stimulus, bearish sentiment among households, and an ongoing government crackdown on systemic risk. Abroad the Democratic Party’s return to power in Washington means that the US will bring more allies to bear in its attempt to curb China’s rise. This combination of factors presents a headwind for Chinese equities and a tailwind for government bonds (Chart 2). This is true at least until the government should hit its pain threshold and re-stimulate. Chart 2Global Investors Still Wary

Global Investors Still Wary

Global Investors Still Wary

New stimulus may not occur in 2022. The Communist Party’s leadership rotation merely requires economic stability, not rapid growth. While the central government has a record of stimulating when its pain threshold is hit, even under the economically hawkish President Xi Jinping, a financial market riot is usually part of this threshold. This implies near-term downside, particularly for global commodities and metals, which are also facing a Chinese regulatory backlash to deter speculation. In this context, President Biden’s call for a deeper US intelligence investigation into the origin of COVID-19 is an important confirming signal of the US’s hawkish turn toward China. Biden gave 90 days for the intelligence community to report back to him. We will not enter into the debate about COVID-19’s origins. From a geopolitical point of view it is a moot point. The facts of the virus origin may never be established. According to Biden’s statement, at least one US intelligence agency believes the “lab leak theory” is the most likely source of the virus (while two other agencies decided in favor of animal-to-human transmission). Meanwhile Chinese government spokespeople continue to push the theory that the virus originated at the US’s Fort Detrick in Maryland or at a US-affiliated global research center. What is certain is that the first major outbreak of a highly contagious disease occurred in Wuhan. Both sides are demanding greater transparency and will reject each other’s claims based on a lack of transparency. If the US intelligence report concludes that COVID originated from the Wuhan Institute of Virology, the Chinese government and media will reject the report. If the report exonerates the Wuhan laboratory, at least half of the US public will disbelieve it and it will not deter Biden from drawing a hard line on more macro-relevant policy disputes with China. The US’s hawkish bipartisan consensus on China took shape before COVID. Biden’s decision to order the fresh report introduces skepticism regarding the World Health Organization’s narrative, which was until now the mainstream media’s narrative. Previously this skepticism was ghettoized in US public discourse: indeed, until Biden’s announcement on May 26, the social media company Facebook suppressed claims that the virus came from a lab accident or human failure. Thus Biden’s action will ensure that a large swathe of the American public will always tend to support this theory regardless of the next report’s findings. At the same time Biden discontinued a State Department effort to prove the lab leak theory, which shows that it is not a foregone conclusion what his administration will decide. The good news is that even if the report concluded in favor of the lab leak, the Biden administration would remain highly unlikely to demand that China pay “reparations,” like the Trump administration demanded in 2020. This demand, if actualized, would be explosive. The bad news is that a future nationalist administration could conceivably use the investigation as a basis to demand reparations. Nationalism is a force to be reckoned with in both countries and the dispute over COVID’s origin will exacerbate it. Traditionally the presidents of both countries would tamp down nationalism or attempt to keep it harnessed. But in the post-Xi, post-Trump era it is harder to control. The death toll of COVID-19 will be a permanent source of popular grievance around the world and a wedge between the US and China (Chart 3). China’s international image suffered dramatically in 2020. So far in 2021 China has not regained any diplomatic ground. Chart 3Death Toll Of COVID-19

Biden Confirmed As A China Hawk (GeoRisk Update)

Biden Confirmed As A China Hawk (GeoRisk Update)

The US is repairing its image via a return to multilateralism while the Europeans have put their Comprehensive Agreement on Investment with China on hold due to a spat over sanctions arising from western accusations of genocide (a subject on which China pointedly answered that it did not need to be lectured by Europeans). Notably Biden’s Department of State also endorsed its predecessor’s accusation of genocide in Xinjiang. Any authoritative US intelligence review that solidifies doubts about the WHO’s initial investigation – even if it should not affirm the lab leak theory – would give Biden more ammunition in global opinion to form a democratic alliance to pressure China (for example, in Europe). An important factor that enables the US to remain hawkish on China is fiscal stimulus. While stimulus helps bring about economic recovery, it also lowers the bar to political confrontation (Chart 4). Countries with supercharged domestic demand do not have as much to fear from punitive trade measures. The Biden administration has not taken new punitive measures against China but it is clearly not worried about Chinese retaliation. Chart 4Large Fiscal Stimulus Lowers The Bar To Geopolitical Conflict

Biden Confirmed As A China Hawk (GeoRisk Update)

Biden Confirmed As A China Hawk (GeoRisk Update)

China’s stimulus is underrated in this chart (which excludes non-fiscal measures) but it is still true that China’s policy has been somewhat restrained and it will need to stimulate its economy again in response to any new punitive measures or any global loss of confidence. At least China is limited in its ability to tighten policy due to the threat of US pressure and western trade protectionism. Simultaneous with Biden’s announcement on COVID-19, his administration’s coordinator for Indo-Pacific affairs, Kurt Campbell, proclaimed in a speech that the era of “engagement” with China is officially over and the new paradigm is one of “competition.” By now Campbell is stating the obvious. But this tone is a change both from his tone while serving in President Obama’s Department of State and from his article in Foreign Affairs last year (when he was basically auditioning for his current role in the Biden administration).1 Campbell even said in his latest remarks that the Trump administration was right about the “direction” of China policy (though not the “execution”), which is candid. Campbell was speaking at Stanford University but his comments were obviously aimed for broader consumption. Investors no longer need to wait for the outcome of the Biden administration’s comprehensive review of policy toward China. The answer is known: the Biden administration’s hawkishness is confirmed. The Department of Defense report on China policy, due in June, is very unlikely to strike a more dovish posture than the president’s health policy. Now investors must worry about how rapidly tensions will escalate and put a drag on global sentiment. Bottom Line: US-China relations are unstable and pose an immediate threat to global risk appetite. The fundamental geopolitical assessment of US-China relations has been confirmed yet again. The US is seeking to constrain China’s rise because China is the only country capable of rivaling the US for supremacy in Asia and the world. Meanwhile China is rejecting liberalization in favor of economic self-sufficiency and maintaining an offensive foreign policy as it is wary of US containment and interference. Presidents Biden and Xi Jinping are still capable of stabilizing relations in the medium term but they are unlikely to substantially de-escalate tensions. And at the moment tensions are escalating. China’s Reaction: The Example Of Australia How will China respond to Biden’s new inquiry into COVID’s origins? Obviously Beijing will react negatively but we would not expect anything concrete to occur until the result of the inquiry is released in 90 days. China will be more constrained in its response to the US than it has been with Australia, which called for an international inquiry early last year, as the US is a superior power. Australia was the first to ban Chinese telecom company Huawei from its 5G network (back in 2018) and it was the first to call for a COVID probe. Relations between China and Australia have deteriorated steadily since then, but macro trends have clearly driven the Aussie dollar. The AUD-JPY exchange rate is a good measure for global risk appetite and it is wavering in recent weeks (Chart 5). Chart 5Australian Dollar Follows Macro Trends, Rallies Amid China Trade Spat

Australian Dollar Follows Macro Trends, Rallies Amid China Trade Spat

Australian Dollar Follows Macro Trends, Rallies Amid China Trade Spat

Tensions have also escalated due to China’s dependency on Australian commodity exports at a time of spiking commodity prices. This is a recurring theme going back to the Stern Hu affair. The COVID spat led China to impose a series of sanctions against Australian beef, barley, wine, and coal. But because China cannot replace Australian resources (at least, not in the short term), its punitive measures are limited. It faces rising producer prices as a result of its trade restrictions (Chart 6). This dependency is a bigger problem for China today than it was in previous cycles so China will try to diversify. Chart 6Constraints On China's Tarrifs On Australia

Constraints On China's Tarrifs On Australia

Constraints On China's Tarrifs On Australia

By contrast, China is not likely to impose sanctions on the US in response to Biden’s investigation, unless Biden attacks first. China’s imports from the US are booming and its currency is appreciating sharply. Despite Beijing’s efforts to keep the Phase One trade deal from collapsing, Biden is maintaining Trump’s tariffs and the US-China trade divorce is proceeding (Chart 7). Bilateral tariff rates are still 16-17 percentage points higher than they were in 2018, with US tariffs on China at 19% (versus 3% on the rest of the world) while Chinese tariffs on the US stand at 21% (versus 6% on the rest of the world). The Biden administration timed this week’s hawkish statements to coincide with the first meeting of US trade negotiators with China, which was a more civil affair. Both countries acknowledged that the relationship is important and trade needs to be continued. However, US Trade Representative Katherine Tai’s comments were not overly optimistic (she told Reuters that the relationship is “very, very challenging”). She has also been explicit about maintaining policy continuity with the Trump administration. We highly doubt that China’s share of US imports will ever surpass its pre-Trump peaks. The Biden administration has also refrained so far from loosening export controls on high-tech trade with China. This has caused a bull market in Taiwan while causing problems for Chinese semiconductor stocks’ relative performance (Chart 8). If Biden’s policy review does not lead to any relaxation of export controls on commercial items then it will mark a further escalation in tensions. Chart 7US Tarrifs Reduce China In Trade Deficit

US Tarrifs Reduce China In Trade Deficit

US Tarrifs Reduce China In Trade Deficit

Bottom Line: Until Presidents Biden and Xi stabilize relations at the top, the trade negotiations over implementing the Phase One trade deal – and any new Phase Two talks – cannot bring major positive surprises for financial markets. Chart 8US Export Controls Amid Chip Shortage

US Export Controls Amid Chip Shortage

US Export Controls Amid Chip Shortage

Congress Is More Hawkish Than Biden Biden’s ability to reduce frictions with China, should he seek to, will also be limited by Congress and public opinion. With the US deeply politically divided, and polarization at historically high levels, China has emerged as one of the few areas of agreement. The hawkish consensus is symbolized by new legislation such as the Strategic Competition Act, which is making its way through the Senate rapidly. Congress is also trying to boost US competitiveness through bills such as the Endless Frontier Act. These bills would subject China to scrutiny and potential punitive measures over a broad range of issues but most of all they would ignite US industrial policy , STEM education, and R&D, and diversify the US’s supply chains. We would highlight three key points with regard to the global impact of this legislation: Global supply chains are shifting regardless: This trend is fairly well established in tech, defense, and pharmaceuticals. It will continue unless we see a major policy reversal from China to try to court western powers and reduce frictions. The EU and India are less enthusiastic than the US and Australia about removing China from supply chains but they are not opposed. The EU Commission has recommended new defensive economic measures that cover supply chains in batteries, cloud services, hydrogen energy, pharmaceuticals, materials, and semiconductors. As mentioned, the EU is also hesitating to ratify the Comprehensive Agreement on Investment with China. Hence the EU is moving in the US’s direction independently of proposed US laws. After all, China’s rise up the tech value chain (and its decision to stop cutting back the size of its manufacturing sector) ultimately threatens the EU’s comparative advantage. The EU is also aligned with the US on democratic values and network security. India has taken a harder stance on China than usual, which marks an important break with the past. India’s decision to exclude Huawei from its 5G network is not final but it is likely to be at least partially implemented. A working group of democracies is forming regardless. The Strategic Competition Act calls for the creation of a working group of democracies but the truth is that this is already happening through more effective forums like the G7 and bilateral summits. Just as the implementation of the act would will ultimately depend on President Biden, so the willingness of other countries to adopt the recommendations of the working group would depend on their own executives. Allies have leeway as Biden will not use punitive measures against them: Any policy change from the EU, UK, India, and Australia will be independent of the US Congress passing the Strategic Competition Act. These countries will be self-directed. The US would have to devote diplomatic energy to maintaining a sustained effort by these states to counter China in the face of economic costs. This will be limited by the fact that the Biden administration will be very reluctant to impose punitive measures on allies to insist on their cooperation. The allies will set the pace of pressure on China rather than the United States. This gives the EU an important position, particularly Germany. And yet the trends in Germany suggest that the government will be more hawkish on China after the federal elections in September. Bottom Line: The Biden administration is unlikely to use punitive measures against allies so new US laws are less important than overall US diplomacy with each of the allies. Some allies will be less compliant with US policies given their need for trade with China. But so far there appears to be a common position taking shape even with the EU that is prejudicial to China’s involvement in key sectors of emerging technologies. If China does not respond by reducing its foreign policy assertiveness, then China’s economic growth will suffer. That drag would have to be offset by new supply chain construction in Southeast Asia and other countries. Investment Takeaways The foregoing highlights the international risks facing China even at a time when its trend growth is slowing (Chart 9) and its ongoing struggle with domestic financial imbalances is intensifying. China’s debt-service costs have risen sharply and Beijing is putting pressure on corporations and local governments to straighten out their finances (Chart 10), resulting in a wave of defaults. This backdrop is worrisome for investors until policymakers reassure them that government support will continue. Chart 9China's Growth Potential Slowing

China's Growth Potential Slowing

China's Growth Potential Slowing

Chart 10China's Leaders Struggle With Debt

China's Leaders Struggle With Debt

China's Leaders Struggle With Debt

China’s domestic stability is a key indicator of whether geopolitical risks could spiral out of control. In particular we think aggressive action in the Taiwan Strait is likely to be delayed as long as the Chinese economy and regime are stable. China has rattled sabers over the strait this year in a warning to the United States not to cross its red line (Chart 11). It is not yet clear how Biden’s policy continuity with the Trump administration will affect cross-strait stability. We see no basis yet for changing our view that there is a 60% chance of a market-negative geopolitical incident in 2021-22 and a 5% chance of full-scale war in the short run. Chart 11China PLA Flights Over Taiwan Strait

Biden Confirmed As A China Hawk (GeoRisk Update)

Biden Confirmed As A China Hawk (GeoRisk Update)

Putting all of the above together, we see substantial support for two key market-relevant geopolitical risks: Chinese domestic politics (including policy tightening) and persistent US-China tensions (including but not limited to the Taiwan Strait). We remain tactically defensive, a stance supported by several recent turns in global markets: The global stock-to-bond ratio has rolled over. China is a negative factor for global risk appetite (Chart 12). Global cyclical equities are no longer outperforming defensives. There is a stark divergence between Chinese cyclicals and global cyclicals stemming from the painful transition in China’s bloated industrial economy (Chart 13). Global large caps are catching a bid relative to small caps (Chart 14). Chart 12Global Stock-To-Bond Ratio Rolled Over

Global Stock-To-Bond Ratio Rolled Over

Global Stock-To-Bond Ratio Rolled Over

Chart 13Global Cyclicals-To-Defensives Pause

Biden Confirmed As A China Hawk (GeoRisk Update)

Biden Confirmed As A China Hawk (GeoRisk Update)

Chart 14Global Large Caps Catch A Bid Versus Small Caps

Global Large Caps Catch A Bid Versus Small Caps

Global Large Caps Catch A Bid Versus Small Caps

Cyclically the global economic recovery should continue as the pandemic wanes. China will eventually relax policy to prevent too abrupt of a slowdown. Therefore our strategic portfolio reflects our high-conviction view that the current global economic expansion will continue even as it faces hurdles from the secular rise in geopolitical risk, especially US-China cold war. Measurable geopolitical risk and policy uncertainty are likely to rebound sooner rather than later, with a negative impact on high-beta risk assets. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Coda: Global Minimum Tax Symbolizes Return Of Big Government On Thursday, the US Treasury Department released a proposal to set the global minimum corporate tax rate at 15%. The plan is to stop what Treasury Secretary Janet Yellen has referred to as a global “race to the bottom” and create the basis for a rehabilitation of government budgets damaged by pandemic-era stimulus. Although the newly proposed 15% rate is significantly below President Biden’s bid to raise the US Global Intangible Low-Taxed Income (GILTI) rate to 21% from 10.5%, it is the same rate as his proposed minimum tax on corporate book income. Biden is also raising the headline corporate tax rate from 21% to around 25% (or at highest 28%). Negotiators at the OECD were initially discussing a 12.5% global minimum rate. The finance ministers of both France and Germany – where the corporate income tax rates are 32.0% and 29.9%, respectively – both responded positively to the announcement. However, Ireland, which uses low corporate taxes as an economic development strategy, is obviously more comfortable with a minimum closer to its own 12.5% rate. Discussions are likely to occur when G7 finance ministers meet on June 4-5. Countries are hoping to establish a broad outline for the proposal by the G20 meeting in early July. It is highly likely that the OECD will come to an agreement. However, it is not a truly “global” minimum as there will still be tax havens. Compliance and enforcement will vary across countries. A close look at the domestic political capital of the relevant countries shows that while many countries have the raw parliamentary majorities necessary to raise taxes, most countries have substantial conservative contingents capable of preventing stiff corporate tax hikes (Table 1, in the Appendix). Our Geopolitical strategists highlight that the Biden administration’s compromise on the minimum rate reflects its pragmatism as well as emphasis on multilateralism. Any global deal will be non-binding but the two most important low-tax players are already committed to raising corporate rates well above this level: Biden’s plan is noted above, while the UK’s budget for March includes a jump in the business rate to 25% in April 2023 from the current 19%. Ireland and Hungary are the only outliers but they may eventually be forced to yield to such a large coalition of bigger economies (Chart 15). Chart 15Global Minimum Corporate Tax Impact Is Symbolic Rather Than Concrete

Biden Confirmed As A China Hawk (GeoRisk Update)

Biden Confirmed As A China Hawk (GeoRisk Update)

Thus a nominal minimum corporate tax rate is likely to be forged but it will not be truly global and it will not change the corporate rate for most countries. The reality of what companies pay will also depend on loopholes, tax havens, and the effective tax rate. Bottom Line: On a structural horizon, the global minimum corporate tax is significant for showing a paradigm shift in global macro policy: western governments are starting to raise taxes and revenue after decades of cutting taxes. The experiment with limited government has ended and Big Government is making a comeback. On a cyclical horizon, the US concession on global minimum tax is that the Biden administration aims to be pragmatic and “get things done.” Biden is also working with Republicans to pass bills covering some bipartisan aspects of his domestic agenda, such as trade, manufacturing, and China. The takeaway from a global point of view is that Biden may prove to be a compromiser rather than an ideologue, unlike his predecessors. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Roukaya Ibrahim Vice President Daily Insights RoukayaI@bcaresearch.com Footnotes 1 Kurt M. Campbell and Jake Sullivan, "Competition Without Catastrophe," Foreign Affairs, September/October 2019, foreignaffairs.com. Section II: Appendix Table 1OECD: Which Countries Are Willing And Able To Raise Corporate Tax Rates?

Biden Confirmed As A China Hawk (GeoRisk Update)

Biden Confirmed As A China Hawk (GeoRisk Update)

GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan – Province Of China

Taiwan-Province of China: GeoRisk Indicator

Taiwan-Province of China: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Australia

Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

Section III: Geopolitical Calendar

On the surface, the April US Durable Goods Report is a disappointment. The headline number declined by 1.3% m/m following a revised 1.3% m/m rise in durable goods orders in March, missing expectations of 0.8% m/m rise. April’s decline is the first monthly…

Underweight As a follow up to yesterday’s Sector Insight report where we reiterated our S&P financials downgrade, today we cover banks that were used as the vehicle to trim financials to a neutral allocation. Housing starts and permits came off the boil last week and failed to live up to economists’ upbeat expectations. Lumber is getting clobbered and entered a bear market having first surged to five standard deviations above its five decade mean. Moreover, the latest news from the University of Michigan survey of consumers’ sentiment on buying conditions for houses made for grim reading signaling that a key bank loan category, mortgage credit, is in for a rough summer/fall season (top panel). Tack on the nosedive in mortgage applications for purchasing a new home courtesy of rising mortgage rates, albeit from a low base, and factors are falling into place for a housing-catalyzed underperformance phase in banks (bottom panel). Bottom Line: This week we trimmed the S&P banks index to underweight. The ticker symbols for the stocks in this index are: BLBG: S5BANKX – JPM, BAC, C, WFC, USB, PNC, TFC, FRC, FITB, SIVB, KEY, MTB, RF, CFG, HBAN, CMA, ZION, PBCT. For more details, please refer to this Tuesday's Strategy Report.

Shy Away From Banks

Shy Away From Banks

Over the past several weeks, the S&P 500 has failed to break above its May 7 all-time high. This stagnation is consistent with indications that the rally was vulnerable to some profit taking. Inflationary fears highlighted by various data releases,…

US bond yields have fallen somewhat in recent days. The 10-year Treasury yield is back below 1.6%, well off its early-April peak of 1.73%. Falling bond yields are difficult to square with all the talk of spiking inflation, but a broader look…

Neutral

Time For A 20% Cash-in

Time For A 20% Cash-in

In this Tuesday’s Strategy Report we closed our overweight financials call and moved this GICS1 sector to neutral from previously overweight capitalizing 20% in relative gains, since last November’s inception. This move is a hedge to our rising inflation view, and we would rather stick to overweighting energy and industrials as ways to express our inflation protection theme as opposed to maintaining an above benchmark allocation in financials. There are some warning signs for the sector as well. The Fed’s easing cycle has reached a zenith and, at the margin, this will weigh on relative financials profitability (bottom panel). The shadow fed funds rate (courtesy of Leo Krippner1) has also troughed and is closing in on the zero line (middle panel). Finally, using the 10-year/shadow fed funds rate yield curve also signals that the yield curve may have peaked already, at least for this early part of the business cycle (top panel). Bottom Line: We downgraded the S&P financials sector to neutral in yesterday’s Strategy Report and pocketed gains to the tune of 20%, since inception. Footnotes 1https://www.ljkmfa.com/test-test/international-ssrs/

Recent US housing market data suggest that rising home prices are denting demand for properties: Home prices are surging. The S&P CoreLogic Case-Shiller National Home Price Index jumped 13.2% y/y in March from 12.0% y/y in February. Similarly, the…

BCA Research’s US Bond Strategy service continues to favor spread product over Treasuries. 5-year/5-year forward TIPS breakeven inflation rates in a range between 2.3% and 2.5% are a reason to turn more cautious on spread product, and the recent rise in…

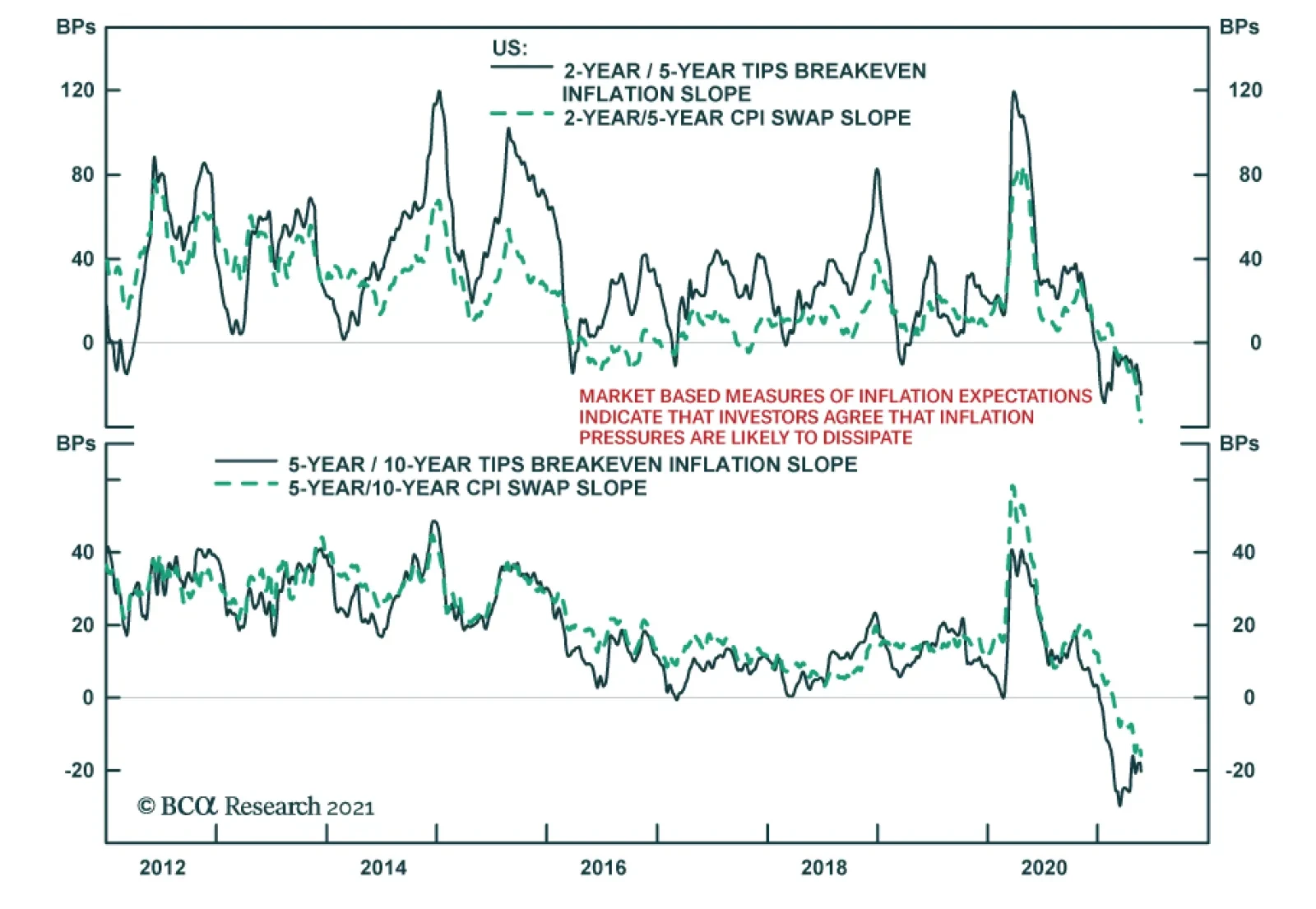

Expectations inform behavior. If a widespread belief that troublesome inflation is going to return takes hold, individual workers and unions will demand higher wages to maintain their purchasing power, businesses up and down the supply chain will insist on…

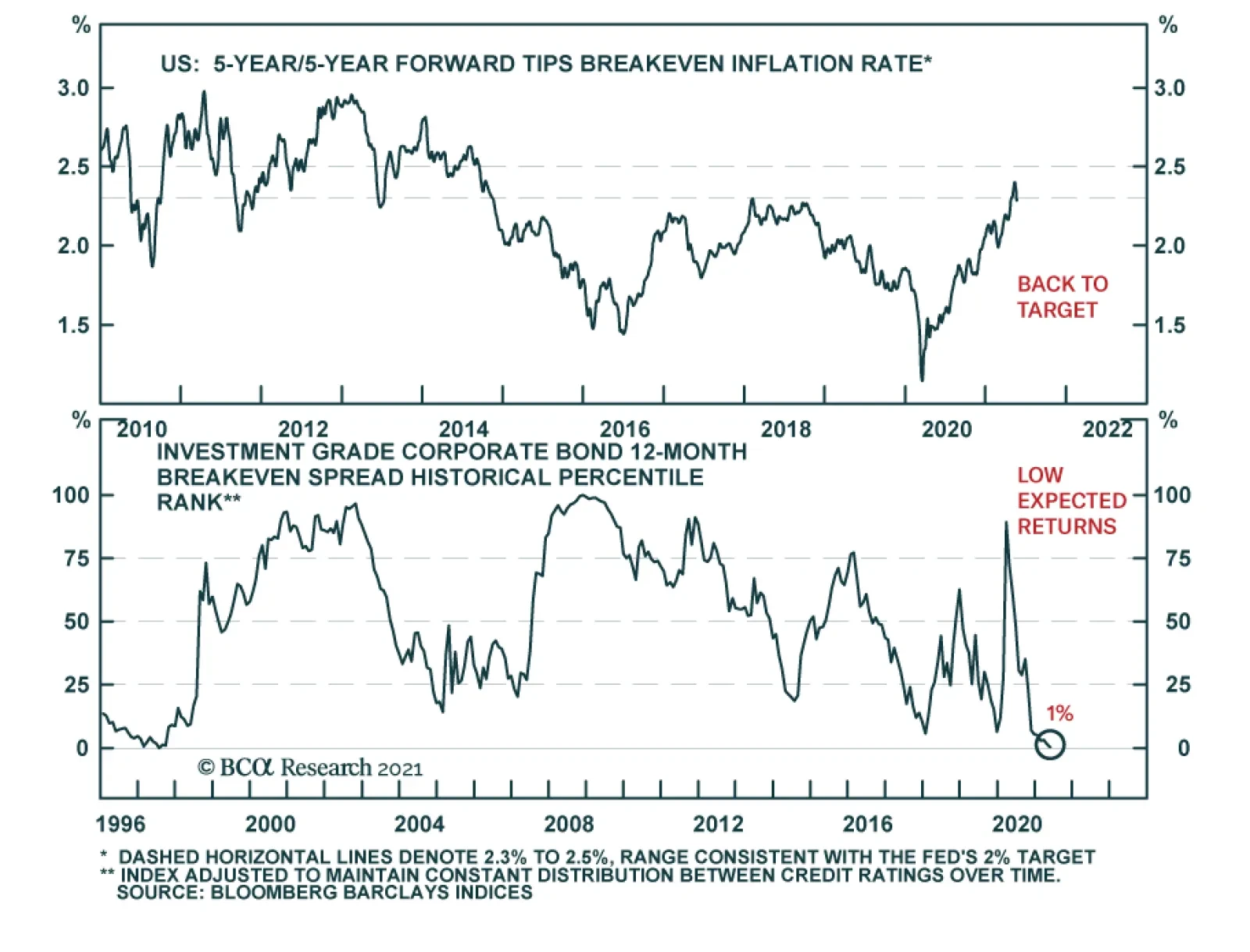

Highlights Monetary Policy: The Fed will not immediately change its policy stance in response to rising inflation and inflation expectations. Rather, it will follow its current forward guidance and only lift rates off zero once the labor market has reached “maximum employment”. However, once the first rate hike has occurred, the Fed will shift its focus toward inflation and inflation expectations. Duration: The overnight index swap curve is priced for a total of 77 bps of rate hikes by the end of 2023. We see strong odds that more hikes will be delivered and therefore continue to recommend a below-benchmark portfolio duration stance. Corporate Bonds: High and rising inflation expectations will eventually pose a risk to credit spreads, but only once the Fed tightens policy in response. For now, we remain overweight spread product versus Treasuries, though we maintain a preference for high-yield corporates, USD-denominated EM Sovereigns and municipal bonds over investment grade corporate bonds. Feature Recent inflationary trends are making the Fed’s job more difficult. Not only was April’s increase in core CPI the largest since 1981, but measures of long-term inflation expectations have also jumped. The 5-year/5-year TIPS breakeven inflation rate has quickly risen to levels that are consistent with the Fed’s 2% inflation target (Chart 1). What’s more, survey measures of inflation expectations have also moved up, in many cases to uncomfortably high levels (Chart 2). Chart 1Back To Target

Back To Target

Back To Target

Chart 2Inflation Expectations Have Jumped

Inflation Expectations Have Jumped

Inflation Expectations Have Jumped

All of this makes the Fed’s zero-lower-bound interest rate policy look increasingly untenable. Can the Fed really just sit on the sidelines as inflation and inflation expectations rise to above-target levels? Our expectation is that the Fed will ignore rising inflation until the labor market is fully recovered, but it may then need to move quickly to contain inflationary pressures. The result could very well be a rate hike cycle that takes a long time to start, but then proceeds at a rapid pace. The Fed’s Liftoff Criteria Are Different Than Its Criteria For Pace A crucial point about the Fed’s forward guidance is that the criteria that will determine the timing of the first rate hike are different than the criteria that will determine the post-liftoff pace of rate hikes. Liftoff Criteria Table 1A Checklist For Liftoff

Lower For Longer, Then Faster Than You Think

Lower For Longer, Then Faster Than You Think

For liftoff, the Fed has been very explicit that three conditions must be met before it will raise rates off the zero bound (Table 1). Of the three conditions listed in Table 1, the timing of when the labor market will reach “maximum employment” is the most uncertain. We have written extensively about how the Fed defines “maximum employment” and about the pace of employment growth that’s necessary to achieve that goal by specific future dates.1 To summarize, we calculate that average monthly nonfarm payroll growth of at least 698k is required to reach “maximum employment” by the end of this year and average monthly payroll growth of at least 412k is required to hit that target by the end of 2022 (Chart 3). Chart 3Employment Growth

Employment Growth

Employment Growth

Chart 4Labor Demand Is Strong

Labor Demand Is Strong

Labor Demand Is Strong

Our assessment is that “maximum employment” will be achieved in time for the Fed to lift rates in 2022, largely because employment growth must rise quickly in order to catch up with skyrocketing indicators of labor demand (Chart 4). The risk, of course, is that inflation continues to run hot as the Fed waits for its “maximum employment” condition to be met. If this occurs, we believe that the Fed will stick to its current forward guidance. It will ignore rising inflation until its liftoff criteria are met. Only then, will Fed policy turn toward containing inflation. Pace Criteria In a recent speech, Fed Vice-Chair Richard Clarida laid out three indicators that he will track to guide the pace of policy tightening post Fed liftoff.2 First, he pointed to inflation expectations. In particular, the Fed’s index of Common Inflation Expectations (CIE):3 Other things being equal, my desired pace of policy normalization post-liftoff to return inflation to 2 percent […] would be somewhat slower than otherwise if the CIE index is, at time of liftoff, below the pre-ELB level. [ELB = effective lower bound]. Chart 2 shows that the CIE index has already broken above its 2018 peak. It stands to reason that, all else equal, an elevated CIE index would speed up the post-liftoff pace of rate hikes. Chart 5Inflation Since August 2020

Inflation Since August 2020

Inflation Since August 2020

Second, Clarida noted that: Another factor I will consider in calibrating the pace of policy normalization post-liftoff is the average rate of PCE inflation since the new framework was adopted in August 2020. The annualized rate of change in core PCE since August 2020 is almost at the Fed’s 2% target already, and it will certainly rise to above-target levels when the April data are released, as was the case with core CPI (Chart 5). Finally, Clarida offered up a detailed Taylor-type monetary policy rule that he says he will consult once the conditions for liftoff are met: Consistent with our new framework, the relevant policy rule benchmark I will consult once the conditions for liftoff have been met is an inertial Taylor-type rule with a coefficient of zero on the unemployment gap, a coefficient of 1.5 on the gap between core PCE inflation and the 2 percent longer-run goal, and a neutral real policy rate equal to my SEP forecast of long-run r*. Chart 6Balanced Approach (Shortfalls) Rule* Recommendations

Lower For Longer, Then Faster Than You Think

Lower For Longer, Then Faster Than You Think

Chart 6 shows the results of a very similar policy rule using median FOMC estimates for r*, NAIRU and the path of inflation. We use a slightly more pessimistic forecast for the unemployment rate and assume that it reaches 4.5% by the end of 2022 and 4% by the end of 2023. Even with those conservative assumptions, the rule still recommends a policy rate of 1.5% by the end of 2022 and 2.65% by the end of 2023. This is not to say that the Fed will immediately lift rates to those levels once it is ready to hike, only that the Fed will have a strong incentive to pursue a rapid pace of rate hikes once it finally lifts rates off the zero bound. Investment Implications For investors, the bottom line is that the Fed will not immediately change its policy stance in response to rising inflation and inflation expectations. Rather, it will follow its current forward guidance and only lift rates off zero once the labor market has reached “maximum employment”. However, once the first rate hike has occurred, the Fed will shift its focus toward inflation and inflation expectations. If inflation and inflation expectations rise further, or even remain sticky near current levels, the Fed will lift rates more quickly than many anticipate. At present, the overnight index swap curve is priced for a total of 77 bps of rate hikes by the end of 2023. We see strong odds that more hikes will be delivered and therefore continue to recommend a below-benchmark portfolio duration stance. Is Inflation A Risk For Spread Product? Yes it is, but not just yet. In past reports, we’ve often pointed to 5-year/5-year forward TIPS breakeven inflation rates in a range between 2.3% and 2.5% as a reason to turn more cautious on spread product (see Chart 1), and the recent rise in inflation expectations certainly does set off some alarm bells. High inflation expectations pose a risk to credit spreads because of what they signal about the future course of Fed policy. If the Fed responds to high inflation expectations by tightening policy into restrictive territory, then economic growth and credit spreads are at risk. All this remains true, but the Fed’s willingness to ignore rising inflation expectations – at least until “maximum employment” and fed funds liftoff are achieved – gives spread product a little more runway than usual. One way to illustrate this dynamic is with the slope of the yield curve (Chart 7). Historically, corporate bond (both investment grade and junk) excess returns are strong at least until the 3-year/10-year Treasury slope flattens to below 50 bps (Table 2). Currently, the 3-year/10-year Treasury slope is well above 100 bps and has shown few signs of rolling over. If the Fed was still following its old forward-looking policy framework, then the yield curve would likely be much flatter today. That is, the curve would be pricing-in some policy tightening in response to high and rising inflation expectations. However, as discussed above, inflation expectations are not currently the Fed’s primary concern and they will only become the Fed’s primary concern once “maximum employment” has been achieved and the funds rate has been lifted off the zero bound. Chart 7Spread Product Returns Are Strong When The Curve Is Steep

Spread Product Returns Are Strong When The Curve Is Steep

Spread Product Returns Are Strong When The Curve Is Steep

Table 2Corporate Bond Performance In Different Phases Of The Cycle

Lower For Longer, Then Faster Than You Think

Lower For Longer, Then Faster Than You Think

All in all, we are concerned that, if inflation expectations remain elevated, the Fed may quickly ramp up its post-liftoff pace of rate hikes, sending credit spreads wider. But we are reluctant to position for that outcome when we are still many months away from Fed liftoff and the slope of the yield curve remains so steep. Chart 8Low Expected Returns In IG

Low Expected Returns in IG

Low Expected Returns in IG

Another factor to consider is that value in spread product is extremely tight. In fact, our measure of the 12-month breakeven spread for the quality-adjusted investment grade corporate bond index is almost at its most expensive level since 1995 (Chart 8). This doesn’t change our assessment of when restrictive Fed policy will cause spreads to widen, but it does reduce our return expectations in the interim. All else equal, since the rewards from being overweight spread product versus Treasuries are low, we will be quicker to reduce our recommended spread product allocation when our indicators start to point toward the end of the credit cycle. Though, at the very least, we will still want to see the 3-year/10-year Treasury slope start to flatten and approach 50 bps before we get too pessimistic on spread product. The bottom line is that high and rising inflation expectations will eventually pose a risk to credit spreads, but only once the Fed tightens policy in response. For now, we remain overweight spread product versus Treasuries, though we maintain a preference for high-yield corporates, USD-denominated EM Sovereigns and municipal bonds over investment grade corporate bonds. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “Overshoot Territory”, dated April 13, 2021. 2 https://www.federalreserve.gov/newsevents/speech/clarida20210113a.htm 3 The CIE is a composite measure of different market-based and survey-based indicators of inflation expectations. https://www.federalreserve.gov/econres/notes/feds-notes/index-of-common-inflation-expectations-20200902.htm Fixed Income Sector Performance Recommended Portfolio Specification