United States

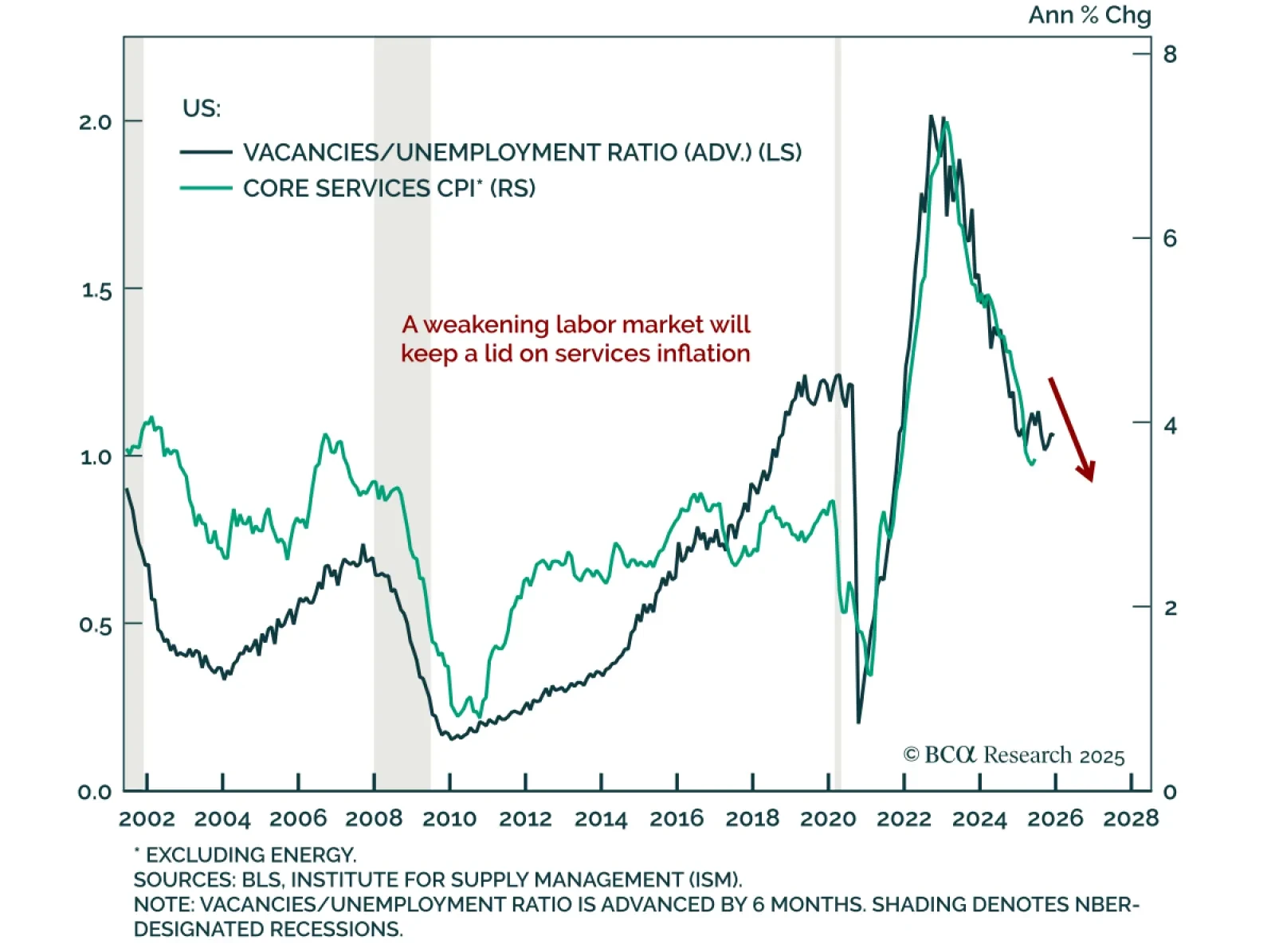

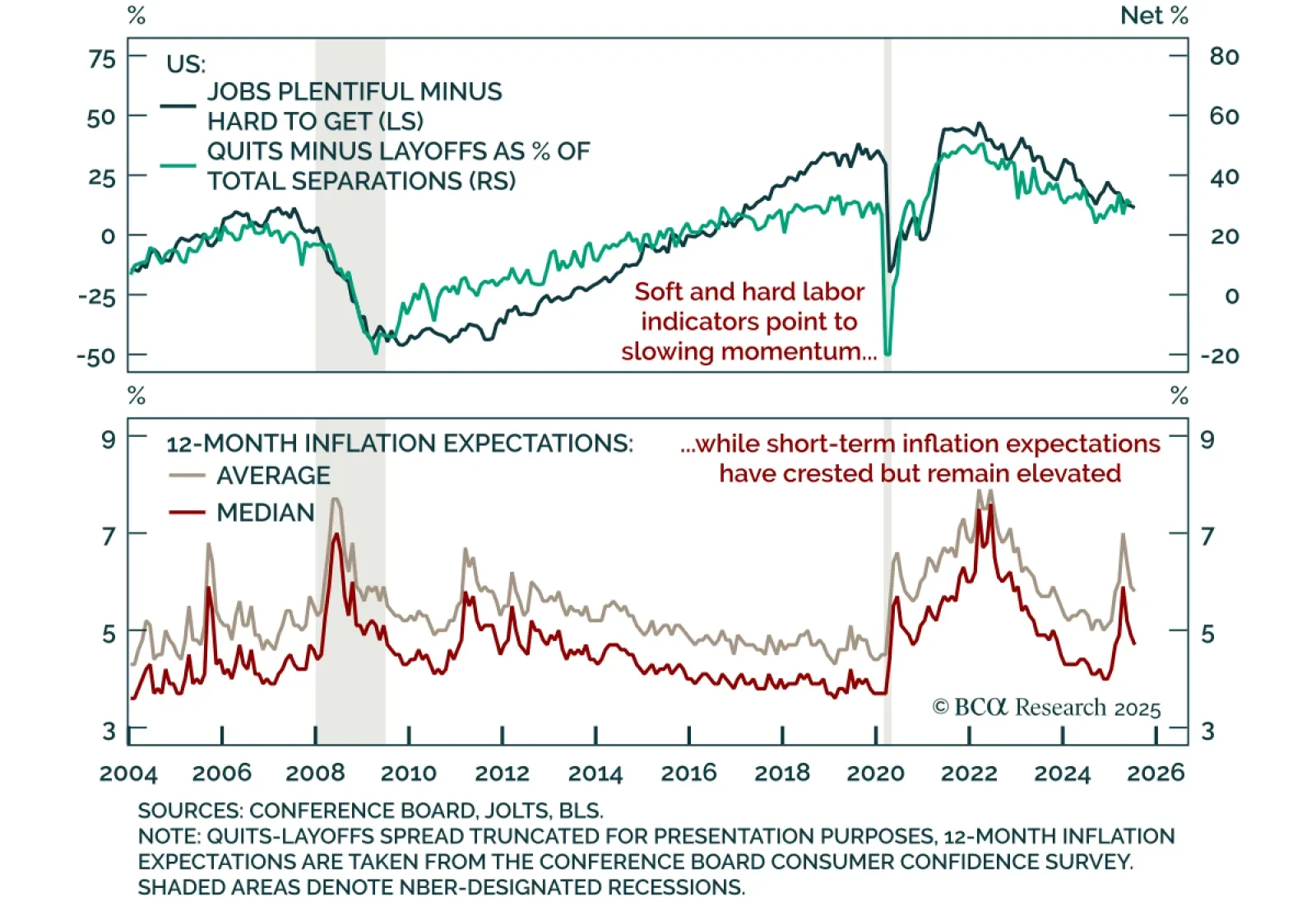

The June JOLTS report showed further weakening in US labor market momentum, reinforcing our overweight duration stance and preference for steepeners. Job openings fell more than expected to 7.4m from a downwardly revised 7.7m, while quits declined to 3.1m and…

The July Conference Board Consumer Confidence report showed improved expectations but weaker current conditions, reinforcing our defensive stance and preference for downside protection. The headline index rose to 97.2 from a revised 95.2 on the back of better…

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

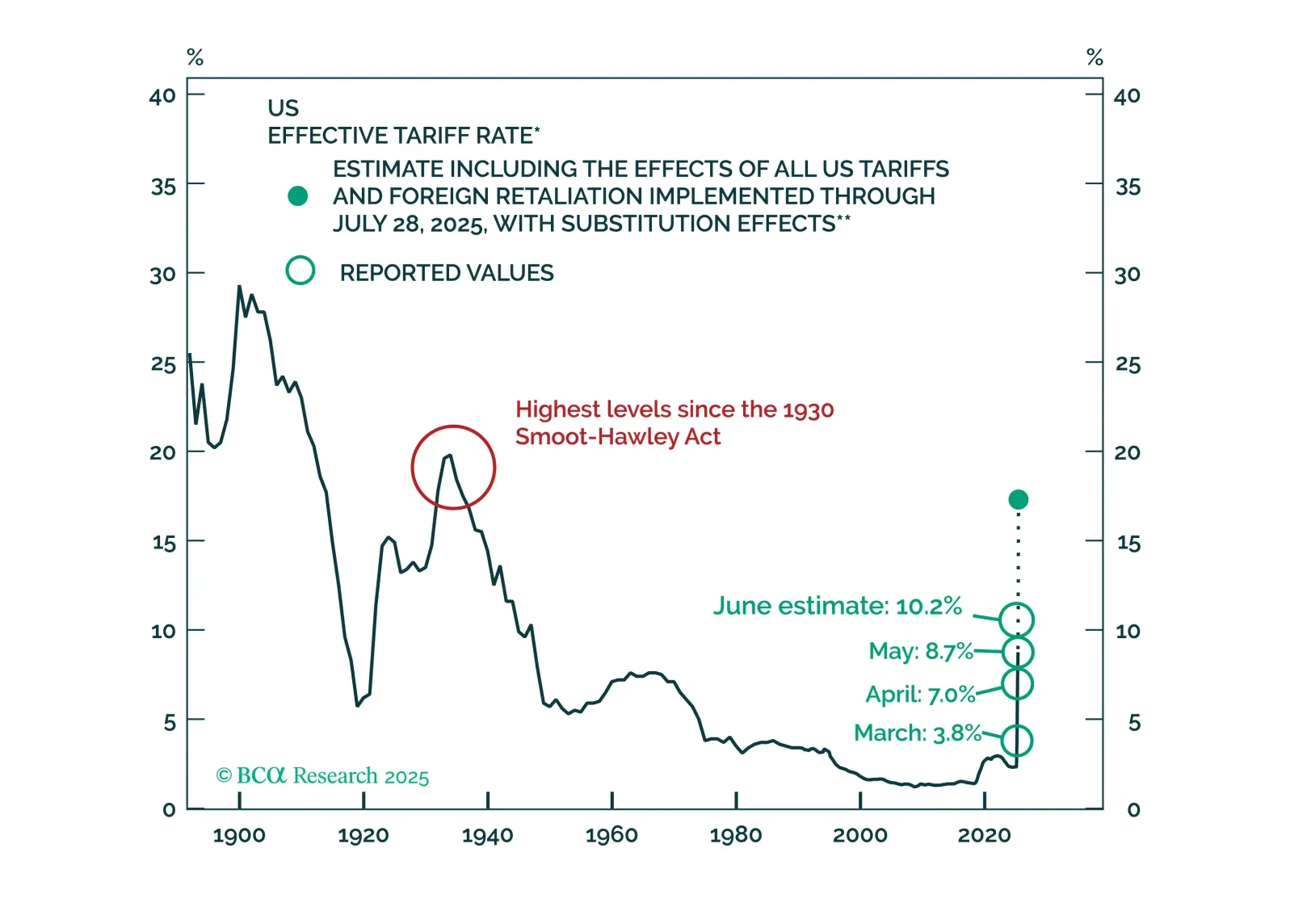

The US-EU trade deal lifts uncertainty but imposes high tariffs, weighing on the EUR and supporting our long USD positioning. The agreement includes a 15% tariff on all EU exports to the US, including cars and potentially, pharmaceutical products,…

The July Dallas Fed survey beat expectations, pointing to a rebound in current activity, but the outlook remains subdued, supporting our modestly defensive asset allocation. The headline index rose to 0.9 from -12.7 in June, with production jumping 20 points…

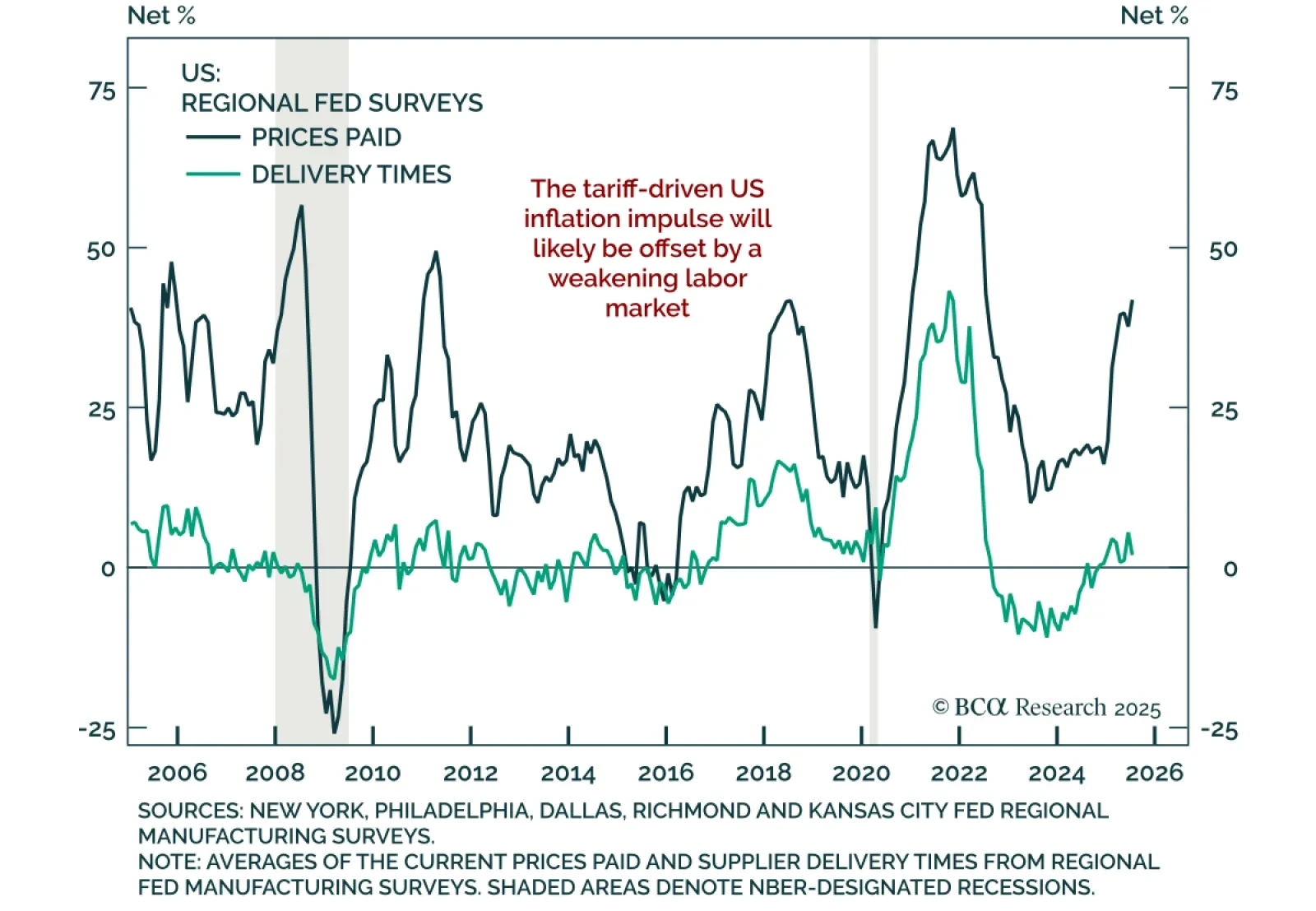

Cresting price pressures and weak global growth reinforce our long duration stance, with labor market slack limiting inflation upside across most major economies. Our price pressure indexes show moderate input inflation outside the US and stable global…

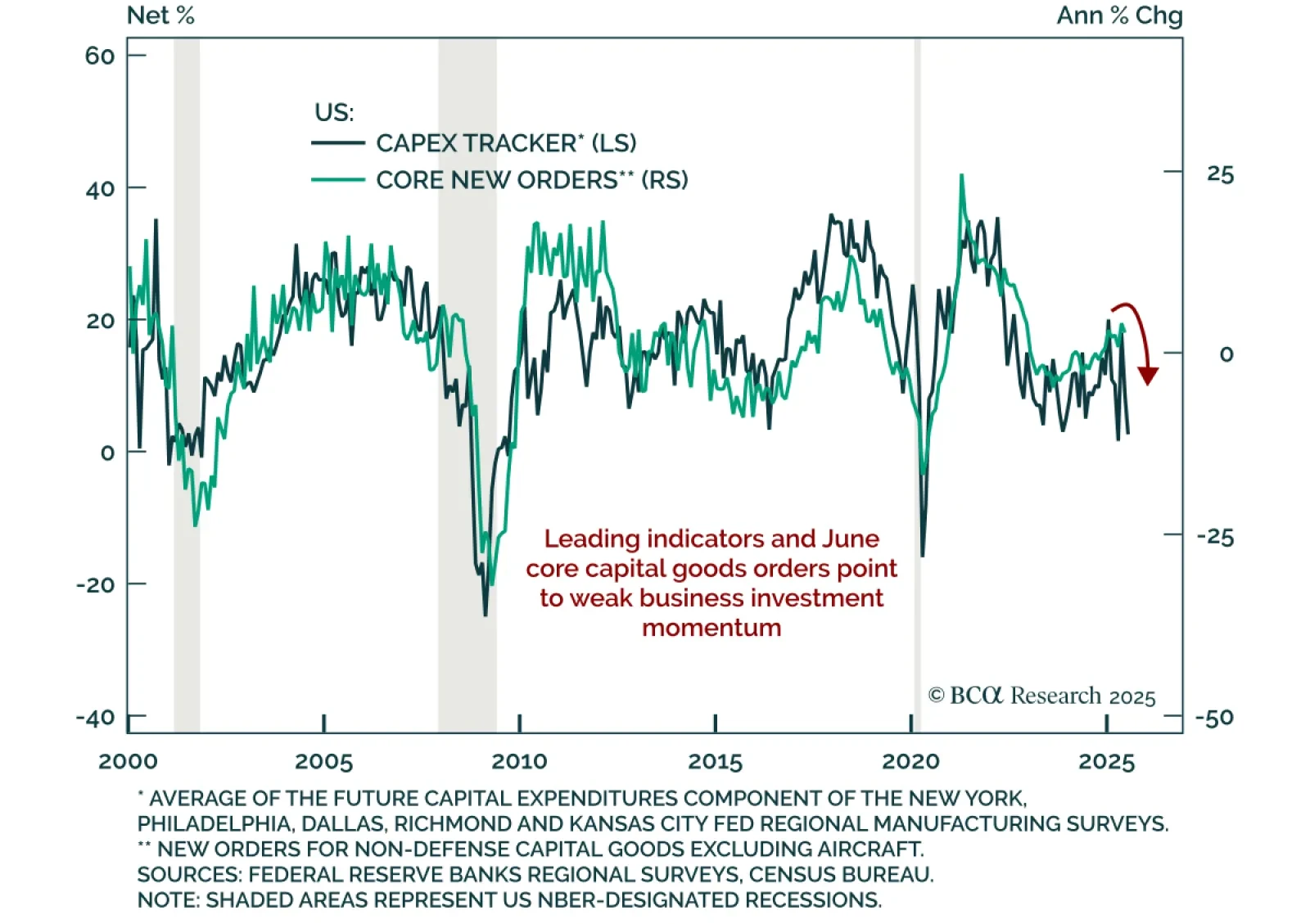

June core capital goods orders missed, confirming subdued capex momentum and reinforcing our defensive stance and long duration bias. Orders fell 0.7% m/m, below expectations, while shipments rose 0.4%. Headline durable goods dropped 9.3%, reversing…

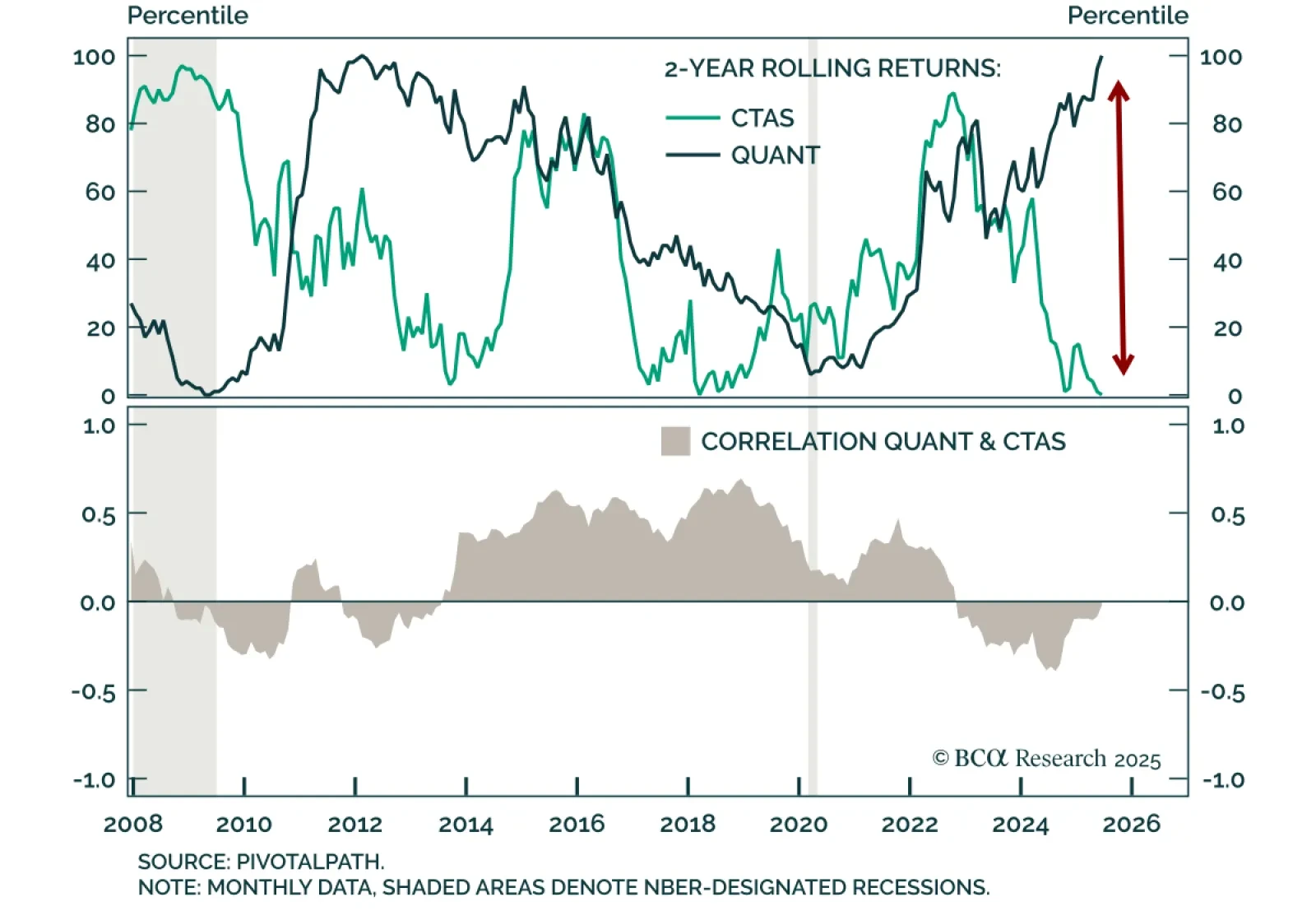

A historic divergence between systematic strategies is creating a compelling entry point into Managed Futures. Our Chart Of The Week comes from Brian Payne, Chief Strategist for our Private Markets & Alternatives team.In their…

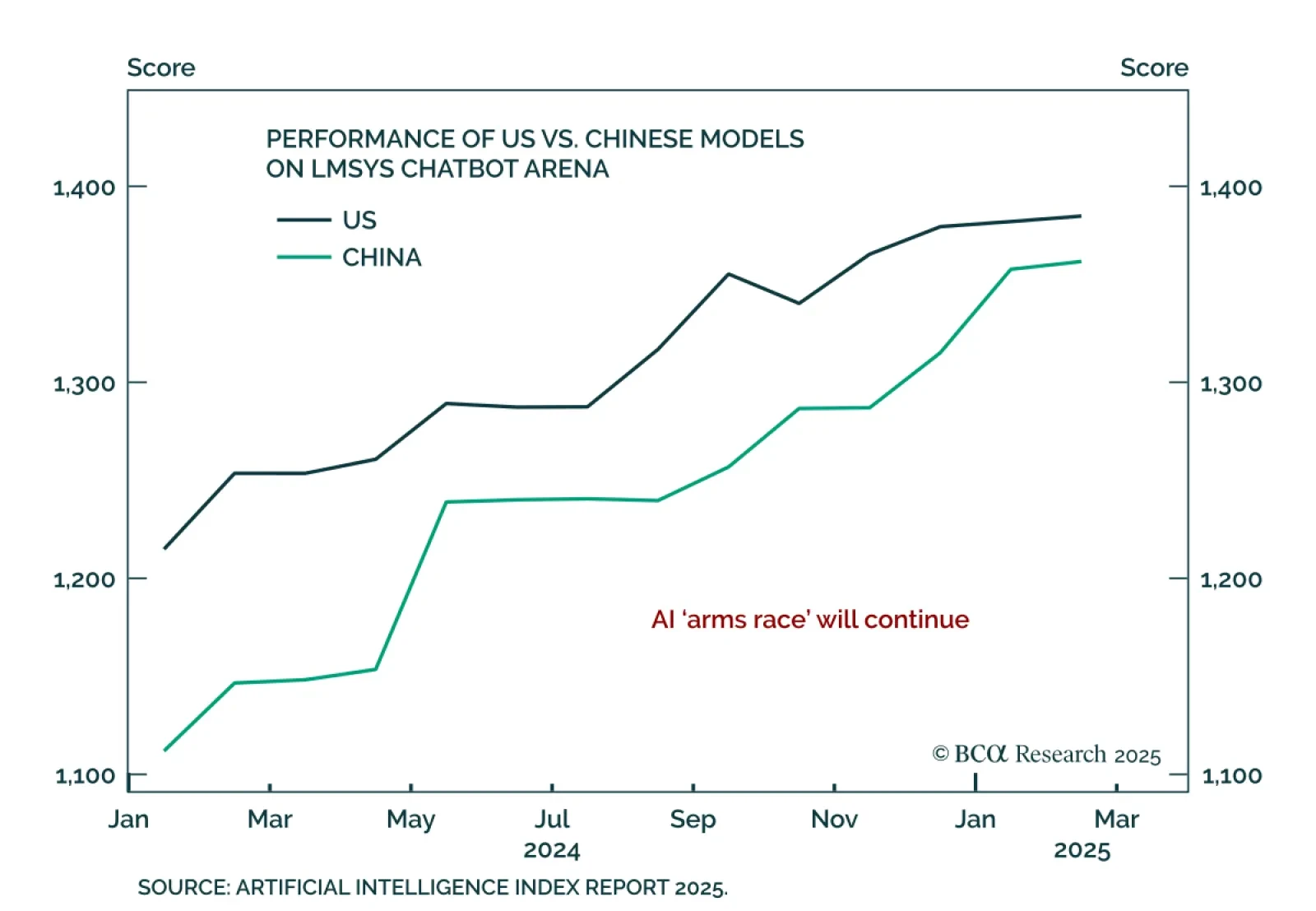

BCA’s Geopolitical strategists argue that artificial intelligence will destabilize both domestic politics and international security, prompting more aggressive fiscal responses. President Trump’s July 23 executive orders to accelerate US AI innovation,…

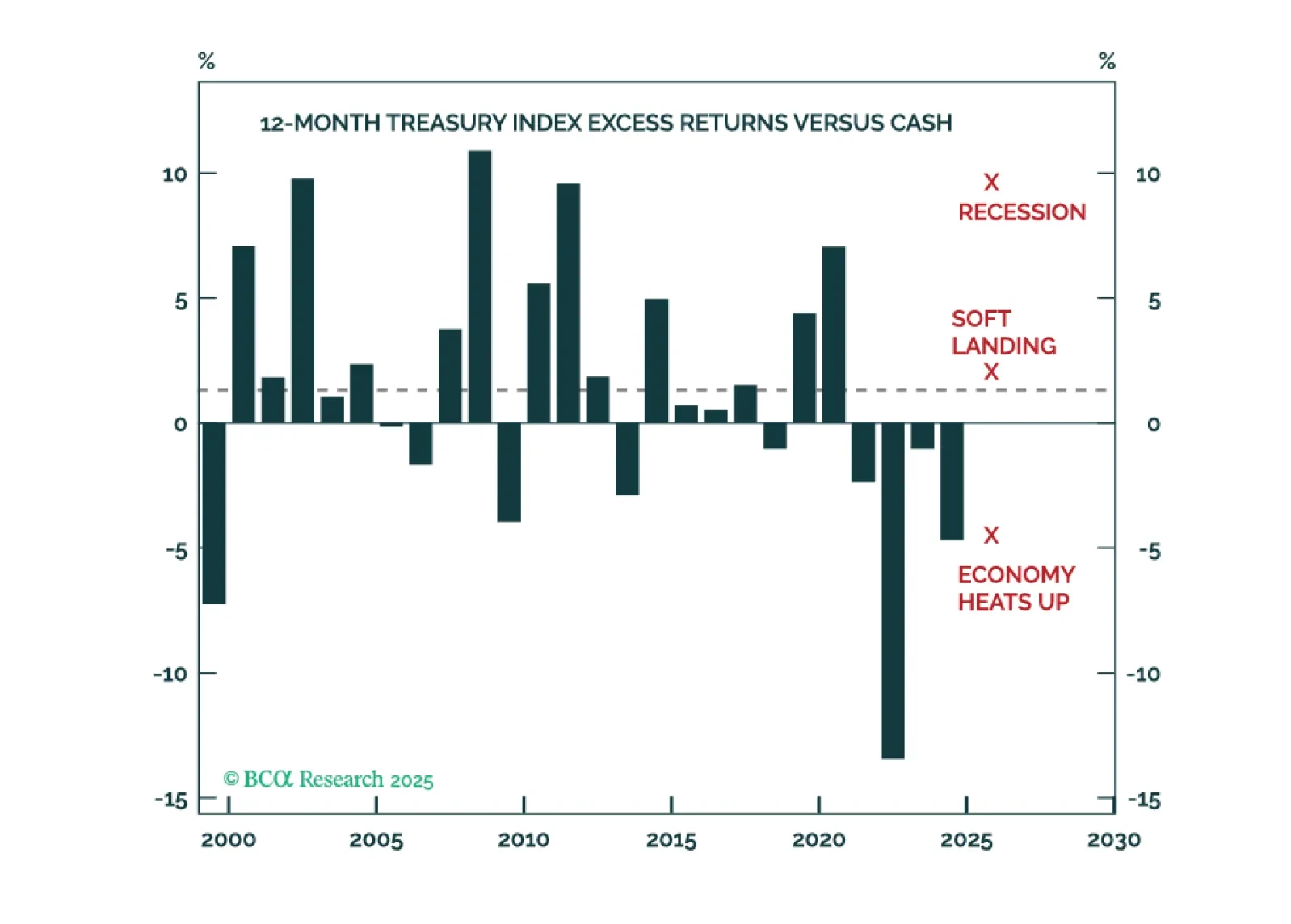

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.