United States

Highlights Continued upgrades to global economic growth – most recently by the IMF this week –will support higher natgas prices. In our estimation, gas for delivery at Henry Hub, LA, in the coming withdrawal season (November – March) is undervalued at current levels at ~ $2.90/MMBtu. Inventory demand will remain strong during the current April-October injection season, following the blast of colder-than-normal weather in 1Q21 that pulled inventories lower in the US, Europe and Northeast Asia. The odds the US will succeed in halting completion of the final leg of the Russian Nord Stream 2 natural gas pipeline into Germany are higher than the consensus expectation. Our odds the pipeline will not be completed this year stand at 50%, which translates into higher upside risk for natural gas prices. We are getting long 1Q22 calls on CME/NYMEX Henry Hub-delivered natgas futures struck at $3.50/MMBtu vs. short 1Q22 $3.75/MMBtu calls at tonight's close. The probability of Nord Stream 2 cancellation is underpriced, which means European TTF and Asian JKM prices will have to move higher to attract LNG cargoes next winter from the US, if the pipeline is cancelled (Chart of the Week). Feature As major forecasting agencies continue to upgrade global growth prospects, expectations for industrial-commodity demand – energy, bulks, and base metals – also are moving higher. This week, the IMF raised its growth expectations for this year and next to 6% and 4.4%, respectively, nearly a full percentage-point increase versus its January forecast update for 2021.1 This upgrade follows a similar move by the OECD last month.2 In the US, the EIA is expecting industrial demand for natural gas to rise 1.35 Bcf/d this year to 23.9 Bcf/d; versus 2019 levels, industrial demand will be 0.84 Bcf/d higher in 2021. For 2022, industrial demand is expected to be 24.2 Bcf/d. US industrial demand likely will recover faster than the EU's, given the expectation of a stronger recovery on the back of massive fiscal and monetary stimulus. Overall natgas demand in the US likely will move lower this year, given higher natgas prices expected this year and next will incentivize electricity generators to switch to coal at the margin, according to the EIA. Total demand is expected to be 82.9 Bcf/d in the US this year vs. 83.3 Bcf/d last year, owing to lower generator demand. Pipeline-quality gas output in the US – known as dry gas, since its liquids have been removed for other uses – is expected to average 91.4 Bcf/d this year, essentially unchanged. Lower consumption by the generators and flat production will allow US gas inventories to return to their five-year average levels of 3.7 Tcf by the end of October, in the EIA's estimation (Chart 2). Chart of the WeekUS-Russia Geopolitical Risk Underpriced

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Chart 2US Natgas Inventories Return To Five-Year Average

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US Liquified Natural Gas (LNG) exports are likely to expand, as Asian and European demand grows (Chart 3). Prior to the boost in US LNG demand from colder weather, exports set monthly records of 9.4 Bcf/d and 9.8 Bcf/d in November and December of last year, respectively, with Asia accounting for the largest share of exports (Chart 4). This also marked the first time LNG exports exceeded US pipeline exports to Mexico and Canada. The EIA is forecasting US LNG exports will be 8.5 bcf/d and 9.2 Bcf/d this year and next, versus pipeline exports of 8.8 Bcf/d and 8.9 Bcf/d in 2021 and 2022, respectively. Chart 3US LNG Exports Continue Growing

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Chart 4US LNG Exports Set Records In November And December 2020

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US LNG exports – and export potential given the size of the resource base at just over 500 Tcf – now are of a sufficient magnitude to be a formidable force in global markets, particularly in Europe. This puts it in direct conflict with Russia, which has targeted Europe as a key market for its pipeline natural gas exports. US-Russia Standoff Looming Over Nord Stream 2 Given the size and distribution of global oil and gas production and consumption, it comes as no surprise national interests can, at times, become as important to pricing these commodities as supply-demand fundamentals. This is particularly true in oil, and increasingly is becoming the case in natural gas. That the same dramatis personae – the US and Russia – should feature in geopolitical contests in oil and gas markets also should not come as a surprise. In an attempt to circumvent transporting its natural gas through Ukraine, Russia is building a 1,230 km underwater pipeline from Narva Bay in the Kingisepp district of the Leningrad region of Russia to Lubmin, near Greifswald, in Germany (Map 1). The Biden administration, like the Trump administration and US Congress, is officially attempting to halt the final leg of the pipeline from being built, although Biden has not yet put America’s full weight into stopping it. Biden claims it will be up to the Europeans to decide what to do. At the same time, any major Russian or Russian-backed military operation in Ukraine could trigger an American action to halt the pipeline in retaliation. Map 1Nord Stream 2 Route

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

In our estimation, there is a 50% chance that the Nord Stream 2 natural gas pipeline will not be completed this year or go into operation as planned given substantial geopolitical risks. The $11 billion pipeline would connect Russia directly to Germany with a capacity of about 55 billion cubic meters, which, combined with the existing Nord Stream One pipeline, would equal 110 BCM in offshore capacity, or 55% of Russia's natural gas exports to Europe in 2019. The pipeline’s construction is 94% complete, with the Russian ship Akademik Cherskiy entering Danish waters in late March to begin laying pipes to finish the final 138-kilometer stretch, according to Reuters. The pipeline could be finished in early August at the pace of 1 kilometer per day.3 The Russian and German governments are speeding up the project to finish it before US-Russia tensions, or the German elections in September, interrupt the construction process again. It is not too late for the US to try to halt the pipeline through sanctions. But for the Americans to succeed, the Biden administration would have to make an aggressive effort. Notably the Biden administration took office with a desire to sharpen US policy toward Russia.4 While Biden seeks Russian engagement on arms reduction treaties and the Iranian nuclear negotiations, he mainly aims to counter Russia, expand sanctions, provide weapons to Ukraine, and promote democracy in Russia’s sphere of influence. The result will almost inevitably be a new US-Russia confrontation, which is already taking shape over Russia’s buildup of troops on the border with Ukraine, where US and Russian meddling could cause civil war to reignite (Map 2). Map 2Russia’s Military Tensions With The West Escalate In Wake Of Biden’s Election And Ukraine’s Renewed Bid To Join NATO

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Tensions in Ukraine are directly tied to US military cooperation with Ukraine and any possibility that Ukraine will join the NATO military alliance, a red line for Putin. Nord Stream 2 is Russia’s way of bypassing Ukraine but a new US-Russia conflict, especially a Russian attack on Ukraine, would halt the pipeline. The pipeline’s completion would improve Russo-German strategic relations, undercut US liquefied natural gas exports to Germany and the EU, and reduce the US’s and eastern Europe’s leverage over Russia (and Germany). Biden says his administration is planning to impose new sanctions on firms that oversee, construct, or insure the pipeline, and such sanctions are required under American law.5 Yet Biden also wants a strong alliance with Germany, which favors the pipeline and does not want to escalate the conflict with Russia. The American laws against Nord Stream have big loopholes and give the president discretion regarding the use of sanctions, which means Biden would have to make a deliberate decision to override Germany and impose maximum sanctions if he truly wanted to halt construction.6 This would most likely occur if Russia committed a major new act of aggression in Ukraine or against other European democracies. The German policy, under the current ruling coalition led by Chancellor Angela Merkel’s Christian Democratic Union, is to finish the pipeline despite Russia’s conflicts with the West and political repression at home. Russia provides more than a third of Germany’s natural gas imports and this pipeline would bypass eastern Europe’s pipeline network and thus secure Germany’s (and Austria’s and the EU’s) natural gas supply whenever Russia cuts off the flow to Ukraine (through which roughly 40% of Russian natural gas still must pass to reach Europe). Germany's Election And Natgas Politics Germany wants to use natural gas as a bridge while it phases out nuclear energy and coal. Natural gas has grown 2.2 percentage points as a share of Germany’s total energy mix since the Fukushima disaster of 2011, and renewable energy has grown 7.7ppt, while coal has fallen 7.3ppt and nuclear has fallen 2.5ppt (Chart 5). The German federal election on September 26 complicates matters because Merkel and the Christian Democrats are likely to underperform their opinion polls and could even fall from power. They do not want to suffer a major foreign policy humiliation at the hands of the Americans or a strategic crisis with Russia right before the election. They will insist that Biden leave the pipeline alone and will offer other forms of cooperation against Russia in compensation. Therefore, the current German government could push through the pipeline and complete the project even in the face of US objections. But this outcome is not guaranteed. The German Greens are likely to gain influence in the Bundestag after the elections and could even lead the German government for the first time – and they are opposed to a new fossil fuel pipeline that increases Russia’s influence. Chart 5Germany Sees Nord Stream 2 Gas As Bridge To Low-Carbon Economy

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Hence there is a fair chance that the pipeline does not become operational: either Americans halt it out of strategic interest, or the German Greens halt it out of environmental and strategic interest, or both. True, there is a roughly equal chance that Merkel’s policy status quo survives in Germany, which would result in an operational pipeline. The best case for Germany might be that the current government completes the pipeline physically but the next government has optionality on whether to make it operational. But 50/50 odds of cancellation is a much higher risk than the consensus holds. The Russian policy is to finish Nord Stream 2 while also making an aggressive military stance against the West’s and NATO’s influence in Ukraine. This would expand Russian commodity and energy exports and undercut Ukraine’s natgas transit income. It would also increase Russian leverage over Germany – and it would divide Germany from the eastern Europeans and Americans. A preemptive American intervention would elicit Russian retaliation. The Russians could respond in the strategic sphere or the economic sphere. Economically they could react by cutting off natural gas to Europe, but that would undermine their diplomatic goals, so they would more likely respond by increasing production of natural gas or crude oil to steal American market share. In any scenario Russian retaliation would likely cause global price volatility in one or more energy markets, in addition to whatever volatility is induced by the cancellation of Nord Stream 2 itself. US-Russia tensions are likely to escalate but only Ukraine and Nord Stream 2, or the separate Iranian negotiations, have a direct impact on global energy supply. If Germany goes forward with the pipeline, then Russia would need to be countered by other means. The Americans, not the Germans, would provide these “other means,” such as military support to ensure the integrity of Ukraine and other nations’ borders. The Russians may gain a victory for their energy export strategy but they will never compromise on Ukraine and they will still need to focus on the broader global shift to renewable energy, which threatens their economic model and hence ultimately their regime stability. So, the risk of a market-moving US-Russia conflict can be delayed but probably not prevented (Chart 6). Chart 6US-Russia Conflit Likely

US-Russia Conflit Likely

US-Russia Conflit Likely

Bottom Line: The Nord Stream 2 pipeline is not guaranteed to be completed this year as planned. The US is more likely to force a halt to the Nord Stream 2 pipeline than the consensus holds, especially if Russia attacks Ukraine. If the US fails to do so, then the German election will become the next signpost for whether the pipeline will become operational. If the Americans halt the pipeline, then US-Russian conflict either already erupted or will occur sooner rather than later and will likely impact global oil or natural gas prices. Investment Implications Our subjective assessment of 50% odds the US will succeed in halting completion of the final leg of Nord Stream 2 are higher than the consensus expectation. This translates directly into higher upside risk for natural gas prices in the US and Europe later this year and next. Given our view, we are getting long 1Q22 calls on CME/NYMEX Henry Hub-delivered natgas futures struck at $3.50/MMBtu vs. short 1Q22 $3.75/MMBtu calls at tonight's close. The probability of Nord Stream 2 cancellation is underpriced, which means the odds of higher prices in the LNG market are underpriced (Chart 7). The immediate implication of our view is European TTF prices will have to move higher to attract LNG cargoes next winter from the US, if the Nord Stream 2 pipeline's final leg is cancelled. This also would tighten the Asian markets, causing the JKM to move higher as well (Chart 8). Any indication of colder-than-normal weather in the US, Europe or Asian markets would mean a sharper move higher. Chart 7Natgas Tails Are Too Narrow For Next Winter

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Chart 8Nord Stream 2 Cancellation Would Boost JKM Prices

Nord Stream 2 Cancellation Would Boost JKM Prices

Nord Stream 2 Cancellation Would Boost JKM Prices

Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Commodities Round-Up Energy: Bullish The US and Iran began indirect talks earlier this week in Vienna aimed at restoring the Joint Comprehensive Plan of Action (JCPOA), otherwise known as the "Iran nuclear deal." All of the other parties of the deal – Britain, China, France, Germany and Russia – are in favor of restoring the deal. BCA Research believes this is most likely to occur prior to the inauguration of a new president who is expected to be a hardliner willing to escalate Iran’s demands. US President Biden can unilaterally ease sanctions and bring the US into compliance with the deal, and Iran could then reciprocate. If a deal is not reached by August it could take years to resolve US-Iran tensions. China could offer to cooperate on sanctions and help to broker negotiations following the signing of its 25-year trade deal with Iran last week. Russia likely would demand the US not pressure its allies to cancel the Nord Stream 2 deal, in return for its assistance in brokering a deal. Base Metals: Bullish Iron ore prices continue to be supported by record steel prices in China, trading at more than $173/MT earlier this week. Even though steel production reportedly is falling in the top steel-producer in China, Tangshan, as a result of anti-pollution measures, for iron ore remains stout. As we have previously noted, we use steel prices as a leading indicator for copper prices. We remain long Dec21 copper and will be looking for a sell-off to get long Sep21 copper vs. short Sep21 copper if the market trades below $4/lb on the CME/COMEX futures market (Chart 9). Precious Metals: Bullish Gold held support ~ $1,680/oz at the end of March, following an earlier test in the month. We remain long the yellow metal, despite coming close to being stopped out last week (Chart 10). The earlier sell-off appeared to be caused by a need to raise liquidity to us. We continue to expect the Fed to hold firm to its stated intent to wait for actual inflation to become manifest before raising rates, and, therefore, continue to expect real rates to weaken. This will be supportive of gold and commodities generally (Chart 10). Ags/Softs: Neutral Corn continues to be well supported above $5.50/bu, following last week's USDA report showing farmers intend to increase acreage planted to just over 91mm acres, which is less than 1% above last year's level. Chart 9

Copper Prices Surge As Global Storage Draws

Copper Prices Surge As Global Storage Draws

Chart 10

Gold Disconnected From US Dollar And Rates

Gold Disconnected From US Dollar And Rates

Footnotes 1 Please see the Fund's April 2021 forecast Managing Divergent Recoveries. 2 We noted last week these higher growth expectations generally are bullish for industrial commodities – energy, metals, and bulks. Please see Fundamentals Support Oil, Bulks, And Metals, which we published 1 April 2021. It is available at ces.bcaresearch.com. 3 For the rate of construction see Margarita Assenova, “Clouds Darkening Over Nord Stream Two Pipeline,” Eurasia Daily Monitor 18: 17 (February 1, 2021), Jamestown Foundation, jamestown.org. For the current status, see Robin Emmott, “At NATO, Blinken warns Germany over Nord Stream 2 pipeline,” Reuters, March 23, 2021, reuters.com. 4 The Democratic Party blames Russia for what it sees as a campaign to undermine the democratic West and recreate the Soviet sphere of influence. See for example the 2008 invasion of Georgia, the failure of the Obama administration’s 2009-11 diplomatic “reset,” the Edward Snowden affair, the seizure of Crimea and civil war in Ukraine, the survival of Syria’s dictator, and Russian interference in US elections in 2016 and 2020. 5 The Countering Russian Influence in Europe and Eurasia Act of 2017, and the Protecting Europe’s Energy Security Act of 2019/2020, contain provisions requiring sanctions on firms that have contributed in any way a minimum of $1 million to the project, or provide pipe-laying services or insurance. There are exceptions for services provided by the governments of the EU member states, Norway, Switzerland, or the UK. The president has discretion over the implementation of sanctions as usual. 6 The German state of Mecklenburg-Vorpommern is creating a shell foundation to enable the completion of the pipeline. It can shield companies from American sanctions aimed at private companies, not sovereigns. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way

Put A Rolling Stop On The "Back-To-Work" Versus "COVID-19 Winners Trade"

Put A Rolling Stop On The "Back-To-Work" Versus "COVID-19 Winners Trade"

We nearly fully captured the economic reopening theme through our long “Back-To-Work”/short “COIVD-19 Winners” baskets pair trade. As a brief summary, we first initiated this trade in the September 8th, 2020 Strategy Report, and subsequently closed it earlier this year for a gain of 21.5% via a rolling stop trigger, until we reopened it once again on February 3. Fast-forward to today, and this pair trade has vaulted another 25.5% since the second inception. Now that the US equity market is euphoric on the back of stimulus news and more importantly given that the bond market is no longer responsive having already priced in four Fed hikes by the end of 2023, we opt to re-introduce a 5% rolling stop as a risk management tool in order to protect handsome profits. Bottom Line: Institute a 5% rolling stop in the long “Back-To-Work”/short “COIVD-19 Winners” baskets pair trade today.

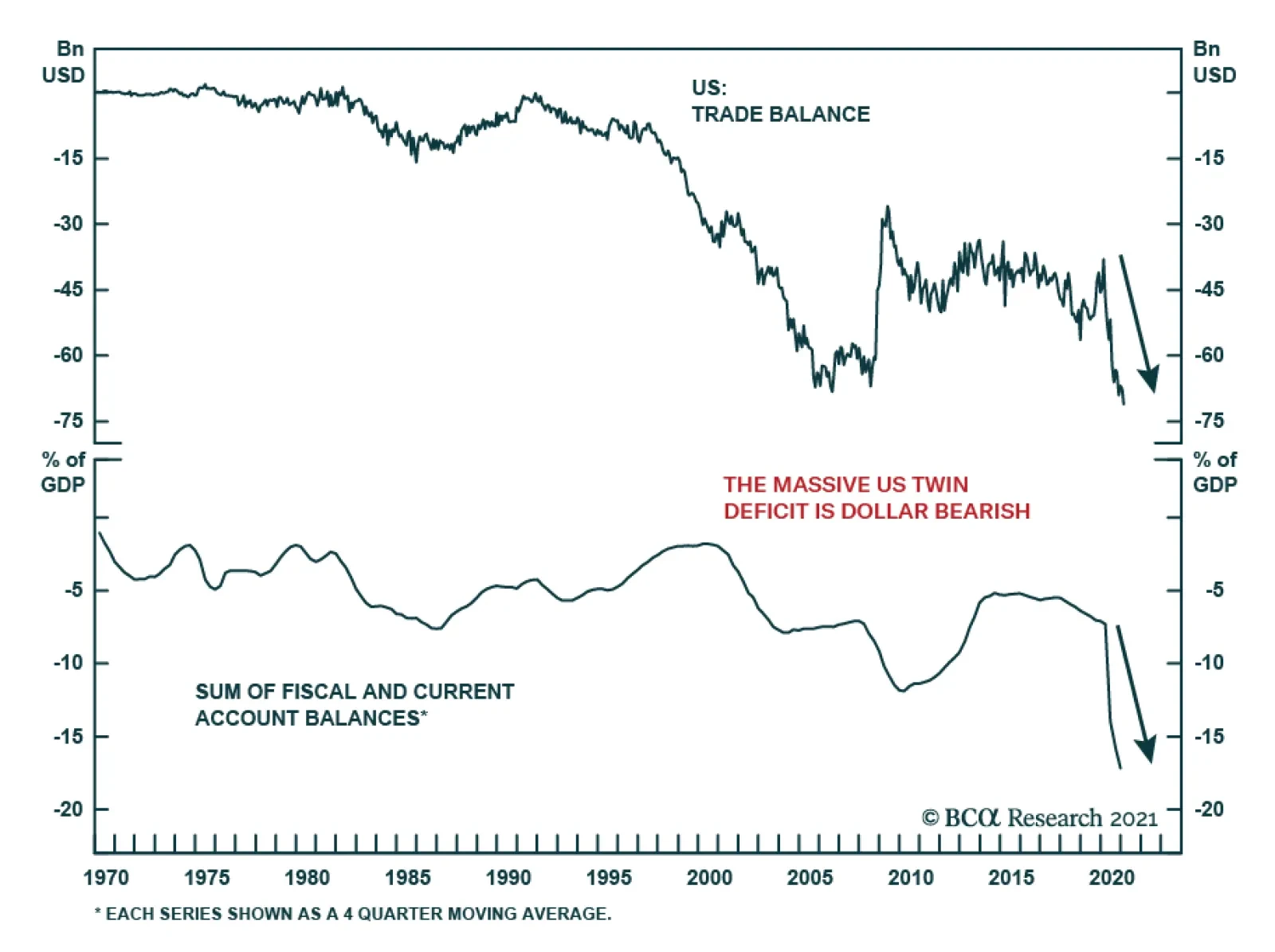

The US trade deficit widened further in February, hitting a record $71.1 billion. The trade balance reflects the recent growth divergence whereby US economic resilience is buoying America’s imports while depressed global growth is weighing on US exports. The…

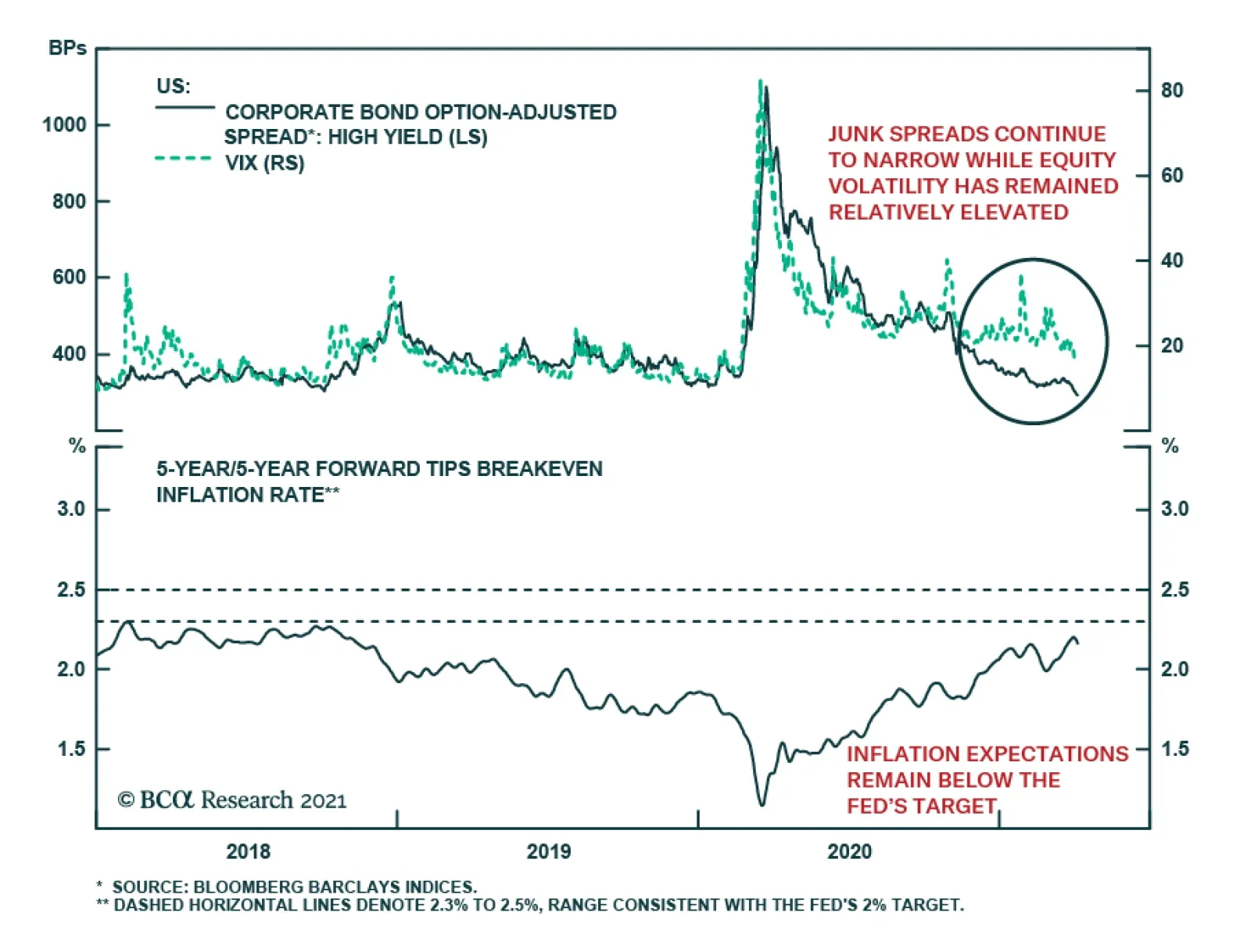

Corporate spreads have sent an upbeat message this year. Junk spreads continue to narrow, and they have recently tightened by the most in over a decade. Meanwhile, equity volatility has remained relatively elevated, which has disrupted the historically strong…

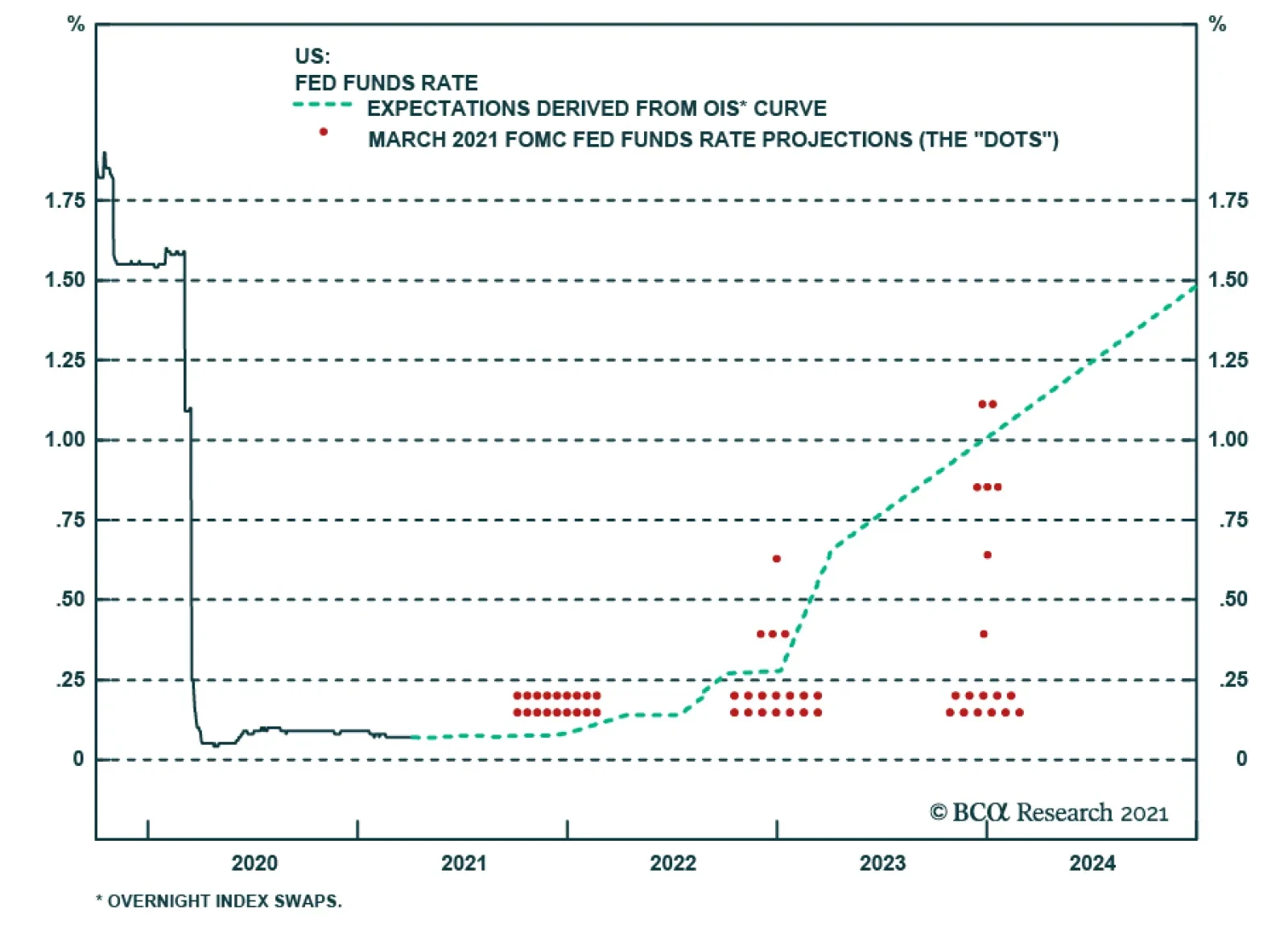

The minutes from the March FOMC meeting, released yesterday, didn’t reveal anything new or shocking about the Federal Reserve’s reaction function. The minutes noted that both the Fed staff and meeting participants revised up their forecasts for real GDP…

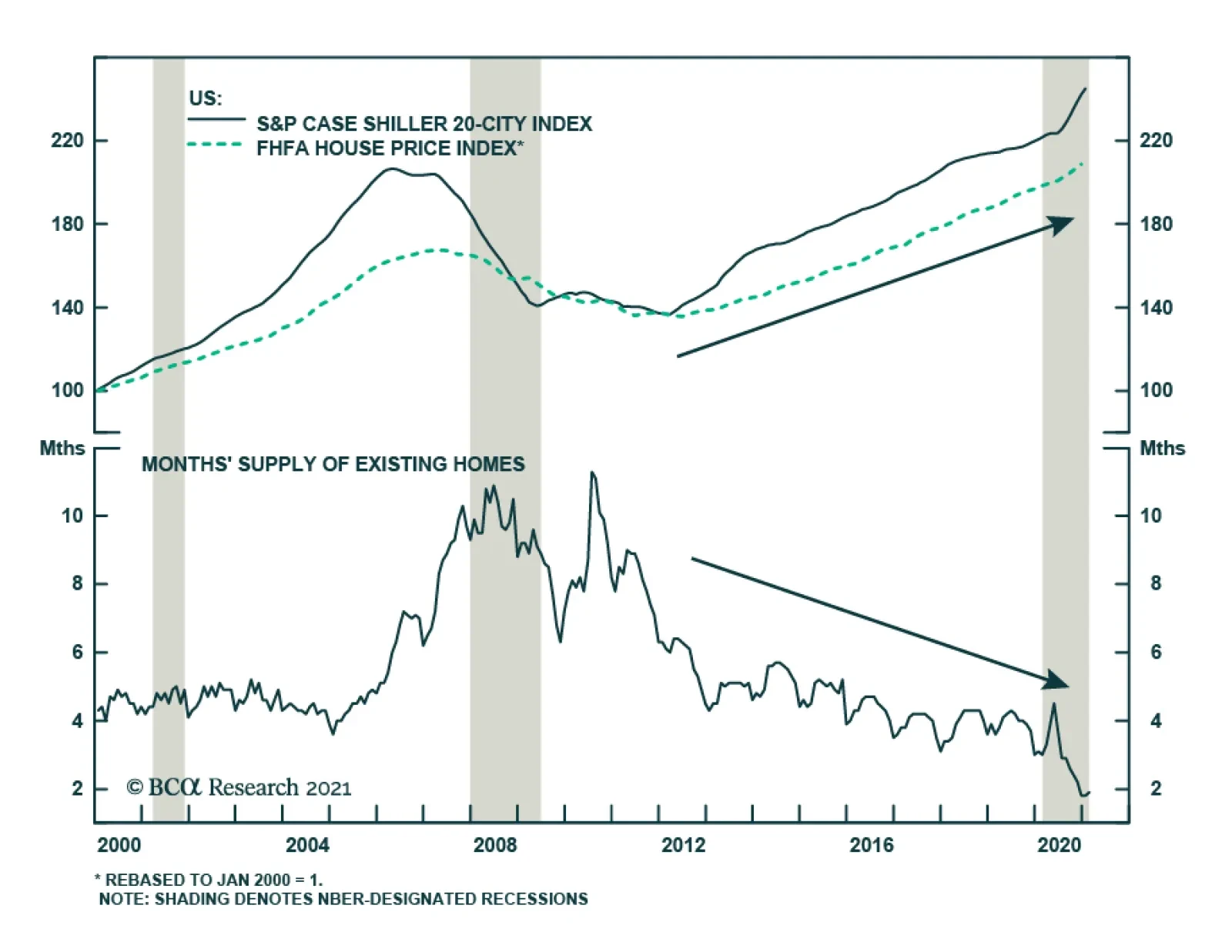

BCA Research’s US Investment Strategy service believes that the US housing boom has at least another year or two to run. The pandemic has stoked demand for suburban single-family homes and it appears that some of the migration from urban centers to…

Highlights Our 80% odds that Biden will pass the $2.3 trillion American Jobs Plan stem from public opinion as well as Democratic control of Congress. Voters favor both higher taxes on corporations and higher infrastructure spending, as well as Biden’s proposal to pay for the latter by means of the former. A bipartisan consensus favors infrastructure spending, including “soft” infrastructure. Republicans who campaigned on the need for infrastructure over the past five years will not gain voter support by opposing it now. The Senate parliamentarian’s recent ruling on budget reconciliation procedures enables the Democrats to pass a second reconciliation bill, as expected. This puts Biden’s American Families Plan, to be detailed this month, officially into play for FY2022. Our initial premise remains a 50/50 chance that the $1.9 trillion bill passes before the 2022 midterms. Infrastructure plays benefit from a rising budget deficit but will also face a global headwind as China’s stimulus and growth momentum wane. Feature The market cheered the Biden administration’s $2.3 trillion American Jobs Plan despite the confirmation that corporate tax rates will go up as expected (Chart 1). The details of the plan are shown in Table 1, which makes it clear that $760 billion can easily be subtracted from the plan during negotiations as not having to do with infrastructure. However, investors should wager that most of the new spending, including the social welfare components, will pass, since Democrats will use the budget reconciliation process. Chart 1Market Response To Biden, Infrastructure, Tax Hikes

Market Response To Biden, Infrastructure, Tax Hikes

Market Response To Biden, Infrastructure, Tax Hikes

Table 1Biden's 'American Jobs Plan'

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

The bigger question is tax hikes. Senator Joe Manchin of West Virginia reiterated that a 25% corporate tax rate is as high as he is willing to go. Since Democrats cannot spare a single vote in the Senate (not to mention six or seven votes, which Manchin claims to have on his side), the corporate tax rates may be compromised. Still, investors should prepare for the worst, i.e. the 28% rate that Biden presented or only slightly less. While Manchin is the critical marginal voter – his vote will turn the balance of power in the Senate – nevertheless there will be enormous pressure on him not to “betray” his party and vote against the signature legislative proposal of the Biden presidency. Insofar as Manchin succeeds, he presents a “less bad” outcome for equity sectors that stand to suffer the most from a higher headline corporate tax rate, such as utilities, health care, and information technology (Chart 2). Chart 2Corporate Tax Rates Will Rise To 25%-28%, A Big Increase For Real Estate, Health Care, Tech, Utilities, And Consumer Staples

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

It will take time to draft and negotiate the spending and tax provisions and then get them passed in both the House and Senate. The Democrats also face tight margins in the House, where they can only lose four votes (the balance in the House is 218-211 after the death of Florida Representative Alcee Hastings). The earliest possible passage – based on historical precedent – is in May. The average length of time would put passage in November. In the worst case the negotiations could drag on till Christmas but we highly doubt the Democrats will take that long (Diagram 1). We attach an 80% subjective probability to the view that the American Jobs Plan will pass by end of year. Diagram 1Time Line For Congress To Pass American Jobs Plan By End Of 2021

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Where we are less certain is in the second part of Biden’s economic plan, the $1.9 trillion American Families Plan, which contains social welfare spending, an expansion of the child tax credit and other tax cuts for the lower and middle classes, and the tax hikes on upper-middle class and wealthy individuals and households. This program will be outlined this month. It will be a challenge to pass it prior to the 2022 midterm elections, depending on how fast infrastructure flies through Congress. Our subjective 50% odds received initial support on April 5 when the Senate parliamentarian, Elizabeth MacDonough, ruled that the Democrats can indeed pass more than one budget reconciliation bill per fiscal year, contrary to previous practice. This bill is just as likely to be the Democratic campaign platform for 2022 as to be passed in early 2022 under the current Congress. Senate Parliamentarian Enables Democrats To Bypass Filibuster We must pause here to note that the parliamentarian’s ruling is highly consequential as it erodes the checks and balances on passing legislation in the Senate. The new ruling holds that under Section 304 of the Congressional Budget Act of 1974 the annual budget resolution can be revised. If it can be revised, then a new budget reconciliation bill can be crafted according to the new budget resolution. And reconciliation enables the ruling party to push through bills on a simple majority (51 votes) in the Senate. It will be hard for the Senate, as a body, to limit the ramifications of this decision in future. If the Democrats can pass two reconciliation bills in FY2021, then who is to say that some later Congress cannot pass three? Regardless, it is hard for a party to pass more than three major pieces of legislation in a single year, so the window is just wide enough to enable major breakthroughs in legislation (and, whenever the opposing party regains the House and Senate, big reversals of legislation). We have argued that Democrats would eventually, if not immediately, remove the Senate filibuster (the rule that requires 60-votes to end debate on regular legislation). At the moment there are still not enough votes to remove the filibuster entirely, although moderate Democrats are looking at technical ways of diminishing its influence, such as via the “talking filibuster” that would increase the difficulty of the process and thus reduce its use in the Senate.1 But this new ruling on budget reconciliation process substantively bypasses the filibuster. While the reconciliation process will still come with various technical limitations (the “Byrd rule,” and relevance to the budget), they are pliable. Clearly the ruling party calls the shots – especially if it is a party in synch with the political establishment in Washington. The Public Favors Tax Hikes For Infrastructure Where do we get our 80% subjective probability that Biden’s American Jobs Plan will pass Congress? Why so confident? First, Democrats have control of Congress, albeit narrowly. Second, public opinion not only favors infrastructure but also favors tax hikes on corporations – especially if they are to pay for infrastructure. The solution has been to rebrand renewable energy, broadband Internet, subsidized housing, and a range of other government programs as “infrastructure,” and meanwhile to rebrand social welfare as “human infrastructure.” Consider the following: The public favors higher taxes on corporations: 69% of Americans believe corporations pay too little in taxes, while only 6% believe they pay too much (Chart 3). While this is a general view, and does not reflect regional variations, it calls into question Joe Manchin’s opposition to a corporate tax rate of 28%. Manchin has his eye on the economic recovery, small business owners, as well as the particular industries and political orientation of his state. But the point is that opposition to corporate tax hikes is politically weak and therefore we continue to expect the result to be closer to Biden’s 28% than to Manchin’s 25%. The public favors higher taxes on high-income earners: As for Biden’s second slate of tax hikes, on individuals and households under the yet-to-be detailed American Families Act, 62% of Americans believe that upper-income earners pay too little in taxes and again only 9% believe they pay too much (Chart 4). Since Biden’s proposals amount to only a partial repeal of President Trump’s Tax Cut and Jobs Act, which was itself unpopular in opinion polling, investors should also have a presumption in favor of individual tax hikes. However, as noted above, the American Families Plan only has a 50% chance of passing prior to the midterms due to the time crunch. Chart 3Public Favors Tax Hikes On Corporations

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Chart 4Public Favors Tax Hikes On The Rich

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Government is not seen as incompetent on infrastructure: Net public approval of the government’s performance on infrastructure is positive, just barely, unlike immigration, health care, or the environment. This means Biden can tap into a greater level of trust in government on this policy, while still calling on a general belief that infrastructure needs to be improved (Chart 5). Chart 5Public Gives Government Decent Grades On Infrastructure

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Chart 6No Partisan Gap On whether Infrastructure Should Be Prioritized

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Infrastructure is bipartisan: The gap in the views of Republicans and Democrats is narrow when it comes to infrastructure, unlike other policy issues that are extremely polarized. The gap is narrow whether infrastructure should be prioritized (Chart 6), whether government should play a larger role (Chart 7), and whether the federal government does a good job in this area (Chart 8). Democrats are more supportive of these propositions and they are currently in charge. But even Republicans tend to agree, as indicated by President Trump’s own emphasis on infrastructure, which the grassroots of his party supported despite establishment Republican hesitations due to concerns about the deficit. These charts also suggest that voters, especially Democratic voters, will not be bothered by the presence of non-traditional or “soft” infrastructure in Biden’s package as long as it can be successfully pitched as helping the economy, jobs, and American supply chains. Chart 7Government Role In Infrastructure Not Too Partisan

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Chart 8Government Performance On Infrastructure Not Too Partisan

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

The public approves of Biden’s corporate-tax-hikes-for-infrastructure tradeoff: About 54% approve outright, in line with Biden’s overall approval rating, including 52% of independents and a non-negligible 32% of Republicans. A further 27% support infrastructure spending without raising taxes, including 42% of Republicans (Chart 9). This poll does not stand alone but corroborates a range of polling over the past decade on both taxes and infrastructure. It strongly implies that the median voter will support Biden’s plan. (And again it suggests that while Senator Manchin may turn the balance in the Senate he is not standing on solid rock in calling for Biden to pare back his corporate tax hikes.) Chart 9Voters Back Tax Hikes For Infrastructure

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

No need to rely on polling – look at how people vote: Ballot measures on the local level for transportation funding usually win high levels of voter approval, meaning that people vote to increase their own taxes if they think traditional infrastructure will be improved. The average approval for such measures stood at 74% in 2016 and rose to 94% in the 2020 election cycle (Chart 10). And voters clearly understood that this combination is what they would get in voting for Biden, given that he did not shy away from his tax proposals in the presidential debates (although he insisted no tax hikes on those who earn less than $400,000 per year). Chart 10Voters Accept Higher Taxes For Infrastructure

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

The Democrats have the votes for an infrastructure package, they have the votes for at least some degree of corporate tax hikes, and they have popular opinion behind the principle of tax hikes in exchange for infrastructure upgrades. Furthermore the rise of geopolitical struggle abroad and populism at home have given Biden and the traditional Democrats extraordinary impetus to pass this bill. If they fail, they will have wasted precious congressional time, they will be less likely to pass the American Families Plan, and they will be more likely to lose control of the House or even the Senate in 2022, as their failure would energize both the democratic socialists on their left and the Trump Republicans on their right. It is unlikely that Senator Manchin alone is willing or able to cause such a train wreck for his party given the popularity of the proposals.2 The implication is that corporate tax hikes will be compromised only somewhat. It is also possible that non-infrastructure components of the bill, such as housing or some social spending, could be pared back, although these are not the controversial parts of the bill and we would not bet on the overall size of spending to be reduced by much. A bill with Biden’s spending measures and only half of the tax hikes would increase the budget deficit by $1.4 trillion, as we showed last week. A bill with all spending and all tax hikes would increase the deficit by $400 billion. Bottom Line: Biden has an 80% chance of passing the American Jobs Act, although some non-infrastructure provisions could be pared back and the corporate tax hike may not reach all the way to 28%. Most likely the final bill will be substantially similar to Biden’s proposal on spending, while the tax hikes will be compromised, reflecting the populist and proactive fiscal turn in US politics. Investment Takeaways A basket of the 50 companies in the S&P 500 with the highest median effective tax rates outperformed the S&P500 upon Trump’s election and subsequent tax cuts (Chart 11). Since Biden’s election they have also outperformed on the expectation of post-pandemic reopening and economic stimulus. However, the high-tax companies and high-tax sectors have underperformed on an equal-weighted basis since the Democratic Party won control of the Senate and tax hikes became inevitable. Tax hikes are largely but not fully priced from this point of view. Historically a rising budget deficit does not have a clear or positive correlation with the S&P 500, cyclical sectors, value stocks, or small caps. Fiscal thrust normally surges during recessions and bear markets. Nevertheless infrastructure plays – by which we include building products, construction materials and services, environmental services, metals and mining, machinery, and steel – tend to perform better when the deficit blows out. That trend looks to be intact today (Chart 12). Chart 11High-Tax Companies Rallied Despite Biden's Tax Hikes (But Not On Equal-Weighted Basis)

High-Tax Companies Rallied Despite Biden's Tax Hikes (But Not On Equal-Weighted Basis)

High-Tax Companies Rallied Despite Biden's Tax Hikes (But Not On Equal-Weighted Basis)

Chart 12US Budget Blow-Out Positive For Infrastructure Plays

US Budget Blow-Out Positive For Infrastructure Plays

US Budget Blow-Out Positive For Infrastructure Plays

The budget deficit is generally a stronger predictor of the performance of these sub-sectors than global manufacturing surveys and leading economic indicators, although the improvement in global sentiment and growth is clearly a positive backdrop (Chart 13). Europe and countries other than China will soon improve their vaccinations, reopen, and start catching up to the US economic rebound. China’s fiscal-and-credit impulse is closely correlated with US infrastructure plays and this has not changed since the trade war began (Chart 14). Importantly, China is tapping on the policy brakes and its economy is set to decelerate in the second half of the year, which has important implications for our BCA Infrastructure Basket and long trades. This indicator suggests that the relative performance of infrastructure plays will face a gradually rising headwind from abroad even as the US economy continues to provide a tailwind. Chart 13Global Sentiment Positive But Not A Big Driver Of US Infrastructure Plays

Global Sentiment Positive But Not A Big Driver Of US Infrastructure Plays

Global Sentiment Positive But Not A Big Driver Of US Infrastructure Plays

Chart 14Infrastructure Plays Face Headwind From China's Waning Stimulus

Infrastructure Plays Face Headwind From China's Waning Stimulus

Infrastructure Plays Face Headwind From China's Waning Stimulus

Infrastructure plays shown here – which consist of goods and services that fall under greater demand when infrastructure is built – should not be confused with infrastructure companies themselves, which tend to be classified under the much more defensive utilities and telecommunication sectors (Chart 15). This ratio is looking very toppy, in keeping with the general rollover in cyclical equity sector performance relative to defensives. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Jesse Anak Kuri Associate Editor jesse.Kuri@bcaresearch.com Chart 15Infrastructure Plays Versus Utilities And Telecoms

Infrastructure Plays Versus Utilities And Telecoms

Infrastructure Plays Versus Utilities And Telecoms

Appendix Table A1Political Risk Matrix

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Table A2Political Capital Index

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Table A3APolitical Capital: White House And Congress

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Table A3BPolitical Capital: Household And Business Sentiment

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Table A3CPolitical Capital: The Economy And Markets

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Table A4Biden’s Cabinet Position Appointments

Will Biden Get The Votes For Infrastructure?

Will Biden Get The Votes For Infrastructure?

Footnotes 1 Molly E. Reynolds, “What is the Senate filibuster, and what would it take to eliminate it?” Brookings Institution, September 9, 2020, brookings.edu. 2 On the contrary, while the bill will pass via party-line voting, it is still conceivable that one or two moderate Senate Republicans could be brought to endorse Biden’s American Jobs Plan.

Book Handsome Gains In Synthetic SPX Long

Book Handsome Gains In Synthetic SPX Long

Last week we highlighted BCA’s Risk Appetite Index (RAI) that has catapulted to uncharted territory. While such euphoria has not historically spelled cyclical or structural SPX trouble, it does warrant some near-term caution. Tack on the blockbuster non-farm payrolls and ISM manufacturing releases from last week and this week’s ISM services all-time high print and investors have further stampeded into stocks. Moreover, we recently showed that seasonality would boost the SPX in April before the dreaded month of May. Lastly, the equity put/call ratio collapsed to 0.38 on Monday, the VIX broke 18 and the SPX surpassed our end-2021 target of 4,000 (please look forward to receiving our SPX DDM update scheduled for the April 19 Strategy Report publication). Amidst such exuberance, and given that the 10-year US Treasury yield appears exhausted unable to breakout to fresh recovery highs, we are compelled to book handsome profits in our synthetic SPX long via closing the long $400/$420 call spread short $340 put on the SPY for June expiry for a gain of $8.86/contract or 2850% since the February 11 inception (middle panel). As a reminder, our previous synthetic long netted us $5.41/contract of 676% return as we managed to lock in gains before it fell to $0 at expiry (bottom panel). For clients that want to roll over the synthetic long position and continue to chase this manic market, we would recommend a long $415/$435 call spread with a short $365 put on the SPY for the August expiry at a net outflow of $0.2/contract. Bottom Line: Crystalize gains of $8.86/contract or 2850% and move to the sidelines on the SPX synthetic long position for now, but stay tuned. The SPX is now above our 4,000 yearend target and some near-term caution is warranted.

The global economy has been characterized by divergent recoveries. For example, the IMF’s April World Economic Outlook upgraded its 2021 US growth forecast by 1.3pp to 6.4%, versus the much more muted 0.2pp upgrade to the Euro Area growth forecast of 4.4%.…

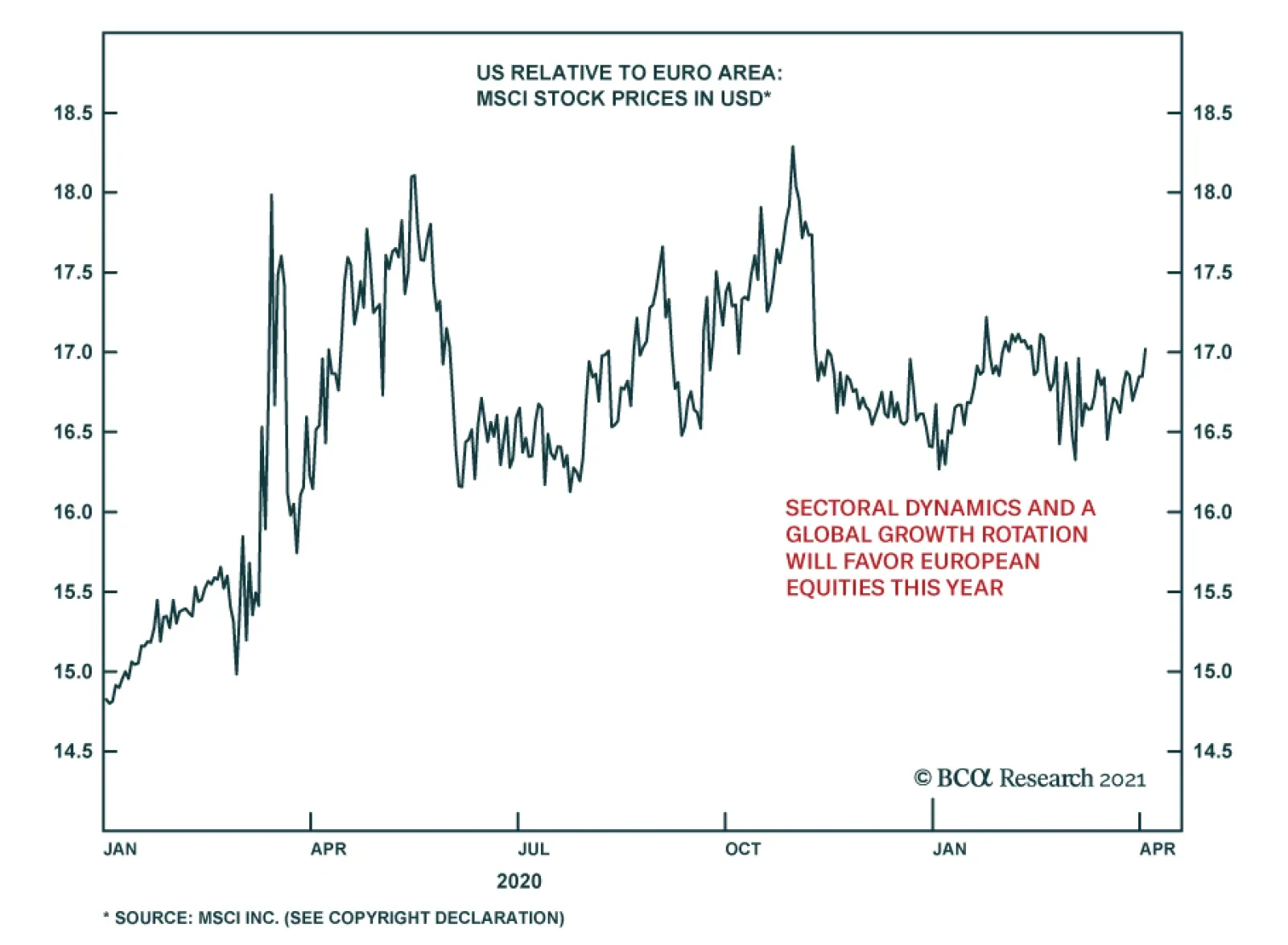

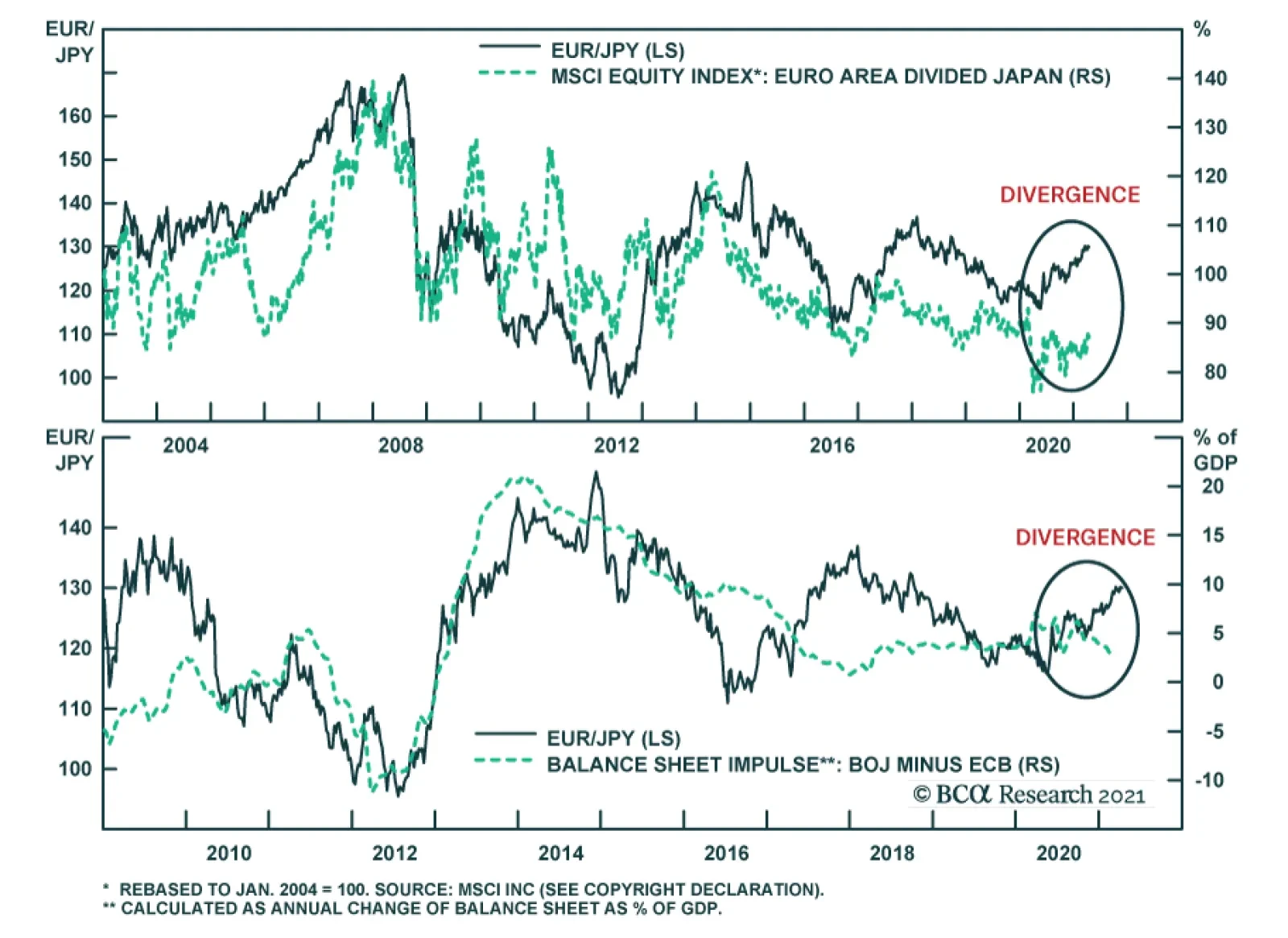

BCA Research’s Foreign Exchange Strategy service concludes that the dollar remains in a sweet spot for now, but it could nonetheless experience violent moves in the coming weeks. Thus, they are opening a short EUR/JPY position as a portfolio hedge. The…