United States

The Philadelphia Fed Business Outlook Survey generated a massive positive surprise. The General Business Conditions Index surged to a nearly 48-year high of 51.8 in March from 23.1 versus expectations of a minute 0.3-point increase. This is mirrored in the…

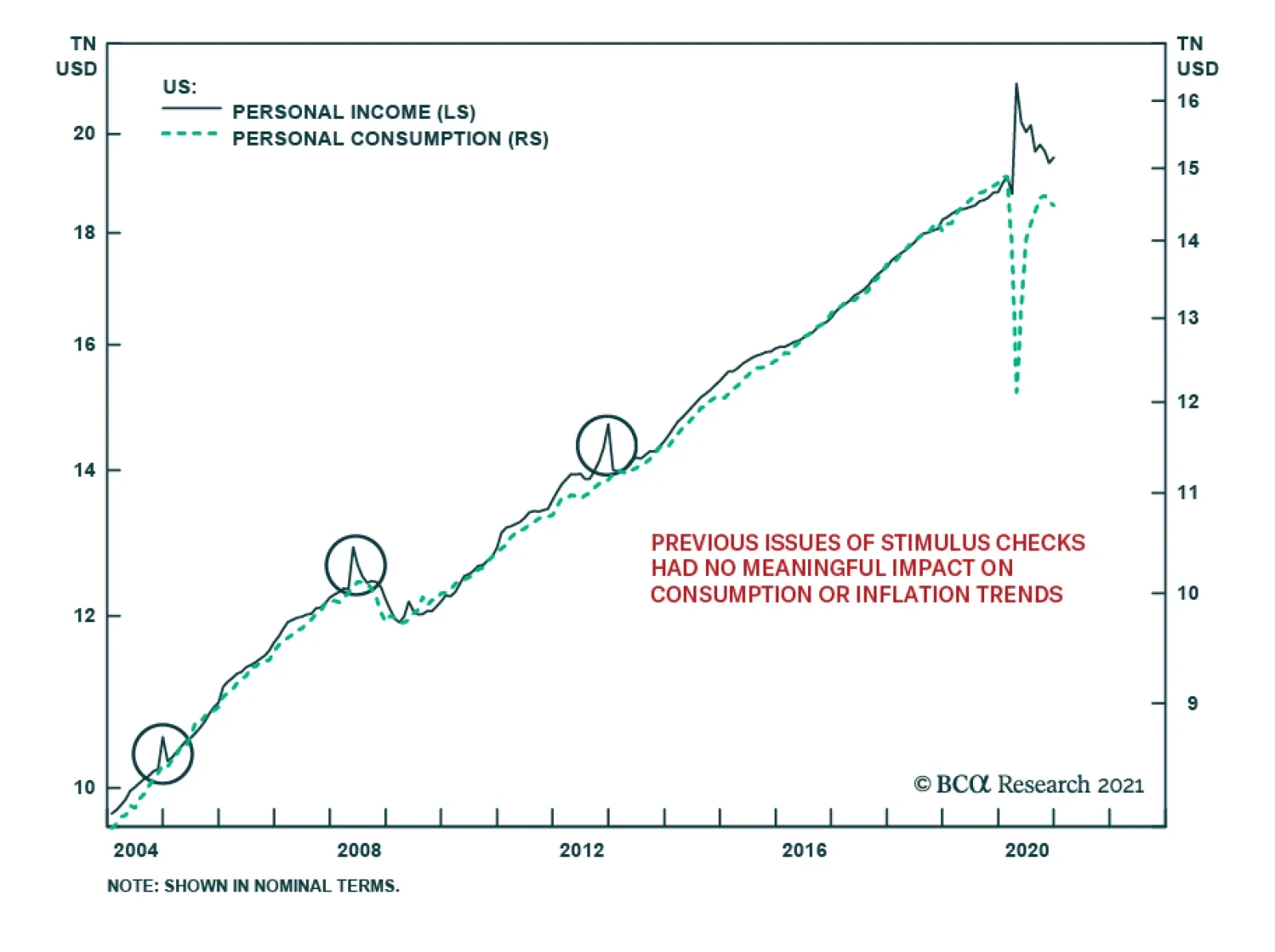

Our newly launched Counterpoint service argues that the inflationary impact of US stimulus checks is exaggerated. Even if social restrictions do fully ease – a big if – the stimulus checks are unlikely to unleash a tsunami of demand. The propensity to…

The pandemic-induced recession surely did hurt earnings, but it also served as a wakeup call to corporate executives as they scrambled to boost business efficiencies. The chart below is showing our proxy (using equally weighted industrials/materials/tech/health care/consumer staples and consumer discretionary) for the degree of operating leverage (DOL) for the broad US equity market. The current reading of just below 2 means that an additional 1% increase in sales translates into a nearly 2% increase in earnings. The fact that DOL has rebounded significantly over the past year from negative territory – where it spent the second half of 2019 likely due to capital misallocation brought by excessive share buybacks – also means that the transmission mechanism from top-to-bottom line growth has been unclogged as corporations cleared out the deadwood. Another message from the recovering US equity market DOL is that the current cycle is just getting started, which also supports our secular 2028 SPX 7000 target. Bottom Line: We remain cyclically and structurally bullish on the prospects of the broad equity market, but are keeping our guard up in the near-term.

Unclogging Earnings Pipes

Unclogging Earnings Pipes

Highlights The American Rescue Plan Act confirms the shift to “Big Government” and proactive fiscal policy in US politics. This sea change in policy is durable for now, given that Democrats can pass one or two more budget reconciliation bills without a Republican vote. Details of forthcoming tax hikes are starting to leak from Washington. Investors should not assume that progressive proposals like a wealth tax, a financial transactions tax, or a minimum corporate tax are dead on arrival. Taxing corporations and the rich is popular. The Republican Party is likely to choose a Trumpian agenda going forward and Trump has a good chance of being the presidential candidate in 2024. But cyclical and structural factors disfavor Republicans at this early stage. Industrials have rallied sharply in advance of Biden’s first law and are now overbought. But we would favor them over health care over a 12-month period, given the macro backdrop and relative policy risks. Feature Were there any surprises in the American Rescue Plan Act (ARPA) signed by President Biden on March 11? Only that some of Biden’s health care and infrastructure agenda slipped into the bill, alongside a provision holding that if states cut taxes and lose revenue, they will lose an equivalent amount in state and local aid. The plan illustrates that the budget reconciliation process is an effective tool for the ruling party to get most of what it wants. The Biden administration will be able to pass one or two more reconciliation bills for FY2022 and FY2023. While the next bills will be harder to pass than the first, and moderate Democratic senators will limit Congress’s options somewhat, the point is that Democrats have just enough political capital to achieve their policy agenda without a single Republican vote. As always, our Political Capital Index is updated in the Appendix and highlights falling political polarization and improving business sentiment, which is positive for Biden’s political capital. Investors will continue to bet on a cyclical recovery but will also become more concerned about tax hikes on one hand and excessive deficit spending on the other. The latter threatens eventually to overheat the economy and speed up the Fed’s rate hike cycle. In this report we conduct a quick recap of the ARPA now that it is official law, we review the tax hike proposals swirling out of the Washington rumor mill, and we update the status of the civil war in the Republican Party. We conclude with a look at industrial stocks, which have rallied tremendously on the back of the cyclical economic upturn (Chart 1) but may still offer some value relative to sectors like health care that face policy risks. Chart 1Cyclical Indicators High On Stimulus

Cyclical Indicators High On Stimulus

Cyclical Indicators High On Stimulus

ARPA Symbolizes The ‘Big Government’ Shift The well-known provisions of the ARPA include: Treasury checks of $1,400 sent directly to individuals who earn less than $80,000 per year; extended unemployment benefits and a renewed federal top-up of $300 per week through September 6, 2021; $65 billion in business aid; and generous funding for various welfare programs such as the expanded Child Tax Credit and larger subsidies for enrollees in the Affordable Care Act health insurance marketplaces (Chart 2).1 Chart 2American Rescue Plan Act

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

In total the US fiscal stimulus amounts to $5 trillion or 23% of GDP since COVID-19 emerged, with $2.8 trillion or 13% of GDP passed since December. It is a gargantuan fiscal stimulus that will supercharge the economy today but lead to a rocky descent once it is exhausted in the coming years (Chart 3). Expiring provisions will occasion political showdowns over whether to make them permanent and how to address waste, corruption, and the long-term budget deficit. Chart 3The COVID-19 Fiscal Blowout

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

The provisions are so far flung that educated American citizens living abroad are reportedly receiving stimulus checks. Nevertheless the bulk of the impact will be felt by low-income people with high marginal propensities to consume. They are the prime beneficiaries of the $850 billion share of the law that funnels cash to individuals as opposed to businesses (Chart 4). This means that at least one-third of the money will be spent, while around two-thirds will be used to pay down debt, enabling consumers to spend more later, according to our Global Investment Strategy. The general effects are very supportive of the recovery. For example, the number of children living in poverty is estimated to fall by 40%, while about one in five renters are expected to catch up on their rent.2 Evictions, bankruptcies, and loan delinquencies will not revive in this context. The total amount of spending is almost twice the size of the output gap, which is now widely expected to be filled by the end of 2022. Chart 4Cash Handouts To Families With High Propensity To Consume

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

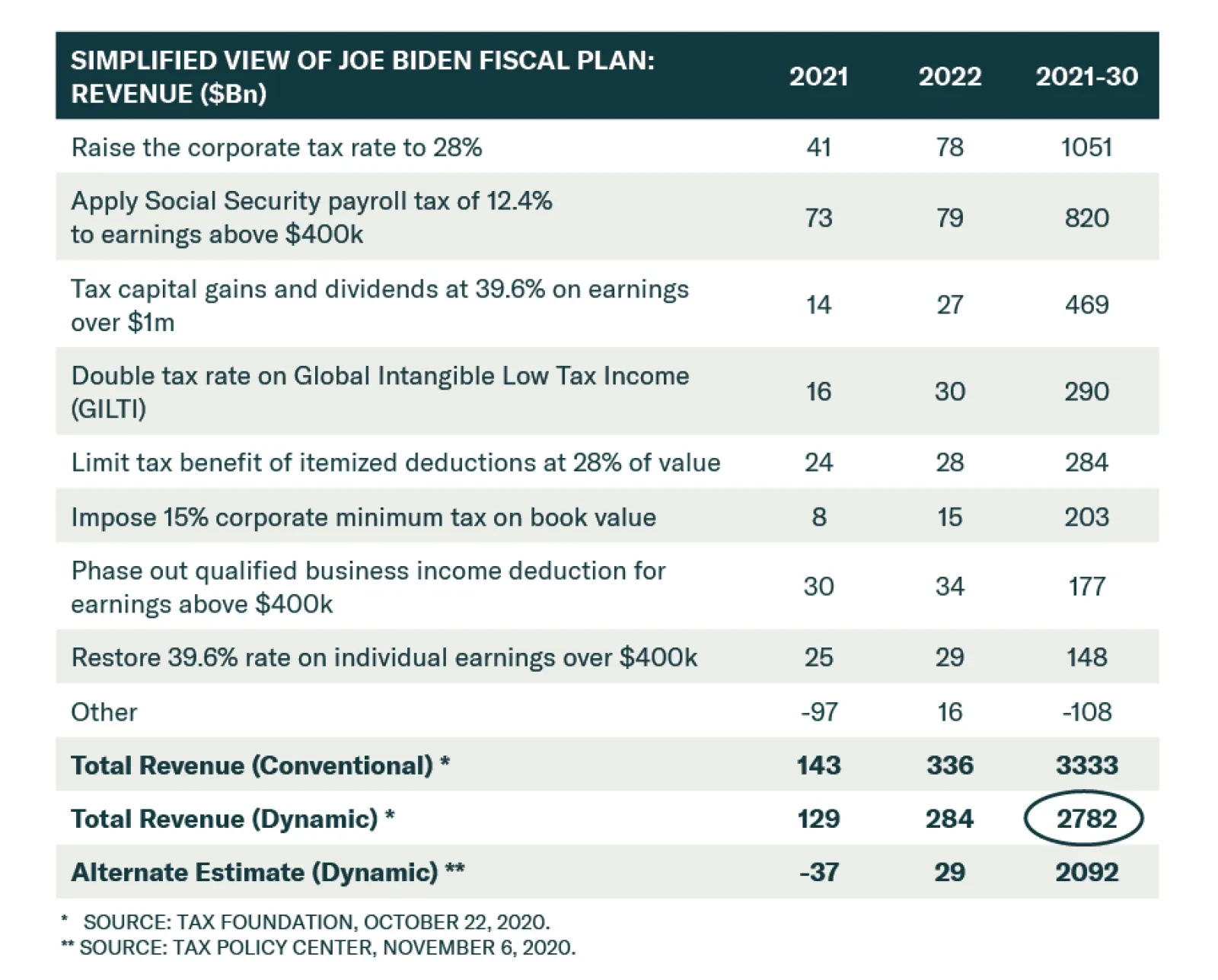

While ARPA mainly consists of short-term cash relief – with pro-productivity investments to come in the reconciliation bill for FY2022 focused on infrastructure and renewables – nevertheless it is not wholly devoid of long-term investment. Each of the 50 states will receive $500 million in aid (more depending on their unemployment rate). Since state and local government revenues are not as dire as expected, some of this money will go into infrastructure, including soft infrastructure like the rural broadband buildout. States will be discouraged from cutting taxes, as mentioned.3 The most important takeaway is that the ARPA will reinforce the shift in public attitudes in favor of a larger government role in the economy. Democrats passed their “liberal wish list” and the result is that a range of constituencies – from those on food and housing programs to those working in the health and education systems – will receive a windfall of federal support. In this way a one-off and probably excessive relief bill will contribute to a sea change in American attitudes toward government. Conservatives and Republicans will still argue in favor of limited government but that is a relative concept and the goalposts just moved. Bottom Line: The ARPA secures the recovery, plugs the output gap, and likely reinforces the shift in public attitudes in favor of a larger role of government in society and the economy. The amount of stimulus is likely excessive, assuming the economy avoids any other bad shocks in the coming years. Hence the law marks a historic shift from reactive to proactive fiscal policy and sets the stage for an inflation overshoot in the long run if not the short run. Yellen Becomes Warren? Not Quite, But Expect Negative Tax Surprises The next budget reconciliation bill is expected to be a 10-year green infrastructure package that will be partially offset by tax hikes. Whether in the same bill, or prioritized above it, we expect Biden to push for his expansion of the Affordable Care Act (only a small part of his health agenda was included in the ARPA). The House will draft its version in April and Biden may sign the final bill into law as early as September or as late as December. We discussed the bill in our March 3 missive. Rumors about the tax proposals are starting to leak out of Washington. At present none of the rumors change the policy consensus, based on Biden’s campaign proposal shown in Table 1. However, they do tentatively support our view that tax hikes will deliver negative surprises to the equity market this year, given that investors have so far been unperturbed by the prospect of higher taxes. Table 1Taxman Cometh

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Secretary of Treasury Janet Yellen raised some eyebrows when she indicated that a wealth tax is being considered by the Biden administration.4 Previously a tax on a person’s (or trust’s) net assets, as opposed to a tax on their income, was the domain of Biden’s progressive-left rivals such as Senators Bernie Sanders and Elizabeth Warren. Warren’s proposal would levy a 2% annual tax on those who possess more than $50 million in net wealth, rising to 3% on billionaires. During the Democratic primary election their proposals were estimated to raise anywhere from $1.4 trillion – if Warren’s proposal met with extreme tax avoidance – to $4.5 trillion, as estimated by Sanders.5 Yellen has also spoken to the finance ministers of France and Germany as part of a diplomatic initiative through the OECD to encourage global participation in a minimum corporate tax rate of around 12%. In exchange for enacting this tax floor, Yellen signaled to the Europeans that she would not insist on providing American Big Tech with a “safe harbor” from Europe’s planned digital tax.6 Whatever ends up happening internationally, the implication is that the Biden administration will push forward with its proposed 15% minimum tax on corporation’s book income. Yellen says that she expects tax hikes to be phased in the latter part of the 10-year budget window for FY2022 so as to make sure that the government’s interest burden is manageable over the long run. She is not concerned about excess deficits or debt in the short run, as they are related to the pandemic relief and economic recovery and interest rates are below the nominal growth rate of the economy. But she has endorsed passing tax hikes for later in the decade, as did both President Biden and Vice President Kamala Harris on the campaign trail. Several of the more ambitious tax proposals face limitations in Congress. Moderate senators like Joe Manchin of West Virginia have raised objections to a large tax hike during trying times. He might be joined by other moderates like John Tester of Montana and the four narrowly elected senators from Arizona and Georgia. However, while these moderates will keep the tax agenda in check, it is important to understand their position. None of these senators are against tax hikes in principle – that would be a Republican stance. They are against tax hikes that increase the burden on the middle class or jeopardize the economic recovery. From that point of view Biden’s proposals are fairly palatable: the highest individual income tax bracket would go back to where it stood in 2016, the corporate rate would go halfway (at most) to its pre-Trump level, and the estate tax would be restored. These proposals focus on big corporations and the wealthy and are likely to be watered down in negotiation, so we would not rule out moderate Democratic support. Investors should not rest easy about the tax agenda until more information is known. Negative surprises are likely. The consensus is that the Democrats will not pass a wealth tax, or a “Wall Street tax” on financial transactions, or other progressive proposals. But these taxes would be popular and politically defensible – some polls even show a majority of Republicans supporting a wealth tax. Therefore these taxes cannot be ruled out in advance.7 Bottom Line: The tax debate is underway and our expectation of negative surprises is looking more, not less, likely. How Will Republicans Respond To The Big Government Onslaught? Republicans have duly retreated to the political wilderness after their election loss and the January 6 Capitol Hill riot. The critical question is whether and how they will regroup to contest future elections – the deeper their divisions, the more certain Democratic policy becomes. At the center of this question is whether the Republican Party will adopt Trumpist policy and whether Trump himself will continue to be the flagbearer and presumptive nominee for the presidential election in 2024. Our answer is that the Republicans will adopt a Trumpist agenda of tough trade and immigration policies combined with fiscal largesse but they will struggle over Trump himself and how to broaden their base. Every election is unique. COVID-19 reinforces the point. There is a clear case to be made that Trump would have won the election if not for the pandemic and recession. We favor this view given how narrowly he lost in the midst of the crisis. But there is also a clear case to be made that he would have lost anyway.8 The problem for the Republicans going forward is that cyclical and structural trends work against them. Cyclically, the economy should be in full stride in 2022-24 and the Federal Reserve is highly likely to play a supportive role. This may or may not prevent the usual midterm opposition gains but it will make it very hard for an opposition presidential candidate to win. True, Democrats will not have a full incumbent advantage if President Biden passes the baton to Vice President Harris. Inflation and other problems will emerge. But given the timing of the pandemic, election, and vaccine, voters will probably be much better off in four years than they were last November, which is the most reliable prediction of whether the incumbent party will stay in power. Structurally, demographic change in America diminishes Trump’s base. A generational shift is transforming the American electorate, as the Silent Generation, which is the most reliably Republican, passes on (Chart 5). Millennials favored the Democratic Party by 6% in the 2020 election (10% in Georgia and 21% in Pennsylvania). Chart 5Generational Shift A Risk To Unreconstructed Republicans

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Ethnic minorities also skew Democratic, generally speaking, and are taking a much larger share of the electorate, especially in critical swing states – as highlighted by Biden’s victories in Arizona and Georgia (Chart 6). Hispanics favored Biden by 33% (24% in Arizona). Chart 6US Demographics Drive Political Change

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Demographic extrapolations by the Center for American Progress show that even if post-Millennial generations grow more conservative over time, the Electoral College will shift inexorably against the Republicans as long as current trends continue (Chart 7). Chart 7Electoral Math Frowns On Republicans Even Without Generational Shift

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Demographics are not destiny: Trump would never have won in 2016 if projections based on age and race were so predictive. Yet Republicans cannot merely wait on cyclical or exogenous events to discredit the Democrats. The electoral math is devastating if they do not broaden their appeal. Their quandary is that generating enthusiasm among their base of white voters with less formal education may exclude the very groups to whom they need to appeal: suburban women, educated whites, and ethnic minorities. The immediate question is what to do about Trump, who has divided the party over the Capitol riot, culminating in seven Republican votes against him in his second impeachment. On the surface the Republican Party is a much older entity than any single member or leader and can therefore play a longer strategy. It could choose the correct electoral strategy of courting independents, women, and Hispanics even if it meant losing an election or two due to divisions with the Trumpists. The problem is that Trump’s personal following is uniquely threatening to the viability of the party. Trump alone could split the Republican Party and nullify its chances in 2022-24 and beyond. Trump has suggested starting his own party, the Patriot Party. Opinion polls show that 46% of Republicans would join it while only 27%would insist on sticking with the Republican Party (Chart 8). Even if a Trumpist party stole only 2-3% of Republican voters it would be enough to ensure a Democratic victory in any election given the very small margins of victory in swing states in recent decades. Trump would easily spoil the Republican bid, just as Ross Perot did in the 1990s, Robert La Follette did for the Democrats in the 1930s, and Theodore Roosevelt did in 1912 (Table 2). As Senator Lindsey Graham said of Trump and the Republican Party, after holding post-election negotiations with the former president: “He can make it bigger. He can make it stronger. He can make it more diverse. And he also could destroy it.”9 Chart 8Trump Could Start Third Party, Give Democrats A Decade-Plus Ascendancy

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table 2Major Third Party Breakaway Candidates Undercut Their Former Party

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

So What Will Republicans Do? We conducted an exercise using game theory to determine the likeliest strategy that Trump and the party will take. We used the famous “Prisoner’s Dilemma” as our template because both sides have a lot to gain if they cooperate and a lot to lose if not.10 But they do not trust each other. And each side will lose the most if it stays true while the other betrays it, worsening the distrust. Diagram 1 shows the outcome. Republicans could win eight years in the Oval Office if they adopted Trump’s agenda yet put forward a young new candidate with Trump’s personal endorsement; or they could win four years if they chose Trump himself (the constitutional limitation). By contrast, if they chose an establishment Republican agenda, they could win eight years (reduced to four in Diagram 1 because less likely) or zero years if Trump opposed. Trump, for his part, would win zero years if he bowed out to support the Republicans regardless of whether they adopted his agenda, but he would have a chance of winning four more years if he ran at the head of a Trumpist Republican Party. The outcome is that the Republicans will adopt Trumpism while Trump himself could easily run for president again, given his sway over the party. Diagram 1Game Theory Says Republicans Will Court Trump

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

The game works out the same way if we assign minimal positive payoffs (e.g. one point for a win, zero points for a loss), various other probability weighted payoffs (50% chance of winning), or negative payoffs for time spent out of power. In each variation a stable equilibrium emerges in which Republicans adopt Trump’s agenda and Trump runs again in 2024. Of course, if one changes the structure of the game or assigns subjective scores a different outcome can be produced. But the clearest and most logical games all produce the same outcome: Trump 2024. This view fits with the consensus in online betting markets. According to the bookies, Trump has between a 20% and 35% chance of running as the Republican nominee in 2024. The same markets give Republicans a 44%-50% chance of winning the White House that year. At this early stage we would take the “over” on Trump and the “under” on a GOP victory given the above points about the cyclical and structural factors weighing against Republicans (Chart 9). Our quantitative US election model, which produced the correct result for all states except Arizona, Georgia and Michigan in 2020, gives the Republicans a 44% chance of winning in 2024 but that number will fall sharply as the economy improves. Chart 9Trump's Odds Of Winning The Republic Nomination In 2024

Trump's Odds Of Winning The Republic Nomination In 2024

Trump's Odds Of Winning The Republic Nomination In 2024

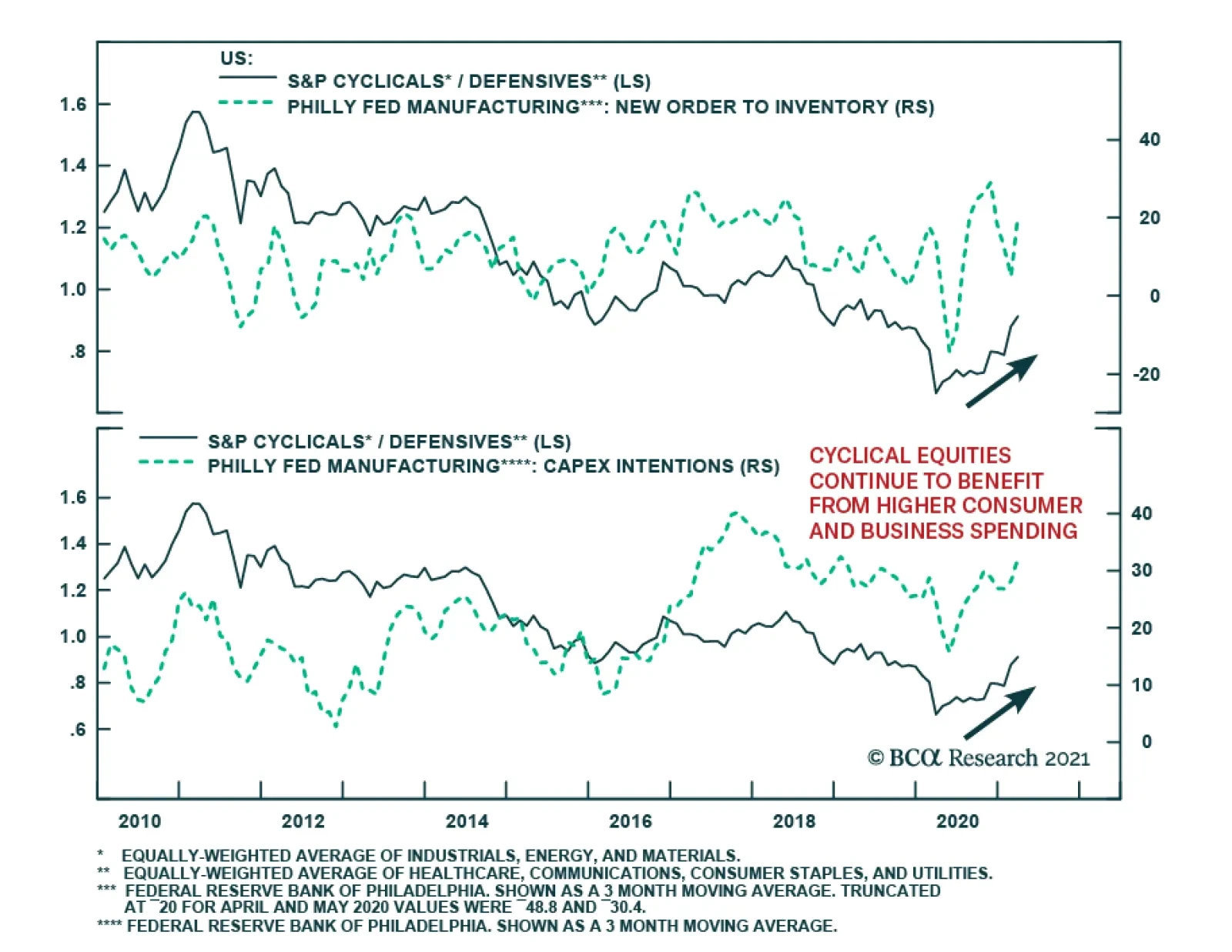

What might change this outcome, according to game theory? Republicans could offer a powerful sweetener to convince Trump to bow out of the race and support the party’s candidate, such as letting one of his children or his son-in-law Jared Kushner run in his place. Alternately Democrats could increase the danger to Trump of their winning again, perhaps by threatening to throw him in jail. Otherwise Trump may not be sufficiently convinced of his party’s loyalty, or frightened of Democratic rule, to bow out of the race. We are never beholden to game theory and there are countless real-world ways in which the 2022-24 election outlook could change. But as things stand today, Republicans are highly likely to adopt Trump’s agenda. Trump may or may not do what is best for the party. He is unpredictable and at critical junctures over the past year he has not done so. He could start his own party just for the fun of it and in doing so break the party of Lincoln. This irrational factor creates an imbalance in the game that the Republican Party will be anxious to prevent, reinforcing its likely decision to adopt his agenda and let him seek the nomination freely. If the Republican Party does split, officially or unofficially, the Democrats will be guaranteed to expand their hold on Congress in 2022 and keep the White House in 2024. Note that Republicans would normally be heavily favored to retake the House of Representatives in 2022, though not the Senate, so such an outcome would be a political earthquake. A Democratic ascendancy could last for more than one election cycle: Republicans held the White House from 1980-92 and Democrats held it from 1932-52. Since we cannot reliably forecast Trump’s individual behavior, we cannot rule out a deep Republican rift. On the other hand, while the demographic trends point to Democratic rule out to 2036 and beyond, no Democratic ascendancy would last that long, given economic cycles, international threats, and the inevitable corruptions of single-party rule. But policy uncertainty would collapse over the 2022-24 cycle, pushing the timing of major policy change to 2026 or later. Investors would face a high probability that a sweeping Democratic agenda would be enacted, even assuming the persistence of checks and balances provided by moderate Democratic senators and the judicial branch. One clear implication is that financial markets may not evade the risk of negative regulatory and tax surprises over the long run even if they manage to do so in the FY2022 and FY2023 reconciliation bills – which we doubt. Bottom Line: Republicans cannot win the White House in 2024 without Trump’s popular base, even though they would prefer to have a fresh face capable of expanding that base. Trump cannot win without the Republican Party but he can unpredictably decide to do something other than win, i.e. endorse a Republican successor or start a third party. As a result a true Republican split cannot be ruled out. Meanwhile Republicans will have to court Trump rather than vice versa. Democratic policy is well ensconced for now, an underrated risk to the equity market. Investment Takeaways We know that Democrats are pushing forward on their legislative agenda and capable of passing one or two more budget reconciliation bills. We know that cyclical and especially structural factors will put Republicans at a disadvantage in the 2024 presidential race and possibly even the 2022 midterm. We also know that the Republican Party has a non-negligible risk of fracturing due to Trump’s personal following and unpredictability. These points suggest investors should not bet against the current policy setup. The macro backdrop favors cyclical sectors such as industrials, energy, materials, and financials. In our US Political Risk Matrix we have highlighted that the policy backdrop is especially beneficial to industrials (Appendix, Table A1). This is reinforced by ARPA and Biden’s forthcoming reconciliation bills on infrastructure and green projects, subsidies for domestic production, and simultaneous attempts to reduce trade tensions with US allies and partners – if not with China. Of course, industrials have rallied enthusiastically alongside a sharp rebound in core durable goods orders, a more gradual improvement in non-residential capital expenditures, and an environment in which capex intentions will respond to a general domestic and global upswing (Chart 10). A weak dollar, premised on a global recovery, excess liquidity, lower interest rates for longer, and large budget and trade deficits, also favors the industrial sector and reinforces the recovery in global trade and growth. Rising commodity prices are driven by supply constraints as much as global demand, as our Commodity & Energy Strategy has showed in depth, and help to restore pricing power to industrial firms (Chart 11). Chart 10Industrials Outperform On Recovery And Stimulus

Industrials Outperform On Recovery And Stimulus

Industrials Outperform On Recovery And Stimulus

Chart 11Commodity Boom Supports Industrials' Pricing Power

Commodity Boom Supports Industrials' Pricing Power

Commodity Boom Supports Industrials' Pricing Power

Hence the good news is largely priced into industrials, which are tactically overvalued according to our BCA valuation indicator. The sector looks more or less expensive on all valuation metrics other than price-to-sales (Chart 12). Therefore the best value must be sought on a relative basis, where industrials are outperforming communications services and just beginning to outperform the superstars, tech and health care. From a policy point of view, health care is one of the biggest losers of the Biden administration, which aims to expand health insurance coverage and reduce drug prices. This may be for the benefit of society but it comes at the expense of old cash cows. Investors should stay guarded against a near-term correction in industrials due to looming tax hikes but strategically favor them over health care and tech (Chart 13), which are even more vulnerable to higher taxes. We will execute this trade by going long against health care over a strategic time frame. Chart 12Industrials Overvalued On Most Measures

Industrials Overvalued On Most Measures

Industrials Overvalued On Most Measures

Chart 13Favor Industrials Over Health Care

Favor Industrials Over Health Care

Favor Industrials Over Health Care

Industrials also have a favorable profile against consumer discretionary stocks but we maintain a positive outlook on the US consumer in an era of government largesse. Our Geopolitical Strategy has also highlighted that Great Power struggle will prevent the Biden administration from cutting defense spending – another boon for industrials. Instead it will have to increase spending for defense as well as supply chain resilience and research and development in the midst of a cold war with China. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1Political Risk Matrix

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A2Political Capital Index

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A3APolitical Capital: White House And Congress

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A3BPolitical Capital: Household And Business Sentiment

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A3CPolitical Capital: The Economy And Markets

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A4Biden’s Cabinet Position Appointments

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Footnotes 1 Garrett Watson and Erica York, “The American Rescue Plan Act Greatly Expands Benefits Through The Tax Code In 2021,” Tax Foundation, March 12, 2021, taxfoundation.org. 2 Committee for a Responsible Federal Budget, “American Rescue Plan Act Will Help Millions And Bolster The Economy,” March 15, 2021, cbpp.org. 3 See footnote 2 above. 4 Paul Kiernan and Catherine Lucey, “Yellen Says Biden Administration Undecided On Wealth Tax,” Wall Street Journal, wsj.com. 5 Kyle Pomerleau, “How Much Revenue Would A Wealth Tax Raise?” On The Margin, American Enterprise Institute, April 20, 2020, aei.org. 6 Jeff Stein, “Yellen pushes global minimum tax as White House eyes new spending plan,” Washington Post, March 15, 2021, washingtonpost.com. 7 Howard Schneider and Chris Kahn, “Majority of Americans favor wealth tax on very rich: Reuters/Ipsos poll,” Reuters, January 10, 2020, reuters.com; Matthew Sheffield, “New poll finds overwhelming support for an annual wealth tax,” The Hill, February 6, 2019, thehill.com. 8 A recession could have happened as a result of the cyclical slowdown from the trade war, which hurt the Midwestern swing states. The yield curve had inverted and the economy’s margin of safety was low. There would not have been any fiscal stimulus without the pandemic. 9 James Walker, “Lindsey Graham Warns Donald Trump Could ‘Destroy’ GOP After Combative CPAC Speech,” Newsweek, March 8, 2021, newsweek.com. 10 The Prisoner’s Dilemma involves two prisoners detained separately and pressured into confessing their crimes. If they both stay quiet, nothing can be proved and they only spend one year in jail. If they both confess, they are proven guilty and both spend five years in jail. If only one of them confesses while the other stays silent, the confessor goes scot free while the other spends 20 years in jail! The incentive is to confess. The equilibrium is for both to confess. The traditional game reveals the benefits of trust as well as the difficulty of maintaining it in isolation and doubt.

US Treasurys sold off on Wednesday morning, with the 10-year Treasury yield making a new intraday pandemic high and the 2/10 yield curve steepening ahead of the conclusion of the Fed meeting. The subsequent Fed message soothed the market and US equities…

BCA Research’s US Political Strategy service concludes that the tax debate underway in Washington makes a tax shock increasingly likely. Rumors about the tax proposals are starting to leak out of the White House. At present, none of the rumors change the…

Monitoring China Closely

Monitoring China Closely

Deterioration in Chinese data pushed us to downgrade the cyclical/defensive portfolio bent from overweight to neutral last month (third panel), and today we highlight yet another warning shot originating across the Pacific Ocean. Bloomberg’s compiled China High-Frequency Economic Activity Index (CHFEAI) has downshifted since peaking last December, warning that investors should keep their “China” guard up. The CSI 300 is following down the path of the CHFEAI (second panel), and the risk is that the S&P 500 may be next in line (top panel), as it has closely tracked China, albeit with a slight lag, since COVID-19 hit, as we first showed in our December 21, 2020 Special Report. Tack on the absence of an SPX valuation cushion, and there are rising odds that select deep cyclical/highly levered/China exposed sectors will start to sniff out some China trouble. Bottom Line: The S&P 500 is nearly perfectly priced and at a spitting distance from our 4,000 end-2021 target. China’s slowdown, especially post the 100 year Communist Party anniversary this summer, remains a key macro risk to monitor and can serve as a catalyst for an SPX correction.

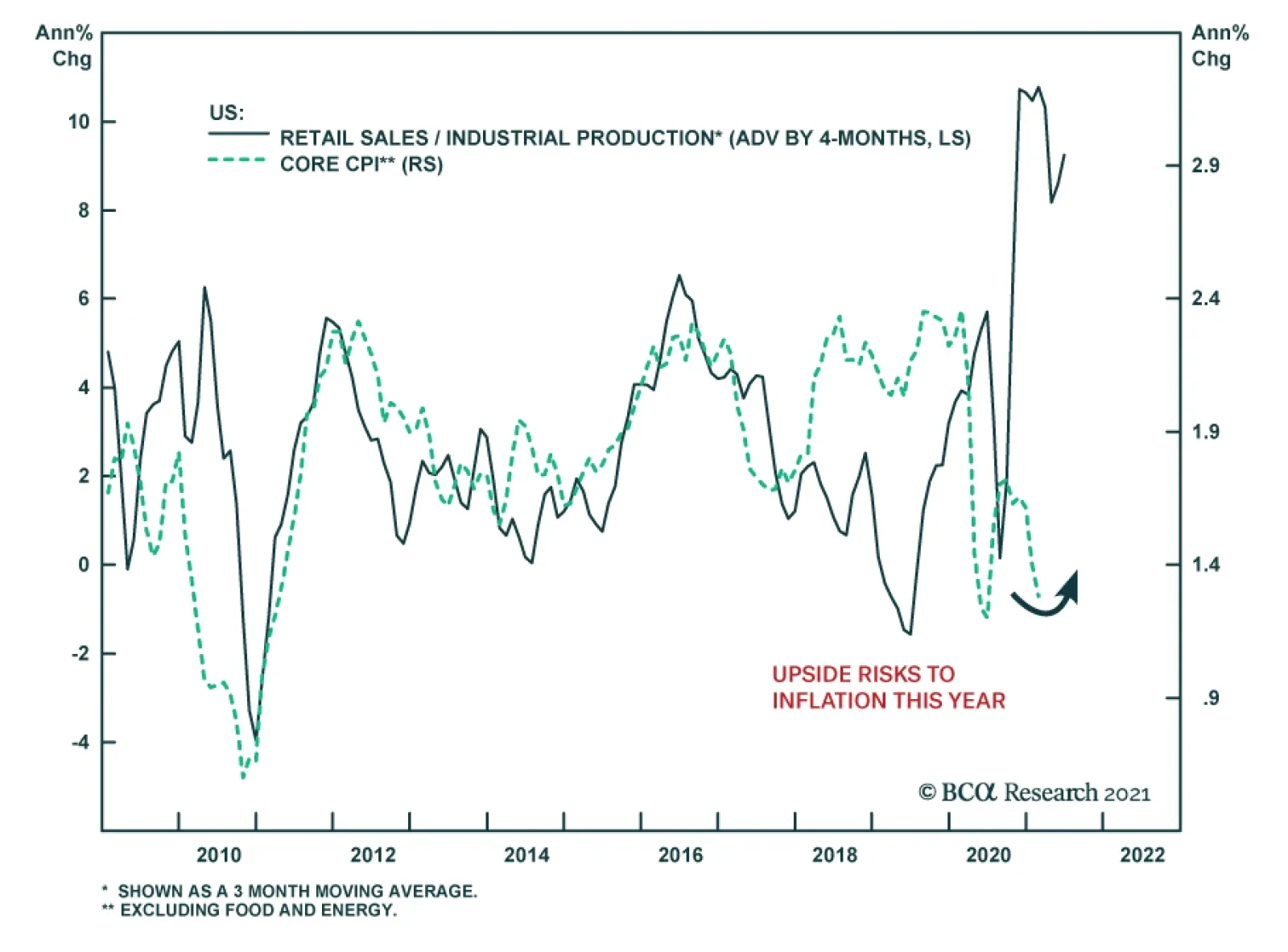

US industrial production and retail sales disappointed in February, declining versus January and falling short of expectations. The industrial production release shows a decrease in output across all major market groups, amounting to a 2.2% drop versus…

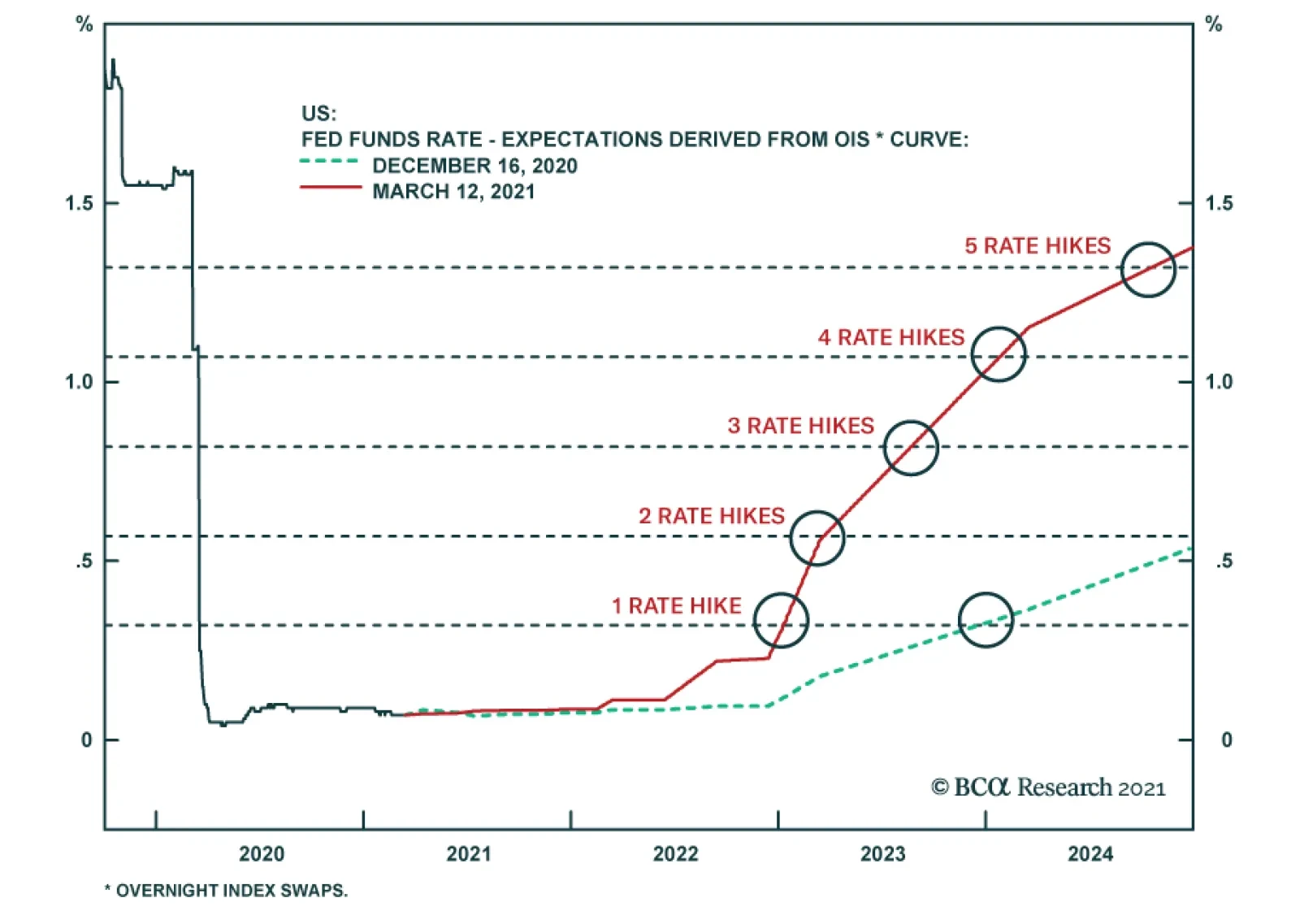

BCA Research’s US Bond Strategy service concludes that the Fed will revise up its interest rate forecasts at Wednesday’s meeting; nonetheless, the new forecasts will remain more dovish than the current market pricing. The market’s fed funds rate…

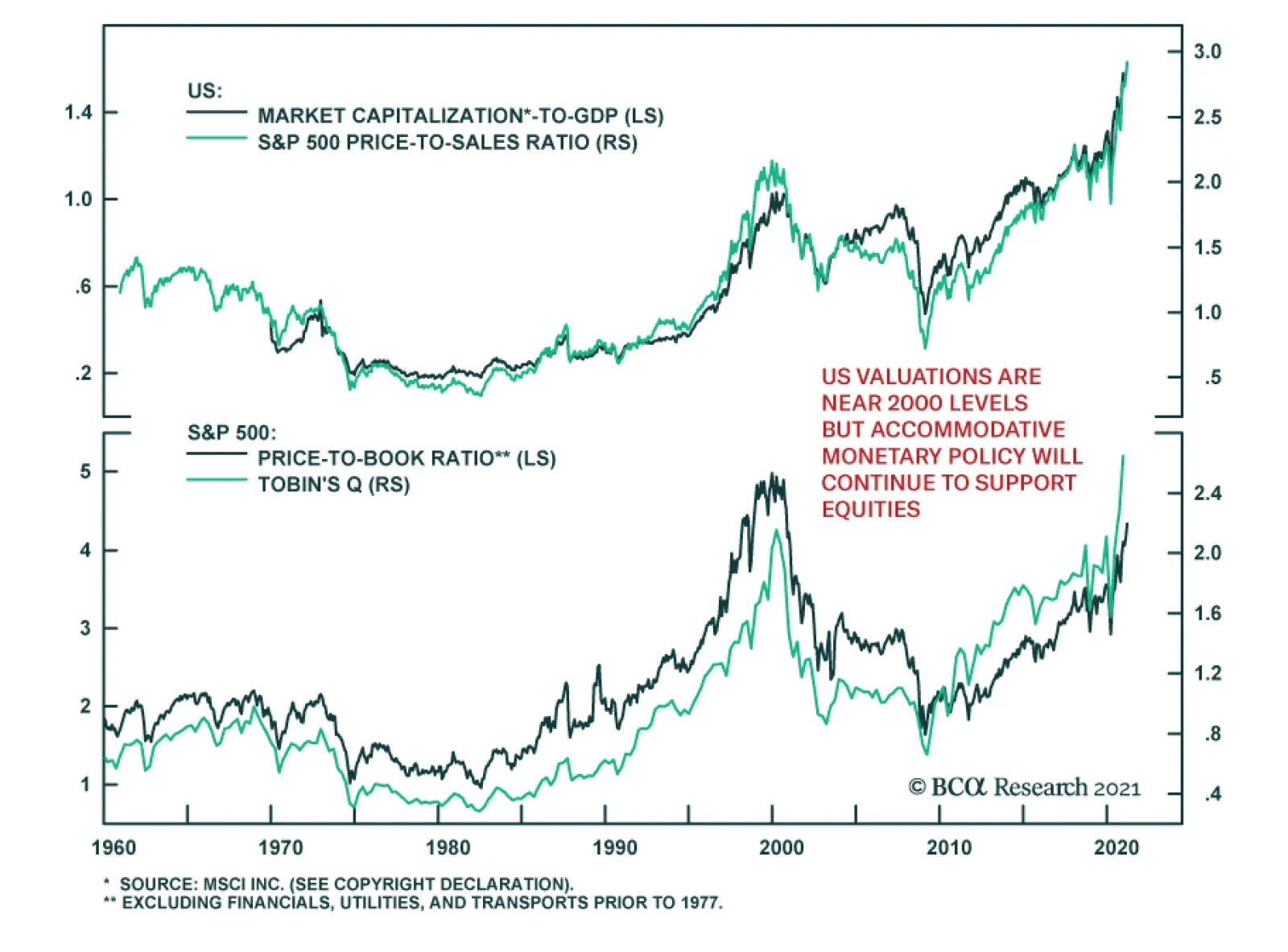

As US equities keep reaching new highs, many parallels are being drawn with the situation in 2000. The simplest one has to do with valuations. Valuations reached nosebleed levels in 2000. While the forward P/E ratio on the S&P 500 is somewhat below its…