United States

Our Portfolio Allocation Summary for May 2026.

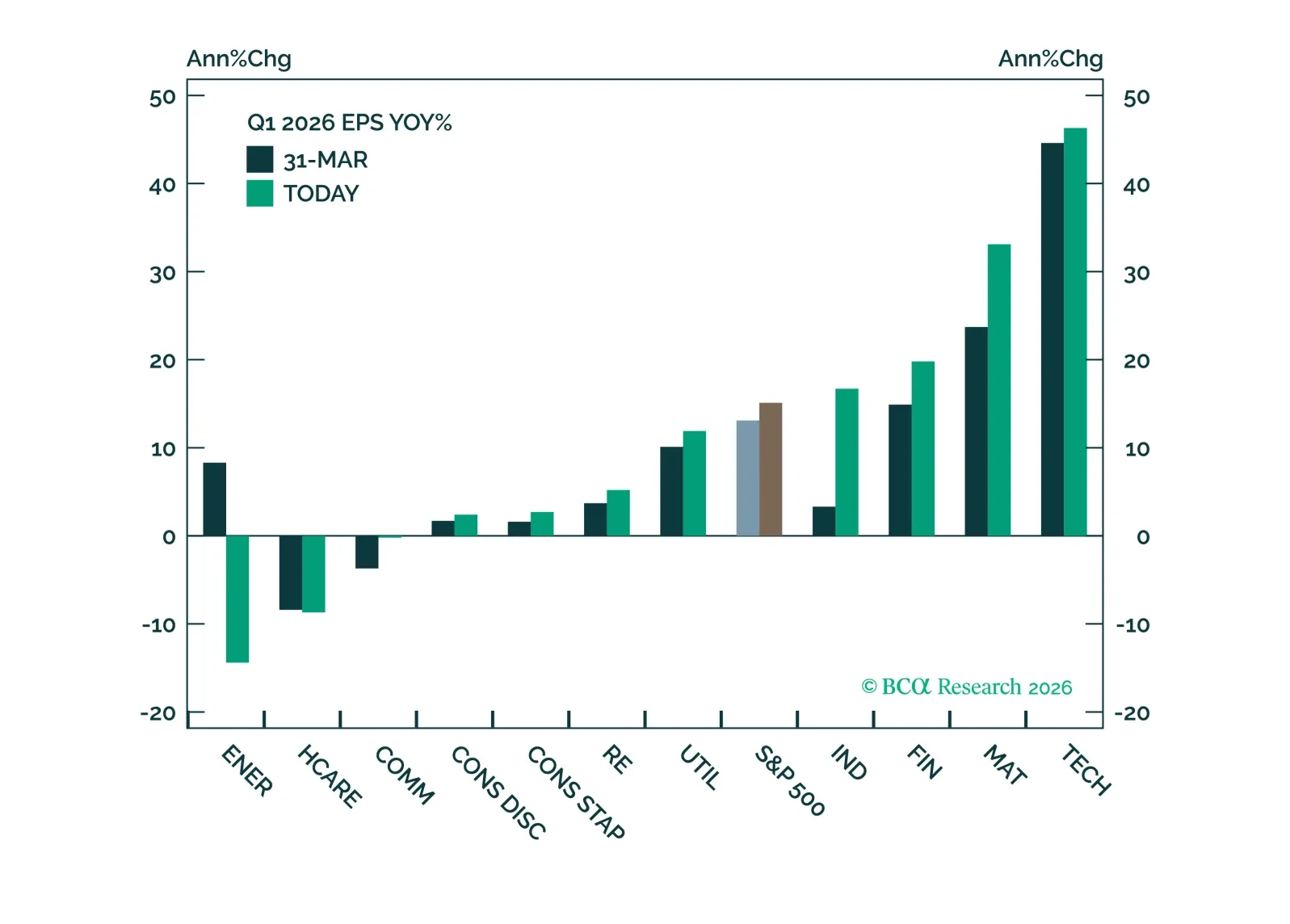

Leadership has rotated toward investment-driven sectors, reflected in both EPS growth and price performance. Expanding margins suggest the cycle may have longer to run, as productivity gains start to work their way through fundamentals. We continue to see upside for the S&P 500, with no change to our sector outlook.

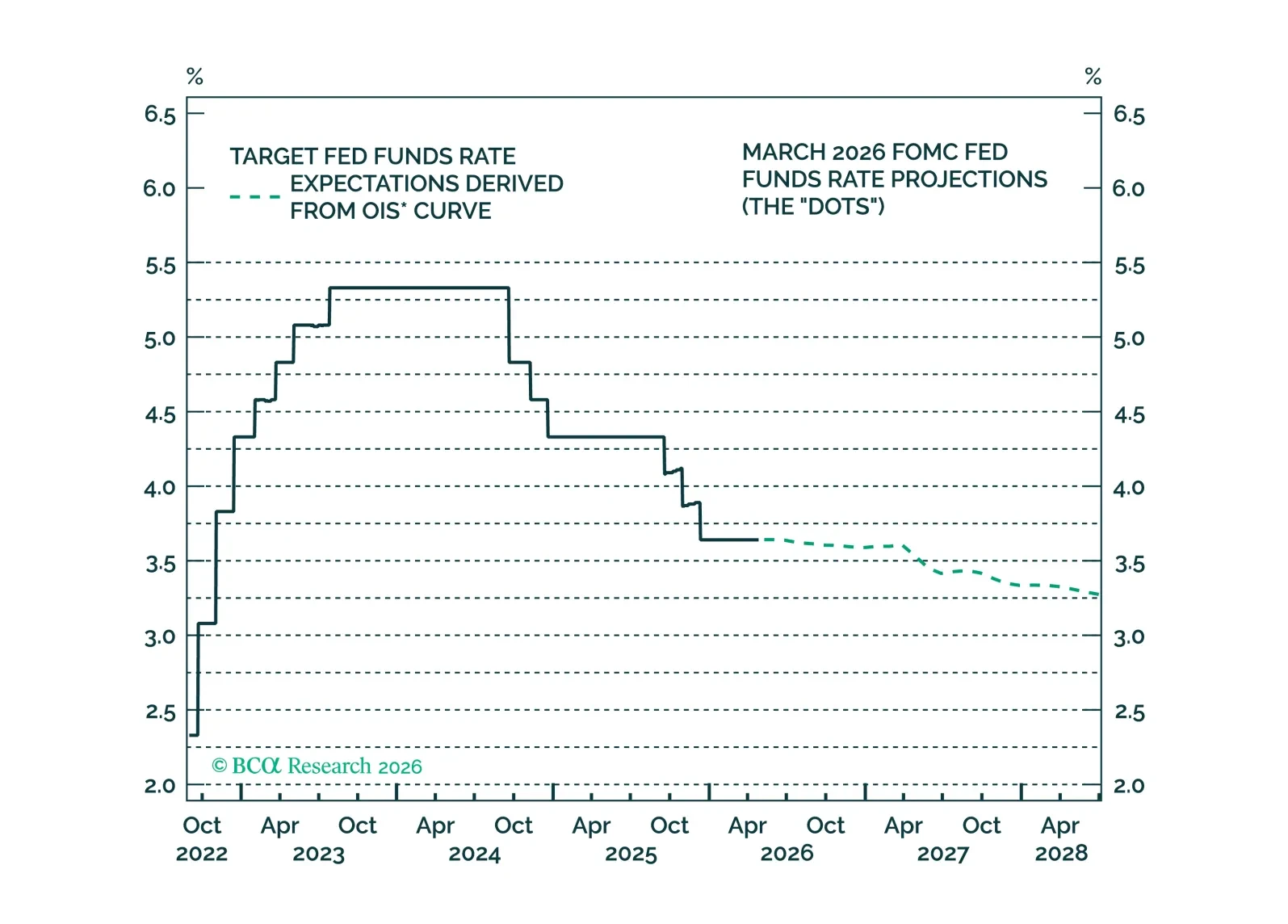

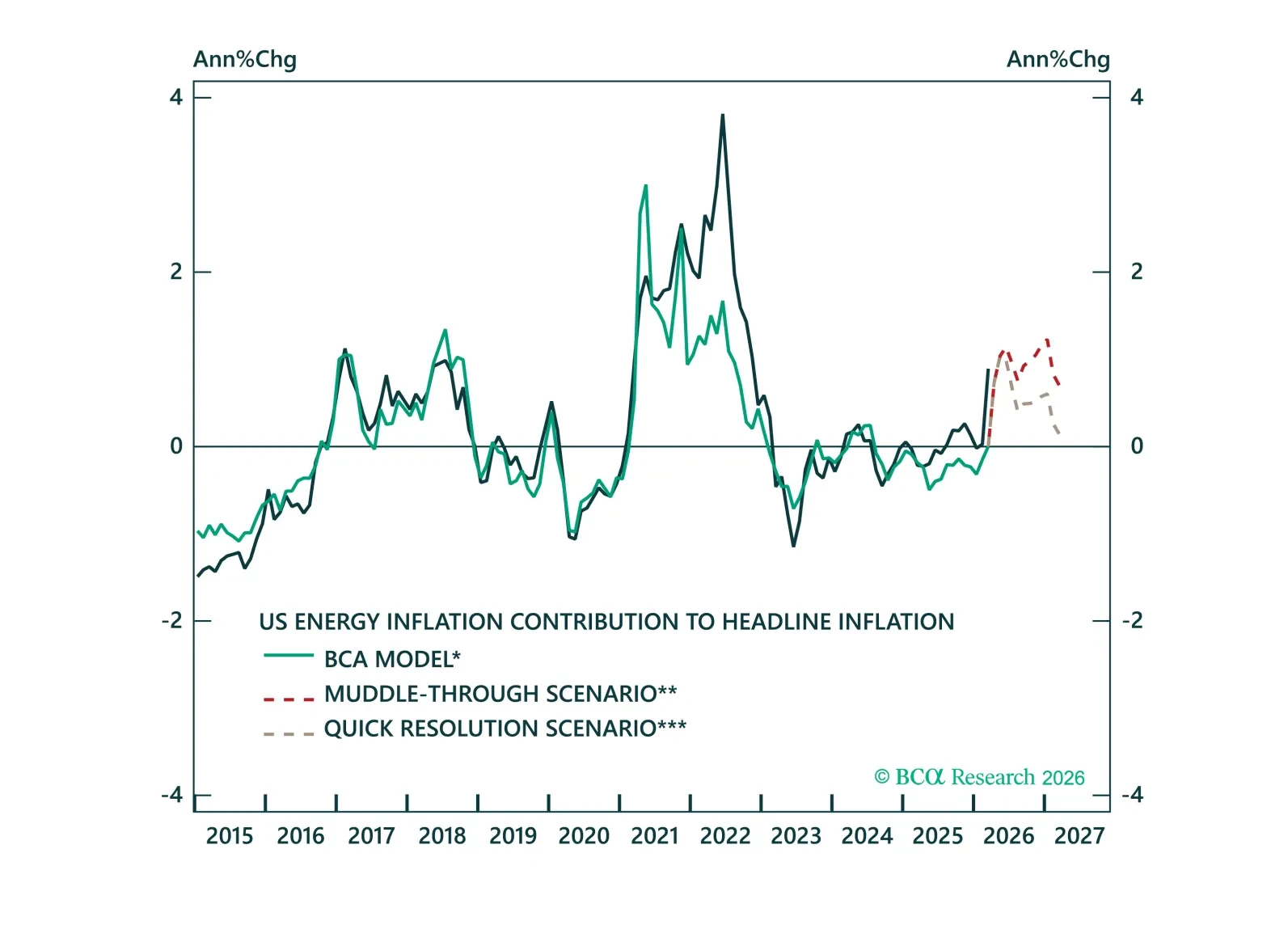

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.

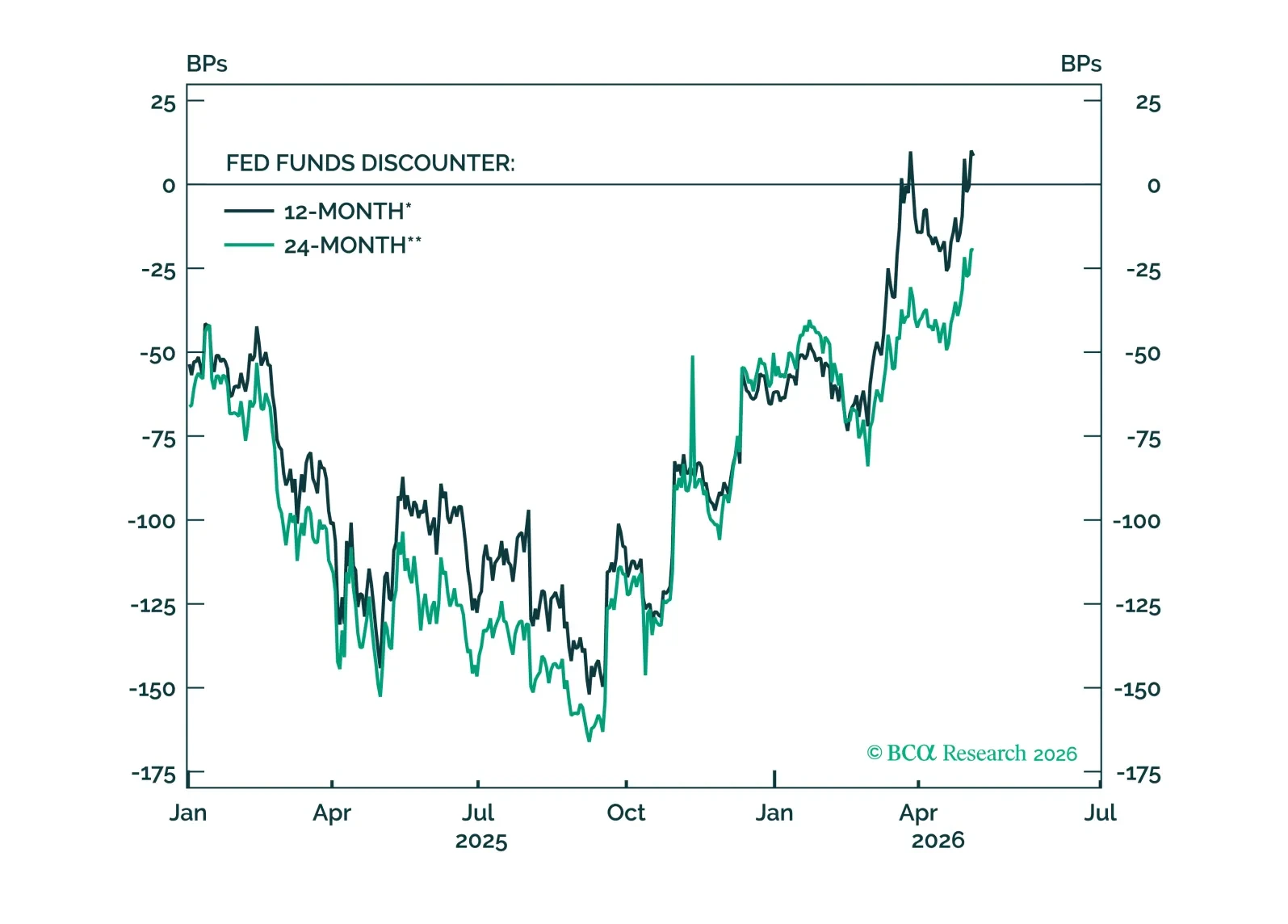

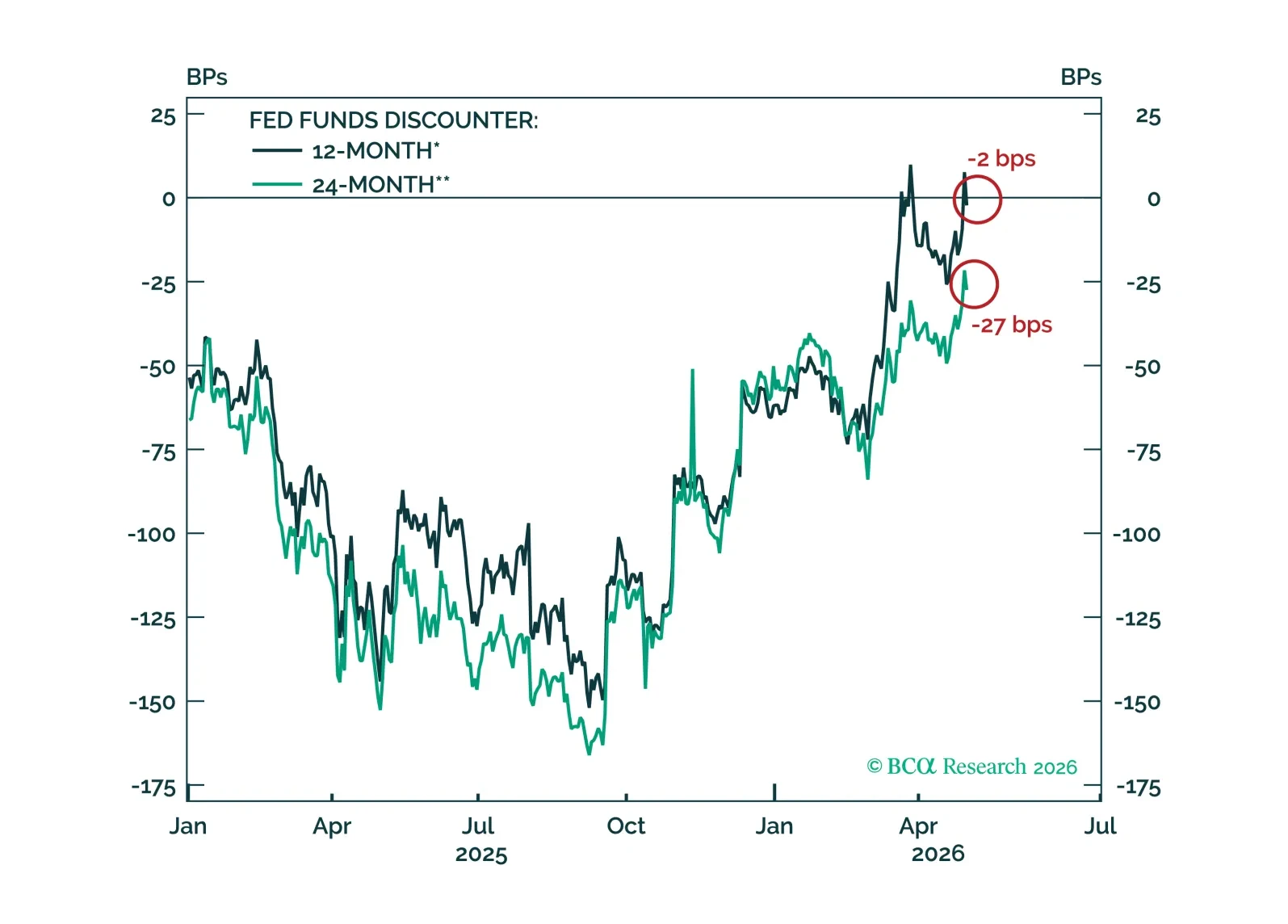

FOMC participants are coalescing around the idea that the funds rate will stay on hold for some time, an outcome that is now well priced in the bond market and that will not materially change under a new Fed Chair.

The S&P 500 finished last week at an all-time high as optimism over earnings has pushed the Iran conflict out of the spotlight. Despite uncertainty in the Strait of Hormuz, we do not think investors have enough evidence to justify underweighting equities and other risk assets.

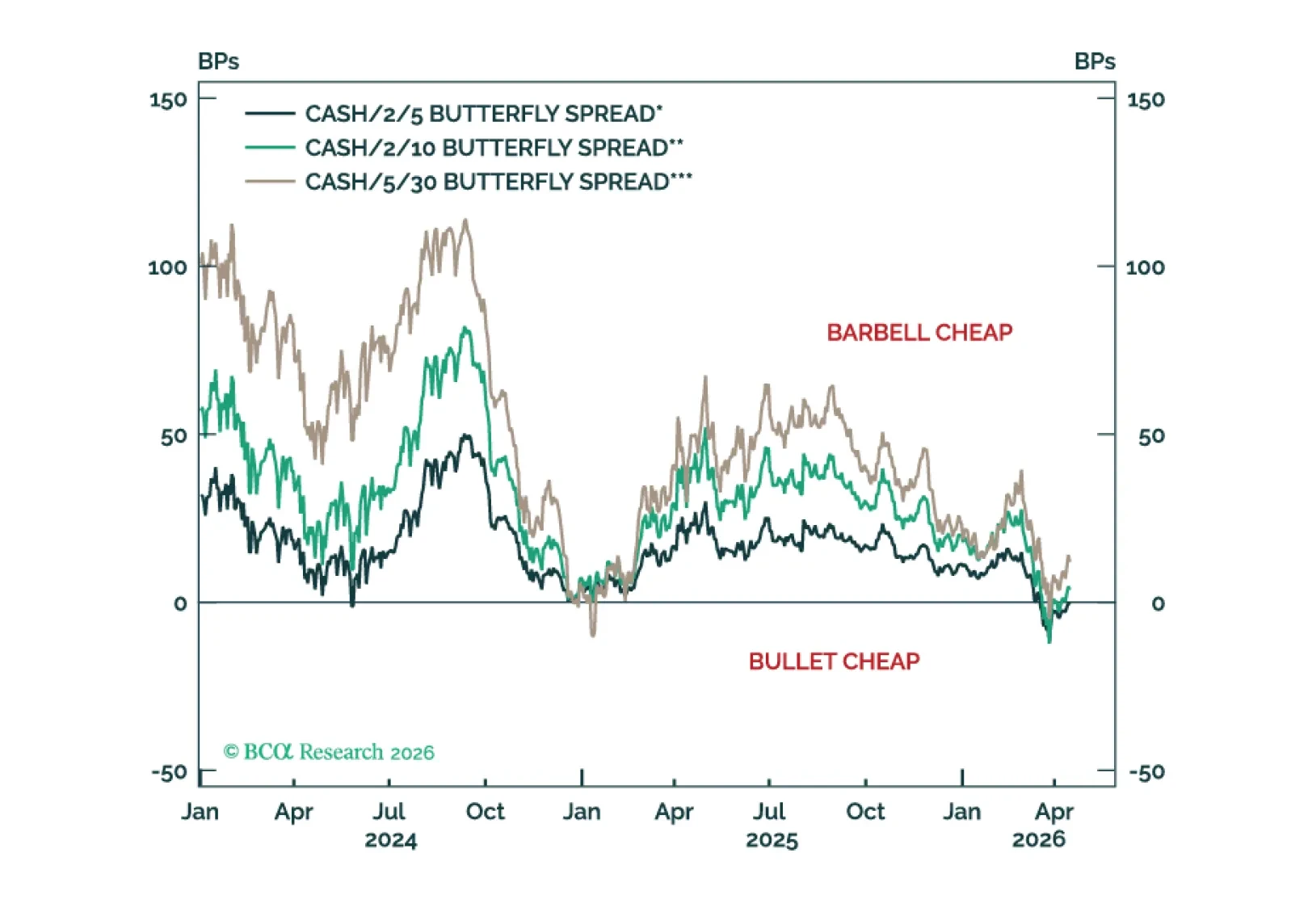

We recommend increasing exposure to spread product as the US economy transitions back into a low rate vol regime.

The S&P 500 rally is likely more than just risk-relief. Market internals reflect strengthening economic growth and higher inflation, with support coming from robust earnings. Tight financial conditions have compressed valuations, particularly within the Tech sector. We are initiating a long Software trade ahead of earnings season, given that multiples have declined and earnings growth is strong.

The rates market is moving back into a low vol regime, but with yields at a higher level. This argues for maximizing carry across the Treasury curve.

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

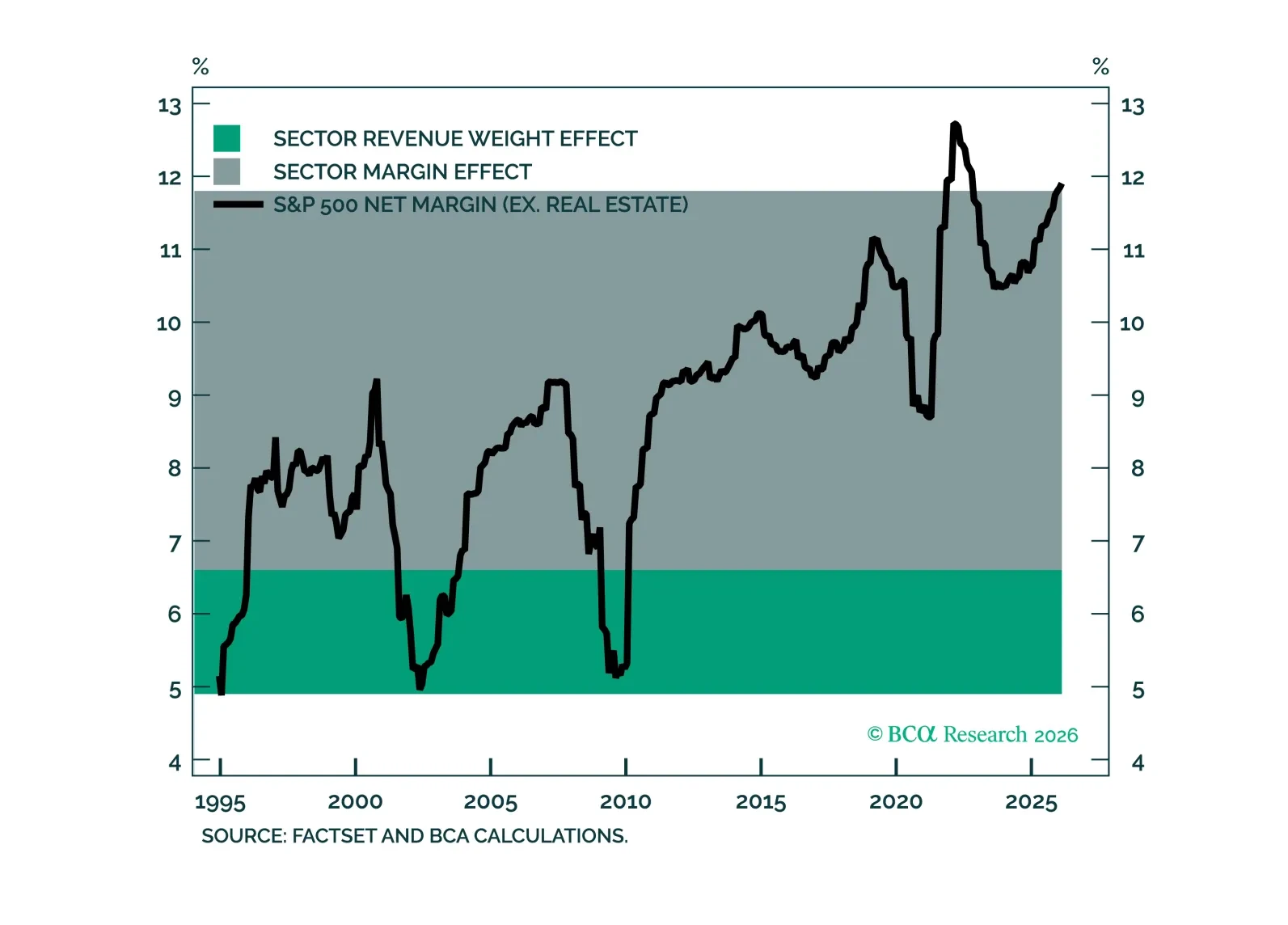

The long-run rise in S&P 500 margins reflects more than a shift toward higher-margin sectors. Most of the increase has come from higher profitability within sectors, supported by favorable mix of macro forces. Looking ahead, many of those tailwinds are likely to fade, with AI-driven productivity gains as a potential offsetting upside driver of margins.