United States

Global bond yields were up (again) on Friday, weighing down on growth stocks (again). Once more, the proximate cause of the bond selloff was good news. This time it was President Biden’s optimistic vaccine outlook. Much ink has been spilled on the impact…

Today we take a deep dive into the S&P 500’s seasonality patterns. While over the last two decades Q1 has been the weakest quarter for stocks, on average, with March registering the steepest losses, using reconstructed S&P 500 daily data since 1928 tells a slightly different story. Interestingly, the market is fairly consistent with the upward sloping, albeit volatile, Q1 long-term seasonal trend. Historically, the weakest months are May, September and October the latter which eventually culminates into the “Santa rally”. Given that Q1 choppiness is 3/4 of the way done, Q2 should prove a lower vol quarter before investors have to contend with the seasonally weak months of September and October. Bottom Line: We reiterate our cyclically constructive broad equity market view.

Seasonality Will Soon Turn Bullish

Seasonality Will Soon Turn Bullish

Highlights The Biden administration’s early actions suggest it will be hawkish on China as expected – and the giant Microsoft hack merely confirms the difficulty of reducing strategic tensions. US-China talks are set to resume and piecemeal engagement is possible. However, most of the areas of engagement touted in the media are overrated. Competition will prevail over cooperation. Cybersecurity stocks have corrected, creating an entry point for investors seeking exposure to a secular theme of Great Power conflict in the cyber realm and beyond. Global defense stocks are even more attractive than cyberstocks as a “back to work” trade in the geopolitical context. Continue to build up safe-haven hedges as geopolitical risk remains structurally elevated and underrated by financial markets. Feature The Biden administration passed its first major law, the $1.9 trillion American Rescue Plan, on March 10. This gargantuan infusion of fiscal stimulus accounts for about 2% of global GDP and 9% of US GDP, a tailwind for risky assets when taken with a receding pandemic and normalizing global economy. The US dollar has perked up so far this year on the back of this extraordinary pump-priming and the rapid rollout of COVID-19 vaccines, which have lifted relative growth expectations with the rest of the world. Hence the dollar is rising for fundamentally positive reasons that will benefit global growth rather than choke it off. Our Foreign Exchange Strategist Chester Ntonifor argues that the dollar has 2-3% of additional upside before relapsing under the weight of rising global growth, inflation expectations, commodity prices, and relative equity flows into international markets. We agree with the dollar bear market thesis. But there are two geopolitical risks that investors must monitor: Cyclically, China’s combined monetary and fiscal stimulus is peaking, growth will decelerate, and the central government runs a non-negligible risk of overtightening policy. However, China’s National People’s Congress so far confirms our view that Beijing will not overtighten. Structurally, the US-China cold war is continuing apace under President Biden, as expected. The two sides are engaging in normal diplomacy as appropriate to a new US administration but the Microsoft Exchange hack (see below) underscores the trend of confrontation over cooperation. Chart 1Long JPY / Short KRW As Geopolitical Risk Is Underrated

Long JPY / Short KRW As Geopolitical Risk Is Underrated

Long JPY / Short KRW As Geopolitical Risk Is Underrated

The second point reinforces the first since persistent US pressure on China will discourage it from excessive deleveraging at home. In a world where China is struggling to cap excessive leverage, the US is pursuing “extreme competition” with China (Biden’s words), and yet the US rule of law is intact, global investors will not abandon the US dollar in a general panic and loss of confidence. They will, however, continue to diversify away from the dollar on a cyclical basis given that global growth will accelerate while US policy will remain extremely accommodative. Reinforcing the point, geopolitical frictions are rising even outside the US-China conflict. A temporary drop in risk occurred in the New Year as a result of the rollout of vaccines, the defeat of President Trump, and the resolution of Brexit. But going forward, geopolitical risk will reaccelerate, with various implications that we highlight in this report. While we would not call an early end to the dollar bounce, we will keep in place our tactical long JPY-USD and long CHF-USD hedges. These currencies offer a good hedge in the context of a dollar bear market and structurally high geopolitical risk. If the dollar weakens anew on good news for global growth then the yen and franc will benefit on a relative basis as they are cheap, whereas if geopolitical risk explodes they will benefit as safe havens. We also recommend going long the Japanese yen relative to the South Korean won given the disparity in valuations highlighted by our Emerging Markets team, and the fact that geopolitical tensions center on the US and China (Chart 1). “Our Most Serious Competitor, China” Why are we so sure that geopolitical risk will remain structurally elevated and deliver negative surprises to ebullient equity markets? Our Geopolitical Power Index shows that China’s rise and Russia’s resurgence are disruptive to the US-led global order (Chart 2). If anything this process has accelerated over the COVID-19 crisis. China and Russia have authoritarian control over their societies and are implementing mercantilist and autarkic economic policies. They are carving out spheres of influence in their regions and using asymmetric warfare against the US and its allies. They have also created a de facto alliance in their shared interest in undermining the unity of the West. The US is meanwhile attempting to build an alliance of democracies against them, heightening their insecurities about America’s power and unpredictability (Chart 3). Chart 2Great Power Struggle Continues

Great Power Struggle Continues

Great Power Struggle Continues

Massive fiscal and monetary stimulus is positive for economic growth and corporate earnings but it reduces the barriers to geopolitical conflict. Nations can pursue foreign and trade policies in their self-interest with less concern about the blowback from rivals if they are fueled up with artificially stimulated domestic demand. Chart 3Biden: ‘Our Most Serious Competitor, China’

More Reasons To Buy Cybersecurity And Defense Stocks

More Reasons To Buy Cybersecurity And Defense Stocks

Total trade between the US and China, at 3.2% and 4.7% of GDP respectively in 2018, was not enough to prevent trade war from erupting. Today the cost of trade frictions is even lower. The US has passed 25.4% of GDP in fiscal stimulus so far since January 1, 2020. China’s total fiscal-and-credit impulse has risen by 8.4% of GDP over the same time period. The Biden administration is co-opting Trump’s hawkish foreign and trade policy toward China, judging by its initial statements and actions (Appendix Table 1). Specifically, Biden has issued an executive order on securing domestic supply chains that demonstrates his commitment to the Trumpian goal of diversifying away from China and on-shoring production, or at least offshoring to allied nations. The Democratic Party is also unveiling bipartisan legislation in Congress that attempts to reduce reliance on China.1 These executive decrees are partly spurred on by the global shortage of semiconductors. China, the US, and the US’s allies are all attempting to build alternative semiconductor supply chains that bypass Taiwan, a critical bottleneck in the production of the most advanced computer chips. The Taiwanese say they will coordinate with “like-minded economies” to alleviate shortages, by which they mean fellow democracies. But this exposes Taiwan to greater geopolitical risk insofar as it excludes mainland China from supplies, either due to rationing or American export controls. The surge in semiconductor sales and share prices of semi companies (especially materials and equipment makers) will continue as countries will need a constant supply of ever more advanced chips to feed into the new innovation and technology race, the renewable energy race, and the buildout of 5G networks and beyond (Chart 4). It takes huge investments of time and capital to build alternative fabrication plants and supply lines yet governments are only beginning to put their muscle into it via stimulus packages and industrial policy. Chart 4Semiconductor Supply Shortage

Semiconductor Supply Shortage

Semiconductor Supply Shortage

Supply shocks have geopolitical consequences. The oil shocks of the 1970s and early 1990s motivated the US to escalate its interventions and involvement in the Middle East. They also motivated the US to invest in stockpiles of critical goods and alternative sources of production so as to reduce dependency (Chart 5). Although semiconductors are not fungible like commodities, and the US has tremendous advantages in semiconductor design and production, nevertheless the bottleneck in Taiwan will take years to alleviate. Hence the US will become more active in supply security at home and more active in alliance-building in Asia Pacific to deter China from taking Taiwan by force or denying regional access to the US and its allies. China faces the same bottleneck, which threatens its technological advance, economic productivity, and ultimately its political stability and international defense. Chart 5ASupply Shortages Motivate Strategic Investments

Supply Shortages Motivate Strategic Investments

Supply Shortages Motivate Strategic Investments

Chart 5BSupply Shortages Motivate Strategic Investments

Supply Shortages Motivate Strategic Investments

Supply Shortages Motivate Strategic Investments

Semiconductor and semi equipment stock prices have gone vertical as highlighted above but one way to envision the surge in global growth and capex for chip makers is to compare these stocks relative to the shares of Big Tech companies in the communication service sector, i.e. those involved in social networking and entertainment, such as Twitter, Facebook, and Netflix. On a relative basis the semi stocks can outperform these interactive media firms which face a combination of negative shocks from rising interest rates, regulation, economic normalization, and ideologically fueled competition (Chart 6). Chart 6Long Chips Versus Big Tech

Long Chips Versus Big Tech

Long Chips Versus Big Tech

What about the potential for the US and China to enhance cooperation in areas of shared interest? Generally the opportunity for re-engagement is overrated. The Biden administration says there will be engagement where possible. The first high-level talks will occur in Alaska on March 18-19 between Secretary of State Antony Blinken, National Security Adviser Jake Sullivan, Central Foreign Affairs Commissioner Yang Jiechi, and Foreign Minister Wang Yi. Presidents Biden and Xi Jinping may hold a bilateral summit sometime soon and the old strategic and economic dialogue may resume, enabling cabinet-level officials to explore a range of areas for cooperation independently of high-stakes strategic negotiations. However, a close look at the policy areas targeted for engagement reveals important limitations: Health: There is little room for concrete cooperation on the COVID-19 pandemic given that the pandemic is already receding, the Chinese have not satisfied American demands for data transparency, Chinese officials have fanned theories that the virus originated in the US, and the US is taking measures to move pharmaceutical and health equipment supply chains out of China. Trade: Trade is an area of potential cooperation given that the two countries will continue trading while their economies rebound. The Phase One trade deal remains in place. However, China only made structural concessions on agriculture in this deal so any additional structural changes will have to be the subject of extensive negotiations. Secretary of Treasury Janet Yellen says the US will use the “full array of tools” to ensure compliance and will punish China for abuses of the global trade system. Cybersecurity: On cybersecurity, China greeted the Biden administration by hacking the Microsoft Exchange email system, an even larger event than Russia’s SolarWinds hack last year. Both hacks highlight how cyberspace is a major arena of modern Great Power struggle, making it unlikely that there will be effective cooperation. The hack suggests Beijing remains more concerned about accessing technology while it can than reducing tensions. The Americans will make demands of China at the Alaska meetings. Environment: As for the environment, the US is a net oil exporter while China imports 73% of its oil, 42% of its natural gas and 7.8% of its coal consumption, with 40% and 10% of its oil and gas coming from the Middle East. The US wants to be at the cutting edge of renewable energy technology but it has nowhere near the impetus of China (or Europe), which are diversifying away from fossil fuels for the sake of national security. Moreover China will want its own companies, not American, to meet its renewable needs. This is true even if there is success in reducing barriers for green trade, since the whole point of diversifying from Middle Eastern oil supplies is strategic self-sufficiency. The Americans would have to accept less energy self-sufficiency and greater renewable dependence on China. Nuclear Proliferation: Cooperation can occur here as the Biden administration will seek to return to a deal with the Iranians restraining their nuclear ambitions while maintaining a diplomatic limiting North Korea’s nuclear weapons stockpile and ballistic missile development. China and Russia will accept the US rejoining the 2015 Iranian nuclear deal but they will require significant concessions if they are to join the US in forcing anything more substantial on the Iranians. China may enforce sanctions on North Korea but then it will expect concessions on trade and technology that the Biden administration will not want to give merely for the sake of North Korea. Bottom Line: The Biden administration’s China strategy is taking shape and it is hawkish as expected. It is not ultra-hawkish, however, as the key characteristic is that it is a defensive posture in the wake of the perceived failures of Trump’s strategy of “attack, attack, attack.” This means largely maintaining the leverage that Trump built for the US while shifting the focus to actions that the US can take to improve its domestic production, supply chain resilience, and coordination with allied producers. Punitive measures are an option, however, and if relations deteriorate over time, as expected, they will be increasingly relied on. Buy The Dip In Cybersecurity Stocks A linchpin of the above analysis is the Microsoft Exchange hack, which some have called the largest hack in US history, since it confirms the view that the Biden administration will not be able to de-escalate strategic tensions with China much. China has been particularly frantic to acquire technology through hacking and cyber-espionage over the past decade as it attempts to achieve a Great Leap Forward in productivity in light of slowing potential growth that threatens single-party rule over the long run. The breakdown in ties between Presidents Barack Obama and Xi Jinping occurred not only because of Xi’s perceived violation of a personal pledge not to militarize the South China Sea but also because of the failure of a cybersecurity cooperation deal between the two. When the Trump administration arrived on the scene it sought to increase pressure on China and cybersecurity was immediately identified as an area where pushback was long overdue. Cyber conflict is highly likely to persist, not only with Russia but also with China. Cyber operations are a way for states to engage in Great Power struggle while still managing the level of tensions and avoiding a military conflict in the real world. The cyber realm is a realm of anarchy in which states are insecure about their capabilities and are constantly testing opponents’ defenses and their own offensive capabilities. They can also act to undermine each other with plausible deniability in the cyber realm, since multiple state and quasi-state actors and a vast criminal underworld make it difficult to identify culprits with confidence. Revisionist states like China, North Korea, Russia, and Iran have an advantage in asymmetric warfare, including cyber, since it enables them to undermine the US and West without putting their weaker conventional forces in jeopardy. Cybersecurity stocks have corrected but the general up-trend is well established and fully justified (Chart 7). It is not clear, however, that investors should favor cybersecurity stocks over the general NASDAQ index (Chart 8). The trend has been sideways in recent years and is trying to form a bottom. Cybersecurity stocks are volatile, as can be seen compared to tech stocks as a whole, and in both cases the general trend is for rising volatility as the macro backdrop shifts in favor of higher interest rates and inflation expectations (Chart 9). Chart 7Cyber Security Stocks Corrected

Cyber Security Stocks Corrected

Cyber Security Stocks Corrected

Chart 8Major Hacks Failed To Boost Cyber Vs NASDAQ

Major Hacks Failed To Boost Cyber Vs NASDAQ

Major Hacks Failed To Boost Cyber Vs NASDAQ

Chart 9Volatility Of Cyber & Tech Stocks Rising

Volatility Of Cyber & Tech Stocks Rising

Volatility Of Cyber & Tech Stocks Rising

Great Power struggle will not remain limited to the cyber realm. There is a fundamental problem of military insecurity plaguing the world’s major powers. Furthermore the global economic upturn and new energy and industrial innovation race will drive up commodity prices, which will in turn reactivate territorial and maritime disputes. Turf battles will re-escalate in the South and East China Seas, the Persian Gulf and Indian Ocean basin, the Mediterranean, and even the Baltic Sea and Arctic. One way to play this shift is as a geopolitical “back to work” trade – long defense stocks relative to cybersecurity stocks (Chart 10). The global defense sector saw a run-up in demand, capital expenditures, and profits late in the last business cycle. That all came crashing down with the pandemic, which supercharged cybersecurity as a necessary corollary to the swarm of online activity as households hunkered down to avoid the virus and obey government social restrictions. Cybersecurity stocks have higher EV/EBITDA ratios and lower profit margins and return on equity compared to defense stocks or the broad market. Chart 10Long Defense / Short Cyber Security: 'Back To Work' For Geopolitics

Long Defense / Short Cyber Security: 'Back To Work' For Geopolitics

Long Defense / Short Cyber Security: 'Back To Work' For Geopolitics

The trade does not mean cybersecurity stocks will fall in absolute terms – we maintain our bullish case for cybersecurity stocks – but merely that defense stocks will make relative gains as economic normalization continues in the context of Great Power struggle. Bottom Line: Structurally elevated geopolitical risks will continue to drive demand for cybersecurity in absolute terms. However, we would favor global defense stocks on a relative basis. The US Is Not As War-Weary As People Think America is consumed with domestic divisions and distractions. Since 2008 Washington has repeatedly demonstrated an unwillingness to confront foreign rivals over small territorial conquests. This risk aversion has created power vacuums, inviting ambitious regional powers like China, Russia, Iran, and Turkey to act assertively in their immediate neighborhoods. However, the US is not embracing isolationism. Public opinion polling shows Americans are still committed to an active role in global affairs (Chart 11). The 2020 election confirms that verdict. Nor are Americans demanding big cuts in defense spending. Only 31% of Americans think defense spending is “too much” and only 12% think the national defense is stronger than it needs to be (Chart 12). Chart 11No Isolationism Here

No Isolationism Here

No Isolationism Here

True, the Democratic Party is much more inclined to cut defense spending than the Republicans. About 43% of Democrats demand cuts, while 32% are complacent about the current level of spending (compared to 8% and 44% for Republicans). But it is primarily the progressive wing of the party that seeks outright cuts and the progressives are not the ones who took power. Chart 12Americans Against ‘Forever Wars’ But Not Truly Dovish

More Reasons To Buy Cybersecurity And Defense Stocks

More Reasons To Buy Cybersecurity And Defense Stocks

Biden and his cabinet represent the Washington establishment, including the military-industrial complex. Even if Vice President Kamala Harris should become president she would, if anything, need to prove her hawkish credentials. Defense spending cuts might be projected nominally in Biden’s presidential budgets but they will not muster majorities in the two narrowly divided chambers of Congress. Biden has co-opted Trump’s (and Obama’s) message of strategic withdrawal and military drawdown. He is targeting a date of withdrawal from Afghanistan on May 1, notwithstanding the leverage that a military presence there could yield in its priority negotiations with Iran. Yet he is not jeopardizing the American troop presence in Germany and South Korea, much more geopolitically consequential spheres of action in a long competition with Russia and China. While it is true (and widely known) that Americans have turned against “forever wars,” this really means Middle Eastern quagmires like Iraq and Afghanistan and does not mean that the American public or political establishment have truly become anti-war “doves.” The US public recognizes the need to counter China and Russia and Congress will continue appropriating funds for defense as well as for industrial policy. The Biden administration will increase awareness about the risks of a lack of deterrence and alliance-building. This is especially apparent given the military buildup in China. The annual legislative session has revealed an important increase in military focus in Beijing in the context of the US rivalry. Previously, in the thirteenth five-year plan and the nineteenth National Party Congress, the People’s Liberation Army aimed to achieve “informatization and mechanization” reforms by 2020 and total modernization by 2035. However, at the fifth plenum of the central committee in October, the central government introduced a new military goal for the PLA’s 100th anniversary in 2027 – a “military centennial goal” to match with the 2021 centennial of the Communist Party and the 2049 centennial goal of the founding of the People’s Republic. While details about this new military centenary are lacking, the obvious implication is that the Communist Party and PLA are continuing to shift the focus to “fighting and winning wars,” particularly in the context of the need to deter the United States. The official defense budget is supposed to grow 6.8% in 2021, only slightly higher than the 6.6% goal in 2020, but observers have long known that China’s military budget could be as much as twice as high as official statistics indicate. The point is that defense spending is going up, as one would expect, in the context of persistent US-China tensions. Bottom Line: Just as US-China cooperation will be hindered by mutual efforts to reduce supply chain dependency and support domestic demand, so too it will be hindered by mutual efforts to increase defense readiness and capability in the event of military conflict. The beneficiary of continued high levels of US defense spending and Chinese spending increases – in the context of a more general global arms buildup – will be global arms makers. Investment Takeaways Geopolitical risk remains structurally elevated despite the temporary drop in tensions in late 2020 and early 2021. The China-backed Microsoft Exchange hack reinforces the Biden administration’s initial foreign policy comments and actions suggesting that US policy will remain hawkish on China. While Biden will adopt a more defensive rather than offensive strategy relative to Trump, there is no chance that he will return to the status quo ante. The Obama administration itself grew more hawkish on China in 2015-16 in the face of cyber threats and strategic tensions in the South China Sea. Cybersecurity stocks will continue to benefit from secular demand in an era of Great Power competition where nations use cyberattacks as a form of asymmetric warfare and a means of minimizing the risks of conflict. The recent correction in cybersecurity stocks creates a good entry point. We closed our earlier trade in January for a gain of 31% but have remained thematically bullish and recommend going long in absolute terms. We would favor defense over cybersecurity stocks as a geopolitical version of the “back to work” trade in which conventional economic activity revives, including geopolitical competition for territory, resources, and strategic security. Defense stocks are undervalued and relative share prices are unlikely to fall to 2010-era lows given the structural increase in geopolitical risk (Chart 13). Chart 13Global Defense Stocks Oversold

Global Defense Stocks Oversold

Global Defense Stocks Oversold

Chart 14Global Defense Stocks Profitable, Less Indebted

Global Defense Stocks Profitable, Less Indebted

Global Defense Stocks Profitable, Less Indebted

Defense stocks have seen profit margins hold up and are not too heavily burdened by debt relative to the broad market (Chart 14). Defense stocks have a higher return on equity than the average for non-financial corporations and cash flow will improve as a new capex cycle begins in which nations seek to improve their security and gain access to territory and resources (Chart 15). Chart 15Defense Stocks: High RoE, Capex Will Revive

Defense Stocks: High RoE, Capex Will Revive

Defense Stocks: High RoE, Capex Will Revive

Chart 16Discount On Global Defense Stocks

Discount On Global Defense Stocks

Discount On Global Defense Stocks

Valuation metrics show that global defense stocks are trading at a discount (Chart 16). Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table 1 Appendix Table 1Biden Administration's First 100 Days: Key Statements And Actions On China

More Reasons To Buy Cybersecurity And Defense Stocks

More Reasons To Buy Cybersecurity And Defense Stocks

Footnotes 1 See Federal Register, "America’s Supply Chains", Mar. 1, 2021, federalregister.gov and Richard Cowan and Alexandra Alper, "Top U.S. Senate Democrat directs lawmakers to craft bill to counter China", Feb. 23, 2021, reuters.com.

The US job openings from the January JOLTS survey were better than expected. Total registered job openings ticked up to 6.92 million (the highest reading since last February) from 6.75 million, surprising expectations of a decline to 6.70 million. This…

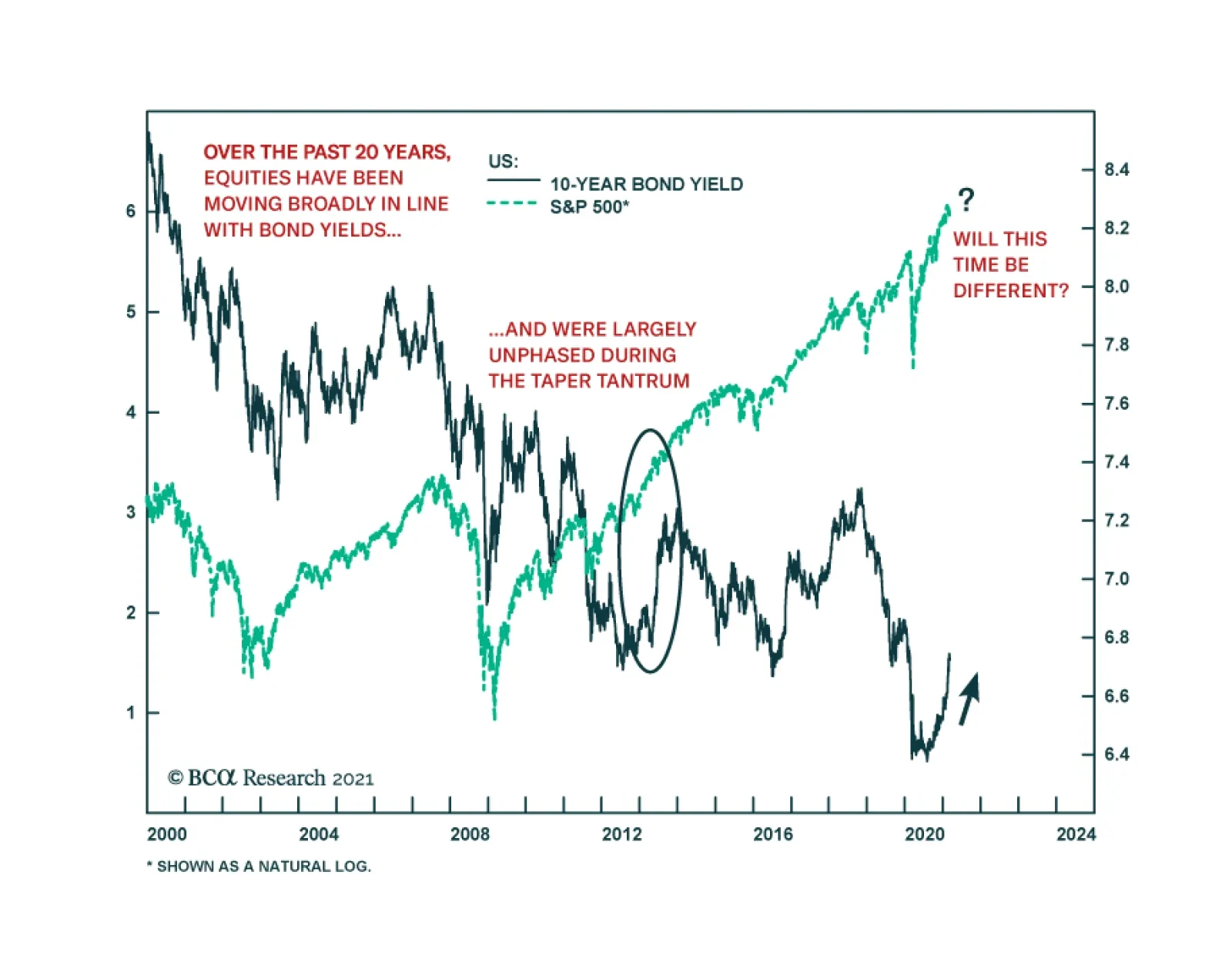

Of Stocks And Bonds

Of Stocks And Bonds

In recent research we have highlighted the intricate relationship between stocks and bonds and how a selloff in the latter can cause some consternation in the SPX (please see Charts 7 and 9A here). Today we take a closer look at the interplay between the long-run median FOMC interest rate projections (DOTS) and the 10-year US Treasury yield. While the data only starts in 2012, we note a special episode that happened early in 2018. Virtually the same week when the 10-year US Treasury yield crossed above the long-run DOTS, the Trump corporate tax cut rally came to an abrupt halt, and the market suffered a 10% pullback (top & middle panels). As the Powell-led Fed embarked on four hikes throughout 2018 sustaining the selloff in the 10-year US Treasury bond market, the SPX remained jittery and fell 20% from the September peak to the Christmas Eve trough. Fast forward to today and while the monetary backdrop is anything but similar to 2018, the selloff in the bond market is gaining momentum. If history at least rhymes, it will take a further 100bps of tightening via a rise in the 10-year US Treasury yield before the bond market’s selloff turns from reflective to restrictive for stocks, assuming no change in the FOMC’s long-run DOTS. Bottom Line: A sizable selloff in the bond market from current levels remains a key risk to our cyclically sanguine equity market view.

Please note that we will be presenting a webcast on Thursday March 11 at 10:00 AM EST for the Americas and EMEA regions and on March 12 at 9:00 HKT/12:00 AEDT for APAC clients. We will be discussing macro themes and investment strategies. Highlights EMs (ex-China, Korea and Taiwan) are better positioned to handle higher US bond yields today than they were in 2013. Yet better does not mean they will be unscathed. The combination of rising US bond yields and a firming US currency will suffocate EM risk assets in the near-term. A neutral allocation is warranted in EM stocks and credit markets within global equity and credit portfolios, respectively. Feature Ever since the US elections concluded in January with a Blue Sweep, we have been warning that rising US bond yields could trigger a setback in global markets in general, and in EM markets in particular. EM equities, currencies and fixed-income markets have recently experienced a correction (Chart 1). The question now is: Is the market rout over? Or is there more to come? We are inclined to believe that the correction is not over. Rising US Treasury yields have been the culprit of the shakeout in global growth stocks, EM equities, as well as EM currencies. Therefore, taking a stance on US bond yields and on the US dollar is critical for assessing the outlook for EM financial markets. Odds are that the selloff in US long-term bonds and the rebound in the US dollar are not yet over because: Positioning and sentiment on US long-dated Treasuries is neutral, as illustrated in Chart 2. Chart 1Rising US Real Yields Have Caused A Shakeout In EM

Rising US Real Yields Have Caused A Shakeout In EM

Rising US Real Yields Have Caused A Shakeout In EM

Chart 2Investor Sentiment And Positioning In US Treasurys Are Neutral

Investor Sentiment And Positioning In US Treasurys Are Neutral

Investor Sentiment And Positioning In US Treasurys Are Neutral

Typically, US bond yields do not reverse their ascent until investor sentiment becomes downbeat and bond portfolios are of materially short duration. These conditions for a top in bond yields are not yet present. US government bond yields would have been much higher if it were not for the Federal Reserve and US commercial banks’ massive bond-buying spree. The Fed has bought $2.8 trillion and US commercial banks have purchased about $300 billion of Treasurys in the past 12 months (Chart 3). One of the main motives for commercial banks to buy US Treasurys has been the SLR relief initiative which commenced on April 1, 2020.1 This SLR relief is due to terminate on March 31, 2021. Unless it is extended, commercial banks will drastically curtail their net government bond purchases. This will exert upward pressure on Treasury yields. Regarding the greenback, investor sentiment remains quite bearish (Chart 4). From a contrarian perspective, this heralds further strength in the US dollar. Chart 3Surging Purchases Of US Treasurys By The Fed And Commercial Banks

Surging Purchases Of US Treasurys By The Fed And Commercial Banks

Surging Purchases Of US Treasurys By The Fed And Commercial Banks

Chart 4Investors Are Still Bearish On The US Dollar

Investors Are Still Bearish On The US Dollar

Investors Are Still Bearish On The US Dollar

From a cyclical perspective, US growth will be stronger relative to its potential, and vis-à-vis other DMs, EMs and China. Growth differentials moving in favor of the US foreshadows near-term strengthening of the dollar. Structurally, the bearish case for the US currency hinges on both the Federal Reserve falling behind the inflation curve and ballooning US twin deficits. In our view, this will ultimately be the case. Hence, the long-term outlook for the US dollar remains troublesome. That said, twin deficits alone are insufficient to produce a continuous currency depreciation. The twin deficits must also be accompanied with low/falling real interest rates – in order to generate sufficient conditions for currency depreciation. As long as US real rates continue rising, the dollar’s rebound will be extended. The USD/EUR exchange rate has been correlated with the 10-year real yield differential and this relationship will persist (Chart 5). Bottom Line: US government bonds will continue selling off. Rising bond yields (including rising real yields) will support the dollar in the near-term. The combination of rising US bond yields and a firming US currency will cause global macro volatility to rise (Chart 6). This will suffocate EM risk assets and EM currencies. Chart 5US Real Yields (TIPS) Will Continue Driving The US Dollar

US Real Yields (TIPS) Will Continue Driving The US Dollar

US Real Yields (TIPS) Will Continue Driving The US Dollar

Chart 6Aggregate Financial Market Volatility: Higher Lows

Aggregate Financial Market Volatility: Higher Lows

Aggregate Financial Market Volatility: Higher Lows

Impact On EM: 2013 Versus Now Are we entering another Taper Tantrum episode as in the spring of 2013 when many EMs were devastated? There are both similarities and differences between the current period of rising US bond yields and the 2013 episode. Similarities: Today, as in early 2013, investor sentiment on EM is very bullish and investors are long EM (Chart 7). Chart 7Investor Sentiment On EM Stocks Was At A Record High In January

Investor Sentiment On EM Stocks Was At A Record High In January

Investor Sentiment On EM Stocks Was At A Record High In January

In early 2013, as is the case today, EM local currency bond yields were very low and EM credit spreads were too tight. When US Treasury yields spiked in the spring of 2013, EM assets tanked. Many commentators blamed it on the Fed. We disagree with that interpretation. Remarkably, the rise in US TIPS yields in 2013 had little impact on equity indices such as the S&P 500 and Nasdaq, or on US corporate spreads (Chart 8). The correction in the US equity market lasted about a week. Yet, EM equities, fixed income markets and currencies experienced a prolonged slump, and in many cases, a bear market. There is no basis to believe that the Fed’s policy and US bond yields are more important to EM than they are to US credit and equity markets. The core rationale for the EM bear market in 2013 was poor domestic fundamentals. The Fed’s tapering was the trigger, not the cause. Differences: The key difference between the current episode and the 2013 Taper Tantrum is EM macro fundamentals. Specifically: EM economies (ex-China, Korea and Taiwan) entered 2013 with booming bank loans and strong domestic demand as well as high inflation (Chart 9). Chart 8US Markets Were Not Hit By The Taper Tantrum In 2013

US Markets Were Not Hit By The Taper Tantrum In 2013

US Markets Were Not Hit By The Taper Tantrum In 2013

Chart 9EM (ex-China, Korea And Taiwan): 2013 Vs Now

EM (ex-China, Korea and Taiwan): 2013 Vs Now

EM (ex-China, Korea and Taiwan): 2013 Vs Now

Chart 10EM (ex-China, Korea And Taiwan): 2013 Vs Now

EM (ex-China, Korea and Taiwan): 2013 Vs Now

EM (ex-China, Korea and Taiwan): 2013 Vs Now

Presently, EM bank credit is subdued, domestic demand is dismal, and inflation is tame. Besides, EMs (ex-China, Korea and Taiwan) had a very large trade deficits in 2013 and were financing them via foreign borrowing, which was roaring prior to 2013 (Chart 10). Presently, their trade balances are in surplus and foreign indebtedness has not increased in recent years. Bottom Line: In 2013, EM economies (ex-China, Korea and Taiwan) were overheating and were addicted to foreign funding. These were the reasons why EM currencies and fixed income markets teetered when US bond yields spiked in 2013. Presently, the majority of EM economies (ex-China, Korea and Taiwan) have different types of malaises: domestic bank loan origination is too timid, consumer spending and capital expenditures are moribund, inflation is low and fiscal policy is tight. Consequently, EMs (ex-China, Korea and Taiwan) are better positioned to handle higher US bond yields today than they were back in 2013. Yet better does not mean they will be unscathed. Investment Strategy Equities: The key variable to watch to assess the vulnerability of both US and EM equity markets is their respective corporate bond yields. Historically, rising corporate bond yields (shown inverted in both panels of Chart 11) heralds lower share prices. Chart 11Rising Corporate Bond Yields Are Bad For Share Prices

Rising Corporate Bond Yields Are Bad For Share Prices

Rising Corporate Bond Yields Are Bad For Share Prices

Given that both EM and US corporate credit spreads are too tight, they are unlikely to narrow further to offset rising US Treasury yields. Instead, EM and US corporate bond yields are likely to rise with US Treasury yields. This will trigger more weakness in share prices. Besides, rising EM local currency government bond yields also point towards more downside in EM equities (yields are shown inverted on the chart) (Chart 12). Chart 12Rising EM Local Currency Bond Yields Heralds Weaker Equity Prices

Rising EM Local Currency Bond Yields Heralds Weaker Equity Prices

Rising EM Local Currency Bond Yields Heralds Weaker Equity Prices

Concerning equity style, global growth stocks have peaked versus global value stocks. In the EM equity space, we have less conviction on growth versus value. As to regional allocation in a global equity portfolio, we continue recommending a neutral allocation to EM, underweighting US and overweighting Europe and Japan. Commodities: Investors’ net long positions in commodities are very elevated (Chart 13). As US bond yields rise and the US dollar continues rebounding, there will be a de-risking in the commodities space resulting in a pullback in commodities prices. Currencies: We continue shorting a basket of EM currencies – including BRL, CLP, ZAR, TRY and KRW versus the euro, CHF and JPY. Several EM currencies have failed to break above their technical resistance levels, suggesting that a pullback could be non-trivial (Chart 14). Chart 13Investors Are Record Long Commodities

Investors Are Record Long Commodities

Investors Are Record Long Commodities

Chart 14Asian Currencies Hit Technical Resistances

Asian Currencies Hit Technical Resistances

Asian Currencies Hit Technical Resistances

In central Europe, we are closing the long CZK/short USD trade with a 3.8% gain. Continue holding the long CZK/short PLN and HUF position. Local fixed income markets: EM local bond yields have risen in response to rising US treasury real yields and the setback in EM currencies. This might persist in the near-term, but we continue to recommend receiving 10-year swap rates in selected countries where inflation risks are low and monetary and fiscal policies are tight. These countries include Mexico, Colombia, Russia, China, India and Malaysia. A further rise in their swap rates would represent an overshoot and hence, should not be chased. EM currencies are more vulnerable to a selloff than local rates are. We continue to wait for a better entry point in currencies to recommend buying cash domestic bonds instead of receiving swap rates. EM Credit: A neutral allocation to EM sovereign and corporate bonds is warranted in a global credit portfolio. Our sovereign credit overweights are Mexico, Russia, Malaysia, Peru, Colombia, the Philippines and Indonesia, while our sovereign credit underweights are Brazil, South Africa and Turkey. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 The Supplementary Leverage Ratio (SLR) is equivalent to Basel III Tier-1 leverage ratio and varies from 3-5% for US banks. Under the relief program last April, the Fed allowed US banks to exclude holdings of US Treasury Bonds and cash kept in reserves at the Fed from their assets when calculating this ratio. The SLR relief is planned to end March 31, 2021. Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights The US has largely passed a “stress test” of its political system. Rule of law is intact. The US dollar and treasuries may fall further due to cyclical and macro developments but not due to a structural loss of confidence in US governance. The judicial system will become the key check on the Biden administration as it shifts from short-term economic relief to its longer-term agenda, especially on executive orders. The court becomes even more important as a check if the Democrats muster the votes to remove the filibuster. This is possible but not imminent. Packing the court is much harder. Major court cases only sometimes have a major impact on the stock market but key sectors can be given certainty through court verdicts after being disrupted by policy. The US dollar is bouncing on the basis of economic recovery and political stability which poses a near-term risk to cyclical sectors. Feature US government bonds continued to sell off over the past week as the economic recovery gained steam and investors rotated into cyclical equities and commodities. The US Senate passed the $1.9 trillion American Rescue Plan – a massive and likely excessive infusion of fiscal relief – sending it to the House where it will be ratified shortly and passed over to President Joe Biden for signing. Across America shops and restaurants are opening up as immunization to COVID-19 advances and hospitalizations collapse. Meanwhile the Supreme Court announced its first set of rulings under the Biden administration: it dismissed former President Trump’s last challenge to the 2020 election and ruled on other issues such as free speech. The country has tentatively passed a political “stress test.” The rule of law remains intact. On the surface these two trends stand in opposition. US treasuries have been attractive to a savings-rich world not just because of the size of the US economy but also because of the country’s 245-year tradition of good governance – the balance of freedom and stability in its government and financial markets. The share of foreign holdings of US treasuries is declining but the reason is that the Federal Reserve is increasing its share (Chart 1). Foreigners are not liquidating their holdings just yet, although it is a risk given the US’s combination of extremely easy monetary and fiscal policy and populist politics. Chart 1Foreign Holdings Of US Treasuries

Foreign Holdings Of US Treasuries

Foreign Holdings Of US Treasuries

In this report we focus on governance in the wake of the Trump administration and COVID-19 pandemic. Is US governance eroding? If so, how will it impact the markets? How will the courts interact with the Biden administration? Should investors care about the rule of law? With a new business cycle beginning, any assurance of a basic level of US governance allows risk appetite to recover and enables investors to pursue higher-yielding cyclical assets with less inhibition. But it also suggests that US assets will remain safe havens. How Rule Of Law Matters To Investors Rule of law and the independence of the judiciary are critical aspects of good governance that make a market attractive to foreign investors and secure for domestic investors. Nowhere is this clearer than in the breakdown of global reserve currencies. The United States and its developed market allies hold pride of place (Chart 2). Nevertheless the US has lost some of its reserve status to other currencies over two decades of partisanship and repeated crises, from 9/11 through Trump’s trade war. Chart 2Rule Of Law: Bedrock For Reserve Currencies

Court Rulings And The Market

Court Rulings And The Market

Government bond yields exhibit some degree of correlation, inversely, with rule of law: better governance implies lower yields and vice versa. As the global savings glut grew over the past few decades, investors sought to preserve capital in securities perceived to be the safest. This is apparent whether judging by a simple comparison of developed and emerging market bond yields or by the World Bank’s Worldwide Governance Indicators.1 The relationship between governance and bond yields is strongest with emerging markets but it loosely holds among developed markets like the US, as shown in Chart 3. Chart 3Bond Yields Lower Where Laws Rule

Court Rulings And The Market

Court Rulings And The Market

It is the level of governance rather than any change matters, since bond yields have fallen for all developed markets regardless of changes in governance over the past decade. However, governments that take negative steps that harm governance attract fewer foreign purchases of their debt than those that improve governance (Chart 4). This is true of developed and emerging economies. The implication is that demand for US treasuries would have been even greater over the past decade if the US political system had remained stable like Canada’s. Chart 4Improved Rule Of Law Attracts Bond Investors

Court Rulings And The Market

Court Rulings And The Market

Differences in developed economy governance only slightly (if at all) correlate with portfolio or direct investment flows (Charts 5 and 6). This is not surprising as governance does not translate into short-term corporate earnings growth and foreign countries invest directly in developed markets to access technology and consumer markets. By contrast, in emerging markets, better governance goes along with stronger equity demand and foreign direct investment. Chart 5Rule Of Law A Boon For Equity Flows?

Court Rulings And The Market

Court Rulings And The Market

Chart 6Eroding Rule Of Law Discourages Direct Investment

Court Rulings And The Market

Court Rulings And The Market

Still the global phenomenon suggests that an erosion of rule of law can shake up one’s faith in a government’s ability or willingness to make debt payments and its operating environment for private companies. Domestically focused investors have to be concerned about rule of law since its collapse would undermine political stability as well as property rights, the surety of contracts, and the redress of grievances. US Rule Of Law Post-Trump And Post-COVID The US has the world’s longest continuously running constitution and one of the highest standards of living. Other countries with similarly high standards of living have similar constitutions or even adopted theirs from the United States. At the same time US governance has deteriorated in recent years, raising the question of whether bond investors or private entrepreneurs face greater governance risk. The drop in rule of law is apparent in the World Bank’s index (Chart 7A). The turmoil of the 2020 election cycle proves beyond doubt that the US suffers from some serious governance problems. At the same time the independence of the US judiciary is rising in the ranks (Chart 7B). Looking ahead, this trend will likely continue as the judicial system managed to get through the disruptive Trump presidency and the 2020 pandemic and election with minimal damage to its independence. Chart 7AUS Rule Of Law Erosion Will Pause

Court Rulings And The Market

Court Rulings And The Market

Chart 7BUS Judicial Independence Has Improved

Court Rulings And The Market

Court Rulings And The Market

This is a remarkable feat as the underlying problem in the US system – political polarization – threatens to entangle the judiciary as much as any other institution. Today, with polarization subsiding yet still at a historically high level, the court’s integrity and credibility are critical to the overall maintenance of the rule of law (Chart 8). Chart 8US Polarization Set To Fall

US Polarization Set To Fall

US Polarization Set To Fall

Chart 9Trust In Supreme Court Fairly Steady

Court Rulings And The Market

Court Rulings And The Market

Polarization creates gridlock in Congress, which forces other branches of government to fill the vacuum and deliver solutions, thus becoming more controversial. This process has ensnared the high court from time to time as well as the central bank and other institutions.2 Over the past ten years the courts have struggled to minimize the damage from polarization. Confidence in the high court has fallen, but not catastrophically, and most voters feel about the same as ever toward the court (Chart 9). Meanwhile disapproval of Congress is stuck around 80%. The Trump era featured a range of claims about the rule of law in America that can now be assessed with some distance. The Democratic Party was not able to remove President Trump through extra-electoral means, while President Trump was not able to ride roughshod over the courts via executive order. Several of Trump’s initiatives were upheld, such as his immigration ban, while others were shot down, such as his attempt to deport the so-called “Dreamers” or add a question about citizenship on the US census. The 2020 election irregularities were not enough to sway the outcome of the electoral vote while the insurrection at the Capitol stood no chance of overthrowing the system. Supreme Court Justice John Roberts refrained from presiding over Trump’s second impeachment – differentiating it from the impeachment of a sitting president – without intervening to tell the Senate whether it could impeach a previous president. Going forward, however, the courts will act as a check on the Biden administration and therefore new controversies will arise. One of the Trump administration’s lasting legacies was to appoint three justices to the high court, creating a six-to-three conservative ideological leaning on the court. Since the Democrats won control of both the White House and Congress, the Supreme Court becomes a critical check on the administration and will thus attract opposition (Chart 10). Speculation about a conservative ideological takeover of the court has proved overrated, based on the court’s neutrality amid the election. Antagonism will inevitably increase going forward as Biden moves away from COVID relief and economic welfare to his larger legislative agenda. Yet the second reconciliation bill, which features infrastructure and green energy investments, would have to include major surprises to create anything as controversial as the dispute over the individual mandate, which imposed a tax on citizens who did not purchase health insurance.3 In other words, a major clash over legislation is more likely only when the Senate Democratic majority removes the filibuster, the rule that effectively requires 60 votes in the Senate to pass regular legislation. This can happen but it does not appear imminent. Senator Joe Manchin of West Virginia opposes removing it, keeping the Democrats at least one vote shy of repealing it, though he has recently shown some flexibility by suggesting that the Senate return to the good old days when senators had to deliver a filibuster in person (and therefore the procedural hurdle was more burdensome to maintain). Chart 10Balance Of Power In The Three Branches

Court Rulings And The Market

Court Rulings And The Market

Thus the main arena of friction between the Biden administration and the judiciary will boil down to executive action, as with the Trump administration. Not all of this friction will be partisan but certainly ideological leanings will matter in the most important cases. While the number of Trump’s judicial appointments is often exaggerated – President Obama appointed more (Chart 11) – it is still the case that conservatives possess an improved ideological advantage due to the past few decades of appointments (Chart 12). So far Biden has faced pushback on his 100-day deportation moratorium. Chart 11Trump's Judicial Impact Overstated

Court Rulings And The Market

Court Rulings And The Market

Chart 12Federal Courts A Bulwark For Conservatives

Court Rulings And The Market

Court Rulings And The Market

Table 1 highlights the most investment-relevant Supreme Court cases coming due in the current session. The court will determine, among other things, whether Facebook can be treated similar to a telephone company in some respects; whether the federal government or states oversee cases brought against oil and natural and gas companies over climate change; and to what extent tech company acquisitions include patents and copyrights. The use of executive authority to reallocate funds that Congress has appropriated for different reasons, and state exemptions for Medicaid requirements, are also on the docket. Table 1Major Cases Pending At Supreme Court

Court Rulings And The Market

Court Rulings And The Market

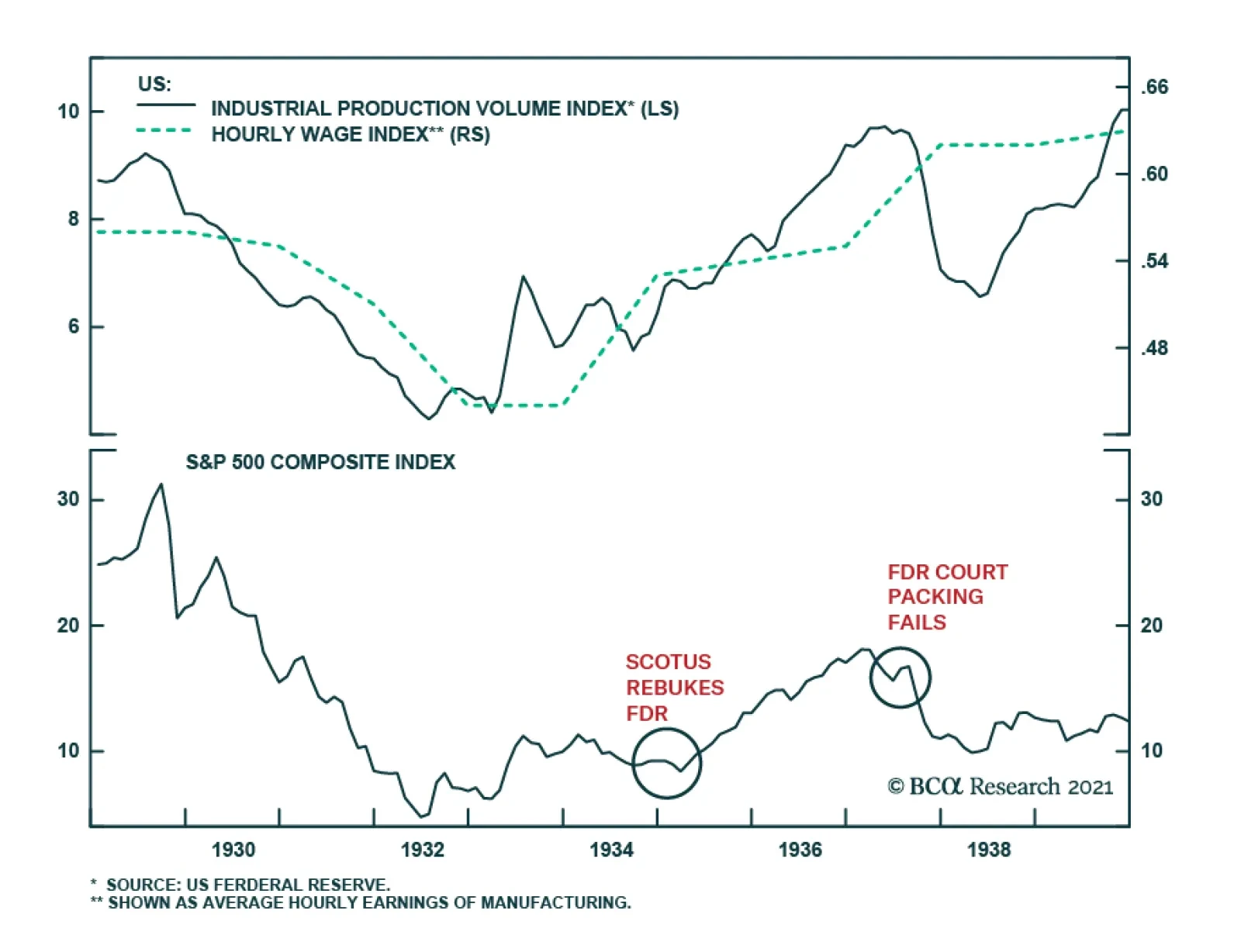

In addition we would identify several policy areas that are likely to become relevant to investors due to contemporary political and geopolitical concerns combined with historical precedent: National Security: The Trump administration relied heavily on the Supreme Court’s historic deference to presidents on issues involving national security and foreign policy. This tendency will likely continue, giving President Biden a freer hand in cases where he claims a national security justification, particularly in dealing with export controls vis-à-vis China. The hack into Microsoft’s Exchange email system, allegedly committed by Chinese state-backed hackers, highlights our Geopolitical Strategy view that the Biden administration will not reduce the US-China power struggle. Industrial Policy: The Supreme Court famously rebuked President Harry Truman for trying to seize control of private steel production during the Korean war (Youngstown Sheet & Tube Company v. Sawyer, 1952). Similar cases could emerge in an era in which the president is attempting to assert US government control over critical supply chains in health, tech, and defense. Immigration: The Supreme Court rebuked the Trump administration on the question of the “Dreamers,” undocumented immigrants brought to the US as children, whom the Obama administration refused to deport under an initiative called Deferred Action for Childhood Arrivals (DACA). The court said the Trump administration failed to provide adequate procedural justification for revoking the DACA program. Now the Biden administration’s executive orders loosening immigration and border controls face challenges from lower courts that could ascend the ladder. Also, following from the logic of Trump’s defeat on this issue, it is possible that the Supreme Court could overturn some of Biden’s revocations of Trump’s orders if not adequately justified. Environment: The Biden administration has pledged to phase out the fossil fuel industry over time, yet legislative majorities will be lacking and much of the activity occurs on private land free from direct federal control. The result is that Biden administration will revive regulatory expansions from the Obama era to attempt to raise the cost of carbon emissions. These actions will likely provoke court rulings. Labor: One of the Clinton presidency’s biggest legal controversies, outside the impeachment, centered on executive orders aimed at stopping businesses from hiring replacements for workers who went on strike. The Biden administration explicitly aims to have a muscular policy on labor regulation and to promote union interests and these could run afoul of the courts. Big Tech and free speech: The court has just ruled with an eight-to-one majority in favor of a free speech case on campus. The only reason Chief Justice Roberts dissented was because the case was moot. Future cases may not be moot in an era in which first amendment quarrels are heating up as Big Business, Big Tech, and mainstream media ramp up censorship of disfavored speech. The Supreme Court is likely to enforce first amendment protections robustly which could result in breaking open the digital arena for alternative platforms and services with looser standards. Bottom Line: With Democratic control over the White House and Congress, the judicial branch will become a critical source of limitations on the Biden administration’s policies. While controversial cases could possibly arise from any ambitious proposals in Biden’s second reconciliation bill, the main source of friction will center on executive orders. This is the case at least until the filibuster is removed, which is possible down the road but not imminent. Could Democrats Pack The Court? Finally there is an ongoing concern over the risk of “court packing,” i.e. partisan enlargement of the Supreme Court, under the Biden administration. During the 2020 campaign several leading Democratic Party figures suggested the party could increase the size of the high court so as to reduce the six-to-three conservative leaning. The threat was partly intended to motivate the progressive voting base and deter the Republicans from going forward with the confirmation of Supreme Court Justice Amy Coney Barrett ahead of the election. However, the possibility of court packing remains as long as polarization is extreme and the ruling party has at least 51 votes needed to repeal the filibuster in the Senate. President Biden said he was “not a fan” of court packing but one of his first acts in office was to appoint a commission of experts to study the idea of Supreme Court reform. This can be interpreted as a way of sidelining the question or as a preliminary to packing the court should it become possible later. Packing the court is politically explosive so while Democrats could remove the filibuster if and when they get the votes, they are less likely to succeed at packing the vote due to public opinion (though it cannot be ruled out over the long run). The bar to altering the filibuster is much lower than that to changing the composition of the court. History suggests that it would be a market-relevant episode if court packing were attempted. Franklin Delano Roosevelt attempted to pack the court after it ruled elements of the New Deal unconstitutional, notably a wage hike mandated by the National Industrial Recovery Act (Schechter Poultry Corp. v. United States, 1935). Roosevelt narrowly fell short of expanding the court after the Senate majority leader, a key ally, passed away unexpectedly. The S&P rallied when higher wages were struck down but there are many reasons for these developments – industrial production was rallying at the time, and when industrial production recovered later, and court packing was ruled out, the market remained low. At minimum one cannot say the case was inconsequential to the market (Chart 13). Chart 13FDR Tried To Stack The Courts

FDR Tried To Stack The Courts

FDR Tried To Stack The Courts

In a more recent example of a Supreme Court ruling having a substantial market impact, the court ruled with a narrow five-to-four vote to uphold the legality of most of the Affordable Care Act, or Obamacare, the signature legislative effort of Obama’s presidency (National Federation of Independent Business v. Sebelius, 2012). The market reaction at that time was positive, even in the health care sector, as the result removed uncertainty. Only later, in 2015, when the major provisions of the law took effect, did the sector start to feel the negative effects (Chart 14). It is reasonable to expect that any showdown over a major piece of legislation and the courts would have a similar impact today: the market would struggle with uncertainty but rally on the verdict. Chart 14Supreme Court Ruling On Obamacare Had Market Impact

Supreme Court Ruling On Obamacare Had Market Impact

Supreme Court Ruling On Obamacare Had Market Impact

Otherwise the Supreme Court’s ideological balance will likely be in place for a while. Justice Stephen Breyer, appointed by President Clinton, is 82 years old while Justice Clarence Thomas, appointed by President Bush, is 72 years old. The other justices are all younger than 66, meaning that conservatives would retain a five-to-four advantage even if Biden had the chance to replace both Breyer and Thomas. Bottom Line: As things stand, court packing is out of reach, more so than removing the filibuster, and therefore the current Supreme Court balance will remain an effective check on the Biden administration. Investment Takeaways The judicial system will become the major check on the Biden administration if its second reconciliation bill contains surprisingly ambitious and controversial provisions or if the Democrats ever get the votes to remove the filibuster. Otherwise the court is primarily a check on Biden’s executive orders. Climate policy is a likely area of friction given that the Biden administration will attempt to pioneer new areas of federal involvement in raising the cost of private industry when it comes to carbon emissions. At the same time the court could insist that the digital arena is a common forum where different voices must be heard, which could open the way to competitors to the tech giants. While the energy sector faces policy risks, it is favored by cyclical economic factors and will also benefit from checks and balances. Whereas the tech sector is not cyclically favored and could face some pushback from courts regarding competition (Chart 15). US rule of law is mostly intact. The selloff in the dollar and treasuries is driven by cyclical factors, not a structural loss of confidence in the rule of law or the American legal and political system. The Trump saga did not in itself trigger a collapse of the US dollar or government bonds – what did that was the Federal Reserve’s shift back to ultra-easy policy and the blowout fiscal spending stemming from the COVID-19 crisis. The US dollar is bouncing on the strong outlook for the economy as well as political stabilization. Chart 16 highlights that this is a near-term risk to cyclical sectors. Assuming the dollar resumes its cyclical weakening path it will power the next leg of outperformance for these sectors. Chart 15Courts Could Impact Energy, Tech

Courts Could Impact Energy, Tech

Courts Could Impact Energy, Tech

Chart 16Dollar Bounce A Near-Term Risk To Cyclical Outperformance

Dollar Bounce A Near-Term Risk To Cyclical Outperformance

Dollar Bounce A Near-Term Risk To Cyclical Outperformance

Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1Political Risk Matrix

Court Rulings And The Market

Court Rulings And The Market

Table A2Political Capital Index

Court Rulings And The Market

Court Rulings And The Market

Table A3APolitical Capital: White House And Congress

Court Rulings And The Market

Court Rulings And The Market

Table A3BPolitical Capital: Household And Business Sentiment

Court Rulings And The Market

Court Rulings And The Market

Table A3CPolitical Capital: The Economy And Markets

Court Rulings And The Market

Court Rulings And The Market

Table A4Biden’s Cabinet Position Appointments

Court Rulings And The Market

Court Rulings And The Market

Footnotes 1 The World Bank uses expert judgment and opinion polls to evaluate rule of law, defined as quality of contract enforcement, property rights, and functioning of the law and justice systems. Biases stem from the policy elite and non-governmental organizations of the western world. For instance, Hong Kong’s high rankings have all too predictably been undercut by Communist China’s power grab there. 2 Polarization escalated after Roe v. Wade and similar rulings that legalized abortion (1973), the Bush v. Gore ruling that decided the 2000 election, the NFIB v. Sebelius ruling that approved the Affordable Care Act (2012), and the Obergefell v. Hodges ruling that legalized gay marriage (2015). 3 The individual mandate is not expected to get shot down by the court this year, though it is conceivable. Even so, Biden’s second reconciliation bill would give the Democrats the chance to respond to any court ruling on health care reform. Biden’s health initiatives of automatic enrollment and government-provided insurance will be challenged but do not seem as controversial as the individual mandate in principle.

BCA Research’s US Political Strategy service concludes that the current Supreme Court balance will remain an effective check on the Biden administration. During the 2020 campaign, several leading Democratic Party figures suggested the party could increase…

At first blush, the message from February’s US CPI print is that the feared inflationary spike being priced into bond yields has not yet materialized. Core CPI continues to ease, falling to 1.3% y/y versus expectations it would remain unchanged at January’s…

Upgrade Autos & Components And Consumer Discretionary To Neutral

Upgrade Autos & Components And Consumer Discretionary To Neutral

Neutral Our 5% rolling stop in the S&P automobiles & components was triggered intraday yesterday on the back of the slipping 10-year Treasury yield, forcing us to crystalize 29% in relative gains and move this early cyclical sub-group from underweight to neutral. This shift also lifts the S&P consumer discretionary sector to a benchmark allocation, locking in gains of 7.5% since the January 25, 2021 inception. Both of these indexes are hypersensitive to rising interest rates as their end-demand user is ultimately the consumer who does not like climbing borrowing costs. Moreover, TSLA in particular commands an astronomical forward P/E and a stratospheric forward P/S, underscoring that rising interest rates weigh heavily on lofty multiples. The opposite is also true. While the US 10-year Treasury yield is likely to rise further in coming months on the back of mounting inflationary pressures, the velocity and ferocity of the up-move in yields year-to-date is in desperate need for a breather. A period of indigestion looms for the 10-year Treasury yield as there is also a near-term self-limiting aspect to the bond market’s selloff (please look forward to tomorrow’s US Sector Insight that will feature further analysis on the 10-year US Treasury and equities). Bottom Line: Book gains of 29% and 7.5% in the S&P automobiles & components and the S&P consumer discretionary indexes, respectively, since the January 25, 2021 inception, and upgrade to neutral.