United States

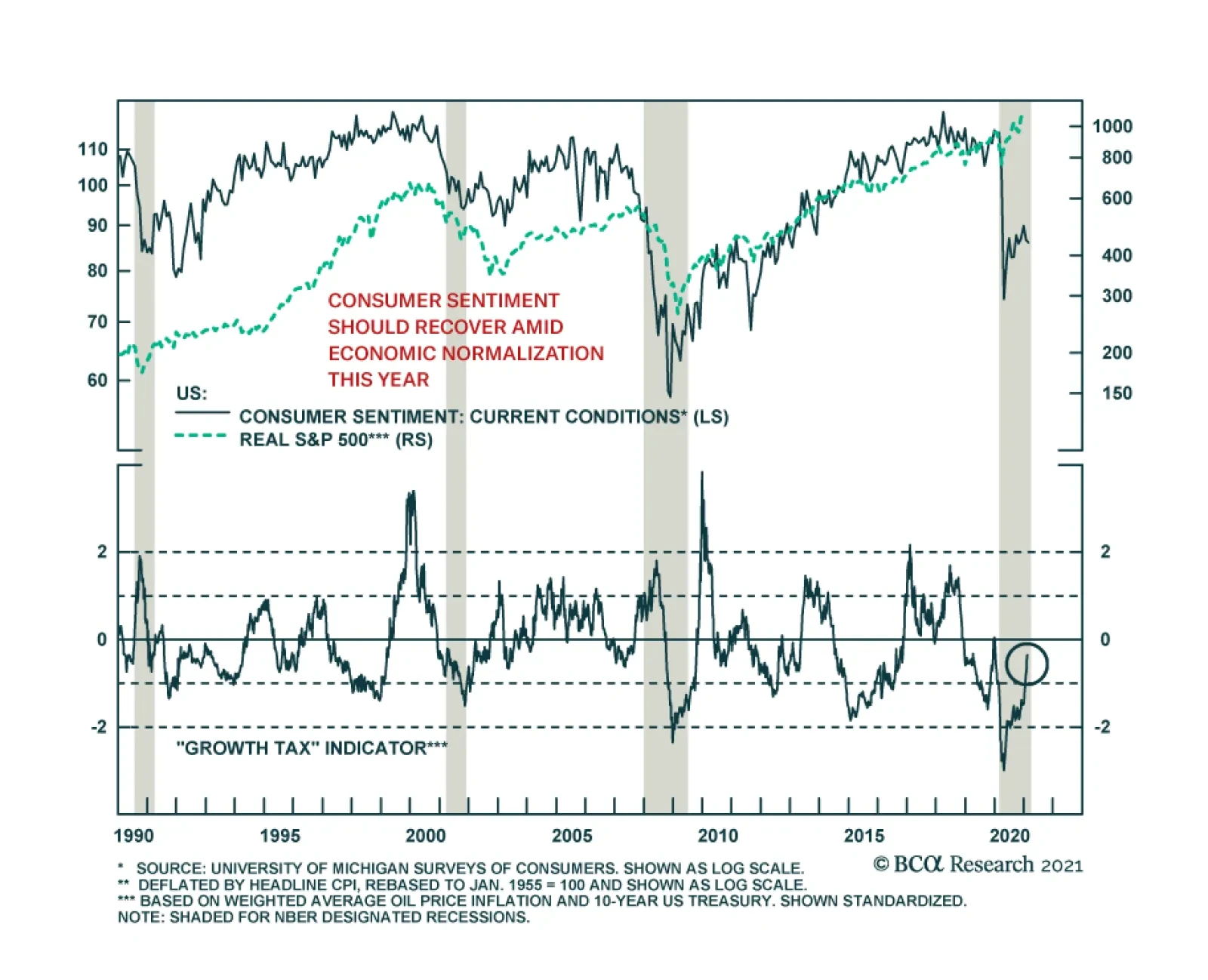

The preliminary release from the University of Michigan’s Survey of Consumers was a significant disappointment, revealing a large decline in sentiment in February. The headline index fell 2.8 points to 76.2, the lowest since August and significantly below…

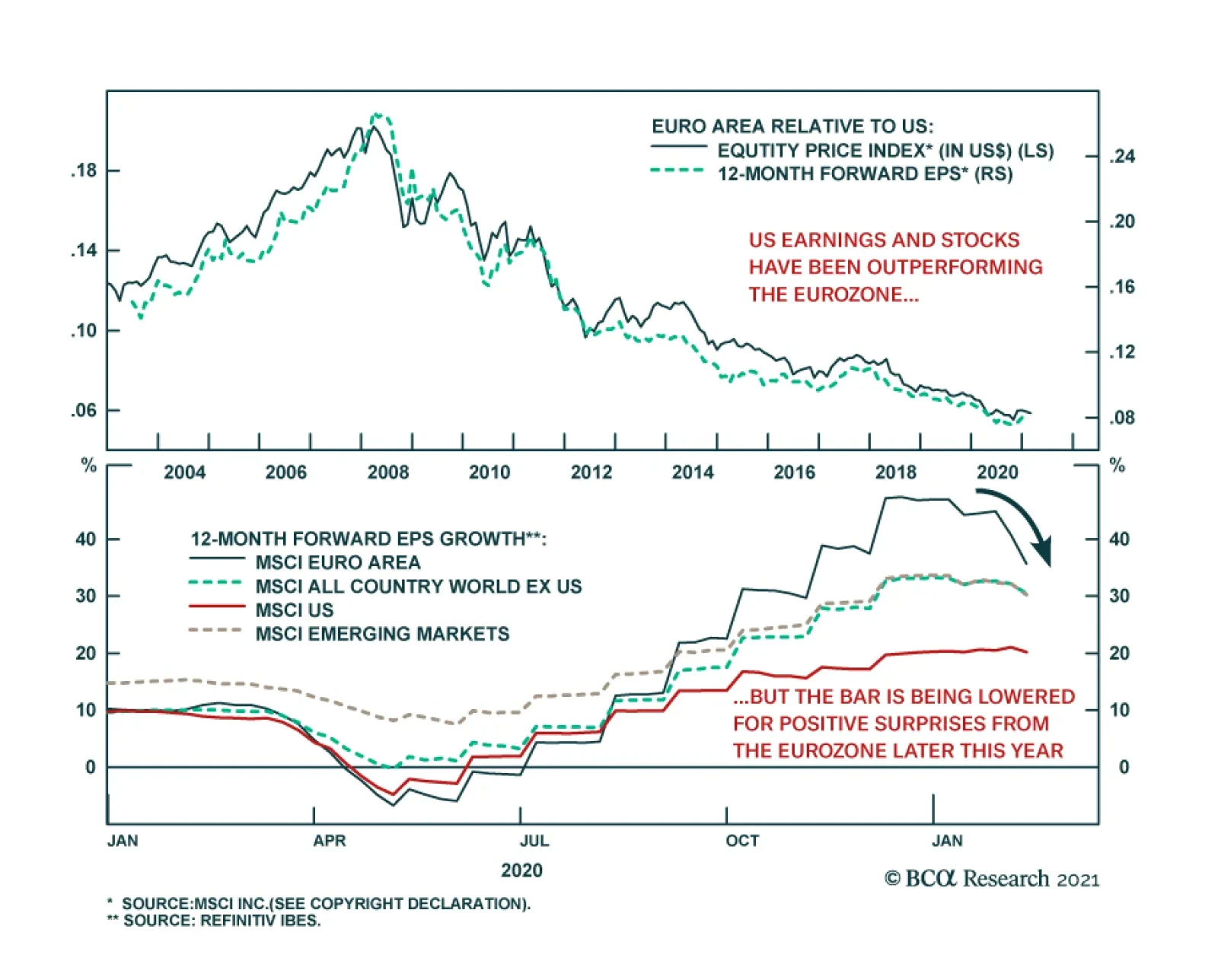

European equities lagged US ones throughout the bulk of last year, and continue to do so in 2021. Several factors explain this mediocre performance. The euro’s strength tightened monetary conditions in the euro area and is weighing on corporate…

Prepare To Lock In Gains In The Cyclicals/ Defensives Portfolio Bent

Prepare To Lock In Gains In The Cyclicals/ Defensives Portfolio Bent

Chinese data is waving a red flag as we highlighted in this Monday’s Strategy Report where we also instituted a 2.5% rolling stop to the cyclicals vs. defensives ratio. Not only are the Chinese authorities trying to engineer a slowdown with the recent reverse repo operations, but also BCA’s China Monetary Indicator and the selloff in the Chinese sovereign bond market are all corroborating the economic deceleration signal (top & middle panels). Railway freight (and infrastructure spending) data also highlight that not everything is as rosy as it appears to the naked eye in the Middle Kingdom, giving us even more reasons to worry about the longevity of the US cyclical/defensive bull market run (bottom panel). Finally, the cyclical/defensive ratio is sitting 14% above its 200-day moving average confirming the dual stretched message that our valuation and technical indicators are emitting (not shown). Bottom Line: We put a 2.5% rolling stop on the cyclicals vs. defensives ratio in order to protect gains north of 17% since inception. Should it get triggered, we will downgrade the ratio from overweight to neutral via trimming the niche materials sector to a benchmark allocation. Stay tuned.

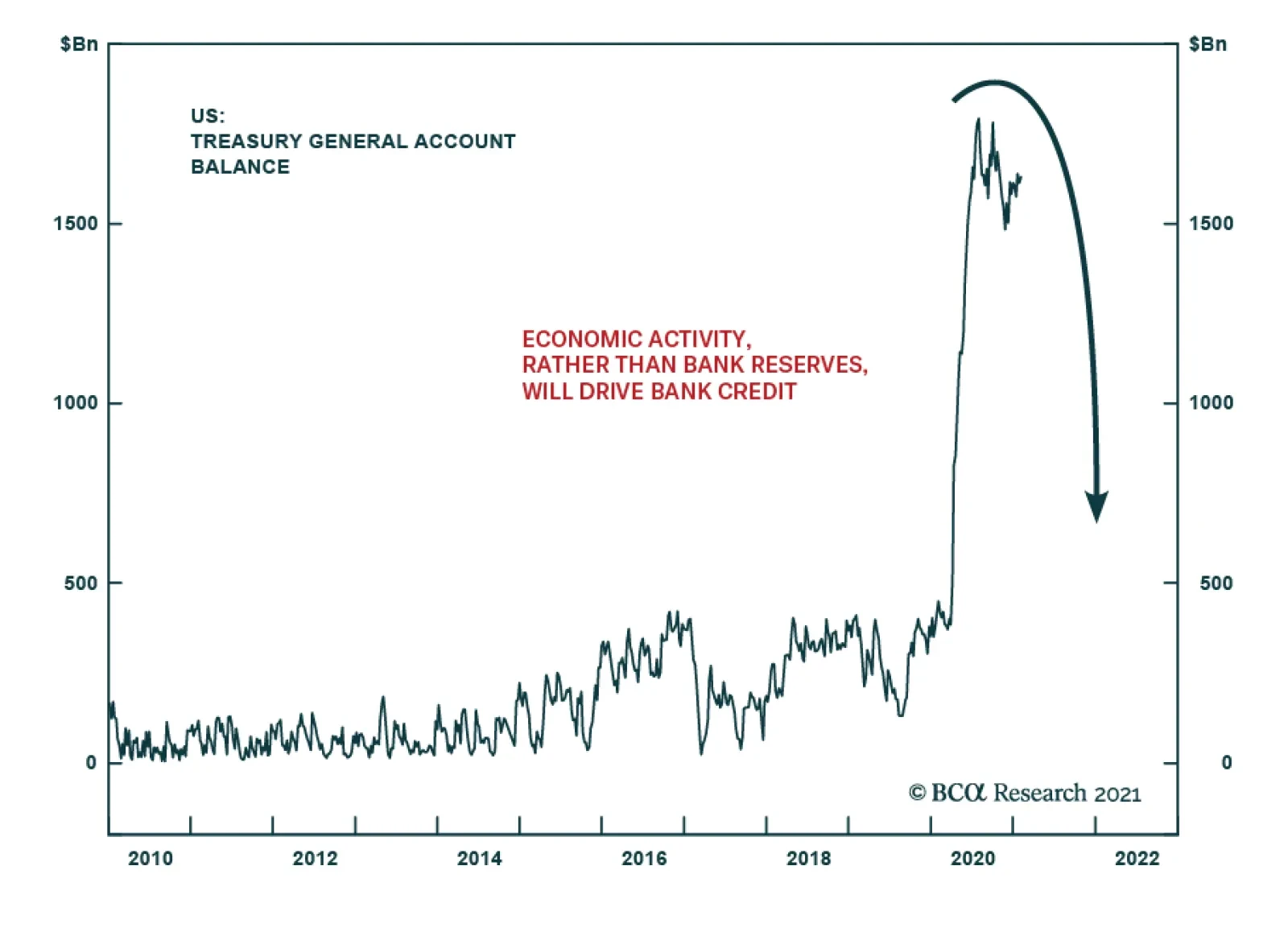

The Treasury Department recently released its financing estimates for the next two quarters. In the release, it indicated plans to reduce its general account (TGA) at the Fed to $800 billion by end-March and $500 billion by end-June. At $1.6 trillion, the TGA…

Closing & Rolling SPY Synthetic Long

Closing & Rolling SPY Synthetic Long

On the January 12 Insight we recommended investors put on a synthetic long SPY position using March 19th, 2021 long SPY $390/$410 call spread financed by a $340 put for a total debit of $0.8/contract, with a max payout of $20/contract. This options structure enabled us to participate on the melt up and concurrently not deploy a significant amount of capital. Today, this 3-legged option strategy has run a long way to the $6.21/contract mark for a 676% return since inception. Given that these gains accrued in just under a month, we are compelled to monetize them and roll the position over to the June expiry. This time, we are buying June 18th, 2021 long SPY $400/$420 call spread and financing it with a $340 put for a total debit of $0.3/contract. Once again this is a covered position recommendation, meaning that we postpone deploying capital today at $390 on the SPY and would rather go long by June at $340. Were the SPY to continue galloping higher in the next few months we would also participate in the mania via the long call spread segment of this option strategy. Bottom Line: Book healthy gains of $5.41/contract or 676% since inception in our synthetic SPY long position and roll it to June via a $400/$420 call spread financed by a short $340 put for an outflow of $0.3/contract and max payout $20/contract.

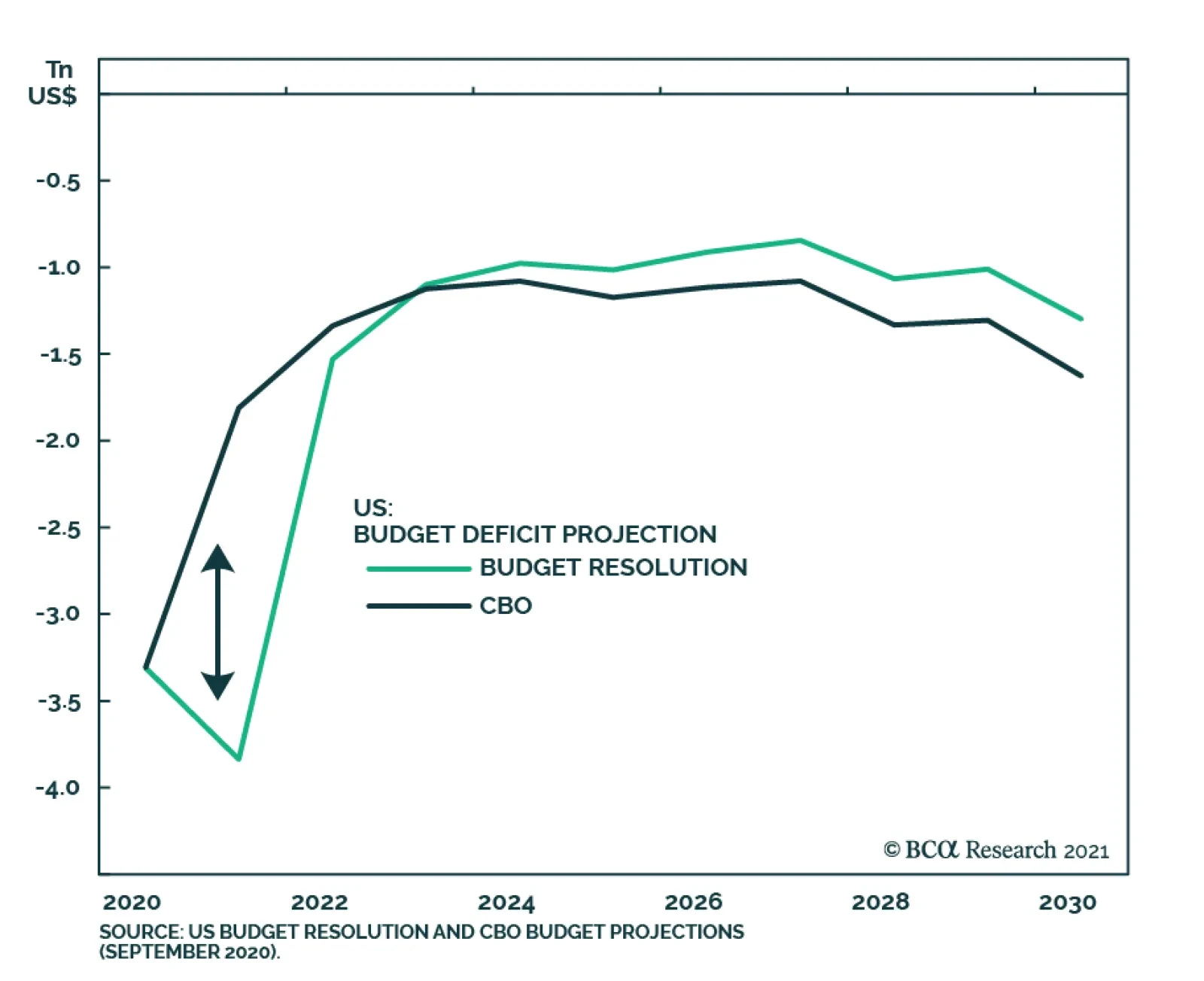

Highlights The Biden administration’s budget reconciliation bill will close the output gap, so markets will have to start thinking about upcoming tax hikes, rising wages, and eventual Fed interest rate hikes. Biden’s lax immigration policies will not have a major negative impact on wage growth. A doubling of the minimum wage, which could still make it into one of two budget reconciliation bills, would include a measure to index the post-2026 minimum wage to the average rate of wage rises. Biden’s industrial policy and support of labor unions would also increase wages. Stay long Treasury inflation-protected securities versus duration-matched Treasuries and long value stocks over growth stocks. Feature The Senate and House of Representatives passed a concurrent resolution on the budget for FY2021, the first step in the budget reconciliation process that will enable Democratic leadership to pass President Joe Biden’s $1.9 trillion American Rescue Plan with only a simple majority in the Senate. The budget resolution is a fantasy that the ruling party uses to bypass the Senate filibuster, as was the case under George W. Bush, Barack Obama, and Donald Trump. The latest such resolution claims that the budget deficit will be smaller, not larger, after the Biden rescue plan than what is currently projected by the Congressional Budget Office (Chart 1). It envisions the entire $1.9 trillion being spent in 2021 and then a huge drop in expenditures in 2022. A fiscal cliff ahead of the 2022 midterm election will not occur. Instead the second budget reconciliation maneuver, for FY2022, will increase spending levels once again with infrastructure and green projects, as per Biden’s campaign platform. Chart 1Democrats Pass Budget Resolution

Biden Opens The Border

Biden Opens The Border

The FY2021 budget resolution does not contain any tax increases, “revenue offsets,” to keep the budget in line because the COVID relief is emergency spending that is one-off, not recurring. The FY2022, however, will aim partially to repeal President Trump’s tax cuts. As such financial markets will continue to “buy the rumor” of additional fiscal spending for now but they will also sell the news given that the next reconciliation bill will push up inflation expectations even further, hasten the Federal Reserve’s policy normalization, and include tax hikes. And the current buy-the-rumor phase could be interrupted anyway by Biden’s immediate foreign policy challenges. Larry Summers And The Output Gap Democrats will err on the larger side of the $1.9 trillion stimulus because they regret erring on the smaller side back in 2009. But it is still possible for the price tag to be knocked down to around $1.5 trillion given that the economy is recovering and several moderate Democrats will balk at the enormous size. After all, $900 billion passed at the end of the year is not yet spent. Biden has already compromised by raising the eligibility requirements for households to receive $1,400 stimulus checks. Larry Summers, a frequent guest at the annual BCA conference and a veteran of the Clinton and Obama White Houses, has stirred up a firestorm over the past month by warning that too much federal money spent on short-term cash handouts today would crowd out the administration’s political capital and the amount of deficit spending that is available for long-term, productivity-enhancing investments. Summers warned that the current proposed stimulus is three times larger than required to fill the output gap. Chart 2 shows the output gap from 2009-12 and projected from 2021-24 alongside the size of the relevant stimulus packages to illustrate his point. Treasury Secretary Janet Yellen defended the $1.9 trillion price tag – like Summers, she is not normally one to worry about overheating the economy, but unlike Summers, she is now an administration official. She predicted that this size of package would bring the economy back to full employment by next year. The Congressional Budget Office, based on earlier congressional actions, had predicted employment would not return to its pre-COVID level until around 2024. The administration will look to Yellen now and in future to make the call on when enough stimulus is enough. With inflation expectations recovering rapidly, the Fed could be forced to hike rates as early as late 2022, though we think 2023 is more likely given our methodological bias as political analysts. This means the scope for overheating is quite large – a point reinforced by the comparison with the economic recovery back in 2009 (Chart 3). Summers’s criticism is not remiss and could come back to haunt the administration.1 When inflation picks up, the Fed will have to allow an overshoot according to its new policy of targeting average inflation. But once it is assured, it will have to start hiking rates. And once it starts hiking rates it could trigger a recession. Plus, even if we set recession risks aside, Summers’s critical point is that too much stimulus today will reduce the political and budgetary scope for Biden’s long-term agenda, which includes what will likely be his second major bill focused on infrastructure and renewables. The reconciliation process makes it highly likely that Democrats will drive through this initiative through the Senate but not if moderate Senate Democrats balk in the face of rising budget deficits and inflation. Chart 2How Much Is Too Much Stimulus?

Biden Opens The Border

Biden Opens The Border

Our base case still holds that Democrats will pass both reconciliation bills over the next roughly 12 months but investors should keep Summers’s warning in mind. Chart 3Recovery Is Ahead Of The Previous Cycle

Recovery Is Ahead Of The Previous Cycle

Recovery Is Ahead Of The Previous Cycle

There are tailwinds for Biden’s agenda. First, his political capital is moderate-to-strong and likely to strengthen over the coming year. It will get bumped up by improving economic conditions, including most recently a marked decline in bankruptcy filings from Q3 to Q4. Our updated Political Capital Index is shown in the Appendix. Second, concern about budget deficits has eroded, as Republican fiscal largesse showed under Trump – the pandemic and atmosphere of crisis greatly reinforce this point. Third, divisions in the Republican Party have produced as many as five moderates who could assist Biden in winning close legislative votes – even beyond the relatively easy passage of the American Rescue Plan in his honeymoon period. This Republican Party split is the only significance of President Trump’s second impeachment. Trump’s legal woes will continue after he is acquitted in the Senate. The deeper Republicans are divided over Trump’s legacy the harder time they will have recovering in the 2022 midterms, where opposition parties are normally favored. But the Biden administration’s leftward agenda will bring Republicans together, especially once the country moves out of the crisis. One of the biggest battles looms over the southern border. Bottom Line: The $1.9 trillion American Rescue Plan will more than close the output gap and yet it is only one of two budget reconciliation bills that the Biden administration will seek to pass over the next 12 months. There are still domestic and international factors that could impede the recovery, not least China’s policy tightening, but the risk of excessively short-term stimulus at the expense of long-term public investment is clear. Republicans Will Regroup Over Immigration To Summers’s warning about Biden’s legislative window of opportunity, recall that President Trump never achieved his signature 2016 policy promise – to build a wall on the border with Mexico – because congressional Republicans led him to prioritize repealing and replacing the Affordable Care Act (which failed) and passing the Tax Cut and Jobs Act (which succeeded). There was no political capital left for a major legislative push on the border and immigration. Immigration is one of the areas where Biden has a major incentive to push his policies aggressively. Immigrants tend to skew Democratic in their party affiliations. Americans increasingly believe immigration should be increased, a trend that accelerated after Trump’s election on an avowedly anti-immigration platform (Chart 4, top panel). Today 34% believe it should be increased in addition to 36% who are comfortable with the current level. Meanwhile the number who believe it should be decreased has fallen to 28%, down from 34%-38% around the time of Trump’s election. An anti-immigration candidate may be able to win within the Republican Party (especially under the specific circumstances of 2015-16) but he or she will have trouble winning general elections. Trump himself discarded the topic in the 2020 race. For Democrats, immigration is also probably the single most effective way to drive a wedge between the populist and establishment factions of the Republican Party. For example, establishment Republican presidents oversaw huge infusions of foreigners into US society, the 1986 Immigration and Reform Control Act, which granted amnesty to three million illegal immigrants, and the 1990 Immigration Act, which increased the quota of legal immigrants. By contrast Trump rose to power by attacking the bipartisan consensus on “open borders.” As long as a substantial cohort of Republicans defends immigration on free market principles, and upholds the corporate interest in having plentiful availability of lower wage seasonal and specialized workers, the party will be divided. The above points explain why the Biden administration will pursue immigration reform more intently than public opinion would leave one to believe. Polls show that voters want to focus on the economic recovery, the pandemic response, and social and civil rights policies more than immigration. There is no question that Biden is prioritizing the pandemic, the economy, and health care (Chart 4, bottom panel). But the Democratic Party has a strategic interest in expanding immigration so Biden will continue to plow forward with executive orders and comprehensive immigration reform in Congress. The US does need immigration reform – to ensure the flow is orderly. President Trump’s “wall” proposal did not come out of nowhere. Like the “Know Nothing Party” that emerged in the 1840s and rose to prominence in the 1850s, the Trump movement arose amid a historic increase in the foreign-born share of the population (Chart 5). But Trump’s policies hardly made a dent in the flow of legal immigrants into the US. Now Biden will reverse them and encourage more incomers. Therefore immigration will persist as a bone of contention in the 2020s. Granted, immigration has amply attested positive effects on the economy – including most clearly by lifting the US’s fertility rate so that it does not suffer from as rapid of an aging process as other developed countries. Indeed, voters are primarily concerned about illegal, not legal, immigration. Still, Republicans will struggle to walk the line between tighter immigration policies and appealing to an audience beyond “old white folks.” This suggests the Biden administration has room to run. Chart 4Public Not Too Concerned About Immigration

Public Not Too Concerned About Immigration

Public Not Too Concerned About Immigration

Chart 5Historically Large Foreign-Born Population

Biden Opens The Border

Biden Opens The Border

It helps Biden that the post-World War II and post-Cold War booms in legal immigration are relatively measured when compared to the overall population. The inflow of migrants was around 0.3% in 2019, very far from its post-war peak of 0.7% per year (Chart 6). Thus the Biden administration will not be overly concerned about being too progressive on this issue. Chart 6Boom In Legal Immigration Less Impressive Relative To Population

Biden Opens The Border

Biden Opens The Border

Chart 7Detainees On The Mexican Border

Biden Opens The Border

Biden Opens The Border

Illegal immigration is the biggest factor motivating periodic public backlashes such as in 2016. Southwestern border apprehensions – the only credible way to measure the unauthorized flow of people over the Mexican border – spiked under President Obama as well as President Trump, though US agents detained nowhere near the numbers witnessed in the 1980s and 1990s (Chart 7). The stock of illegal immigrants in the US ranges from 10-11 million and has remained flat, or fallen slightly, since the financial crisis of 2008. The weakening of the US economy, in the context of tighter border security, reduced incentives to make the difficult journey (Chart 8). The fact that President Obama and Trump increased detentions suggests that the demand to get into the country recovered over the course of the last business cycle. Based on President Biden’s voting record in the Senate and statements during the 2020 campaign, he is not an ultra-dove on the border – but his party has moved to the left on the issue. This is clear from his rivals’ positions in the Democratic primary election. Even his Vice President Kamala Harris, who was not the most radical on stage, supported decriminalizing illegal border crossings and downgrading Immigration and Customs Enforcement. Still, until Democrats repeal the filibuster in the Senate, they will not have a chance of passing comprehensive immigration reform with Republicans unless they accept stronger enforcement provisions. Biden voted for the 2006 Secure Fence Act but more recently has emphasized high-tech upgrades to better monitor crossovers. Harris also accepted high-tech security funding that did not involve building a wall. Even with these compromises, it will still be a stretch to find 10 Republicans willing to cross the aisle on this issue while Trump and his faction remain active to punish them in primary elections. Chart 8Estimate Of Total Illegal Immigrants

Biden Opens The Border

Biden Opens The Border

The demand to enter the US will revive once the pandemic is over. The big surge in illegal border crossings in the 1980s-90s coincided with a period in which US economic growth and wellbeing far outpaced that of Mexico and Central America (Chart 9). The gap in GDP per capita is the crudest possible measure and does not reflect the dramatic differences in quality of life that drive people to relocate. Nevertheless, the gap remains drastic, especially with Mexico. Chart 9The Grass Is Greener On The Other Side

Biden Opens The Border

Biden Opens The Border

The gap in current economic activity, such as manufacturing PMIs, between the US and Mexico is as wide as ever. Even as manufacturing contracts in Mexico, the demand for workers in US service industries is soaring (Chart 10). Moreover the US economic revival will be super-charged by the gargantuan fiscal stimulus of 2020-21 whereas Mexican government support for the economy is comparatively austere (Chart 11) Chart 10Super-Charged US Recovery Opens Big Gap With Mexico

Super-Charged US Recovery Opens Big Gap With Mexico

Super-Charged US Recovery Opens Big Gap With Mexico

Chart 11Less Government Support In Mexico Than US

Less Government Support In Mexico Than US

Less Government Support In Mexico Than US

Bottom Line: Biden is opening up the borders at a time of economic disparity between the US and Latin America that will lead to an influx of immigration. This is positive for US labor force growth and productivity but it will be hard to pass a long-term solution through Congress. The Republican Party is deeply divided on the issue today but it is likely to become a rallying cry as numbers of newcomers increase and as Trump-style populism remains an active force within the party. Immigration, Wages, And The Minimum Wage The macroeconomic and market impact of easier border and immigration controls boils down to the impact on wages. There is a vast literature on this subject and we will not pretend to be comprehensive. We will merely make a few observations. The foreign-to-native-born wage differential has narrowed substantially over the past twenty years. The discount to hire immigrants has shrunk from 24% to 15% (Chart 12). This is a reflection of the high demand for immigrant labor and especially the increase in high-skilled workers alongside the booming tech, legal, financial, personal care, and health care industries in the United States – the fastest growing sectors for foreign-born workers since 2003. Earnings growth for foreign workers is more cyclical than for native workers and has been rising faster in recent decades (Chart 13). Chart 12Immigrants Command A Higher Price Than They Used To

Biden Opens The Border

Biden Opens The Border

Chart 13Immigrant Wages Grow In Boom Times

Biden Opens The Border

Biden Opens The Border

Immigrants work the lowest-wage jobs and hence there is some correlation between the share of foreign-born workers in any given industry and the hourly wage, just as there was at the turn of the century (Chart 14). But it does not follow that an increase in immigration suppresses wages as a whole. Chart 15 shows that, over the last business cycle at least, a change in the foreign worker share of a given industry does not correlate with a change in wage growth. Of course, it stands to reason that increasing the supply of labor decreases the price. But not if demand is growing sufficiently to raise the price for all workers. As we have seen, since migrants are willing to undertake long and dangerous journeys for work, they are likely to go where the demand is strong and the price is right – and the flow drops when the jobs dry up. Chart 14Immigrants Work The Lowest Wage Jobs

Biden Opens The Border

Biden Opens The Border

Chart 15More Immigration Not Necessarily A Pay Cut

Biden Opens The Border

Biden Opens The Border

Academics debate the impact on wages. There could be a negative impact, especially for low-skilled native workers, but the aggregate effect is small. One study showed that wages for native workers fell by three percent cumulatively over the 20-year period from 1980-2000 due to immigration.2 This is not dramatic. We can test the connection between immigration and wage growth informally by plotting the growth of southwest border detentions and legal permanent residence admissions alongside that of real wages. There is no clear relationship either way (Chart 16). The same is true if we test it with real median wages – the surge in border apprehensions under President Trump coincided with a boom in wages across the spectrum. Chart 16Border Influx Does Not Suppress Wages

Border Influx Does Not Suppress Wages

Border Influx Does Not Suppress Wages

Thus we cannot rule out the possibility that the Biden administration’s relaxation of border controls will have a dampening effect on wages over the long run but we cannot endorse it either. Chances are that the rollout of COVID-19 vaccines and government spending will continue to power a recovery that tightens the labor market and lifts wages for most workers. What about the administration’s simultaneous policy of doubling the federal minimum wage to $15 per hour by the year 2026 – and indexing wage growth after that date to the median hourly wage? The minimum wage hike might yet make it into the budget reconciliation bill under negotiation – but Biden has already signaled it can be delayed. There is a growing fear about the negative impact on small businesses struggling during the pandemic. The Congressional Budget Office estimates that anywhere from 1 million to 2.7 million jobs could be lost in 2025 if the wage hike were implemented now and businesses would pay $333 billion.3 But the proposal will return when the second budget reconciliation bill is up for consideration unless the Senate parliamentarian rules it out, in which case its passage becomes much less likely. Only about 2% of workers are paid at or below the current minimum wage of $7.25 per hour so a minimum wage hike but the CBO estimates that 10 percent of workers would be below the proposed wage level by 2025 (Chart 17). The states with higher proportions of minimum wage workers will be the ones most affected and are mostly in the south, including South Carolina, Mississippi, Kentucky, and Texas, though there are a few in the north such as New Hampshire and Pennsylvania (Chart 18). Chart 17Most Workers Earn More Than Minimum Wage

Biden Opens The Border

Biden Opens The Border

Chart 18Minimum Wage Workers By State

Biden Opens The Border

Biden Opens The Border

Previous minimum wage hikes did not prevent the economy from reaching full employment – nor did they lead to a lasting pickup in overall wage growth. But indexation to overall wage growth would mark a big change in favor of an eventual wage-price spiral. It cannot be ruled out given that the reconciliation option might be available to Democrats, though it would not take effect till 2026. Bottom Line: There is no firm link between immigration growth and wage growth. Increased immigration flows often coincide with higher incomes and wages as growth and productivity improve. Meanwhile a change in the minimum wage will have a limited impact from a macro point of view alone but a bigger impact if it is indexed to wage growth after 2026, which is possible. In the coming years the much greater impact of Biden’s policies will stem from the massive infusion of fiscal spending he is likely to pass through Congress, which will close the output gap quickly and put upward pressure on wages. Investment Takeaways Easier immigration and a higher minimum wage are not the only Biden policies that will affect wages. One of the biggest developments since Biden took office is his confirmation that he will maintain a tougher trade policy than his predecessors, excluding Trump. Biden won the election among Midwestern blue collar voters at least partly by stealing Trump’s thunder on trade and globalization. Since taking office he has issued a “Buy American” executive order and declared that he will maintain “extreme” competition with China. His cabinet appointees – notably Antony Blinken at the State Department and Janet Yellen at the Treasury – have given words of warning to China over trade as well. Geopolitical risk is one reason we are cutting back on our participation in the market’s exuberance at the moment, given that critical foreign policy stances are likely to be tested early in Biden’s term. But there is also a long-term implication of the Democrats’ marginal increase in protectionism. It was the overall policy context of hyper-globalization that led to sluggish wage growth in the United States over the previous forty years. A major factor was the decline of manufacturing and unionization as a result of a lack of competitiveness in the US as global production came online. The erosion in manufacturing jobs only stopped in recent years (Chart 19). Popular support for unions has risen to levels last seen in the late 1970s and 1990s since the Great Recession – under Trump even Republicans talked up unions. Chart 19Blame Fall In Manufacturing, Not Foreign Workers, For Flat Wages

Blame Fall In Manufacturing, Not Foreign Workers, For Flat Wages

Blame Fall In Manufacturing, Not Foreign Workers, For Flat Wages

Biden’s policies outlined above are reminiscent of the “third way” Democrats in the 1990s – particularly Bill Clinton, who oversaw an increase in the minimum wage and a surge in both legal and illegal immigration. But on trade Biden is shaping up to be more like Trump than Clinton, albeit directing his protectionism more at China than other trade partners. His spending bills will also use fiscal spending to promote industrial policy. Meanwhile labor protections will go up and unionization will at least stem its multi-decade decline. For the stock market the risk of higher wages looms mostly due to the super-charging of the economy with stimulus. But shoring up domestic manufacturing, unions, labor perks and protections, and possibly indexing the minimum wage will contribute to faster wage growth and – to corporations – higher employment costs (Chart 20). This is a headwind to the corporate earnings outlook. But like the Biden administration’s tax hikes it is not yet affecting the market’s overall bullishness – and may not until the first reconciliation bill passes and the narrative shifts from stimulus to structural reform. Investors may soon find out that they will be dealing with higher wages, higher taxes, higher inflation, and a higher cost of capital. Chart 20Higher Wages, Lower Corporate Profits

Higher Wages, Lower Corporate Profits

Higher Wages, Lower Corporate Profits

Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Jesse Anak Kuri Associate Editor jesse.Kuri@bcaresearch.com Appendix Table A1APolitical Capital: White House And Congress

Biden Opens The Border

Biden Opens The Border

Table A1BPolitical Capital: Household And Business Sentiment

Biden Opens The Border

Biden Opens The Border

Table A1CPolitical Capital: The Economy And Markets

Biden Opens The Border

Biden Opens The Border

Table A2Political Risk Matrix

Biden Opens The Border

Biden Opens The Border

Table A3Biden’s Cabinet Position Appointments

Biden Opens The Border

Biden Opens The Border

Footnotes 1 See BCA Global Investment Strategy, “Fiscal Stimulus: How Much Is Too Much?” January 8, 2021, bcaresearch.com. 2 George J. Borjas and Stephen J. Trejo, “The Evolution of the Mexican-Born Workforce in the United States,” in Borjas, ed, Mexican Immigration to the United States (Chicago: Chicago University Press, 2005), pp.13-55. 3 See “The Budgetary Effects of the Raise the Wage Act of 2021,” Congressional Budget Office, February 2021, cbo.gov.

After bottoming in early August, US 10-year Treasury yields have risen steadily, just shy of the 1.2 mark. Do higher yields create a risk for equities? The dividend discount model provides some insight. The dividend yield can be expressed as a function of…

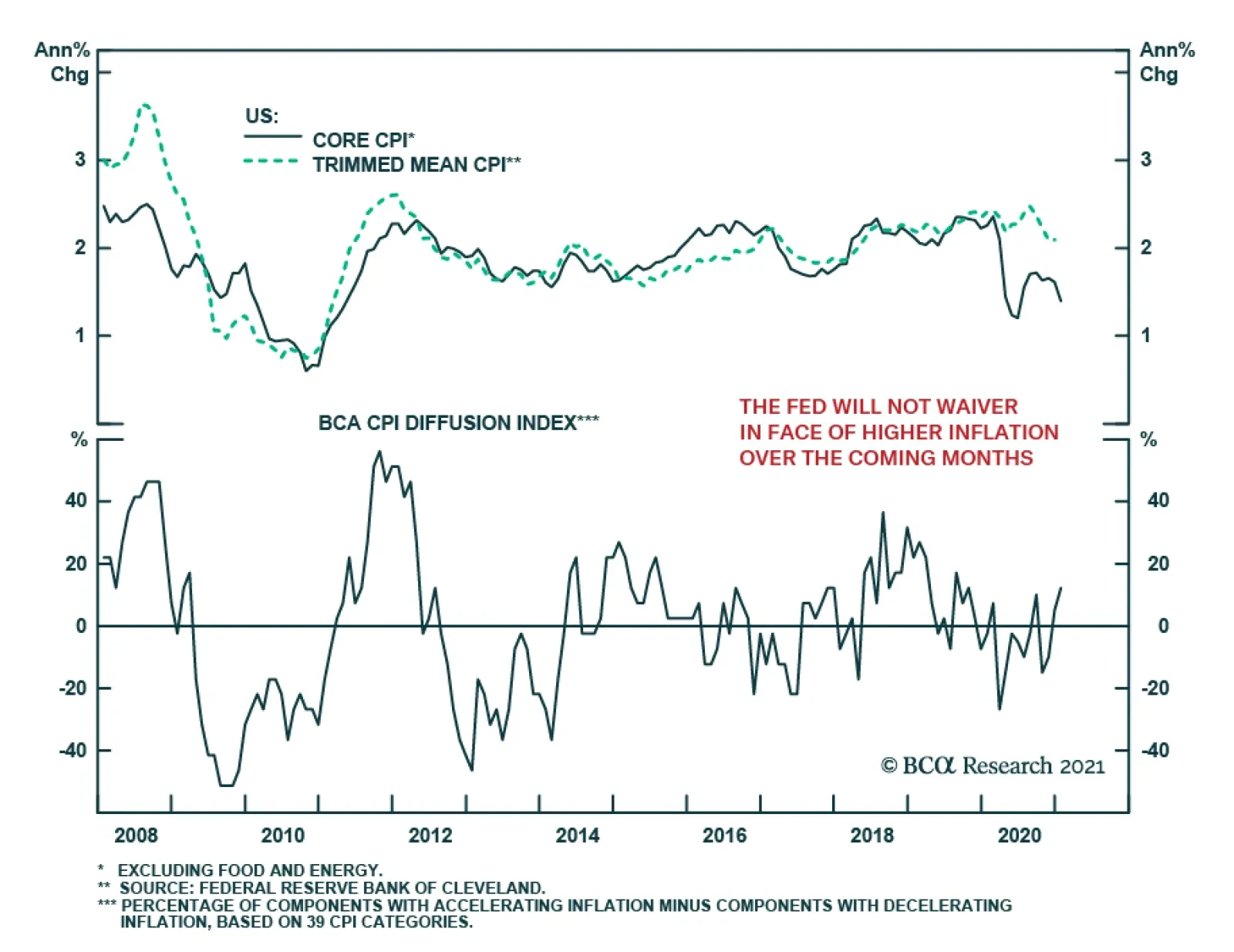

According to January’s CPI data, fears of rising inflation in the US are thus far unfounded. Headline and core inflation were both 1.4% y/y in January, slightly below expectations of 1.5% y/y for the two. For the core measure, this marks a slight downtick…

According to BCA Research’s US Political Strategy service, the Biden administration’s current budget reconciliation bill will lead to another reconciliation bill on infrastructure spending and green projects ahead of the 2022 mid-term election. The Senate…

Two Portfolio Changes And A Stop Buy Order

Two Portfolio Changes And A Stop Buy Order

Today we close two high-conviction trades and place a stop buy order for the June 2021 expiry VIX futures as a hedge to the remaining positions. Homebuilders have proven to be more resilient than we expected, especially given the selloff in the bond market. Clearly the US consumer is not concerned about a rebound in rates, at least not yet. Moreover, the looming fiscal stimulus will only facilitate more excesses, even in the residential housing market, as a fresh wave of liquidity will likely more than offset the tightening in monetary conditions. Thus, we have lost confidence in our high-conviction underweight stance in this niche consumer discretionary group and are taking a loss of 11% since inception. The S&P consumer staples sector was a natural high-conviction underweight given our end-2021 4,000 SPX target that we arrived at on the November 9 Special Report. Now that the market is within spitting distance of our target, the risk reward is no longer as favorable as it used to be for this defensive sector. Thus, we are closing this high-conviction trade today for a gain of 8% since inception. Finally, we successfully capitalized on our long VIX futures hedge to the tune of 19% recently, but given that volatility is settling down, it pays to institute a stop buy order for the June 2021 expiry VIX futures near the 25 mark. Bottom Line: Close the S&P consumer staples and the S&P homebuilding high-conviction underweights for 8% and -11% returns, respectively since the December 7 inception; and place a stop buy order for the June 2021 VIX futures at the 25 level.