United States

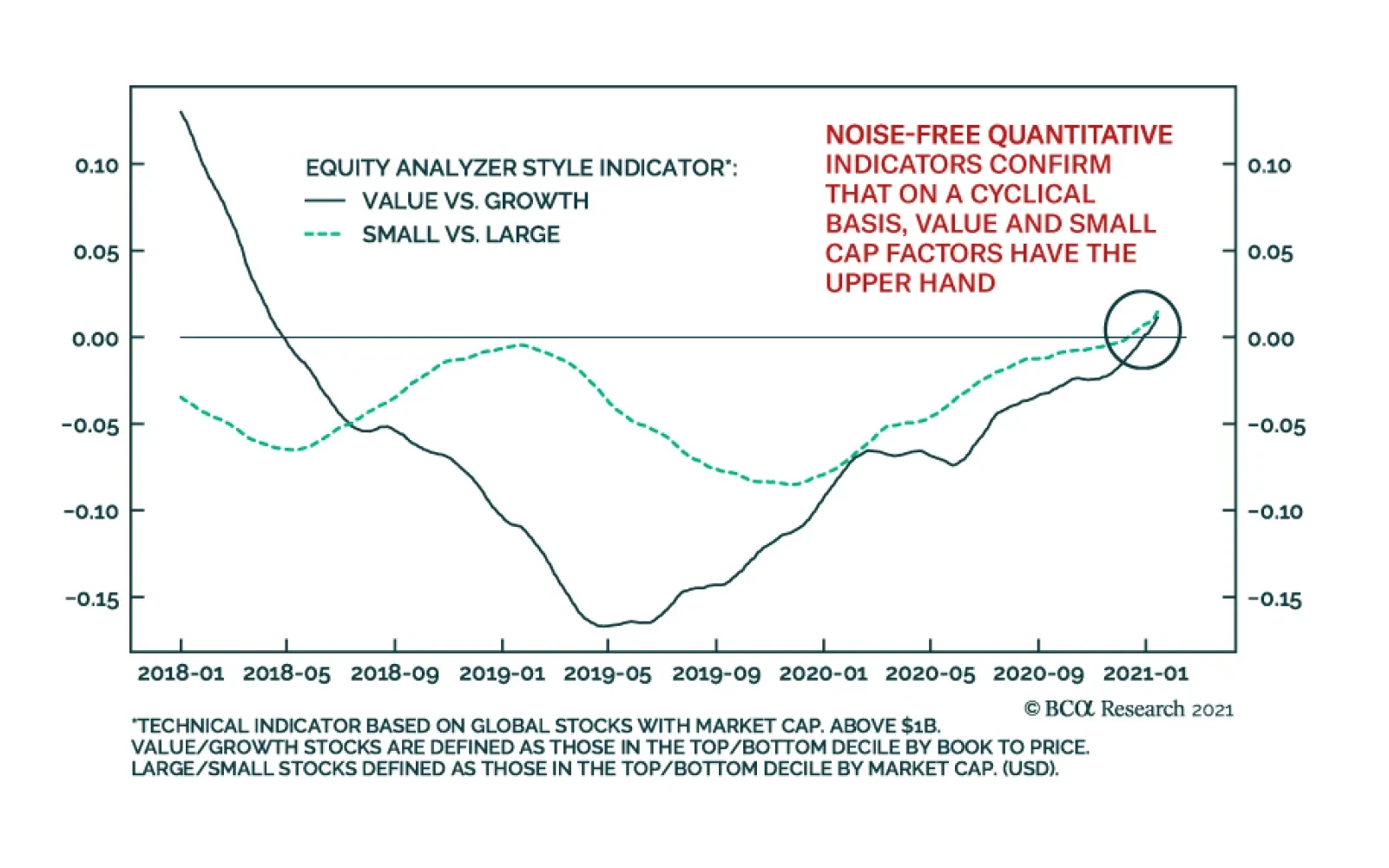

An important model shift has occurred over the past few weeks in Equity Analyzer (EA); our proprietary style factors now favor value over growth and small over large caps. These indicators represent the relative acceleration of value vs. growth and small vs.…

BCA Research’s Foreign Exchange Strategy service concludes that over the next one to three months, a garden-variety 5-10% correction in the S&P 500 will coincide with a 2-4% bounce in the DXY. An equity market correction is a potential catalyst that…

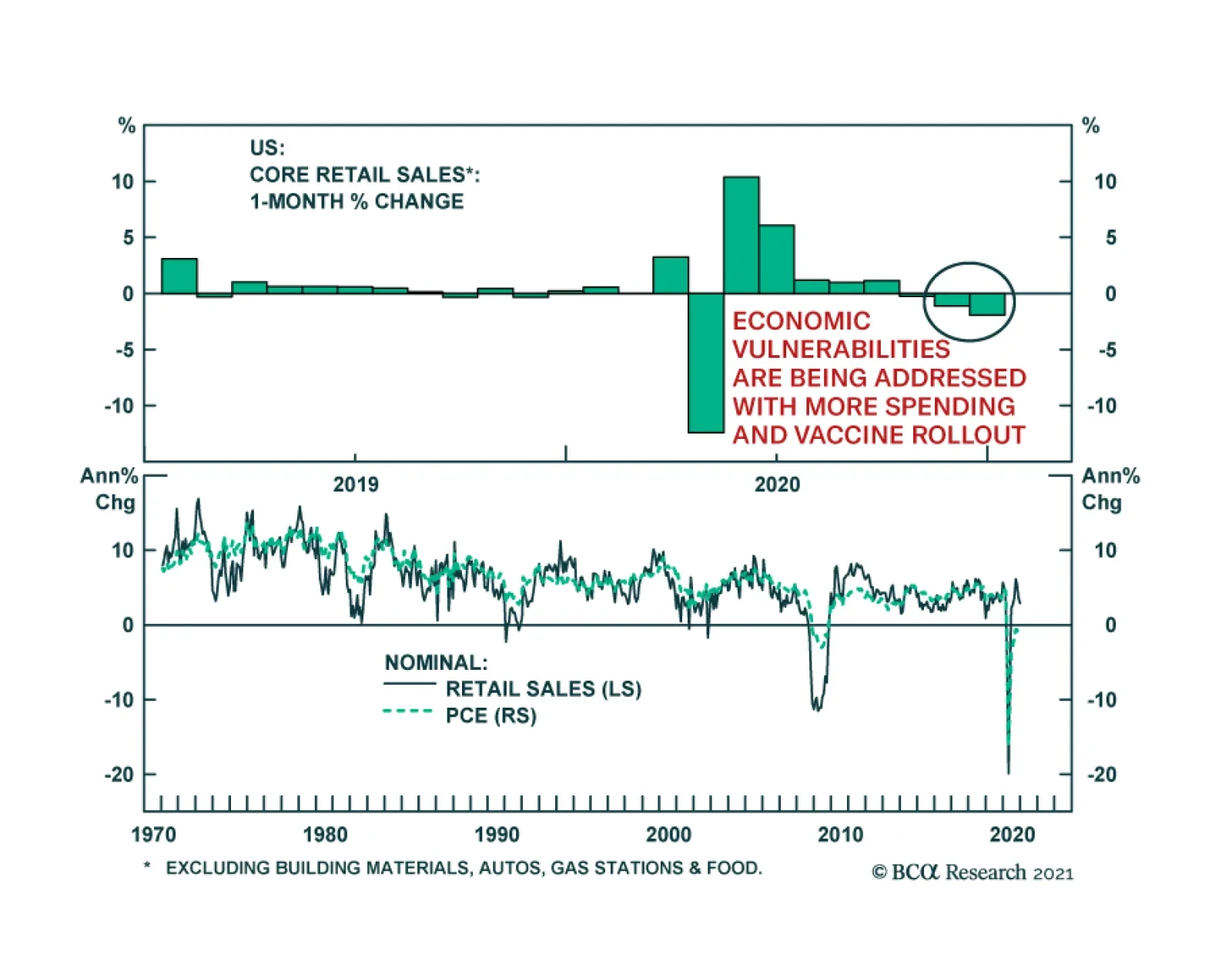

US retail sales were dismal in December. The headline figure fell 0.7% m/m, disappointing expectations of no change after a 1.1% m/m decline in November. Similarly, the retail sales control group, which corresponds more closely with the consumer spending…

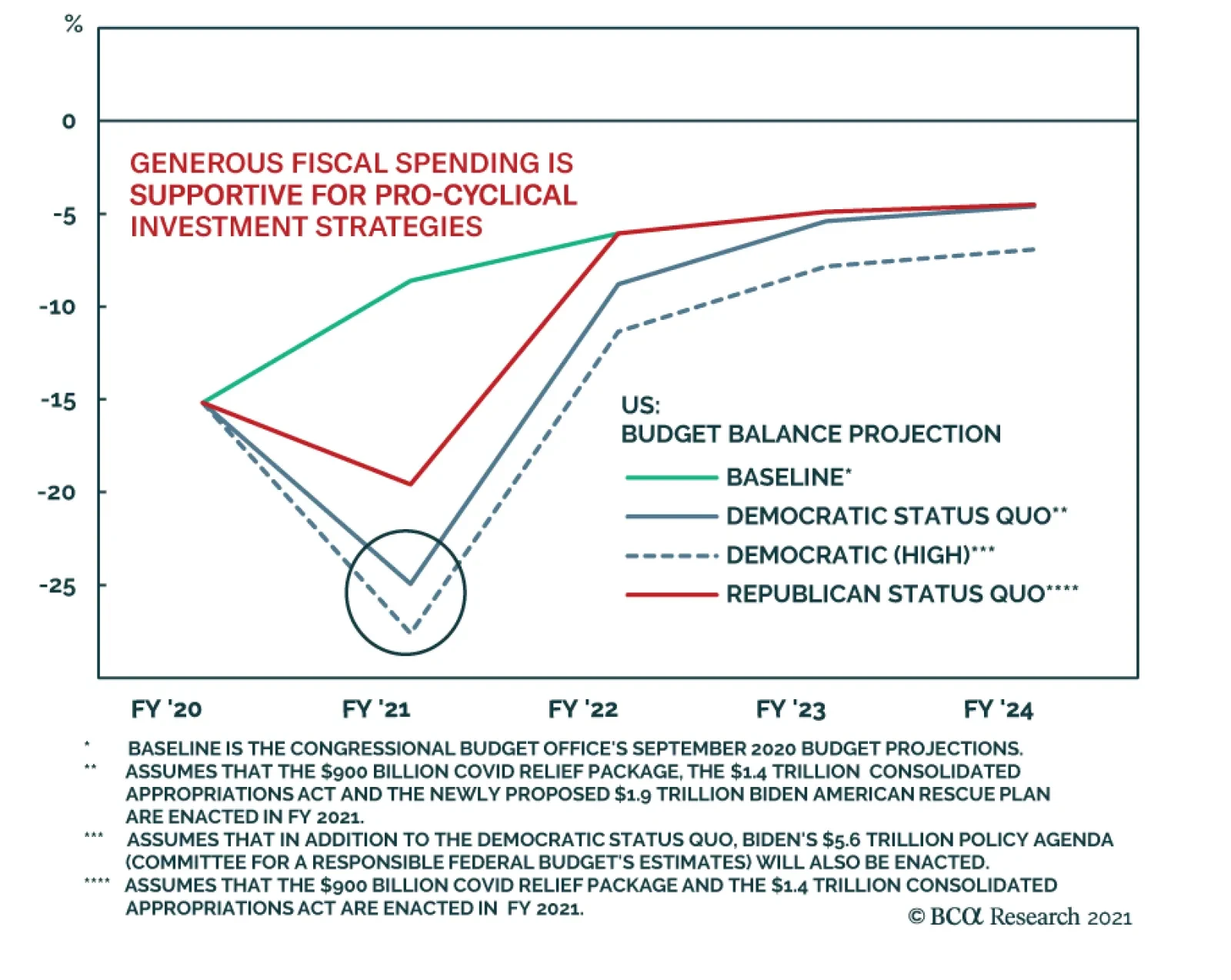

President-elect Joe Biden revealed his $1.9 trillion emergency relief package on Thursday, which in addition to the $900 billion bill passed by Congress in December, aims to act as a reflationary bridge until the pandemic is behind us. The plan includes…

Dear client, In lieu of our regular report next Friday, we will be sending you a special report on Australia next Tuesday, co-authored with our Global Fixed Income colleagues. We hope you will find the report insightful. Kind regards, Chester Highlights Any tactical bounce in the dollar should be limited to 2-4%. A barbell strategy is the most attractive positioning in the next one to three months: a basket of the cheapest currencies and some safe havens. Remain short the gold/silver ratio. Feature Chart I-1Dollar Downside Hits Q1 Forecasts

Dollar Downside Hits Q1 Forecasts

Dollar Downside Hits Q1 Forecasts

The market narrative towards the dollar is turning more bullish. Fundamental analysts point to the recent rise in US interest rates, relative to countries like Germany or the United Kingdom, as a serious cause for concern. A rules-based technical approach certainly warned that the dollar was getting much oversold last year, and the recent bounce is reinvigorating the possibility of a more powerful countertrend move. Being in the dollar-bearish camp, the key question is: how large could a potential dollar bounce be, and for how long can it last? According to Bloomberg forecasters, the dollar has already exhausted any potential decline penciled in for the first quarter of this year. Q1 consensus forecasts for the DXY index sit at 90, exactly where the index level rests today (Chart I-1). Bloomberg has consistently lowballed the level of the dollar since 2018, making the current forecast unduly bullish. This dovetails with recent market commentary that the decline in the dollar is largely done, and powerful catalysts for a countertrend move could take hold. Risks From The Reflation Trade Chart I-2A Stock Market Rout Could Derail The Dollar

A Stock Market Rout Could Derail The Dollar

A Stock Market Rout Could Derail The Dollar

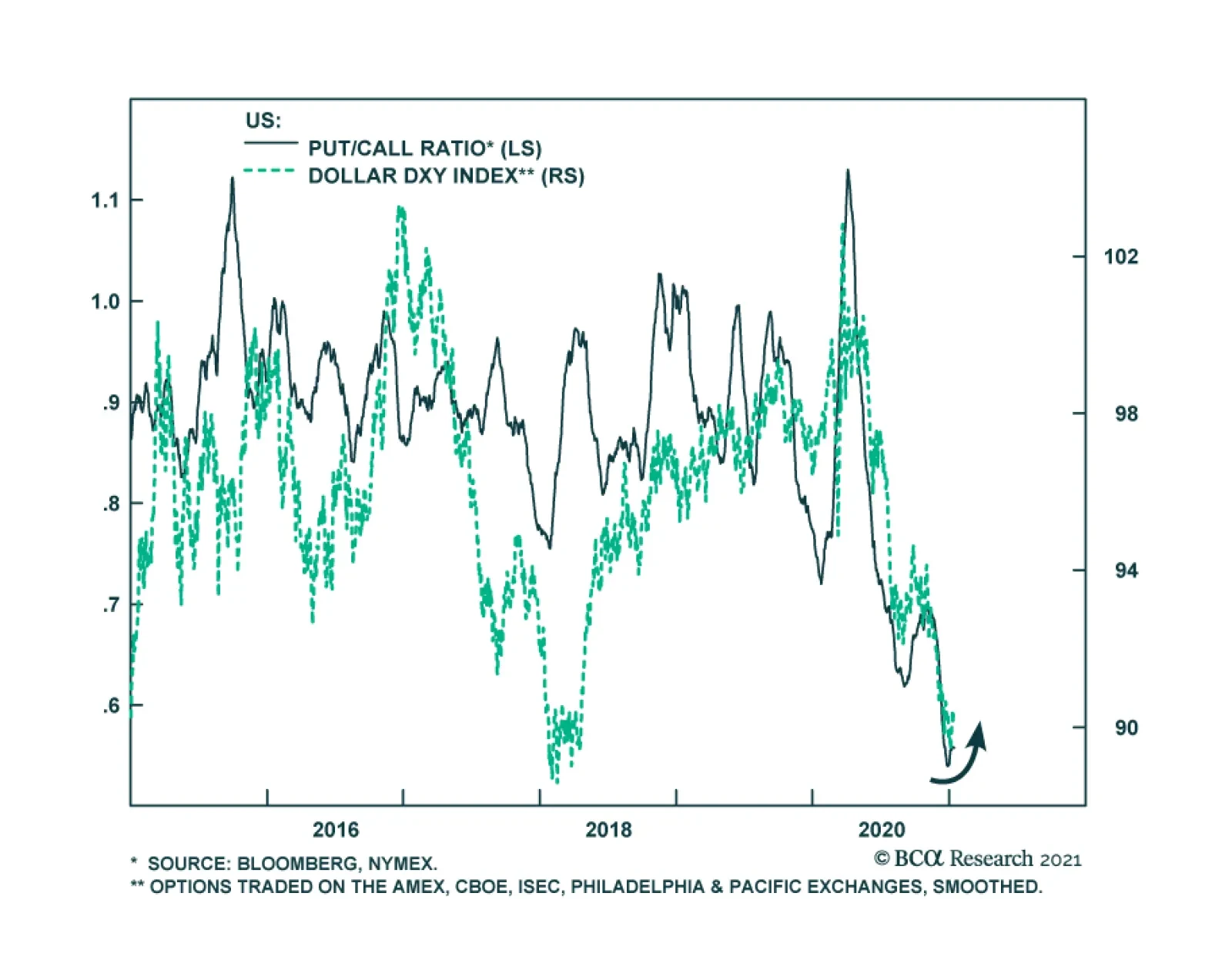

An equity market correction could be one of the potential catalysts that pushes the dollar higher. We showed last week that the dollar and the S&P 500 have had a near-perfect inverse correlation (Chart I-2). When a stock market and its currency exhibit an inverse correlation, it means that foreign investors have been hedging their equity purchases by selling the currency forward. This is not usually the norm (equity relative performance and currencies tend to move together), but was especially the case last year as inflows into US equities surged, but the dollar declined. Should any profit taking ensue, this will trigger a knee-jerk rally in the dollar, as forward shorts are closed. A few equity indicators warn that we could be at the cusp of such a counter-trend move: The put/call ratio in the US is extremely depressed. This warns that positioning is lopsided and could easily topple the equity market rally. A rising put / call ratio has been synonymous with a higher dollar over the past few years (Chart I-3). This will be consistent with foreign investors unwinding their dollar hedges (as they take profits on equities) and/or safe-haven inflows into the dollar. Chart I-3Both Puts And The Dollar Offer Protection

Both Puts And The Dollar Offer Protection

Both Puts And The Dollar Offer Protection

Cyclical stocks continue to outperform defensive ones of late, but the cracks are beginning to emerge, specifically in the industrials space. Industrials share prices have been relapsing of late (Chart I-4). The dollar tends to weaken when cyclical stocks are outperforming defensive ones, and vice versa. This is because non-US equity markets have a much higher concentration of cyclical stocks in their bourses. The huge correction in the relative performance of the global tech sector also warns that the tech-heavy US bourse might benefit from any bounce in tech equities. Global earnings revisions are heading higher, but the momentum of US earnings has regained the upper hand, especially relative to the euro area. Bottom-up analysts are usually too optimistic about the level of earnings, but are generally spot on about their direction. Relative earnings revisions between the US and other markets have led the dollar by about nine to 12 months (Chart I-5). Should cyclical earnings hit a soft patch as the pandemic engulfs much of the developing world, the more defensive US market might prove resilient. Chart I-4A Red Flag From Global Industrials

A Red Flag From Global Industrials

A Red Flag From Global Industrials

Chart I-5Earnings Revisions And The Dollar

Earnings Revisions And The Dollar

Earnings Revisions And The Dollar

In a nutshell, corrections in equity markets are usually a healthy reset for the bull market to resume. In similar fashion, a washing out of stale US dollar short positions will ensure the bear market for 2021 unfolds with higher conviction. A garden-variety 5-10% cyclical correction in the S&P 500 has usually coincided with a 2-4% bounce in the DXY, as can be seen from Chart I-2. This could be the story over the next one to three months. The Signal From Currency Markets Our dollar capitulation index hit a nadir in July last year and has since been rebounding from very oversold levels. It has been very rare that a drop in this index below the 1.5 level did not trigger a rebound in the dollar (Chart I-6). Part of the reason this did not happen this time around has been concentration. Dollar short positions since 2020 have mostly been against the euro, yen and Swiss franc, with positioning in currencies such as the Australian dollar and Mexican peso more neutral. This will limit the extent to which the broad dollar index could rise from a flushing out of stale shorts. Chart I-6BCA Dollar Capitulation Index Suggests Some Upside

BCA Dollar Capitulation Index Suggests Some Upside

BCA Dollar Capitulation Index Suggests Some Upside

For example, the exchange rate that best signals whether we are in a reflationary/deflationary environment is the AUD/JPY rate. Since the Great Recession, the yen has been the best performer during equity drawdowns, while the Aussie has been the worst. As a result, the AUD/JPY cross has consistently tracked the drawdown of the broad equity market (Chart I-7). As the bottom panel shows, exuberance in the AUD/JPY cross has also coincided with equity market peaks. That exuberance hardly exists today. The AUD/JPY cross has consistently tracked the drawdown of the broad equity market. That said, speculators are very short the dollar, even if the currencies used to implement these views are very concentrated. Sentiment towards the dollar is the lowest in over a decade and our intermediate-term indicator is at bombed-out levels (Chart I-8). Chart I-7AUD/JPY As A Risk On Gauge

AUD/JPY As A Risk On Gauge

AUD/JPY As A Risk On Gauge

Chart I-8The Dollar Is Oversold

The Dollar Is Oversold

The Dollar Is Oversold

In a nutshell, the message from technical indicators is that a bounce in the dollar is to be expected. However, the magnitude will be smaller than prior episodes. Ever since the dollar peaked in March 2020, counter-trend moves have been in the order of 2-3%. We expect this time to be no different. The Dollar And Commodities Commodity prices across the board have been on a tear. This has usually been an environment where the dollar is in a broad-based decline. Commodity prices hold a special place as FX market indicators, since they are both driven by final demand and financial speculation. More importantly, rising commodity demand can signal an improving FX trend between commodity producing (Australia, Canada, Mexico, Colombia, Russia) and importing (Euro area, India, Turkey, or even China) countries. We will buy the currencies of commodity producers on weakness as the bull market continues. Metals prices have exploded higher on strong demand, especially from China (Chart I-9). Not surprisingly, speculative positioning in copper options and futures is also extremely elevated. If investors have been betting on higher copper prices, based on the expectation of a lower dollar, then a relapse in the red metal will be synonymous with a higher greenback. That said, commodity bull markets have tended to last over a decade, with the recent rise in prices also driven by deficient supply. As such, we will buy the currencies of commodity producers on weakness, rather than sell on strength, as the bull market continues. This also argues for a fleeting technical bounce in the dollar. Chart I-9A Bull Market In Metals

A Bull Market In Metals

A Bull Market In Metals

Chart I-10The Gold/Silver Ratio is Rebounding

The Gold/Silver Ratio is Rebounding

The Gold/Silver Ratio is Rebounding

Within the commodity space, watching the gold/silver ratio (GSR) is instructive. The GSR tends to track the US dollar (Chart I-10). This is because it has usually rallied on safe-haven demand and relapsed once there is a pickup in economic (or manufacturing) activity. Gold benefits from plentiful liquidity and very low real rates, while silver benefits from rising industrial demand. It is possible the surge in global infections dampens economic activity and lifts demand for safe havens. This will be good for the dollar. However, as vaccinations take hold and the economy reopens, silver will surge. Relative Interest Rates Interest rates are moving in favor of the dollar, and there has been a long-standing relationship between relative real rates and the US currency. The question is whether the rise in US interest rates has been sufficient to compensate investors for the higher budget deficits they will need to finance. To answer this, it is always instructive to look at the relationship between gold and US Treasuries. Remarkably, the ratio of the total return in US government bonds-to-gold prices has tracked the dollar pretty well since the end of the Bretton Woods system in the early 1970s. The bond-to-gold ratio is an important signal for the dollar, since both US Treasuries and gold are safe-haven assets and thus, by definition, are competing assets (Chart I-11). The ratio of the US bond ETF (TLT)-to-gold (GLD) is an important proxy for investor sentiment on the dollar (Chart I-12). Ultimately, investors are driven by real rates. Positive real returns will favor Treasuries, while negative real returns will favor gold. The latter appears to have the upper hand for now. Remarkably, the ratio of the total return in US government bonds-to-gold prices has tracked the dollar pretty well since the end of the Bretton Woods system in the early 1970s. Chart I-11Gold and Treasurys Are Competing Assets

Gold and Treasurys Are Competing Assets

Gold and Treasurys Are Competing Assets

Chart I-12Watch The Bond-To-Gold Ratio

Watch The Bond-To-Gold Ratio

Watch The Bond-To-Gold Ratio

The implication is that the rise in US interest rates has not yet convinced investors that a significant margin of safety exists for possible runaway inflation. This augurs badly for the dollar, beyond the near term. Investment Implications Our investment strategy is simple: hold a basket of the cheapest currencies and, some safe havens that will benefit if the dollar bounces. Opportunities at the crosses also make sense. On safe-haven currencies, our preferred vehicle is the Japanese yen, which sports an attractive real rate relative to the US. Relative value is particularly attractive on short CAD/NOK, long AUD/NZD, short EUR/GBP and long EUR/CHF. Stick with them. Stay short USD/JPY and long the Scandinavian currencies as a core holding. Remain short the gold/silver ratio. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the US have been resilient: The headline 140K job loss last Friday was not as dire, looking into the details. There was a net two-month revision of +135K jobs. Core CPI came in line at 1.6% year-on-year, while average weekly earnings surged by 4.9%. MBA mortgage applications came in at a blockbuster 16.7% week-on-week, for the week ending on January 8. The DXY rose by 0.3% this week. There was some element of consolidation in markets earlier this week, with a few equity bourses softening and the dollar catching a bid. However, that has been overwhelmed by the reflation trade as we go to press. We expect any dollar bounce to be technical in nature, and in order of magnitude of around 2-4%. Report Links: The Dollar In A Blue Wave - January 8, 2021 The Dollar Conundrum And Protection - November 6, 2020 The Dollar In A Market Reset - October 30, 2020 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data from the euro area have help up: The unemployment rate in the euro area fell from 8.4% to 8.3% in November. Sentix investor confidence remains resilient at 1.3 in January, versus -2.7 the previous month. Industrial production in the euro area is recovering, as signaled by the PMI releases. The euro fell by 0.5% against the US dollar this week. The unfolding political crisis in Italy warns that the euro might be due for a setback, as European peripheral bond spreads rise. We remain bullish the euro longer-term, but short-term trades are at risk from lopsided positioning. Report Links: The Dollar Conundrum And Protection - November 6, 2020 Addressing Client Questions - September 4, 2020 On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 The Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data from Japan has been better than expected: The expectations component of the Eco Watchers Survey rose from 36.5 to 37.1, versus expectations of 30.5 in December. Machine tool orders continued to inflect higher in December, to the tune of 8.7% year-on-year. Bank lending remained around a robust 6% in December. The Japanese yen was flat against the US dollar this week. Japanese fixed income investors are in a quagmire, since nominal rates are better in the US, but real rates are more favorable in Japan. The yen could remain caught in a tug of war between these forces, with a slight advantage to Japanese rates. We remain long the yen as a portfolio hedge. Report Links: The Dollar Conundrum And Protection - November 6, 2020 The Near-Term Bull Case For The Dollar - February 28, 2020 Building A Protector Currency Portfolio - February 7, 2020 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

There was scant data out of the UK this week: BRC like-for-like sales rose by 4.8% year-on-year in December. The British pound rose by 0.8% against the US dollar this week. Vaccinations continue to progress smoothly in the UK, but cracks are already starting to emerge in the post Brexit UK-EU relationship. There are mounting food shortages in Northern Ireland and a hiccup in fish exports from the UK, as the necessary paperwork adds a layer of bureaucracy. As investors digest the potential impact to the pound, it will add to volatility. Ultimately, a cheap pound should outperform both the dollar and euro. Report Links: The Dollar Conundrum And Protection - November 6, 2020 Revisiting Our High-Conviction Trades - September 11, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

There was little data out of Australia this week: The final retail sales print was 7.1% month-on-month in November. The Australian dollar appreciated by 0.4% against the US dollar this week. Base metals, especially copper and iron ore have been on a tear this year. This is boosting Australian terms of trade. More importantly, a shortage of ships has catapulted Asian LNG prices to all-time highs as a cold spell hits countries like Japan and Korea. This should be beneficial for Australian energy producers. We are currently long AUD/NZD. Report Links: An Update On The Australian Dollar - September 18, 2020 On AUD And CNY - January 17, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

There was scant data out of New Zealand this week: REINZ house sales rose by 36.6% year-on-year in December. Building permits rose 1.2% month-on-month in November. The New Zealand dollar fell by 0.3% against the US dollar this week. The release of the US WASDE report confirmed a looming agricultural shortage, as production forecasts were slashed on weather worries. This is NZD bullish. That said, technically, agricultural prices are stretched, and so some consolidation will deflate air off the high-flying kiwi. In a commodity basket, we prefer the Aussie that is underpinned by more structural factors. Report Links: Currencies And The Value-Versus-Growth Debate - July 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Place A Limit Sell On DXY At 100 - November 15, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data from Canada have been disappointing: Employment fell by 62.6K jobs in December. However, this was driven by 99K part-time job losses, with full-time job gains of 36.5K. The sales outlook in the BoC survey improved from 39 to 48 in 4Q 2020. The Canadian dollar appreciated by 0.5% against the US dollar this week. Oil prices are dominating commodity gains this year, given the shift from Saudi Arabia and the prospect of higher transport demand. This bodes well for the loonie. Report Links: Currencies And The Value-Versus-Growth Debate - July 10, 2020 More On Competitive Devaluations, The CAD And The SEK - May 1, 2020 A New Paradigm For Petrocurrencies - April 10, 2020 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data from Switzerland have been mixed: The unemployment rate was flat at 3.4% in December. FX reserves increased from CHF 876 billion to CHF 891 billion. The Swiss franc fell by 0.2% against the US dollar this week. The biggest risk to Switzerland and the SNB authorities is a potential correction in the euro, which encourages safe-haven flows into the franc. This will also be a risk to our long EUR/CHF position. Our bias is that the valuation cushion on the cross provides an ample margin of safety. Report Links: The Dollar Conundrum And Protection - November 6, 2020 On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Currency Market Signals From Gold, Equities And Flows - January 31, 2020 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

The data out of Norway has been robust: Headline CPI came in at 1.4% year-on-year, while underlying CPI was a whopping 3%. House prices rose 2.9% quarter-on-quarter in Q4. Industrial production came in at -0.9% in November, an improvement from -2.7% the previous month. The Norwegian krone is the best performing currency this year at +1.5%. Good management of the COVID-19 situation as well as rising oil prices have been positive catalysts. We expect the krone to keep outperforming for the rest of the year. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 A New Paradigm For Petrocurrencies - April 10, 2020 Building A Protector Currency Portfolio - February 7, 2020 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data from Sweden has been rather disappointing: Private sector production fell by 1% year-on-year in November. We would expect this to reverse with the improvement in the December PMIs. Industrial orders rose 5.7% year-on-year in November. Household consumption fell 5% year-on-year in November. The Swedish krona has been the worst performing currency this year, falling by 0.7% against the US dollar this week. That said, it might be a case of profit taking. The Swedish krona remains cheap and should benefit from an upshot in the global manufacturing cycle. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights In the wake of COVID-19, the low-probability, high-impact “Black Swan” event is as relevant as ever. Investors should already expect US terrorist incidents, a fourth Taiwan Strait crisis, and crises involving Turkey – these are no longer black swans. What if Russia had a color revolution, Japan confronted China, or Saudi Arabia collapsed? What if the US and China brokered a North Korean deal? Or a major terrorist attack caused government change in Germany? Ultimately this exercise illustrates what the market is not prepared for – a new rally in the US dollar – though some scenarios would fuel the rise of the euro and renminbi. Feature The COVID-19 pandemic reminded us all of the power of the “Black Swan” – the random, unpredictable event with massive ramifications. As historian Niall Ferguson pointed out at the BCA Conference last fall, COVID-19 was not really a black swan, as epidemiologists had predicted that a pandemic would occur and the world was not ready. Astrophysicist Martin Rees made a bet with psychologist and linguist Steven Pinker that “bioterror or bioerror will lead to one million casualties in a single event within a six month period starting no later than 31 December 2020.”1 Tellingly, countries neighboring China were the best prepared for the outbreak, having dealt with SARS and bird flu. COVID accelerated major trends building up throughout the past decade – notably the shift toward pro-active fiscal policy, which had been gaining traction in policy circles ever since the austerity debates of the early 2010s. In that sense forecasting is still necessary. If solid trends can be identified, then random shocks may simply reinforce them (Chart 1). Chart 1US Fiscal Stimulus About To Get Even Bigger

Five Black Swans For 2021

Five Black Swans For 2021

In this year’s “Five Black Swans” report, we focus on geopolitical risks that are highly unlikely, not at all being discussed, and yet would have a major impact on financial markets. Domestic terrorist events in the United States in 2021 would not qualify as a black swan by this definition. A crisis in the Taiwan Strait, which we have warned about for several years, is now widely (and rightly) expected. Black Swan #1: A Color Revolution In Russia Russia is one of the losers of the US election. Not because Trump was a Russian agent – the Trump administration ended up authorizing a fairly hawkish posture toward Russia in eastern Europe – but rather because the Democratic Party threatens Russia with a strengthening of the trans-Atlantic alliance and a recovery of liberal democratic ideology. Geopolitical risk surrounding Russia is therefore elevated, as we argued last year. Both President Vladimir Putin and his government have seen their approval rating drop, a development that has often led Russia to lash out abroad (Chart 2). But our expectation of rising political risk within Russia’s sphere has been reinforced by Russia’s alleged poisoning of opposition politician Alexei Navalny and the eruption of pro-democracy protests in Belarus. Vladimir Putin is increasingly focusing on home affairs due to domestic instability worsened by the pandemic and recession. Fiscal and monetary austerity have weighed on the public. The largest protests since 2011 occurred in mid-2019 in opposition to the fixing of the Moscow municipal elections. This could be a harbinger of larger unrest around the Russian legislative elections on September 19, 2021. Nominal wage growth has collapsed and is scraping its 2015-16 lows (Chart 3). Chart 2Black Swan #1: A Color Revolution In Russia

Black Swan #1: A Color Revolution In Russia

Black Swan #1: A Color Revolution In Russia

Chart 3Russia's Fiscal Austerity

Russia's Fiscal Austerity

Russia's Fiscal Austerity

Meanwhile US policy toward Russia will become more confrontational. New US presidents always start with outreach to Russia, but the Democratic Party blames Russia for betraying the good faith of the Obama administration’s “diplomatic reset” from 2009-11. Russia invaded Ukraine and took Crimea in exchange for cooperating on the 2015 Iran nuclear deal. Adding in the Snowden affair, the 2016 election interference, and now the monumental SolarWinds cyberattack, the Democratic Party will want to strike back and reestablish deterrence against Russia’s asymmetrical warfare. While Biden will seek to negotiate an extension of the New START missile treaty from February 5, 2021 until 2026, he will gear up for confrontation in other areas. The US could seek to go on offense with Russia’s wonted tools: psychological warfare and cyberattacks. The Americans are not willing or able to attempt regime change in Moscow. That would be taken as an act of war among nuclear powers. But if Russia is less stable internally than it appears, then US meddling could hit a weak spot and set off a chain reaction. Even if the US is incapable of anything of the sort, Russia is still ripe for social unrest. Should the authorities mishandle it, it could metastasize. Russia has a long tradition of peasant uprisings – a descent into anarchy is not out of the question. The regime would not be devoting so much attention to suppressing domestic dissent if the conditions for it were not ripe.2 Putin’s constitutional reforms in mid-2020, which could extend his term until 2036, also speak to concerns about regime stability. A successful Russian uprising would threaten to raise serious instability in Europe and the world. When great but decadent empires are destabilized, political struggle can intensify rapidly and spill out to affect the neighbors. Bottom Line: Russian domestic political instability could produce a black swan. The ruble would tank and the US dollar would catch a bid against European currencies. Black Swan #2: A Major Terror Attack In Germany 2020 was a banner year for European solidarity. Brexit went forward but none of the European states have followed – nor would any want to follow given the political turmoil it aroused. Brussels initiated a recovery fund to combat the global pandemic that consisted of a mutual debt scheme – in what has been hailed somewhat excessively as a “Hamiltonian moment,” a move toward federalism. Germany stood at the center of this process. After opening the doors to a flood of migrants from Syria in 2015, Chancellor Angela Merkel suffered a blow to her popularity and was eventually forced to make plans for her exit. But she stuck to her core liberal policies and her fortunes have recovered (Chart 4). She is stepping down in 2021 as the longest-serving chancellor since Helmut Kohl and an influential European stateswoman. The EU member states are more integrated than ever while Germany has taken another step toward improving its international image. The public has rewarded the ruling coalition for its relatively competent handling of the global pandemic (Chart 5). Chart 4Black Swan #2: A Major Terror Attack In Germany

Black Swan #2: A Major Terror Attack In Germany

Black Swan #2: A Major Terror Attack In Germany

Chart 5German People Happy With Their Government

Five Black Swans For 2021

Five Black Swans For 2021

Merkel’s approval coincides with a recovery of the liberal democratic consensus in Europe after a series of challenges from anti-establishment and populist parties. Only in Italy did populists take power, and they were forced to back down from their extravagant fiscal policy demands while modifying their policy platform with regard to membership in the monetary union. Even today, as Italy’s ruling coalition comes apart at the seams, the risk of a populist backlash is lower than it was in most of the past decade. One of the main ways the European establishment neutralized the populist challenge was by tightening control over immigration and cracking down on terrorism (Charts 6 and 7). These two forces have played a large role in generating support for right wing parties, and these parties have declined in popularity as these two forces have abated. Chart 6Terrorist Attacks Have Fallen In Europe

Terrorist Attacks Have Fallen In Europe

Terrorist Attacks Have Fallen In Europe

Chart 7Europeans Softening Toward Immigrants?

Europeans Softening Toward Immigrants?

Europeans Softening Toward Immigrants?

Still, the risk posed by terrorist groups has not disappeared – and it is always possible that disaffected individuals could evade detection. French President Emmanuel Macron faced seven terrorist attacks over the past year, which partly stemmed over the commemoration of the Charlie Hebdo massacre but also points to the persistence of underground extremist networks (Chart 8).3 Chart 8French Fear Of Terrorism Has Increased

Five Black Swans For 2021

Five Black Swans For 2021

Chart 9European Breakup Risk At Testing Point

European Breakup Risk At Testing Point

European Breakup Risk At Testing Point

What would happen if a major attack occurred in Germany in 2021? Would it upset the country’s liberal consensus and fuel another surge in popular support for far-right parties like the Alternative for Germany? Only a major attack would have a lasting impact. A systemically important attack in the pivotal year of Merkel’s retirement could create more uncertainty in domestic German politics than has been seen since the 1990s and early 2000s. It is possible that an attack could strengthen the ruling coalition and the public’s desire to continue with the leadership of the Christian Democrats after Merkel. More likely, however, it would divide the conservative and right-wing parties among themselves. Merkel’s chosen successor, Defense Minister Annagret Kramp-Karrenbauer, was forced to abandon her bid for the chancellorship last year after members of her Christian Democratic Union in the state of Thuringia voted along with the anti-establishment Alternative for Germany to remove the state’s left-wing leader. The cooperation was minimal but it set off a firestorm by suggesting that Kramp-Karrenbauer was willing to work together with the far right.4 She bowed out and now the party is about to pick a new leader. The point is that if any event strengthens the far right, it would suck away votes from the Christian Democrats. The latter could also see divisions emerge with their Bavarian sister party, the Christian Social Union, which has differed on immigration in the past. Or the conservatives could alienate the median German voter by tacking too far to the right to preempt the anti-establishment vote (e.g. overreacting to the attack). Either way, German politics would be rocked. Ironically, if the coalition was seen as mishandling the response, a left-wing coalition of the Greens and the Social Democrats could be the beneficiaries. The risk of a government change – in the wake of Merkel and the pandemic – is greatly underrated, entirely aside from black swans. Nevertheless a major shock that strengthens the far right would be a black swan by forcing the question of whether the center-right is willing to cooperate with its fringe. If that occurred, then Europe would be stunned. If it did not, then the conservatives could lose the election and plunge into intra-party turmoil. The takeaway of a rightward shift on the back of any shock would be a renewed risk of fiscal hawkishness – a partial relapse from the past two years’ fiscal expansion to the more traditionally austere German posture. The takeaway of a leftward shift would be the opposite – a doubling down on that fiscal expansion. German hawkishness would increase the European breakup risk premium, while a confirmation of the new German dovishness would further suppress it (Chart 9). Bottom Line: The fiscal dovish turn is the more likely response to such a black swan in today’s climate, but a major terrorist attack could have unpredictable consequences. Black Swan #3: A US-China Deal On North Korea Critics misunderstood President Trump’s policy on North Korea. Trump’s policy – even his belligerent rhetoric – echoed that of Bill Clinton in the 1990s. The intention of the US show of force was to create an overwhelming threat that would force Pyongyang into serious negotiations toward a nuclear deal. That in turn would pave the way to economic cooperation. Trump’s efforts failed – Kim Jong Un stonewalled him in the final year and a half. Kim’s bet paid off since he avoided making major concessions and now Biden must start from scratch. Pyongyang has ramped up its threats and Kim has elevated his sister, Kim Yo Jong, to a higher standing in the party – apparently to lob attacks at South Korea full-time. Biden will put the technocrats and Korea experts in charge. Pyongyang may test nuclear weapons or launch intercontinental ballistic missiles to attract Biden’s attention. But Kim could also go straight to negotiations. Optimistically, a few years of talks could result in a phased reduction of sanctions in exchange for nuclear inspections. Kim has the incentive and the dictatorial powers to open up the economy and engage in market reforms while managing any backlash among the army. He has already prepared the ground by elevating economic policy to the level of military policy in the national program. For years he has allowed some market activity to little effect. The North must have suffered from the pandemic, as Kim publicly confessed to the failure of economic management at the latest party meeting. His country needs a vaccine for COVID. And if he intends to go the way of Vietnam, then he needs to open up the doors while a new global business cycle is beginning (Chart 10). The black swan would emerge if the Biden administration’s attempt to reboot relations with China produced a unified effort to force a resolution onto Kim. It is undeniable that Trump broke diplomatic ice by meeting with Kim directly, giving Biden the option of doing so quickly and with minimal controversy if he should so desire. Most importantly, China has enforced sanctions, if official statistics can be trusted (Chart 11). Beijing made no secret that it saw North Korea as an area of compromise to appease US anger. After all, success on the peninsula would remove the reason for the US to keep troops there. Chart 10Black Swan #3: A US-China Deal On North Korea

Five Black Swans For 2021

Five Black Swans For 2021

Chart 11An Area Of US-China Cooperation Under Biden?

An Area Of US-China Cooperation Under Biden?

An Area Of US-China Cooperation Under Biden?

The last point is the material point. If the North sought to open up, it would likely have to do so through talks with the US, China, South Korea, and Japan. Success would mean that US-China engagement is still effective. Bottom Line: A breakthrough on the Korean peninsula would mean that investors could begin imagining a future in which the US and China are not “destined for war” but rather capable of reviving their old cooperative approach. This has far-reaching positive implications, but most concretely the Korean won and Chinese renminbi would rally against the US dollar and Japanese yen on the historic reduction of war risk. Black Swan #4: Saudi Arabia (And Oil Prices) Collapse Saudi Arabia is an even greater loser from the US election than Russia. The Saudis came face to face with their geopolitical nightmare of US abandonment under the Obama administration, as the US gained energy independence while reaching out to Iran. The 2015 nuclear deal gave Iran a strategic boost and enabled it to resume pumping oil (Chart 12). The Saudis, like the Israelis, lobbied hard to stop the deal but failed. They threw their full support behind President Trump, who reciprocated, and now face the restoration of the Obama policy under Joe Biden. Chart 12Black Swan #4: Saudi Arabia (And Oil Prices) Collapse

Black Swan #4: Saudi Arabia (And Oil Prices) Collapse

Black Swan #4: Saudi Arabia (And Oil Prices) Collapse

Chart 13Fiscal Pressure On Saudis

Fiscal Pressure On Saudis

Fiscal Pressure On Saudis

Global investors should expect Biden to return to the nuclear deal with Iran as quickly as possible, notwithstanding Iran’s latest nuclear provocations, since the latter are designed to increase negotiating leverage. The Joint Comprehensive Plan of Action was an executive agreement that Biden could restore with the flick of his wrist, as long as Iranian President Hassan Rouhani returned to compliance. Rouhani can do so before a new president is inaugurated in August – he could secure his legacy at the cost of taking the blame for “dealing with the devil.” This would save the regime from further economic and social instability as it prepares for the all-important succession of the supreme leader in the coming years. A black swan would occur if this diplomatic situation led to a breakdown in support for Crown Prince Mohammed bin Salman (MBS). MBS, whose nickname is “reckless,” in part because his foreign policies have backfired, could attempt to derail or sabotage the US-Iran détente. If he tried and failed, the US could effectively abandon Saudi Arabia – energy self-sufficiency, public war-weariness, and Iranian détente would pave the way for the US to downgrade its commitment. This would create an existential risk for the kingdom, which depends on the US for national security. It could also be the final straw for MBS, who already faces opposition from elites who have been shoved aside and do not wish to see him ascend the throne in a few years’ time. A different trigger for the same black swan would be a collapse of the OPEC 2.0 oil cartel. The Saudis and Russians have fought two market-share wars over the past seven years. They could relapse into conflict in the face of shifting global dynamics, such as the green energy revolution, that disfavor oil. Arthur Budaghyan and Andrija Vesic, of BCA’s Emerging Markets Strategy, have argued that financial markets will start pricing in a higher probability of Saudi currency depreciation versus the US dollar in coming years. Lower-for-longer oil prices (say $40 per barrel average over next few years) would pose a dilemma to the authorities: either (1) cut fiscal spending further and tighten liquidity or (2) resort to local banks financing (money creation “out of thin air”) to sustain economic activity. The first scenario would impose severe fiscal austerity on the population (Chart 13), which is politically difficult to endure in the long run. The second scenario will lead to depleting the country’s FX reserves, robust money growth and some inflation culminating in downward pressure on the currency. The main reason for believing the devaluation will not happen is that it would topple the regime. Currency devaluation would result in unbearable inflation in a country that lacks domestic production and domestically sourced staples. But that is precisely why it is a black swan risk. After all, prolonged fiscal austerity may not be feasible either. Bottom Line: MBS controls the security forces and has consolidated power for years but that may not save him if his foreign policies led to American abandonment or a breakdown of the peg. Black Swan #5: A Sino-Japanese Crisis For the first time since 2016, we are not including US-China tensions over Taiwan in our list of black swans. A crisis in the strait is only a matter of time and the global news media is increasingly aware of it (Chart 14). It would not necessarily have to be a war or even a show of military force, though either are possible. A mere Chinese boycott or embargo of Taiwan would violate the US’s Taiwan Relations Act and trigger a US-China crisis from the get-go of the Biden administration. What is less widely recognized is that peaceful resolution of the China-Taiwan predicament is not just a concern for the United States. It is a concern for Japan and South Korea as well – whose vital supplies must travel around the island one way or another. These two nations would face constriction if mainland China reunified Taiwan by force – and therefore Beijing’s signals of increasing willingness to contemplate armed action are already reverberating among the neighbors. Japan sounded an uncharacteristically stark warning just last month. The hawkish statement from State Minister of Defense Yasuhide Nakayama is worth quoting at length: We are concerned China will expand its aggressive stance into areas other than Hong Kong. I think one of the next targets, or what everyone is worried about, is Taiwan … There’s a red line in Asia – China and Taiwan. How will Joe Biden in the White House react in any case if China crosses this red line? The United States is the leader of the democratic countries. I have a strong feeling to say: America, be strong!5 China and Japan have improved trade relations through the RCEP agreement, as Beijing looks to diversify from the United States. But China’s rise is of enormous strategic concern for Japanese policymakers. COVID-19 and the rollback of Hong Kong’s freedoms have made matters worse. The belt of sea and land around China – the “first island chain” – is the critical area from which Beijing seeks to expel American and foreign military presence. With China already having shown a willingness to clash with India and Australia simultaneously in 2020 – as it carves a sphere of influence in the absence of American pushback – it should be no surprise to see conflicts erupt in the East or South China Sea (Chart 15). Chart 14Differences In The Taiwan Strait

Differences In The Taiwan Strait

Differences In The Taiwan Strait

Chart 15Black Swan #5: A Sino-Japanese Crisis

Black Swan #5: A Sino-Japanese Crisis

Black Swan #5: A Sino-Japanese Crisis

In the aftermath of the last global crisis, in 2010, China and Japan clashed mightily over maritime-territorial disputes in the East China Sea. China imposed a brief embargo on exports of rare earth elements to Japan. The two clashed again the following year and tensions escalated dramatically when China rolled out an Air Defense Identification Zone (ADIZ) in 2013. Tense periods come and go and are often attended by mass anti-Japanese protests, as in 2005 and 2012. Usually these events are of passing importance, though they have the potential to escalate. What would truly be a black swan would be if Japan took the initiative to challenge China and test the Biden administration’s commitment to Japanese security. With the US internally divided and distracted, and China ascendant, Japan could grow increasingly insecure and seek to take precautions. China could see these as offensive. A new Sino-Japanese crisis could ensue that would catch investors by surprise. It is highly unlikely that Tokyo would provoke China – hence the black swan designation – but the effective absence of the Americans is a strategic liability that Tokyo may wish to resolve sooner rather than later. In this case the market reaction would be predictable – the yen would appreciate while the renminbi and Taiwanese dollar would fall. The risk-off period could be extended if the US failed to reinforce the Japanese alliance for fear of China, with the whole world watching. Bottom Line: Global investors would be blindsided if a sudden explosion of Sino-Japanese tensions prevented any US-China thaw and confirmed their worst fears about China’s economic decoupling from the West. Investment Takeaways This exercise in identifying black swans may be useful in at least one way: it exposes the vulnerability of financial markets to a sudden reversal of the US dollar’s weakening trend (Chart 16). The dollar would surge on broad Russian instability, Sino-Japanese conflict, or another exogenous geopolitical shock. This kind of dollar surprise would be much greater than a temporary counter-trend bounce, which our Foreign Exchange Strategist Chester Ntonifor fully expects. It would upset the financial community’s dollar-bearish consensus, with far-reaching ramifications for the global economy and financial markets. A rising dollar against the backdrop of a recovering global economy represents a de facto tightening of global financial conditions. Equity markets, for example, have only started to rotate away from the US and this trend would be reversed (Chart 17). Whereas further appreciation of the euro and the renminbi is not only expected but would support global reflation. Chart 16The USD Over Trump's Four Years

The USD Over Trump's Four Years

The USD Over Trump's Four Years

Chart 17Global Market Cap Over Trump's Four Years

Global Market Cap Over Trump's Four Years

Global Market Cap Over Trump's Four Years

There is a much plainer and straighter way to an upset of the dollar-bearish consensus. Rather than a black swan it is a “gray rhino,” the term that Michele Wucker uses for risks that are common, expected, and staring you right in the face.6 This would be the peak of China’s stimulus, which holds out the risk of a major reversal to the pro-cyclical global financial market rally in late 2021 (Chart 18). Chart 18China Impulse Will Linger In 2021, But EM Stocks Tactically Stretched

China Impulse Will Linger In 2021, But EM Stocks Tactically Stretched

China Impulse Will Linger In 2021, But EM Stocks Tactically Stretched

It would be a colossal error if Beijing over-tightened monetary and fiscal policy in 2021 in the context of high debt, deflation, and unemployment (Chart 19). Chart 19Three Reasons China Will Avoid Over-Tightening (If It Can)

Three Reasons China Will Avoid Over-Tightening (If It Can)

Three Reasons China Will Avoid Over-Tightening (If It Can)

Nevertheless the government’s renewed efforts to contain asset bubbles and credit excesses clearly increase the risk. Financial policy tightening is always a risky endeavor, as global policymakers routinely discover. Chart 20Book Profits But Stay Cyclically Positive On Reflation Trades

Book Profits But Stay Cyclically Positive On Reflation Trades

Book Profits But Stay Cyclically Positive On Reflation Trades

We maintain that China’s major stimulus will have a lingering positive effects for the economy for most of this year and that the authorities will relax policy and regulation as needed to secure the recovery. The Central Economic Work Conference in December suggested that the Politburo still views downside economic risks as the most important. But this is a clear and present risk that will have to be monitored closely. Clearly the global reflation trend has extended to dangerous technical extremes over the past month on the realization that US fiscal stimulus will surprise to the upside. Therefore we are doing some housekeeping. We will book 31.1% profit on long cyber security, 16.7% on long US infrastructure, and 24.3% on long US materials. We will also book 9.5% gains on our long EM-ex-China equity trade, which has gone vertical (Chart 20). Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Such epidemiologists include Michael Osterholm and Lawrence Brilliant. For Pinker and Rees, see George Eaton, "Steven Pinker interview: How does a liberal optimist handle a pandemic?" The New Statesman, July 22, 2020, newstatesman.com. 2 Thomas Grove, "New Russian Security Force Will Answer To Vladimir Putin," Wall Street Journal, April 24, 2016, wsj.com. 3 Elaine Ganley, "Grisly beheading of teacher in terror attack rattles France," Associated Press, October 16, 2020, apnews.com. 4 Philip Oltermann, "German politician elected with help from far right to step down," The Guardian, February 6, 2020, theguardian.com. 5 Ju-min Park, "Japan official, calling Taiwan ‘red line,’ urges Biden to ‘be strong,’" Reuters, December 25, 2020, reuters.com. 6 See www.wucker.com.

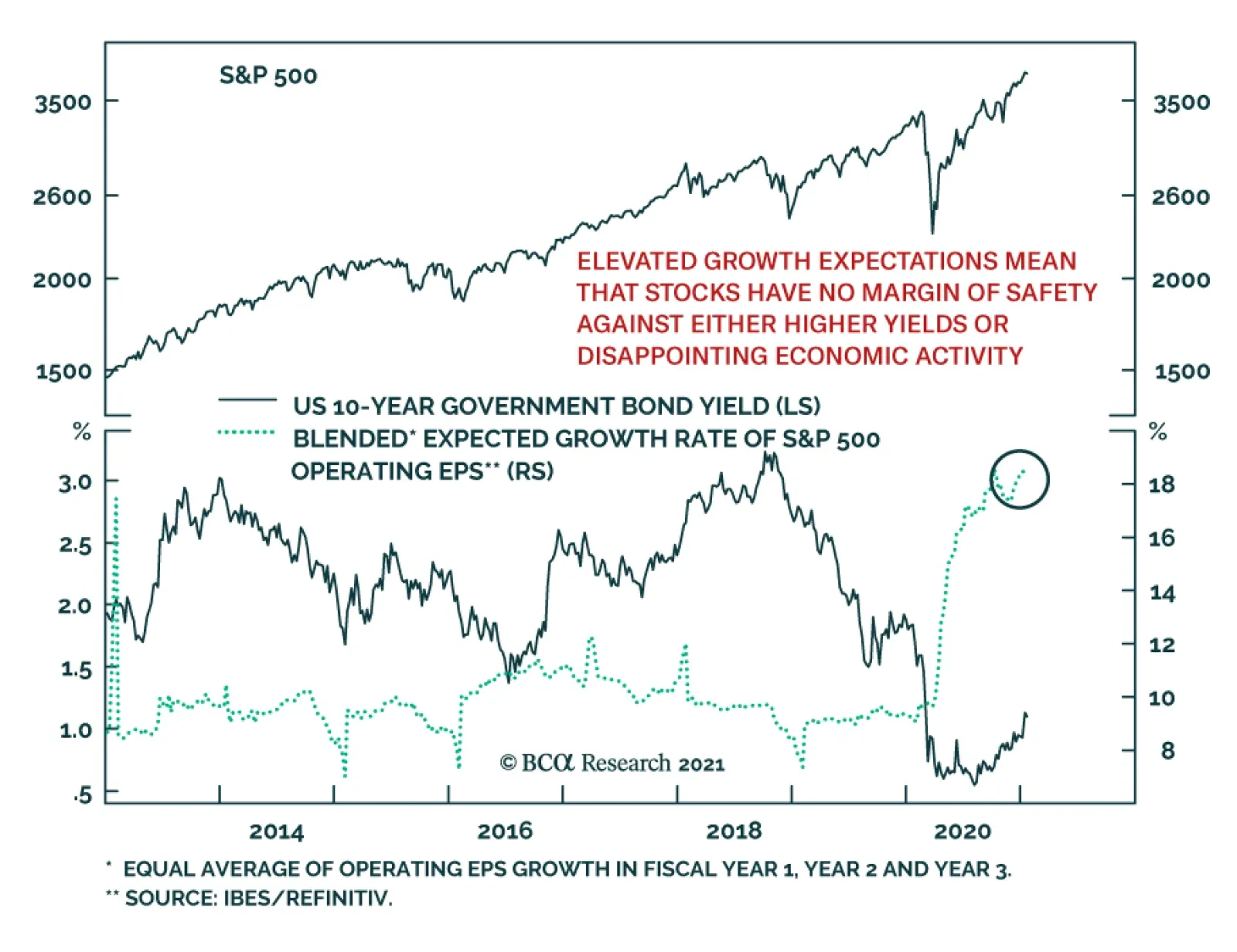

Many commentators have written that higher yields will be the cause of the eventual pullback in stocks. However, recent history does not corroborate this assertion, stocks and yields have been strongly correlated this cycle. Nonetheless, there is some…

There is little good news left that the market can discount to push the SPX higher through the multiple expansion pathway. This implies that earnings will have to do the heavy lifting and pull the SPX higher. The near all-time high 23x forward P/E multiple-implied SPX level will remain a bar hard to surpass and, similar to last summer when the market discounted the second wave of infections, it will face stiff resistance. We are already cautious on the near-term equity market prospects and would also recommend investors fade any overshoots above the 23 handle on the forward P/E level as the risk/reward ratio will be skewed to the downside (top & third panels). Tuesday’s Insight drew parallels with 2009-2010, and today we continue the analogy further and disaggregate the SPX return into its two components: forward P/E and “E”. Importantly the 2009-2010 episode is a close resemblance to today (third & bottom panels). The forward P/E similarity is especially striking. In fact, in order for the SPX to continue cyclically grinding higher to reach our end-2021 target of about 4,000, a repeat of 2010 is required when the forward multiple passed the baton to profits (see the second chart on the next page). Bottom Line: Lofty valuations add to our near-term cautious broad equity market view. Stay tuned.

Pushing On A String?

Pushing On A String?

Pushing On A String?

Pushing On A String?

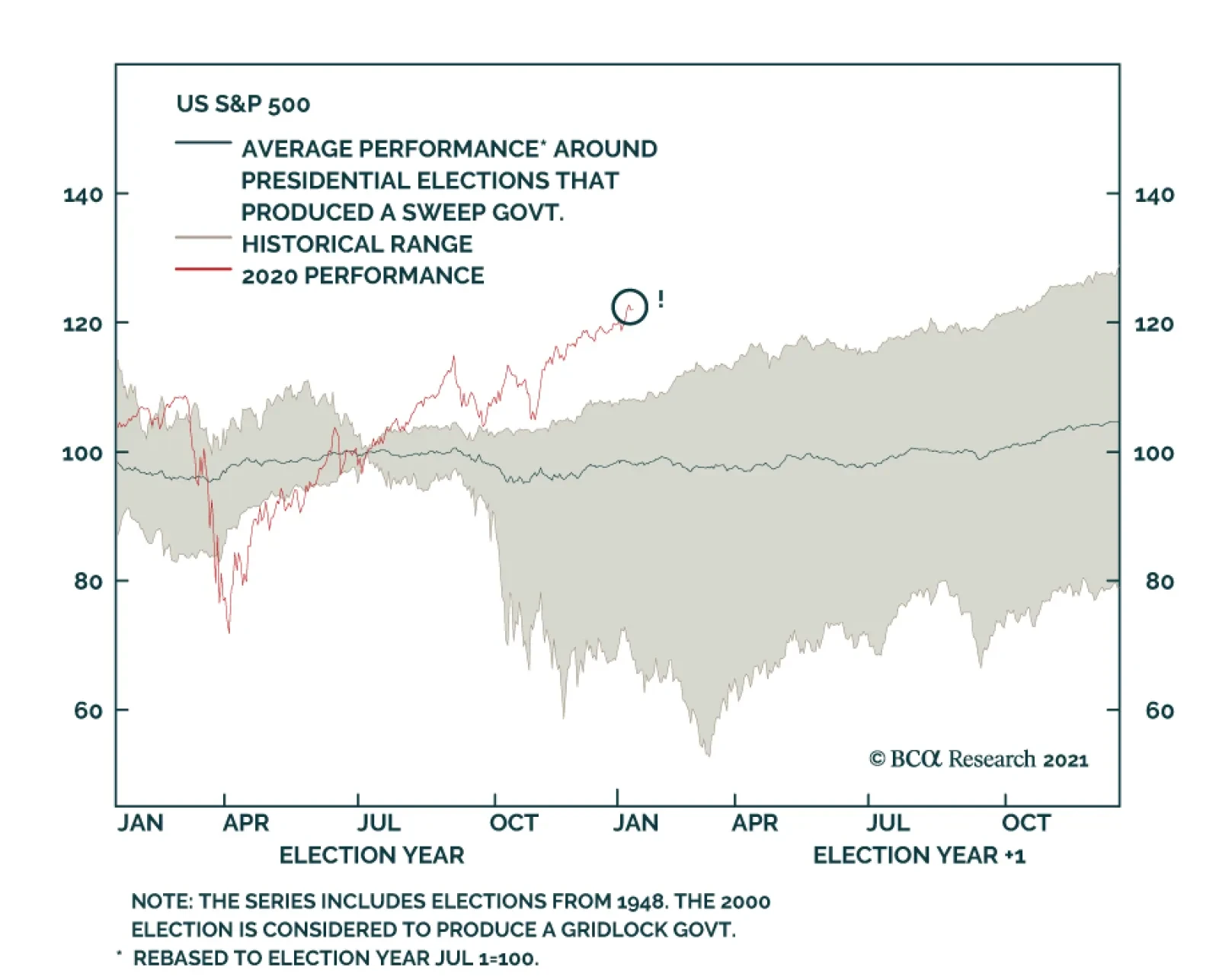

BCA Research’s US Political Strategy service concludes that structural reform is coming to the United States in the wake of the riotous 2020 election cycle. The incoming administration of President-elect Joe Biden will usher in a stabilization of US…

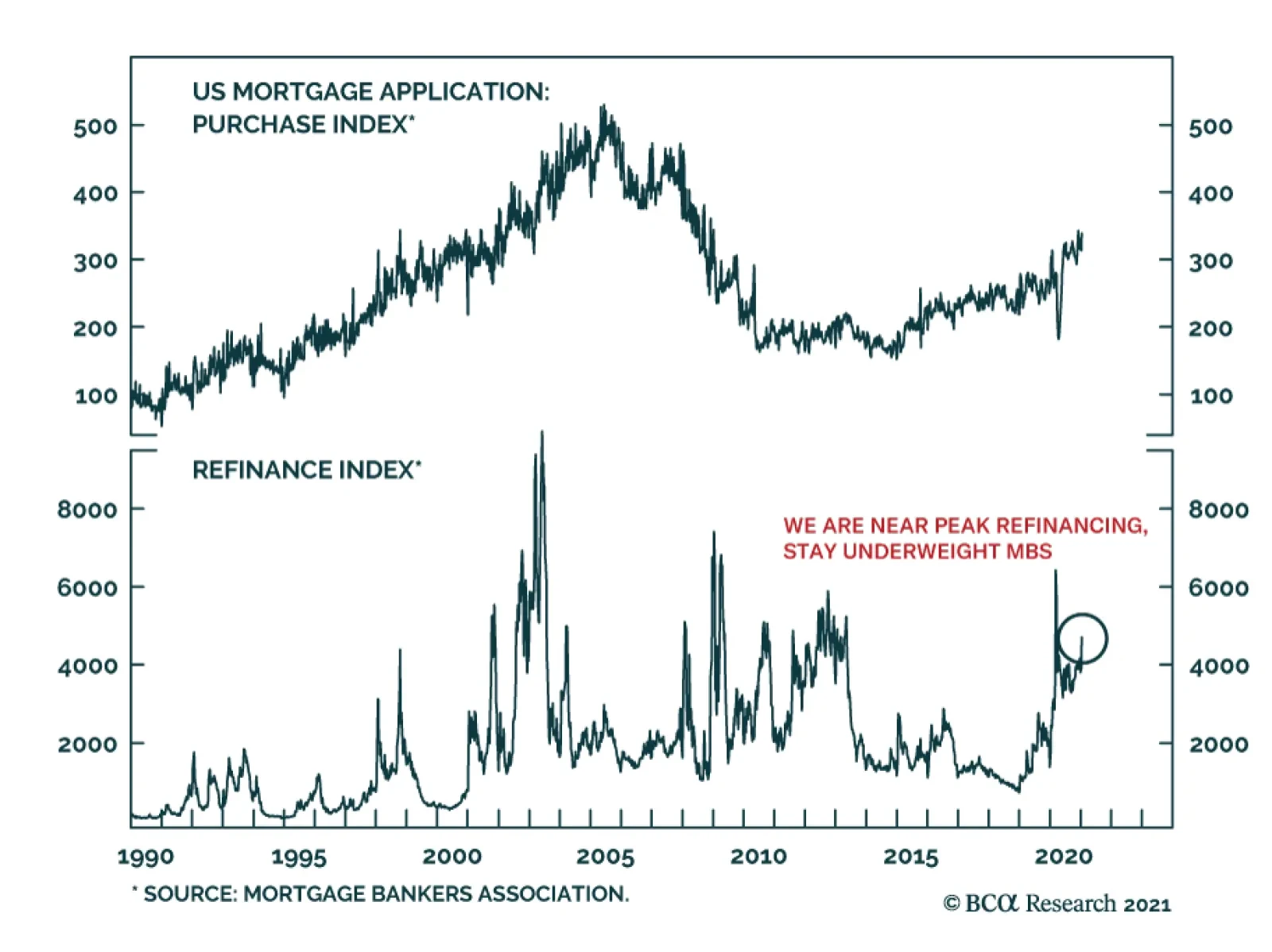

Demand for mortgages in the US remains strong. The MBA Mortgage Applications Index rose 16.7% in the week ending January 8, 2021 bringing mortgage applications to their highest level since March 2020, and October 2012 before that. This was supported by…