United States

Highlights We remain constructive on the economy and financial markets, … : US households have stored up a great deal of dry powder for consumption once the economy fully reopens, last month’s stopgap fiscal measures will help relieve pressure on the most vulnerable households, and the Georgia Senate results ensure that even more fiscal transfers are in store. … but there is a non-negligible risk that investors will get too excited about the positive backdrop: The exceedingly supportive policy backdrop could easily help the S&P 500 push into the low 4,000s, but it’s not clear what investors will have to look forward to for the rest of 2021 if it ascends to that level early in the year. We do not share the bubble-spotters’ alarm, but we are willing to study their arguments: We like to test our convictions by seeking out opposing views and we therefore read Jeremy Grantham’s bubble essay with great interest. We do not share his urgent concern, and our recommended asset allocations are nearly the mirror image of his, but we are taking a deep dive into his view and its implications. Feature As a grad student on the South Side of Chicago, I used to run on the bike path along the lake. On windless days, the three or four miles north from Hyde Park Boulevard felt especially easy, and I would think, “this is what it’s like when there’s no wind.” Then I’d head for home and discover there’d been a breeze behind me all along. A mile or two in, I’d realize it was no breeze and marvel at how I hadn’t noticed it on the way out. The moral of the story, as I told it then, is that if you think it’s not windy in Chicago, just turn around. Now it seems that it has a broader, weightier lesson: it can be easy to miss the wind when it’s behind you. Jeremy Grantham’s carefully reasoned bubble warning, posted online last Tuesday,1 has inspired us to re-examine our outlook and how widely it’s shared. We are not changing our view – we remain vigilantly bullish – but it is worth devoting ample time to consider the risks to it. This week, we highlight the elements of Grantham’s piece that most caught our attention; next week, we will discuss strategies to try to reduce an investor’s vulnerability to them. The Belated Blue Wave Grantham’s essay highlights vulnerabilities that could come to the fore sometime in the near future, but the Democratic sweep of Georgia’s Senate seats has immediate market implications. By virtue of Vice President-elect Harris’s tie-breaking vote, the Democrats will hold a majority in the 50-50 chamber beginning January 20th. The outcome ensures that the Biden administration will have slim majorities in both houses of Congress for its first two years (pending appointments and special elections). Although a five-seat House majority and the slimmest possible Senate majority will not give the incoming administration carte blanche to enact sweeping legislative changes, it will have an easier time pursuing its agenda than it would have had the Republicans held on to just one of the Georgia Senate seats. Item number one on that agenda is likely to be bulked-up fiscal aid for struggling households, states and municipalities. The economic and market significance of the blue wave is that Congress can now become a full partner supporting the monetary policy aim of erring to the side of providing too much accommodation. With the Fed pledging that it won’t take its foot off the gas any time soon, revived fiscal spending will provide the economy with an incremental reflationary boost that should benefit risk assets. Fiscal transfers will be at least partially funded with increased taxes on corporations and high-earning individuals. Profit margins will narrow, but empirical evidence of a relationship between tax rates and economic growth is elusive (Chart 1). Economic growth is largely a function of growth in the size of the working-age population and growth in productivity. Investment leads productivity – workers become more productive when endowed with more and better tools – but history suggests that investment spending is indifferent to corporate tax rates (Chart 2), as is productivity (Chart 3). Chart 1We Don't Like Taxes, Either ...

We Don't Like Taxes, Either ...

We Don't Like Taxes, Either ...

Chart 2... But They Do Not Seem To Impact Investment ...

... But They Do Not Seem To Impact Investment ...

... But They Do Not Seem To Impact Investment ...

Chart 3... Or Productivity Growth

... Or Productivity Growth

... Or Productivity Growth

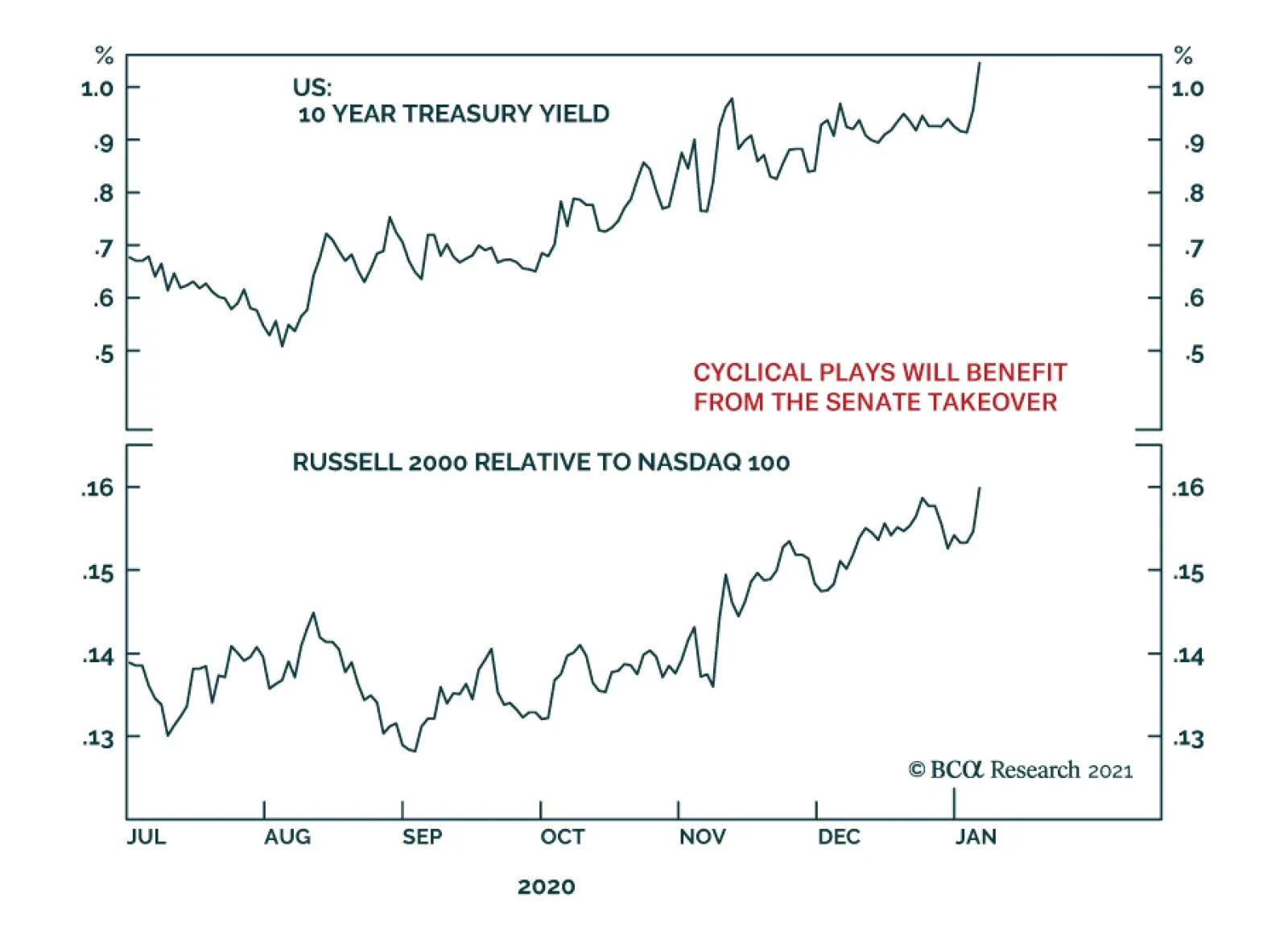

We are disposed to agree with the idea that higher taxes are a drag on growth. Transferring spending power from the private sector to government apparatchiks is not likely to improve efficiency. Business executives are as fallible as any other experts, however, and changes in tax rates have a smaller multiplier effect than the proposed spending measures. Net-net, we expect that the outcome of the Georgia run-offs will lead to slightly higher interest rates, a steeper yield curve, increased consumption and fewer defaults, a welcome mélange for credit performance and the equities that were left behind as investors flocked to COVID winners. A Slippery Slope Chart 4Bull Markets Tend To Go Out With A Bang

Let's Not Get Carried Away

Let's Not Get Carried Away

[G]reat bubbles are where fortunes are made and lost – and where investors truly prove their mettle. For positioning a portfolio to avoid the worst pain of a major bubble breaking is likely the most difficult part. Every career incentive in the industry and every fault of individual human psychology will work toward sucking investors in. [Emphasis added.] As Jeremy Grantham lays it out, the latter stages of a bull market are especially perilous. Given that bull markets run hot before they end (Chart 4), it becomes fiendishly difficult to resist their pull. The recency bias drives an investor to focus on the most recent data points to the exclusion of older ones, pointing to higher expected returns than might be inferred from a more comprehensive sample. The phenomenon encourages equity overexposure at inopportune times if returns are mean-reverting. Professional investors are as susceptible to recency bias and overconfidence (fueled by having had the wind at their back) as non-professionals, and their judgment can be additionally clouded by career pressures. Those who achieve the longest tenures are at least subconsciously attuned to Keynes’ dictum that it is better to fail conventionally than to succeed unconventionally. Staying at the party too long with lots of others may hold far less risk than staking out a solitary position. The bottom line is that asset management incentives encourage groupthink, especially as late-stage bull markets go into overdrive. Dizzying Heights The long, long bull market since 2009 has finally matured into a fully-fledged epic bubble. Featuring extreme overvaluation, explosive price increases, frenzied issuance, and hysterically speculative investor behavior, I believe this event will be recorded as one of the great bubbles of financial history[.] Bubbles are only identifiable in retrospect, but several aspects that financial historian Charles Kindleberger associated with manias are evident. Money is cheap and readily available and valuations are quite high. One could argue that anticipation of short-term capital gains is drowning consideration of future earnings for at least some equity investors or, as Grantham puts it, “stocks [are] rising … simply because they are rising.” Make no mistake: Equity valuations are demanding and de-rating appears more likely than continued re-rating. The main valuation metrics clearly indicate that equities are richly priced. The S&P 500’s forward earnings multiple is hovering around two standard deviations above the mean, at heights previously reached only in the late ‘90s and early ‘00s (Chart 5). Price-to-sales is at an all-time high, three standard deviations above the mean (Chart 6, top panel), while book (Chart 6, middle panel) and cash flow multiples (Chart 6, bottom panel) are elevated but not yet extreme. Price-to-sales should rise if markets believe pandemic-induced margin pressure is temporary and will reverse once the country is vaccinated, but the one-plus-sigma surge above pre-COVID levels would seem to be a bit much. Chart 5Equity Valuations Are Pushing The Envelope

Equity Valuations Are Pushing The Envelope

Equity Valuations Are Pushing The Envelope

Chart 6Making A Run At '99-'00

Making A Run At '99-'00

Making A Run At '99-'00

Equity option and IPO activity is redolent of euphoria and overtrading. Equity call option volume has surged to record levels (Chart 7, top panel), reportedly on the back of an explosion in small retail activity, and the put-call ratio has fallen to dot-com-bubble levels as demand for exposure has swamped demand for protection (Chart 7, bottom panel). New IPOs have been coming fast and furious (Chart 8, top panel) at a relatively tender average age (Chart 8, bottom panel). Sponsors’ shift away from hoarding early- and middle-stage returns to inviting the public to share them may prove to be telling. There are many reasons to sell equity interests, but expecting them to blast higher isn’t typically one of them. Chart 7The Merry Men Of Sherwood Forest Have Discovered Options Are A Gas, Too

The Merry Men Of Sherwood Forest Have Discovered Options Are A Gas, Too

The Merry Men Of Sherwood Forest Have Discovered Options Are A Gas, Too

Chart 8Take The Money And Run

Take The Money And Run

Take The Money And Run

The Legend Who Cried Wolf This isn’t the first time Grantham or one of his colleagues has expressed concern about rising stock prices. It may be unduly harsh to call him a perma-bear, but GMO has consistently underestimated equities and the firm has seen its assets under management (AUM) cut in half over the last five years, to $60 billion, while its flagship asset allocation fund has lost over 60% of AUM. As an RIA firm executive told a Bloomberg reporter, “I can see how clients lose patience with them. They get defensive way before anybody else.2” It’s important to recognize different commentators’ biases/agendas when evaluating their arguments. Grantham calls out the broker-dealers as perpetual market cheerleaders, but he has a stake in convincing GMO clients and prospects that value investing principles are still relevant. BCA’s business model is far more insulated from markets’ direction, but our research services have a bias to fit inherently unruly markets into tidy narratives. Disclosing the risks to our views is an essential part of our process, but the hypotheses we reject will always get less of an airing than the ones we embrace – no investor has time to read weekly 50-page deliberations. Why Now? The canonical BCA question – So What? – is meant to keep researchers focused on the market relevance of their inquiries. But we have long advocated for a second question – Why Now? – to keep our focus on timeliness. Spotting imbalances, which can take a maddeningly long time to reverse, isn’t enough to earn alpha. To translate macro analysis into promising investment ideas, an investor also needs to identify potential catalysts that might unwind the imbalance. Bull markets become exhausted once so much capital is invested in them that there is no one left to keep buying, just as bear markets end when the urgency to sell dissipates. Sentiment can offer clues into remaining buying or selling power, and the day before the Grantham piece appeared, an experienced financial advisor with a stellar portfolio management record emailed that, “This is one of the few times in my career where I feel like the market is simple and the consensus is right. It almost always feels like there is something obviously bad on the horizon but this market feels like there is really good news on the horizon.” I have known him for over 30 years and can attest to his intelligence, diligence and savvy. His clients are in excellent hands and his constructive take may well be spot on. Indeed, we hope so, since it dovetails with ours, but his assurance gave us pause. For now, it doesn't seem to be universal, as it contrasted starkly with this musing from another trusted confidante (a family office CIO) as 2020 was winding down, “What can be said about work other than make certain we don’t mistake this bull market for brilliance.” Valuation is a notoriously lousy timing indicator and sentiment is a squishy concept that is hard to pin down. Both can remain stretched for a long period of time. An investor shouldn't bet against them unless s/he has a good reason for believing they are on the verge of reversing. Perhaps not having to run on the relative performance hamster wheel like most professional investors gives the family office CIO, who also has a great track record, a little broader perspective, but every investor could use a dose of humility. Skepticism is an essential component of successful investing as well, especially as stocks are making new highs. If you think it’s not windy … Investment Implications We respect Jeremy Grantham’s experience and formidable accomplishments and listen closely to any insights he’s willing to share. We acknowledge that there are many signs of froth across financial markets and that the Kindleberger red line of purchasing assets without regard to their intrinsic merit could be crossed in the not-too-distant future. We echo the sentiment that central bankers are not omnipotent and that easy monetary policy is not a magical elixir. We do, however, assert that the combination of extremely easy monetary policy and a new round of fiscal aid offers equities and spread product a supportive backdrop that should be expected to hold throughout the year provided that markets don’t get over their skis by bidding up asset prices too far. The bottom line is that market vulnerabilities are cropping up but we disagree with the view that they are about to bring an end to risk asset outperform-ance. We remain overweight equities and spread product while keeping an eye out for anything untoward. As we have been saying for several weeks, we are bullish, albeit vigilantly so. One of our roles is to worry for our clients, and we are scanning the horizon for signs of trouble even more thoroughly than normal. Until we see those signs, or until risk asset prices rise so much that they sour their risk-reward prospects, we will stick with our call. On the last point, we are in complete agreement with Grantham: The one reality that you can never change is that a higher-priced asset will produce a lower return than a lower-priced asset. You can’t have your cake and eat it. You can enjoy it now, or you can enjoy it steadily in the distant future, but not both – and the price we pay for having this market go higher and higher is a lower 10-year return from the peak. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1https://www.gmo.com/americas/research-library/waiting-for-the-last-dance/ Accessed January 5, 2021. Grantham is the octogenarian co-founder of Grantham, Mayo and van Otterloo (GMO), a value-oriented asset manager for institutional investors. 2 McDonald, Michael. "Grantham’s Bear Market Call Tests Patience of GMO Fund Investors," Bloomberg, November 24, 2020.

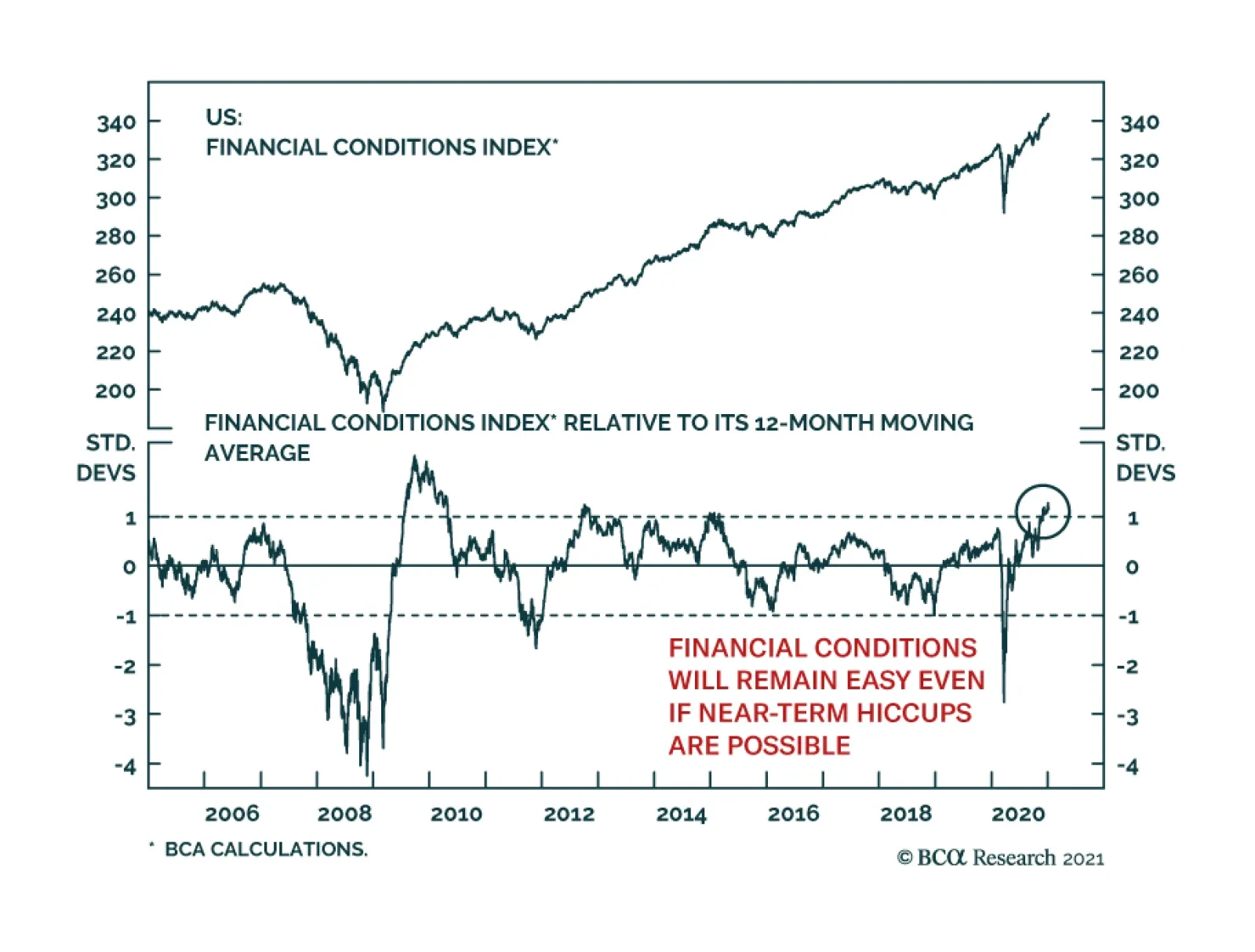

Markets have rallied on the back of easy fiscal and monetary conditions, both of which will boost growth this year, especially now that vaccines will allow for a more permanent softening of rolling lockdowns in the second half of 2021. However, a virtuous…

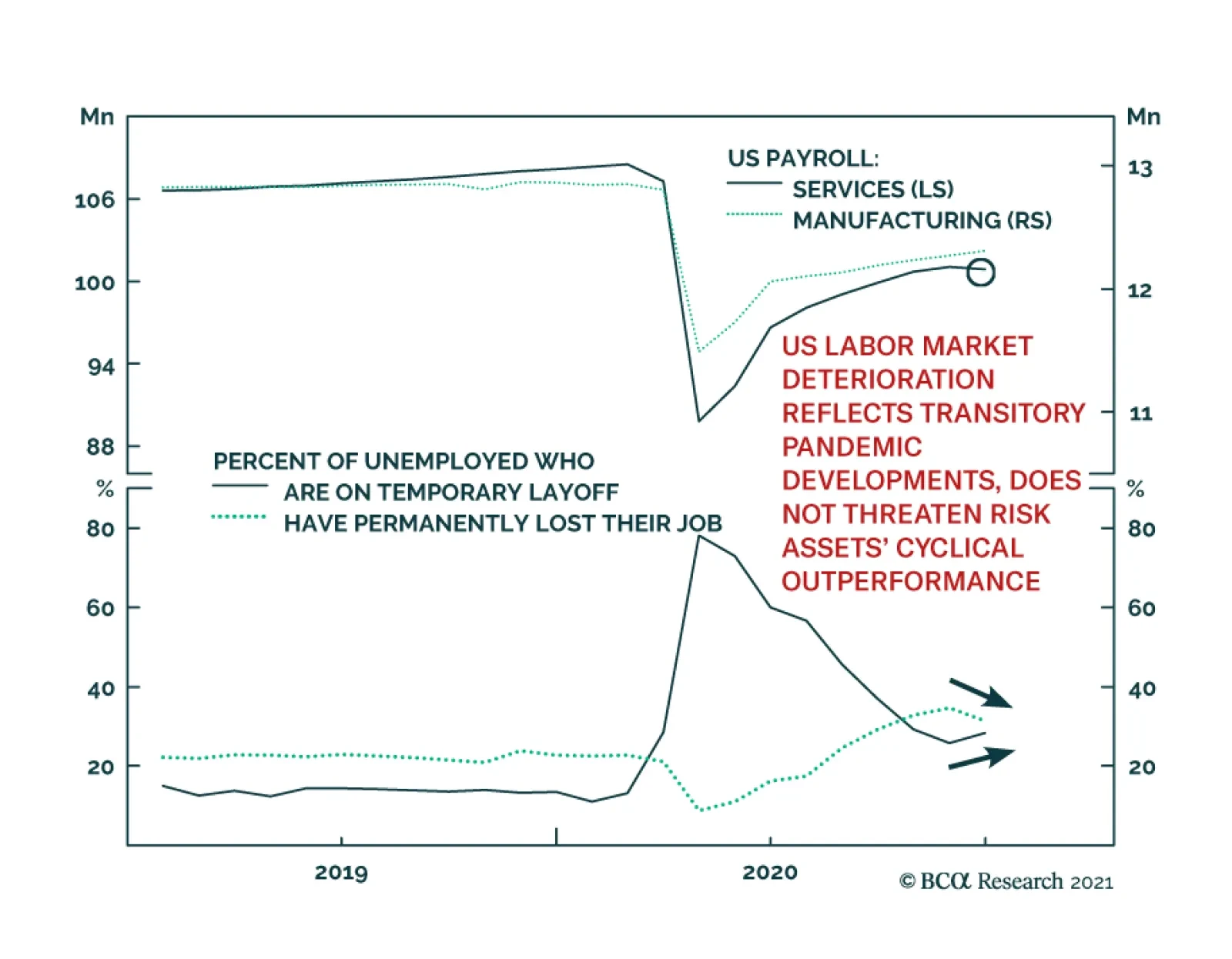

Total US nonfarm payrolls were a major disappointment, falling by 140 thousand in December, after rising in the previous 7 months. But the contents of the report are not nearly as negative for markets as the headline number suggests. Rather than implying…

Highlights A blue wave will likely supercharge the dollar’s downtrend in 2021. The key beneficiaries of this decline will be the much undervalued Scandinavian currencies, as well as those of commodity-producing countries. The initial knee-jerk reaction from the dollar could be positive as inflation lags the improvement in aggregate demand. Our trading model continues to recommend shorting the dollar. This simple three-factor model has outperformed the DXY index by over 300% since 1980. We were stopped out of our short NZD/CAD trade. This is a portfolio hedge. Look to reinstate. Feature The US political landscape is becoming more dollar bearish. This is because a blue wave will likely supercharge fiscal spending and allow for a partial repeal of the Trump tax cuts. Both will boost aggregate demand, without an equivalent offset from higher US interest rates. As we explain below, this is negative for the greenback. As a key reflator for the global economy, a lower US dollar will lead to an outperformance of non-US bourses, lifting animal spirits abroad and in a virtuous cycle, pressuring the dollar even lower. From a technical perspective, the dollar remains very oversold, having declined in almost a straight line since last March. While we continue to expect a dollar bounce, we had initially highlighted in previous reports it will be technical in nature, capped at around 2%-4%. Given this week’s news, chances of a technical bounce remain high, but the amplitude will be much more muted than we initially expected. This dovetails nicely with our trading model, which is politically agnostic, and continues to recommend shorting the dollar for the month of January. Implications Of A Blue Sweep It has been clear since the US election campaign began that Democratic leaders have been more aggressive in their demands for a greater government role in the economy. As such, a blue wave should widen the US budget deficit by much more than was expected under a Republican Senate. All things equal, a wider budget deficit is negative for the greenback. All things equal, a wider budget deficit is negative for the greenback (Chart I-1).1 Higher aggregate demand (via higher government spending) should allow the US output gap to close faster than would have otherwise been the case. This should begin to put upward pressure under domestic inflation. If the Federal Reserve chooses to allow an inflation overshoot, this will depress US real rates further and hurt the dollar in the process. There is a well-established relationship between real interest rate differentials and the greenback (Chart I-2). Chart I-1The Dollar And Budget Deficits

The Dollar And Budget Deficits

The Dollar And Budget Deficits

Chart I-2The Dollar And Real Interest Rates

The Dollar And Real Interest Rates

The Dollar And Real Interest Rates

The US continues to run a large current account deficit, meaning domestic savings have been insufficient to finance investment. A higher budget deficit is likely to widen the current account deficit, assuming private-sector savings do not rise significantly. To finance the shortfall in spending, foreign investors might require a higher risk premium on US assets via higher yields and/or a lower exchange rate. With the Federal Reserve effectively capping nominal yields, a lower exchange rate will be needed to entice foreign investors. A reason behind the dollar’s decline last year has been a stampede out of the Treasury market by foreign investors (Chart I-3). Chart I-3A Dearth Of Foreign Investors

A Dearth Of Foreign Investors

A Dearth Of Foreign Investors

Part of the Biden campaign pledge has also been to raise both corporate and personal income taxes. The US currently enjoys favorable corporate taxes relative to its G10 and BRICS peers (Chart I-4). Higher taxes would lower the return on capital for US investments. Our US Equity Strategists reckon the hit to the technology and health care sectors from a change in the tax rate will be particularly acute, in an order of magnitude of about 13.5% and 13.1% of earnings-per-share, respectively. Inflows into US equities exploded higher last year on the back of low rates and the higher weighting of technology and health care sectors in US bourses (Chart I-5). A reversal of these flows will hurt the dollar. This will occur at a time when expected returns on US equities are particularly low, compared to those in Europe and Japan (Chart I-6). Chart I-4Biden's Tax Plan In Perspective

The Dollar In A Blue Wave

The Dollar In A Blue Wave

Chart I-5US Equity Inflows Have Been Strong

US Equity Inflows Have Been Strong

US Equity Inflows Have Been Strong

Chart I-6ALow Expected Return On US Equities

The Dollar In A Blue Wave

The Dollar In A Blue Wave

Chart I-6BBetter Expected Returns On Eurozone Equities

The Dollar In A Blue Wave

The Dollar In A Blue Wave

Chart I-6CBetter Expected Returns On Japanese Equities

The Dollar In A Blue Wave

The Dollar In A Blue Wave

Is COVID-19 A Red Herring? Chart I-7A Covid-19 Growth Scare?

A Covid-19 Growth Scare?

A Covid-19 Growth Scare?

The analysis above suggests the outlook for the dollar should be bearish. Then why has the greenback been rebounding since the unveiling of a blue sweep? There are two reasons. First, the dollar was already very oversold, suggesting the short-term reward/risk from shorting the currency was not very favorable. Second, inflation is a lagging economic variable, so any impact from fiscal stimulus will first be on real growth, with inflation rising much later. Therefore, fiscal stimulus in the US will likely boost US economic performance relative to its peers in the short term. Meanwhile, as we navigate the winter season in the northern hemisphere, a new wave of infections has taken root. This will likely lead to a widespread deterioration in economic conditions, as economies enter more stringent lockdowns. Around the G10, various measures of lockdowns are being implemented, with particularly restrictive measures in the UK and Canada where new cases are close to record highs. Infection trends remain favorable in Australia and New Zealand, probably due to previous localized lockdowns (Chart I-7). However, with new, more infectious strains being first spotted in the UK and then South Africa, the bar is very low for a worldwide-renewed infection wave. The impact on currency markets is two-fold. First, the dollar is a counter-cyclical currency and so will benefit from safe-haven flows that will erupt with any renewed relapse in growth. With the dollar having traded inversely neck-in-neck with the S&P 500, any equity correction will provide a much healthy catalyst for a dollar bounce (Chart I-8). Any bounce in the USD should be faded as robust global growth in 2021 is expected. More directly, the impact for currency markets will be through relative economic growth. The improvement in the December Purchasing Managers’ Index was more favorable outside the US, particularly in Sweden, Canada, and the UK. That said, the greenback has undershot the trend dictated by the relative economic performance between the US and the rest of the G10 (Chart I-9). Should the US quickly bridge the gap between herd immunity (through vaccinations) and the spread of the virus, US economic growth could gain the upper hand. Chart I-8The Dollar And Markets

The Dollar And Markets

The Dollar And Markets

Chart I-9The Dollar And Relative Growth

The Dollar And Relative Growth

The Dollar And Relative Growth

Ultimately, the near-term potential impact from COVID-19 will be much less than economies endured in the first half of 2020. The main reason is that the vaccine rollout is accelerating, with many other candidates in the pipeline. This will allow for robust global growth in 2021, which will ease safe-haven flows into the US dollar. Thus, any bounce in the USD should be faded rather than leaned into, as we have been arguing since October of last year.2 FX Trading Model Chart I-10BCA FX Trading Model

BCA FX Trading Model

BCA FX Trading Model

How does our trading model feel about a blue sweep? It is agnostic, given that none of the inputs are directly driven by US politics. The one area where US politics could affect the model is through real rates, but as we have argued, this is a slow-moving process. More importantly, the model serves as a rules-based approach in trading foreign exchange. In short, three criteria drive the model:3 A macroeconomic variable that captures the most important relative price between any two currencies: the real interest rate. A valuation measure that captures dislocation in a currency pair relative to its own history. A key assumption is stationarity, meaning the currency cross will mean-revert back to fair value over time. A sentiment indicator. The key assumption here is that the dollar is a momentum currency. This very simplistic approach has outperformed a buy-and-hold DXY portfolio by 325% since 1980 (Chart I-10). Given the encouragement from this initial result, we will be releasing part two of the model in the coming weeks. The FX market is likely to become more volatile and provide more opportunities. For now, the model recommends shorting the DXY for the month of January, driven by long positions in the Swedish krona, Swiss franc, and Japanese yen. Less favorable currencies are the Australian and New Zealand dollars (Chart I-11). Such a barbell strategy of some high-beta currencies, together with some safe havens, might be just what the doctor ordered. In our FX portfolio, we prefer to stick with trades at the crosses. So far, our trading recommendations have benchmarked favorably against the model recommendations (Chart I-12). We will build on this success in future iterations. Chart I-11Long = Greater Than 0; Short = Less Than 0

The Dollar In A Blue Wave

The Dollar In A Blue Wave

Chart I-12Man Versus BCA Machine

The Dollar In A Blue Wave

The Dollar In A Blue Wave

Housekeeping Our portfolio has benefited tremendously from the overall short dollar position we have been recommending since 2019. However, in light of possible volatility in the coming weeks, we are tightening stop-losses on a few of our profitable trades. We hold a basket of Scandinavian currencies against both the dollar and the euro. Tighten the stop loss to a 2% loss from initiation, given recent gains. Stay long silver versus gold but tighten the stop loss to 75 to lock in some profits. Our long yen portfolio hedge has performed quite well. Tighten the stop loss from 110 to 105. We were stopped out of our short NZD/CAD trade for a loss of 1.8%. Stand aside for now, with a view to re-establish later. We are still short NZD versus AUD. Tighten the stop loss to 1.02. In our view, the FX market is likely to uncover many macro opportunities as the year unfolds. Stay tuned. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Weekly Report, “The Dollar And The Budget Deficit: From Theory To Practice,” dated August 14, 2020. 2 Please see Foreign Exchange Strategy Weekly Report, “Tail Risks In FX Markets,” dated October 2, 2020. 3 Please see Foreign Exchange Strategy Weekly Report, “Building A Protector Currency Portfolio,” dated February 7, 2020. Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the US have been robust: The final read of the Markit Manufacturing PMI was 57.1 in December, compared to a prior reading of 56.5. The ISM manufacturing index came in at a very robust 60.7 for the month of December, well above expectations. The trade balance in the US remained near cycle lows at -$68.1bn for November. The DXY index fell slightly this week. It is becoming quite clear that December was a robust month for economic data, both in the US and abroad. As a result, the US dollar, which is a counter-cyclical currency, depreciated modestly. With the prospect of higher fiscal stimulus in the US, but an accommodative Federal Reserve, lower real rates should keep a cap on the dollar. Report Links: The Dollar Conundrum And Protection - November 6, 2020 The Dollar In A Market Reset - October 30, 2020 A Few Market Observations - October 23, 2020 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data from the euro area have held up: The Markit Manufacturing Index remained at the 55 level for the month of December (from 55.5 to 55.2). Producer prices continue to deflate at 2% per year, but the November decline compares favorably to the 5% year-on-year drop in May last year. Core CPI remained flat at 0.2% in December. The euro appreciated by 0.2% against the US dollar this week. The dominant theme in markets remains a broad-based dollar decline, with the euro being the key liquid beneficiary of this move. Most of Europe has managed to flatten the infection curve for Covid-19, which should allow economic momentum to improve further. Report Links: The Dollar Conundrum And Protection - November 6, 2020 Addressing Client Questions - September 4, 2020 On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 The Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data from Japan has been quite disappointing: Cash earnings fell by 2.2% for the month of November. The key driver was a 10.3% decline in overtime pay and 22.9% decline in bonus payments. The Jibun manufacturing PMI was relatively flat at the 50 boom/bust level in December. On a positive note, vehicle sales improved by 7.4% year-on-year in December. It is becoming more evident that a replacement cycle in Japanese autos in underway. The Japanese yen depreciated by 0.7% against the US dollar this week. The key theme this week was a rise in US bond yields, which made the allure of Japanese fixed income less attractive. With Japanese yields anchored at 0%, rising global yields make Japan fixed income returns attractive, but the currency a short in a global portfolio. We are long the Japanese yen and are tightening stops to protect profits. Report Links: The Dollar Conundrum And Protection - November 6, 2020 The Near-Term Bull Case For The Dollar - February 28, 2020 Building A Protector Currency Portfolio - February 7, 2020 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the UK have been mixed: The Markit Manufacturing PMI printed a final 57.5 for December. Mortgage approvals continue to inflect higher, with 105K submissions absorbed in November. UK services remain in recession. The Markit services PMI came in at 49.4 in December, from 49.9 last month. The British pound was flat this week. The Brexit imbroglio is now behind us, and the UK must now contend with the uncomfortable combination of rising Covid-19 cases and a new relationship with the EU. This has prevented the pound from fully celebrating an end to uncertainty. Our roadmap remains valuation, as we see the pound as cheap versus both the dollar and euro, hence our short EUR/GBP position. Report Links: The Dollar Conundrum And Protection - November 6, 2020 Revisiting Our High-Conviction Trades - September 11, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been solid: Building approvals improved 2.6% month-on-month in November. The trade balance remains at a healthy surplus of A$5bn in November. While imports expanded 10% month-on-month, exports remained a healthy 3% over the October print. The Australian dollar appreciated by 1.2% against the US dollar this week. The AUD continues to benefit from favorable terms-of-trade, not only from high iron ore prices, but from the looming shortage of readily available liquefied natural gas (LNG) as Japan and Korea enter unusually cold weather. This is bullish the AUD. Report Links: An Update On The Australian Dollar - September 18, 2020 On AUD And CNY - January 17, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

There was scant data out of New Zealand this week: CoreLogic house prices expanded by 11.1% year-on-year in December. The New Zealand dollar appreciated by 1.1% against the US dollar this week. The kiwi has been on fire in recent weeks, driven not only by the unwinding of expectations of negative rates by the RBNZ, but also by rising terms of trade as agricultural prices recover. We have been fading the kiwi rally, and were offside on our short NZD/CAD trade for a cumulative loss 1.8% loss this week. We are standing aside for now. Report Links: Currencies And The Value-Versus-Growth Debate - July 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Place A Limit Sell On DXY At 100 - November 15, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data from Canada have held up: The Markit manufacturing PMI came in at 57.9 in December, an increase from the prior read of 55.8. The trade balance remains in a deficit of $C3.34bn for November, in line with the previous month. The Canadian dollar appreciated by 0.8% against the US dollar this week. There was good news on the oil front that boosted the loonie. Saudi Arabia agreed to absorb cuts of 1 million barrels a day, allowing a more fervent rebalancing of the oil market. This boosted petrocurrencies, including the loonie. Report Links: Currencies And The Value-Versus-Growth Debate - July 10, 2020 More On Competitive Devaluations, The CAD And The SEK - May 1, 2020 A New Paradigm For Petrocurrencies - April 10, 2020 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data from Switzerland have been mixed: The manufacturing PMI came in at 58 in December, well above expectations of 54.3 and a prior reading of 55.2. Switzerland remains in deflation. Core CPI came in at -0.4% in December versus expectations of -0.2%. Headline CPI was even more negative at -0.8%. The Swiss franc depreciated by 0.4% against the US dollar this week. There is no doubt that the strong franc is exerting deflationary pressures into the Swiss economy. This is evident not only from tradeable prices, but also from domestic inflation. Encouragingly, the manufacturing sector is picking up, which is providing a valve for less intervention by the SNB. We are long EUR/CHF on grounds that the franc is too strong versus the euro. Report Links: The Dollar Conundrum And Protection - November 6, 2020 On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Currency Market Signals From Gold, Equities And Flows - January 31, 2020 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

There was scant data out of Norway this week: The DNB/NIMA manufacturing PMI was flat at 51.9 in December. The Norwegian krone surged by 1.44% against the US dollar this week as the best performing G10 currency. Given the lack of economic data, the key narrative was the oil deal where the Saudis curtailed production. As our top pick for currency outperformance this year, this is much welcomed news. Stay long NOK versus both the USD and EUR. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 A New Paradigm For Petrocurrencies - April 10, 2020 Building A Protector Currency Portfolio - February 7, 2020 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data from Sweden have been robust: The Swedbank/Silf manufacturing PMI surged from 59.1 to 64.9. The Swedish krona rose by 0.7% against the US dollar this week. Sweden is in a sweet spot, where low interest rates are emboldening risk taking and a robust global manufacturing cycle is keeping Swedish supply chains busy. With this virtuous cycle slated to continue, this would continue to be a boost for the krona. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights Further fiscal easing is likely in the US now that the Democrats are set to take control of the US Senate following Tuesday’s runoff elections in Georgia. With the end of the pandemic in sight, a growing chorus of commentators, including none other than Larry Summers, are sounding the alarm over fears that fiscal policy could end up being too stimulative. In the short term, the risk that economies will overheat due to excessive fiscal support is low. There is still too much labor market slack, the bulk of any stimulus checks will be saved, and the short-run Phillips curve remains quite flat. Looking beyond the next two years, fiscal policy could indeed turn out to be inflationary. Political populism is rising. Central banks, fearful of the zero lower-bound constraint on interest rates, want higher inflation. Falling interest rates have also made it easier for governments to run larger budget deficits. We estimate that the US can run a primary budget deficit that is more than 2% of GDP larger than at the start of 2019, while still achieving a stable debt-to-GDP ratio. The “fiscal envelope” has increased significantly in other major economies as well. Ironically, in a world where interest rates are below the trend growth in GDP, a higher debt-to-GDP ratio permits larger budget deficits. Investors should remain overweight stocks relative to bonds over a cyclical 12-month horizon, favoring “value stocks” which will benefit more from steeper yield curves and the dismantling of lockdown measures. Financial markets will face a period of extreme turbulence in a couple of years once inflation begins to accelerate. A Race Against Time The past few weeks have seen a race between the virus, which continues to infect people at an alarming rate, and efforts to vaccinate the most vulnerable members of society. So far, the virus has the upper hand. Chart 1Tracking The Progress In Global Vaccination Rates

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

The “UK strain” has become more prevalent around the world.1 By some estimates it is 70% more contagious than the original virus that emerged in Wuhan, China. Another, potentially even more dangerous strain, has surfaced in South Africa and has spread to South America. The early evidence suggests that the recently approved vaccines will be effective in fighting the UK strain. Unfortunately, there is not enough data to judge whether this is also true for the South African strain. Right now, only 0.2% of the world’s population has been inoculated, but that number will rise rapidly over the coming months (Chart 1). Assuming that existing vaccines are effective against the myriad virus strains, the infection rate should fall precipitously by the middle of the year. Georgia Runoffs Will Lead To Even More Stimulus Governments eased fiscal policy significantly last year in response to the unfolding crisis (Chart 2). At the worst point of the pandemic in April, US real disposable income was up 14% year-over-year (Chart 3). Transfers to households fell sharply following the expiration of the CARES Act, but are set to rise again thanks to the recently completed stimulus deal. Chart 2Fiscal Policy In 2020: Governments Eased Significantly In Response To The Unfolding Crisis

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

The victory by both Democratic candidates in the Georgia Senate runoff races on Tuesday moves the political configuration in Washington even further towards fiscal easing. Having gained control of the Senate, the Democrats will now be able to use the “reconciliation process” to pass a budget that boosts spending on health care, education, infrastructure, and the environment. Granted, reconciliation requires that any extra spending be offset by additional revenue measures over a 10-year budgetary horizon. Thus, corporate taxes will probably rise. Nevertheless, the combination of more spending and higher corporate taxes will still produce a net boost to aggregate demand. This is partly because any revenue measures are likely to be backloaded. It is also because raising corporate taxes will not reduce investment by very much. The experience from the Trump tax cuts revealed that the main consequence of lowering corporate tax rates was to lower corporate tax receipts. The touted boost to corporate investment from lower taxes never materialized. In fact, outside of the energy sector – which benefited from an unrelated recovery in crude oil prices – US corporate capex grew more slowly between Q4 of 2016 and Q4 of 2019 than it did over the preceding three years (Chart 4). Chart 3Personal Income Jumped Early On In The Pandemic

Personal Income Jumped Early On In The Pandemic

Personal Income Jumped Early On In The Pandemic

Chart 4No Evidence That Trump Corporate Tax Cuts Boosted Investment

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

For stock market investors, the prospect of higher taxes will take some of the bloom off the rose from additional fiscal stimulus. That said, the impact will vary considerably across equity sectors. Cyclical stocks such as industrials and materials will benefit from stimulus-induced economic growth. Banks will also gain because stronger growth will suppress loan losses, while leading to steeper yield curves, thus raising net interest margins in the process. Value stocks have more exposure to banks and deep cyclicals, and hence we remain positive on them. Small caps also have more exposure to these sectors, but are starting to look increasingly pricey. Stimulus: How Much Is Enough? Chart 5Commercial Bankruptcies Are Well Contained

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Fiscal stimulus helped avert the cascade of business failures that normally accompany recessions. Despite a tick up in bankruptcies among large companies shortly after the pandemic began, 16% fewer companies filed for bankruptcy in the first 11 months of 2020 compared to the same period in 2019 (Chart 5). Overall bankruptcy filings, which include personal bankruptcies, have fallen to a 35-year low according to Epiq AACER. The pipeline for bankruptcies also looks fairly narrow. Junk bond prices have been rebounding and consumer loan delinquency rates have been trending down (Table 1). Table 1Personal Loan Delinquencies Have Also Been Trending Lower

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Generous fiscal transfers have allowed households to accumulate plenty of savings, which should help propel future spending. Chart 6 shows that accumulated US household savings are about $1.5 trillion above their pre-pandemic trend. We estimate that the combination of increased savings, rising home prices, and a surging stock market pushed up household net worth by $8 trillion in Q4 alone, leaving it 11% above Q4 2019 levels. In comparison, household net worth fell by over 15% during the Great Recession. Chart 6Households Have Accumulated Lots Of Savings, Which Should Help Propel Future Spending

Households Have Accumulated Lots Of Savings, Which Should Help Propel Future Spending

Households Have Accumulated Lots Of Savings, Which Should Help Propel Future Spending

Little Risk Of Near-Term Fiscal Overheat With the prospect of a vaccine-led economic recovery in sight, a growing chorus of commentators are sounding the alarm over fears that fiscal policy could end up being too stimulative. In an interview with Bloomberg Television, Larry Summers contended that President Trump’s attempt to increase the size of stimulus checks from $600 per person to $2000 was “a serious mistake” that risked overheating the economy. Summers argued for a more streamlined approach that prioritized aid to state and local governments and increased funding for Covid testing and vaccine deployment. Despite Larry’s admonition, we see little risk that loose fiscal policy will cause any major economy to overheat in the near term, even if the Senate does enact more stimulus. For one thing, recent stimulus proposals have emphasized direct transfers to households. Unlike most other types of spending, across-the-board stimulus checks will go mainly into savings. The New York Fed has estimated that less than 30% of the direct stimulus payments in the CARES Act were used for consumption, with 36% saved and 35% used to pay down debt. Consistent with past experience, households expect to spend only about one-third of the forthcoming stimulus checks according to CivicScience, a market research firm (Chart 7). Chart 7How Will Americans Spend Their Second Stimulus Check?

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Chart 8Employment-To-Population Ratios Remain Well Below Pre-Pandemic Levels

Employment-To-Population Ratios Remain Well Below Pre-Pandemic Levels

Employment-To-Population Ratios Remain Well Below Pre-Pandemic Levels

Moreover, there is still plenty of labor market slack. Chart 8 shows the employment-to-population ratio for prime-aged workers remains well below pre-pandemic levels across the OECD. In a best-case scenario, it will take a couple more years for employment levels to return to normal. Long-term inflation expectations are also well anchored, implying that the short-run Phillips curve is quite flat. In simple English, this means that a temporary burst of stimulus is unlikely to trigger an inflationary price-wage spiral. Some decline in budget deficits is also likely after the pandemic ends. The Hutchins Center at Brookings expects the fiscal package passed by the US Congress in December to boost GDP by 7% in the first quarter. However, it expects the four-quarter moving average in the fiscal contribution to growth to turn negative in the third quarter, and stay that way right through 2022 (Chart 9). Likewise, in its most recent forecasts, the IMF projected a negative fiscal impulse in the major advanced economies in 2021-22 (Chart 10). Chart 9Budget Deficits Set To Decline, But Remain High By Historic Standards (Part I)

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Chart 10Budget Deficits Set To Decline, But Remain High By Historic Standards (Part II)

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Long-Term Fiscal Picture Is More Inflationary Granted, a negative fiscal impulse simply means that the structural budget deficit is declining over time. In absolute terms, the IMF expects budget deficits to remain quite large by historic standards, even if they do come down from their pandemic peak. Remember, it is the level of the budget deficit that helps determine the level of demand throughout the economy. Economies overheat when the level of aggregate demand exceeds the level of aggregate supply. If private-sector demand recovers more quickly than budget deficits come down, overall demand will rise. As such, it is certainly possible that excessively easy fiscal policy will contribute to an inflationary overshoot once labor market slack has been fully absorbed in two-to-three years. Politically, such an overshoot seems quite plausible. Populism is rising both on the left and the right. It is noteworthy that the Republican candidates in Tuesday’s runoff Senate races supported President Trump’s call for boosting the size of stimulus checks. The same goes for Senators Lindsey Graham of South Carolina and Marco Rubio of Florida. Rubio is widely considered an early front-runner for the 2024 Republican presidential nomination. Economically, the case for bigger budget deficits has also become more appealing. Real interest rates are negative across the major economies. Low interest rates allow governments to take on more debt without having to make large interest payments. Indeed, the Japanese government today receives more interest than it pays by virtue of the fact that more than half of its debt was issued at negative rates. Persistent worries about the zero lower-bound constraint also encourage central banks to pursue policies that could fuel inflation, such as refraining from tightening monetary policy in response to looser fiscal policy. The current level of policy rates gives central banks almost no scope to cut rates in response to an adverse economic shock. If inflation were to rise, central banks would be able to bring real rates even further into negative territory should economic conditions warrant it. The Paradox Of Debt Sustainability When r Is Less Than g One might think that today’s high debt-to-GDP ratios would force governments to slash deficits to keep debt from spiraling out of control. However, things are not so straightforward in a world of ultra-low interest rates. As Appendix A shows, the primary budget balance that is consistent with a stable debt-to-GDP ratio can be expressed as:

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Where p is the primary budget balance (the difference between tax receipts and non-interest spending, expressed as a share of GDP), r is the real interest rate, and g is the growth rate of the economy. Notice that when r is less than g, a higher debt-to-GDP ratio corresponds to a larger primary budget deficit (i.e., a more negative p). In other words, by taking on more debt, governments would not only be able to raise spending or cut taxes, but they would also have enough money left over to pay the additional interest on the debt. And they could do all this without putting the debt-to-GDP ratio on an unsustainable upward trajectory. Chart 11More Space For Bigger Budget Deficits In The US...

More Space For Bigger Budget Deficits In The US...

More Space For Bigger Budget Deficits In The US...

What sort of funky magic allows this to happen? The answer is that even a small percentage increase in debt will correspond to a large increase in the absolute stock of debt when debt levels are elevated to begin with. If interest rates are low, most of the additional debt can go into financing a larger primary deficit instead of higher interest payments. One can see this point with a simple example. Suppose that initially, debt is 50, GDP is 100, and hence the debt-to-GDP ratio is 50%. Let us also assume that the primary deficit is 1% of GDP, the interest rate is 2%, and GDP grows at 4%. Next year, debt will be 50+50*0.02+1=52 while GDP will be 100*1.04=104. Hence, the debt-to-GDP ratio will remain 52/104=50%. Now rerun the same example but assume that debt is initially equal to 100, implying an initial debt-to-GDP ratio of 100%. In that case, it is simple to verify that the debt-to-GDP ratio would fall to 103/104≈99% the following year if the primary deficit remained at 1% of GDP. The primary deficit would have to rise to 2% of GDP to keep the debt-to-GDP stable – double what it was in the first example. The level of the US primary budget deficit that is consistent with a stable debt-to-GDP ratio has risen from 0.8% of GDP at the start of 2019 to 3.1% today if one uses the Congressional Budget Office’s estimate of trend growth and the 10-year TIPs yield as a proxy for the real interest rate (Chart 11). A similar trend is visible abroad (Chart 12). Chart 12... As Well As In Other Major Economies

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Investment Conclusions Thanks to the drop in interest rates, governments today have more scope to run larger budget deficits than they did in the past. This suggests that the sort of fiscal tightening that impeded the recovery following the Great Recession is unlikely to reoccur. The combination of above-trend growth and continued low rates will buoy equities in 2021. Investors should remain overweight stocks relative to bonds over a cyclical 12-month horizon, favoring “value stocks” which will benefit both from steeper yield curves and the dismantling of lockdown measures. Financial markets will face a period of extreme turbulence in a couple of years as unemployment approaches pre-pandemic levels and central banks begin to contemplate raising interest rates. A higher debt burden allows for a larger budget deficit when r is less than g, but requires a bigger budget surplus when r rises above g. If debt-saddled governments are unable or unwilling to tighten fiscal policy, they may end up applying political pressure on central banks to keep rates artificially low in order to suppress interest payments. As such, excessively easy monetary policy could trigger a bout of inflation. With that in mind, investors should maintain below-benchmark duration exposure in fixed-income portfolios, favor inflation protected-securities over nominal bonds, and hold other inflation hedges such as gold and farmland. Cryptocurrencies could potentially serve as an inflation hedge, but given the recent run up in bitcoin prices, we would avoid this area of the market for the time being. Appendix AThe Arithmetic Of Debt Sustainability

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 A number of SARS-CoV-2 variants are circulating globally. The WHO reported this week that the UK variant of Covid-19 has spread to 40 other countries. Initial research suggests that the UK strain is more transmissible, but is characterized by unchanged disease severity compared to the original virus. The South African strain is also believed to be more contagious and was detected in six other countries. Some have raised concerns about the high number of mutations found in the South African variant. Research is ongoing to determine the potential consequences of the emerging variants on the speed of transmission, disease severity, ability to evade detection, and the efficacy of current treatments and vaccines. Please see Antony Sguazzin, “South Africa Virus Strain More Transmissible, Not More Severe,” Bloomberg, January 7, 2021; Gabriele Steinhauser, “The New Covid-19 Strain in South Africa: What We Know,” The Wall Street Journal, January 6, 2021; “Weekly epidemiological update - 5 January 2021,” World Health Organization; and “Emerging SARS-CoV-2 Variants,” Centers for Disease Control and Prevention, updated January 3, 2021. Global Investment Strategy View Matrix

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Special Trade Recommendations

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Current MacroQuant Model Scores

Fiscal Stimulus: How Much Is Too Much?

Fiscal Stimulus: How Much Is Too Much?

Highlights Markets largely ignored the uproar at the US Capitol on January 6 because the transfer of power was not in question. Democratic control over the Senate, after two upsets in the Georgia runoff, is the bigger signal. US fiscal policy will become more expansive yet the Federal Reserve will not start hiking rates anytime soon. This is a powerful tailwind for risk assets over the short and medium run. Politics and geopolitics affect markets through the policy setting, rather than through discrete events, which tend to have fleeting market impacts. The current setting, in the US and abroad, is negative for the US dollar. The implication is positive for emerging market stocks and value plays. Go long global stocks ex-US, long emerging markets over developed markets, and long value over growth. Cut losses on short CNY-USD. Feature Chart 1Market's Muted Response To US Turmoil

Market's Muted Response To US Turmoil

Market's Muted Response To US Turmoil

Scenes of mayhem unfolded in the US Capitol on January 6 as protesters and rioters flooded the building and temporarily interrupted the joint session of Congress convened to count the Electoral College votes. Congress reconvened later and finished the tally. President-elect Joe Biden will take office at noon on January 20. Financial markets were unperturbed, with stocks up and volatility down, though safe havens did perk up a bit (Chart 1). The incident supports our thesis that the US election cycle of 2020 was a sort of “Civil War Lite” and that the country is witnessing “Peak Polarization,” with polarization likely to fall over the coming five years. The incident was the culmination of the past year of pandemic-fueled unrest and President Trump’s refusal to concede to the Electoral College verdict. Trump made a show of force by rallying his supporters, and apparently refrained from cracking down on those that overran Congress, but then he backed down and promised an orderly transfer of power. The immediate political result was to isolate him. Fewer Republicans than expected contested the electoral votes in the ensuing joint session; one Republican is openly calling for Trump to be forced into resignation via the 25th amendment procedure for those unfit to serve. The electoral votes were promptly certified. Vice President Mike Pence and other actors performed their constitutional duties. Pence reportedly gave the order to bring out the National Guard to restore order – hence it is possible that Pence and Trump’s cabinet could activate the 25th amendment, but that is unlikely unless Trump foments rebellion going forward. Vandals and criminals will be prosecuted and there could also be legal ramifications for Trump and some government officials. Do Politics And Geopolitics Affect Markets? The market’s lack of concern raises the question of whether investors need trouble themselves with politics at all. Philosopher and market guru Nassim Nicholas Taleb tweeted the following: If someone, a year ago, described January 6, 2021 (and events attending it) & asked you to guess the stock market behavior, admit you would have gotten it wrong. Just so you understand that news do not help you understand markets.1 This is a valid point. Investors should not (and do not) invest based on the daily news. Of course, many observers foresaw social unrest surrounding the 2020 election, including Professor Peter Turchin.2 Social instability was rising in the data, as we have long shown. When you combined this likelihood with the Fed’s pause on rate hikes, and a measurable rise in geopolitical tensions between the US and other countries, the implication was that gold would appreciate. So if someone had told you a year ago that the US would have a pandemic, that governments would unleash a 10.2% of global GDP fiscal stimulus, that the Fed would start average inflation targeting, that a vaccine would be produced, and that the US would have a contested election on top of it all, would you have expected gold to rise? Absolutely – and it has done so, both in keeping with the fall in real interest rates plus some safe-haven bonus, which is observable (Chart 2). Chart 2Gold Price In Excess Of Fall In Real Rates Implies Geopolitical Risk

Gold Price In Excess Of Fall In Real Rates Implies Geopolitical Risk

Gold Price In Excess Of Fall In Real Rates Implies Geopolitical Risk

The takeaway is that policy matters for markets while politics may only matter briefly at best. Which brings us back to the implications of the Trump rebellion. What Will Be The Impact Of The Trump Rebellion? We have highlighted that this election was a controversial rather than contested election – meaning that the outcome was not in question after late November when the court cases, vote counts, and recounts were certified. This was doubly true after the Electoral College voted on December 14. The protests and riots yesterday never seriously called this result into question. Whatever Trump’s intentions, there was no military coup or imposition of martial law, as some observers feared. In fact the scandal arose from the President’s hesitation to call out the National Guard rather than his use of security forces to prevent the transfer of power, as occurs during a coup. This partially explains why the market traded on the contested election in December 2000 but not in 2020 – the result was largely settled. The Biden administration now has more political capital than otherwise, which is market-positive because it implies more proactive fiscal policy to support the economic recovery. Trump’s refusal to concede gave Democrats both seats in the Georgia Senate runoffs, yielding control of Congress. Household and business sentiment will revive with the vaccine distribution and economic recovery, while the passage of larger fiscal stimulus is highly probable. US fiscal policy will almost certainly avoid the mistake of tightening fiscal policy too soon. Taken with the Fed’s aversion to raising rates, greater fiscal stimulus will create a powerful tailwind for risk assets over the next 12 months. The primary consequence of combined fiscal and monetary dovishness is a falling dollar. The greenback is a counter-cyclical and momentum-driven currency that broadly responds inversely to global growth trends. But policy decisions are clearly legible in the global growth path and the dollar’s path over the past two decades. Japanese and European QE, Chinese devaluation, the global oil crash, Trump’s tax cuts, the US-China trade war, and COVID-19 lockdowns all drove the dollar to fresh highs – all policy decisions (Chart 3). Policy decisions also ensured the euro’s survival, marking the dollar’s bottom against the euro in 2011, and ensuring that the euro could take over from the dollar once the dollar became overbought. Today, the US’s stimulus response to COVID-19 – combined with the Fed’s strategic review and the Democratic sweep of government – marked the peak and continued drop-off in the dollar. Chart 3Euro Survival, US Peak Polarization, Set Stage For Rotation From USD To EUR

Euro Survival, US Peak Polarization, Set Stage For Rotation From USD To EUR

Euro Survival, US Peak Polarization, Set Stage For Rotation From USD To EUR

Chart 4China's Yuan Says Geopolitics Matters

China's Yuan Says Geopolitics Matters

China's Yuan Says Geopolitics Matters

The Chinese renminbi is heavily manipulated by the People’s Bank and is not freely exchangeable. The massive stimulus cycle that began in 2015, in reaction to financial turmoil, combined with the central bank’s decision to defend the currency marked a bottom in the yuan’s path. China’s draconian response to the pandemic this year, and massive stimulus, made China the only major country to contribute positively to global growth in 2020 and ensured a surge in the currency. The combination of US and Chinese policy decisions has clearly favored the renminbi more than would be the case from the general economic backdrop (Chart 4). Getting the policy setting right is necessary for investors. This is true even though discrete political events – including major political and geopolitical crises – have fleeting impacts on markets. What About Biden’s Trade Policy? Trump was never going to control monetary or fiscal policy – that was up to the Fed and Congress. His impact lay mostly in trade and foreign policy. Specifically his defeat reduces the risk of sweeping unilateral tariffs. It makes sense that global economic policy uncertainty has plummeted, especially relative to the United States (Chart 5). If US policy facilitates a global economic and trade recovery, then it also makes sense that global equities would rise faster than American equities, which benefited from the previous period of a strong dollar and erratic or aggressive US fiscal and trade policy. Trump’s last 14 days could see a few executive orders that rattle stocks. There is a very near-term downside risk to European and especially Chinese stocks from punitive measures, or to Emirati stocks in the event of another military exchange with Iran (Chart 6). But Trump will be disobeyed if he orders any highly disruptive actions, especially if they contravene national interests. Beyond Trump’s term we are constructive on all these bourses, though we expect politics and geopolitics to remain a headwind for Chinese equities. Chart 5Big Drop In Global Policy Uncertainty

Big Drop In Global Policy Uncertainty

Big Drop In Global Policy Uncertainty

US tensions with China will escalate again soon – and in a way that negatively impacts US and Chinese companies exposed to each other. Chart 6Geopolitical Implications Of Biden's Election

Geopolitical Implications Of Biden's Election

Geopolitical Implications Of Biden's Election

The cold war between these two is an unavoidable geopolitical trend as China threatens to surpass the US in economic size and improves its technological prowess. Presidents Xi and Trump were merely catalysts. But there are two policy trends that will override this rivalry for at least the first half of the year. First, global trade is recovering– as shown here by the Shanghai freight index and South Korean exports and equity prices (Chart 7). The global recovery will boost Korean stocks but geopolitical tensions will continue to brood over more expensive Taiwanese stocks due to the US-China conflict. This has motivated our longstanding long Korea / short Taiwan recommendation. Chart 7Global Economy Speaks Louder Than North Korea

Global Economy Speaks Louder Than North Korea

Global Economy Speaks Louder Than North Korea

Chart 8China Wary Of Over-Tightening Policy

China Wary Of Over-Tightening Policy

China Wary Of Over-Tightening Policy

Chart 9Global Stock-Bond Ratio Registers Good News

Global Stock-Bond Ratio Registers Good News

Global Stock-Bond Ratio Registers Good News

Second, China’s 2020 stimulus will have lingering effects and it is wary of over-tightening monetary and fiscal policy, lest it undo its domestic economic recovery. The tenor of China’s Central Economic Work Conference in December has reinforced this view. Chart 8 illustrates the expectations of our China Investment Strategy regarding China’s credit growth and local government bond issuance. They suggest that there will not be a sharp withdrawal of fiscal or quasi-fiscal support in 2021. Stability is especially important in the lead up to the critical leadership rotation in 2022.3 This policy backdrop will be positive for global/EM equities despite the political crackdown on General Secretary Xi Jinping’s opponents will occur despite this supportive policy backdrop. The global stock-to-bond ratio has surged in clear recognition of these positive policy trends (Chart 9). Government bonds were deeply overbought and it will take several years before central banks begin tightening policy. What About Biden’s Foreign Policy? Chart 10OPEC 2.0 Cartel Continues (For Now)

Accommodative US Monetary Policy, Tighter Commodity Markets Will Stoke Inflation OPEC 2.0 Cartel Continues (For Now)

Accommodative US Monetary Policy, Tighter Commodity Markets Will Stoke Inflation OPEC 2.0 Cartel Continues (For Now)

Iran poses a genuine geopolitical risk this year – first in the form of an oil supply risk, should conflict emerge in the Persian Gulf, Iraq, or elsewhere in the region. This would inject a risk premium into the oil price. Later the risk is the opposite as a deal with the Biden administration would create the prospect for Iran to attract foreign investment and begin pumping oil, while putting pressure on the OPEC 2.0 coalition to abandon its current, tentative, production discipline in pursuit of market share (Chart 10). Biden has the executive authority to restore the 2015 nuclear deal (Joint Comprehensive Plan of Action). He is in favor of doing so in order to (1) prevent the Middle East from generating a crisis that consumes his foreign policy; (2) execute an American grand strategy of reviving its Asia Pacific influence; (3) cement the Obama administration’s legacy. The Iranian President Hassan Rouhani also has a clear interest in returning to the deal before the country’s presidential election in June. This would salvage his legacy and support his “reformist” faction. The Supreme Leader also has a chance to pin the negative aspects of the deal on a lame duck president while benefiting from it economically as he prepares for his all-important succession. The problem is that extreme levels of distrust will require some brinkmanship early in Biden’s term. Iran is building up leverage ahead of negotiations, which will mean higher levels of uranium enrichment and demonstrating the range of its regional capabilities, including the Strait of Hormuz, and its ability to impose economic pain via oil prices. Biden will need to establish a credible threat if Iran misbehaves. Hence the geopolitical setting is positive for oil prices at the moment. Beyond Iran, there is a clear basis for policy uncertainty to decline for Europe and the UK while it remains elevated for China and Russia (Chart 11). Chart 11Relative Policy Uncertainty Favors Europe and UK Over Russia And China

Relative Policy Uncertainty Favors Europe and UK Over Russia And China

Relative Policy Uncertainty Favors Europe and UK Over Russia And China

The US international image has suffered from the Trump era and the Biden administration’s main priorities will lie in solidifying alliances and partnerships and stabilizing the US role in the world, rather than pursuing showdown and confrontation. However, it will not be long before scrutiny returns to the authoritarian states, which have been able to focus on domestic recovery and expanding their spheres of influence amid the US’s tumultuous election year. Chart 12GeoRisk Indicators Say Risks Underrated For These Bourses

GeoRisk Indicators Say Risks Underrated For These Bourses

GeoRisk Indicators Say Risks Underrated For These Bourses

The US will not seek a “diplomatic reset” with Russia, aside from renegotiating the New START treaty. The Democrats will seek to retaliate for Russia’s extensive cyberattack in 2021 as well as for election interference and psychological warfare in the United States. And while there probably will be a reset with China, it will be short-lived, as outlined above. This situation contrasts with that of the Atlantic sphere. The Biden administration is a crystal clear positive, relative to a second Trump term, for the European Union. The EU and the UK have just agreed to a trade deal, as expected, to conclude the Brexit process, which means that the US-UK “special relationship” will not be marred by disagreements over Ireland. European solidarity has also strengthened as a result of the pandemic, which highlighted the need for collective policy responses, including fiscal. Thus the geopolitical risks of the new administration are most relevant for China/Taiwan and Russia. Comparing our GeoRisk Indicators, which are market-based, with the relative equity performance of these bourses, Taiwanese stocks are the most vulnerable because markets are increasingly pricing the geopolitical risk yet the relative stock performance is toppy (Chart 12). The limited recovery in Russian equities is also at risk for the same reason. Only in China’s case has the market priced lower geopolitical risk, not least because of the positive change in US administration. We expect Biden and Xi Jinping to be friendly at first but for strategic distrust to reemerge by the second half of the year. This will be a rude awakening for Chinese stocks – or China-exposed US stocks, especially in the tech sector. Investment Takeaways Chart 13Global Policy Shifts Drive Big Investment Reversals

Global Policy Shifts Drive Big Investment Reversals

Global Policy Shifts Drive Big Investment Reversals

The US is politically divided. Civil unrest and aftershocks of the controversial election will persist but markets will ignore it unless it has a systemic impact. The policy consequence is a more proactive fiscal policy, resulting in virtual fiscal-monetary coordination that is positive both for global demand and risk assets, while negative for the US dollar. The Biden administration will succeed in partially repealing the Trump tax cuts, but the impact on corporate profit margins will be discounted fairly mechanically and quickly by market participants, while the impact on economic growth will be more than offset by huge new spending. Sentiment will improve after the pandemic – and Biden has not yet shown an inclination to take an anti-business tone. The past decade has been marked by a dollar bull market and the outperformance of developed markets over emerging markets and growth stocks like technology over value stocks like financials. Cyclical sectors have traded in a range. Going forward, a secular rise in geopolitical Great Power competition is likely to persist but the macro backdrop has shifted with the decline of the dollar. Cyclical sectors are now poised to outperform while a bottom is forming in value stocks and emerging markets (Chart 13). We recommend investors go strategically long emerging markets relative to developed. We are also going long global value over growth stocks. We are not yet ready to close our gold trade given that the two supports, populist fiscal turn and great power struggle, will continue to be priced by markets in the near term. We are throwing in the towel on our short CNY-USD trade after the latest upleg in the renminbi, though our view continues to be that geopolitical fundamentals will catch yuan investors by surprise when they reassert themselves. We also recommend preferring global equities to US equities, given the above-mentioned global trends plus looming tax hikes. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 January 6, 2020, twitter.com. 2 See Turchin and Andrey Korotayev, "The 2010 Structural-Demographic Forecast for the 2010-2020 Decade: A Retrospective Assessment," PLoS ONE 15:8 (2020), journals.plos.org. 3 Not to mention that 2021 is the Communist Party’s 100th anniversary – not a time to make an unforced policy error with an already wobbly economy.

According to BCA Research’s new US Political Strategy service, investors should go long risk assets and reflation plays on a 12-month basis. We recommend value over growth stocks, materials over tech, TIPS over nominal treasuries, infrastructure plays, and…

The December ISM Services Index points to an acceleration in the US service sector’s recovery, with the headline index rising 1.3 percentage points to 57.2 and beating expectations of 54.5. The headline index was supported by an acceleration in Business…

The Democrats look set to take control of the US senate by the slimmest margin possible. The odds of more reflationary policies have increased, even if corporate taxes are set to rise as well. The increase in taxes is a problem for Wall Street but is…