The dollar is breaking down, as capital leaves the US. The important question investors must answer is how much downside is left for the greenback, and whether depreciation will continue in a straight line over the coming months or pause (and even stage a countertrend rally).Tactically, we will be buying the dollar. This is because our technical indicators are telling us that the dollar is much oversold and due for a countertrend bounce.Trade Idea #1: Buy The DXYThe greenback bottomed in 2008, at the depth of the financial crisis and has been in an uptrend since. For the DXY, that trend has been defined by the consistent pattern of higher lows and higher highs since the Great Financial Crisis (Chart 1).

Chart 1

The Dollar Is Approaching A Critical Resistance Level

The Dollar Is Approaching A Critical Resistance Level

Chart 2

The Dollar Is Oversold

The Dollar Is Oversold

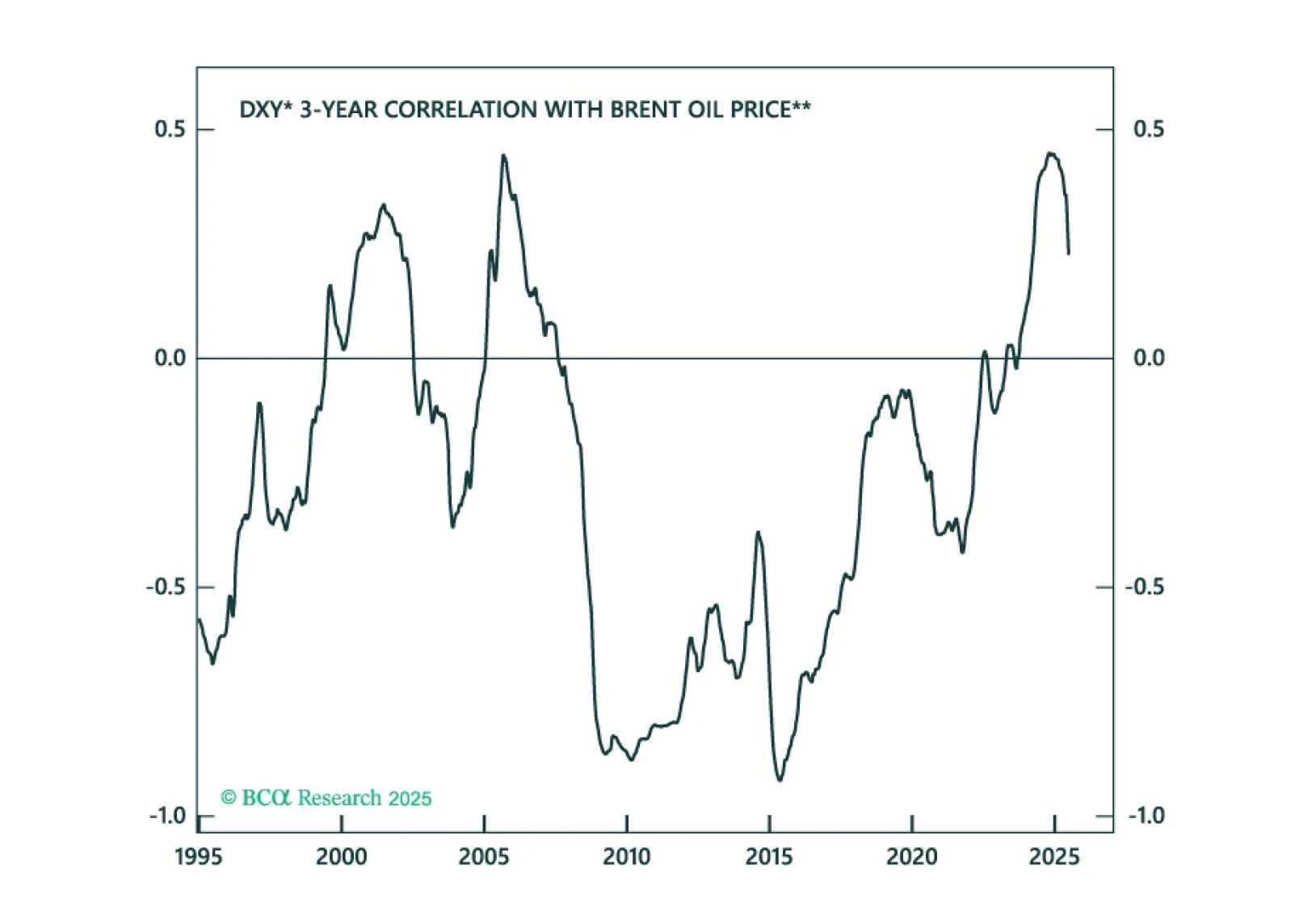

That bull market is now under threat. Year-to-date, the DXY has fallen by circa 10.4%. Given the greenback’s history of moving in very long cycles, the question most investors face today is: Is more weakness forthcoming, or is it time to become a contrarian?From purely technical lens, we will be buying the DXY on Independence Day for three key reasons. The DXY is approaching an important support level. This is defined by the upward sloping trendline, drawn from the 2008 lows, which currently pins support around 96. We will expect at least a tactical bounce at these levels as stale shorts fold their positions.Our comprehensive momentum and positioning indicator shows that the dollar is also very much oversold. Historically, this has led to countertrend bounces in the greenback (Chart 2). This measure is sitting at a standard deviation below the mean. When these levels have been hit in the past, a sharp reversal often ensued. It is remarkable that the higher-frequency momentum component almost hit two standard deviations below the mean.5%-10% rallies in DXY are common within the context of a long-term bear market. This will especially be the case if the world economy enters a recession. The dollar bear market from 2000 to 2008 saw many countertrend rallies, notably in 2005. Similarly, the bull market since 2008 has seen many pullbacks, some as deep as 10%. These have all been tactical trading opportunities.The key message is that the dollar might be going through a regime shift. This regime shift will be more focused on balance of payments, as the reserve status of the dollar is put under a microscope, amidst President Donald Trump’s policies. This is long-term bearish for the USD.That said, for now, the drawdown in the greenback is tactically approaching levels that have typically signaled a countertrend move. That will be around the 96 level for DXY. Trade Idea #2: Oil Producers Versus ConsumersThe dollar is the natural driver of all other FX market moves. This means that if a tactical bounce in the dollar occurs, as we expect, it will weigh on other G10 and EM currencies. The good news is that a few attractive trades exist at the crosses, that are not closely correlated to the overall dollar trend. The clearest one is buying a currency basket of oil producers, relative to oil consumers. There are three key reasons why this trade might prove fruitful:First, most oil producers tend to sport current account surpluses, while energy importers tend to be deficit countries. So naturally, in a world that is increasingly focused on balance of payments, you want to be long a basket of currencies from oil producing nations (Chart 3).Second, with the US being the largest oil producer in the world, the dollar has become a de facto petrocurrency. This means that rising oil prices benefit the US, as they do for Saudi Arabia, Canada, Norway, Nigeria, Angola or even Iran (Chart 4). So, a trading strategy of going long petrocurrencies versus the USD will not work out if one expects higher oil prices.

Chart 3

The US Dollar Is A Petro Currency

The US Dollar Is A Petro Currency

Chart 4

Buy A Select Basket Of Oil Producers

Buy A Select Basket Of Oil Producers

Finally, there is very little geopolitical risk premium in the current oil price of $68, which the Kansas Fed estimates as the marginal production cost for US producers. Bottom Line: The correlation between the dollar and oil prices has turned structurally positive (Chart 5). A bearish bet on oil will mean a lower dollar in this case. That said, if the dynamics driving markets are balance of payments, it pays to be long a basket of oil producing nations (that tend to have a current account surplus), versus oil consuming nations. This trade will also benefit from a rise in the geopolitical risk premium in oil prices.

Chart 5

Higher Oil Prices Will Lift The Dollar

Higher Oil Prices Will Lift The Dollar

Chart 6

Buy Precious Metals

Buy Precious Metals

Trade Idea #3: Buy Precious MetalsAlmost 90% of transactions globally are still conducted in US dollars. For all the talk about de-dollarization, that share has been rising over the last decade. What has been true this year is a clear willingness by foreign nationals to diversify away from this dependence on the dollar. That is true for petro nations such as Russia to geopolitical rivals to the US such as China.For developing nations, the clear choice has been to park their USDs into gold. In 2010, gold was about 10% of central bank reserves. Today, it has become the largest holding by central banks outside the US dollar and the euro.Given that the dollar tends to move in long cycles, the same is true for precious metals. As this diversification away from the dollar continues, gold will still benefit but cheaper precious metals will flare amidst the blaze. We already saw that with silver and platinum prices. The next candidate will be palladium (Chart 6). Chester NtoniforForeign Exchange/Global Fixed Income Strategistchestern@bcaresearch.comFollow me onLinkedIn & X