United States

Dear Client, The US Capitol is going on lockdown as we write to introduce BCA Research’s newest investment service, US Political Strategy, in this inaugural report. US Political Strategy will provide timely and actionable policy insights for US-dedicated, multi-asset investors. It grew naturally out of our successful Geopolitical Strategy service, which has become an industry leader in combining geopolitical and market analysis over the past decade. By client demand, we are expanding our policy team and deepening our coverage of policy-induced macro and market themes and trends. US Political Strategy will delve deep into domestic US politics: executive orders, Capitol Hill, regulatory risk, the Supreme Court, emerging socioeconomic trends, and their impacts on key US sectors and assets. Meanwhile, Geopolitical Strategy will redouble its focus on truly global and geopolitical risks and opportunities, including US foreign and trade policy but more especially China, Europe, and other major markets. Both strategies utilize our proprietary analytical framework, which relies on data-driven assessments of the “checks and balances” that shape policy outcomes. As with all our research, we are agnostic about political parties, transparent about our conviction levels and scenario probabilities, and solely focused on actionable investment advice. For more information please visit the US Political Strategy webpage. For a free trial please reach out to your BCA Research account manager or email contactbca@bcaresearch.com. We trust you will find this enhancement of coverage insightful and profitable. Happy New Year! All very best, Matt Gertken Vice President BCA Research The outgoing Trump administration is powerless to stop the presidential transition and the US military and security forces will not participate in any “coup.” Investors should buy the dip if social instability affects the markets between now and President-elect Joe Biden’s Inauguration Day. Democrats have achieved a sweep of US government with two victories in Georgia’s Senate election. The Biden administration is no longer destined for paralysis. Investors no longer need fear a premature tightening of US fiscal policy. Fiscal thrust will expand by around 6.9% of GDP more than it otherwise would have in FY2021 and contract by 12.3% of GDP in FY2022. Democrats will partly repeal the Trump tax cuts to pay for new spending programs, including an expansion and entrenchment of Obamacare. Big Tech is the most exposed to the combination of higher corporate taxes and inflation expectations. Investors should go long risk assets and reflation plays on a 12-month basis. We recommend value over growth stocks, materials over tech, TIPS over nominal treasuries, infrastructure plays, and municipal bonds. The special US Senate elections in Georgia produced a two-seat victory for Democrats on January 5 and have thus given the Democratic Party de facto control of the Senate.Financial markets have awaited this election with bated breath. The “reflation trade” – bets on economic recovery on the back of ultra-dovish monetary and fiscal policy – had taken a pause for the election. There was a slight setback in treasury yields and the outperformance of cyclical, small cap, and value stocks, which rallied sharply after the November 3 general election (Chart 1). The Democratic victory ensures that US corporate and individual taxes will go up – triggering a one-off drop in earnings per share of about 11%, according to our US Equity Strategist Anastasios Avgeriou (Table 1). But it also brings more proactive fiscal policy. Since the Democrats project larger new spending programs financed by tax hikes, the big takeaway is that the US economic recovery will gain momentum and will not be undermined by premature fiscal tightening. Chart 1Markets Will Look Through Unrest To Reflation

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Table 1What EPS Hit To Expect?

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 2Democrats Won Georgia Seats, US Senate

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Republicans Snatch Defeat From Jaws Of Victory The results of the Georgia runoffs, at the latest count, are shown in Chart 2. Republican Senator David Perdue has not yet officially lost the race, as votes are still being tallied, but he trails his Democratic challenger Jon Ossoff by 16,370 votes. This is a gap that is unlikely to be changed by subsequent vote disputes or recounts (though it is possible and the results are not yet declared as we go to press). President-elect Joe Biden only lost 1,274 votes to President Trump when ballots were recounted by hand in November. The Democratic victory offers some slight consolation for opinion pollsters who underestimated Republicans in the general election in certain states. Opinion polls had shown a dead heat in both of Georgia’s races, with Republican Senators Perdue and Kelly Loeffler deviating by 1.4% and 0.4% respectively from their support rate in the average of polls in December. Democratic challengers Jon Ossoff and Raphael Warnock differed by 1.3% and 2.3% from their final polling (Charts 3A & 3B). Chart 3AOpinion Pollsters Did Better …

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 3B… In Georgia Runoffs

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

By comparison, in the November 3 general election, polls underestimated Perdue by 1.3% and overestimated Warnock by 5.3% (Chart 4). On the whole, the election shows that state-level opinion polling can improve to address new challenges. Our quantitative Senate election model had given Republicans a 78% chance of winning Georgia. This they did in the first round of the election, but conditions have changed since November 3, namely due to President Trump’s refusal to concede the election after the Electoral College voted on December 14.1 Our model is based on structural factors so it did not distinguish between the two Senate candidates in the same state. For the whole election, the model predicted that Democrats would win a net of three seats, resulting in a Republican majority of 51-49. Today we see that the model only missed two states: Maine and Georgia. But Georgia has made all the difference, with the result to be 50-50, for Vice President Kamala Harris to break the tie (Chart 5). Chart 4Ossoff In Line With Polls, Warnock Slightly Beat

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 5Our Quant Model Missed Maine And Georgia – And Georgia Carries Two Seats To Turn The Senate

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

COVID-19 likely took a further toll on Republican support in the interim between the two election rounds. The third wave of the COVID-19 pandemic has not peaked in the US or the Peach State. While the number of cases has spiked in Georgia as elsewhere, the number of deaths has not yet followed (Chart 6). Chart 6COVID-19 Surged Since November

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Lame Duck Trump Risk Before proceeding to the policy impacts of the apparent Democratic sweep of both executive and legislative branches, a word must be said about the presidential transition and President Trump’s final 14 days in office. First, the Joint Session of Congress to count the Electoral College ballots to certify the election of the new US president has been interrupted as we go to press. There is zero chance that protesters storming the proceedings will change the outcome of the election. The counting of the electoral votes can be interrupted for debate; it will be reconvened. Disputes over the vote could theoretically become meaningful if Republicans controlled both the House and the Senate, as the combined voice of the legislature could challenge the legitimacy of a state’s electoral votes. But today the Republicans only control the Senate, and while some will press isolated challenges, based on legal disputes of variable merit, these challenges will not gain traction in the Senate let alone in the Democratic-controlled House. What did the US learn from this controversial election? US political polarization is reaching extreme peaks which are putting strain on the formal political system, but Trump lacks the strength in key government bodies to overturn the election. Second, there was no willingness of state legislatures to challenge their state executives on the vote results. This has to do with the evidence upon which challenges could be lodged, but there is also a built-in constraint. Any state legislature whose ruling party opposes the popular result will by definition put its own popular support in jeopardy in the next election. Third, the Supreme Court largely washed its hands of state-level disputes settled by state-level courts. Historically, the Supreme Court never played a role in presidential elections. The year 2000 was an exception, as the high court said at the time. The 2020 election has established a high bar for any future Supreme Court involvement, though someday it will likely be called on to weigh in. Hysteria regarding the conservative leaning on the court – which is now a three-seat gap – was misplaced. The three Supreme Court justices appointed by Trump took no partisan or interventionist role. Nevertheless, the court’s conservative leaning will be one of the Trump administration’s biggest legacies. The marginal judge in controversial cases is now more conservative and will take a larger role given that Democrats now have a greater ability to pass legislation by taking the Senate. President Trump is still in office for 14 days. There is zero chance of a successful military coup or anything of the sort in a republic in which institutions are strong and the military swears allegiance to the constitution. Attempts to oppose the Electoral College and Congress will be opposed – and ultimately they will be met with an overwhelming reassertion of the rule of law. All ten of the surviving secretaries of defense of the United States have signed an open letter saying that the election results should no longer be resisted and that any defense officials who try to involve the military in settling electoral disputes could be criminally liable.2 With Trump’s options for contesting the election foreclosed, he will turn to signing a flurry of executive orders to cement his legacy. His primary legacy is the US confrontation with China, so he will continue to impose sanctions on China on the way out, posing a tactical risk to equity prices. The business community will be slow to comply, however, so the next administration will set China policy. There is a small possibility that Trump will order economic or even military action against Iran or any other state that provokes the United States. But Trump is opposed to foreign wars and the bureaucracy would obstruct any major actions that do not conform with national interests. Basically, Trump’s final 14 days may pose a downside risk to equities that have rallied sharply since the November 9 vaccine announcement but we are long equities and reflation plays. Sweeps Just As Good For Stocks As Gridlock The balance of power in Congress is shown in Chart 7. The majorities are extremely thin, which means that although Democrats now have control, there will remain high uncertainty over the passage of legislation, at least until the 2022 midterm elections. Investors can now draw three solid conclusions about the makeup of US government from the 2020 election: The White House’s political capital has substantially improved – President-elect Joe Biden no longer faces a divided Congress. He won by a 4.5% popular margin (51.4% of the total), bringing the popular and electoral vote back into alignment. He will have a higher net approval rating than Trump in general, and household sentiment, business sentiment, and economic conditions will improve from depressed, pandemic-stricken levels over the course of his term. The Senate is evenly split but Democrats will pass some major legislation – Thin margins in the Senate make it hard to pass legislation in general. However, the budget reconciliation process enables laws to pass with a simple majority if they involve fiscal matters. Hence, Democrats will be able to legislate additional COVID relief and social support that they were not able to pass in the end-of-year budget bill. They can pass a reconciliation bill for fiscal 2022 as well. They will focus on economic recovery followed by expanding and entrenching the Affordable Care Act (Obamacare). We fully expect a partial repeal of Trump’s Tax Cut and Jobs Act, if not initially then later in the year. Democrats only have a five-seat majority in the House of Representatives – Democrats will vote with their party and thus 222 seats is enough to maintain a working majority. But the most radical parts of the agenda, such as the Green New Deal, will be hard to pass. Chart 7Democrats Control Both Houses

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

With the thinnest possible margin, the Senate has a highly unreliable balance of power. Table 2 shows top three Republicans and Democrats in terms of age, centrist ideology, and independent mentality. Four senators are above the age of 85 – they can vote freely and could also retire or pass away. Centrist and maverick senators will carry enormous weight as they will provide the decisive votes. The obvious example is Senator Joe Manchin of West Virginia, who has opposed the far-left wing of his party on critical issues such as the Green New Deal, defunding the police, and the filibuster. Table 2The Senate Will Hinge On These Senators

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

The Democrats could conceivably muster the 51 votes to eliminate the filibuster, which requires a 60-vote majority to pass most legislation, but it will be very difficult. Senators Dianne Feinstein (D, CA), Angus King (I, ME), Kyrsten Sinema (D, AZ), Jon Tester (D, MT), and Manchin are all skeptical of revoking this critical hurdle to Senate legislation.3 We would not rule it out, however. The US has reached a point of “peak polarization” in which surprises should be expected. By the same token, Republican Senators Lisa Murkowski and Susan Collins often vote against their party. Collins just won yet another tough race in Maine due to her ability to bridge the partisan gap. There are also mavericks like Rand Paul – and Ted Cruz will have to rethink his populist strategy given his thin margins of victory and the Trump-induced Republican defeat in the South. Not shown are other moderates who will be eager to cross the political aisle, such as Senator Mitt Romney of Utah. None of the above means Democrats will fail to raise taxes. All Democrats voted against Trump’s Tax Cut and Jobs Act, which did not end up being popular or politically beneficial for the Republicans. The Democratic base is fired up and mobilized by Trump to pursue its core agenda of increasing the government role in US society and the economy and redressing various imbalances and disparities. This requires revenue, especially if it is to be done with only 51 votes via the budget reconciliation process. The two Democratic senators from Arizona are vulnerable, but they will toe the party line because Trump and the GOP were out of step with the median voter. Moreover, Arizonians voted for higher taxes in a state ballot measure in November. Since 1980, gridlocked government has resulted in higher average annual returns on the S&P500. But since 1949, single-party sweeps have slightly edged out gridlocked governments in stock returns, though the results are about the same (Chart 8). The point is that gridlock makes it hard for government to get big things done. Sometimes that is positive for markets, sometimes not. The macro backdrop is what matters. The Federal Reserve is unlikely to start tightening until late 2022 at earliest and fiscal thrust in 2021-22 will be more expansionary now that the Democrats have control of the Senate. This policy backdrop is negative for the dollar and positive for risk assets, especially equity sectors that will suffer least from impending corporate tax hikes, such as energy, industrials, consumer staples, materials, and financials. Chart 8Sweeps Don’t Always Underperform Gridlock

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Meanwhile, Biden will have far less trouble getting his cabinet and judicial appointments through the Senate (Appendix). His appointees so far reflect his desire to return the US to “rule by experts,” as opposed to Trump’s disruptive style of personal rule. Investors will cheer the return to technocrats and predictable policymaking even if they later relearn that experts make gigantic mistakes too. Fiscal Policy Outlook The critical feature of the Trump administration was the COVID-19 pandemic, which sent the US budget deficit soaring to World War II levels relative to GDP. In the coming years, the change in the budget deficit (fiscal thrust) will necessarily be negative, dragging on growth rates (Chart 9). Fiscal policy determines how heavy and abrupt that drag will be. Chart 9US Budget Deficit Surged – Pace Of Normalization Matters

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 10 presents four scenarios that we adjusted based on data from the Congressional Budget Office. The baseline would see an extraordinary 6.7% of GDP contraction in the budget deficit that would kill the recovery, which the Georgia outcome has now rendered irrelevant. The “Republican Status Quo” scenario is now the minimum. Chart 10Democratic Sweep Suggests Big Fiscal Thrust In FY2021 And Less Contraction FY2022

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

The “Democratic Status Quo” scenario assumes that the $600 per household rebate will be increased to $2,000 per family and that the remaining $2.5 trillion of the Democrats’ proposed HEROES Act will be enacted. The “Democratic High” scenario adds Biden’s $5.6 trillion policy agenda on top of the Democratic status quo, supercharging the economic recovery with a fiscal bonanza. Biden will not achieve all of this, so the reality will lie somewhere between the solid blue and dotted blue lines. This Democratic status quo implies a 6.9% of GDP expansion of the deficit in FY2021. It also implies that the deficit will contract by 12.3% of GDP in FY2022, instead of 13.5% in the Republican status quo scenario. The economic recovery will be better supported. So, too, will the Fed’s timeline for rate hikes – but the Fed’s new strategy of average inflation targeting shows that it is targeting an inflation overshoot. So the threat of Fed liftoff is not immediate. The longer the extraordinary fiscal largesse is maintained, the greater the impact on inflation expectations and the more upward pressure on bond yields (Chart 11). Big Tech will be the one to suffer while Big Banks, industrials, materials, and energy will benefit. Chart 11Bond Bearish Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Our US Political Risk Matrix There is no correlation between fiscal thrust and equity returns. This is true whether we consider the broad market, cyclicals/defensives, value/growth stocks, or small/large caps (Chart 12). Normally, fiscal thrust surges when recessions and bear markets occur, leading to volatility in asset prices. However, in the new monetary policy context, the risk is to the upside for the above-mentioned sectors, styles, and segments. Looking at sector performance before and after the November 3 election and November 9 vaccine announcement, there has been a clear shift from pandemic losers to pandemic winners. Big Tech and Consumer Discretionary (Amazon) thrived during the period before the vaccine, while value stocks (industrials, energy, financials) suffered the most from the lockdowns. These trends have reversed, with energy and financials outperforming the market since November (Chart 13). The Biden administration poses regulatory risks for Big Oil and arguably Big Banks, but these will come into play after the market has priced in economic normalization and the emerging consensus in favor of monetary-fiscal policy coordination, which is very positive for these sectors. Chart 12Fiscal Thrust Not Correlated With Stocks

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 13Energy And Financials Turned Around With Vaccine

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

In the case of energy, as stated above, the Biden administration will still struggle to get anything resembling the Green New Deal approved in Congress. Nevertheless, environmental regulation will expand and piecemeal measures to promote research and development, renewables, electric vehicles, and other green initiatives may pass. Large cap energy firms are capable of adjusting to this kind of transition. Coal companies are obviously losers. In the case of financials, Biden’s record is not unfriendly to the financial industry. His nominee for Treasury Secretary, former Fed Chair Janet Yellen, approved of the relaxation of some of its more stringent financial regulations under the Trump administration. Big Banks are no longer the target of popular animus like they were after the 2008 financial crisis – in that regard they have given way to Big Tech. Our US Investment Strategist Doug Peta argues that the Democratic sweep will smother any gathering momentum in personal loan defaults, which would help banks outperform the broad market. Biden’s regulatory approach to Big Tech will be measured, as the Obama administration’s alliance with Silicon Valley persists, but tech stands to suffer the most from higher taxes, especially a minimum corporate tax rate. With a unified Congress, it is also now possible that new legislation could expand tech regulation. There is a bipartisan consensus emerging on tech regulation so Republican votes can be garnered. Tech thrives on growth-scarce, disinflationary environments whereas the latest developments are positive for inflation expectations. In the recent lead-up to the Georgia vote, industrials, financials, and consumer discretionary stocks have not benefited much, even though they should (Chart 14). These are investment opportunities. Chart 14Upside For Energy And Financials Despite Regulatory Risk

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

In our Political Risk Matrix, we establish these views as our baseline political tilts, to be applied to the BCA Research House View of our US Equity Strategy. The results are shown in Table 3. When equity sectors become technically stretched, the political impacts will become more salient. Table 3US Political Risk Matrix

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Investment Takeaways Over the past few years our sister Geopolitical Strategy has written extensively about “Civil War Lite,” “Peak Polarization,” and contested elections in the United States. We will dive deeper into these themes and issues in forthcoming reports, but for now suffice it to say that extremist events will galvanize the majority of the nation behind the new administration while also driving politicians of both stripes to use pork-barrel spending to try to stabilize the country. Congress will err on the side of providing too much fiscal stimulus just as surely as the Fed is bent on erring on the side of providing too much monetary stimulus. That means reflation, which will ultimately boost stocks in 2021. We also expect stocks to outperform government bonds, at least on a tactical 3-6 month timeframe. As the above makes clear, we prefer value stocks over growth stocks. Specifically we favor cyclical plays like materials over the big five of Google, Apple, Amazon, Microsoft, and Facebook. An infrastructure bill was one of the few legislative options for the Biden administration under gridlock, now it is even more likely. Infrastructure is popular and both presidential candidates competed to see who could offer the bigger plan. Moreover, what Biden cannot achieve under the rubric of climate policy he can try to achieve under the rubric of infrastructure. The BCA US Infrastructure Basket correlates with the US budget deficit as well as growth in China/EM and we recommend investors pursue similar plays. In the fixed income space, Treasury inflation protected securities (TIPS) are likely to continue outperforming nominal, duration-matched government bonds. Our US Bond Strategist Ryan Swift is on alert to downgrade this recommendation, but the change in US government configuration at least motivates a tactical overweight in TIPS. The chances of US state and local governments receiving fiscal support – previously denied by the GOP Senate – has increased so we will also go long municipal bonds relative to treasuries. Matt Gertken Vice President US Political Strategy mattg@bcaresearch.com Appendix Table A1Biden’s Cabinet Position Appointments

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Footnotes 1 Perdue defeated Ossoff on November 3 but fell short of the 50% threshold to avoid a second round; meanwhile the cumulative Republican vote in the multi-candidate special election outnumbered the cumulative Democratic vote on November 3. 2 Ashton Carter, Dick Cheney, William Cohen, et al, “All 10 living former defense secretaries: Involving the military in election disputes would cross into dangerous territory,” Washington Post, January 3, 2021, washingtonpost.com. 3 Jordain Carney, “Filibuster fight looms if Democrats retake Senate,” The Hill, August 25, 2020, thehill.com.

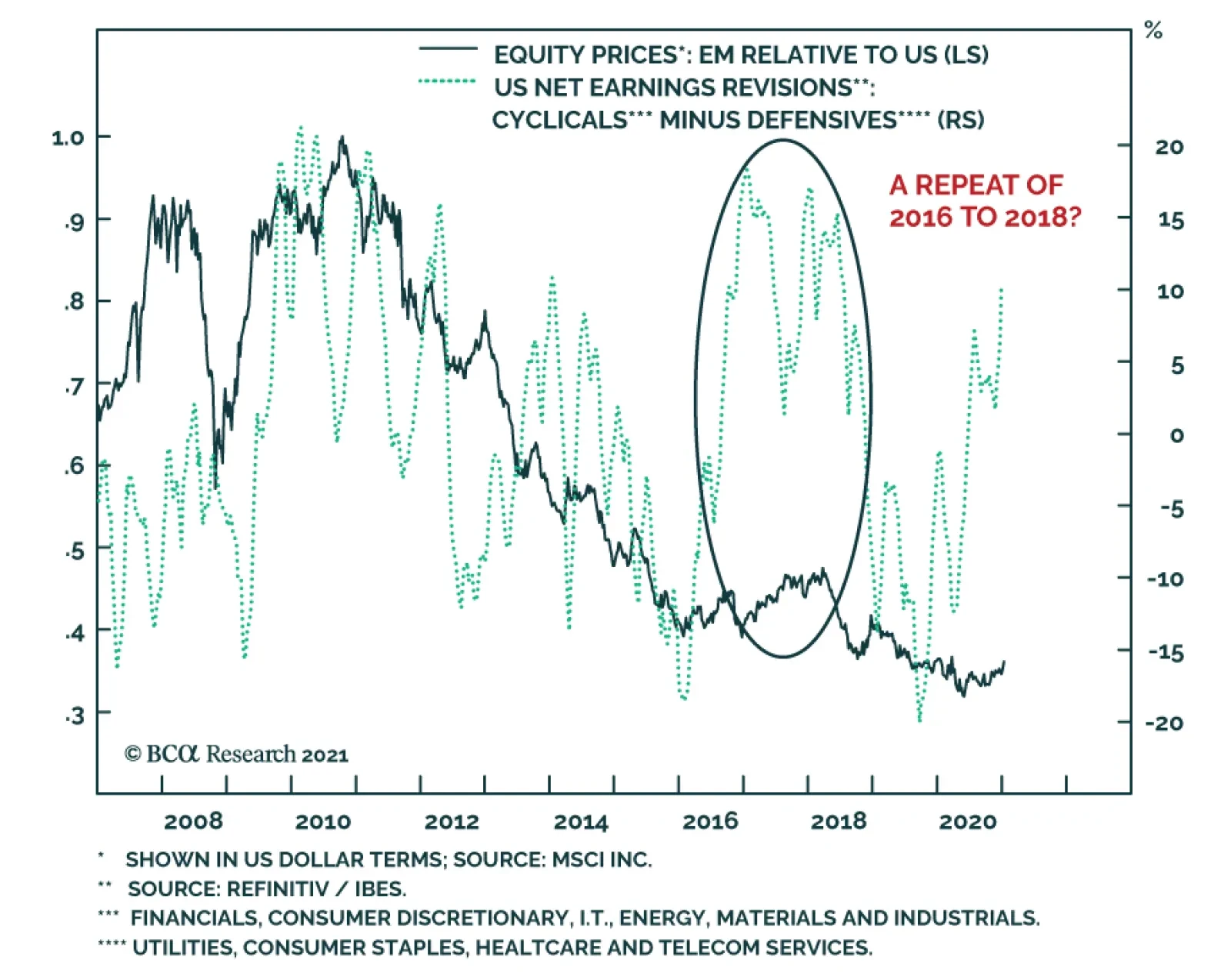

The reality that the market rally will become more volatile (see Indicator Spotlight) does not preclude a meaningful outperformance of EM equities relative to the US. In fact, BCA Research expects EM equities to perform in line with the EAFE benchmark and…

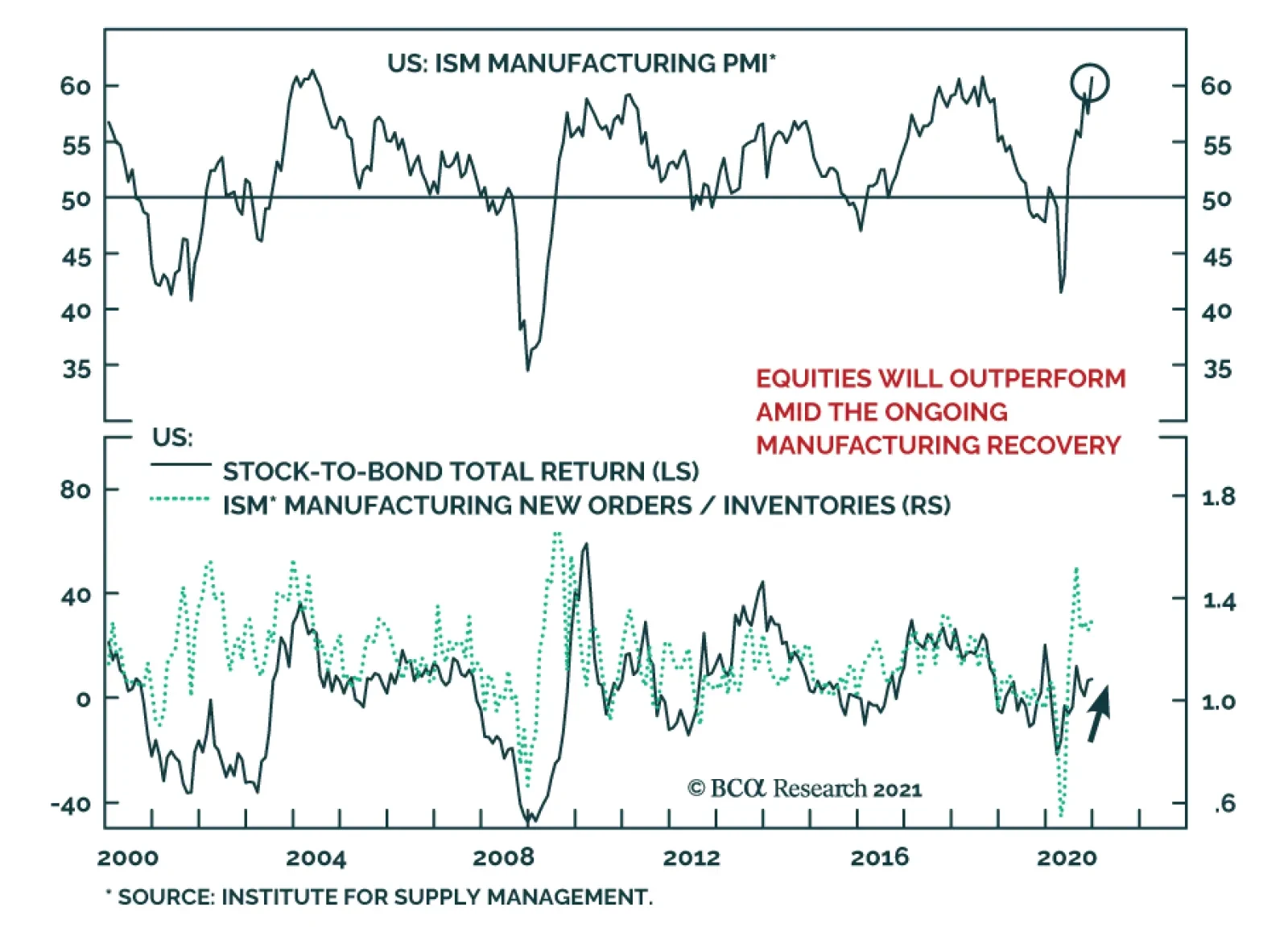

The December ISM Manufacturing PMI rose to 60.7 from 57.5 versus expectations of a decline to 56.8, corroborating evidence that the economy has grown somewhat desensitized from pandemic developments. This is consistent with the message from Monday’s strong US…

Highlights Chart 12020 Returns

2020 Returns

2020 Returns

After a tumultuous start to the year, corporate bonds rallied in 2020 H2, managing to eke out small annual gains versus Treasuries. Specifically, investment grade corporates outperformed duration-equivalent Treasuries by 4 basis points in 2020 and high-yield outperformed by 185 bps (Chart 1). Treasuries, for their part, bested cash by 7% on the year but returns have been trending down since August. As we look forward to 2021, the economic cycle is in what we call a sweet spot for spread product returns. Economic growth is above trend, but inflation is low and monetary conditions are highly accommodative. This macro back-drop will lead to positive spread product returns versus Treasuries and a moderate bear-steepening of the Treasury curve in 2021. However, stretched valuations for investment grade corporates mean that investors must be selective within spread product. We think the Ba credit tier offers the best risk-adjusted opportunity in the corporate bond space, and also recommend favoring tax-exempt municipal bonds over equivalent-quality investment grade corporates. Feature Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-matched Treasury index by 79 basis points in December and by 4 bps in 2020. The investment grade corporate index eked out a small gain relative to the duration-matched Treasury index in 2020. Corporates underperformed Treasuries by 18% from the beginning of the year until March 23, the day that the Fed stopped the bleeding in credit markets by unveiling its suite of emergency lending facilities. With the Fed’s backstops in place, the corporate index went on to outperform Treasuries by 22% between March 23 and the end of the year (Appendix A). As we noted in our 2021 Key Views Special Report, the corporate bond index option-adjusted spread is not quite back to its pre-COVID low.1 However, valuation is close to all-time expensive after adjusting for changes in the index’s average credit rating and duration. The 12-month breakeven spread for the Bloomberg Barclays Corporate Index (adjusted to keep the average credit rating constant) has only been tighter 4% of the time since 1995 (Chart 2). The same figure for the Baa-rated credit tier is 5%. As noted, the macro environment of above-trend growth and accommodative Fed policy is very positive for spread product returns. However, better value exists outside of the investment grade corporate space. In particular, we advise investors to look at Ba-rated high-yield corporates and tax-exempt municipal bonds. High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 190 basis points in December and by 185 basis points in 2020. Ba-rated junk bonds outperformed duration-matched Treasuries by 431 bps in 2020, while B-rated and Caa-rated bonds lagged by 13 bps and 238 bps, respectively. Since the March 23 peak in spreads, Ba-rated bonds outperformed Treasuries by 33%, B-rated bonds outperformed by 30% and Caa-rated bonds outperformed by 36% (Appendix A). We view Ba-rated junk bonds as the sweet spot within the corporate credit space. The sector is relatively insulated from default risk and yet still offers a sizeable spread pick-up over investment grade corporates (Chart 3). We noted in our 2021 Key Views Special Report that the additional spread earned from moving down in quality below Ba is in line with historical averages.2 Assuming a 25% recovery rate on defaulted debt and a minimum required risk premium of 150 bps, we calculate that the junk index is priced for a default rate of 2.8% for the next 12 months (panel 3). This represents a steep drop from the 8.4% default rate observed during the most recent 12-month period. However, only seven defaults occurred in November, down from a peak of 22 in July. Job cut announcements, an excellent indicator of the default rate, are also falling rapidly (bottom panel). Overall, we see room for spread compression across all junk credit tiers in 2021 but believe that Ba-rated bonds offer the best opportunity in risk-adjusted terms. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Cyclical Sweet Spot

The Cyclical Sweet Spot

Table 3BCorporate Sector Risk Vs. Reward*

The Cyclical Sweet Spot

The Cyclical Sweet Spot

MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 22 basis points in December but underperformed by 17 bps in 2020. The conventional 30-year MBS index option-adjusted spread (OAS) tightened 10 bps on the month to reach 61 bps (Chart 4). This is higher than the 58 bps offered by Aa-rated corporate bonds, the 49 bps offered by Agency CMBS and the 24 bps offered by Aaa-rated consumer ABS. Despite the relatively attractive OAS, we continue to view the elevated primary mortgage spread as a material risk for MBS investors. The elevated spread suggests that mortgage rates need not rise alongside Treasury yields in the near-term, meaning that mortgage refinancings can continue at their current rapid pace (panel 3). Our view is that expected prepayment losses embedded in MBS spreads (aka the option cost) are too low relative to this pace of refinancing. Last year’s spike in the mortgage delinquency rate was driven by households that were granted forbearance by the federal government’s CARES act (panel 4). The risk for MBS holders is that these households will not be able to resume their regular mortgage payments when the forbearance period ends this spring. While the situation bears close monitoring, our sense is that excess savings built up during the past nine months will be sufficient to prevent a surge of bankruptcies when the forbearance period ends. The recent stimulus package provides households with even more assistance. Government-Related: Underweight Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 62 basis points in December but underperformed by 161 bps in 2020. Sovereign debt outperformed duration-equivalent Treasuries by 176 bps in December but underperformed by 98 bps in 2020. Foreign Agencies outperformed the Treasury benchmark by 7 bps in December but underperformed by 640 bps in 2020. Local Authority debt outperformed Treasuries by 146 bps in December but underperformed by 86 bps in 2020. Domestic Agency bonds outperformed by 14 bps in December but underperformed by 9 bps in 2020. Supranationals outperformed by 2 bps in December and by 3 bps in 2020. US dollar weakness is usually a boon for Emerging Market (EM) Sovereign and Foreign Agency returns. However, 2020’s dollar weakness was mostly relative to other Developed Market currencies (Chart 5). Value has improved somewhat for EM Sovereigns during the past few weeks, but the index continues to offer less spread than the Baa-rated US Credit index (panel 4). At the country level, Turkey, Colombia, Mexico, Russia, South Africa and Indonesia are the only countries that offer a spread pick-up relative to duration and quality-matched US corporates. Of those, only Mexico looks attractive on a risk/reward basis. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds outperformed the duration-equivalent Treasury index by 56 basis points in December but underperformed by 286 bps in 2020 (before adjusting for the tax advantage). We upgraded municipal bonds to “maximum overweight” in our recent 2021 Key Views Special Report.3 Attractive valuations are the main reason for this move. First, spreads between Aaa-rated municipal bonds and equivalent-maturity Treasuries are elevated compared to history across the entire yield curve (Chart 6). Second, municipal bonds look even more attractive relative to duration and quality-matched credit. The Bloomberg Barclays Revenue Bond index offers a greater yield than the quality-matched Credit index across the entire maturity spectrum (before adjusting for the tax advantage). The same is true for the Bloomberg Barclays General Obligation index beyond the 12-year maturity point (panel 3). While the failure to include state & local government aid in the recent relief bill is a big blow to municipal budgets that are already stretched, we think municipal bond spreads offer more-than-adequate compensation for default/downgrade risk. State & local governments are already engaging in austerity measures that will help protect bondholders (bottom panel) and State Rainy Day Fund balances were at all-time highs heading into the COVID downturn. Both of these things should help stave off a wave of municipal downgrades. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve bear-steepened in December. The 2/10 Treasury slope steepened 13 bps to 81 bps. The 5/30 Treasury slope steepened 7 bps to 129 bps. Our expectation is that continued economic recovery will cause investors to price-in eventual monetary tightening at the long-end of the Treasury curve. With the Fed maintaining a firm grip on the front end, this will lead to Treasury curve bear steepening. A timely vaccine roll-out and the recently passed fiscal relief bill will serve to speed this process along. We recommend positioning for a steeper curve by owning the 5-year Treasury note and shorting a duration-matched barbell consisting of the 2-year and 10-year notes. This position is designed to profit from 2/10 curve steepening. Valuation is a concern with our recommended steepener, as the 5-year yield is below the yield on the duration-matched 2/10 barbell (Chart 7). However, the 5-year looked much more expensive during the last zero-lower-bound period between 2010 and 2013 (bottom 2 panels). We anticipate a return to similar levels. TIPS: Overweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 141 basis points in December and by 117 bps in 2020. The 10-year and 5-year/5-year forward TIPS breakeven inflation rates rose 22 bps and 18 bps on the month. They currently sit at 2.01% and 2.07%, respectively. Core CPI rose 0.22% in November, pushing the year-over-year rate from 1.63% to 1.65%. Meanwhile, 12-month trimmed mean CPI fell from 2.22% to 2.09%, narrowing the gap between trimmed mean and core (Chart 8). We anticipate further narrowing in 2021 Q1 and therefore expect core CPI to print relatively hot. For this reason, we recommend maintaining an overweight allocation to TIPS versus nominal Treasuries for the time being, even though the 10-year TIPS breakeven inflation rate looks somewhat elevated on our Adaptive Expectations Model (panel 2).4 Inflation pressures may moderate once the core and trimmed mean inflation measures converge, and this could give us an opportunity to tactically reduce TIPS exposure in the first half of this year. We also recommend holding real yield curve steepeners and inflation curve flatteners. With the Fed now officially targeting an overshoot of its 2% inflation goal, we expect the cost of 2-year inflation protection to rise above the cost of 10-year inflation protection (panel 4). With the Fed also exerting more control over short-dated nominal yields than over long-term ones, we expect short-maturity real yields to come under downward pressure relative to the long end (bottom panel). ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 15 basis points in December and by 98 bps in 2020. Aaa-rated ABS outperformed the Treasury benchmark by 12 bps in December and by 81 bps in 2020. Non-Aaa ABS outperformed by 33 bps in December and by 207 bps in 2020 (Chart 9). On paper, the Treasury department’s decision to let the Term Asset-Backed Loan Facility (TALF) expire at the end of 2020 is quite negative for ABS. However, as we explained in a recent report, we don’t anticipate a material impact on spreads.5 For one thing, Aaa ABS spreads are already well below the borrowing cost offered by TALF. But more importantly, consumer credit quality is strong. As we first explained last June, the stimulus received from the CARES act led to a significant increase in disposable income and a jump in the savings rate (panel 4).6 Faced with an income boost and few spending opportunities, many households paid down consumer debt. Given the recently passed additional fiscal support and the substantial savings that have already accrued, we see household balance sheets as being in a good place. As such, we advise moving down-in-quality to pick up extra spread in non-Aaa ABS. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 113 basis points in December but underperformed by 57 bps in 2020. Aaa Non-Agency CMBS outperformed Treasuries by 58 bps in December and by 56 bps in 2020. Non-Aaa Non-Agency CMBS outperformed Treasuries by 277 bps in December but underperformed by 360 bps in 2020 (Chart 10). We continue to recommend an overweight allocation to Aaa-rated Non-Agency CMBS and an underweight allocation to non-Aaa CMBS. Even with the expiry of TALF, Aaa CMBS spreads are already well below the cost of borrowing through TALF and thus will not be negatively impacted.7 Meanwhile, the structurally challenging environment for commercial real estate could lead to problems for lower-rated CMBS (panels 3 & 4). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 50 basis points in December and by 105 bps in 2020. The average index spread tightened 7 bps in December to reach 49 bps (bottom panel). At its September meeting, the Fed decided to slow its pace of Agency CMBS purchases. It is no longer looking to increase its Agency CMBS holdings, but rather, will only purchase what is “needed to sustain smooth market functioning”. This is nonetheless a backstop of the market, and it does not change our overweight recommendation. Appendix A: Buy What The Fed Is Buying The Fed rolled out a number of aggressive lending facilities on March 23. These facilities focused on different specific sectors of the US bond market. The fact that the Fed has decided to support some parts of the market and not others has caused some traditional bond market correlations to break down. It has also led us to adopt of a strategy of “Buy What The Fed Is Buying”. That is, we favor those sectors that offer attractive spreads and that benefit from Fed support. The below Table tracks the performance of different bond sectors since the March 23 announcement. We will use this to monitor bond market correlations and evaluate our strategy’s success. TablePerformance Since March 23 Announcement Of Emergency Fed Facilities

The Cyclical Sweet Spot

The Cyclical Sweet Spot

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of December 31ST, 2020)

The Cyclical Sweet Spot

The Cyclical Sweet Spot

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of December 31ST, 2020)

The Cyclical Sweet Spot

The Cyclical Sweet Spot

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 85 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 85 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Cyclical Sweet Spot

The Cyclical Sweet Spot

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of December 31ST, 2020)

The Cyclical Sweet Spot

The Cyclical Sweet Spot

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Special Report, “2021 Key Views: US Fixed Income”, dated December 15, 2020, available at usbs.bcaresearch.com 2 Please see US Bond Strategy Special Report, “2021 Key Views: US Fixed Income”, dated December 15, 2020, available at usbs.bcaresearch.com 3 Please see US Bond Strategy Special Report, “2021 Key Views: US Fixed Income”, dated December 15, 2020, available at usbs.bcaresearch.com 4 For more details on our model please see US Bond Strategy Weekly Report, “How Are Inflation Expectations Adapting?”, dated February 11, 2020, available at usbs.bcaresearch.com 5 Please see US Bond Strategy Weekly Report, “Preparing For A Dark Winter … But Do Markets Care?”, dated November 24, 2020, available at usbs.bcaresearch.com 6 Please see US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020, available at usbs.bcaresearch.com 7 Please see US Bond Strategy Weekly Report, “Preparing For A Dark Winter … But Do Markets Care?”, dated November 24, 2020, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

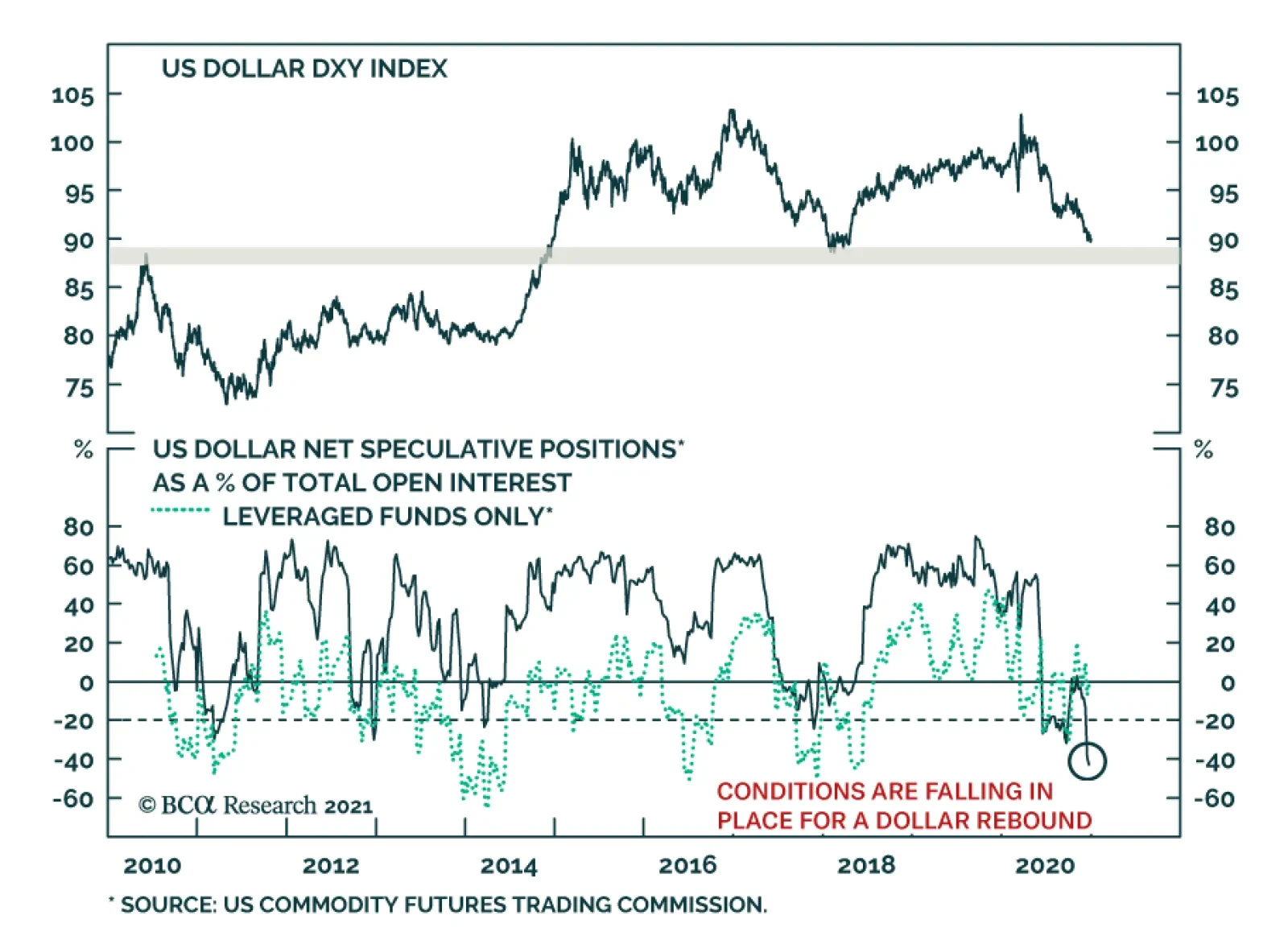

Can the dollar weakness continue in 2021? Economic forces suggest that the most likely outcome is further depreciation. The dollar is a counter-cyclical currency and the continued recovery this year will weigh on the Greenback. Moreover, the strength of US…

BCA Research’s US Bond Strategy service’s base case view is that the eventual pace of Fed tightening will be determined by inflation expectations and that no lift-off will happen until core PCE is above 2% and unemployment near 4%. However, one wildcard could…

This is US Bond Strategy’s final report of the year. Our regular publication schedule will resume on January 5th with our Portfolio Allocation Summary for January 2021. We wish you a happy, healthy and prosperous new year. Highlights Interest Rate Policy: The Fed has given us a checklist of three criteria that must be met before it will lift rates off the zero bound. After those criteria are met, the pace of the eventual rate hike cycle will be determined by how quickly inflation expectations move back to “well-anchored” levels. We don’t expect Fed liftoff in 2021. Balance Sheet Policy: The Fed will only increase the pace or lengthen the maturity of its asset purchases if the economy or risk assets undergo a significant negative shock in 2021. Absent that, Fed communications in late-2021 will increasingly focus on the eventual tapering of asset purchases. Given the current vague guidance about when tapering will start, a scaled-down repeat of the 2013 Taper Tantrum is possible in late-2021 or 2022. Emergency Lending Facilities: The Fed will not undertake efforts to subvert Congress and re-establish its emergency lending facilities in 2021. However, the absence of the facilities will not have a negative impact on financial markets. Fiscal/Monetary Coordination: Looking beyond 2021, we see the lines between fiscal and monetary policy continuing to blur. The Fed will be increasingly incentivized to dip its toes into the fiscal arena and fiscal policymakers will let it. Feature Chart 1An Eventful Year

An Eventful Year

An Eventful Year

It would be an understatement to say that 2020 was a busy year for the Federal Reserve. The Fed cut rates to the zero bound when the recession struck in March. It also exploded its balance sheet to fresh all-time highs and rolled out brand-new emergency lending facilities to support flagging credit markets (Chart 1). Then, to top it all off, the Fed concluded a Strategic Review of its monetary policy strategy in August and officially adopted an Average Inflation Target. This report touches on the market implications of 2020’s big Fed moves, but its focus is on what the Fed is likely to do in 2021. The first three sections discuss how we see the Fed’s interest rate policy, balance sheet policy and emergency lending facilities evolving next year. The final section considers a longer time horizon as it discusses what might be the next frontier for monetary policy: increased cooperation between monetary and fiscal authorities. Interest Rate Policy With the fed funds rate at its effective lower bound, bond investors will spend 2021 trying to determine the eventual start date and magnitude of the next tightening cycle. This will be especially complicated because the Fed’s adoption of an Average Inflation Target means that old models of its reaction function must be discarded. We discussed the implications of the move toward Average Inflation Targeting in a September Special Report.1 To quickly recap, the Fed made three main changes that will influence our outlook for interest rate policy in 2021. First, the Fed edited its Statement on Longer-Run Goals and Monetary Policy Strategy to include a new interpretation of its price stability mandate. The new Statement reads: In order to anchor longer-term inflation expectations at [2 percent], the Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.2 Second, the Fed modified its Statement on Longer-Run Goals and Monetary Policy Strategy to signal that it will rely less on labor market indicators to forecast future inflation. In its old Statement, the Fed talked about minimizing “deviations of employment from the Committee’s assessments of its maximum level.” The revised Statement talks about mitigating “shortfalls of employment from the Committee’s assessment of its maximum level.” In other words, the Fed is saying that it will be less inclined to view an unemployment rate below its estimated natural level (NAIRU) as a signal that inflation is about to accelerate. The Fed’s adoption of an Average Inflation Target means that old models of its reaction function must be discarded. Finally, at the September FOMC meeting, the Fed translated the changes it made to its Statement on Longer-Run Goals and Monetary Policy Strategy into more explicit guidance about when it will consider lifting rates off the zero bound. That guidance is as follows: … it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.3 The Timing Of Liftoff Table 1A Checklist For Liftoff

The Fed In 2021

The Fed In 2021

Digging into the new guidance, we identify three criteria for lifting rates off the zero bound (Table 1). First, the unemployment rate must reach levels consistent with the Committee’s assessments of NAIRU. Currently, those estimates range from 3.5% to 4.5% (Chart 2). Practically, we view this as the least important of the three criteria. NAIRU estimates are revised based on what happens with inflation, and the Fed has already acknowledged that it is now less inclined to view a sub-NAIRU unemployment rate as an inflationary signal. In short, if inflation were to rise sustainably above 2% with the unemployment rate still at 5%, the Fed would simply revise up its NAIRU estimates and begin the rate hike cycle. Chart 2Criteria For Lifting Rates

Criteria For Lifting Rates

Criteria For Lifting Rates

The Fed’s second criterion for lifting rates is also the most specific. Inflation must rise to 2 percent before the Fed will consider hiking rates. In a recent speech, Fed Vice-Chair Richard Clarida said he interprets this to mean that 12-month PCE inflation must be at least 2% before the Fed will consider hiking (Chart 2, bottom panel).4 This is helpful for bond investors. We can be certain that no rate hikes will occur at least until 12-month PCE inflation reaches 2%. Finally, the Fed also wants to be certain that inflation is “on track to moderately exceed 2 percent for some time.” This means that the event of 12-month PCE reaching 2% won’t automatically lead to a rate increase. The Fed must also view inflation gains as sustainable. This will likely become an issue in the first half of 2021 when we know that base effects will push 12-month PCE sharply higher, possibly even above 2%. However, we also know that those gains will be short lived.5 Of course, the Fed also knows about the impact of base effects and it will look past any temporary jump in inflation in H1 2021. More generally, while we advise investors to not pay much attention to the Fed’s NAIRU estimates, the unemployment rate will play a role in the Fed’s determination of whether above-2% inflation is sustainable. That is, the Fed is more likely to view above-2% inflation as sustainable if the unemployment rate is 4% than it is if the unemployment rate is 6%. What Does The Market Think? The bond market has been quick to price-in the big shift in the Fed’s interest rate guidance. At present, the overnight index swap curve is priced for a single 25 basis point rate hike in mid-2023 and only one more by mid-2024 (Chart 3). We see a good chance that the Fed’s three liftoff criteria are met before then, a view that forms the basis of our below-benchmark portfolio duration recommendation for 2021.6 In addition, the New York Fed’s Survey of Market Participants shows that only 43% of respondents expect liftoff before the end of 2023 and only 31% before the end of 2022 (Table 2A). This is further evidence that bond yields have room to rise if it looks like the Fed’s three liftoff criteria will be met in 2022 or the first half of 2023. Finally, the New York Fed’s survey shows that market participants understand the Fed’s three liftoff criteria and that differences in opinion about the timing of liftoff reflect differences in views about the economic outlook, not differences in understanding the Fed’s reaction function. The bulk of survey respondents think that the unemployment rate will be between 3.5% and 4.2% (consistent with the Fed’s NAIRU estimates) and that 12-month PCE inflation will be between 2.2% and 2.5% at the time of liftoff (Table 2B). Chart 3The Fed May Lift Rates Sooner Than Markets Expect

The Fed May Lift Rates Sooner Than Markets Expect

The Fed May Lift Rates Sooner Than Markets Expect

Table 2ALiftoff Expectations

The Fed In 2021

The Fed In 2021

Table 2BMarkets Understand The Fed’s Guidance

The Fed In 2021

The Fed In 2021

The Pace Of Tightening And Why We’re Watching Inflation Expectations We’ve seen the three criteria upon which the Fed will condition its decision to hike rates off the zero bound. But the timing of liftoff is not the only thing that bond investors need to consider. We also need to get a sense of how quickly rate hikes will proceed once the next tightening cycle begins. According to the Fed’s interest rate guidance, even after liftoff the Fed will seek to maintain accommodative monetary conditions until it has achieved its price stability goal under its new Average Inflation Target. Recall that this goal is defined as achieving “inflation that averages 2 percent over time”. This is somewhat vaguer than the Fed’s liftoff guidance. Over what time period should we seek to hit average 2% inflation? One option is to start calculating the average when the new regime was adopted in August. In that case, average PCE inflation is running at 0.96%, well below 2%. Alternatively, we could calculate average inflation since the Fed last cut rates to zero in March 2020 (1.50%) or average inflation since the Fed cut rates to zero in December 2008 (1.43%). The point is that the Fed has not given us a clearly defined target. Differences in opinion about the timing of liftoff reflect differences in views about the economic outlook. For this reason, it’s important for bond investors to understand why the Fed has shifted to an Average Inflation Target. The reason has to do with trying to re-anchor inflation expectations. Box 1 shows an example of an Expectations-Augmented Phillips Curve, the Fed’s go-to framework for thinking about inflation. As the accompanying quote from Janet Yellen explains, the Fed thinks about inflation’s long-run trend as being driven by expectations. Shocks to economic slack and import prices can cause inflation to deviate from its long-run trend, but expectations drive the trend itself. This makes it critical for a central bank to keep expectations well anchored near its inflation target. Box 1The Expectations-Augmented Phillips Curve (aka The Fed’s Inflation Model)

The Fed In 2021

The Fed In 2021

This is the underlying rationale for the Fed’s Average Inflation Target. The Fed has observed that inflation expectations have been too low in recent years. In the Fed’s model, this signals that inflation’s long-run trend has shifted down. In order to get expectations back up to target, the Fed understands that it will probably need to accept a period of above-target inflation. Since economic agents have just experienced a long period of sub-2% inflation, it will probably require a significant period of above-2% inflation before their expectations sustainably shift higher.7 To sum it all up, the Fed will seek to keep monetary conditions accommodative, and thus supportive for risk assets, until inflation expectations are deemed to be re-anchored. At that point, monetary policy will shift to a neutral or restrictive stance and risk asset performance will be challenged. But don’t just take our word for it. Here is what Vice-Chair Clarida said in a recent speech (referenced above): It is important to note, however, that the goal of the new framework is to keep inflation expectations well anchored at 2 percent, and, for this reason, I myself plan to focus more on indicators of inflation expectations themselves – especially survey-based measures – than I will on the calculation of an average rate of inflation over any particular window of time. It is clear that inflation expectations will dictate the eventual pace of Fed tightening. But the question of what measure of inflation expectations to track remains unresolved. Measures of inflation expectations fall into three main categories: Market-based measures Survey measures Trend measures Market-based measures are derived from inflation-linked bonds. Specifically, we derive TIPS breakeven inflation rates for different time horizons by taking the difference between a nominal yield and TIPS yield of the same maturity. In this publication, we often refer to the 10-year and 5-year/5-year forward TIPS breakeven inflation rates and have found that a range of 2.3% to 2.5% has historically been consistent with periods when inflation expectations were deemed “well anchored” (Chart 4A). One potential issue with using market-based measures of inflation expectations is that TIPS prices can sometimes move around for reasons unrelated to changing inflation expectations. That is, regulations or broader portfolio diversification concerns could change the risk premium an investor is willing to accept from TIPS, even if that investor’s underlying inflation view is unchanged. Academics have made attempts to solve this problem by using affine term structure models to decompose yields into various components. Chart 4B presents one such model from D’Amico, Kim and Wei (DKW).8 The DKW model splits the TIPS breakeven inflation rate (or inflation compensation) into an inflation expectation, a liquidity premium that compensates investors for the lower liquidity in TIPS compared to nominal Treasuries and an inflation risk premium that represents the extra compensation investors require to take inflation risk. We are skeptical of the usefulness of affine term structure models. In general, these models have too few inputs to reliably generate the components they purport to measure. However, the Fed clearly pays some attention to the DKW decomposition. If a future increase in TIPS breakeven inflation rates is driven entirely by movement in the liquidity or inflation risk premium components, it would be reasonable to question whether the Fed will react. Chart 4AInflation Expectations: Market-Based Measures

The Fed In 2021

The Fed In 2021

Chart 4BA Decomposition Of TIPS##br## Breakevens

The Fed In 2021

The Fed In 2021

Survey measures of inflation expectations are exactly that: Responses from surveys, usually of professional forecasters or households (Chart 4C). One drawback of survey measures compared to market-based measures is that they are updated less frequently. Another is that survey respondents, particularly households, may only be able to distinguish very large swings in prices. That said, the Fed tracks a wide range of survey measures and they were even singled out by Vice-Chair Clarida as being particularly important in the above quote. Trend inflation measures are statistical measures of the trend in the actual PCE or CPI inflation data. Chart 4D shows both a very simple trend measure, the 10-year annualized rate of change, and a slightly more complex trend measure based on an exponential smoothing rule. Academics have developed even more complex trend inflation measures.9 The logic behind these measures is that expectations tend to adapt only slowly to changes in the actual inflation data. Chart 4CInflation Expectations: Survey Measures

The Fed In 2021

The Fed In 2021

Chart 4DInflation Expectations: Trend Measures

The Fed In 2021

The Fed In 2021

Finally, we should point out a relatively new measure that the Fed will be using to track inflation expectations going forward. It is called the Common Inflation Expectations Index and it is a composite of 21 different survey and market-based inflation measures (Chart 4E), no trend inflation measures are included.10 Chart 4EIntroducing The Common Inflation Expectations Index

The Fed In 2021

The Fed In 2021

To summarize, the Fed has given us a checklist of three criteria that must be met before it will lift rates off the zero bound. After those criteria are met, the pace of the eventual rate hike cycle will be determined by how quickly inflation expectations move back to levels that are considered “well anchored”. Once that happens, the Fed will no longer have an incentive to keep monetary conditions accommodative and risk asset performance will be challenged. Charts 4A-4E in this report provide a wide array of different measures of inflation expectations to monitor. We will keep an eye on all of them, but in particular, we will track the Common Inflation Expectations Index’s progress back to 2.1% and the 5-year/5-year forward TIPS breakeven inflation rate’s progress back to a range of 2.3%-2.5%. While we don’t expect the Fed’s rate hike criteria to be met in 2021, a 2022 liftoff is possible if the COVID vaccine spurs a rapid economic recovery. However, we do expect that, in 2021, the market will start to price-in an earlier liftoff date and quicker pace of tightening than is currently discounted, thus pushing bond yields higher. The Financial Conditions Wildcard Chart 5Financial Conditions

Financial Conditions

Financial Conditions

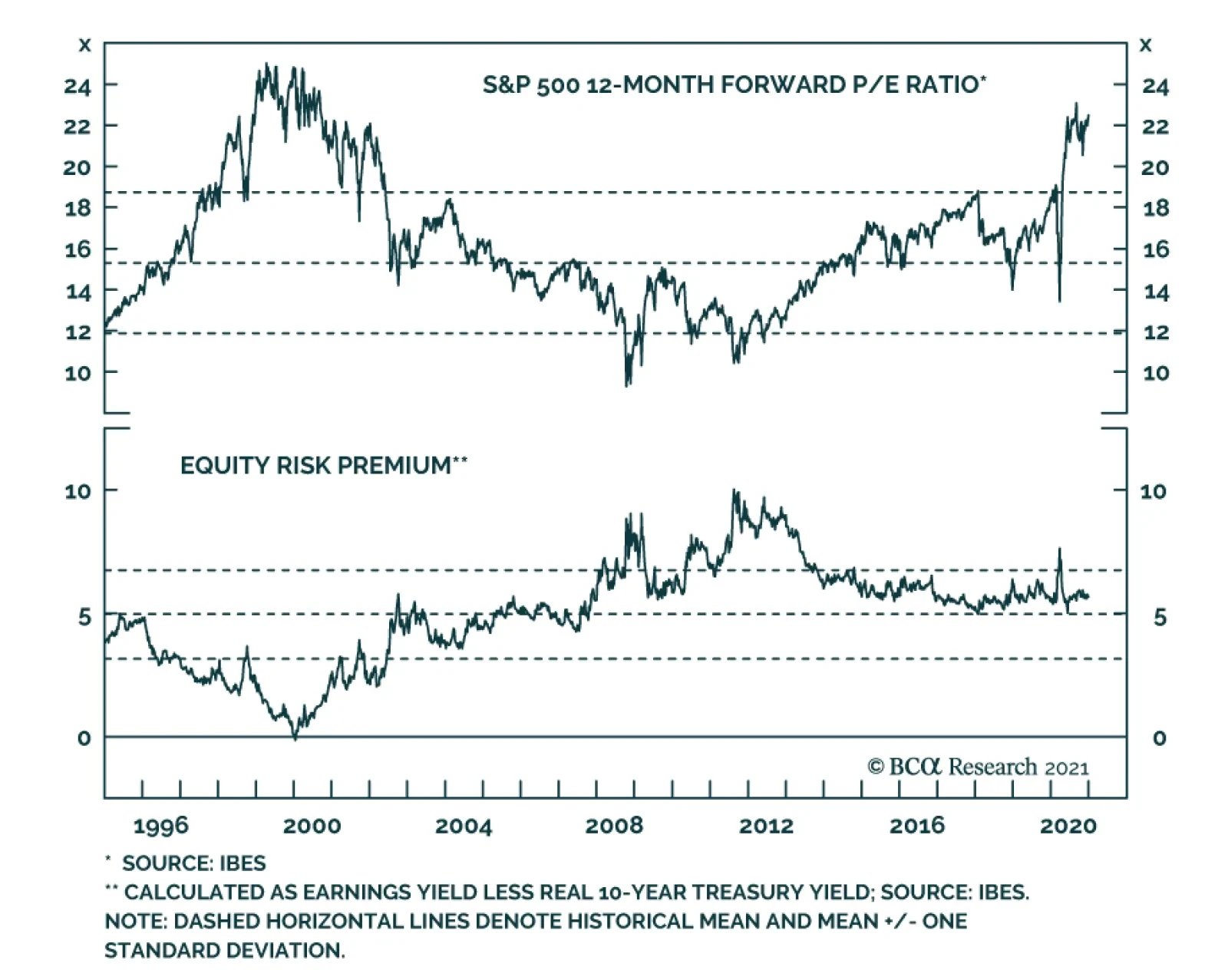

Our base case view is that the eventual pace of Fed tightening will be determined by inflation expectations. However, there is one wildcard that could cause the Fed to abandon its inflation expectations goal and tighten policy earlier. That wildcard is financial conditions. Presently, financial asset valuations are a mixed bag (Chart 5). Corporate bond spreads are tight, but not at all-time expensive levels. Equity P/E ratios are very elevated, but equities don’t look expensive compared to bonds. If these valuations stay relatively stable, the Fed will continue to rely on inflation expectations to guide the pace of tightening. However, if inflation expectations take a long time to rise, it is conceivable that such a long period of low interest rates could lead to historically stretched financial asset valuations. In short, if inflation doesn’t return within the next couple of years, the Fed may have to tighten policy to take the wind out of an asset bubble that might otherwise burst and lead to an economic recession. We stress that we are not yet close to this point and that the bar for the Fed to abandon its inflation goal will be very high, but we would place financial conditions alongside inflation expectations as the two most important variables to monitor to assess the eventual pace of Fed tightening. Balance Sheet Policy With the funds rate pinned at zero and the Fed’s interest rate guidance essentially set in stone, changes to the pace and composition of asset purchases are the principal tool that the Fed will use to provide more or less immediate monetary accommodation in 2021. The Fed is currently purchasing $80 billion of Treasuries and $40 billion of Agency MBS each month, with Treasury purchases spread out across the yield curve. If this pace and distribution of Treasury purchases is maintained in 2021, the Fed will end up purchasing less and less of the Treasury flow. The Treasury Department has a stated policy goal of increasing the average maturity of the outstanding debt and it has been pursuing that goal by raising the amount of coupon issuance at the expense of bills. The Treasury has already given us its planned coupon issuance schedule for Q4 2020 and Q1 2021. Chart 6 shows that net Fed coupon purchases will gradually decline as a percentage of gross issuance, assuming the Treasury follows through with its plan and the Fed’s balance sheet policy is unchanged. Chart 6The Path For Treasury Supply And Fed Demand

The Fed In 2021

The Fed In 2021

Can The Fed Do More? … Will The Fed Do More? It is possible that the Fed will use its balance sheet to provide more monetary easing in 2021. There are two ways it could do this. First, it could simply increase the monthly pace of asset purchases. Alternatively, it could keep the same pace of purchases but shift Treasury buying toward the long-end of the curve. The idea here would be to prevent long-dated yields from rising too quickly. One or both of these changes could happen in 2021, but only if the economy experiences a negative growth shock or risk asset prices (equities and corporate credit) fall significantly. In that case, the Fed will want to be seen as responding to a negative shock, but absent that, the Committee seems comfortable with its current balance sheet strategy. Chart 7Rate-Sensitive Sectors Have Recovered

Rate-Sensitive Sectors Have Recovered

Rate-Sensitive Sectors Have Recovered

Some have suggested that, even if the economic recovery stays on track, the Fed will try to use its balance sheet to lean against rising long-maturity bond yields. We doubt this. First, it is not obvious that the Fed would be able to stop the 10-year Treasury yield from rising to a range of, say, 1.25% to 1.5% by increasing bond purchases in that maturity range by a few billion dollars. As long as the Fed’s interest rate guidance is unchanged, the market’s interest rate expectations will continue to exert a powerful influence on bond yields across the entire curve. Unless the Fed announces a cap on long-dated bond yields, and pledges to buy enough securities to enforce that cap, we are skeptical about the effectiveness of just changing the quantity of asset purchases. Second, it is also not clear that a 10-year Treasury yield between 1.25% and 1.5%, in the context of a steepening yield curve and improving economic growth, would be a problem for either the economy or risk assets. In fact, these sorts of environments tend to be very positive for risk asset performance.11 It is only when the Fed is shifting to a more restrictive monetary policy stance and the yield curve is flattening that bond yields start to exert a negative influence on the economy and risk assets. Even if the Fed is not worried about a moderate bear-steepening of the Treasury curve, a case could be made for providing more easing right now in order to spur a quicker recovery. This question was posed to Chair Powell several times at the last FOMC press conference. In response, Powell noted that the sectors of the economy that are most sensitive to interest rates – residential investment and consumer spending on durable goods – have already recovered (Chart 7). The lagging sectors of the economy – particularly consumer spending on services – cannot recover until the COVID vaccine is widely distributed, irrespective of the level of interest rates. In our view, this is an acknowledgement that the Fed does not see much value in trying to provide further accommodation through the balance sheet channel. All in all, our base case scenario is that the Fed will maintain its current pace and maturity distribution of asset purchases throughout 2021. However, it will increase the pace and/or lengthen the maturity if there is a significant shock to the economy and/or financial markets. Later in 2021, if the recovery stays on track, Fed communications will increasingly take up the issue of when it will be appropriate to taper its pace of asset purchases. The Exit From Asset Purchases And The Possibility Of A Taper Tantrum Chart 8Remember The Taper Tantrum

Remember The Taper Tantrum

Remember The Taper Tantrum

The Fed has already given us a timeline for how it will wind down its asset purchases. According to the minutes from the November FOMC meeting, most participants support a timeline where the Fed will start tapering its pace of asset purchases sometime before the first rate hike. It will then begin lifting interest rates and will stop purchases altogether sometime after that. At the December FOMC meeting, the Fed gave us additional guidance on when it will start the tapering process. Unfortunately, this guidance is quite vague and only confirms the fact that tapering will start before the liftoff date. Specifically, the Fed said that tapering will begin when “substantial further progress has been made toward the Committee’s maximum employment and price stability goals.” Because the guidance around the timing of the tapering process is quite vague, we think it’s possible that it could sneak up on investors and lead to a sharp upward re-adjustment in rate hike expectations, and thus a bond sell-off. In essence, a tamer version of the 2013 Taper Tantrum is possible in late-2021 or 2022. On May 22, 2013, Fed Chair Ben Bernanke explained the Fed’s plan to eventually start tapering its asset purchases. Because investors took this to mean that the rate hike cycle would start much sooner than anticipated, the bond market underwent a sharp re-adjustment. The market quickly went from pricing-in only 35 bps of rate hikes over the next 24 months to 116 bps, and Treasury returns fell precipitously as a result (Chart 8). The Fed has learned a few lessons about communications since then, and it will do its best to keep market expectations aligned with its own strategy. However, unless firmer guidance is provided about when tapering will begin, the risk of a hawkish surprise around the tapering announcement remains. Bottom Line: The Fed will only increase the pace or lengthen the maturity of its asset purchases if the economy or risk assets undergo a significant negative shock in 2021. Absent that, Fed communications in late-2021 will increasingly focus on the eventual tapering of asset purchases. Given the current vague guidance about when tapering will start, a scaled-down repeat of the 2013 Taper Tantrum is possible in late-2021 or 2022. Emergency Lending Facilities In addition to cutting rates to zero and massively scaling up the size of its balance sheet, the Fed also responded to the COVID recession by launching a slew of emergency lending facilities, some re-treads from the financial crisis and some brand new. Facilities to support the corporate bond market (The Primary and Secondary Market Corporate Credit Facilities) and the Municipal Liquidity Facility were particularly successful at capping bond spreads versus Treasuries, even if their actual usage was quite low. In fact, corporate bond spreads peaked on the very day that the Fed announced its corporate credit facilities in March (Chart 1). More recently, however, Treasury Secretary Steve Mnuchin refused to authorize the continuation of most of the Fed’s emergency lending facilities beyond the end of the year. We wrote in November that, even with the Treasury taking back the funds used to set up the facilities, the Fed could re-launch them in 2021 if incoming Treasury Secretary Janet Yellen provides her approval.12 However, a late addition to the recently passed fiscal stimulus package appears to prohibit the re-authorization of the facilities without Congressional approval. At the time of publishing, we have not been able to see the details of the new provision, so there remains some uncertainty about what the Fed can and cannot do in this regard. Credit spreads are no longer trading at distressed levels, primary issuance markets are functioning properly, and the Fed’s facilities have hardly been used at all. Nonetheless, while the new bill raises interesting questions about Fed independence in the long-run, we doubt that markets will respond negatively to the absence of the Fed’s emergency facilities in 2021. Credit spreads are no longer trading at distressed levels, primary issuance markets are functioning properly, and the Fed’s facilities have hardly been used at all (Table 3). Table 3Usage Of The 2020 Federal Reserve Emergency Lending Facilities

The Fed In 2021

The Fed In 2021