United States

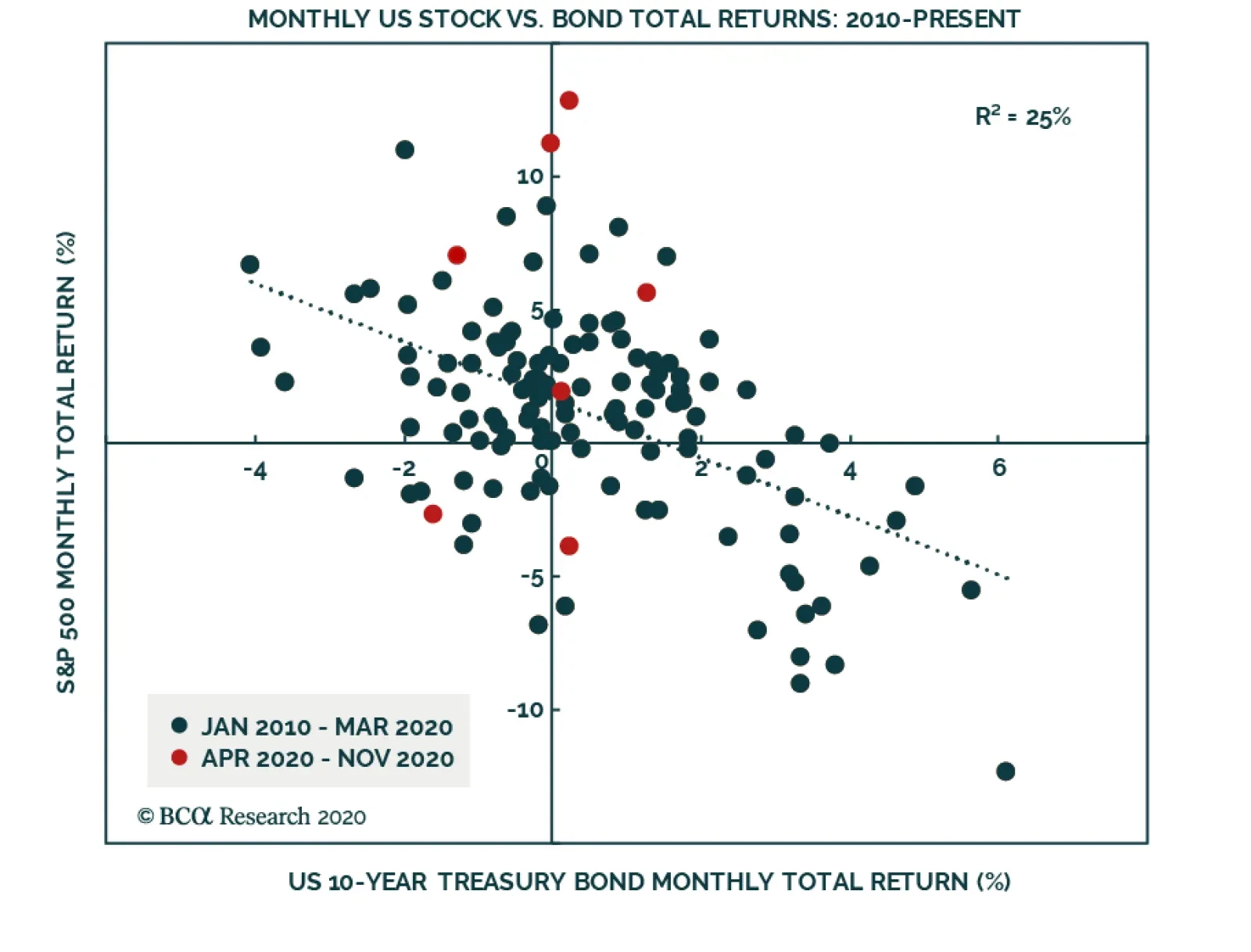

The chart above presents a scatterplot of monthly total returns for the S&P 500 index and 10-year US Treasurys. The chart highlights that the relationship has been reliably negative over the past decade, meaning that the correlation between stock prices…

In a previous Insight, we showed the 1-year rolling “alpha” for four MSCI global equity factor portfolios, and argued that an equity factor rotation is coming over the next 6-12 months. We calculated alpha using Jensen’s approach, which subtracts the…

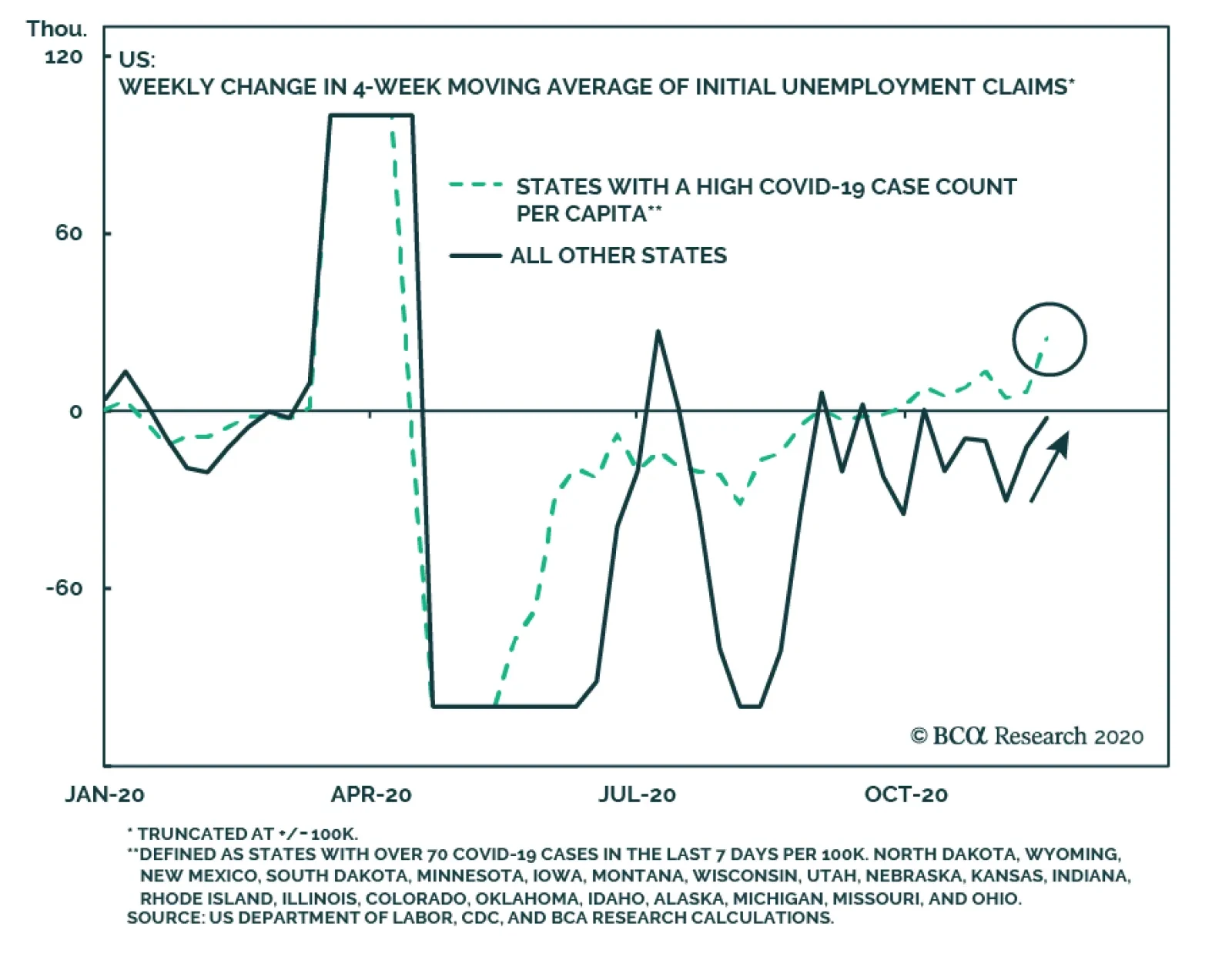

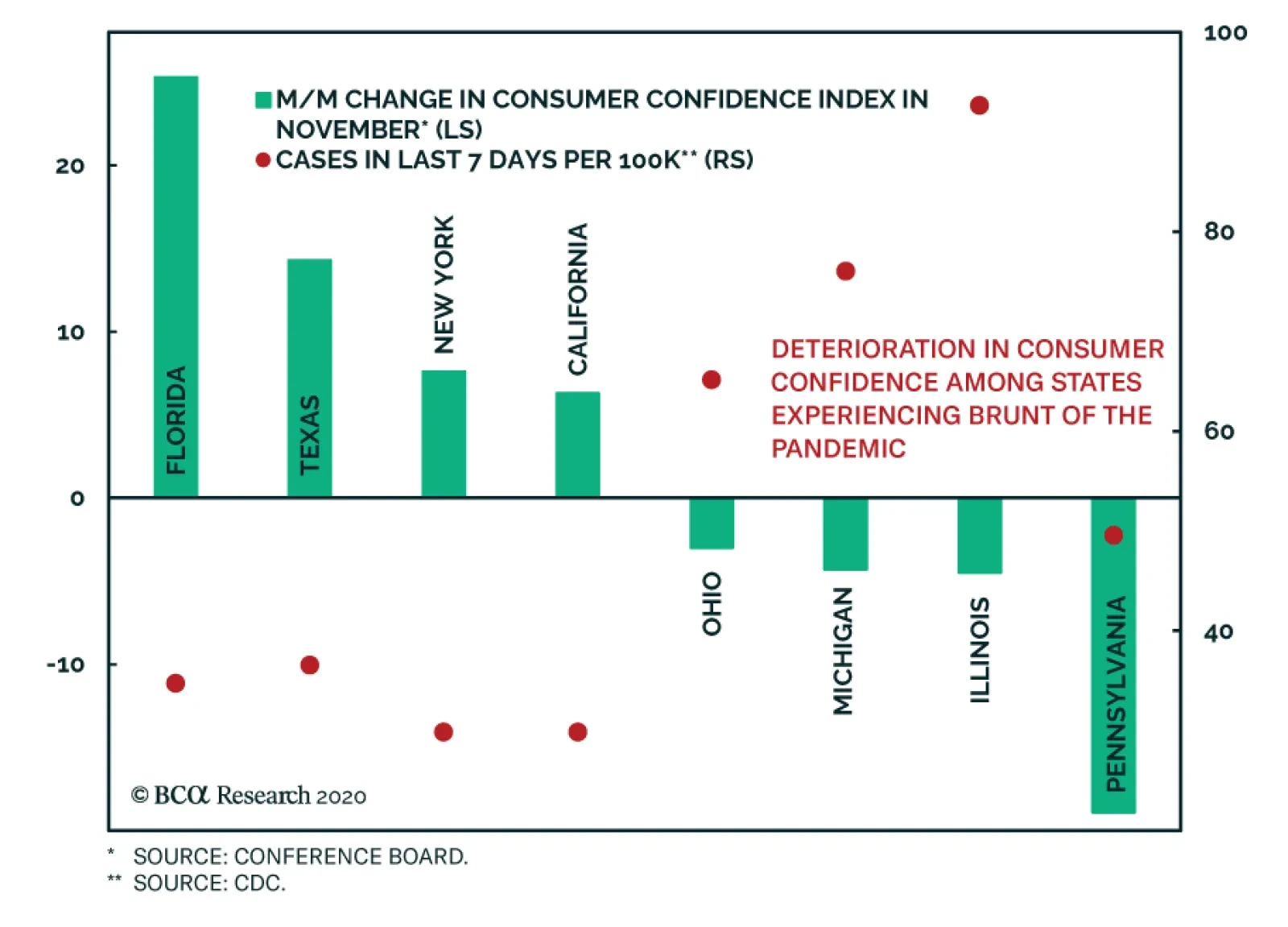

In a previous Insight, we warned that rising initial jobless claims among states experiencing the brunt of the pandemic served as a warning sign for the overall labor market. At the time, total initial claims had fallen by the most in five weeks. This…

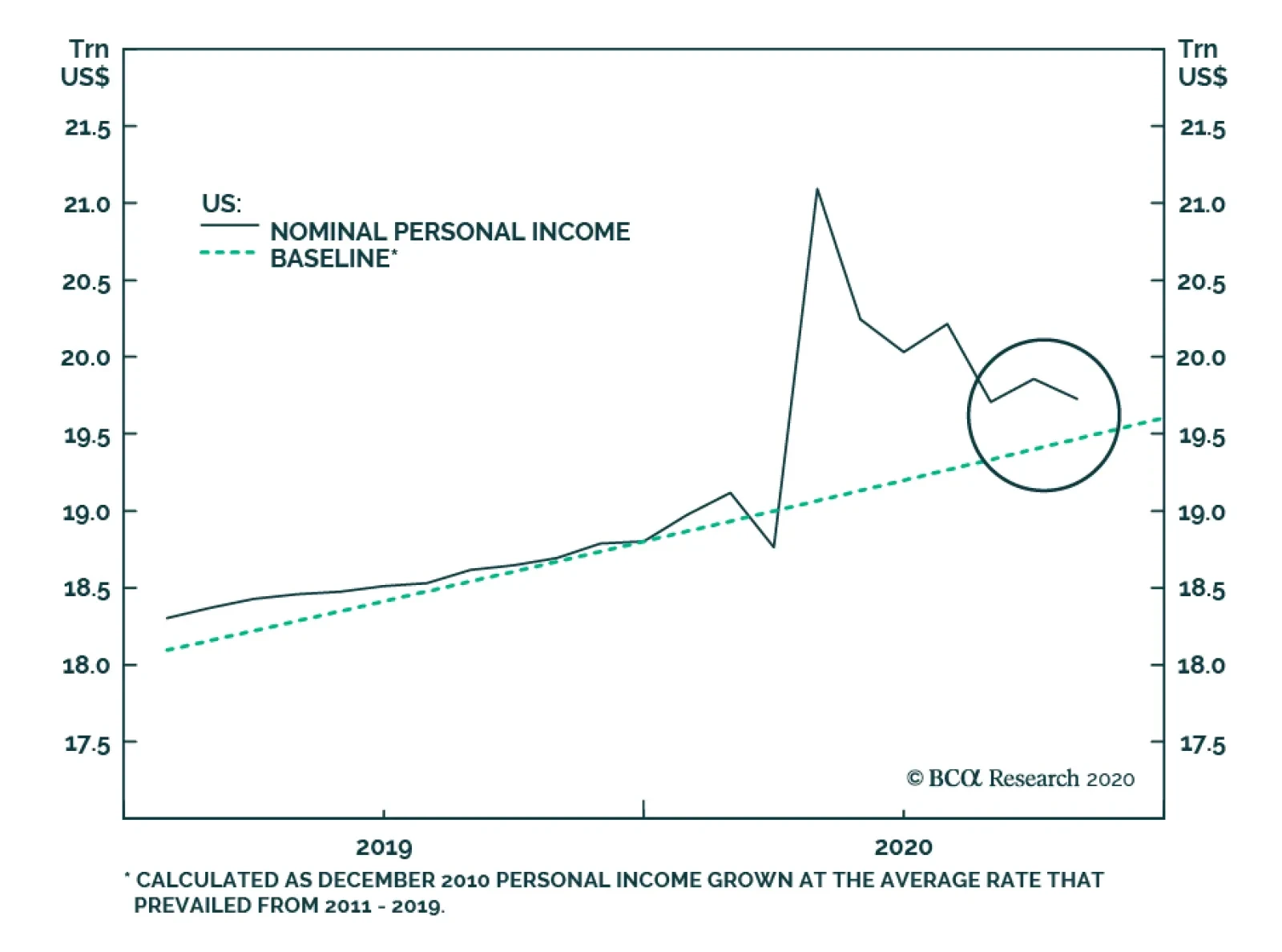

The US October Personal Income and Outlays report was released on Wednesday, and provided investors with at least some positive news. While nominal consumer spending remains roughly 1.6% below its pre-pandemic level, it continued to grow in October. That…

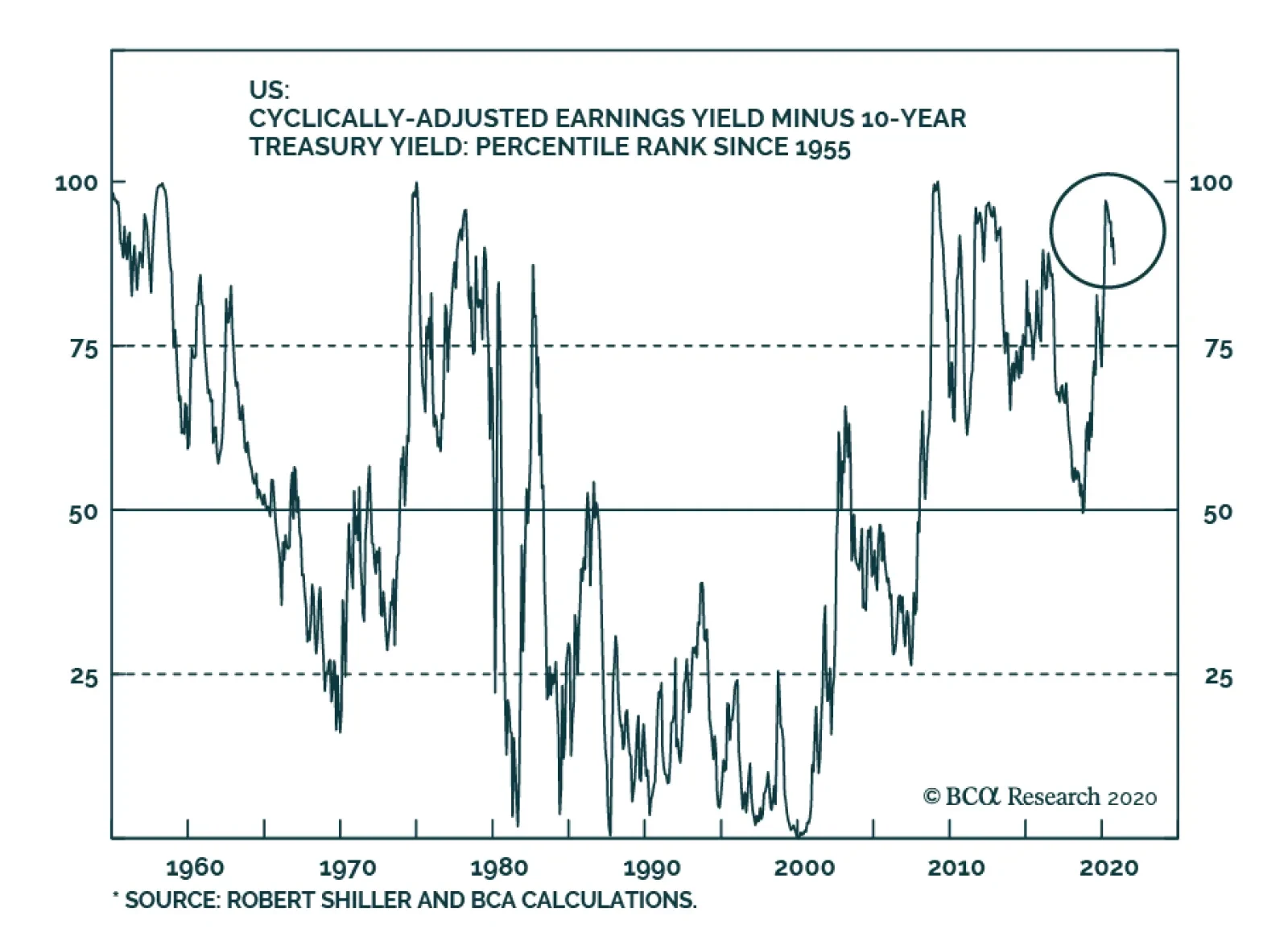

The cyclically-adjusted PE ratio (CAPE) pioneered by Robert Shiller is a yardstick that investors often cite to illustrate that US equity valuations have climbed decisively in recent years. The Shiller CAPE currently sits close to 32 times cyclically-adjusted…

Open For Business

Open For Business

In this Monday’s Strategy Report we upgraded the S&P hotels, resorts & cruise lines index to an above benchmark allocation in light of the improving macro backdrop. Consumer sentiment has staged a W-shaped recovery and while still flimsy, the brightening vaccine efficacy news should catapult it higher in the coming quarters. The implication is that the wide gulf between consumer confidence and relative hotels share prices will narrow via a catch-up phase in the latter (top panel). Closely linked to the budding recovery in confidence are discretionary versus non-discretionary retail sales. The latter have been correlated with the oscillations in relative share prices, and the current message is positive (bottom panel). Finally, the ISM non-manufacturing survey is on a sling shot recovery following the depths of the spring readings. This rebound also suggests that the path of least resistance is higher for lodging stocks (middle panel). Bottom Line: Upgrade the S&P hotels, resorts & cruise lines index to overweight. The ticker symbols for the stocks in this index are: BLBG: S5HOTL – MAR, HLT, CCL, RCL, NCLH.

According to BCA Research's US Bond Strategy service, weaker Q4 economic growth could cause Treasury yields to fall in the near-term, but the knowledge that a vaccine is coming in 2021 will limit the downside. Investors should maintain below-benchmark…

The Conference Board Consumer Confidence Index fell to 96.1 in November from 101.4, below expectations of 98. The expectations component was the biggest drag on the overall index, dropping to 89.5 from a revised 98.2. Meanwhile, the present situation…

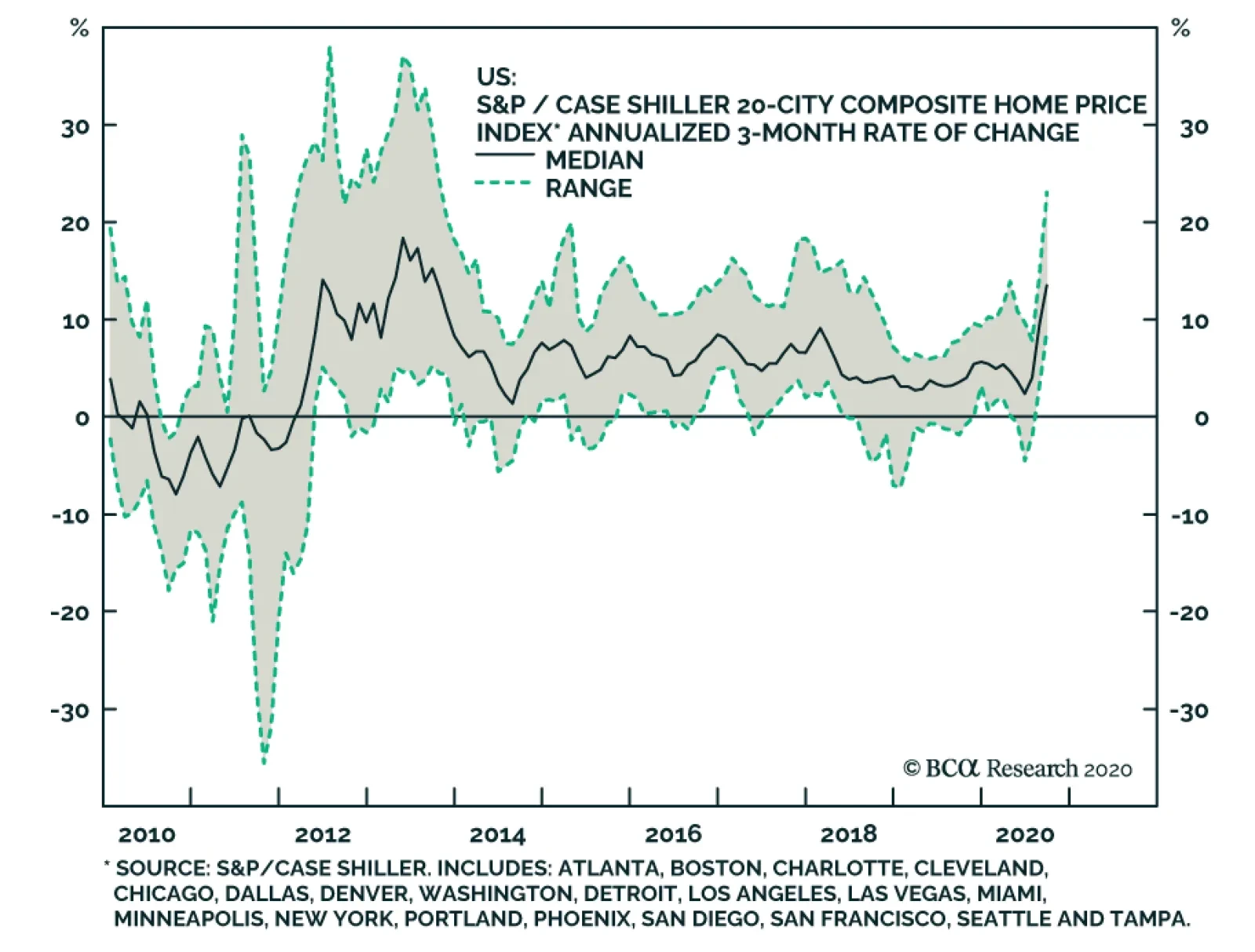

Yesterday’s September update to the S&P Corelogic Case-Shiller index highlighted that US house prices are soaring. The 20-City Composite posted a 6.6% year-over-year gain, up from 5.3% in the previous month, and the chart above highlights that the gains…

What Does EUR/USD At 1.50 Mean For US Equity Sectors?

What Does EUR/USD At 1.50 Mean For US Equity Sectors?

Our macro view assumes a lower US dollar in the New Year. Our sister BCA Foreign Exchange service published a Strategy Report last week exploring a possible 1.50 print on EUR/USD. The bottom panel of the chart shows that China is firing on all cylinders and is pulling all the levers in reflating global growth. Keep in mind that increasing global trade is synonymous with a declining USD. As the supply/circulation of US dollars increases with rising global exports, a virtuous cycle takes root where a lower USD begets increasing trade in a positive feedback loop. This sparked a thought experiment on our end: what are the US equity sectors implications of EUR/USD at 1.50? First, deep cyclical and high operating leverage sectors will accelerate their outperformance phase as they are responsible for the lion’s share of SPX foreign sourced revenues. In contrast and in a relative sense, landlocked domestic sectors with little if any international sales will underperform in a steeply declining USD backdrop. Taken together our cyclicals over defensives portfolio bent will catch on fire (middle panel). Bottom Line: Rising prospects of a virtuous cycle where the revival in global trade pushes the US dollar lower and ignites a positive feedback loop will further boost deep cyclical sectors at the expense of defensives.