United States

Highlights The vaccine promises an eventual return to “normal” life – just as Americans voted to “return to normalcy.” Markets are cheering and hinting at an eventual rotation into value stocks. The contested US election can still cause volatility even though Trump is highly unlikely to change the result. The fiscal stimulus cliff is still a risk to the normalcy rally in the short run. But gridlock is the best political outcome over the coming 12-24 months. Stay strategically long global stocks over bonds. Tactically maintain safe-haven positions, add risk gradually, and stay short China/Taiwan. Feature The news of Pfizer’s success in developing a COVID-19 vaccine galvanized financial markets this week. America’s leading public health official Anthony Fauci also predicted that Moderna’s vaccine candidate would be similarly effective. It will take time to distribute these vaccines but the world can look toward economic recovery next year. Stocks rallied, bonds sold off, and value outperformed growth on the back of the news (Charts 1A and 1B). Chart 1ABiden: Return To Normalcy

Biden: Return To Normalcy

Biden: Return To Normalcy

Chart 1BVaccine: Return To Normalcy

Vaccine: Return To Normalcy

Vaccine: Return To Normalcy

The vaccine announcement super-charged the “return to normalcy” rally that followed the US election. The election’s likeliest policy outcome is that President Elect Joe Biden will not raise sweeping tariffs while Republican senators will not raise taxes next year, the best-case scenario for markets. This is genuinely positive news. The benefits are very clear over the next 12 months. But the risks are also very clear over the next three months: the virus will remain a problem until the vaccine is widely distributed, the US is in the midst of a contested election that could still cause negative surprises, the Republican senators are less likely to agree to fiscal relief, and President Trump will take aggressive actions to cement his legacy during the “lame duck” period of his last 68 days in office. The takeaway is that the US dollar will see a near-term, counter-trend rally and developed markets will outperform emerging markets for a while longer. We are only gradually adding risk to our strategic portfolio as we keep dry powder and maintain tactical safe-haven trades. Is The Election Over Or Not? Yes, most likely the election is over. But our definitive guide to contested US elections will teach any reader to be sensitive to the tail risks. The counting of ballots is not finished and the Electoral College does not vote until December 14. First, it is still possible that President Trump could pull off a victory in Georgia, which will now recount ballots by hand. Biden’s margin of victory of 14,045 votes is not so large there as to make it impossible that Trump would come back with a win (though history suggests recounts only change hundreds, not thousands, of votes). Trump is also narrowing the gap in Arizona, where counting continues, though the latest reports suggest he is still falling short of the roughly 60% share of late ballots that he needs to close the 11,635 vote gap and win the state. Second, there is a 50/50 chance that the Supreme Court will rule that Pennsylvania must stick to the statutory November 3 deadline, i.e. not accept mail-in ballots that arrived in the three days after that date. While the high court would prefer to let Pennsylvania settle its own affairs, this case is of the sort that the court could feel compelled to weigh in. The constitution is crystal clear that legislatures, not courts, decide how a state’s electors are chosen. Such a ruling probably would not reverse Biden’s projected victory in Pennsylvania. Trump is currently trailing Biden by 53,980 votes in this state. State officials say that the ballots that arrived late amount to only 7,800 and would not be able to change the outcome.1 This may be understating the risk but it is probably accurate in the main. Table 1 shows the share of mail-in votes that arrived late in this year’s primary elections. The share was 1.07% in Pennsylvania and up to 3% in other states. Applying the high water mark of 3% to the November 3 general election mail-in ballots, it is possible that 77,187 votes arrived late and would be excluded by a Supreme Court ruling. However, 85% of those ballots would have to have gone to Biden in order for Trump to come out the winner. This is far-fetched. Table 1Share Of Ballots Arriving Late In Primary Election Extrapolated To General Election

The "Normalcy" Rally

The "Normalcy" Rally

It is also unlikely that Republican legislatures will take matters into their own hands and defy the election boards of their state by nominating their own slate of Republican electors – a scenario we entertained in our definitive guide. If Biden leads the statewide vote, then a state legislature would be politically suicidal to appoint the state’s electors to vote for Trump. It would invite a popular backlash. In the case of Pennsylvania, Republican leaders of the lower and upper chambers have explicitly denied any willingness or ability to choose electors other than those entailed by the popular vote. Thus the 1876 “Stolen Election” scenario is extremely unlikely in this critical state. It is just as unlikely in Arizona, Nevada, or Georgia.2 Nevertheless, if President Trump wins in Georgia or gets a favorable Supreme Court verdict, investors will have to increase the probability that the election result will be overturned, which currently stands at 16% (Chart 2). This will cause a bout of volatility even if it changes nothing in the end. If somehow Trump pulls off a Rutherford B. Hayes and overturn the result, markets should sell off. Yes, Trump is an exclusively commercial and reflationary president, but his election on a constitutional technicality would create nearly unprecedented social and political instability in the United States and it would presage major instability globally. Chinese, European, and Canadian assets would be hardest hit (Chart 3). Chart 2Trump’s Tiny Chance Of Reversing Election

The "Normalcy" Rally

The "Normalcy" Rally

Otherwise Trump and the Republicans are trying to do four things with their litigation: (1) probing for weaknesses that can delay or change the Electoral College math (2) conducting due diligence in case fraud really did tip over one of the states (3) saving face for President Trump and his allies, who otherwise would be exposed as failures (4) keeping their base motivated for the showdown in Georgia on January 5, which will determine control of the Senate. Chart 3Trump's Loss Favors Euro, Renminbi, Loonie

Trump's Loss Favors Euro, Renminbi, Loonie

Trump's Loss Favors Euro, Renminbi, Loonie

In Georgia, opinion polls show Republican David Perdue slightly leading Democrat Jon Ossoff, in keeping with his superior showing on November 3. However, Republican Kelly Loeffler is trailing Democrat Raphael Warnock (Charts 4A and 4B). Last week we argued that the odds of Democrats winning both races stood around 20%. If anything this view is generous – given that Perdue already beat Ossoff, and Warnock will continue to suffer attacks for associating with Fidel Castro – but it is in line with online betting markets (Chart 5). Chart 4AVoters Split On Georgia Senate Runoffs

The "Normalcy" Rally

The "Normalcy" Rally

Chart 4BVoters Split On Georgia Senate Runoffs

The "Normalcy" Rally

The "Normalcy" Rally

Chart 5Democrats Have ~20% Chance To Win Senate

The "Normalcy" Rally

The "Normalcy" Rally

Investors should plan on the US government being gridlocked unless something occurs that fundamentally changes the Georgia race. Gridlock is positive, so if Trump’s election disputes keep the Republican political base spirited for the Georgia runoffs, then Trump’s activities have an ironic upside for markets. That is, as long as he doesn’t succeed in overturning the election result and the flames of discontent do not break out into a significant violent incident. Other fears about the transition period are less concerning. Several clients have asked us what should happen if President Elect Biden came down with COVID-19 or were otherwise incapacitated. The answer is that Vice President Elect Kamala Harris would take his place, as she now has popular consent to do exactly that. Prior to the Electoral College voting on December 14, the Democratic National Committee would have to nominate a candidate to replace Biden, almost certainly Harris. After December 14, the regular succession would apply under the twentieth amendment and Harris would automatically fill Biden’s shoes. Harris is only slightly more negative for equities than Biden: her regulatory pen would be more anti-business, but like Biden her main policies depend entirely on control of the senate. Bottom Line: It ain’t over till it’s over. The big picture is positive for risk assets but a surprise from ongoing election disputes or the unusually rocky transition of power would trigger a new bout of volatility. Stay long Japanese yen and health stocks on a tactical time frame. Trump’s Lame Duck Risk An investor in the Wild West has often criticized us for arguing that Trump would become a “war president” as he became a political lame duck at home. This war president view did pay off with Iran in January 2020, but otherwise the criticism is valid (see Trump’s Abraham Accords). Now Trump is almost certainly a lame duck so we will find out what he intends to do when unshackled from election concerns. Stay long Japanese yen and health stocks on a tactical time frame. Since losing the election, Trump has fired Defense Secretary Mark Esper, several defense officials have resigned, and CIA Director Gina Haspel is rumored to be next on the chopping block. Most of the officials to depart had broken with the president over the course of the election year, so he may just be dishing out punishment now that the campaign is over. But it is possible that Trump is planning a series of final actions to cement his legacy and that these officials were removed because they got in the way. Chart 6Trump's Lame Duck Risk To China And Taiwan Strait

Trump's Lame Duck Risk To China And Taiwan Strait

Trump's Lame Duck Risk To China And Taiwan Strait

First, there is no doubt that Trump is already tightening sanctions on China and Iran. China was the origin of the coronavirus pandemic and Trump has called for reparations, which could mean more tariff hikes. His outstanding legacy in US history will be his insistence that the US confront China. We are fully prepared for this outcome and remain short the renminbi and Taiwanese equities, despite their strong performance year-to-date (Chart 6). Trump could also raise tariffs on Europe. However, investors should be used to tariffs and sanctions by now. The impact would be fleeting and the next administration could reverse it. In the case of the renminbi, or any tariffs that weigh on the euro, investors should buy on the dips. By contrast, there are some conceivable actions – we are speculating – that would be extremely destabilizing and possibly irreversible. These would include: Extending diplomatic recognition to Taiwan, potentially provoking a war with China. Sending aircraft carriers into the Taiwan Strait, like Bill Clinton did during the Third Taiwan Strait Crisis, to shore up US deterrence. Launching surgical strikes against Iran’s ballistic missile and nuclear facilities or critical infrastructure. A prominent official has already denied that Trump intends anything of the sort. Launching surgical strikes against North Korea’s ballistic missile and nuclear facilities. No sign of this, but Kim Jong Un did enhance his capabilities after his meetings with Trump, thus embarrassing the president on a major foreign policy initiative ahead of the election. Providing intelligence and assistance to US allies like Israel who may seek to sabotage or attack Iran now or in future to prevent it from acquiring nuclear weapons. Withdrawing US troops from Germany or South Korea – which is much more consequential than hasty withdrawals from Afghanistan or Syria, which Trump clearly intends. War actions are largely infeasible. The bureaucracy would refuse to implement them. Assuming the Department of Defense would slow-walk any attempts to reduce troops in important regions like Germany or Korea, it would almost certainly avoid instigating a war. Withdrawing troops from Afghanistan or Syria is manageable, and fitting with Trump’s legacy, but it would not be disruptive for financial markets. A diplomatic upgrade or a show of force to demonstrate the American commitment to defend Taiwan is possible and highly disruptive for global financial markets. The critical risk may come from US allies or partners that are threatened by the impending Biden administration and have a window of opportunity to act with full American support while Trump still inhabits the Oval Office. The likeliest candidate would be Israel and Saudi Arabia on the Iranian nuclear program. Trump’s onetime national security advisor, H. R. McMaster, has already warned that Israel could act on the “Begin Doctrine,” which calls for targeted preventive strikes against hostile nuclear capabilities.3 Even here, Israel is unlikely to jeopardize its critical security relationship with the United States, so any actions would be limited, but they could still bring a major increase in regional tensions. Saudi Arabia can do little on its own but President Trump could willingly or unwilling encourage provocative actions. Chart 7Big Tech Is Not Priced For Surprises

Big Tech Is Not Priced For Surprises

Big Tech Is Not Priced For Surprises

Any number of incidents or provocations could occur in this risky interregnum between Trump and Biden. Some suggest Trump will release a treasure trove of documents to discredit Washington and the Deep State. If that is all that occurs, then investors will be able to give a sigh of relief, as revelations of government intrigue would have to be truly consequential for future events in order to cause a notable market impact. Last-minute executive orders on regulating domestic industries are just as likely to shock markets as any international moves. We speculate that Big Tech is in Trump’s sights for censoring his comments during the election. In the wake of the Supreme Court’s decision in Department of Homeland Security versus Regents of the University of California, the Trump administration is positively incentivized to issue a flurry of executive orders and write them in a way that makes them hard for the Biden administration to rescind them.4 Tech is priced for perfection, despite ruffles due to the vaccine this week, and investors expect Biden-Harris to maintain Obama’s alliance with Silicon Valley, not least because Biden has named executives from Facebook and Apple to his transition team and is considering putting former Google chief Eric Schmidt in charge of a Big Tech task force (Chart 7).5 Ultimately we have no idea what the Trump administration will do in its final two months. A lot of Trump’s attention will be focused on contesting the election. Drastic or reckless decisions will likely be obstructed by the bureaucracy. But the president still retains immense powers and there are executive orders that are legitimate and would benefit the US’s long-term interests even if disruptive for financial markets – and these would be harder for officials to disobey. Trump is an anti-establishment player who intends to shake up Washington, stay involved in politics, and cement his legacy. There is a reason for investors to take political risk seriously rather than to assume that the transition to a more market-friendly administration will be smooth. Bottom Line: Stay long gold on geopolitical risk, despite the potential for a counter-trend rise in the US dollar. We are neutral tech: polarization and fiscal risks are positive for tech shares but reopening and Trump lame duck risks are negative. Biden’s Cabinet Picks This “lame duck Trump” risk explains why we are not overly concerned about Biden’s cabinet picks. Insofar as Biden’s choices affect the market at all, they will confirm the “return to normalcy” theme and hence will be market-friendly. Take for example Biden’s just-announced chief of staff, Ronald Klain, who was chief of staff when Biden served as vice president from 2009- 16. The current transition is obstructed by election disputes, as occurred in November-December of 2000, but the cabinet picks are not likely to bring negative surprises. Already Biden has announced a coronavirus advisory board, a bipartisan transition team, and is pondering other picks, some of which will be known by Thanksgiving. None of the choices are in the least disruptive or radical – and most are acceptable to Wall Street. Biden will pick experts and technocrats who are known from his political career, the Obama administration, the Clinton administration, the Democratic Party, and academia. The market will invariably approve of establishment nominations after four years of anti-establishment picks and spontaneous firings. Since the Senate will remain in Republican hands, the cabinet members will have to be centrist enough to be confirmed. While Biden will inevitably nominate a few progressives, they will either fail in the Senate or take up marginal posts. Stay long gold on Trump “lame duck” geopolitical risks. Biden may have the opportunity to appoint three or even four members to the Federal Reserve’s board of governors. The Trump administration failed to fill two seats, while Fed Chair Jerome Powell’s term will expire in February 2022 (Diagram 1). If Biden appoints Lael Brainard to another post, such as Treasury Secretary, he will have a fourth space to fill. Diagram 1Biden Could Have Three-To-Four Fed Picks

The "Normalcy" Rally

The "Normalcy" Rally

Chart 8Facing Gridlock, Biden Will Re-Regulate

The "Normalcy" Rally

The "Normalcy" Rally

The implication will be a further entrenchment of dovish policy, with greater attention to new concerns that fall outside of traditional monetary policy such as climate change and racial inequality. The Fed has already committed to pursuing “maximum employment,” refraining from rate hikes till the end of 2023, and targeting average inflation – all a major boon to the Biden administration as it attempts to revive the economy. What is negative for markets is that Biden will re-regulate the economy – after Trump’s deregulatory shock – and that this will bring about political risks for small business and key industries like health, financials, and energy (Chart 8). Biden has little other option given that his legislative agenda will be largely stymied. Nevertheless, the sectors most likely to be heavily impacted are attractively valued and stand to benefit from economic normalization if not from Biden’s version of normalcy. Bottom Line: Stay long health and energy. Yes, Gridlock Is Best For Markets Some clients have asked us about our view that gridlocked government is truly the best for financial markets. Wouldn’t Democrats winning control of the Senate in Georgia be better, as it would usher in greater political certainty and larger fiscal spending? We have addressed this issue in previous reports so we will be brief. First, yes, gridlock has higher returns than single-party sweep governments on average over the past 120 years (Chart 9). Clearly the normalcy rally can go higher, but it is equally clear that it will get caught by surprise when the political reality hits home. Second, however, the stock market’s annual returns are roughly average under single-party sweeps during this period (Chart 10). Chart 9Gridlock Best For Markets

The "Normalcy" Rally

The "Normalcy" Rally

Chart 10Single-Party Sweeps Generate Average Annual Returns

The "Normalcy" Rally

The "Normalcy" Rally

So while investors can cheer gridlock, it is not as if they should sell everything if Democrats do win control of the Senate on January 5. Chart 11Sweeps As Good As Gridlock Over 70 Years

The "Normalcy" Rally

The "Normalcy" Rally

Indeed, looking at the period after World War II, sweep governments have witnessed average annual returns that are the same or slightly better than under gridlock (Chart 11). Whereas limiting the study to the post-Reagan era, gridlocks are clearly favored. If greater fiscal resources are needed then gridlock will quickly become a market risk rather than an opportunity. It is notable that over the past 120 years, there is not an example of a Democratic president presiding over a Republican senate and a Democratic House. There was only one case of the inverse – a Republican President, a Democratic senate, and a Republican House – which occurred in 2001-02 and coincided with a bear market. In fact, this episode should be classified as a Republican sweep, as in Table 2, since a sweep was the result of the 2000 election and the context of the key market-relevant legislation in 2001.6 Table 2Average Annual Equity Returns And Gridlock Government

The "Normalcy" Rally

The "Normalcy" Rally

Chart 12Market Predicted Gridlock In 2020

Market Predicted Gridlock In 2020

Market Predicted Gridlock In 2020

In 2020 the stock market clearly anticipated a gridlocked outcome – the market’s performance matches with the historical profile of divided government (Chart 12). We argued that this was the best case for the market because it meant neither right-wing populism nor left-wing socialism. But we also highlighted that any relief rally on election results (reduced uncertainty) would be cut short by the major near-term implication of gridlock: a delay of fiscal support for the economy in the near term. This was the only deflationary scenario on offer in this election. Hence bad news in winter 2020-21 would precede the good news over the entire 2020-22 period. This is still largely our view, but we admit that the vaccine announcement erodes near-term risk aversion even further. There is little substance to the discussion of whether Americans will take the vaccine or not. Evidence shows that Americans are no less likely to take vaccines than other developed country citizens – assuming they are demonstrated to be safe and effective (Chart 13). Chart 13Yes, Americans Take Vaccines

The "Normalcy" Rally

The "Normalcy" Rally

So gridlock looks even better now than it did previously. Yet we still think the near-term fiscal risks will hit markets sometime soon. Senate Republicans have been emboldened by the fact that their relative hawkishness paid off in the election on November 3. If they would not capitulate to House Speaker Nancy Pelosi prior to the election, they are even less likely to do so after gaining seats in the House, retaining the Senate, and crying foul over the presidential election. McConnell could agree to a $500 billion deal before Christmas – or not. There is no clear basis for optimism. A government shutdown is even possible if the continuing resolution expires on December 12. If the economic data turns sour and/or markets sell off dramatically then the Republicans will be forced to agree to a bigger deal, but as things stand they are not forced to do anything. And that presents a downside risk to the normalcy rally. Investment Takeaways Today’s post-election environment is comparable to the period after 2010, when a new business cycle was beginning and a new President Barack Obama had to face down Republican fiscal hawks in the House of Representatives. Today’s GOP senators may prove somewhat more cooperative with President Elect Biden, but that remains to be seen. Given how tight the election was, Republicans have an incentive to obstruct, slow down the economic recovery, and contest the 2022 midterms and 2024 election on the back of another slow-burn recovery. It worked last time. The debt ceiling crises of 2011 and 2012-13 were different than the fiscal stimulus cliff that Washington faces today but the market implications are similar. At the climax of brinkmanship between the president and the senate, treasuries will rally, the dollar will rally, stocks will fall, and emerging markets will underperform (Charts 14A and 14B). Today there is a greater limit on how far the dollar will rise and how far treasury yields will fall, but a fiscal impasse will still drive flows into these assets. Chart 14AObama’s Debt Ceiling Crises…

Obama's Debt Ceiling Crises...

Obama's Debt Ceiling Crises...

Chart 14B… Presage Biden’s Fiscal Cliffs

... Presage Biden's Fiscal Cliffs

... Presage Biden's Fiscal Cliffs

This is what we expect over the next three months. The fact that President Trump could bring negative surprises only enhances this expectation. Therefore we are only gradually adding risk to our strategic portfolio and maintaining tactically defensive positions. Clearly the normalcy rally can go higher, but it is equally clear to us that it will get caught by surprise when the political reality hits home. Since this could be anytime over the next two months, we are only gradually adding new risk. We would not deny that the outlook is brighter over the 12-24-month periods due to the vaccine and election results. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 See Chris Matthews, "Alleging fraud, GOP seeks to overturn election results in Michigan, Pennsylvania," MarketWatch, November 10, 2020, marketwatch.com. 2 See Senator Jake Corman and Representative Kerry Benninghoff, "Pennsylvania lawmakers have no role to play in deciding the presidential election," Centre Daily, October 19, 2020, centredailly.com. As for the 1876 “Stolen Election,” the initial election results suggested that Democrat Samuel Tilden had won 184 electoral votes while Republican Rutherford B. Hayes had won 165. The amount needed for a majority in the Electoral College at the time was 185, so Tilden fell one vote short while Hayes fell 20 votes short. After partisan litigation, actions by state legislatures, an intervention by the US House of Representatives, and a grand political compromise, Hayes won with 185 votes. 3 See Charles Creitz, "McMaster warns Biden on Iran deal: Don't resurrect 'political disaster masquerading as a diplomatic triumph,’" Fox News, November 12, 2020, foxnews.com. 4 In this ruling, which was decided on a 5-4 split with Chief Justice John Roberts siding with liberal justices, the Supreme Court denied the Trump administration’s effort to overturn the Obama administration’s policy known as Deferred Action on Childhood Arrivals (DACA), which stopped the US from deporting illegal immigrants who came to the US as children. The majority opinion argued that the Trump administration had merely asserted, not demonstrated, that the Obama administration’s executive orders were unconstitutional. In doing so, it established a precedent by which the court can determine whether one president’s executive orders should overrule another’s. While future administrations may follow better procedures in attempting to revoke their predecessors’ orders, this decision likely incentivizes the Trump administration to try to issue decrees that will be difficult to revoke. See John Yoo, "How the Supreme Court’s DACA decision harms the Constitution, the presidency, Congress, and the country," American Enterprise Institute, June 22, 2020, aei.org. 5 See Kiran Stacey, “What can Silicon Valley expect from Joe Biden?” Financial Times, November 8, 2020, ft.com. 6 The election produced a Republican sweep, with a 50-50 balance in the Senate, that led to the Bush tax cuts in May 2001. The business cycle was ending, however. In June, Democrats took the senate majority when Republican Senator Jim Jeffords of Vermont became an independent and began caucusing with Democrats. In September terrorists attacked the World Trade Center causing a market collapse.

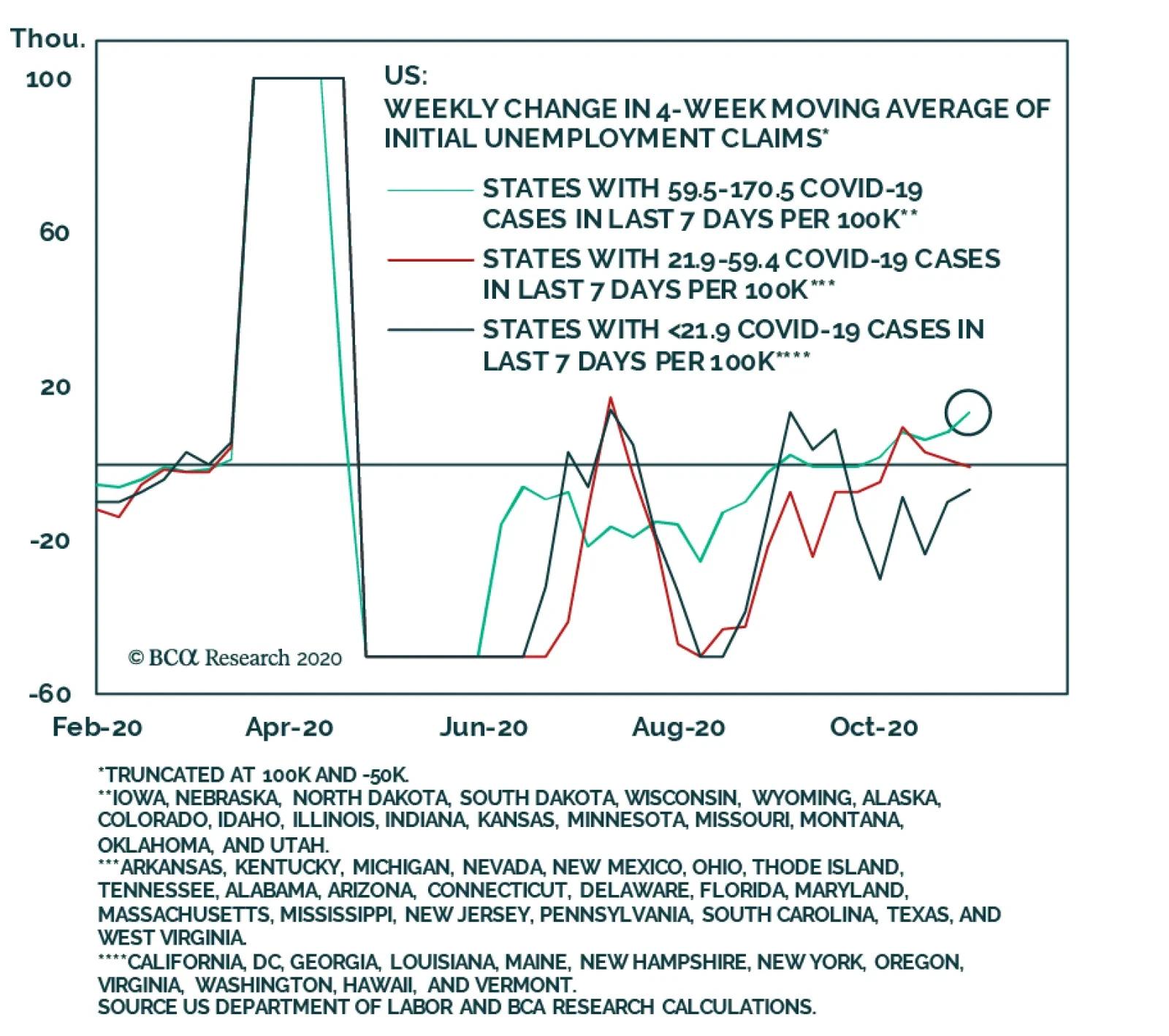

On the surface, this week’s US jobless claims data appear promising. Initial unemployment claims fell by the most in five weeks, coming in at 709 thousand, beating expectations of 731 thousand. Continuing claims declined to 6,786 thousand from 7,222 thousand…

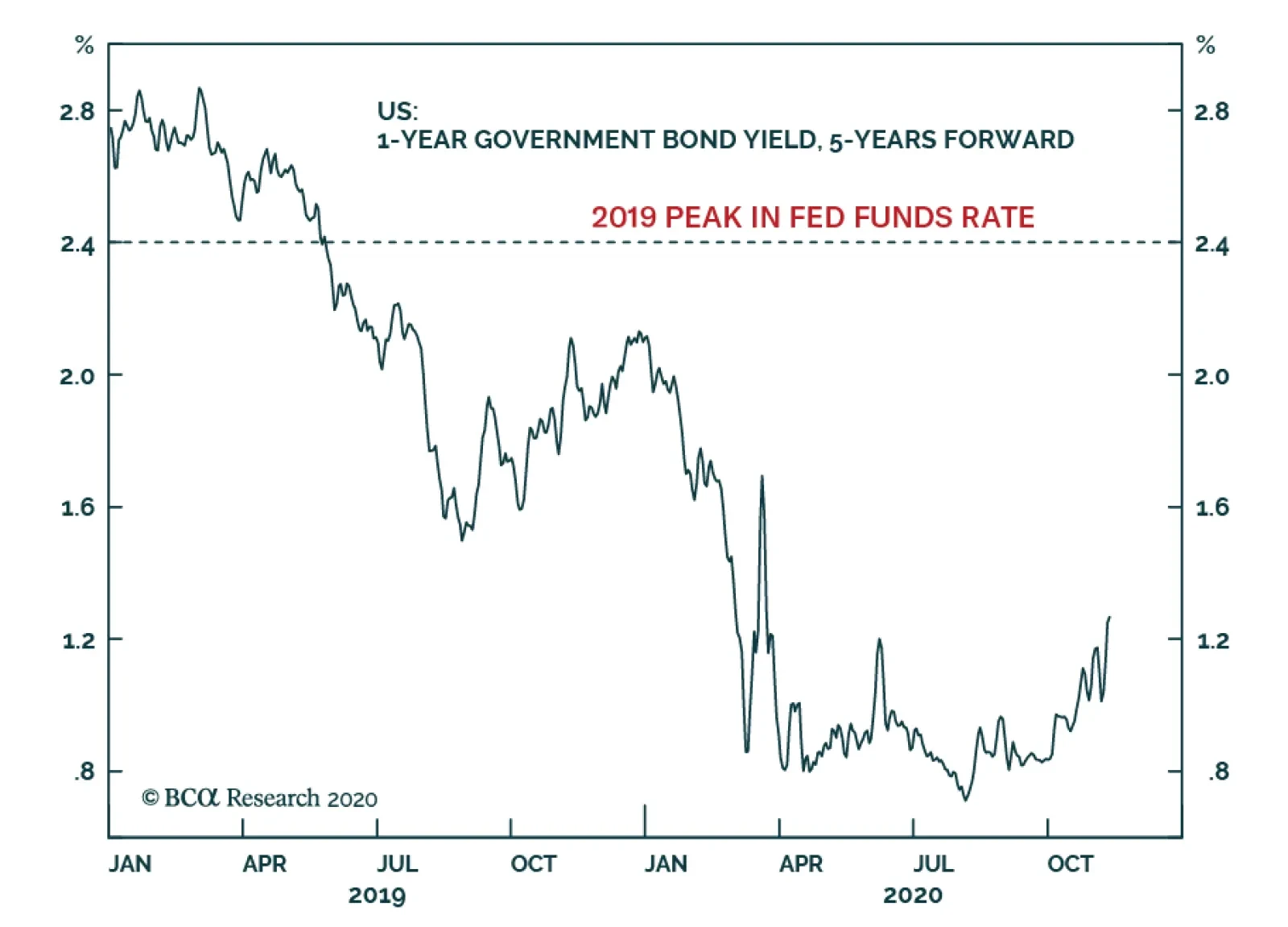

The chart above presents the implied 1-year US government bond yield 5 years from today, which is a proxy for investor expectations of what Fed funds rate will prevail around the middle of the decade. The dotted horizontal line represents the prior cycle peak…

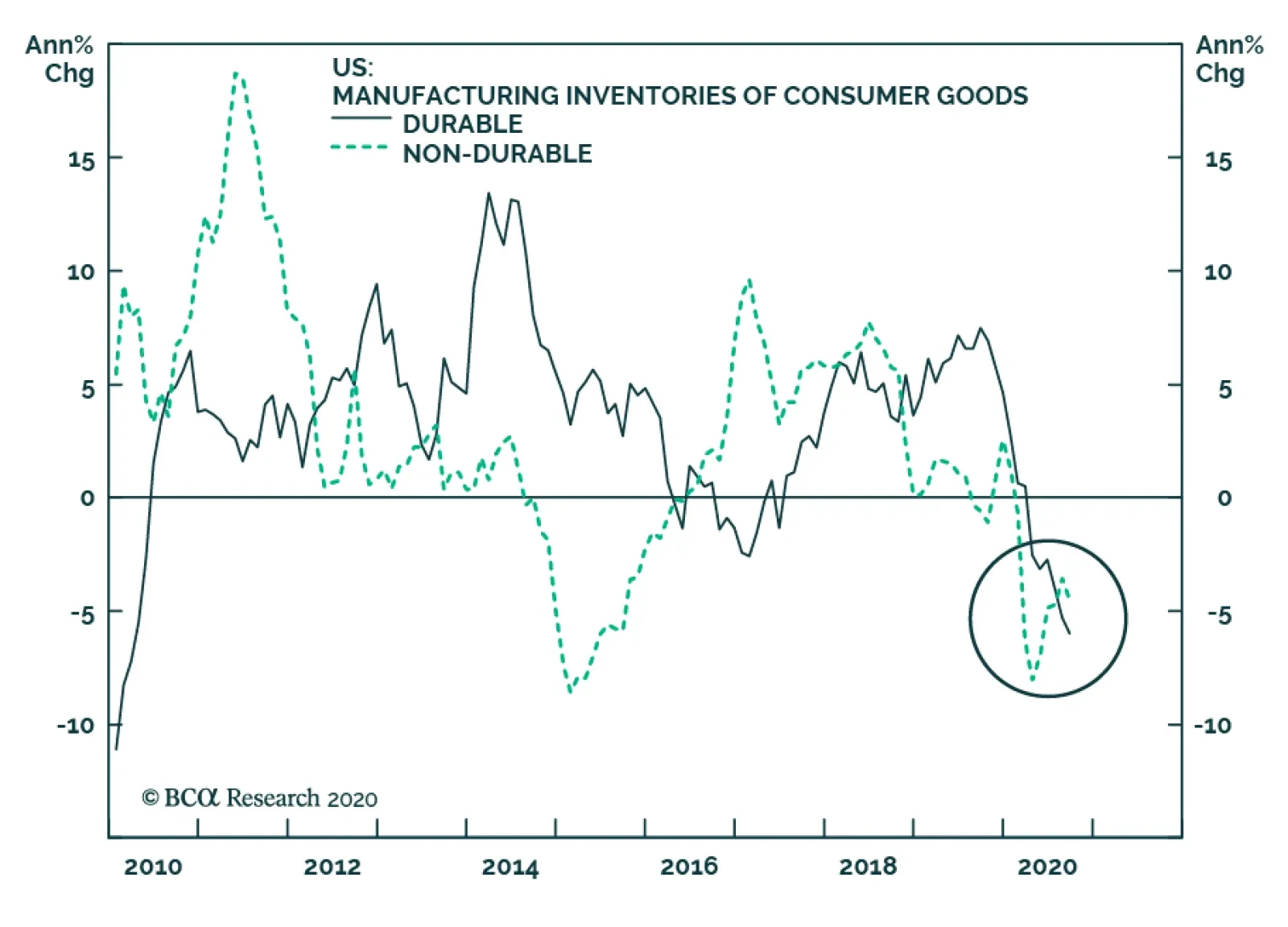

The US manufacturing and services PMIs in October highlighted the relative strength of the former. We noted in a previous Insight that the ISM manufacturing index was surprisingly strong last month, and that the new orders to inventories ratio remained…

Small Caps Have The Upper Hand

Small Caps Have The Upper Hand

The vaccine announcement this week accelerated the unwinding of the long tech short everything else pandemic trade. While such a rotation is augmenting our portfolio via an explicit long “Back To Work”/short “COVID-19 Winners” trade, as we highlighted in yesterday’s Daily US Sector Insight, our small cap size bias is another prime beneficiary. Specifically, small caps outshined large caps by nearly 4% this week. One of the key drivers behind such a quick move is the delta in sector composition between the small and large cap indexes. The relative gap in deep cyclicals alone is 13% as we highlighted in recent research. The implication is that as manufacturing rebounds, so will the relative performance of small caps (top panel). Moreover, easy fiscal policy is a tonic to the small/large share price ratio. As a flood of money enters the economy with a slight lag, small caps will continue to make up ground lost during the early stages of the pandemic (fiscal balance shown inverted, bottom panel). Bottom Line: We reiterate our recent small cap bias.

Highlights US inflation expectations will moderate, and US real yields will rise. This will support the US dollar. The potential rebound in the US dollar will cap any upside in EM ex-TMT stocks. Rising US real yields are a risk to high-multiple global growth stocks. Maintain a neutral allocation to EM in global equity and credit portfolios. Feature In this week’s report we identify market-relevant issues and topics and then present the investment implications of these potential developments. Current key investment-relevant topics and issues are as follows: 1. Implications of the US elections Fiscal Stimulus: In the context of Biden’s victory and the Senate remaining Republican, the odds of a meaningful fiscal package in the next several months are quite low. The Republican Senate did not support a fiscal package going into the elections. Odds are low that it will now agree to a fiscal package larger than $750 billion. Chart 1Rising US Real Yields Are Positive For The US Dollar

Rising US Real Yields Are Positive For The US Dollar

Rising US Real Yields Are Positive For The US Dollar

According to the US Congressional Budget Office’s calculations, without a new fiscal package, the fiscal thrust in 2021 will be -7.5% of GDP or $1.5 trillion. Hence, fiscal stimulus should be more than $1 trillion to avoid a slump in growth. Granted that the recovery in US consumer income and spending that has been underway since April has to a large extent been supported by US fiscal transfers, the lack of current government income support to households poses a risk to the economy. Of course, if US economic activity tanks again and the stock market plunges, Republicans will support a much larger package. However, as things stand now, the probability of a substantial (more than $1 trillion) fiscal package is low. The lack of fiscal stimulus implies that US growth and inflation expectations will moderate. Chart 1 shows that US inflation expectations have probably reached an apex and will downshift for now. US nominal bond yields are capped on the upside (by the Fed’s purchases and its commitment not to raise interest rates for several years) and on the downside (by the Fed’s reluctance to reach negative interest rates). Consequently, swings in inflation expectations will drive fluctuations in real yields, as has been occurring in recent months. As inflation expectations decline, real yields will rise. Impact of rising US real yields on financial markets: A stronger US dollar and lower prices for Nasdaq stocks. Rising real rates will support the US dollar (Chart 1, bottom panel). Chart 5 on page 5 reveals that the real rates differential between the US and the euro area has recently been moving in favor of the greenback. Chart 2Rising US Real Yields Are Negative For Growth Stocks

Rising US Real Yields Are Negative For Growth Stocks

Rising US Real Yields Are Negative For Growth Stocks

Budding investor realization that the US might not pursue an aggressively expansionary fiscal policy, as has been expected since spring, could also support the greenback. Less issuance of Treasury securities might be interpreted as less public debt monetization and less money creation by the Federal Reserve. Such a viewpoint will also be marginally positive for the US dollar. As to the equity market, US real (TIPS) yields have been negatively correlated with the Nasdaq index (Chart 2). As US real yields continue to rise, odds are that global growth stocks will come under selling pressure. Geopolitical ramifications: The impact of the forthcoming change in the White House on US foreign policy has been widely anticipated and has already been priced in by financial markets. A Biden administration will have a positive impact on the euro area, Canada, Mexico and Asia Pacific countries with the exception of China – as was not the case under the Trump administration. On the other end, Russia, Turkey and Saudi Arabia will be under heat from Biden’s White House. In our view, the impact on China will be neutral, not better than during Trump’s administration. It might be mildly positive in the near term but negative in the long run. In the short run, the new US administration will be less likely to use global trade as a weapon. In the long run, however, Biden will likely mobilize Europe to join its geopolitical confrontation with China. This will be negative for the Middle Kingdom. One country where the impact of Biden’s administration has not been fully priced in is Brazil. The US executive branch will take a tougher stance in its dealings with Brazil’s right-wing government because their social values are not aligned and policy priorities differ. We remain short the BRL and underweight Brazilian equity and fixed-income markets within their respective EM portfolios. 2. Vaccines We have no better expertise than the market’s judgement on the timing of vaccine availability and its effectiveness in containing the pandemic in EM ex-China countries. It is clear, however, that the process of vaccine acquisition and distribution might be slower in EM ex-China than in advanced countries. On all three fronts – the spread of the pandemic, policy stimulus and vaccine distribution – EM excluding China, Korea and Taiwan will continue lagging DM. Therefore, EM ex-China domestic demand will continue to underperform relative to expectations and versus those in DM. This argues for continuous underweight, or at best a neutral allocation, in EM ex-China, Korea and Taiwan equities versus their DM peers. Chart 3Chinese Onshore Equities Have Been In A Trading Range Since Early July

Chinese Onshore Equities Have Been In A Trading Range Since Early July

Chinese Onshore Equities Have Been In A Trading Range Since Early July

3. China: the business cycle and regulatory clampdown China’s business cycle recovery has further to go. The stimulus injected into the economy has been considerable and will continue to work its way into the economy. Even though we believe that China has reached peak stimulus, the latter works with a time lag of 6-12 months and economic growth will top only around mid-2021. That said, Chinese onshore share prices have been in a consolidation phase since early July and this is likely not over yet (Chart 3). In turn, Chinese investable stocks have been surging in absolute terms and outperforming the global equity index (Chart 4, top panel). However, the entire Chinese equity outperformance has been due to growth stocks (TMT/new economy). Excluding these, the absolute and relative performance of Chinese investable stocks has been lackluster (Chart 4, top and bottom panels). Chart 4Chinese Investable Stocks: Surging TMT And Lackluster Performance By Ex-TMT Stocks

Chinese Investable Stocks: Surging TMT And Lackluster Performance By Ex-TMT Stocks

Chinese Investable Stocks: Surging TMT And Lackluster Performance By Ex-TMT Stocks

In short, the spectacular performance of Chinese investable stocks this year has been attributed to three new economy stocks: Alibaba, Tencent and Meituan. These three stocks presently account for 40.5% of China’s MSCI Investable Index and 17.5% of the aggregate EM MSCI equity index. Concerns about regulatory clampdowns on new economy stocks have been, and remain, a major risk, not only in China but also in advanced economies. It is impossible to time regulatory actions. Nevertheless, investors should take into account the possibility that regulation may curb the profitability of new economy companies, especially if they are de-facto monopolies or oligopolies. Chinese authorities will not back down from imposing new regulation and scrutiny over the activities of giant new economy companies. Hence, risks of further de-rating remain elevated. In short, even though the mainland business cycle recovery is on a track, Chinese share prices remain at risk of correction due to overbought conditions and re-pricing of regulatory risks for new economy stocks. Will The US Dollar Capture Some Of Its Luster? US real yields are rising not only in absolute terms, but also relative to real yields in the euro area (Chart 5). Rising real yields in the US versus the euro area generally lead to a dollar rally against the euro. Apart from rising US real bond yields, there are a number of other factors that will likely support the greenback: Investor sentiment on the US dollar is very low (Chart 6). From a contrarian perspective, this is positive. Chart 5The US Versus Euro Area: Real Yield Differentials And Exchange Rate

The US Versus Euro Area: Real Yield Differentials And Exchange Rate

The US Versus Euro Area: Real Yield Differentials And Exchange Rate

Chart 6Investors Are Downbeat On The US Dollar

Investors Are Downbeat On The US Dollar

Investors Are Downbeat On The US Dollar

Consistently, investors are very short the US dollar, especially versus DM currencies (Charts 7and 8). Positioning is less short in the US dollar versus cyclical DM and high-beta EM currencies (Chart 8). That said, the fundamentals of EM high-beta currencies such as BRL, TRY, ZAR and IDR are poor. Chart 7Investors Are Very Long Safe-Haven Currencies…

Investors Are Very Long Safe-Haven Currencies...

Investors Are Very Long Safe-Haven Currencies...

Chart 8...And Modestly Long Cyclical Currencies

...And Modestly Long Cyclical Currencies

...And Modestly Long Cyclical Currencies

The Republican Senate will block corporate tax increases and limit any regulatory initiatives by Democrats in Congress. Such business-friendly policies are currency bullish. In short, a Republican Senate is broadly positive for the US dollar, and markets have not priced it in. The fact that broad US equity averages – such as small caps and equal-weighted equity indexes – continue outperforming the rest of the world in local currency terms is also dollar bullish (Chart 9). The reasoning is that US equity outperformance versus the rest of the world suggests better profitability and return on capital in the US versus its peers. That favors a firmer US dollar. Finally, the broad-trade weighted US dollar is oversold and is sitting on a long-term technical resistance level (Chart 10). Chart 9US Relative Equity Outperformance Heralds A Stronger US Dollar

US Relative Equity Outperformance Heralds A Stronger US Dollar

US Relative Equity Outperformance Heralds A Stronger US Dollar

Chart 10The US Dollar Is Very Oversold

The US Dollar Is Very Oversold

The US Dollar Is Very Oversold

Bottom Line: We have been highlighting downside risks to the US dollar since July 9. However, the conclusion of the US election raises the odds of a playable US dollar rebound. EM Strategy EM Equities We have been advocating for a neutral allocation toward EM in a global equity portfolio since July 30. If the US dollar rebounds, as we expect, EM stocks will not outperform the global equity index (Chart 11). Notably, excluding Chinese investable stocks, EM share prices have not outperformed the global benchmark (Chart 12). Besides, as shown in the top panel of Chart 4 on page 4, China’s outperformance against the global equity benchmark has been driven exclusively by new economy stocks. Chart 11EM Stocks Do Not Outperform When The Dollar Rallies

EM Stocks Do Not Outperform When The Dollar Rallies

EM Stocks Do Not Outperform When The Dollar Rallies

Chart 12EM Versus Global Equity Performance: With And Without China

EM Versus Global Equity Performance: With and Without China

EM Versus Global Equity Performance: With and Without China

All in all, Charts 4 and 12 reveal that excluding three large Chinese new economy stocks – Alibaba, Tencent and Meituan – EM share prices have underperformed the global equity benchmark. Going forward, the potential rebound in the US dollar will cap any upside in EM ex-TMT stocks. Meanwhile, the correction in the NASDAQ and the increased scrutiny on the part of Chinese authorities over new economy stocks poses a risk to Chinese mega-cap TMT share prices. In absolute terms, we have been waiting for a pullback to buy EM equities, but they have surged following the US elections and the news on Pfizer’s vaccine. Chart 13EM Equity Index: No Breakout Yet

EM Equity Index: No Breakout Yet

EM Equity Index: No Breakout Yet

The EM equity index could still advance and reach its 2011 or 2018 highs before rolling over (Chart 13). However, given our view on the US currency and risks to EM stemming from a rising US dollar, we refrain from playing such limited upside. EM currencies EM currencies will be at a risk if the US dollar stages a rebound. Since July 9, we have been shorting a basket of BRL, CLP, TRY, KRW, ZAR and IDR versus an equally-weighted basket of the euro, CHF and JPY. We are sticking with this strategy. Even if the US dollar rebounds, downsides in the euro, CHF and JPY against the greenback will be relatively limited. However, investors might consider adding the US dollar to the long side of this strategy. EM local bonds and EM credit markets We continue recommending long duration in EM local rates. However, we remain reluctant to take on currency risk. We maintain our recommendations from April 23 about receiving 10-year swap rates in Mexico, Colombia, Russia, India, China and Korea. We are also receiving 2-year rates in Malaysia and South Africa as a bet on rate cuts in these economies. In the EM credit space, we are also neutral. Our sovereign credit overweights are Mexico, Colombia, Peru, Russia, Thailand, Malaysia and the Philippines. Our underweights are South Africa, Turkey, Indonesia, Argentina and Brazil. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

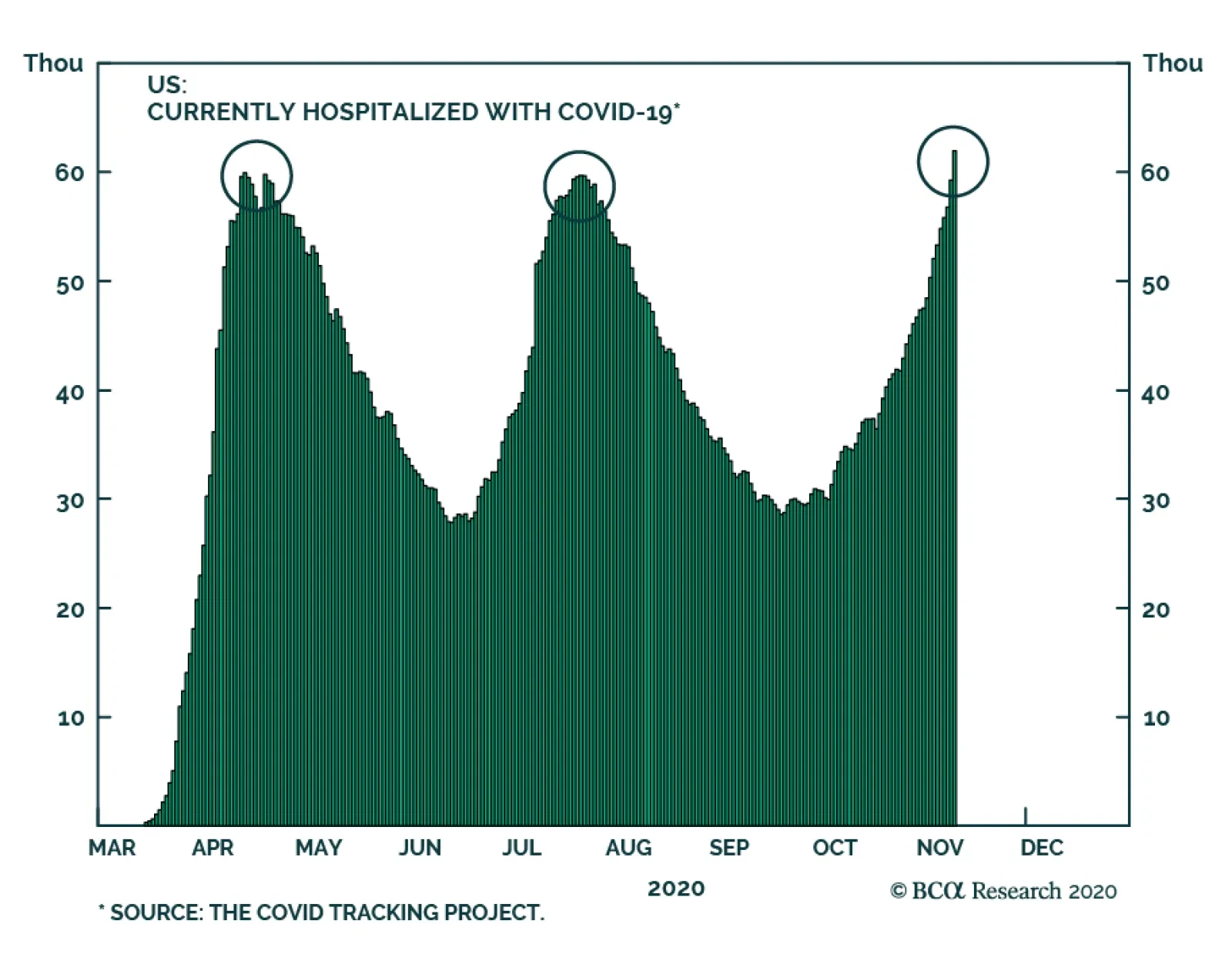

Since the onset of the COVID-19 pandemic, global investors have become accustomed to tracking new case counts as a leading indicator of both consumer spending and the likely response of policymakers. While the pace of infection is an extremely important…

Back To Work Trade Is On Fire

Back To Work Trade Is On Fire

Yesterday’s vaccine news reawakened investors to the reality that the world might be going back to normality much sooner than previously anticipated unleashing a violent equity rotation. Perhaps one of the most illustrative examples is the one-day percentage change in our “Back To Work” and “COVID-19 Winners” baskets. The top and middle panels of the chart on the right highlight the point: 7/14 stocks in the “Back To Work” basket experienced more than a 10% increase with AXP leading the pack with a mighty 21% rise. On the other side, pandemic beneficiaries got clobbered with ZM losing 17% of its value. As a reminder, we have been recommending being long our “Back To Work” basket at the expense of the “COVID-19 Winners” basket since early September, and this trade is currently up 15% since inception. Importantly, the economic normalization process has just begun and according to the ISM manufacturing PMI new orders sub-category there is likely a long runway ahead for this pair trade (bottom panel). Bottom Line: Stick with the long “Back To Work” basket / short “COVID-19 Winners” basket, but recent market action is enticing us to put a trailing stop at the 10% return mark in order to protect profits.

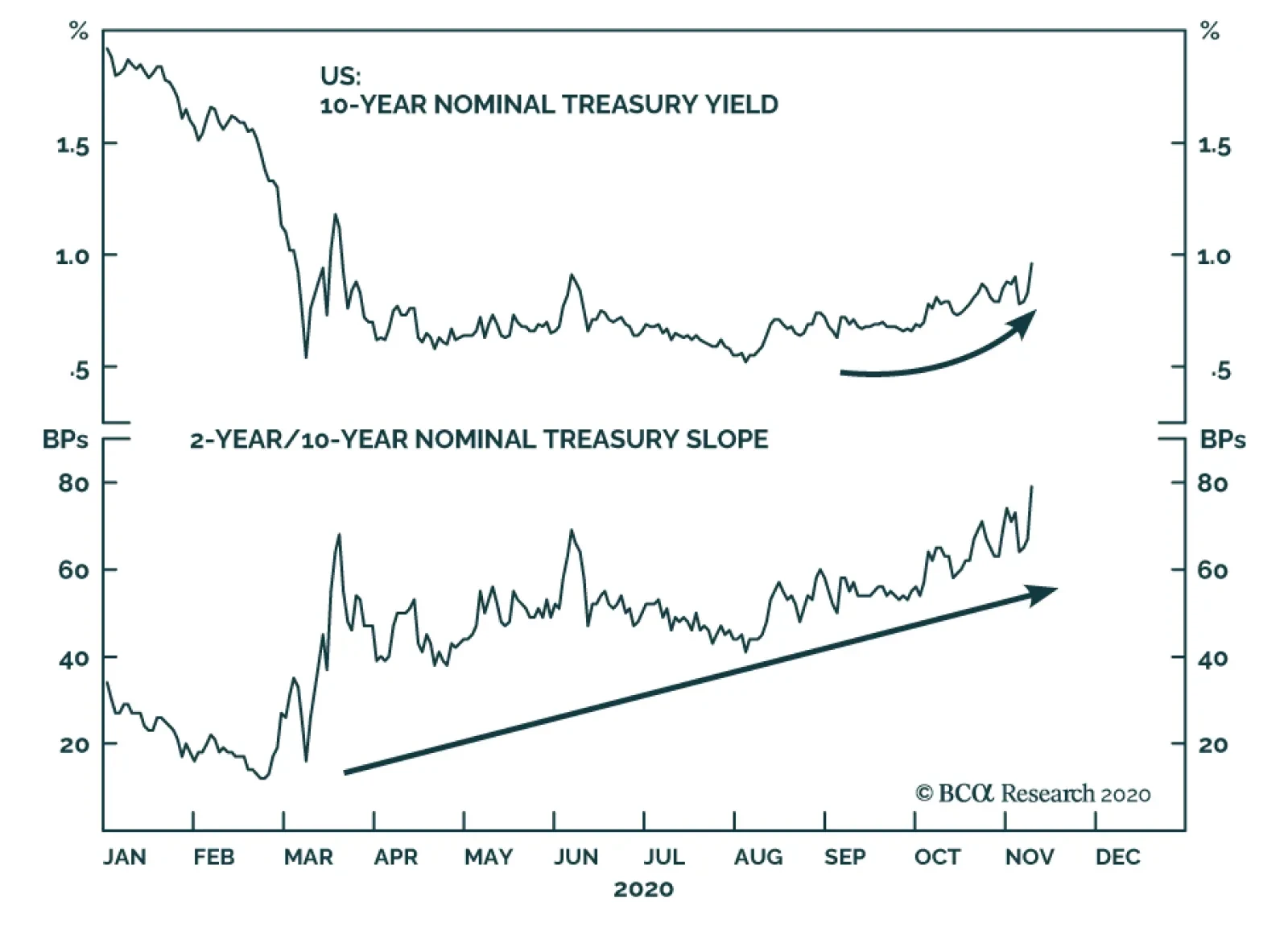

BCA Research's US Bond Strategy service concludes that a moderate bear-steepening of the Treasury curve remains the most likely outcome for the next 6-to-12 months. Of course, the outlook is somewhat clouded by the fact that the dust has not completely…

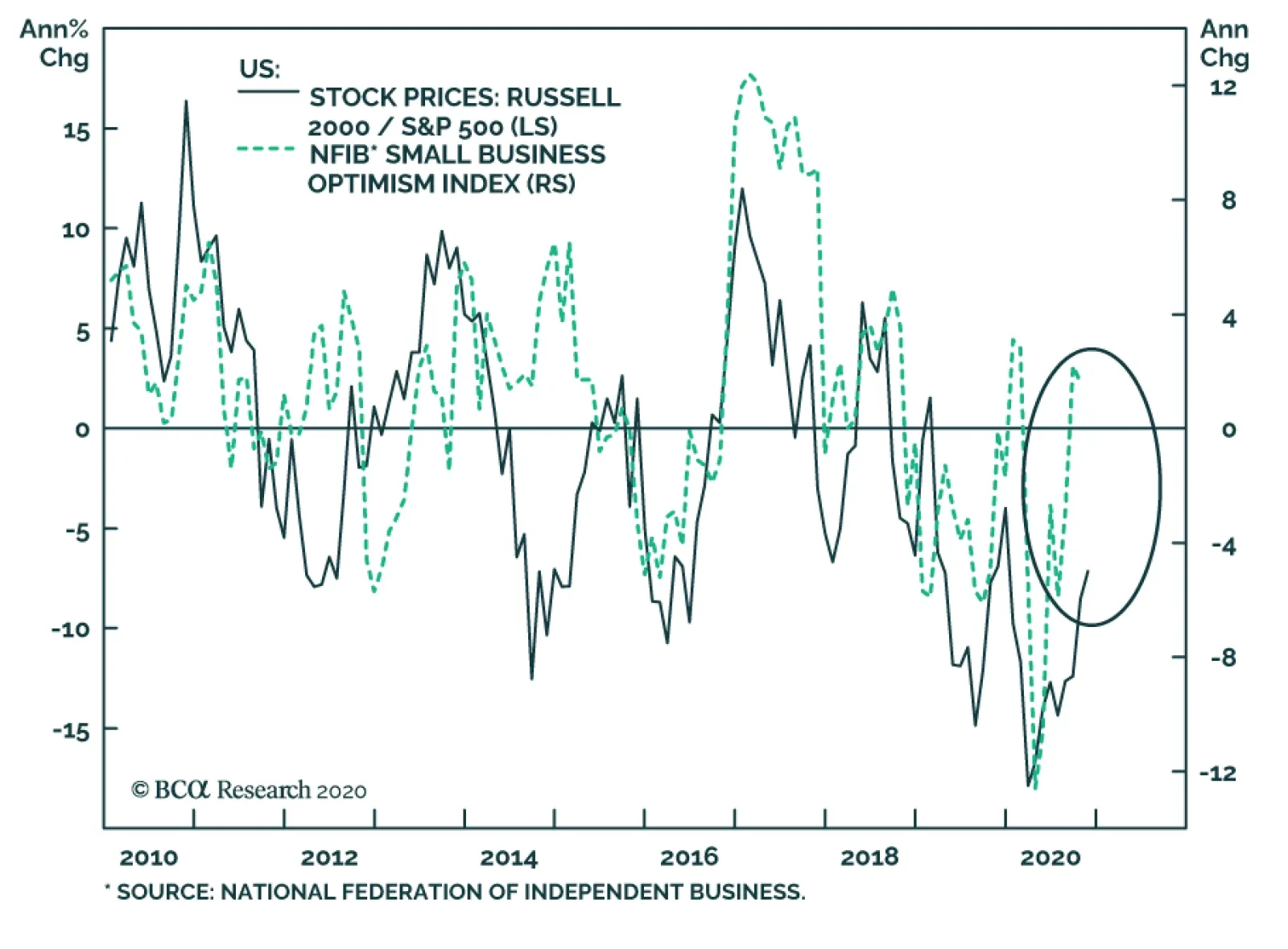

Yesterday’s NFIB Small Business Optimism Index was positive news for US small cap stocks. The overall index was unchanged in October, but remained at a very elevated level relative to its history. Five of the ten index subcomponents declined in October,…