United States

Last week, global equities recorded their strongest weekly gains since July, the dollar fell significantly and 10-year Treasury yields rose to their highest level since June. All of this happened while cacophony in Washington increased dramatically and the…

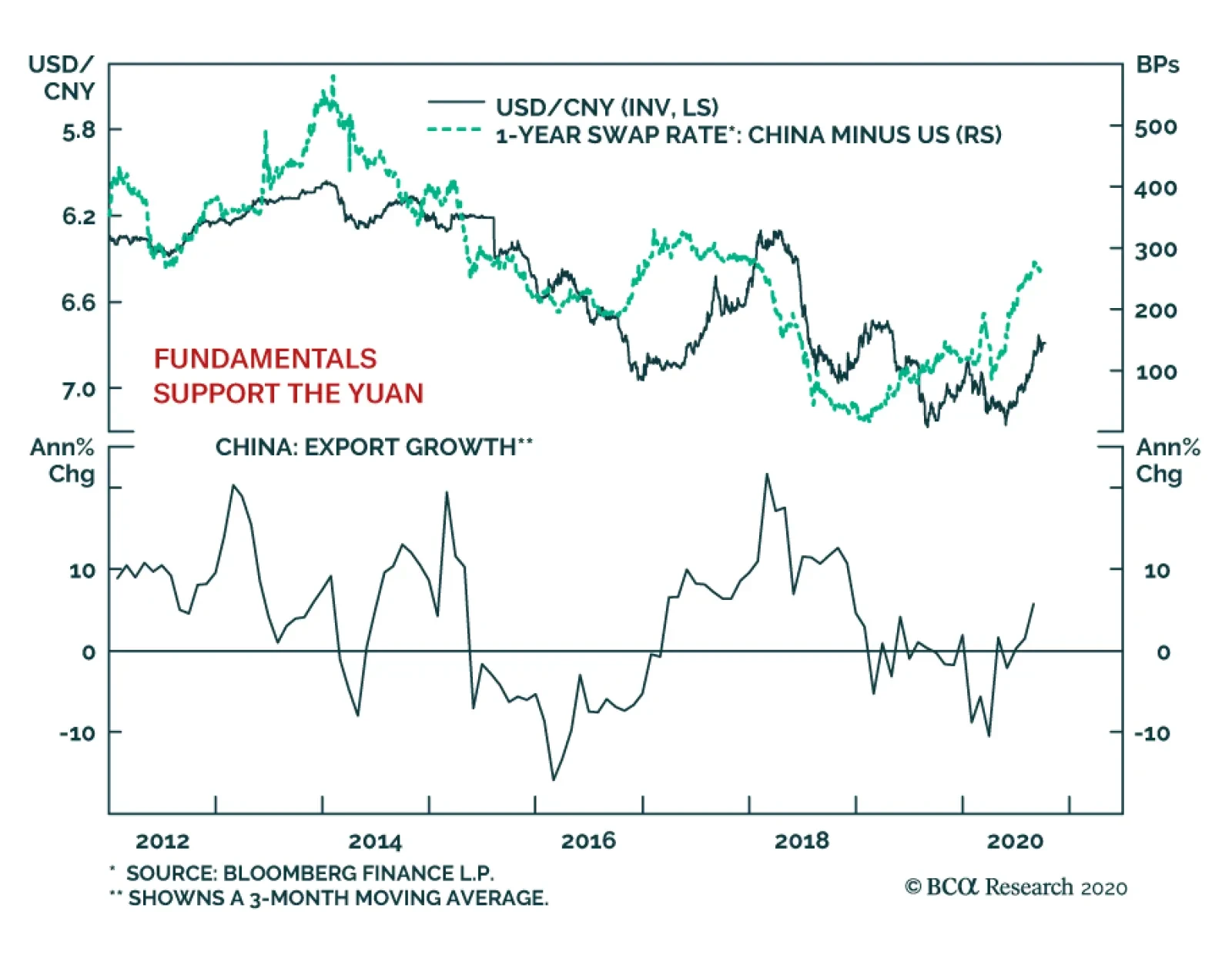

Since May 27, the onshore CNY has appreciated more than 7% against the USD and it trades at levels last seen in April 2019, just prior to the imposition of additional tariffs by the Trump administration on US$250 billion of Chinese exports to the US. A few…

Buybacks Will Be Back

Buybacks Will Be Back

Most recent Standard and Poor’s data show that SPX buybacks collapsed to $88bn in Q2, from roughly $200bn in Q1, which is a whopping 67% quarter-over-quarter fall. Such a corporate buyer’s strike is negative for the near-term prospects of the S&P 500, but we expect buybacks to come back as the V-shaped economic recovery all but guarantees a rebound sometime in 2021 (top panel). Importantly, CEO confidence has also slingshot higher and coupled with the overall economic recovery, will pave the way for a resumption of shareholder friendly activities (middle panel). Bottom Line: Artificial EPS boosting via equity retirement will come back in 2021, especially in light of the ZIRP that is here to stay for the next five-seven years. For more details, please refer to this Monday’s Weekly Report.

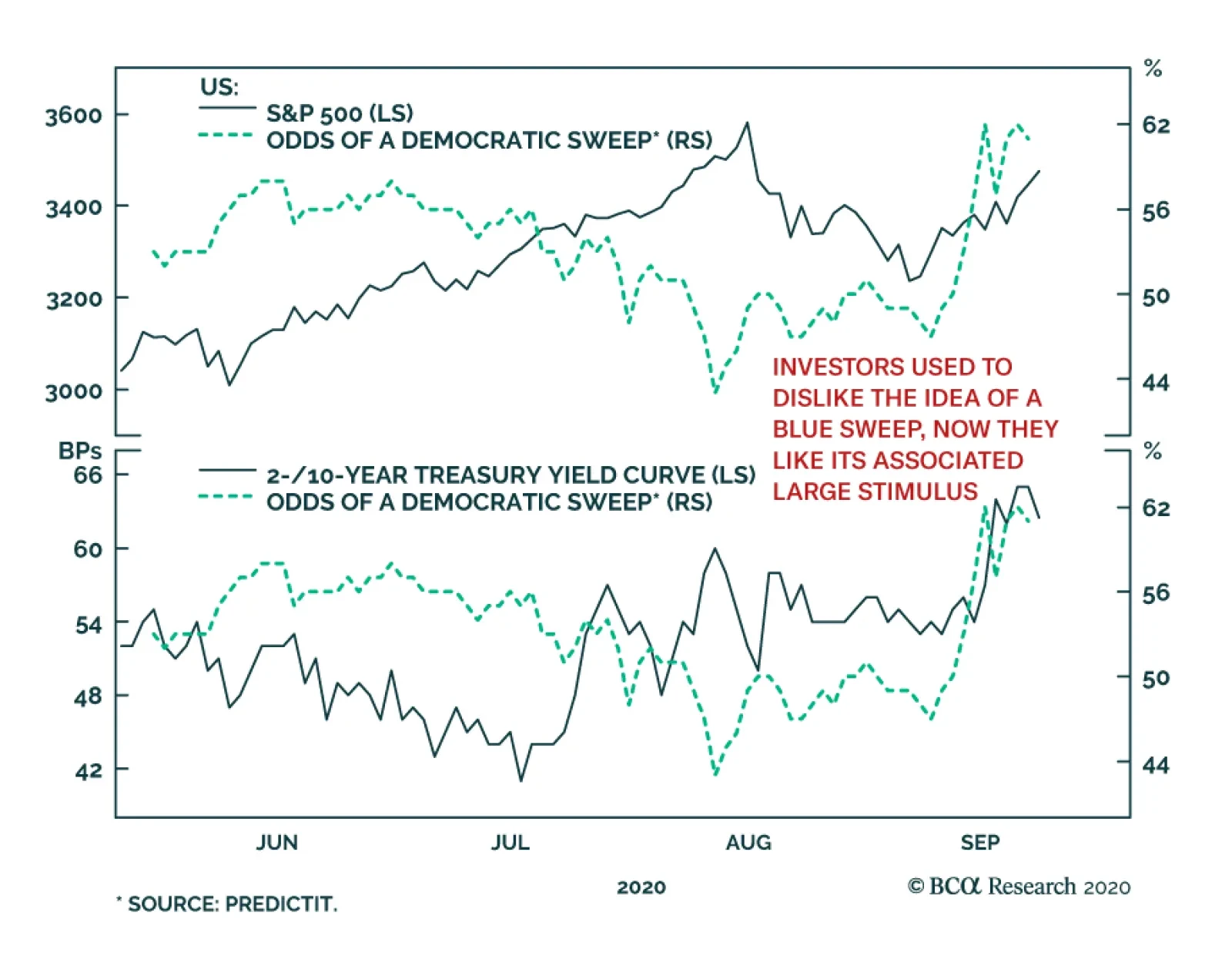

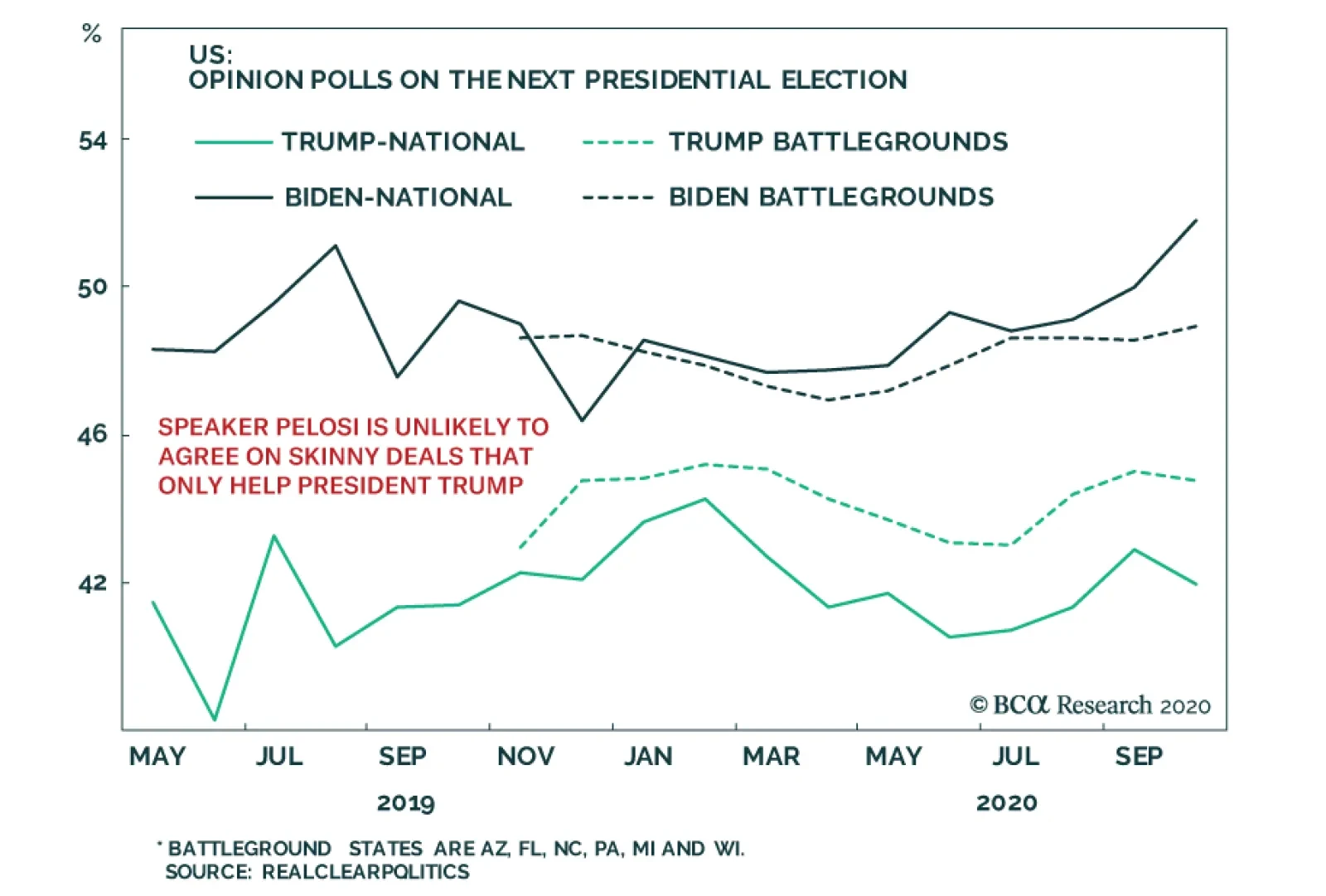

Highlights Both public opinion polls and betting markets suggest that Joe Biden will become President, with the Democrats gaining control of the Senate and retaining the House of Representatives. Such a “blue wave” would have mixed effects on the value of the S&P 500. On the one hand, corporate taxes would rise under a Biden administration. On the other hand, trade relations with China would improve. The Democrats would also push for more fiscal stimulus, which the stock market would welcome. The odds of Republicans and Democrats agreeing on a major new stimulus deal before the November elections look increasingly slim. In a blue wave scenario, the Democrats will enact $2.5-to-$3.5 trillion in pandemic relief shortly after Inauguration Day. Joe Biden‘s platform also calls for around 3% of GDP in additional spending on infrastructure, health care, education, climate, housing, and other Democratic priorities. Unlike in late 2016, the Fed is in no mood to raise interest rates. Large-scale fiscal easing will push down the value of the US dollar, while giving bond yields a modest boost. Non-US stocks will outperform their US peers. Value stocks will outperform growth stocks. Looking further out, Republicans will move to the left on economic issues, leaving corporate America with no clear backer among the two major parties. As such, while we are constructive on equities over the next 12 months, we see grave dangers ahead later this decade. Look, Here's The Deal: Joe Biden Is In The Lead With four weeks remaining until the US presidential election, Joe Biden remains on course to become the 46th president of the United States. According to recent public opinion polls, the former vice president leads Donald Trump by 10 percentage points nationwide, and by 4 points in battleground states (Chart 1). Far fewer voters are undecided today compared to 2016. This suggests that there is less scope for President Trump to narrow his deficit in the polls. Betting markets give Biden a 68% chance of prevailing in the race for the White House (Chart 2). They also assign a 67% probability that the Democrats will take control of the Senate and 89% odds that they will retain their majority in the House of Representatives. Chart 1Opinion Polls Favor Biden ...

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Chart 2.... As Do Betting Markets

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Mixed Impact On The S&P 500 What would the market implications of a “blue wave” be? Our sense is that the overall impact on the value of the S&P 500 would be small, largely because some negative repercussions from a Democratic sweep would be offset by positive repercussions. On the negative side, Biden has pledged to raise the corporate income tax rate from 21% to 28%, bringing it halfway back to the 35% rate that prevailed in 2017. He has also promised to introduce a minimum of 15% tax on the income that companies report in their financial statements to shareholders, raise taxes on overseas profits, and lift payroll taxes on households with annual earnings in excess of $400,000. Together, these measures would reduce S&P 500 earnings-per-share by 9%-to-10%. On the positive side, while geopolitical tensions will persist, US trade relations with China would likely improve if Joe Biden were to become the president. Biden has roundly criticized Trump’s tariffs, saying that they are “crushing farmers” and “hitting a lot of American manufacturing… choking it to within an inch of its life.”1 He has pledged to honor multilateral agreements. The World Trade Organization concluded on September 15 that Trump’s tariffs violated international trade rules. This judgement and the desire to turn the page on the Trump era could give Biden the impetus to eventually roll back some of the tariffs. In contrast, having been stricken by what he has called the “China virus,” Trump could take things personally and retaliate with a flurry of new punitive measures. Fiscal policy would be further loosened in a blue wave scenario, an outcome that the stock market would welcome. Voters would also applaud more pandemic relief. Table 1 shows that 72% of Americans, including the majority of Republicans, support the broader contours of the $2 trillion stimulus package that President Trump has rejected. Table 1Voters Support A New $2 Trillion Coronavirus Stimulus Package By A Fairly Wide Margin

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

At this point, the odds of Republicans and Democrats agreeing on a major new stimulus deal before the November elections look increasingly slim. If Biden wins and the Republicans lose control of the senate, the Democrats would likely enact a stimulus package worth $2.5-to-$3.5 trillion shortly after Inauguration Day on January 20. In addition to pandemic-related stimulus, Joe Biden has called for around 3% of GDP in spending on infrastructure, health care, education, climate, housing, and other Democratic priorities. Only about half of those expenditures would be matched by higher taxes, implying substantial net stimulus for the economy. A Weaker Dollar And Modestly Higher Bond Yields The greenback jumped on Tuesday after President Trump said he is breaking off negotiations with the Democrats over a new stimulus bill. This suggests that the dollar will weaken if fiscal policy is loosened. If that were to happen, it would be different from what transpired following Trump’s victory in 2016 when the dollar strengthened. Why the disconnect between now and then? The answer has to do with the outlook for monetary policy. Back then, the Fed was primed to start raising rates again – it hiked rates eight times beginning in December 2016, ultimately bringing the fed funds rate to 2.5% by end-2018 (Chart 3). This time around, the Fed is firmly on hold, with the vast majority of FOMC members expecting policy rates to stay at rock-bottom levels until at least 2023. This suggests that nominal bond yields will rise less than they did in late 2016. Since inflation expectations will likely move up in response to more stimulative fiscal policy, real yields will rise even less than nominal yields. Over the past 18 months, US real rates have fallen a lot more in relation to rates abroad than what one would have expected based on the fairly modest depreciation in the US dollar (Chart 4). If US real rates remain entrenched deep in negative territory, while the US current account deficit widens further on the back of strong domestic demand, the dollar will continue to weaken. Chart 3Trump Victory Was Followed By Rising Interest Rates

Trump Victory Was Followed By Rising Interest Rates

Trump Victory Was Followed By Rising Interest Rates

Chart 4A Relatively Muted Decline In The Dollar Given The Move In Real Yield Differentials

A Relatively Muted Decline In The Dollar Given The Move In Real Yield Differentials

A Relatively Muted Decline In The Dollar Given The Move In Real Yield Differentials

Favor Non-US And Value Stocks Non-US stocks typically outperform their US peers when the dollar is weakening (Chart 5). This partly stems from the fact that cyclical stocks are overrepresented in stock markets outside of the United States. It also reflects the fact that cash flows denominated in say, euros or yen, are worth more in dollars if the value of the dollar declines. Chart 5A Weaker Dollar Tends To Benefit Cyclical And Non-US Stocks

A Weaker Dollar Tends To Benefit Cyclical And Non-US Stocks

A Weaker Dollar Tends To Benefit Cyclical And Non-US Stocks

Financial stocks are overrepresented outside the US (Table 2). They are also overrepresented in value indices (Table 3). While a Biden administration would subject the largest US banks to additional regulatory scrutiny, the impact on their bottom lines would likely be small. US banks have been living under the shadows of the Dodd-Frank Act for over a decade. Today, banks operate more as stable utilities than as cavalier casinos. Table 2Financials Are Overrepresented In Ex-US Indexes, While Tech Dominates The US Market

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Table 3Financials Are Overrepresented In Value, While Tech Dominates Growth Indexes

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Stronger stimulus-induced growth next year will allow many banks to release some of the hefty provisions against bad loans that they built up this year, while modestly steeper yields curves will boost net interest margins. Tech stocks are overrepresented in growth indices. Better trade relations would help US tech companies, as would a weaker dollar. That said, Joe Biden’s plan to increase taxes on overseas profits would hit tech companies disproportionately hard since the tech sector derives over half its revenue from outside the United States. Stepped up antitrust enforcement and more stringent privacy rules could also weigh on tech profits. On balance, while there are many moving parts, a Democratic sweep would favor non-US equities over US equities, and value stocks over growth stocks. Trumpism Transcends Trump Chart 6Trump Targeted Socially Conservative Voters

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

In 2016, we bucked the consensus view that Hillary Clinton would win the election. On September 30, 2016, we predicted that “Trump will win and the dollar will rally,” noting that “Trump has seen a huge (yuge?) increase in support among working-class whites. If the so-called “likely voters” backing Clinton are, in fact, less likely to turn out at the polls than those backing Trump, this could skew the final outcome in Trump's favor.”2 Right-wing populism was the $1 trillion bill lying on the sidewalk that no mainstream Republican politician seemed eager to pick up. According to the Voter Study Group, only 4% of the US electorate identified as socially liberal and fiscally conservative in 2016, compared to 29% who saw themselves as fiscally liberal and socially conservative (Chart 6). The latter group had no political home, at least until Donald Trump came along. Rather than waxing poetically about small government conservatism – as most establishment Republicans were wont to do – Trump railed against mass immigration, unfair trade deals, rising crime, never-ending wars, and what he described as out-of-control political correctness. While Trump was able to carry out parts of his protectionist agenda, most of his other actions fell well short of what he had promised. His only major legislative achievement was a massive tax cut for corporations and wealthy individuals – something that the vast majority of his base never asked for. The Rich Are Flocking To The Democratic Party How did corporations and wealthy Americans reward Trump for lowering their taxes? By shifting their allegiances towards the Democrats, that’s how. According to the Pew Research Center, households earning more than $150,000 favored Democrats by 20 percentage points during the 2018 Congressional elections, a 13-point jump from 2016. Households earning between $30,000 and $149,999 favored Democrats by only 6 points in 2018. The only other income group that strongly favored Democrats were those earning less than $30,000 per year (Table 4). Table 4Democratic Candidates Had Wide Advantages Among The Highest-And-Lowest Income Voters

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Chart 7Democratic Districts Have Fared Better Over The Past Decade

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Other data tell a similar story. Median household income in Democratic congressional districts rose by 13% between 2008 and 2017. It fell by 4% in Republican districts. Today, on average, Republican districts have a median income that is 13% below Democratic districts (Chart 7). Campaign donations have shifted towards the Democrats. The latest monthly fundraising data shows that the Biden campaign received three times more large-dollar contributions in total than the Trump campaign. The nation’s CEOs have not been immune from this transformation. Seventy-seven percent of the business leaders surveyed by the Yale School of Management on September 23 said they would be voting for Joe Biden.3 As elites desert the Republican Party, will the Democratic Party start championing lower taxes and less regulation? That seems unlikely. According to the Voter Study Group, higher-income Democrats are actually more likely to support raising taxes on families earning more than $200,000 per year than lower-income Democrats (83% versus 79%). Among Republicans, the opposite is true: 45% of lower-income Republicans are in favor of raising taxes, compared to only 23% of higher-income Republicans.4 There used to be a time when companies tried to steer clear of the political limelight. This is starting to change. As the relative purchasing power of Democratic voters has risen, many companies have become emboldened to adopt overtly political stances on a variety of hot-button social and cultural issues, even if those stances alienate many conservative customers. What does this imply for investors? If big business abandons conservative voters, conservative voters will abandon big business. Corporate America will be left with no clear backer among the two major parties. Over the long haul, this is likely to be bad news for equity investors. As such, while we are constructive on equities over the next 12 months, we see grave dangers ahead later this decade. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 “Biden Takes On ‘Trump’s Tariffs’,” The Wall Street Journal, June 12, 2019. 2 Please see Global Investment Strategy Special Report, “Three (New) Controversial Calls,” dated September 30, 2016. 3 “CEO Caucus Survey: Business Leaders Fault Trump Administration on COVID and China,” Yale School of Management, September 24, 2020. 4 Lee Drutman, Vanessa Williamson, Felicia Wong, “On the Money: How Americans’ Economic Views Define — and Defy — Party Lines,” votersstudygroup.org, June 2019. Global Investment Strategy View Matrix

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Current MacroQuant Model Scores

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Highlights President Trump is waffling on fiscal relief. Our constraints-based framework still points to a deal, but the odds have clearly fallen. US and global stocks have rallied despite the fiscal failure. Markets evidently believe stimulus is coming regardless, particularly if Democrats win a blue sweep – our base case election scenario. However, our quantitative election model has boosted Republican odds, flagging a major risk to the blue sweep scenario. Moreover a blue sweep will remove checks and balances on the new administration and thus bring negative surprises that the market is underrating. We maintain our tactical risk-off positioning on the expectation of another leg of election-related volatility. Over a 12-month time horizon we remain invested in reflation plays. Feature Financial markets came around to our “blue sweep” base case for the US election this week. Betting markets shifted sharply after the first presidential debate (Chart 1). Support for Biden surged in national opinion polls while Trump dropped off, albeit to a lesser extent in swing states. Worryingly for the White House, the few polls taken since Trump took ill with COVID-19 on October 2 do not show a sympathy bounce for the president (Chart 2). Chart 1Consensus Forms Around ‘Blue Sweep’ Base Case

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Chart 2Trump Takes A Dive With Little Time On Clock

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

In a very dangerous turn for the president’s re-election chances, Trump discontinued negotiations with House Democrats over a fiscal relief bill, promising to pass a large new stimulus after the election. Partially walking back those comments, he said he would sign any targeted stimulus bills that Congress sends him in the meantime (such as a new round of $1,200 rebates for households). House Speaker Nancy Pelosi shot down the option of a skinny bill, as we have argued she would. Now they are going back and forth. While the S&P 500 rallied on the news, other reflation trades like US cyclicals, oil, and silver show the risk of premature fiscal tightening (Chart 3). Investors may have to wait until late January until getting a new infusion of government support. Chart 3Lack Of Stimulus Still A Risk To Reflation Trades

Lack Of Stimulus Still A Risk To Reflation Trades

Lack Of Stimulus Still A Risk To Reflation Trades

Chart 4Market Rally Not Based On Blue Sweep Odds

Market Rally Not Based On Blue Sweep Odds

Market Rally Not Based On Blue Sweep Odds

True, a fiscal deal could be passed in the lame duck session in November or December, but Republican Senators unwilling to pony up around $500 billion to bail out blue states – when they face a possible wipeout in a historic election – will be even less willing if they lose the election. They will be more hawkish since they will want to pin deficits on the Democrats in future. If Republicans retain control of the Senate despite the latest news – which is possible, especially given the Democratic candidate’s new vulnerability in the North Carolina race due to a sex scandal – then investors have two years of fiscal hawkishness to contend with. Diagram 1 highlights the market implications of this Senate risk. Diagram 1Scenarios For US Election Outcomes And Market Impacts

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

So we need to look elsewhere to explain why the market rallied when odds of a fiscal deal fell. The above reasoning leaves us with the following options: The economy is recovering so robustly that new fiscal stimulus is unnecessary. This is not the view of Federal Reserve Chairman Jay Powell, who all but pleaded for Congress to conclude a deal to secure the recovery, or of other mainstream economists. Stimulus is coming regardless of election outcome. Congress will be forced to support the country during a slump. Debt monetization is the relevant point, even if there is a month-or-two delay in stimulus. Financial markets are cheering the higher odds of a Democratic clean sweep of Congress and the White House since it implies fiscal largesse. The market may already have discounted some of the impending tax hikes over the past month. The second explanation is the best but the third is rapidly becoming the new consensus on Wall Street. Chart 4 suggests there is no connection between the S&P rally and the odds of a blue sweep. With the Fed pursuing “maximum employment” and average inflation targeting, it makes sense that the real mover in the macro landscape has become fiscal policy. Hence the outcome that produces the most proactive fiscal policy is positive for financial markets. A blue sweep is verification of the shift toward debt monetization, which is missing from option two above. The problem is that a blue sweep also brings downside risks. Domestic policy uncertainty will only fall temporarily after the election if there is a blue sweep. Checks and balances will vanish. Eventually Democrats will become overweening in their policy agenda, delivering negative surprises to financial markets. A “New Deal”-style policy agenda would weigh on the corporate earnings outlook. For example, Democrats have refused to forswear removing the filibuster or stacking the Supreme Court, both of which would lie in their power and either of which would enable them to pass an ambitious “New Deal”-style policy agenda that would bring unforeseen consequences – largely in the direction of wealth redistribution away from corporations. Table 1What EPS Hit To Expect?

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Redistribution would start to correct US social and economic imbalances, improve middle class spending power, and boost consumption – but it would first weigh on the corporate earnings outlook. Net profit growth, which grew by 16% above what was otherwise expected due to the Trump tax cuts (Chart 5), could suffer more than the expected 11% one-off contraction (Table 1), as our US equity strategist Anastasios Avgeriou has shown. Chart 5Partial Repeal Of Trump Tax Cut Bad For Earnings

Partial Repeal Of Trump Tax Cut Bad For Earnings

Partial Repeal Of Trump Tax Cut Bad For Earnings

New proposals will also emerge that the market is not taking account of. To take just the latest example, former Fed Chair Janet Yellen recently stated that the US could adopt a $40 per ton tax on carbon emissions under a Biden administration.1This proposal is not part of Biden’s official plan, hence not priced by markets along with Biden’s expected tax hikes (Table 2). But control of the Senate would make it a real option given Biden’s ambitious climate goals. Table 2Biden Needs Senate To Raise Taxes

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Consumer confidence in the US will suffer from political polarization. Recall that in 2016, the economy was in fine shape but Republicans did not believe it, weighing down the average until President Trump won the election. Today the economy is in a slump but Republicans may not recognize the bad news until President Trump loses. Democrats, for their part, will suddenly abandon their doom and gloom if Biden wins the election. Applying a comparable partisan shock to consumer confidence for 2021 would suggest that overall confidence will be lackluster (Chart 6). At least this is true until the passage of new stimulus and an advancing recovery outweigh the partisan effect. Chart 6Biden Will Not Recreate Trump Confidence Boost

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

A similar case can be made that small business sentiment will worsen in a blue sweep scenario. Fear of higher regulation and taxes will spike and weigh on animal spirits (Chart 7). Historically the first year after an election sees smaller equity upside and larger downside with unified government as opposed to divided government (Chart 8). If this time is different it is because of the sea change in the US to embrace debt monetization. But that sea change occurred under a Republican administration and is likely to persist due to the output gap. Chart 7SMEs Will Fear Blue Wave

SMEs Will Fear Blue Wave

SMEs Will Fear Blue Wave

Chart 8Stock Market Profile Fits Divided Government, Which Has More Upside

Stock Market Profile Fits Divided Government, Which Has More Upside

Stock Market Profile Fits Divided Government, Which Has More Upside

A Republican Senate under a Biden presidency would bring higher fiscal risk, but the truth is that neither trade war risks nor corporate taxes would go up, yet Republicans would eventually have to concede to spending bills (just as Democrats did under Trump). Hence divided government is not as negative as it is made out to be as it contains mostly known quantities, whereas a blue sweep would lead the US in a redistributionist direction that is initially disruptive. Relative to divided government, it would be positive for aggregate demand but negative for corporate earnings. Bottom Line: US and global equities will rise over the coming 12 months on the back of eventual US stimulus and ongoing global stimulus. A blue sweep is our base case election outcome but it brings mixed results. Global equities would benefit more than US equities which will face a spike in taxes and regulation. US equities will still rise but they face more upside under a divided government in which Republicans halt tax hikes. Supreme Court Confirmation Looms Of course, a blue sweep outcome is not guaranteed. Indeed the fact that it is now consensus makes us nervous, as there are still 26 days until the election. Our quantitative election model gives the Republicans a 49% chance of winning the White House on the back of the V-shaped recovery in the states, which delivers Florida to the Republican camp, leaving Trump with 259 Electoral College votes (Chart 9). This probability is well above our subjective 35% judgment and the new market consensus on Trump’s odds. Chart 9Quant Election Model Gives Trump 259 Electoral College Votes And 49% Odds Of Victory

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Trump’s decision to break off the fiscal talks probably sealed his doom, but we would still maintain that a correct reading of the various political and economic constraints point toward a fiscal deal. Hence there is still some chance that a deal will be snatched from the jaws of defeat. At that point we would upgrade Trump’s chances to something closer to our election model. But it would not be bullish, as the market would need to price a higher risk of trade war. Subjectively Trump has a 35% chance of re-election, but our quant model flags a risk to this view. The market also must contend with COVID-19 risks (Charts 10A and 10B). Stimulus is necessary to prevent COVID-19 risks from hitting the market, as more distancing will be necessary in states where cases are rising. Chart 10ACOVID-19 Cases Rising

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Chart 10BCOVID-19 Hits Swing States

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

The reason President Trump cut short the fiscal talks was to ensure that they would not interfere with the Senate’s ability to confirm his Supreme Court nominee Amy Coney Barrett. The confirmation hearings will go up for a floor vote in the Senate sometime around October 23, ensuring a massive constitutional brawl just ahead of the election. The dollar has more upside if Trump wins. Chart 11Risk: Trump Comeback Boosts The Greenback

Risk: Trump Comeback Boosts The Greenback

Risk: Trump Comeback Boosts The Greenback

We do not expect this showdown to change the game, since boosting turnout among Trump’s conservative base will be insufficient in an election fought in the face of major national shocks that affect the median voter (pandemic, recession, social unrest). This election is already going to be a high turnout election – preliminary information suggests it could be the highest since 1908 at 65% of eligible voters2 — which means that Republicans will suffer from the leftward tilt of the median voter. However, if Trump’s polling improves between now and then – and if mFarkets inexplicably rally all month despite the withdrawal of fiscal support – then we could be surprised. Our quantitative model provides a basis for believing that Republicans are now underrated. This implies that the dollar has more upside in the near term as the risk of a contested election and/or a Trump second term, and hence another shock to the US political system and global trading system, must still be guarded against (Chart 11). Investment Takeaways The market faces near-term downside risk and volatility until the US fiscal support is restored. This is particularly the case as long as COVID-19 cases are not subdued. The rising odds of a blue sweep, our base case, is not sufficient to dampen volatility over the coming month. Depending on the election results, volatility will subside in November or January at the latest. Not only is a contested election a non-negligible risk – based on our quant model’s reading – but also President Trump will remain in office till January 20 and could easily dish out some negative surprises, particularly on China relations. Hence we are maintaining our tactical risk-off and safe-haven trades: long US treasuries, Japanese yen, US health care equipment stocks (which will outperform the overall sector amid the Democratic regulatory threat), and EUR-GBP volatility. Over the 12-month time frame, we have little doubt that the US adoption of debt monetization, in keeping with Chinese and global stimulus, will push equities and risky assets higher. The reflation trade remains the core of our strategic portfolio. Global stocks should outperform under a Biden presidency. Biden will be positive for global trade ex-China, as both US electoral politics and grand strategy will drive any administration to take a hard line on China, though Biden will not wield tariffs like Trump. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 See Matthew Green, "U.S. could adopt carbon tax under a Biden presidency, ex-Fed Chair Yellen says," Reuters, October 8, 2020, reuters.com; see also Group of Thirty, "Mainstreaming The Transition To A Net-Zero Economy," October 2020, group30.org. 2 See John Whitesides, "More than 4 million Americans have already voted, suggesting record turnout," Reuters, October 6, 2020, reuters.com.

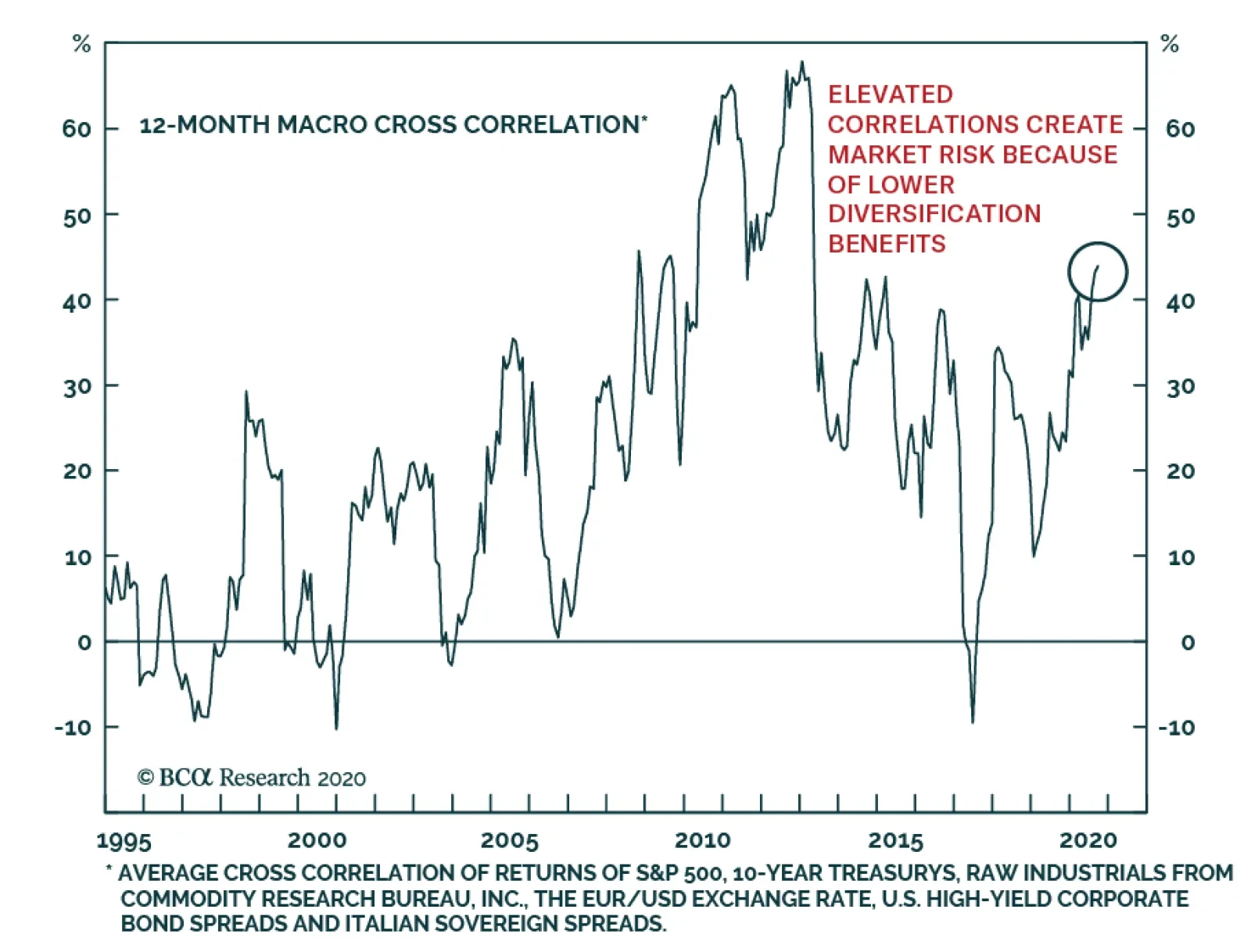

Correlations across asset classes move higher in times of crisis. 2020 proved no exception to this rule, which is problematic as it makes diversification more difficult to achieve exactly when investors need it most. The good news is that as economic…

Highlights US market risks stem from both the lack of fiscal stimulus before the new president assumes office in late January. Risk-off moves in US financial markets will weigh on EM. China’s stimulus has peaked and the country has begun a destocking phase in commodities inventories. These factors could add to investor worries reinforcing the pullback in commodities prices and EM currencies. The key risks to our strategy are that financial markets might look through the lack of US fiscal stimulus in the next several months and ignore the commodity destocking cycle in China. This will be the case if investors instead focus on the US and China’s benign growth outlook over the next nine months. In that regard, we are positive too. Hence, the difficulty is to navigate markets in the near-term. If EM risk assets and currencies prove resilient in the short term, we will upgrade our stance sooner than later. Feature Global risk assets are vulnerable as US Republicans and Democrats have failed to agree on a new round of fiscal stimulus. The odds of enacting significant stimulus legislation – including income support for the unemployed – before the new president assumes office in late January are low. Global risk assets will suffer due to their dependence on continuous government stimulus. The rally since late March has created an air pocket, somewhat disconnecting risk asset prices from their fundamentals. In particular, the gaps between share prices and corporate earnings and between corporate spreads and projected corporate default rates have widened dramatically (Chart I-1). We do not mean that corporate earnings will not recover. Our point is that share prices have risen too far, too fast. Absent a large fiscal stimulus package in the US, risk asset prices will likely experience a meaningful setback. These gaps have been sustained by hopes of continuous fiscal and monetary stimulus. However, absent a large fiscal stimulus package in the US, risk asset prices will likely experience a meaningful setback. We continue recommending EM investors maintain a defensive positioning for now. Asset allocators should remain neutral on EM equities and credit within their respective global portfolios. In the near term, EM currencies will depreciate against the US dollar. We continue shorting a basket of EM currencies versus the euro, CHF and JPY. These DM currencies are likely to experience some, but not substantial, downside versus the greenback. Elevated Expectations Economic growth expectations are rather elevated and investor sentiment is complacent: The Global ZEW expectations index – based on a survey of analysts from banks, insurance companies and finance departments from the corporate sector – is close to an all-time high (Chart I-2). This implies that investors’ and analysts’ growth expectations are substantially inflated. Chart I-1The Rally Has Been Too Fast, And Gone Too Far

The Rally Has Been Too Fast, And Gone Too Far

The Rally Has Been Too Fast, And Gone Too Far

Chart I-2Investor Expectations Are Very Elevated

Investor Expectations Are Very Elevated

Investor Expectations Are Very Elevated

The very low level of the SKEW for US stocks signifies investor complacency (Chart I-3). A low SKEW reading means investors are not pricing in tail risks. Further, the rally since March lows has been reinforced by the substantial speculative trading activities of retail investors. Finally, investors’ net long positions in copper are at their previous cyclical highs (Chart I-4). Chart I-3Low SKEW Signifies That Investors Are Not Ready For Tail Risks

Low SKEW Signifies That Investors Are Not Ready For Tail Risks

Low SKEW Signifies That Investors Are Not Ready For Tail Risks

Chart I-4Investors Are Very Long Copper

Investors Are Very Long Copper

Investors Are Very Long Copper

Peak Stimulus? China is approaching peak stimulus. Chart I-5 shows that the projected bond issuance by central and local governments will decline in the coming months. Besides, the loan approval index of the PBoC banking survey has rolled over decisively (Chart I-6). Chart I-5Peak Fiscal Stimulus In China?

Peak Fiscal Stimulus In China?

Peak Fiscal Stimulus In China?

Chart I-6Peak Credit Growth In China?

Peak Credit Growth In China?

Peak Credit Growth In China?

A combination of less government bond issuance and less loan origination by banks implies that the credit impulse will roll over in the coming months. This does not mean that the mainland economy will weaken in the coming months. The credit and fiscal spending as well as broad money impulses lead the economy by about nine months (Chart I-7). Therefore, even if the credit and fiscal spending impulse rolls over later this year, the economy will continue improving at least until next spring. Therefore, from a cyclical perspective, we remain positive on China’s business cycle. China’s peak stimulus and destocking phase in commodities could add to investor worries. That said, China-related financial markets have already rallied quite a bit and are likely to experience a pullback as US equity and credit markets sell off. Additionally, after having stockpiled commodities since spring, China has probably entered a commodity destocking cycle. Even though final demand in China will be firming, resource prices will likely relapse in the near term due to diminished mainland imports. In the US, the massive fiscal stimulus from the CARES Act has led to a surge in household income amidst the worst collapse in economic activity since the Great Depression and the massive layoffs that accompanied it. Government transfers during recessions are typically devised to moderate income decline but not lead to a boom in income as has occurred in the US this year (Chart I-8). Chart I-7China's Business Cycle Will Continue Improving

China's Business Cycle Will Continue Improving

China's Business Cycle Will Continue Improving

Chart I-8US Household Income Surged Amid Economic Collapse

US Household Income Surged Amid Economic Collapse

US Household Income Surged Amid Economic Collapse

Chart I-9Credit Standards At US Banks Are Tight

Credit Standards At US Banks Are Tight

Credit Standards At US Banks Are Tight

Without renewed fiscal transfers to households, personal income will erode and consumer spending will weaken. Further, state and local governments are retrenching as their revenue streams have evaporated. Finally, bank lending standards have tightened dramatically (Chart I-9). Crucially, the majority of investors are long risk assets because of expectations of recurring fiscal stimulus and the Federal Reserve’s implicit put on stocks and corporate credit. If one of these two pillars – in this case fiscal stimulus – fades away, some investors might throw in the towel. In EM excluding China, Korea and Taiwan, economic activity is rebounding post lockdowns. However, these economies are also approaching peak stimulus at a time when the level of economic activity in many countries remains very low. In addition, hit by a wave of defaults, banks in these economies are not in a position to originate new loans. Thereby, the transmission mechanism of monetary policy is partially broken. Their central banks’ stimulus have not been fully transmitted to the real economies. Bottom Line: Risks to the rally in US equities stem from both the lack of fiscal stimulus and political uncertainty following a possibly contested presidential election. Risk-off moves in US financial markets will weigh on EM. China’s peak stimulus and destocking phase in commodities could add to investor worries, reinforcing the pullback in commodities and EM risk assets. Indicator Review A number of indicators point to downside in EM risk assets and currencies. The advance-decline line for EM equities is below zero stocks (Chart I-10). This points to poor equity breadth in the EM universe. Chart I-10Poor Breadth In EM Equities

Poor Breadth In EM Equities

Poor Breadth In EM Equities

Chart I-11A Warning Signal For EM Stocks

A Warning Signal for EM Stocks

A Warning Signal for EM Stocks

The cross rate of the Swedish koruna versus the Swiss franc (de-trended) has been a good coincident indicator for EM share prices and it points to a selloff (Chart I-11). The implied volatility index for EM currencies is rising (shown inverted in the chart), pointing to a relapse in EM exchange rates versus the US dollar (Chart I-12, top panel). Chart I-12Red Flags For EM Equities And Currencies

Red Flags For EM Equities and Currencies

Red Flags For EM Equities and Currencies

Chart I-13Are Commodities In A Soft Spot?

Are Commodities In A Soft Spot?

Are Commodities In A Soft Spot?

Platinum prices are gapping down. This rings alarm bells for EM currencies as the two are strongly correlated (Chart I-12, bottom panel). Chinese steel rebar futures, global steel stocks and Glencore’s share price – a global bellwether for commodities – have all begun relapsing, even before Trump’s withdrawal from the fiscal stimulus talks (Chart I-13). Also, the latter has failed to break above its 200-day moving average. The same is true for oil prices. We read such a technical configuration as a telltale sign that these commodity plays have not entered a bull market and remain vulnerable. In emerging Asia, high-yield corporate credit’s relative performance versus investment-grade corporates has rolled over at its previous highs (Chart I-14). In the past several years, the failure to break above this technical resistance level was followed by a material selloff in EM credit and equity markets. Bottom Line: The majority of indicators for EM risk assets and currencies are presently flashing red. Investment Considerations The rally in share prices and drop in the US dollar yesterday following Trump’s cancellation of stimulus talks is puzzling. We expect the market to realize that the odds of considerable fiscal stimulus with meaningful income support for the unemployed is low until the new president assumes office in late January. We believe large and recurring US fiscal stimulus packages are very likely following the elections, favoring reflation and inflation strategies in the medium and long run, and weighing on the US dollar. That was the basis upon which we turned bearish on the US dollar on July 9 and upgraded EM stocks from underweight to neutral on July 30. However, in the near term, the lack of fiscal stimulus favors the deflation trade: a bet on lower growth and lower inflation. If EM risk assets and currencies prove resilient in the near term, we will upgrade our stance sooner than later. If the markets agree with our assessment that US growth will meaningfully disappoint without fiscal stimulus, not only will global share prices drop but also US inflation expectations will decline, US real rates will rise and the US dollar will rebound (Chart I-15). This would produce a bearish cocktail for EM currencies, credit markets and stocks in the near term. Chart I-14A Message From Emerging Asian Credit Markets

A Message From Emerging Asian Credit Markets

A Message From Emerging Asian Credit Markets

Chart I-15A Reset In US Inflation Expectations, Real Rates And US Dollar Is Overdue

A Reset In US Inflation Expectations, Real Rates And US Dollar Is Overdue

A Reset In US Inflation Expectations, Real Rates And US Dollar Is Overdue

The key risks to our strategy are that financial markets might look through the lack of US fiscal stimulus in the next several months and ignore the commodity destocking cycle in China. It will be the case if investors focus on the US and China’s benign growth outlook over the next nine months. In that regard, we are positive too. Hence, the difficulty is to navigate markets in the near-term. If EM risk assets and currencies prove resilient in the near term, we will upgrade our stance sooner than later. Stay tuned. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategy For Philippine Markets xChart II-1Philippine Equities: Relative & Absolute Performance

Philippine Equities: Relative & Absolute Performance

Philippine Equities: Relative & Absolute Performance

Our underweight stance on Philippine stocks has played out well as this bourse has massively underperformed the EM equity benchmark (Chart II-1, top panel). Notably, in absolute terms, Philippine share prices look disconcerting as they have stalled at their long-term moving average (Chart II-1, bottom panel). We continue to recommend an underweight position in this bourse for dedicated EM portfolios and a cautious stance for absolute-return investors. In terms of the currency market, our short position on the Philippine peso has not played out as the exchange rate has been very resilient. We are removing the PHP from our short EM currency basket by closing the short PHP/long the euro, CHF and JPY trade with a 1% loss. The key reason for the peso’s strength has been the rapidly improving current account balance (Chart II-2). The latter has moved into a surplus due to the collapse in domestic demand and imports as well as ballooning remittances. In brief, the balance of payment surplus has been so large that the currency appreciated against the US dollar even though the central bank accumulated large amounts of foreign exchange reserves. Such strong remittance inflows are probably due to returning expatriate Filipino workers from Gulf countries, bringing their entire savings with them. If so, such remittance inflow will not reoccur. Nevertheless, the trade and current account deficits are unlikely to widen rapidly because imports will stay subdued - due to weak domestic demand - and exports will be supported by electronics exports (Chart II-3). The latter make up 57% of total goods exports. Chart II-2Current Account Balance Is In Surplus

Current Account Balance Is In Surplus

Current Account Balance Is In Surplus

Chart II-3Philippine Exports Are Recovering

Philippine Exports Are Recovering

Philippine Exports Are Recovering

Commercial banks in the Philippines have tightened their lending standards meaningfully. On domestic demand, the post lockdown recovery will be moderate and slow and corporate profits will disappoint: Chart II-4Decelerating Bank Loan Growth

Decelerating Bank Loan Growth

Decelerating Bank Loan Growth

The country has not been handling the pandemic well. The health system is showing signs of stress and the authorities have been forced to continuously roll out new lockdowns and social distancing measures. This will prevent a strong revival in business activity in an economy where consumer spending represents 70% of GDP. The Philippine government has unleashed fiscal stimulus packages of about 4% of GDP to counter the pandemic-induced recession. With the fiscal year nearing its end, the cyclical growth outlook will depend on next year’s budget. Next year’s government spending will likely be 5% higher than the original 2020 budget, i.e., excluding extraordinary stimulus measures from both 2020 and 2021 budgets. Therefore, the 2021 budget is unlikely to be enough to support growth materially. Besides, even though the government is trying to roll out more stimulus for next year, its concerns about the size of budget deficit and its financing will limit stimulus. Crucially, bank loan growth is decelerating sharply (Chart II-4). Commercial banks will be reluctant to originate much new credit in this weak growth environment. In brief, the negative credit impulse will offset the fiscal stimulus. The Philippine central bank has been very aggressive in its measures. It has unleashed an unprecedented QE program – buying government bonds en masse – and has also injected liquidity into the banking system and cut its policy rate by 175 basis points (Chart II-5). Yet, the monetary transmission mechanism has been broken in the Philippines and the monetary easing has not benefited the real economy. In particular, commercial banks in the Philippines have tightened their lending standards meaningfully. In turn, banks’ lending rates have not dropped. As with many other EMs, this is occurring because Philippine banks want to protect or increase their net interest rate margins at a time when they are witnessing mounting non-performing loans, rising provisions, and tanking profits (Chart II-6). Chart II-5Philippine: Central Bank Is Doing QE

Philippine: Central Bank Is Doing QE

Philippine: Central Bank Is Doing QE

Chart II-6Banks Are Facing Mounting NPLs

Banks Are Facing Mounting NPLs

Banks Are Facing Mounting NPLs

Bottom Line: Continue underweighting Philippine stocks in an EM equity portfolio. Within this bourse, we are taking profit on the short position in property stocks. This recommendation has generated a 10% gain since its initiation on November 1, 2018. As to fixed-income markets, consistent with our view change on the currency we are upgrading Philippine sovereign credit from underweight to overweight and domestic bonds from underweight to neutral. Ayman Kawtharani Editor/Strategist ayman@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Underweight

Avoid REITs

Avoid REITs

We remain bearish on the prospects of the S&P real estate sector as the pandemic will continue to severely bruise REITs. Already, YTD relative share prices are down 10%, and were it not for the tech/communications-laden – tower and digital storage – REITs that the S&P specialized REITs subgroup houses, then the relative underperformance would sink to 25%. According to the latest Q2 Fed release, CRE delinquencies are on the rise (not shown) and CRE prices are on the verge of contracting (bottom panel). A fresh stimulus bill could come to the rescue, but recent news of President Trump halting negotiations jeopardizes chances for near-term relief. Refinancing risk is another threat that could cause a gap down in CRE prices, as bankers remain unwilling to dole out CRE loans despite a collapse in interest rates. Once the underlying asset gets repriced lower, then the debt related house of cards comes crumbling down (top & middle panels). Bottom Line: We remain underweight the S&P real estate sector. The ticker symbols for the stocks in this index are: BLBG: S5RLST-AMT, EQIX, PLD, CCI, DLR, PSA, SBAC, AVB, WELL, ARE, O, SPG, WY, CBRE, EQR, ESS, FRT, PEAK, VTR, BXP, DRE, EXR, MAA, UDR, AIV, HST, IRM, KIM, REG, SLG, VNO. For more details, please refer to this Monday’s Weekly Report.

Following yesterday’s proposal of skinny, targeted fiscal stimulus by President Trump, BCA Research’s geopolitical strategists curtailed the odds of any significant stimulus deal ahead of the election to 20%. The decision was not taken on Tuesday when…

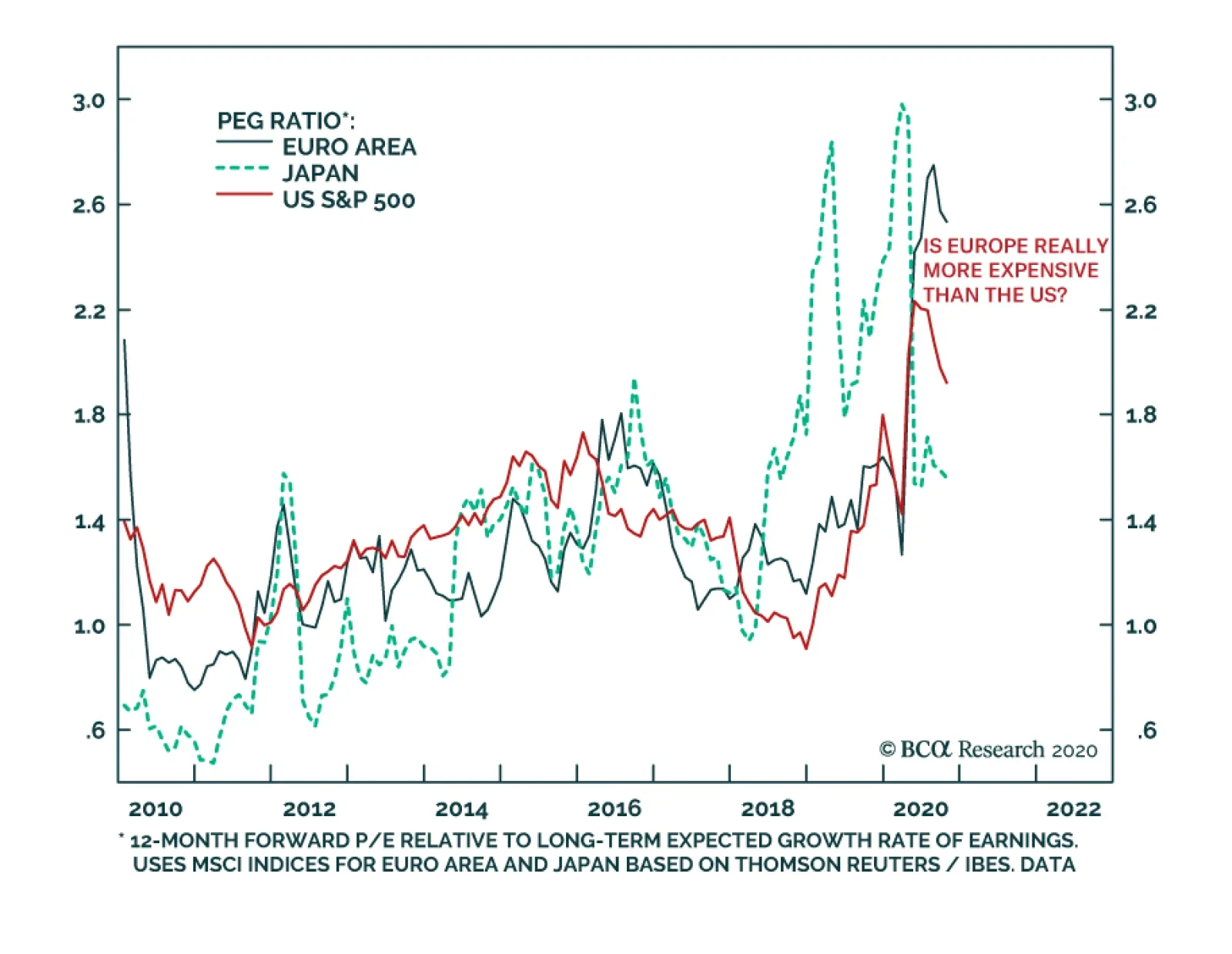

When looking at multiples like the price-to-book or price-to-earnings ratios, it is easy to paint the S&P 500 as exceptionally expensive compared to other major equity markets. However, the picture becomes murkier if we take into account growth…