United States

Feature Investors are increasingly concerned that the US presidential election this year will fail to produce a legitimate result, leading to an escalation in political instability and uncertainty. In this report we hold a Q&A session that we hope will serve as your concise and definitive guide to a contested US election – by which we mean an election that is not decided by the popular vote or Electoral College but requires the intervention of the US Congress or Supreme Court to determine the final outcome. As always, this report draws on the best academic work on the subject, but is not limited to academic conclusions. We apply our geopolitical method and macroeconomic perspective to determine the likeliest scenarios and financial market impacts. The takeaway? Most likely the election result will be decisive, as incumbent presidents tend to lose amid recessions. However, with President Trump staging a comeback, a contested election is possible and investors would be wise to prepare for volatility over the next two-to-four months at minimum. Chart 1Trump At Disadvantage In Popular Opinion

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

A good rule of thumb: Trump is at a disadvantage in raw popular opinion (Chart 1), so anything that directs the election decision away from the popular vote and toward constitutional procedures should be seen as a lifeline for Trump, and hence a recipe for a bigger trade war and prolonged US equity outperformance. How Is The US President Elected? The US elects presidents by means of electors, private citizens appointed by each of the 50 states to vote on their population’s behalf, i.e. the Electoral College. The popular vote, or canvass, has been the prevailing method of choosing each state’s electors since the 1840s. The vote is held and tallied by the election authorities of the states on the first Tuesday after the first Monday of November (e.g. November 3, 2020). Each state has different laws on how to hold elections and appoint a slate of electors loyal to the winning candidate in the state. The constitution grants state legislatures the power to appoint the electors. This could become a source of controversy in a contested election.1 Generally the state’s secretary of state approves the popular tally which then determines which slate of electors is appointed. The state governor certifies the names of the electors and the numbers of votes received, signs the letter and applies the state seal, and then sends multiple copies to various authorities for surety.2 If disputes arise over a state’s election results, the state will ideally resolve them by December 8 (Table 1), six days before the electors meet to fill out their ballots for the president and vice-president. Electors meet in the state capital on the first Monday after the second Wednesday of December (e.g. Monday, December 14, 2020) and cast their vote. They send certificates of their vote to the President of the United States Senate in Washington, DC, who is also the nation’s vice president, currently Mike Pence. Table 1Calendar Of US Election 2020

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

On January 6 of the New Year (2021), the President of the Senate presides over a special joint session of the new Congress, which itself convenes on January 3. He presents the states’ electoral votes to Congress alphabetically. The votes are counted, with Congress employing official tellers to record the sums.3 If any disputes are raised against any state’s electoral votes, the two houses of Congress must agree in order to disqualify those votes. If the two houses disagree, the votes will be counted. The Senate President, as the constitutional keeper of the electoral returns and presiding officer of the joint session, has some influence, which is another potential source of controversy. When the count is done, the tellers hand their results to the Senate President, who reads them off. Usually the leading candidate captures an absolute majority of the Electoral College (270/538 votes), so the next president is crystal clear and the whole ceremony is finished in half an hour. Alas, not always. What Electoral Results Can Be Ruled Out In 2020? Before getting into contested elections, it is important to address what is highly unlikely to occur in 2020. First, President Trump will not win the popular vote. Chart 2Trump Highly Unlikely To Win Popular Vote

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Trump won 46% of the popular vote in 2016, trailing Hillary Clinton by 2.9 million votes. Since 2017, Trump’s national approval rating has never risen above 50% in the average of polls. His disapproval rating is almost always higher than his approval (Chart 2). Thus if Trump wins the election it will be through his Electoral College strategy, as in 2016 – or through a contested election. The US has split the popular and Electoral College vote on five occasions, yielding a historical probability of 9%. The fifth time was President Trump’s victory in 2016; he would be the first president to do so twice. This is possible because the regional and demographic factors behind Trump’s win four years ago are still largely intact. Currently our quantitative election model gives Trump a 45% chance of winning the election (Chart 3). This is in line with the consensus view, as online betting markets put Trump’s odds at 43%. However, online gamblers put the odds of the next president losing the popular vote in a range of 27%-31%, which implies that his odds are lower given his low popularity (Chart 4). Chart 3Our Quant Election Model Gives Trump 45% Chance Of Victory

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Chart 4Trump Odds Weighed Down By Low Chance Of Popular Win

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Subjectively, we are sticking with our 35% chance of Trump winning, which falls in the middle of this range. What is clear is that Trump has a much greater chance than the historical 9% probability of winning without the popular vote. There is nothing illegitimate about an Electoral College victory – far from it, it is the constitutional way in which the presidency is won. Nevertheless a victory without a popular mandate deprives the new administration of political capital. A second-term Trump is likely to be stymied at home and more inclined to act unilaterally abroad, a downside risk to global equity markets. Second, Republicans will not reclaim a majority of the House of Representatives. Chart 5Republicans Highly Unlikely To Win House Of Representatives

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

To do so, the GOP would have to retain all Republican-leaning seats (yielding 186) plus all “toss up” seats (totaling 214) and then four additional Democratic-leaning seats. Yet there are only two Democratic-leaning seats that do not benefit from the incumbent advantage (Chart 5).4 The re-election rate in the House and Senate is around 85-95%. Neither the state of the economy nor Trump’s approval rating suggest that Republicans are capable of such a big victory in the House (Chart 6). Chart 6Trump An Albatross For House Republicans

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Third, Democrats are unlikely to win a majority of the state delegations in the House of Representatives. Currently, Republicans have a majority on 26 of the 50 delegations of lawmakers that the states send to the US House of Representatives. Democrats control 23 state delegations, while Pennsylvania is neutral. If the presidential election is close, then the balance of power among the state delegations will most likely stay the same. Republicans are likely to retain 25 state delegations, whereas Democrats would have to win all five toss-up delegations plus Florida merely to tie the Republicans with 25 delegations (Table 2). This is a tall order. Table 2Democrats Unlikely To Win Majority Of State Delegations In House Of Representatives

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

The Republicans’ state-by-state House majority would prove critical in a contested election, as we will see. Otherwise it doesn’t matter much. What Is A Contested Election? Chart 7Extreme Political Polarization Means Election Disputes Will Rage

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

The 2020 election will inevitably see legal challenges, vote recounts, and procedural problems. Partisanship is at extreme levels, meaning that the two parties will do anything to win (Chart 7). The unprecedented large-scale adoption of mail-in voting due to the COVID-19 pandemic also ensures that recounts and legal disputes will abound.5 Neither candidate is likely to concede defeat quickly or easily. While President Trump is explicit about his reluctance to concede, there is zero chance that Joe Biden will bow out quietly like Al Gore did in the 2000 dispute. However, investors should distinguish a contested election, in which the resolution of disputes will determine the final outcome, from a controversial election, in which the final outcome is known but the defeated candidate refuses to concede. Either could be market-relevant, but the first scenario is the primary concern as it yields the powers of the presidency. The rest is aftermath. The bedrock principle of US presidential succession is as follows: Constitutionally, if the Electoral College vote falls short of a clear majority (270 out of 538), the House of Representatives chooses the president on a majority vote, with each state receiving only one vote. Similarly, the Senate chooses the vice president.6 President Trump is favored to win in this scenario. As mentioned, Republicans may well hold 26 of the 50 state delegations in the House. A clear majority on either side removes any risk of indecision: the next president will be chosen on a party-line vote of the states. For Democrats to choose the president in the House, they need a landslide victory. This is possible, but then it would imply that President Trump has been soundly beaten in the presidential race. A contested election presupposes a close national race that is likely to result in the status quo balance of power among the states in Congress, and hence an advantage for Trump if the House chooses the president. Map 1 illustrates the fundamental shift in American political power if the House of Representatives votes on a state-by-state basis to resolve a contested election. It alters the geography of each state according to the voting age population, the Electoral College representation from 2016, and an equal weighting in which each state gets the same number of votes, as in the House’s contested election procedure. The Electoral College is not nearly as distortive of the popular will as is often made out. However, the red states greatly increase their prominence in an equal weighting (just as in the US Senate). Map 1Trump Disfavored In Popular Vote, But Favored If Contested Election Decided In House Of Representatives

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

The fundamental takeaway is that President Trump is disfavored when it comes to the popular vote in the states, but if the election is contested and shifts to the House of Representatives, he has a lifeline. Yet if Democrats win the Senate in the election, this lifeline will be cut off. Moreover, the Supreme Court is a wild card, as discussed below. What Can We Learn From Past Contested Elections? Chart 8US Contested Elections Often Coincide With Deflationary Economy

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

The US has witnessed four contested elections under our definition. Most of them occurred amid deflationary economic trends, which would fit with today’s environment (Chart 8). Each episode can be described as a “stolen election,” depending on one’s point of view. The key lessons for today are as follows: 1800 – “The Revolution” – Vice President Thomas Jefferson, as Senate President, chose to count the electoral votes from Georgia even though they lacked the governor’s signature and failed to meet federal requirements. This gave him a majority of the electoral votes, which ultimately led to his election.7 If he had rejected these votes, the outgoing House of Representatives would have chosen his rival candidate, John Adams, as president. Takeaway: The vice president has the constitutional authority to present the electoral votes for counting and to oversee the joint session of Congress. If Congress is divided, and the vice president has a decision as to whether to present a certain set of electoral votes, then the vice president could tip the election in his own party’s favor. Also noteworthy: the presence or absence of a governor’s signature on a state’s electoral votes is not definitive. 1824 – “The Corrupt Bargain” – Andrew Jackson lost the election despite winning both the popular vote and the Electoral College vote. With a hung vote in the college, the House of Representatives decided the election among the top three candidates. The Speaker of the House threw his weight behind John Quincy Adams, who then nominated the speaker as the secretary of state in his new administration. Takeaway: Washington insiders can determine the outcome arbitrarily if they control the House of Representatives. A hung Electoral College, or tie, throws the election to the House and thus favors Trump. 1876 – “The Stolen Election” – Democrat Samuel Tilden won the popular vote and the most electoral votes, at 184, while Republican Rutherford Hayes won 165 electoral votes. Tilden was one vote shy of an Electoral College majority (185), while Hayes fell 20 votes shy. Republican control of four states led to an alternative set of Republican electoral votes being sent to Washington. Congress then had to choose between the rival electoral slates. To resolve the dispute, Congress created a special bipartisan committee. The tiebreaking member of the committee was disqualified by a fluke, leading to a replacement who voted on party lines, awarding all 20 disputed electoral votes to Hayes, who thus won the presidency. Simultaneously lawmakers negotiated a grand compromise to ensure Congress would not filibuster the committee’s decision: Hayes would withdraw federal troops from the South, which had been occupied since the Civil War. Takeaway: A party can use control of states to send an alternate set of electoral returns to Washington, muddying the electoral counting process and throwing the election into Congress’s hands. Also, Congress is supreme and can create special mechanisms to resolve electoral disputes. Political solutions are essential when constitutional mechanisms fail. 2000 – Bush versus Gore – Contested election results in Florida led Democrat Al Gore to withdraw his concession to Republican George W. Bush. The Gore legal team convinced the Florida Supreme Court to allow several recounts, including a statewide recount. The Florida legislature, along with Florida Governor Jeb Bush, prepared to certify Jeb’s brother’s victory and send electoral votes to Washington. The US Supreme Court intervened, halting a statewide recount, on the basis of the equal protection clause of the fourteenth amendment and in rejection of the Florida court’s novel recount scheme. Takeaway: The Supreme Court can and will intervene in a state election dispute if it is becoming a legal morass. Previously the states settled disputes themselves, or the US Congress settled disputes in Washington. Though the Supreme Court claimed that its ruling did not set a precedent, the clear precedent is that the Supreme Court will intervene if there is a power vacuum. Each of these contested elections sparked extreme partisan controversy.8 In two of them, both the popular and electoral results were thrown out the window. The lesson is that the House of Representatives is definitive. Unless, of course, the Supreme Court preempts it. Since both the Constitution and statutory history point to Congress, not the Supreme Court, as the arbiter of presidential elections, it is unlikely that the Supreme Court would overrule the House if the House makes its decision first. But it is still possible, and this is a major source of uncertainty for 2020 or future elections. To fix the various problems that have arisen over the years, Washington has passed several laws, such as the twelfth amendment (1804) and the Electoral Count Act (1887). But fundamental disagreements can still emerge: namely over the constitutional power of the state legislatures to appoint electors, the value of the governor’s signature on his or her state’s electoral votes, and whether the President of the Senate has a substantive or merely ceremonial role. Any of these factors could result in confusion and controversy in 2020-21. How Will States Settle Disputes? On the state level, prior to the joint session of Congress to count the electoral votes on January 6, a range of shenanigans could occur, and the states may never actually settle their disputes. States are supposed to settle any internal recounts or disputes by December 8, 2020 for “safe harbor” status. This status urges, but does not require, the US Congress to accept the state’s final determination of its own electoral votes. If a state fails of this status, Congress may still count its votes, but it has a freer hand to do as it pleases. Thus each party will attempt through judicial or legislative actions to rush and achieve safe harbor status if it believes it won the popular vote count, and will attempt to delay and deprive the state of that status if not. If the legislature and governor agree, then this will be no problem. If they do not agree, the risk emerges that a state battle could escalate all the way to Washington. States with Republican governors, and a Republican or at least a divided legislature, could ensure that Republican electoral votes are sent to Washington in the event of a dispute. This is particularly important in the case of Arizona and Florida, but it also applies to Georgia, Iowa, Ohio, and Texas in 2020. The same goes for Democrats, although there are fewer swing states that fit this description (e.g. Minnesota), as Table 3 shows. Table 3Swing States: Balance Of Legislative And Executive Power

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

The reason for this is that the Electoral Count Act of 1887 instructs Congress to favor the electoral votes with the governor’s signature if there is any dispute about which results to accept when the US Congress holds the final count. If the governor is not opposed by his own legislature, then his certified results will be the ones that go to Congress. However, states with a unified legislature, either Republican or Democratic, could conceivably send electoral votes of their choice regardless of what the state governor does – and this is relevant for several of the most important swing states in 2020, specifically Republican legislatures under Democratic governors in Pennsylvania, Wisconsin, Michigan, and North Carolina, and Democratic legislatures under Republican governors, as in New Hampshire. The constitution endows state legislatures with the power to appoint electors, so legislatures could attempt to override their governors – or even their state supreme courts. Indeed, Florida’s legislature and governor were prepared to send Republican electoral votes to Washington regardless of the Florida high court’s actions in the year 2000. How Will Congress Count The Votes? Republicans will not have unified control of the federal legislature and executive, as noted above. Hence Republican congressmen and senators will not be able to pick and choose which electoral votes to accept at their discretion when the votes are counted on January 6, 2021. House Democrats would prevent them from rejecting any state’s electoral votes for arbitrary reasons. On the other hand, the Democrats are quite likely to pick up the Senate, and a united Democratic Congress would have the power to pick and choose electoral votes at its discretion. The Democrats could disqualify the electoral votes of a state that voted for Trump in the event of a dispute, tipping the scales in Biden’s favor, during the electoral counting process. For example, say President Trump wins 270 electoral votes and Biden wins 268 – a likely scenario if Trump wins all the 2016 states but loses Pennsylvania and Michigan. Ostensibly President Trump would be re-elected. But the Democratic House and Senate could disqualify the 10 electoral votes of Wisconsin due to any disputes in that state over its popular vote or electors. Trump’s votes would fall to 260 while Biden would retain his original 268. A unified Congress could simultaneously decide to disqualify Wisconsin’s electors from the 538 total of appointed electors, saying the electors were not legally appointed, bringing the total denominator of electors to 528, thus giving Biden a three-vote margin of victory (majority: 265/528). Biden would become the president. If Congress is divided then this kind of manipulation is not possible. Either a bipartisan agreement would determine whether to count a state’s votes – which would be credible and legitimate – or a bipartisan disagreement would lead to the disputed electoral votes being counted. Chart 9Democrats Likely To Win Senate, Hence Congress – Huge Perk In Electoral Count

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Hence the makeup of the Senate on January 3, which may not be wholly complete at that time, is of great consequence. Democrats are structurally favored to win the Senate this year. They have 12 seats up for re-election versus 23 for Republicans, and only two of their seats are at risk whereas 10 are at risk for Republicans (Chart 9). We expect Democrats to take the Senate, but in a close presidential race the Senate could tie at 50-50. If Republicans retain the Senate, then Vice President Mike Pence could take on a substantive role in counting the Electoral College votes, rather than a merely ceremonial role of presenting the electoral returns to the joint session. If a state sends questionable electoral returns, or more than one set of returns, Pence could conceivably choose which results to present to Congress. A unified Congress could override him but a divided Congress might not. There is precedent for a vice president making a decision on electoral counting that affects the outcome in his own favor, as noted above. While modern scholars tend to highlight the conflict of interest here, the constitution could be read as giving the vice president this advantage so as to more speedily settle any disputes.9 The Electoral Count Act of 1887 says that when in doubt, Congress should accept the electoral votes certified by a state’s governor. But this position was controversial at the time and may not be constitutional. The vice president could assert his own authority to present the legitimate votes to Congress to be counted. It is not clear that a conservative-leaning Supreme Court would contradict him, since neither the constitution nor the Electoral Count Act envisions the court as arbitrating these kinds of disputes. Thus it is conceivable that a situation could arise in which a critical swing state sends two sets of returns and Vice President Pence chooses the electors in favor of himself and President Trump, with a Republican Senate preventing the Democratic House from doing anything about it. A strict constructionist Supreme Court would likely defer to whatever happens in Congress. However, the court could be activist, given that Chief Justice John Roberts is a well-known swing player. It could interpose in a way that precludes any actions deemed entirely arbitrary or lacking a plausible basis in the facts of the state’s election results and laws. As we saw, the court will be inclined to fill a power vacuum. The takeaway is that a unified Congress could count the electoral votes in such a way as to secure a Biden win, while a divided Congress could count the electoral votes in such a way as to give President Trump a lifeline in a disputed election. The Supreme Court is a wild card. What About An Electoral College Tie Or Faithless Electors? A contested election, using the narrow definition, would occur due to an Electoral College tie at 269-269 or any other anomalies that prevent either candidate from reaching a 270-vote majority. Again, the House of Representatives would decide on a state-by-state basis, likely favoring Trump. For example, some electoral votes could be disqualified, a third party candidate could split the vote, or “faithless electors” could vote contrary to their state’s popular choice.10 An electoral tie is not a negligible risk in 2020 – there are 68 possible combinations, and many of them are plausible.11 In 2016, 11 states had a margin of victory less than 5%. Take two equally realistic examples. If Trump lost Pennsylvania and Michigan (likely) as well as Nebraska’s second district (Omaha/suburbs, which President Obama won) then he would tie Biden at 269. Or, if Trump lost Pennsylvania, Michigan, and Arizona (which leaned Democratic in 2018), yet gained Minnesota (the epicenter of the crisis over race and law enforcement), a tie would occur. In a near-tie, a few wayward electors could deprive either candidate of a win. This is far more likely to happen to Trump than Biden. Table 4Range Of Electoral College Votes, 2020

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

The current combinations of truly competitive states suggest that the Democrats have a lock on 268-319 electoral votes while Republicans only have a lock on 169-219 electoral votes (Table 4). Trump is widely expected to lose both Pennsylvania and Michigan, which alone cut him down to 270 votes; the loss of a single vote from there would deprive him of a majority. By contrast, Biden would hit 278 votes at minimum by picking off a single Republican state in addition to Pennsylvania and Michigan. It is more likely that Trump would lose one or two faithless electors than that Biden would lose nine or ten. So it is more likely that faithless electors would deprive Trump of a win than Biden. But then the House of Representatives would have to resolve the impasse, and would likely favor Trump. What Is The Line Of Succession If The House Fails To Choose A President? What happens if a contested election goes to the House but the state delegations tie at 25-25? Then the House must continue voting over and over until one of the presidential candidates gets the majority. A single lawmaker in a critical state could swing the balance. That lawmaker could be swayed by conscience, bribes, or chance. In 1824, a critical lawmaker from New York changed his vote at the last minute because he found a ballot with John Q. Adams’s name on it and believed it was a sign from God. In 1876, the tiebreaking Supreme Court judge in the congressional commission delegated to work out a compromise solution was disqualified after it was found he had won a simultaneous race for a seat in the Senate.12 The House would eventually decide, but if the state delegations are evenly split, the voting could continue through January 20, Inauguration Day. The vice president would take over at that time. The vice president is chosen by a majority vote of the Senate. If Democrats take the Senate, they would choose California Senator Kamala Harris as the vice president, and she would act as president until the House made its choice. If the Senate vote also split at 50-50 on the new vice president, then the Speaker of the House, who is likely still to be California Representative Nancy Pelosi, would serve as acting president under the statutory line of presidential succession (Table 5). Table 5US Line Of Succession If Presidency Vacant

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Obviously both the House and the Senate would be under immense pressure to make a decision, so the power vacuum would not last more than a couple of months at most. The US would not be without a leader. However, its leader would be an interim leader with limited ability to make major policy changes or act proactively at home or abroad. It might be a good time for China to stage a surprise attack on Taiwan, or for other revisionist powers like Russia, Iran, or Turkey to make aggressive moves, while the global policeman is asleep at the wheel.13 What Is The “Blue Shift” And Does It Matter? The scholar Edward Foley has called attention to the phenomenon of the “Blue Shift” as a possible pretext for President Trump to contest the election result. The blue shift is the emerging tendency for US election tallies to change significantly after election day as a result of absentee and mail-in ballots that arrive after in-person ballots are counted.14 In 2018, the Arizona senate election went from Republican, as of the tally on November 6 to Democratic as of November 12 as a result of the blue shift. This produced whiplash for Republican supporters who thought they had won (Table 6). Table 6“ Blue Shift” Means Vote Count Leans Democratic As Late Votes Arrive

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Will COVID-19 exacerbate the blue shift in 2020? While Republicans are less fearful of the virus and Democrats more enthusiastic about mail-in voting, the pandemic’s effect will be for more people in general to vote by mail, which should reduce the Democratic skew relative to previous elections. Still, there will be some Democratic skew which opens the possibility that an election that looks like a Republican win in the wee hours of November 4 could later fall to the Democrats. Foley entertains a scenario in which President Trump disputes the election on the basis of this apparent, but not real, shift in the election results. However, a blue shift would not prevent state-level election boards from correctly tallying and certifying the result. Trump can always cry foul, but only a small group of Republican supporters will believe him if the results are duly and transparently verified by a bipartisan consensus among the branches of state government. This scenario is thus governed by the points made above regarding the role of state legislatures: if a swing state’s legislature genuinely disagrees with the state’s election board or governor, then it could send its own set of electoral votes to Washington. If Republicans control the Senate, then this alternate set of electoral votes could be accepted. What Happens After A Contested Election? The constitutional power to count the Electoral College votes, and to determine the election if the college is indecisive, lies with Congress (and/or the Supreme Court). The rest is just the wailing and gnashing of teeth. This wailing and gnashing could still prove market-relevant, however. If the defeated candidate has enough popular support, he would reduce the effectiveness of the new administration. If President Trump is re-elected on any of the technicalities above, he will face an unprecedented popular opposition and social unrest, likely fanned by Biden and a unified Democratic Party. Trump’s administration would be weak at home and would only have influence abroad, creating downside for global risk assets. Polarization is extreme – the two parties will do anything to win the White House. Chart 10Republicans Will Drop Trump Like Nixon If He Loses

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

By contrast, if President Trump loses and refuses to concede, then he will actually reduce policy uncertainty in the United States. Trump’s support among Republicans is premised on his ability to win and drive through their favored policies; his support will plummet if he loses, just as Richard Nixon’s plummeted after the Watergate tapes were revealed (Chart 10). Trump could create an alt-right social media empire and serve as a gadfly, or he could lead a “rump” of the Republican Party to break away. Either way, he would divide and weaken the Republicans relative to the now-ruling Democrats, which would eventually lead to greater policy certainty. Without steady opposition, Democrats would achieve more of their agenda. This would increase risks for certain equity sectors (health care, energy), but would actually reduce polarization as the Democratic majority would more easily cooperate with moderate Republicans. The latter scenario would be hugely important. Trump could hobble the Republicans for years. This would pave the way for a Democratic ascendancy. Such an ascendancy is already possible based on trends in age, demographics, and ideology, but a serious split in the Republican Party would ensure that it comes to pass. The negative side-effect is that the populist fringe would be more likely to become disaffected or radicalized. Implications For The Long Run The advanced democracies have seen a period of relative peace and prosperity since World War II that kept their electoral disputes limited. They have sought to use multilateral institutions to promote free and fair elections across the rest of the world. But globalization has disrupted their internal political balances, particularly in the United States, making them vulnerable to governance and electoral failures usually associated with emerging and frontier markets (Table 7). Table 7Worldwide Contested Elections Rarely End Peacefully

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Even prior to COVID-19 the US had reached historic levels of political polarization. The downward spiral of partisanship began when the Soviet Union collapsed and the country no longer faced a common external enemy. The Democrats and Republicans rapidly descended into a fratricidal battle over what they thought would be world supremacy. Today polarization is exploding into open power struggle, with President Trump preemptively casting doubt on the legitimacy of the election and his challenger suggesting that the US military will have to remove him from office if he defies the election result (with prominent generals explicitly contemplating “collective action” to remove Trump).15 Social unrest is morphing into ideological and political violence in the streets. There is ample fuel for unrest and violence to intensify. The party that comes out on top of the 2020 election will have significant influence over the future, including taxing and spending, trade and foreign policy, Supreme Court picks, redistricting after the 2020 census, the fate of the Senate filibuster, and the debate over statehood for Washington, DC. If President Trump wins, it will either be narrowly, through the Electoral College, or through a contested election settled in the House of Representatives. It will prevent a new consensus forming on fiscal policy and the redistribution of wealth. The same goes for a Biden win with Republicans keeping the Senate. As such, polarization will increase for a few more years, before the next generation’s leftward political shift overtakes the Republicans. Nevertheless, while domestic policy will swing on the Senate, the next president will mostly be important in shaping US policy toward the rest of the world. In this respect, it is notable that Biden and Trump are both competing to see who is more mercantilist and protectionist. The US’s secular competition with China is likely to help cultivate national consensus on a range of policies in the coming decade. And if the Democrats win with a clean sweep – which we still see as the most likely outcome – the painful process of forming a new consensus on taxing and spending will begin in 2021. The US will have witnessed a sea change in fiscal policy as well as trade policy. Partisanship will remain high, but a strong Democratic majority on taxing and spending, combined with Democrats flagrantly coopting Trump’s stance on trade and China, looks to us like the seeds of a new national policy consensus that will reduce US political polarization over the long run. A Trump victory on a technicality will lead to a weak government and trade war. A Biden victory will have popular support and lead to higher taxes. Chart 11Stock Market Will Sell Off Amid Contested Election, As In Past

The Definitive Guide To Contested US Elections

The Definitive Guide To Contested US Elections

Unfortunately, this year and the next few years will still see polarization at extremes. It goes without saying that the US election cycle in 2020-21 will bring surprises and likely induce financial market volatility, beyond what has been seen. Judging by history, a full-fledged contested election will likely lead to a substantial equity pullback (Chart 11) – especially in a recessionary context, as in the case of the 1876 “Stolen Election.” Beyond that, Trump’s re-election would pose a major trade war risk for global assets, a boon for continued US equity outperformance relative to the world. Biden would reduce global risks, while hiking domestic risks due to higher taxes and regulation, thus encouraging the opposite effect. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 See Article II, Section I of the US Constitution. 2 See “Electoral College Instructions To State Officials,” National Archives and Records Administration, Office of the Federal Register, available at archives.gov. 3 See Article II, i and Amendment XII of the Constitution. There is some disagreement about what the constitution says regarding who does the counting. But a miscounting of the results, if the results are clear, is not credible. The vice president cannot deliberately miscount the vote, nor could Congress. However, if the results are not clear, disagreements could emerge in which the vice president could have a decisive impact. See Stephen A. Siegel, “The Conscientious Congressman’s Guide To The Electoral Count Act of 1887,” Florida Law Review 56 (2004), floridalawreview.com. Throughout this report we are highly indebted to Siegel’s authoritative study. 4 See Cook Political Report, “2020 House Race Ratings,” August 21, 2020, cookpolitical.com. 5 See for example Anna Baringer et al, “Voting by Mail and Ballot Rejection: Lessons from Florida for Elections in the Age of the Coronavirus,” University of Florida Election Science Group, August 20, 2020, electionscience.clas.ufl.edu. 6 See Amendment XII of the Constitution. 7 See Siegel, “The Conscientious Congressman’s Guide.” For the historical details in this section, see Paul F. Boller, Jr., Presidential Campaigns: From George Washington To George W. Bush (Oxford: OUP, 1984 [2004]). The House had to vote between Jefferson and his vice presidential candidate, Aaron Burr, who had the same number of electoral votes. At that time the president and vice president were not treated separately. Jefferson ultimately won when a handful of state delegations in the House abstained after several rounds of voting. Subsequently the twelfth amendment to the constitution was passed so that presidents and vice presidents were chosen separately, avoiding an Electoral College tie between two members of the same party ticket. 8 In 1800, Thomas Jefferson warned of civil war. In 1824, Andrew Jackson fumed that the will of the people had been cheated and plotted revenge, which he got in 1828. In 1876, Washington sent federal troops to monitor state election boards and some southern states threatened to rise up again. In 2000, a debatable court intervention fueled a left-wing backlash and a vicious spiral of polarization that continues to this day. 9 Here and elsewhere in this report we are indebted to Edward B. Foley, “Preparing for a Disputed Presidential Election: An Exercise in Election Risk Assessment and Management,” Loyola University Chicago Law Journal 51:2 (2019), lawecommons.luc.edu. 10 Regarding “faithless electors,” the Supreme Court this year unanimously upheld the ability of states to punish electors who break their pledge. But faithless electors are still possible, and could conceivably deprive an Electoral College winner of his victory. The 2016 election saw seven electors deviate from their party (out of 10 who tried), abnormally high. The extreme political environment is likely to produce defectors. See “Supreme Court Clarifies Rules for Electoral College: States May Restrict Faithless Electors,” Congressional Research Service, July 10, 2020, crsreports.congress.gov. 11 See “Electoral College Tie Finder,” 270 To Win, www.270towin.com. 12 See Boller, Presidential Campaigns. 13 See Admiral James A. Winnefeld and Michael J. Morell, "The War That Never Was?" US Naval Institute Proceedings 146: 8 (August 2020), usni.org. 14 See Foley, “Preparing for a Disputed Presidential Election.” This trend began with electoral reforms that made absentee balloting easier in 2002, but it is also a broader trend. Republicans tend to vote in person; those who vote through mail skew Democratic. Therefore the initial results favor Republicans, while the final results bring in a rush of ballots favoring Democrats. 15 See Brittany Bernstein, “Mattis Told Then-DNI Coats They May Be Forced to Take ‘Collective Action’ against ‘Unfit’ Trump, According to New Woodward Book,” National Review Online, September 9, 2020, nationalreview.com.

In July we first highlighted the monstrous contribution of the top five stocks to the S&P 500’s return and cautioned that such a high concentration of returns in a handful of tech titans was not sustainable. More recently, we warned again about the danger of concentrated returns, and currently the same stocks that were pushing the market higher are the ones pulling it down. In other words the pendulum is swinging the opposite way, as concentration of returns cuts both ways. Table 1 shows MAGAF stocks losses in index points since the September 2nd peak and highlights that they are responsible for 46% of total SPX losses despite having “only” a 25% market cap weight in the index. Bottom Line: A healthy rotation out of overvalued tech titans and into beaten down cyclical stocks is likely getting underway. As a reminder, in the most recent Weekly Report we went long a basket of bombed out “back to work” stocks at the expense of a “Covid-19 winners” basket. Table 1

Double-Edged Sword

Double-Edged Sword

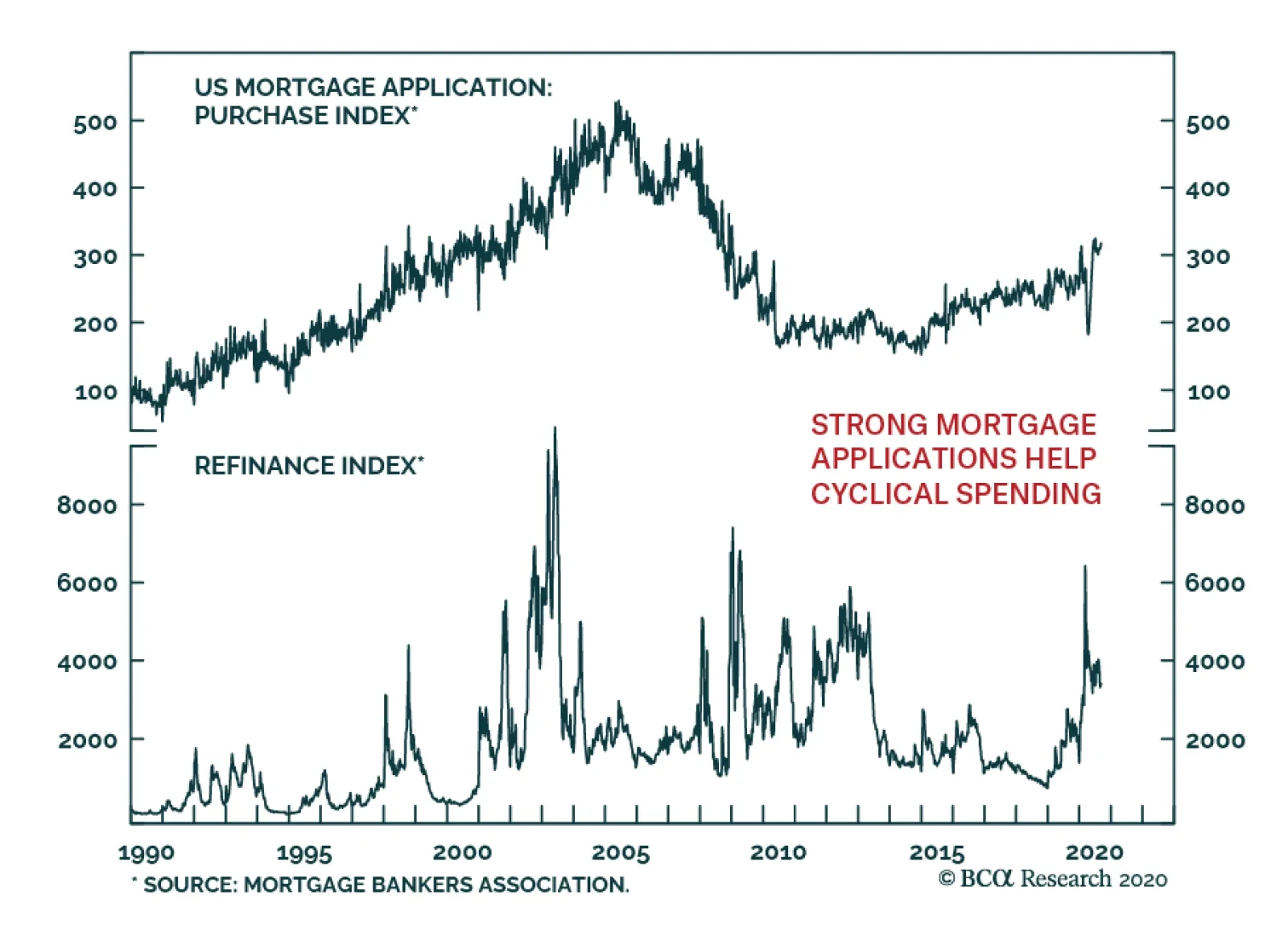

Despite the softening highlighted by the Fed Senior Loan Officers Survey, demand for mortgages remains strong. The MBA Mortgage Application Index stands at elevated levels, buoyed by both refinancing and purchase applications. This is a clear indication…

Neutral In mid-April we went overweight the S&P home improvement retail (HIR) index on the back of demand-stimulating zero interest rate monetary policy, loose fiscal policy as well as rising lumber prices. As a reminder, HIR companies make a set margin on lumber sales, hence higher lumber prices are a tonic to the industry’s top and bottom lines.

Book Gains In Home Improvement Retailers

Book Gains In Home Improvement Retailers

However, in mid-June we highlighted weakness in our HIR macro model, a hook down in existing home sales and tick up in inventories. Together, those factors compelled us to institute a stop at the 10% relative return mark, which we subsequently increased further to 15%. Last week our stop was triggered, and we booked 15% in relative gains and moved to the sidelines in home improvement retailers. Bottom Line: Downgrade the S&P HIR index to neutral and book 15% in relative gains since the mid-April inception. The ticker symbols for the stocks in this index are: BLBG: S5HOMI – HD, LOW.

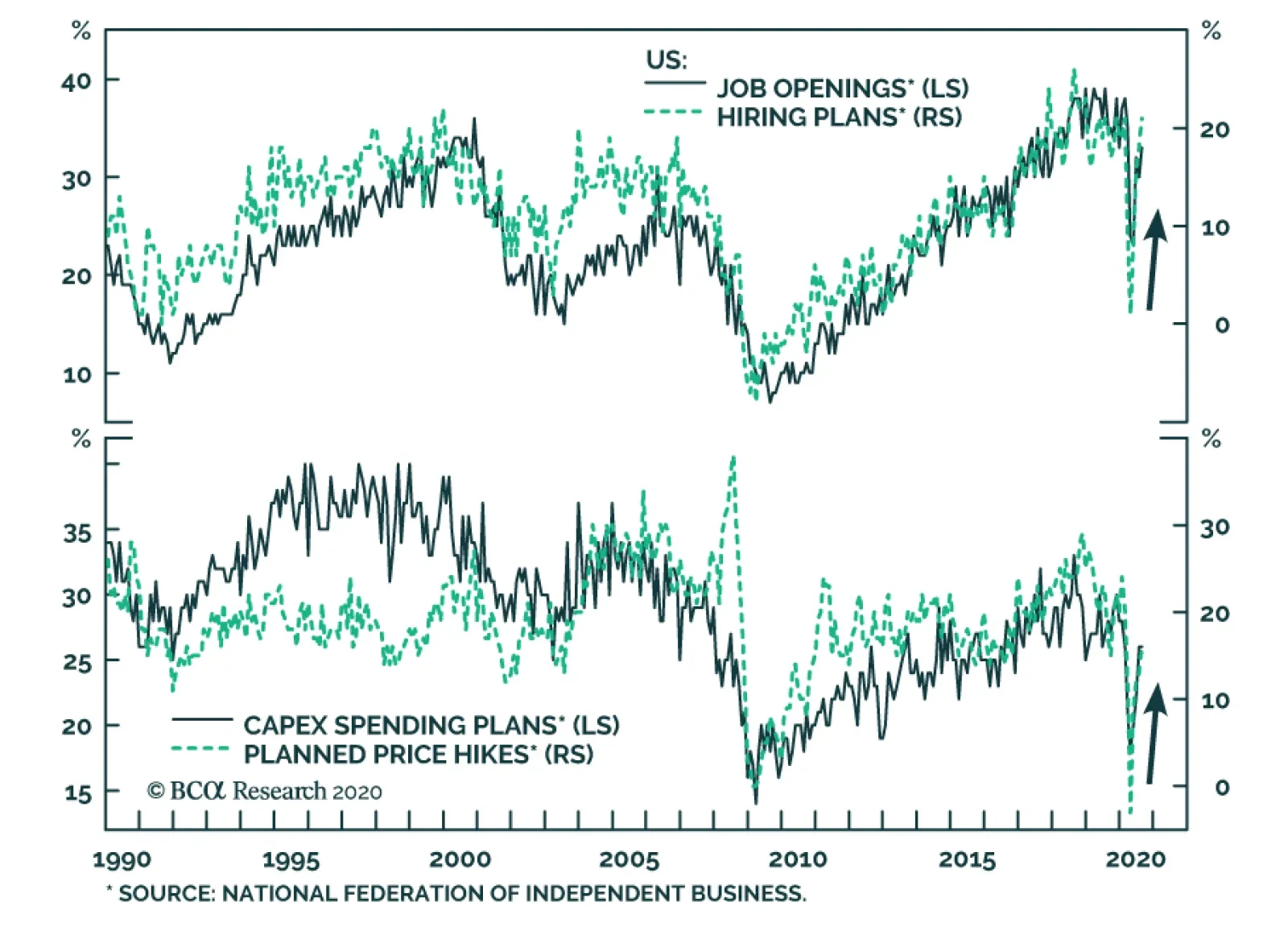

According to the NFIB Small Business Optimism Index, small US firms felt better in August. The headline index rose from 98.8 to 100.2, easily beating expectations of 99. The good news runs deeper than the headline index suggests. Naturally, as temporary…

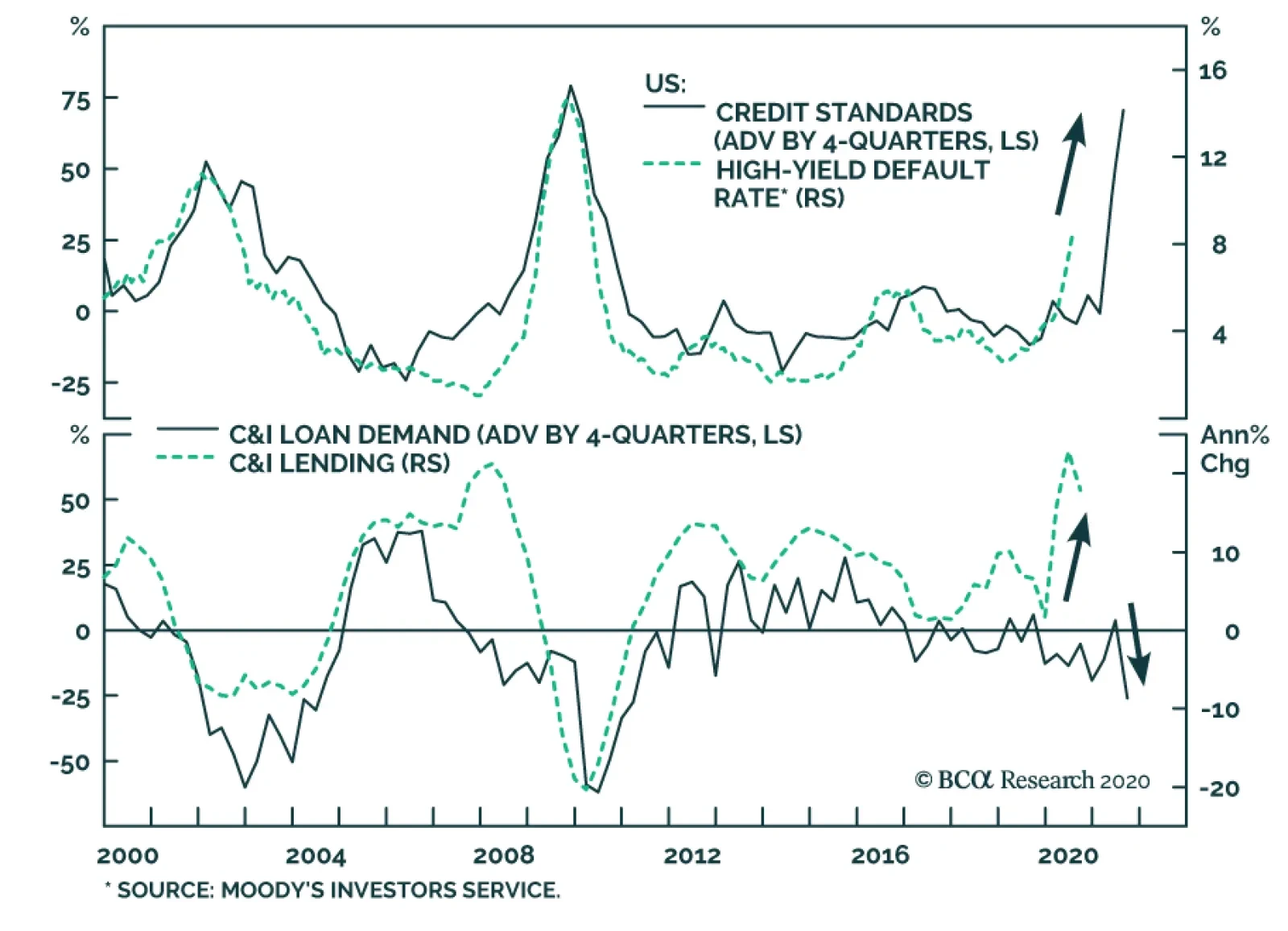

BCA Research's Global Fixed Income Strategy service assesses US credit conditions. Overall credit standards for US businesses, measured as an average of standards faced by small, medium and large firms, tightened dramatically in Q2/2020. Unsurprisingly,…

S&P 500 At 7000?

S&P 500 At…

Highlights Portfolio Strategy We are introducing a structurally constructive US equity market view with an SPX 7000 target for year 2028 on the back of peak cycle EPS of $310 and peak cycle P/E multiple of 23. The reopening of the global economy is enticing us to recommend a trade going long a basket of 14 laggard “back to work” stocks versus a basket of 14 high-flying “COVID-19 winners.” While we maintain a cyclical and secular bullish outlook on the broad market, a short-term correction due to technical and (geo) political reasons is likely in the cards. In the last segment of the Weekly Report we identify five technical reasons, in no particular order. A playable short-term pullback is in order. Recent Changes Go long a basket of 14 “back to work” stocks versus a basket of 14 COVID-19 proof stocks. Table 1

SPX 7000

SPX 7000

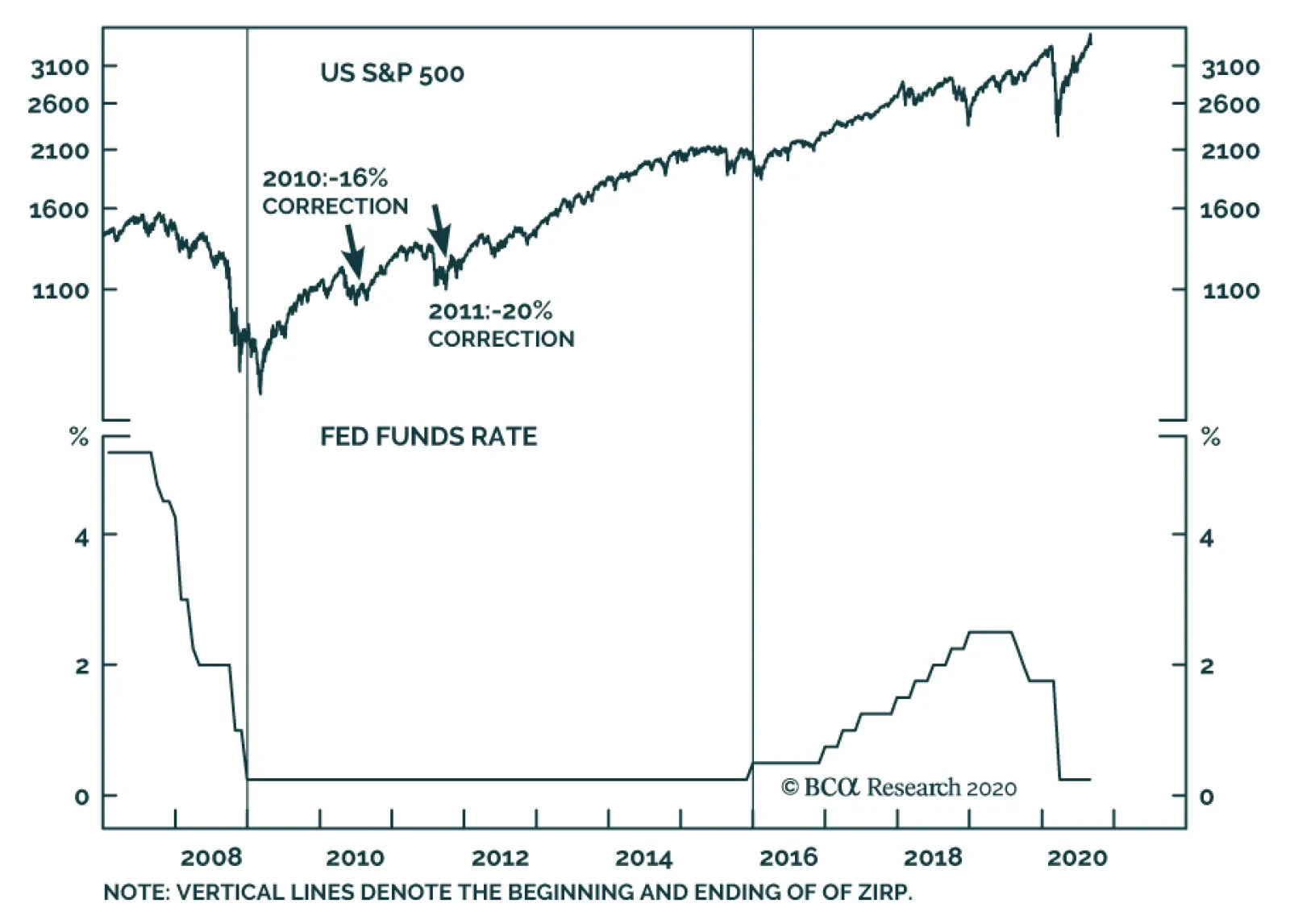

Feature Our structural target is neither a joke nor a marketing ploy. And yes, it really does read SPX 7000! This is our S&P 500 target for the year 2028. A new business cycle has commenced and with it a fresh bull market. Our secular US equity market view is bullish. Our readers can fault us for our optimistic view on the world. But we live by the Buffett maxim that “there are no short sellers in the Forbes Billionaires list.” What gives us confidence in this prima facie hyperbolic market view? The Fed’s explicit acceptance that it is ready to incur inflation risk, cementing the fed funds rate near the zero-lower bound for as long as the eye see. In the last cycle, it took the Fed seven years to lift the fed funds rate from zero, a move that ended being judged as premature and forced the Yellen-led Fed to pause for another year (bottom panel, Chart 1). Seven years. As such, there is a good chance the Fed will stay put until the year 2028, another election year. Even if it ultimately raises interest rates faster due to an overheated economy goosed up on the sweet nectar of fiscal largesse, it is highly likely to be behind the curve. Before we move on to justifying our target, some observations on ZIRP are in order. Chart 1Prolonged ZIRP Neither Eliminates Corrections…

Prolonged ZIRP Neither Eliminates Corrections…

Prolonged ZIRP Neither Eliminates Corrections…

First, the Fed’s unorthodox monetary policy (QE and ZIRP) in the last cycle did not prevent stock market corrections, including a near 20% fall in 2011 (top panel, Chart 1). In other words, we do not expect smooth sailing or a 45-degree angle line in the SPX heading to 2028. Rather, an era of volatility with a plethora of sizable corrections is upon us, but the path of least resistance will be higher. Make no mistake, we are in a “buy the dip” market now. Similar to 2008-2015, there will be a lot of fits and starts and a number of mini economic cycles will develop. Chart 2 highlights that the ISM oscillated violently during the ZIRP years and so did equity momentum and the 10-year Treasury yield. Granted, the Fed managed to suppress economic volatility as real GDP averaged ~2%/annum in the aftermath of the GFC, but mini economic cycles and profit growth scares did not disappear (top panel, Chart 3). Importantly, while the 10-year Treasury yield moved with the ebbs and flows of the ISM manufacturing survey’s readings, it remained in a downtrend and every bond market selloff proved a buying opportunity in the era of ZIRP (third panel, Chart 2). What the Fed failed to generate was inflation – of either the CPI or PCE deflator variety. In fact, the Fed has not seen core PCE price inflation overshoot 2.5% since the early 1990s (bottom panel, Chart 3). Chart 2...Nor Mini Economic Cycles

...Nor Mini Economic Cycles

...Nor Mini Economic Cycles

Chart 3“Lowflation”/Disinflation Has Been The Story Of The Past 30 years

“Lowflation”/Disinflation Has Been The Story Of The Past 30 years

“Lowflation”/Disinflation Has Been The Story Of The Past 30 years

Another feature of the ZIRP years in the last cycle was that early on easy monetary policy coincided with easy fiscal policy, as was warranted for the first few years post the GFC. Subsequently, fiscal thrust increased starting in 2016 counterbalancing the Fed’s interest rate hikes. Despite all that fiscal easing, real GDP growth peaked at 3% in 2018 before decelerating last year, raising a question mark about the long-term health of the US economy, a question to be answered in a future Special Report. Frequent readers of US Equity Strategy know our long-held view that the two primary equity market drivers have been easy fiscal and monetary policies since the March carnage. Looking ahead, the Fed has cemented the view that easy monetary policy will stay with us for quite some time. While the jury is still out on fiscal policy, it appears at the moment that profligacy has staying power as no party in Washington is campaigning on austerity or worrying about paying down the debt (save for the lone voice of the Kentucky Senator Rand Paul). The Buenos Aires Consensus is a paradigm shift, and the most important long-term consequence will be higher inflation. The US has abandoned the guardrails on populism established by the Washington Consensus – countercyclical fiscal policy, independent central banking, free trade, laissez-faire economic policy – and has adopted something… different. A new Consensus. These are extremely potent macro forces and given that there is a lag between the time both easy monetary and loose fiscal policies hit the economy, their effects will be long lasting. Especially given that they are now synchronized – unlike for large periods of the previous cycle – and undertaken at a much greater order of magnitude than after the GFC. With that macro backdrop in mind, let us circle back to our 7000 SPX target. A fresh bull market has commenced and we consider the breakout above the previous cycle’s highs as its starting point. In August, the SPX surpassed the February 19, 2020 highs, giving birth to the new bull market. Using empirical evidence since the late-1950s we conclude that, on average, the SPX doubles from its breakout point (Table 2). This gives us the SPX 7000 reading before the new bull is slayed in the plaza de toros of economic cycles. While this qualitative analysis is enticing, ultimately earnings have to deliver in order to justify the equity market’s appreciation. Put differently, easy fiscal and monetary policies the world over will deliver EPS inflation. Table 2

SPX 7000

SPX 7000

On the quantitative EPS front, we first turn to the reconstructed S&P 500 earnings back to the late-1920s. On average, EPS have grown by 7.5%/annum, effectively doubling every decade (Chart 4). Chart 4Average Annual EPS Growth Since 1920s = 7.5%

Average Annual EPS Growth Since 1920s = 7.5%

Average Annual EPS Growth Since 1920s = 7.5%

More recently, using I/B/E/S data, there have been four distinct EPS growth periods over the past four decades with different durations. From trough-to-peak, EPS have enjoyed an average CAGR of over 10% (top panel, Chart 5). Chart 5EPS Can Double In Next Eight Years

EPS Can Double In Next Eight Years

EPS Can Double In Next Eight Years

The current trough in forward EPS stands just shy of $140. Applying the average CAGR until 2028 results in a $310 EPS figure. This is our starting point of our EPS sensitivity analysis. Assigning the current forward multiple equates to an SPX terminal value of over 7000. Table 3 showcases different EPS and forward P/E multiple permutations with the grey shaded area representing our tight range of peak cycle multiples and peak EPS estimates. Table 3SPX EPS & Multiple Sensitivity

SPX 7000

SPX 7000

With regard to what is currently priced in by sell side analysts, the 5-year forward EPS growth rate – the longest duration estimate available – is near a trough reading of 10%. The historical mean is 12% since 1985, with a range of 19% near the dotcom bubble peak and a trough of 9% at the depths of the 2016 manufacturing recession (bottom panel, Chart 5). A few words on presidential cycles are relevant given our structural bullish equity market view. We first noticed Tables 4 & 5 in the WSJ in late-2016 and we have corrected some minor mistakes and updated them filling in the gaps. Drawdowns are frequent during term presidencies1 dating back to Hoover. Table 4Every Presidency Experiences Drawdowns

SPX 7000

SPX 7000

Table 5S&P 500 Returns During Presidential Terms

SPX 7000

SPX 7000

What is truly remarkable, however, is that since the late-1920s only three term presidencies ended up in the red. What the WSJ article did not mention was that in all three market declines GOP presidents were at the helm and had taken over at/or near all-time highs in the SPX! This represents a risk to our SPX 7000 view. If President Trump wins the upcoming election, given the recent modest recovery in the polling, he could meet the same fate as his Republican predecessors. Our sister Geopolitical Strategy service still assigns 35% probability for the incumbent to remain in office, a solid figure that suggests the race remains close. Importantly, while we believe a transition to a Democratic president will be tumultuous as we have been cautioning investors recently, a Biden presidency along with the possibility of a “Blue Wave” will bode well for the long-term prospects of the US equity market, if history at least rhymes. BCA’s Geopolitical strategist Matt Gertken assigns 65% odds to a Biden win and 55% to a Blue trifecta. Finally, on a technical note, the recent megaphone formation has stirred a lot of debate among technical analysts in the blogosphere and is eerily reminiscent of a similar formation that lasted from 1965 until 1975. Typically, these megaphone formations get resolved/completed by a diamond formation (Chart 6). Chart 6Of Megaphones And Diamonds

Of Megaphones And Diamonds

Of Megaphones And Diamonds

While this points to a selloff in the broad equity market in the near-term, which is in accordance with our tactically cautious view (please see the last section of this Weekly Report), it is very bullish for the long-term, as equities catapult higher from such a diamond base formation (Chart 7). In other words, odds are much higher that the SPX will hit 7000 first, before it ever revisits 2200. Adding it all up, we are introducing a structurally constructive US equity market view with an SPX 7000 target for year 2028 on the back of peak cycle EPS of $310 and peak cycle P/E multiple of 23. Chart 7Diamond Base Is Long Term Bullish

Diamond Base Is Long Term Bullish

Diamond Base Is Long Term Bullish

This week we recommend a basket of 14 stocks to play the “back to work” reopening of the global economy versus a basket of 14 "COVID-19 winners". We also reiterate our view not to chase the broad equity market higher in the short-term and back it up with five key technical reasons. “Back To Work” Versus “Stay At Home” Today we recommend buying a basket of 14 stocks levered to the economic reopening and the “back to work” theme, at the expense of a basket of 14 “COVID-19 winners” stocks. There is no question that we are in a V-shaped economic recovery, partly due to arithmetic, i.e. base effects. The severe blow to the economy that the pandemic-induced shutdowns inflicted is reversing violently. Easy monetary and loose fiscal policy have been a tonic and are allowing enough time for the economy to heal and stand on its own two feet. Chart 8 shows a number of economic variables that are in this V-shaped recovery. Our sense is that there will be a rotation out of mostly high-flying tech titans and select health care COVID-19 beneficiaries and into laggard stocks that would benefit from the reopening of the global economy. The transition to these stocks will be anything but smooth, however, it is a necessary precondition for the continuation of the rally late in the year post the election and into 2021. Clearly, the "COVID-19 winners" have stolen demand from the future. Now that the working-from-home setup is nearly complete for most workers, the pendulum is likely to swing in the opposite direction. In other words, at the margin, employees will slowly start to return to work and the economic reopening should serve as a catalyst for this rotation. Chart 8V-Shapes Galore

V-Shapes Galore

V-Shapes Galore

Chart 9Buy "Back To Work" Stocks

Buy “Back To Work” Stocks

Buy “Back To Work” Stocks

Importantly, a definitive vaccine breakthrough will assist some of the beaten down stocks and sectors that at some point were priced for bankruptcy. We remain hopeful that such positive news will soon hit the tape. As a result, this will unleash a stream of bargain hunters out of the woodwork in favor of “back to work” equities and send short sellers reeling. Ultimately, the violent recovery in relative earnings forecasted by the sling shot recovery in the ISM manufacturing survey and most of its subcomponents will boost the “back to work” basket at the expense of the “COVID-19 winners” (Chart 9). For the “back to work” basket we have selected two airlines, two hotels, two oil producers, two restaurant operators, two capital goods manufacturers, two credit card companies, an automobile manufacturer, and a steel producer. In contrast, the “COVID-19 winners” basket that we first created in mid-March currently includes: a bankruptcy consultant, a software company that enables remote access, three grocers, a tele-medicine company, two biotech giants, a Big Pharma company, the biggest online store in the US, an online streaming service company, a teleconferencing company, and finally two household/cleaning products leaders. Bottom Line: Go long a basket of 14 “back to work” stocks at the expense of 14 “COVID-19 winners” equities. The ticker symbols for the stocks in the US Equity Strategy “back to work” basket are: LUV, DAL, MAR, HLT, CVX, EOG, SBUX, MCD, CAT, HON, AXP, COF, NUE, GM. The ticker symbols for the US Equity Strategy “COVID-19 winner” basket are: TDOC, FCN, ZM, CTXS, JNJ, AMGN, REGN, CLX, RBGLY, WMT, COST, KR, NFLX, AMZN. Five Reasons Not To Chase Equities In the Near-Term Over the past weeks, we have been cautioning investors not to chase the equity market higher as the risk/reward trade-off at current levels is tilted to the downside. While we maintain a 9-12 month bullish view on the broad market, a short-term correction due to technical and/or (geo) political reasons is likely in the cards. Consequently, patient investors will be rewarded with a compelling entry point likely in the coming months. Below are five reasons, in no particular order, arguing that a playable short-term pullback is in order: Reason #1: The 200-day Moving Average Moving averages are a perfect tool to put the speed of any rally in perspective and to highlight extreme investor optimism. Chart 10 shows standardized SPX and Nasdaq 100 (NDX) price ratios with respect to their 200-day moving averages. If we look at the current cycle, whenever both the SPX and NDX crossed above the one standard deviation (std) line, a sizable pullback was quick to follow. While NDX has been well above its 1 std line for some time, last week’s price action finally pushed the SPX into the overstretched column. The implication is that a correction is looming. Chart 10Overstretched

Overstretched

Overstretched

Reason #2: Monthly Moving Averages For the second reason, we look at the concept of price deviations from the moving average through a different lens – Bollinger bands (BBs). A traditional (20,2) BB includes a 20-period moving average of the price, as well as 20-period 2-standard standard deviation lines. While it can be plotted on any time frame, we use monthly data as set ups in longer time frames (i.e. monthly) dictate the behavior of the shorter (i.e. daily) time frames. Chart 11 shows the S&P 500 together with its (20,2) BBs on a monthly time frame. Whenever the market spikes above the 2 std line, a sizable correction ensues. Currently, the market is squarely above the 2 std line, which has historically been a precursor to a 5-10% drawdown. Chart 11Too Far Too Fast

SPX 7000

SPX 7000

Reason #3: Growth/Value Staying on the topics of extreme rallies, Chart 12 shows the year-over-year growth rate in the S&P growth / S&P value share price ratio. In the entire history of the data, never has it printed a jaw-dropping 34% growth rate, not even after the depths of GFC or to the lead up to the dotcom March 2000 peak. Such a pace is clearly not sustainable and since growth stocks are dominated by FAANG-like companies that have done all of the heavy lifting year-to-date, a reset in the S&P growth / S&P value ratio will weigh on the overall market. A selloff in the bond market will likely serve as a catalyst to boost the allure of beaten down value stocks at the expense of overvalued tech titans. Chart 12In Need Of A Breather

In Need Of A Breather

In Need Of A Breather

Reason #4: Options/Volatility Markets Option and related volatility market movements reveal some vulnerabilities in the broad equity market. More specifically, the VIX and the VXN which by construction are inversely correlated with the S&P 500 and NASDAQ 100, respectively, serve as an excellent timing tool. We look at the 20-day moving correlation of those respective variables, and similarly to Reason #1, a reliable sell signal is given once both (VIX, SPX) and (VXN, NDX) 20-day moving correlations shoot into positive territory (Chart 13). While the (VXN, NDX) correlation has been going haywire over the past quarter as likely single stock call option buying has been heavily hedged by NDX put buying, the (VIX, SPX) moving correlation only slingshot higher at the end of last week - finally producing a decisive sell signal. Again, similarly to Reason #2, each sell signal resulted into a sizable correlation in the SPX, warning that a 5-10% pullback – the sixth since the March lows – is inevitable in the coming weeks. Chart 13Unsustainable Correlation

Unsustainable Correlation

Unsustainable Correlation

Reason #5: Bad Breadth Tech stocks have clearly been the work horse behind this rally pushing markets into uncharted territory in a very short period of time since the March lows. However, and as we highlighted in our previous research, it is only a handful of tech titans that propelled the markets to all-time highs. Overconcentration of returns in just a few tickers is not healthy, and a reset is only a question of time. Chart 14 highlights that today only 58% of NASDAQ Composite stocks are trading above their respective 50-day moving average, which stands in marked contrast to the all-time highs in the NASDAQ Composite. Such a divergence is unsustainable and typically gets resolved by a snap back in equity prices. While Chart 14 cannot be used as a precise timing tool, it has been consistently leading the NASDAQ Composite especially at peaks, cautioning that a healthy pullback is forthcoming. Chart 14Bad Breadth

Bad Breadth

Bad Breadth

Bottom Line: While we maintain a cyclical and structural stance in the broad equity market, the shorter-term risk/reward trade-off is tilted to the downside, and presents a playable opportunity. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Footnotes 1 By term presidencies we are referring to the different duration of Presidents staying in office. Current Recommendations Current Trades Strategic (10-Year) Trade Recommendations

Drilling Deeper Into Earnings

Drilling Deeper Into Earnings

Size And Style Views July 27, 2020 Overweight cyclicals over defensives April 28, 2020 Stay neutral large over small caps June 11, 2018 Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, TSLA, V). January 22, 2018 Favor value over growth

To all clients, Next week, in lieu of publishing a regular report, I will be hosting a webcast on September 15th at 10 am EDT, discussing our latest views on global fixed income markets. Sign up details for the Webcast will arrive in your inboxes later this week. Best regards, Robert Robis, Chief Fixed Income Strategist Feature Much of the global rebound in economic activity, and recovery in equity and credit markets, seen since the COVID-19 shock earlier this year can be attributed to historic levels of monetary and fiscal stimulus. However, the effective transmission of various monetary policy measures such as liquidity injections and refinancing operations, and by extension a sustained global recovery, is dependent on the continued smooth flow of credit from lenders to borrowers. As such, the tightening in bank lending standards seen across developed markets in the second quarter of 2020 could imperil the recovery if banks remain cautious with borrowers (Chart 1). Chart 1Credit Standards Across Developed Markets

Introducing The GFIS Global Credit Conditions Chartbook

Introducing The GFIS Global Credit Conditions Chartbook

This week, we are introducing the BCA Research Global Fixed Income Strategy (GFIS) Global Credit Conditions Chartbook—a review of central bank surveys of bank lending standards and loan demand. We will be publishing this chartbook on an occasional basis going forward to help inform our fixed income investment recommendations. Where it is relevant to our analysis, we will also make special note of the one-off questions asked in some of these surveys that are germane to the economic situation at hand. Where To Find The Bank Lending Surveys A number of central banks publish regular surveys of bank lending conditions in their domestic economies. The surveys, and the details on how they are conducted, can be found on the websites of the central banks: US Federal Reserve: https://www.federalreserve.gov/data/sloos.htm European Central Bank: https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/html/index.en.html Bank of England: https://www.bankofengland.co.uk/credit-conditions-survey/ Bank of Japan: https://www.boj.or.jp/en/statistics/dl/loan/loos/index.htm/ Bank of Canada: https://www.bankofcanada.ca/publications/slos/ Reserve Bank of New Zealand: https://www.rbnz.govt.nz/statistics/c60-credit-conditions-survey US Chart 2US Credit Conditions

US Credit Conditions

US Credit Conditions

Overall credit standards for US businesses, measured as an average of standards faced by small, medium and large firms, tightened dramatically in Q2/2020 (Chart 2). Unsurprisingly, gloomier economic outlooks, reduced risk tolerance, and worsening industry-specific problems were the top reasons cited by US banks for tightening standards. US banks reported that commercial and industrial (C&I) loan demand from all firms also weakened in Q2, owing to a decrease in customers’ inventory financing and fixed investment needs. This suggests that the surge in actual C&I loan growth data during the spring was fueled by companies drawing down credit lines to survive the lack of cash flow during the COVID-19 lockdowns and should soon peak. Standards for consumer loans tightened significantly in Q2, as well. A continuation of this trend would pose a major risk to the US economic recovery, given the still fragile state of US consumer confidence. Business lending standards typically lead US high-yield corporate bond default rates by about one year, suggesting that defaults will continue to climb over the next few quarters (Chart 2, top panel). Tightening US junk bond spreads have ignored the rising trend in defaults and now provide no compensation for the likely amount of future default losses, suggesting poor value in the overall US high-yield market (Chart 3). Turning to the real estate market, lending standards have tightened significantly for both commercial and residential mortgage loans (Chart 4). In a special question asked in the Q2 survey, US banks indicated that lending standards for both those categories are at the tighter end of the range that has prevailed since 2005. Business lending standards typically lead US high-yield corporate bond default rates by about one year, suggesting that defaults will continue to climb over the next few quarters. Chart 3US Junk Spreads Do Not Compensate For Default Risk

US Junk Spreads Do Not Compensate For Default Risk

US Junk Spreads Do Not Compensate For Default Risk

Chart 4The White Picket Fence Is Looking Out Of Reach

The White Picket Fence Is Looking Out Of Reach

The White Picket Fence Is Looking Out Of Reach

Euro Area Italy is seeing the greater benefit from ECB support, however, with loan growth now at a new cyclical high. Chart 5Euro Area Credit Conditions

Euro Area Credit Conditions

Euro Area Credit Conditions

In contrast to the US, credit standards actually eased slightly in the euro area in Q2/2020 (Chart 5). Banks reported increased perceptions of overall risk from a worsening economic outlook, but that was more than offset by the massive liquidity and loan guarantee programs that were part of the policy response to the COVID-19 recession. Going forward, banks expect lending standards to tighten as the maximum impact of those policies begins to fade. Credit demand from firms rose in Q2, driven by acute liquidity needs during the COVID-19 lockdowns. At the same time, demand for longer-term financing for capital expenditure was very depressed. Banks expect credit demand to normalize in Q3, as easing lockdown restrictions dampen the immediate need for liquidity. Credit demand from euro area households plummeted in Q2. Banks reported that plunging consumer confidence was the leading cause of decline in credit demand, followed closely by reduced spending on durable goods. Consumer confidence has already rebounded and banks expect demand to follow suit, as economies re-open and spending opportunities return. Chart 6HY Spreads In The Euro Area Are Unattractive

HY Spreads In The Euro Area Are Unattractive

HY Spreads In The Euro Area Are Unattractive

As with the US, we expect that tighter credit standards to firms will drive up euro area high-yield default rates. Current euro area high-yield spreads offer little compensation for the coming increase in default losses, suggesting a similar poor valuation backdrop to US junk bonds (Chart 6). Looking at the four major euro area economies, credit standards eased across the board in Q2, with the largest moves seen in Italy and Spain (Chart 7). The ECB’s liquidity operations have helped support lending in those countries, each with a take-up from long-term refinancing operations (LTROs) equal to around 14% of total bank lending (Chart 8). Italy is seeing the greater benefit from ECB support, however, with loan growth now at a new cyclical high and Spanish banks projecting a much sharper tightening of lending standards in Q3 relative to Italian banks. Chart 7Loan Growth Accelerating Across Most Of The Euro Area

Loan Growth Accelerating Across Most Of The Euro Area

Loan Growth Accelerating Across Most Of The Euro Area

Chart 8Italy & Spain Taking Full Advantage Of LTROs

Italy & Spain Taking Full Advantage Of LTROs

Italy & Spain Taking Full Advantage Of LTROs

UK For consumers, UK banks are projecting loan demand to improve in Q3, although that will require a sharper rebound in consumer confidence than has been seen to date. Chart 9UK Credit Conditions

UK Credit Conditions

UK Credit Conditions

In the UK, corporate credit standards eased significantly in Q2 2020 thanks to the massive liquidity support programs provided by the UK government (Chart 9). Lenders reported a larger proportion of loan application approvals from all business sizes, with the greatest improvements seen in small businesses and medium-sized private non-financial corporations (PNFCs). However, lenders indicated that average credit quality on new PNFC borrowing facilities had actually declined, with default rates increasing, for all sizes of borrowers. This divergence between increased lending and declining borrower creditworthiness attests to the impact of the UK’s substantial liquidity provisions in response to the COVID-19 shock. The credit demand side mirrors the supply story with a massive spike in Q2 2020. In contrast to euro area counterparts, UK businesses reportedly borrowed primarily to facilitate balance sheet restructuring. However, as with the euro area, the story for Q3 is much more bearish. Banks are projecting credit standards to turn more restrictive as stimulus programs run out and borrowers rein in credit demand. Going forward, decreasing risk appetite of UK banks will likely contribute to a tightening in lending standards. For consumers, UK banks are projecting loan demand to improve in Q3, although that will require a sharper rebound in consumer confidence than has been seen to date. UK banks surprisingly reported that the average credit quality of new consumer loans improved in Q2, suggesting that consumer loan demand could rebound strongly in Q3 as lockdown restrictions fade. Japan Perversely, the latest improvement in Japanese business optimism could translate to lower business loan demand going forward. Chart 10Japan Credit Conditions

Japan Credit Conditions

Japan Credit Conditions

Before the pandemic hit, credit standards in Japan were in a structural tightening trend for both firms and households (Chart 10). Fiscal authorities have taken a number of measures to ease conditions for businesses, including low interest rate loan programs and guarantees for large businesses as well as small and medium-sized enterprises, which has translated into the easiest credit standards for Japanese firms since 2005. The correlation between business loan demand and business conditions is not as clear-cut in Japan compared to other countries. Japanese firms tend to borrow more when the economic outlook is poor, indicating that loans are being used to meet emergency funding or restructuring needs rather than being put towards capital expenditure or inventory financing. Perversely, the latest improvement in Japanese business optimism could translate to lower business loan demand going forward. However, the consumer picture is a bit more conventional—consumer loan demand and confidence tend to track quite closely. While consumer confidence has yet to stage a convincing rebound, it has clearly bottomed. The more positive projections for consumer loan demand from the Japan bank lending survey seem to confirm this message. Canada And New Zealand In Canada, business lending standards tightened in Q2/2020 as loan growth slowed (Chart 11). Although loan growth is far from contracting on a year-on-year basis, further tightening in conditions could pose an obstacle to Canadian recovery. On the mortgage side, the Canadian government has been active in easing pressures for lenders by relaxing loan-to-value requirements for mortgage insurance, making it easier for them to collateralize and sell their assets to the Canadian Mortgage and Housing Corporation (CMHC). Although this has yet to translate to the standards faced by borrowers, residential mortgage growth remains buoyant. In New Zealand, credit standards for firms (including both corporates and SMEs) tightened significantly in Q2 (Chart 12). Many banks expect to apply tighter lending standards to borrowers in industries most impacted by the pandemic, such as tourism, accommodation, and construction. Demand for credit from firms was driven by working capital needs while capital expenditure funding demands fell drastically. Chart 11Canada Credit Conditions

Canada Credit Conditions

Canada Credit Conditions

Chart 12New Zealand Credit Conditions

New Zealand Credit Conditions

New Zealand Credit Conditions

On the consumer side, residential mortgage standards increased somewhat, and banks expect to perform more due diligence on income and job security. The hit to credit demand was broad-based across credit card, secured, and unsecured lending and coincided with a sharp fall in loan demand. Shakti Sharma Research Associate ShaktiS@bcaresearch.com Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Introducing The GFIS Global Credit Conditions Chartbook

Introducing The GFIS Global Credit Conditions Chartbook

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Chart 1Permanent Job Losses Still Rising

Permanent Job Losses Still Rising

Permanent Job Losses Still Rising

The biggest event in bond markets last month was the Fed’s shift toward a regime of average inflation targeting. Treasuries sold off in the days following the announcement and, overall, the Bloomberg Barclays Treasury index underperformed cash by 111 basis points in August (Chart 1). We view this market reaction as sensible, since it seems clear that the Fed’s new commitment to tolerate an overshoot of its 2% inflation target will be bearish for bonds in the long run. However, for this bond bear market to play out the US economy must first generate some inflation. This will take time. Despite the drop in the headline U3 unemployment rate, August’s employment report showed that permanent job losses continue to rise (bottom panel). This is a clear sign that the economic recovery is not yet on a solid footing. We advise bond investors to keep portfolio duration close to benchmark for the time being. We also recommend several yield curve trades across the nominal, real and inflation compensation curves (see pages 10 & 11). Feature Investment Grade: Overweight Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview