United States

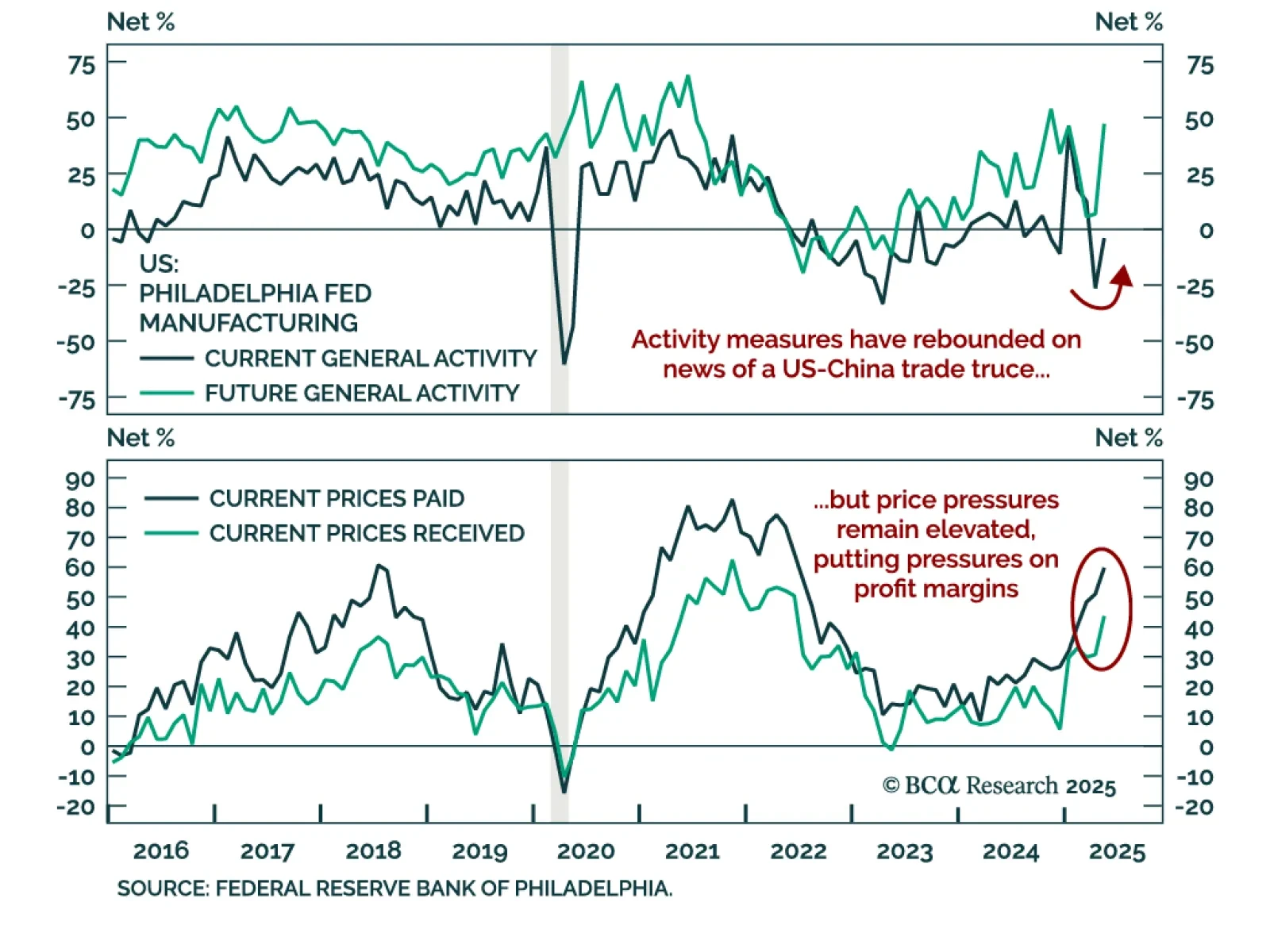

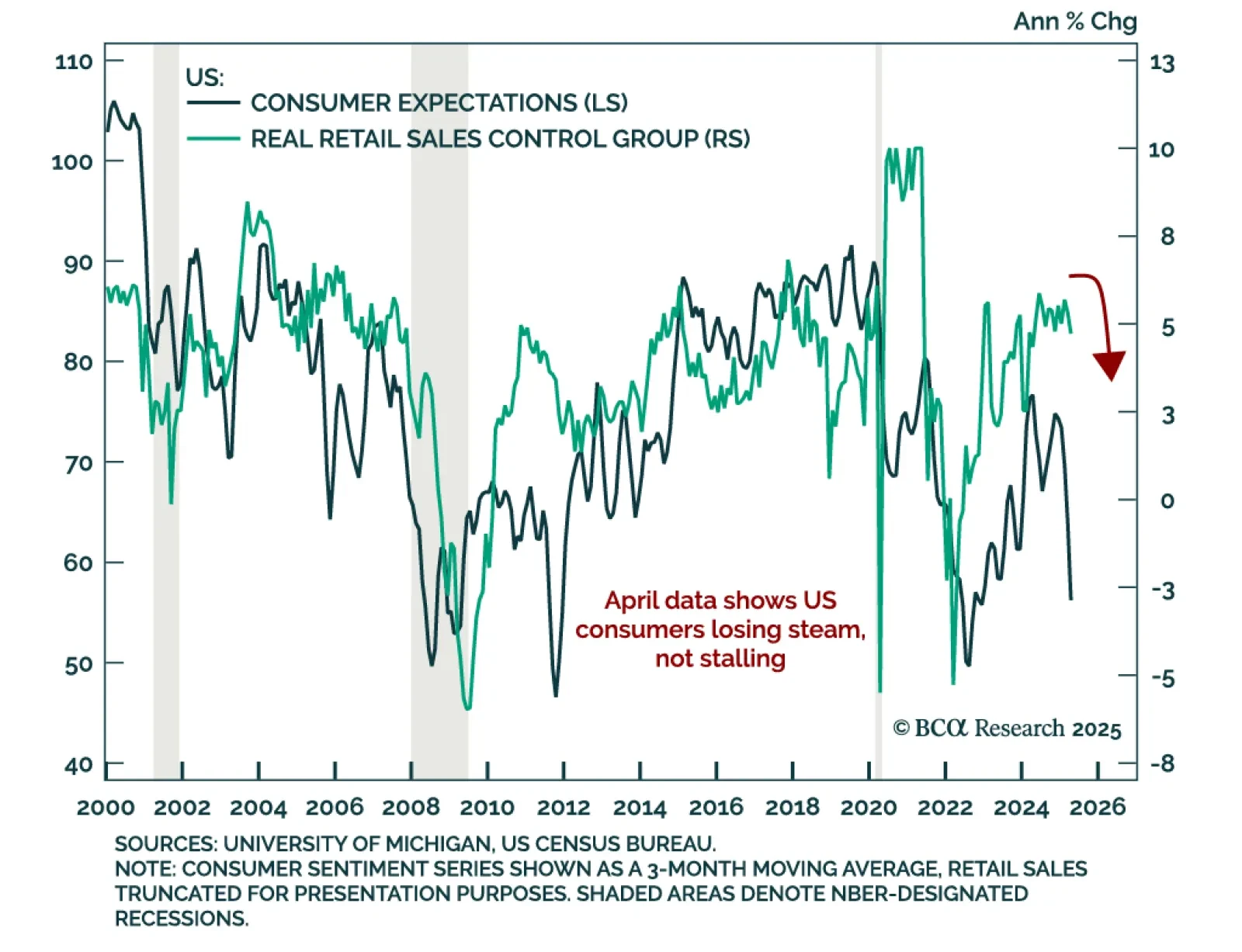

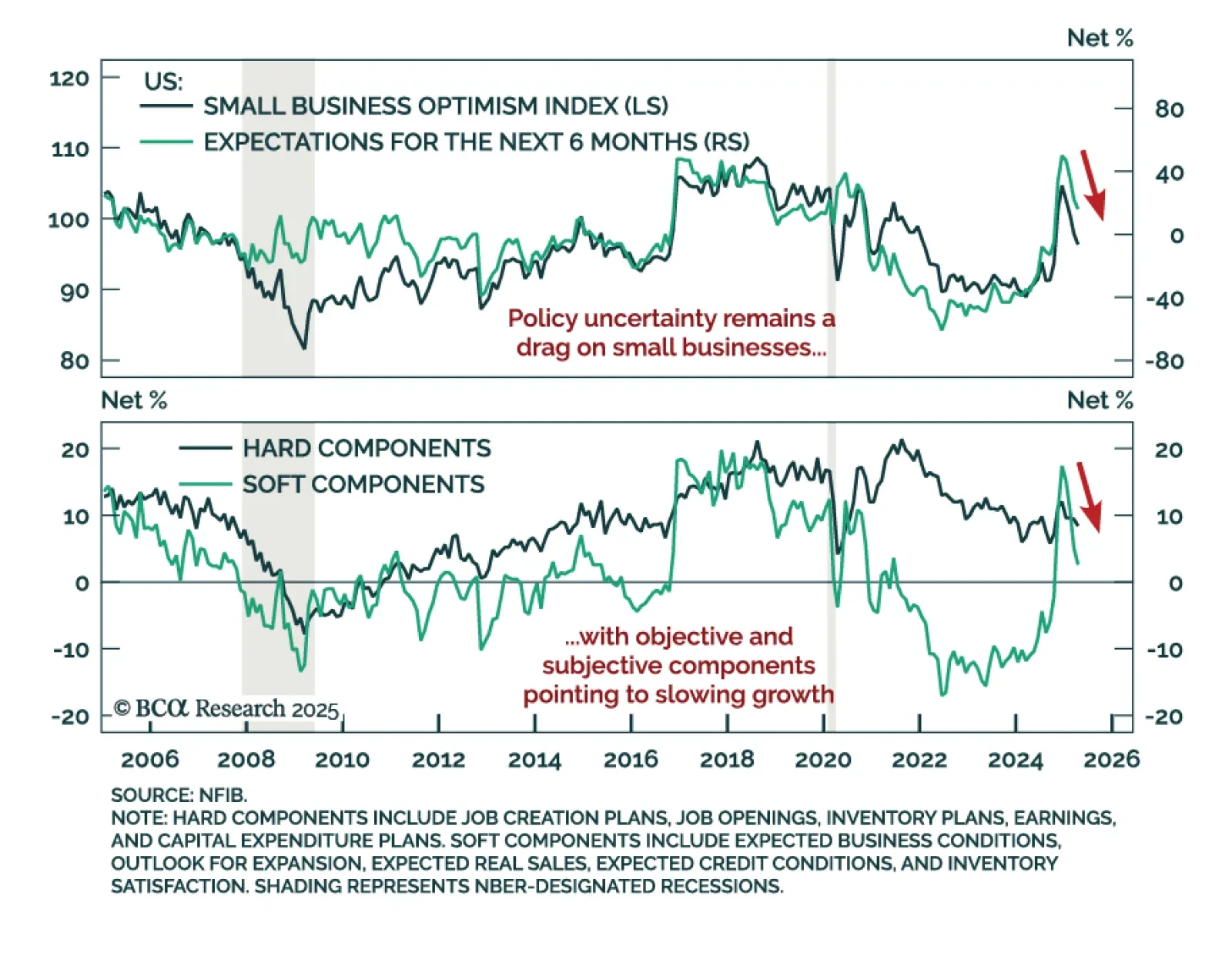

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.

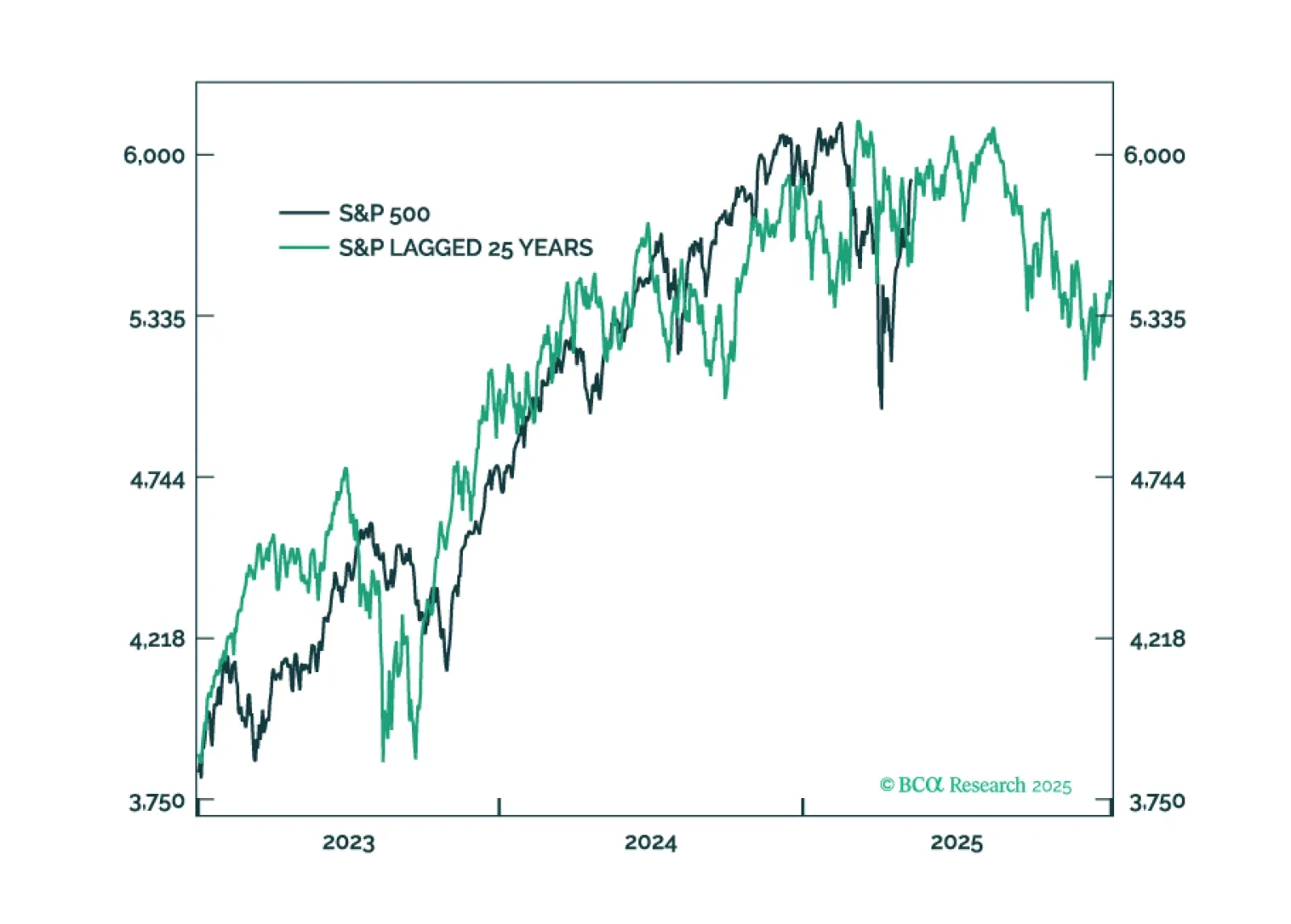

This year’s plunge in tech stocks followed by the recent strong countertrend rally is eerily reminiscent of 2000. But the market and economic parallels between 2025 and in 2000 run much deeper. This report lists 10 striking parallels between 2025 and 2020, then highlights some important differences, and ends by describing how the rest of 2025 might unfold based on a playbook that is: 2025 = ‘2000 with some tweaks.’

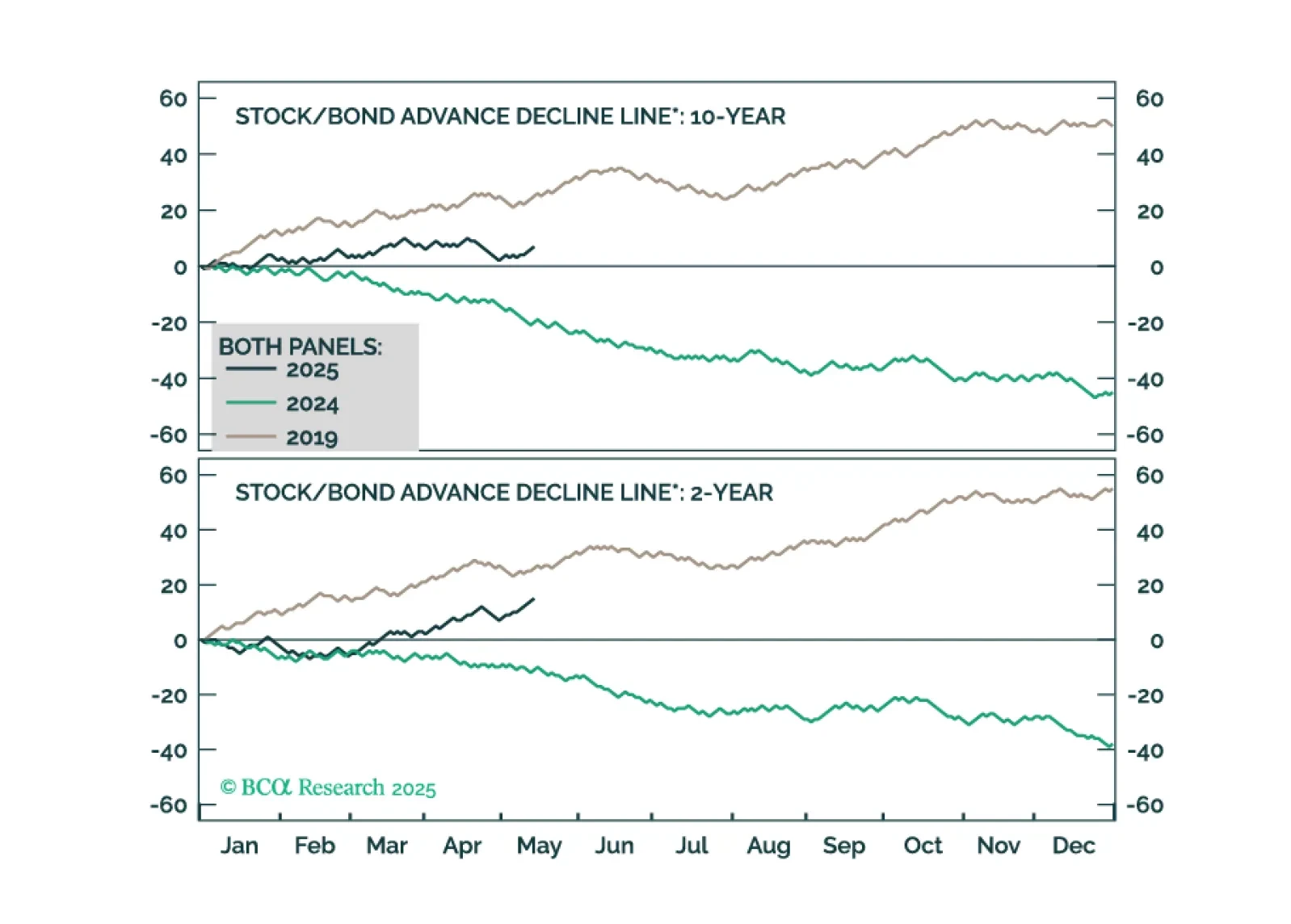

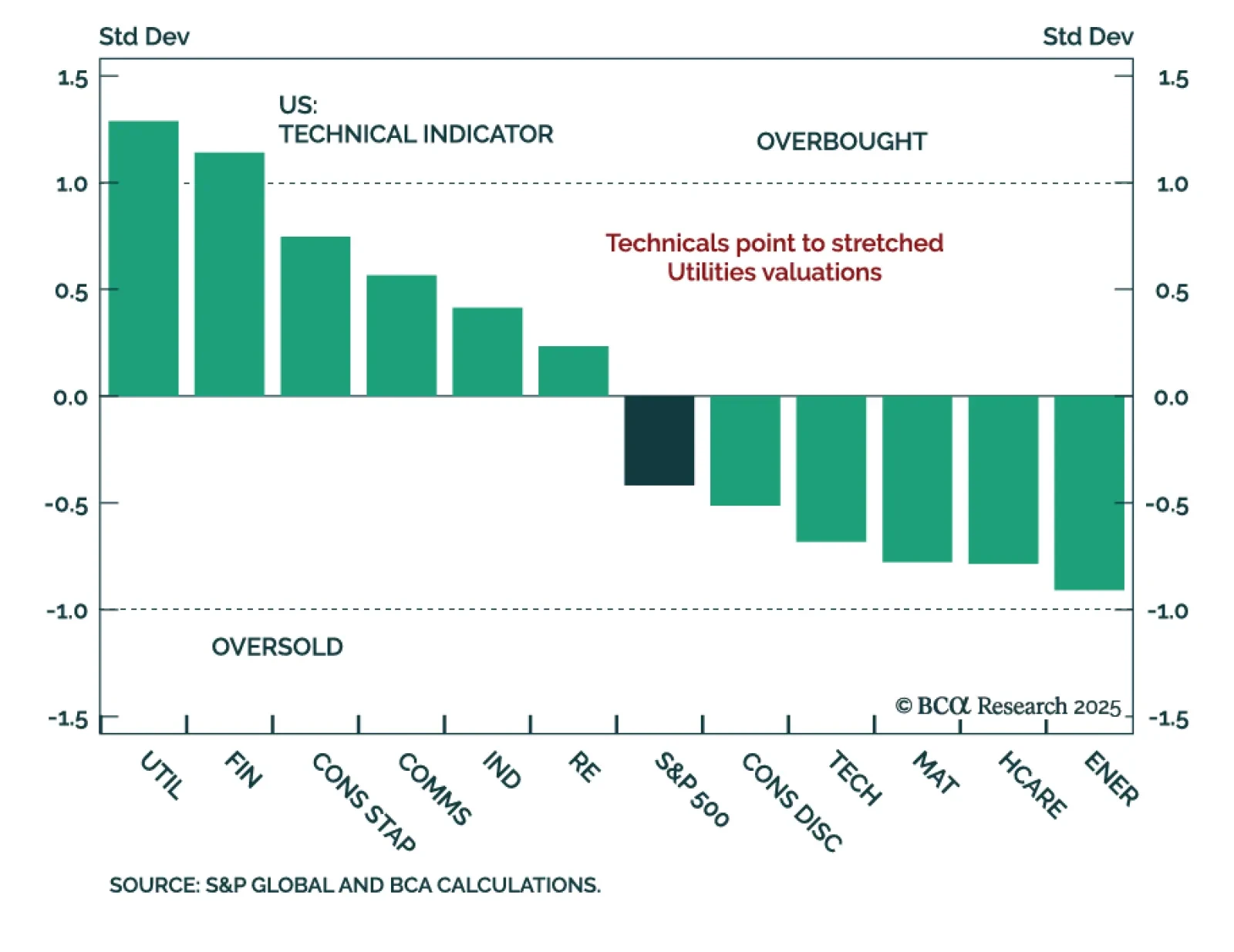

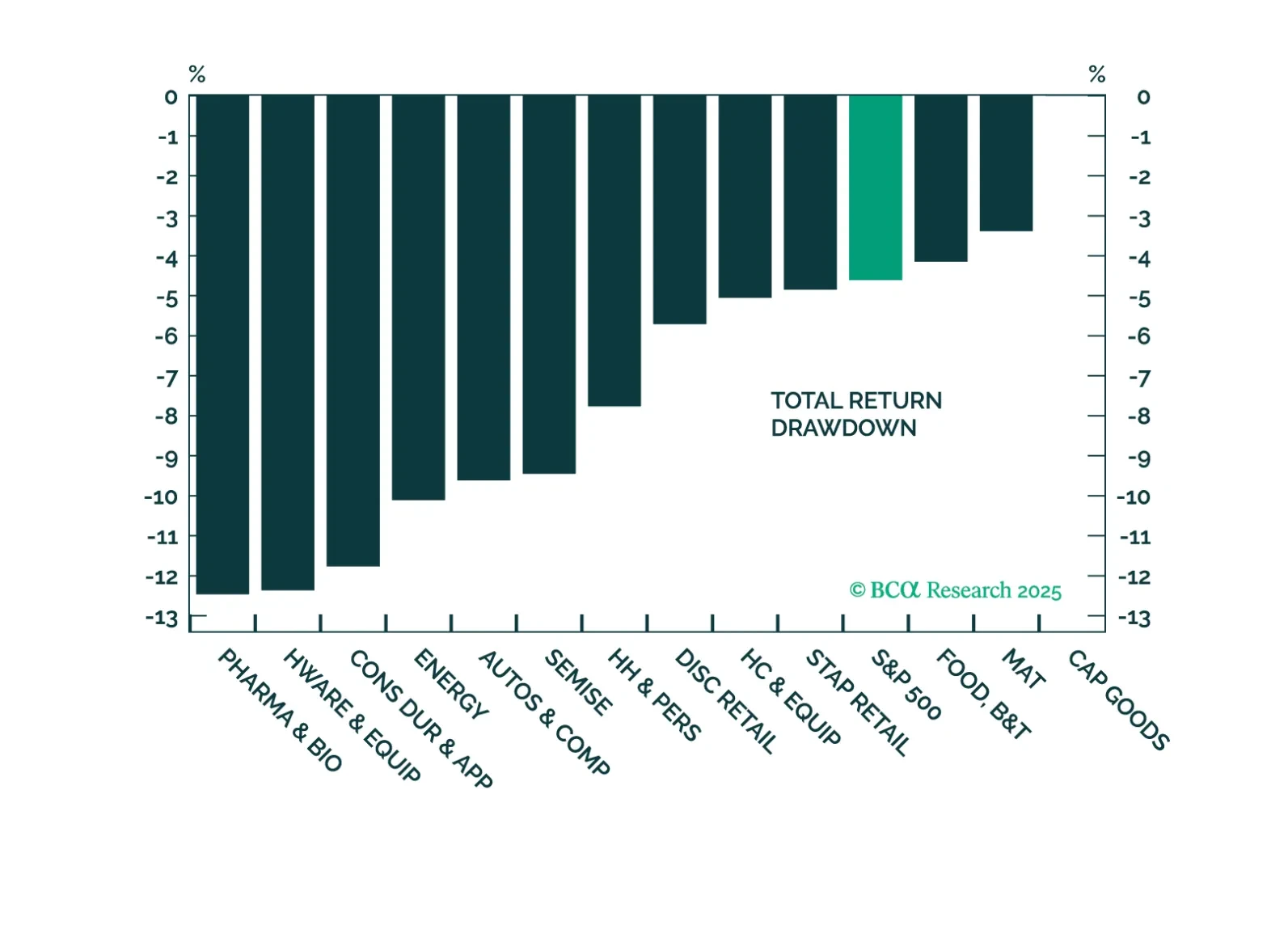

Markets are pricing out the worst trade policy fears, and while tariffs will still dent earnings, the impact looks smaller than initially feared. With sector rotation gaining traction and oversold names rebounding, we are adjusting our portfolio to reflect the rotation thesis.