United States

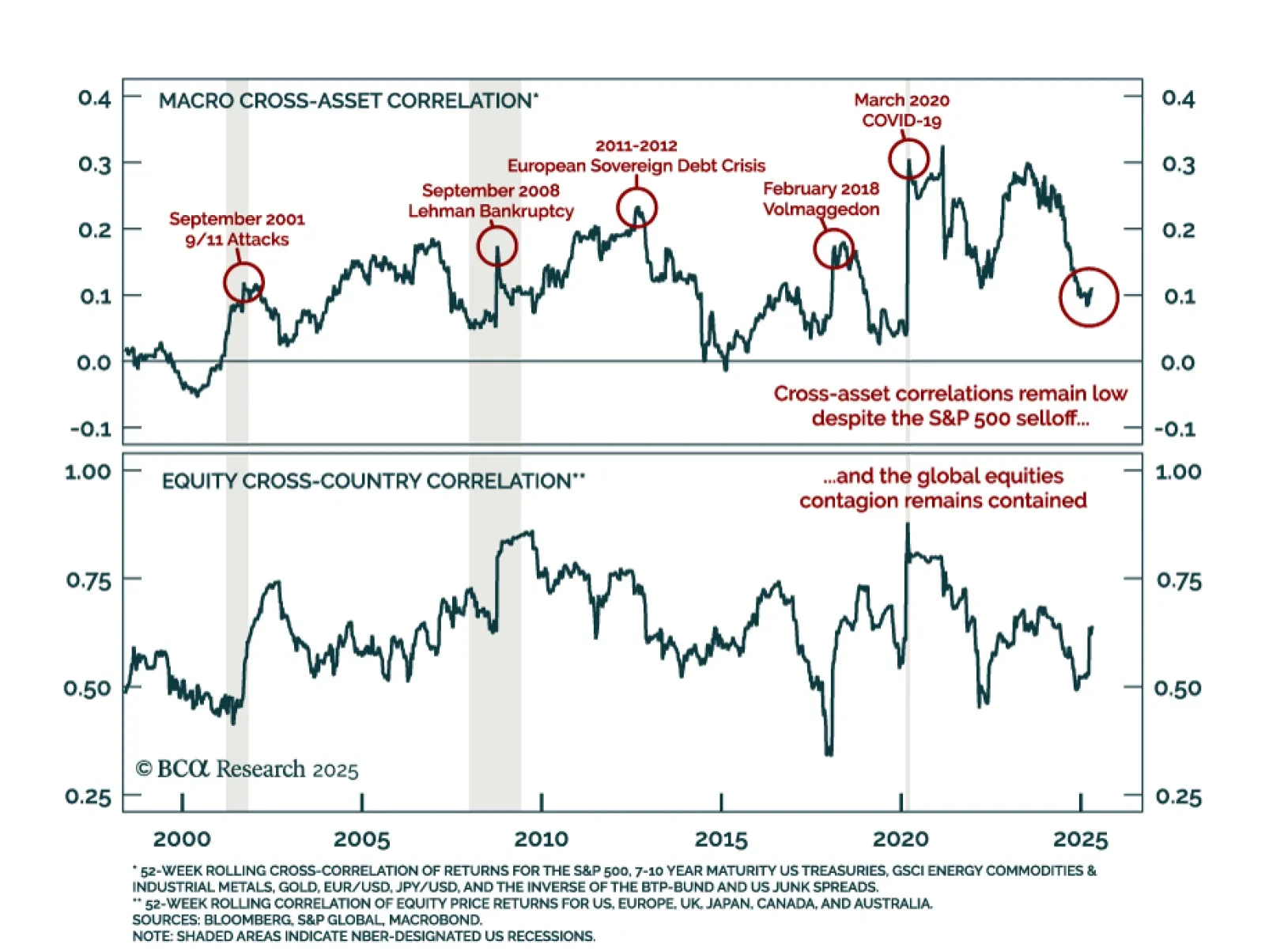

Cross-asset signals remain distorted by policy developments, but we expect the US dollar to rebound tactically. More than observable fundamentals, policy headlines have been driving cross-asset movements. Traditional leading indicators have had limited market…

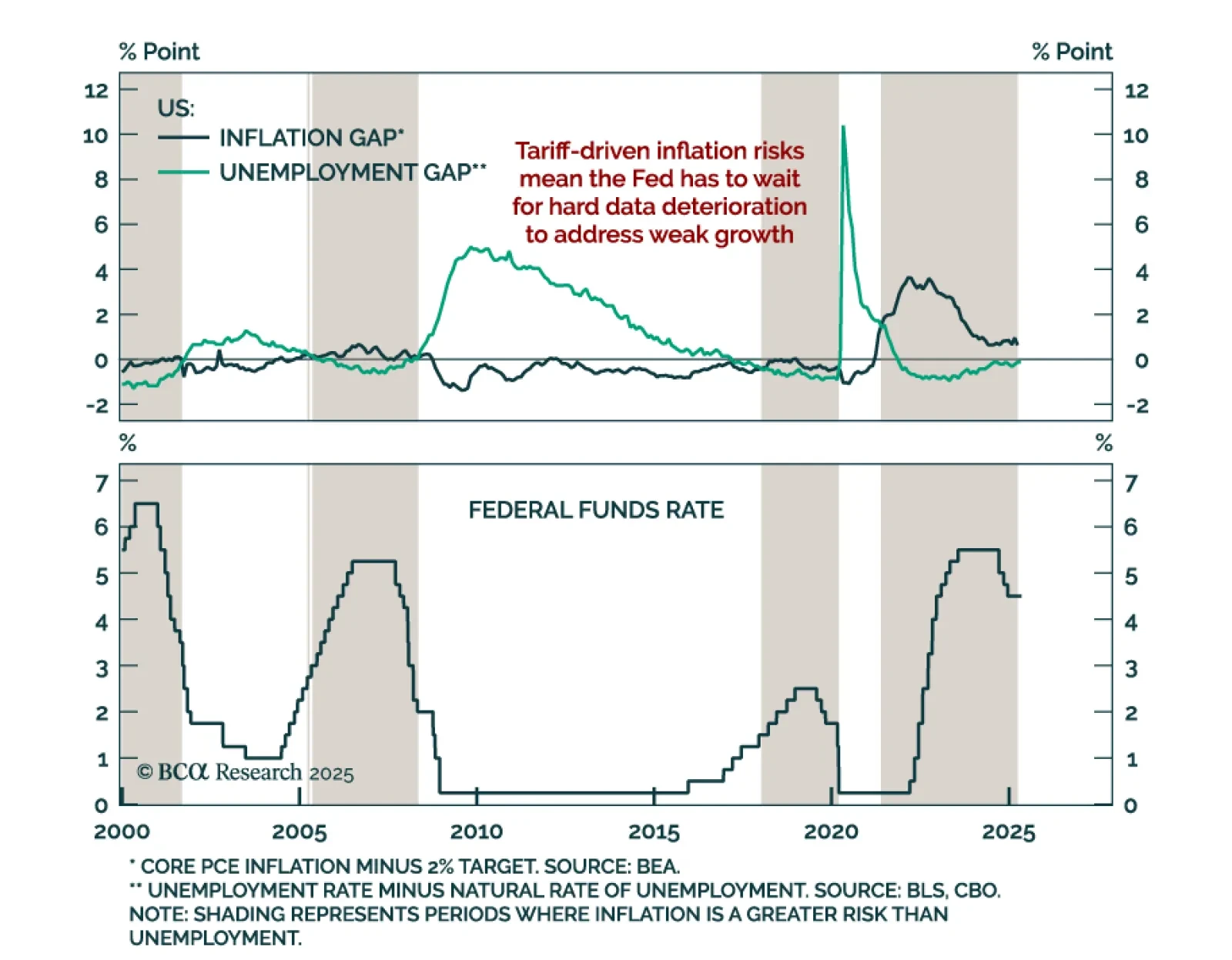

The Fed’s tight policy stance and focus on hard data reinforce our US Bond strategists’ call for above-benchmark duration and Treasury curve steepeners. As expected, the Fed held rates between 4.25% to 4.5% and flagged heightened uncertainty and two-sided…

The Fed held rates steady this afternoon, and the timing of its next move will be dictated by whether the tariff shock to inflation is transitory or more long lasting.

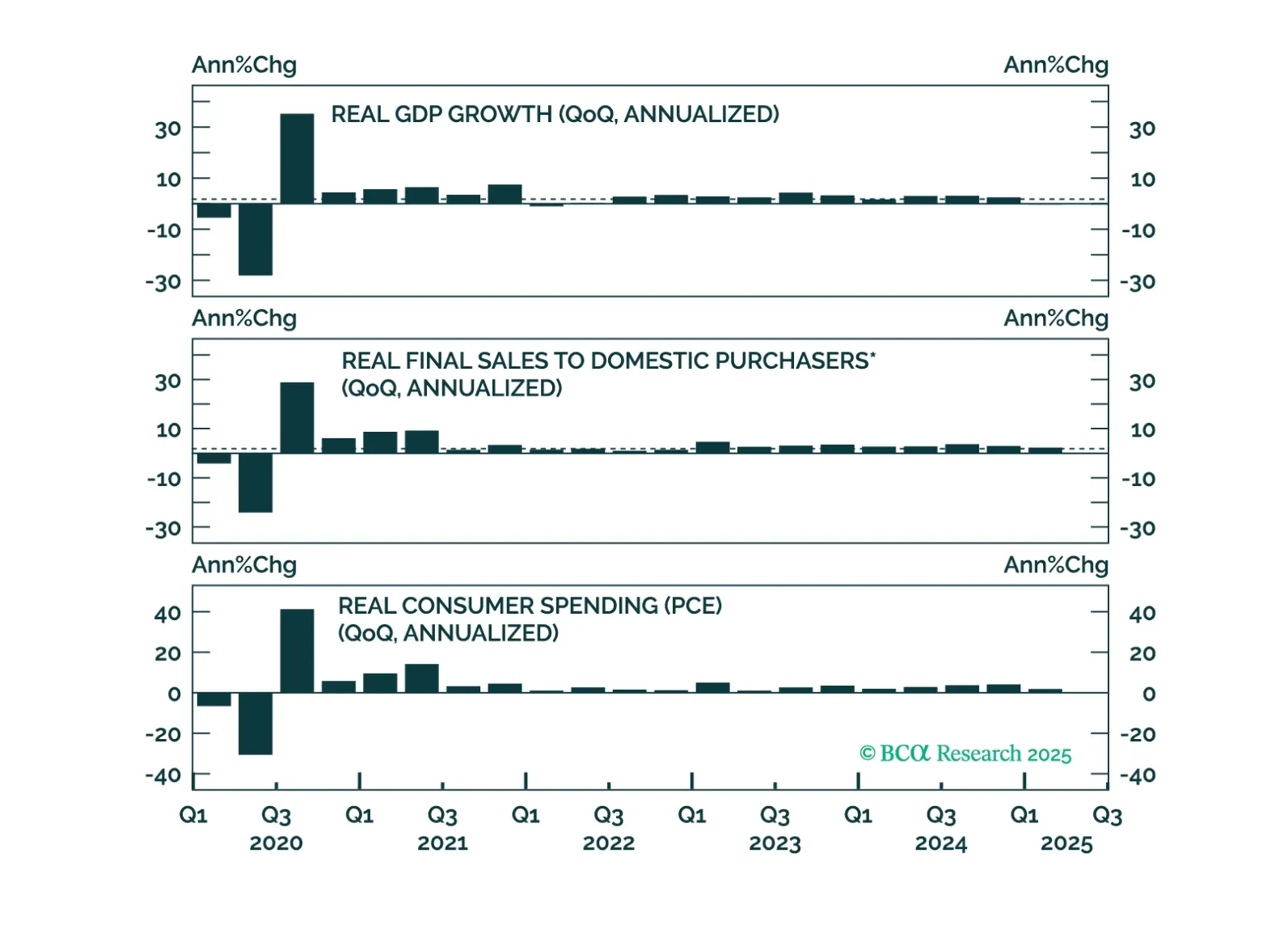

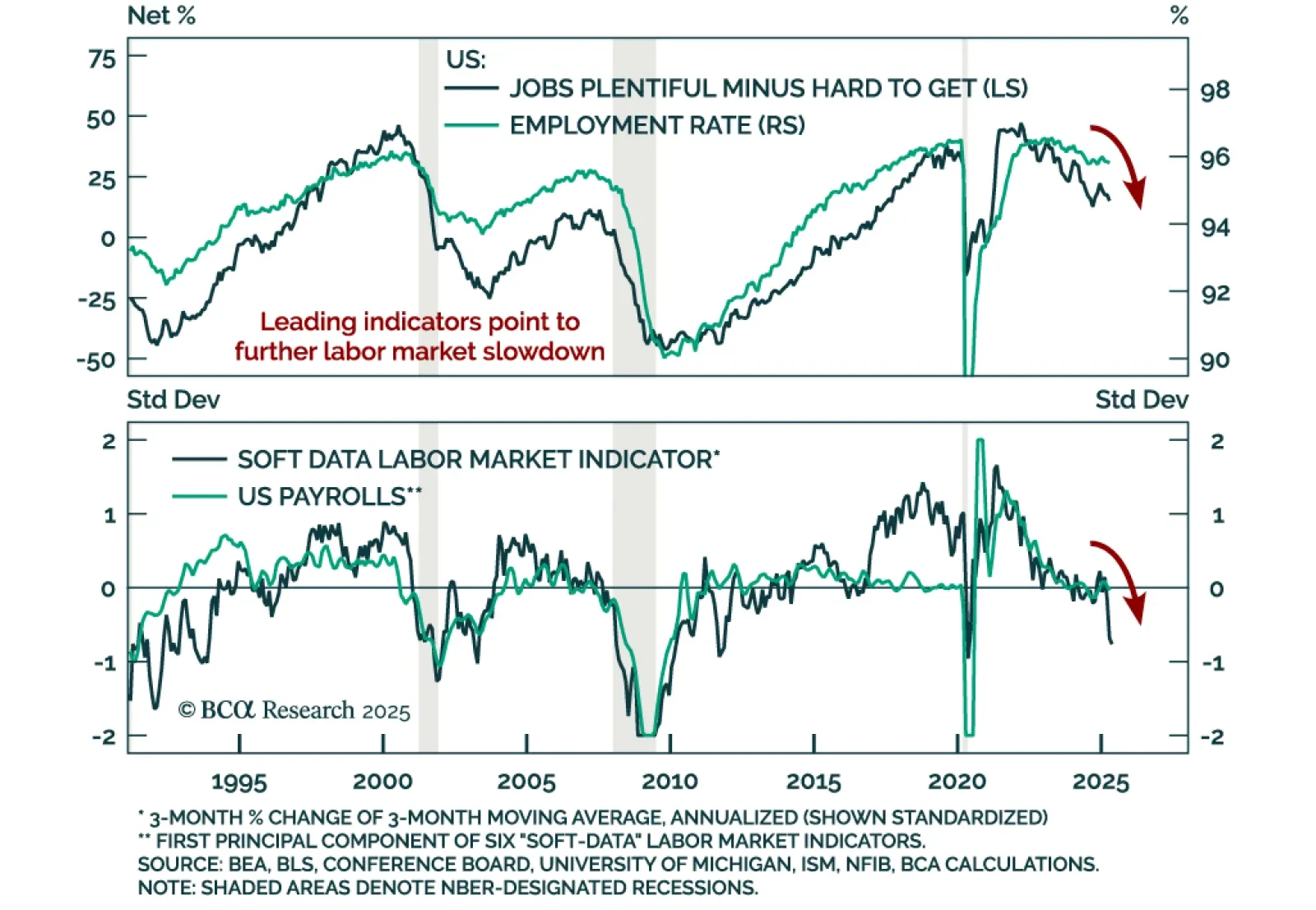

Markets no longer trade on soft-data fears; they now wait for hard-data proof, keeping us defensive on risk assets. Friday’s payroll beat highlighted the soft-hard split: Surveys flag weakness, but actual jobs hold up. In past cycles, markets priced…

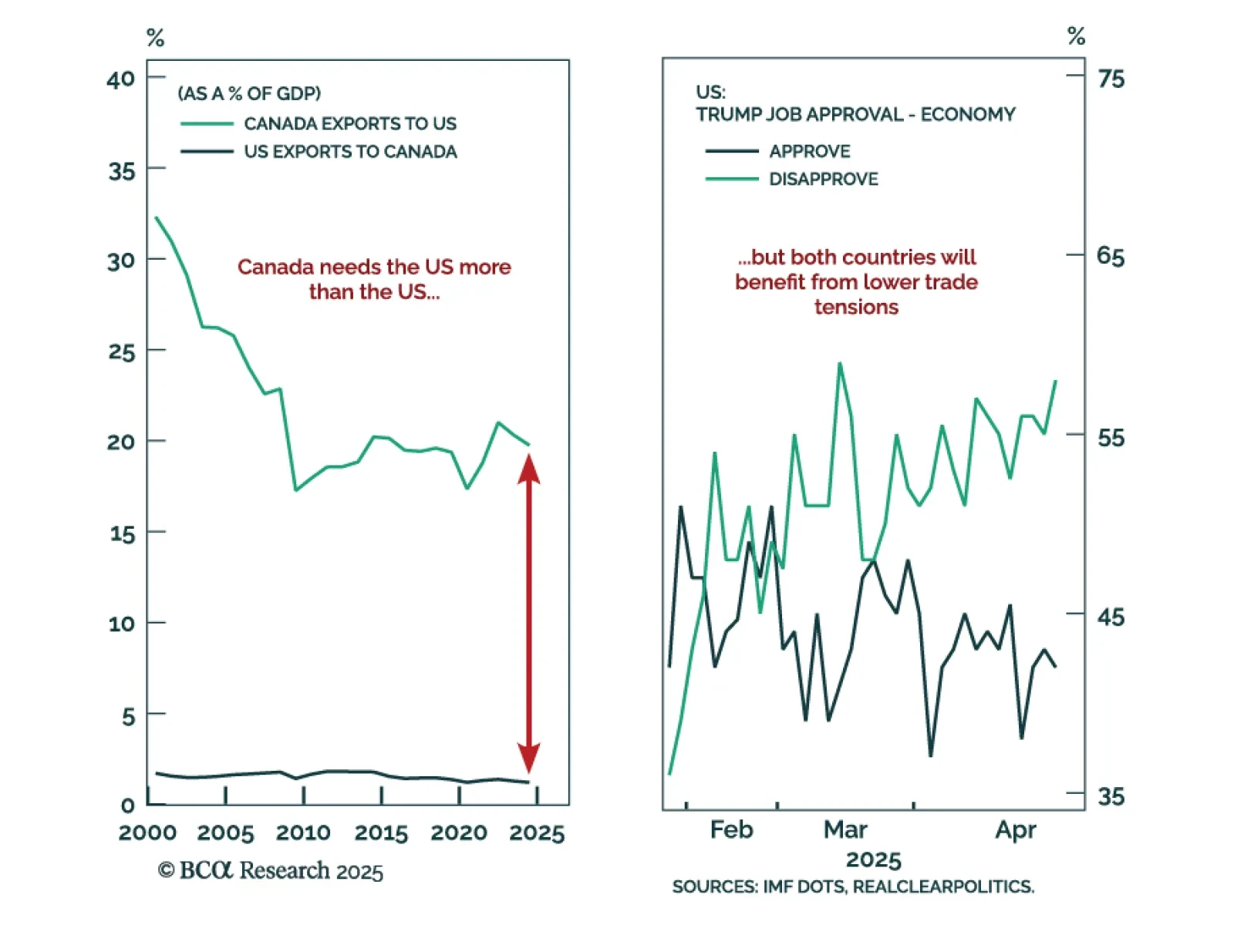

The Carney-Trump summit signals an early shift toward trade de-escalation, creating a tactical tailwind for risk assets. President Trump referred to the Canada-US relationship as a “wonderful marriage.” Moreover, both leaders acknowledged that the USMCA is “a…

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

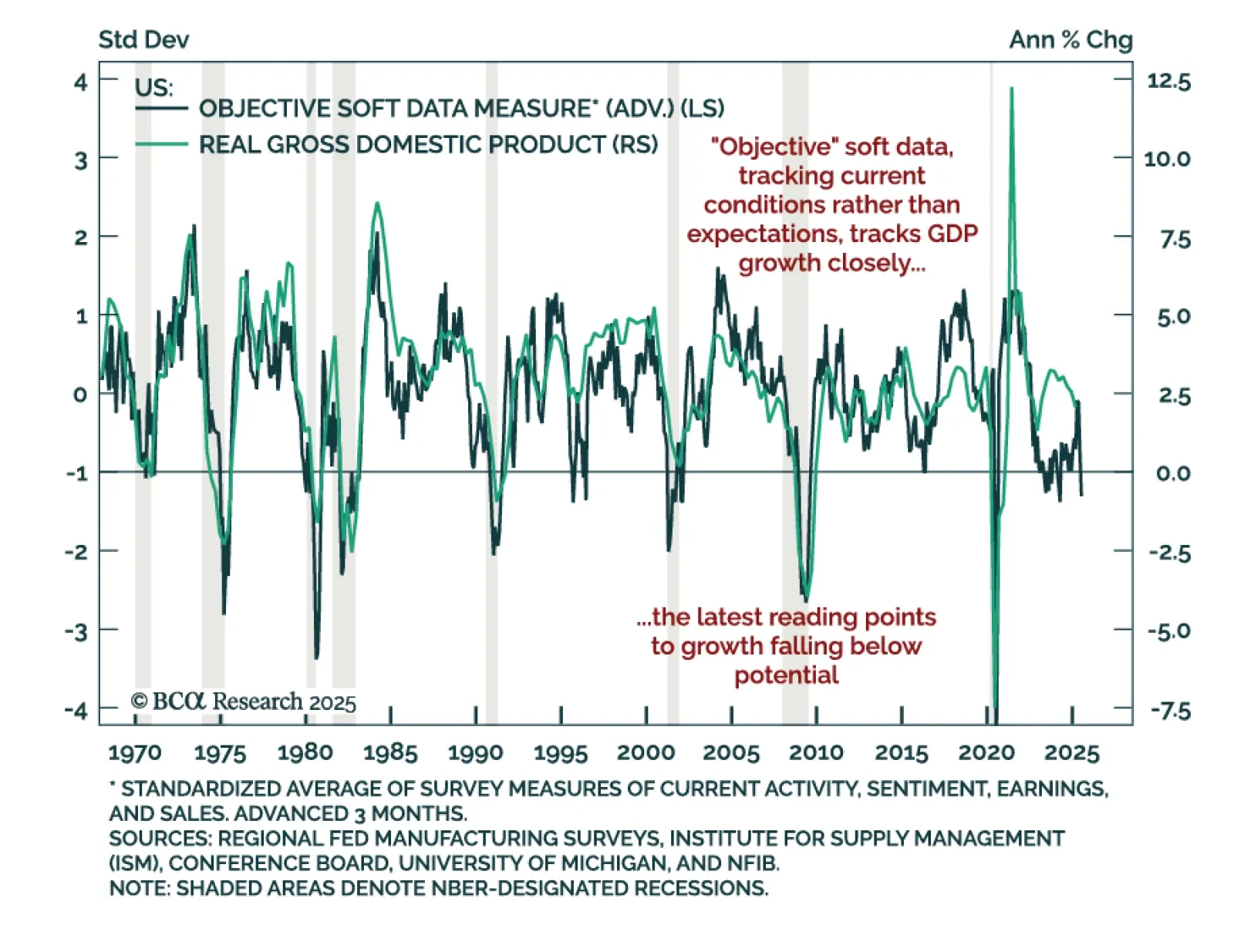

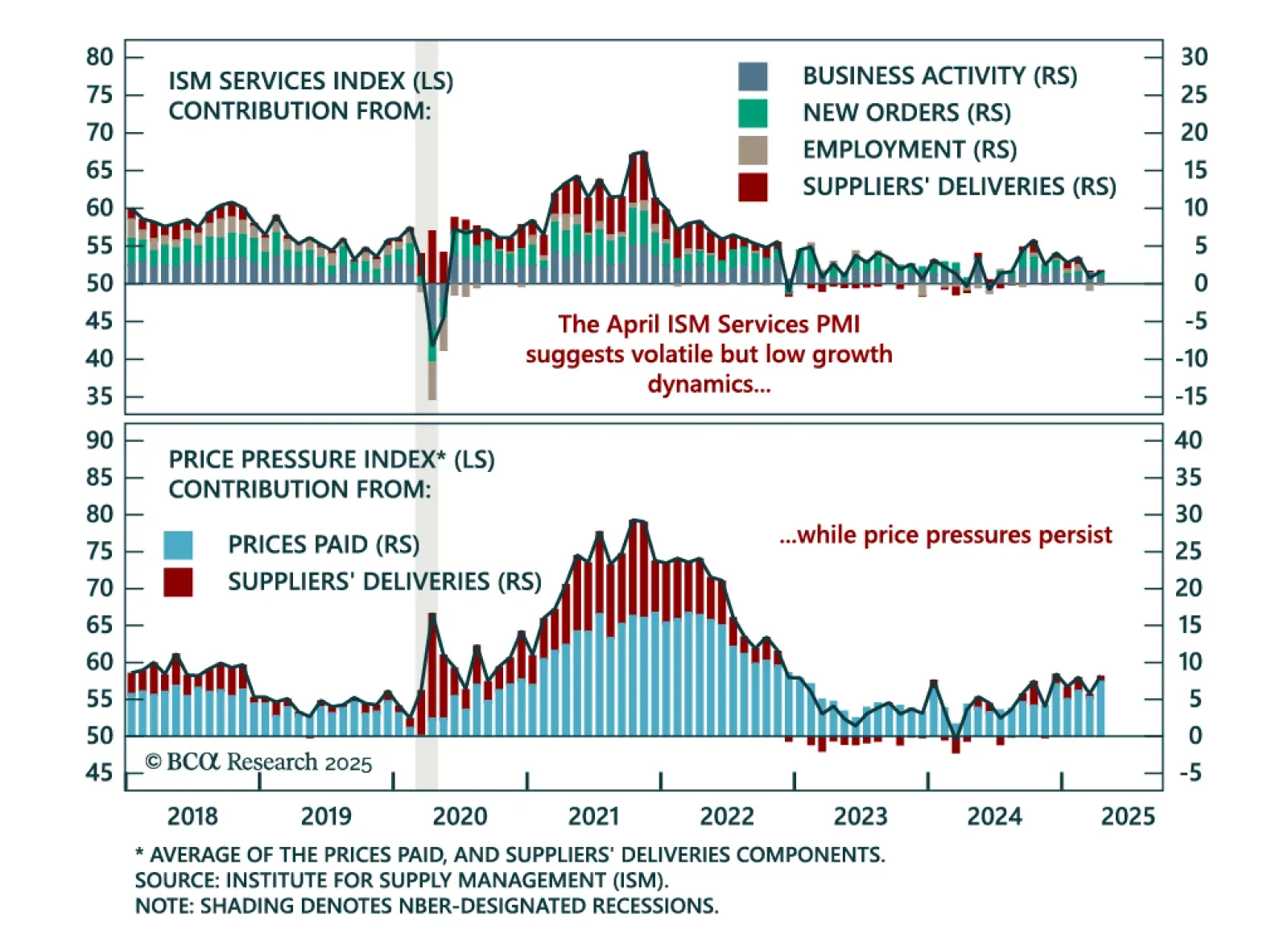

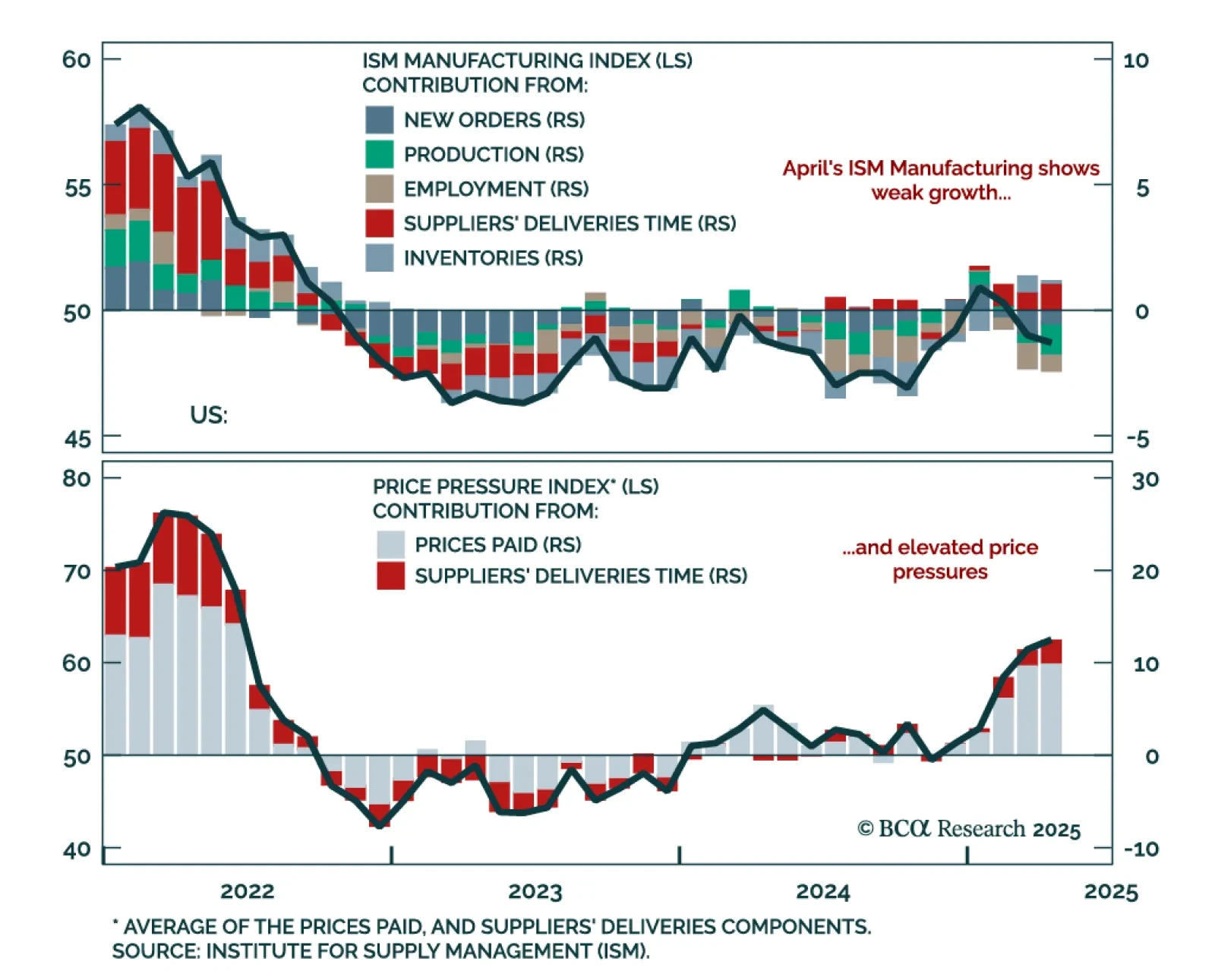

April’s ISM Services upside surprise does not shift our defensive stance, as its components show mixed momentum and rising price pressures. The headline index beat estimates, rising to 51.6 from 50.8. Business activity and new orders picked up, yet the…

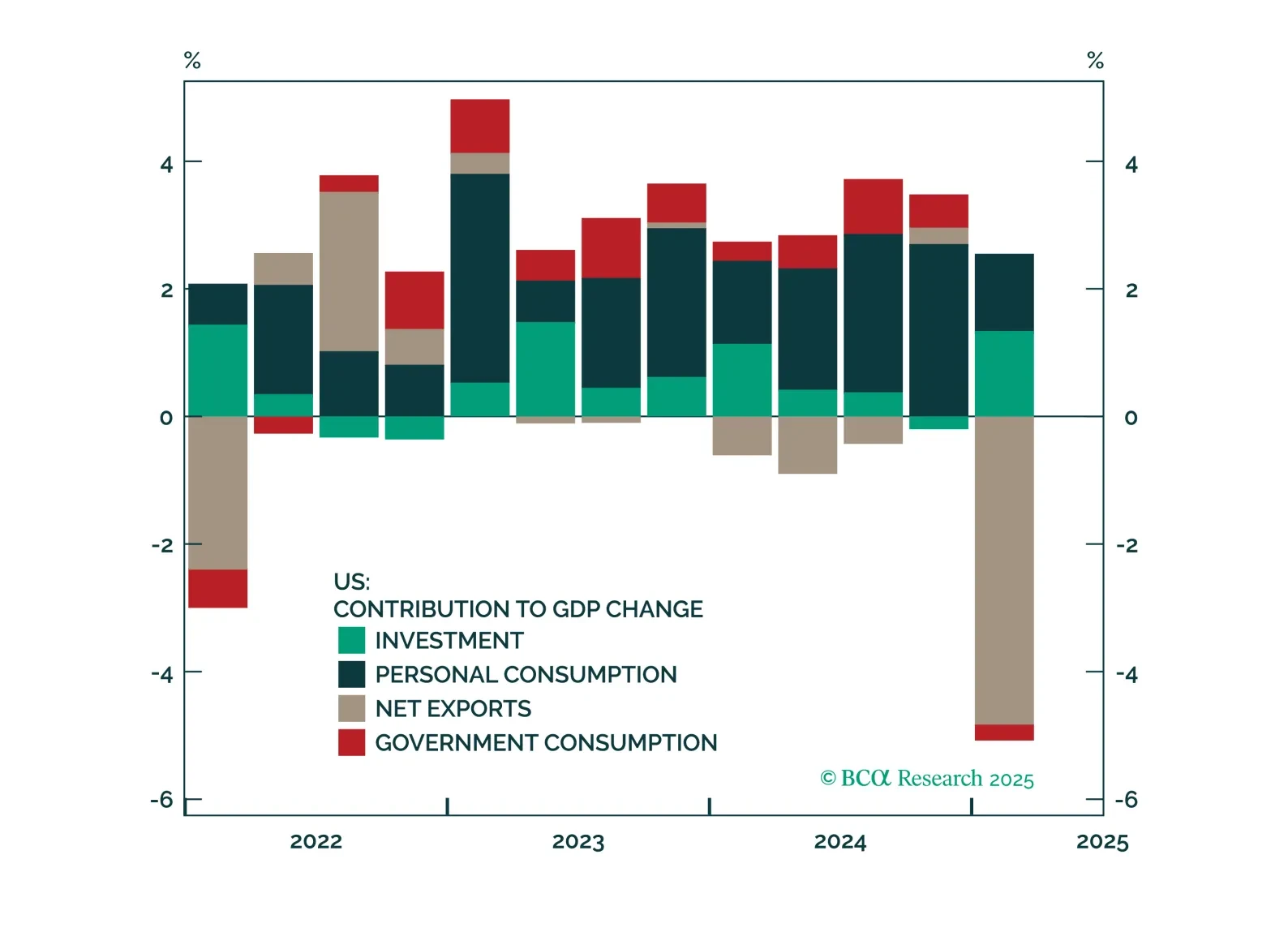

April’s stronger-than-expected US jobs report eased recession concerns, but underlying trends support our defensive positioning. Nonfarm payrolls rose 177k, but downward revisions to prior months totaled 58k, leaving the three-month average at 155k. The…

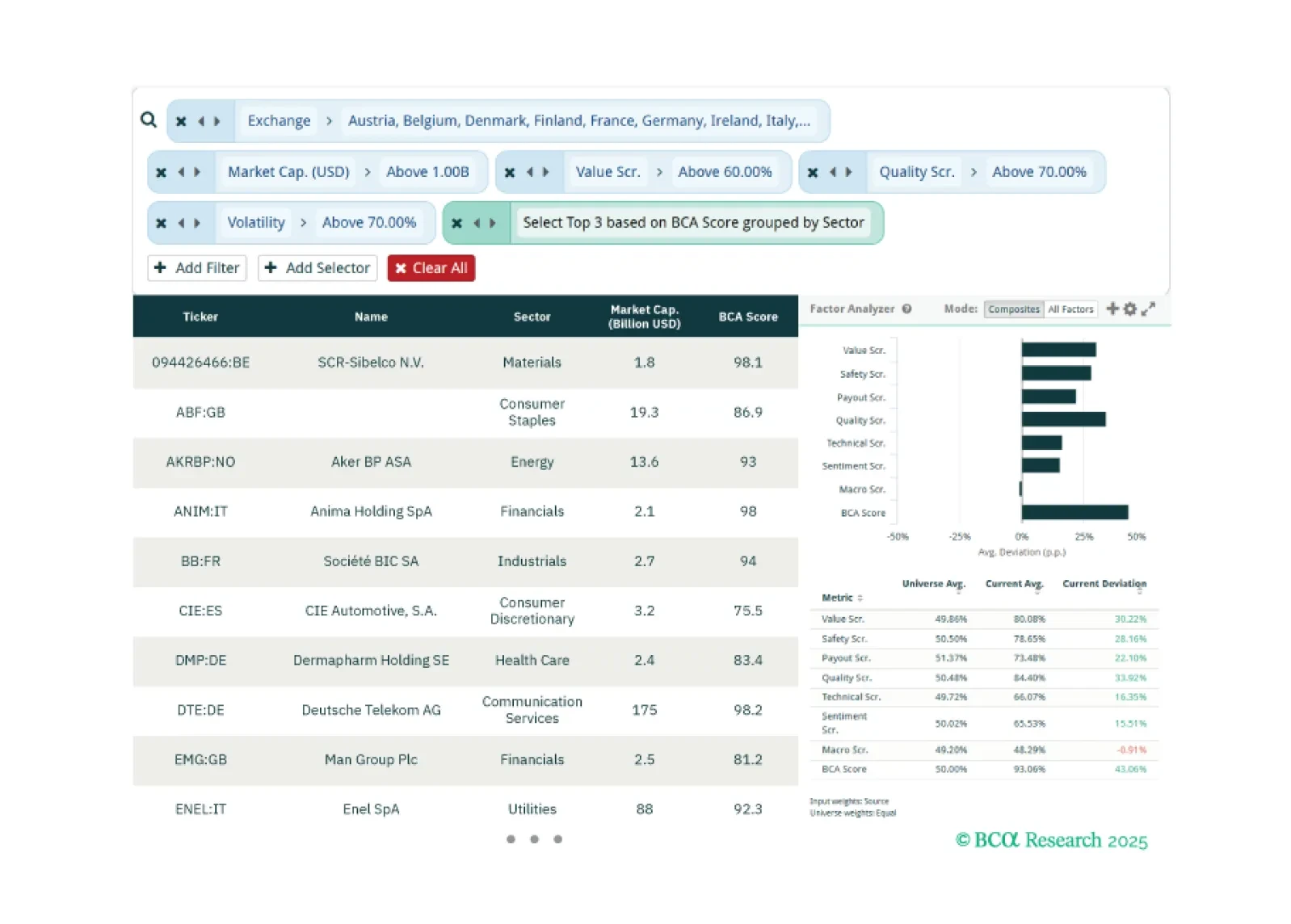

This week, our three screeners cover: Favoring European equities over US equities, cybersecurity stocks, and large caps with large moves in their BCA Score.

The April ISM Manufacturing adds to recession risks: Collapsing export orders and weak domestic momentum reinforce our defensive positioning. The index slipped to 48.7 from 49.0, with new orders still contracting and new export orders plunging to 43.1, a…