United States

This year’s corporate bond sell off has hit high-yield more than investment grade, and high-yield spreads have turned relatively more attractive as a result.

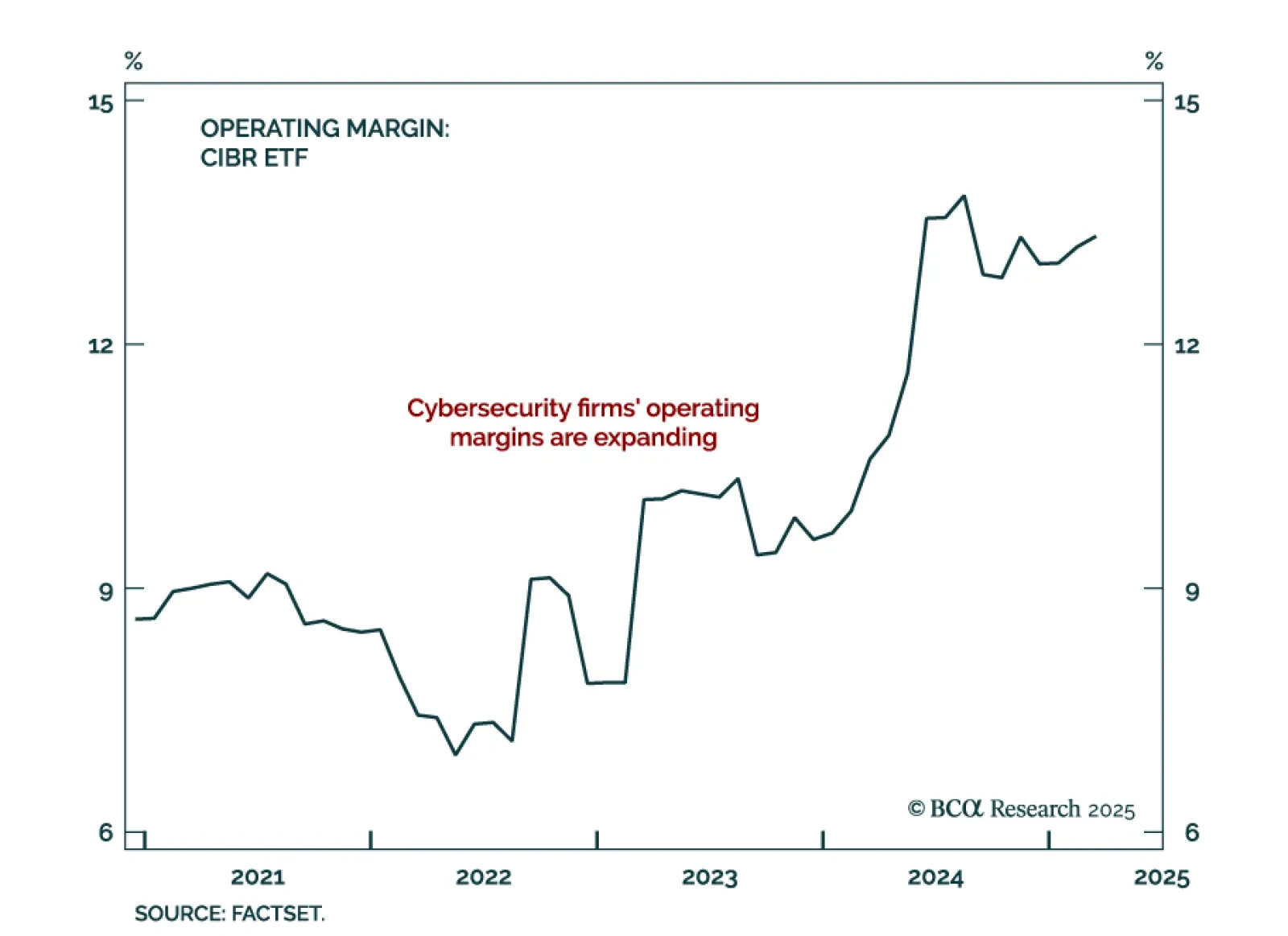

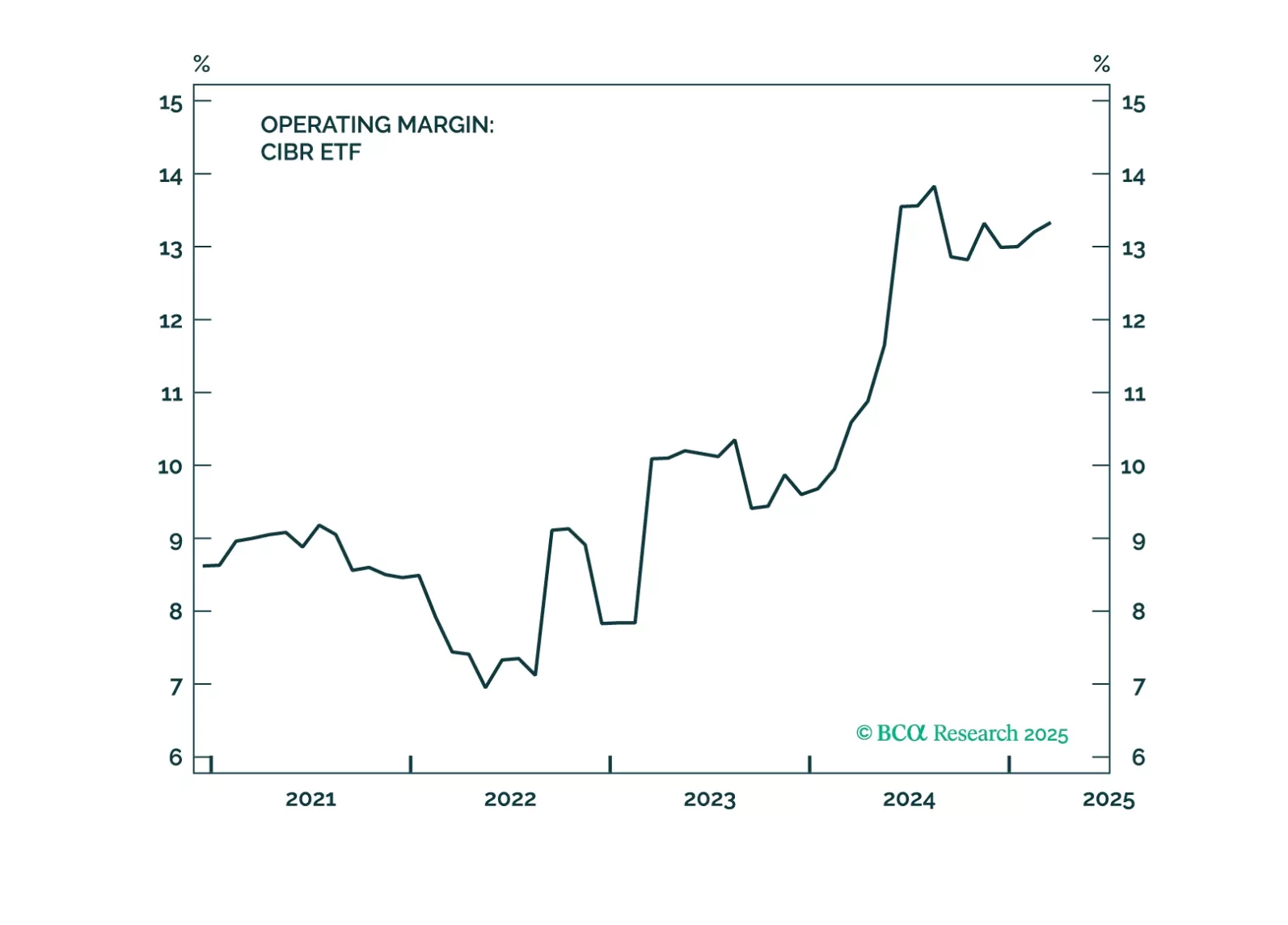

Cybersecurity is a strategic investment theme, which looks particularly interesting in light of the trade war and heightened geopolitical tensions. It is less exposed to tariffs than other industries and, if anything, benefits from geopolitical tensions as customers seek protection from international cyberattacks and cybercrime. The industry’s fundamentals are improving, while valuations are moderating. A recent pullback presents an attractive entry point into the theme.

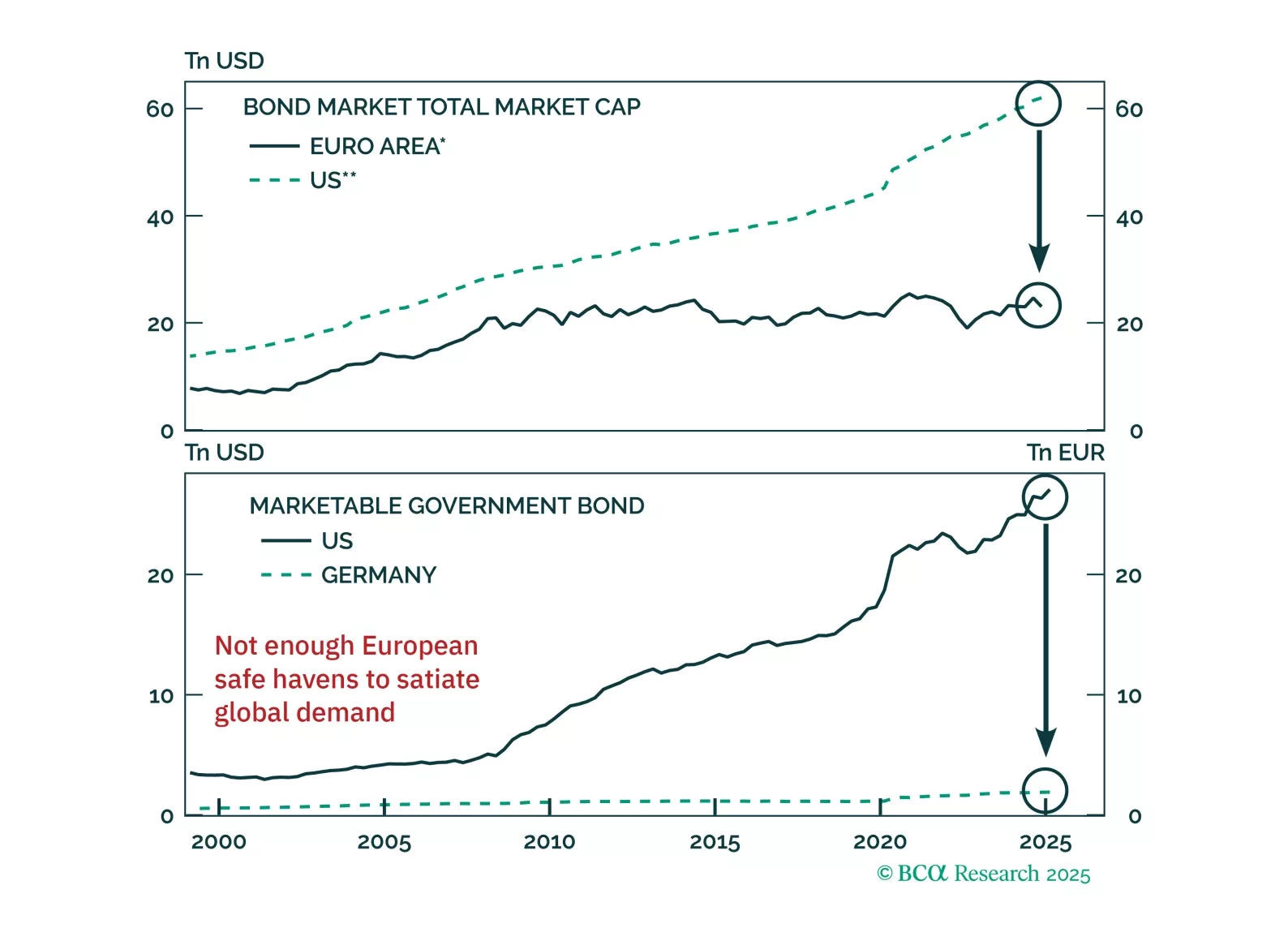

Are bunds the new Treasurys? The euro and German debt are gaining favor as safe havens, but markets may be overplaying the shift. Our latest report dissects what's durable, what's not, and how to trade the dislocation.