United States

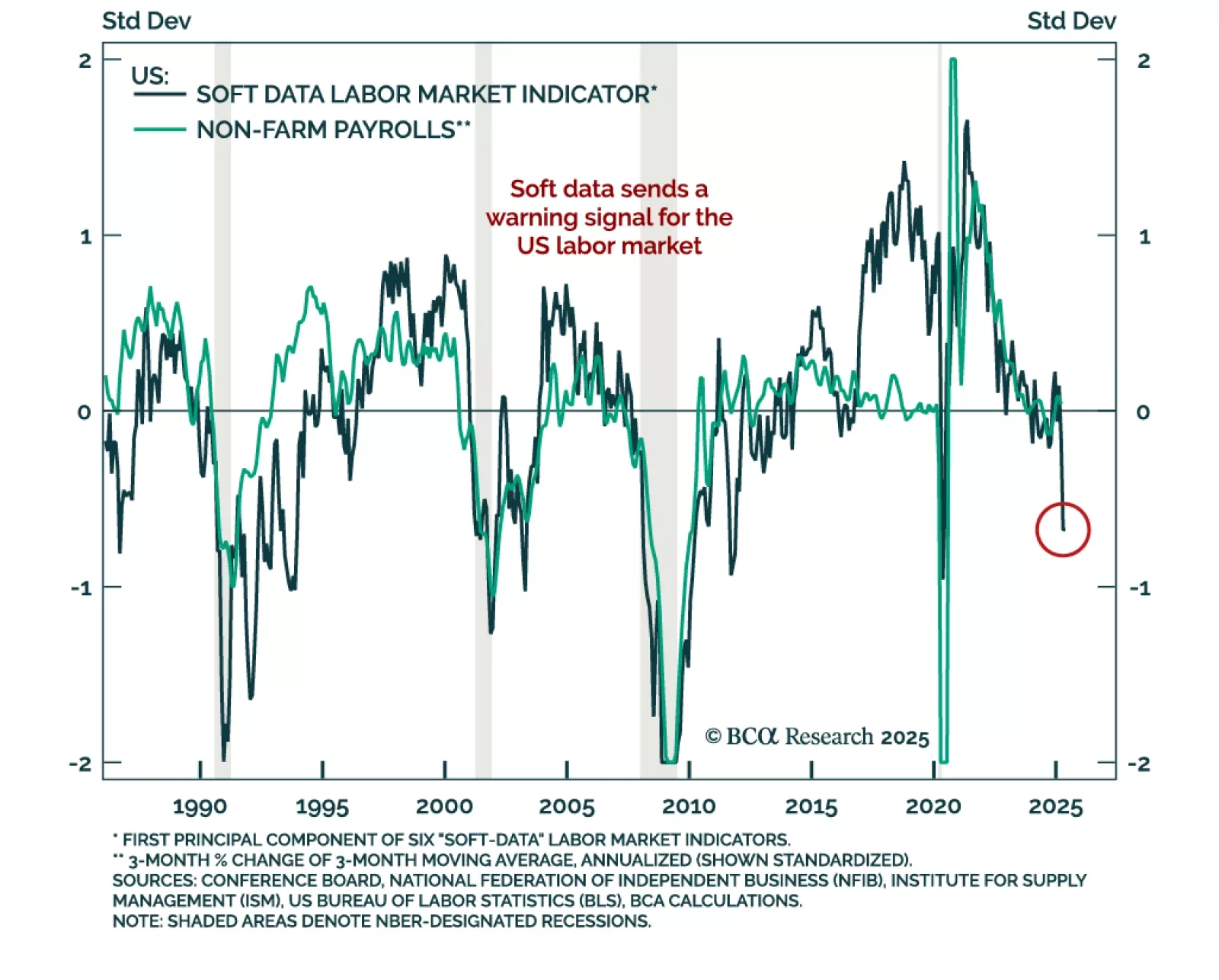

Soft data for the US labor market has turned sharply lower, reinforcing the case for a defensive asset allocation. Our Chart Of The Week comes from Miroslav Aradski from our Global Investment Strategy team. While it may take months for the tariff shock and…

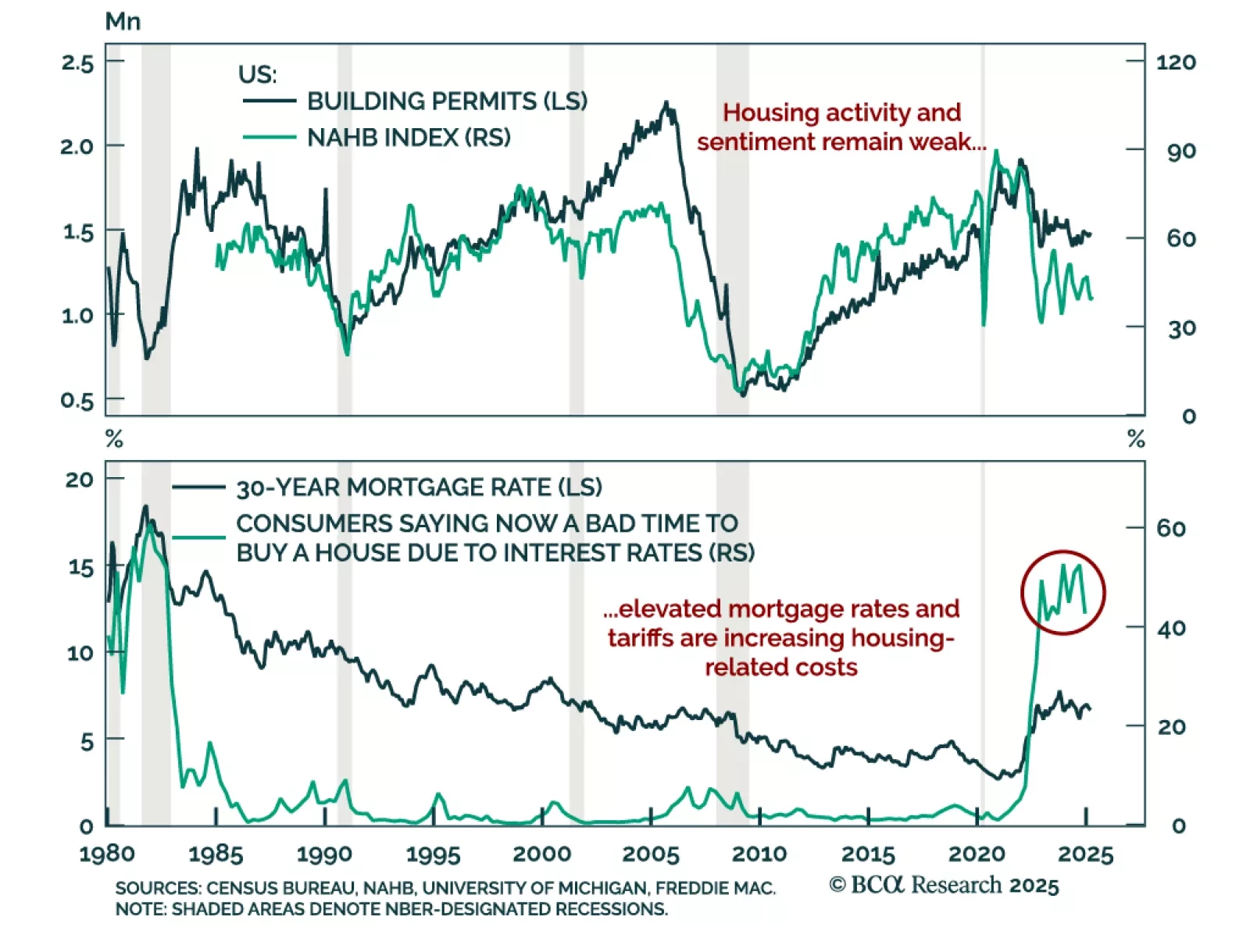

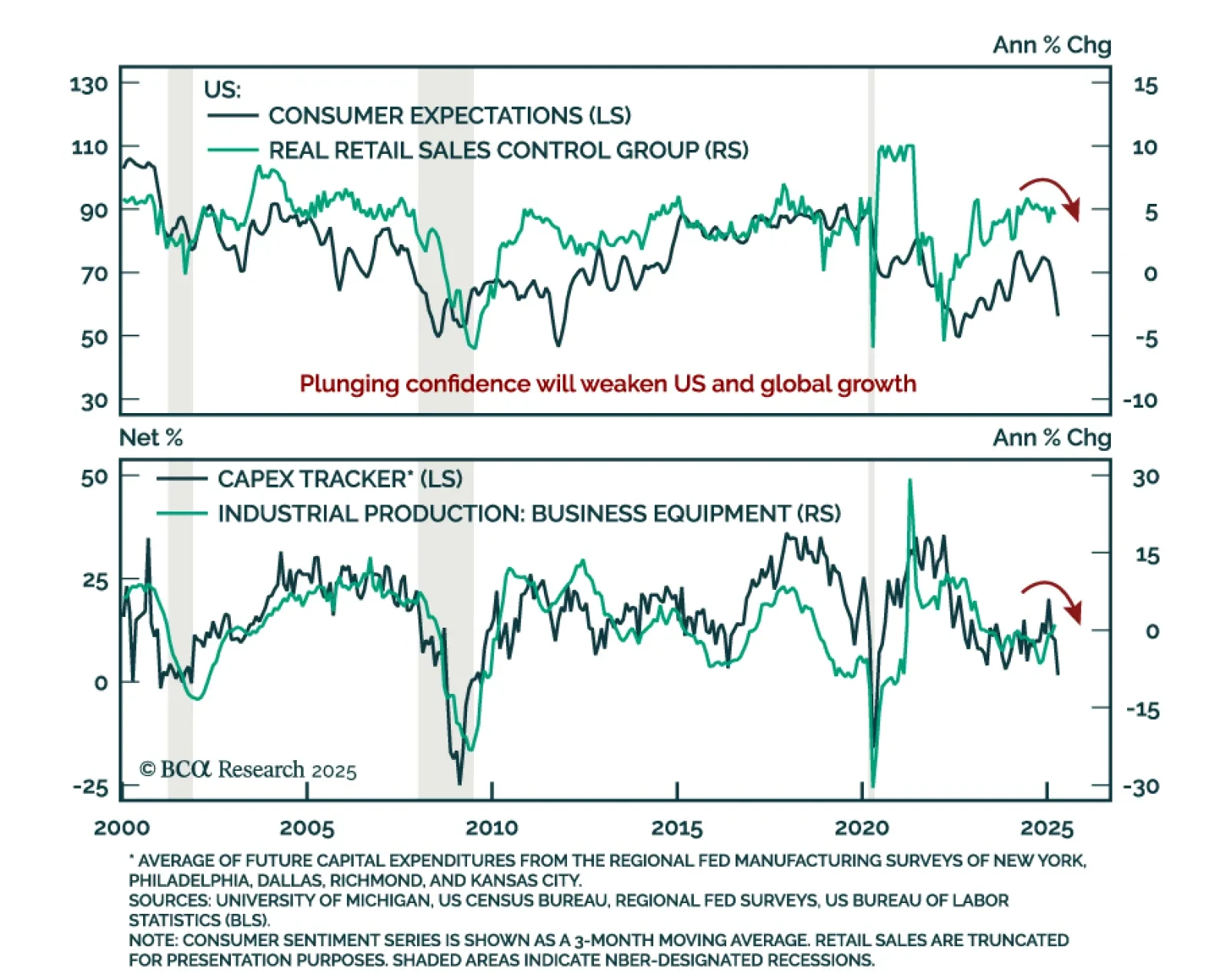

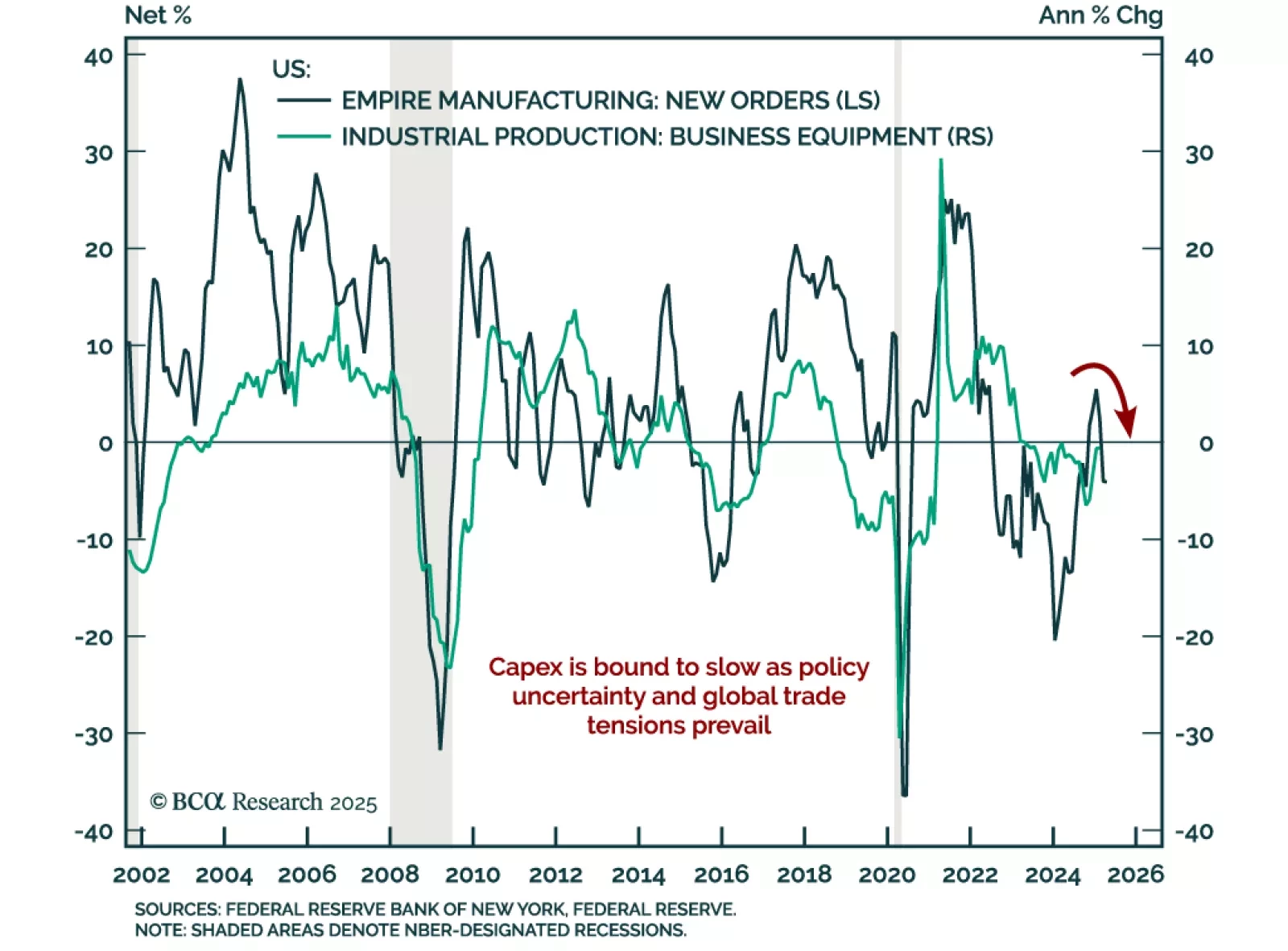

Soft data continues to deteriorate and hard data will soon follow, reinforcing our defensive asset allocation. Consumer and business confidence have plunged as policy uncertainty and inflation expectations rise, with spending, hiring and capex plans…

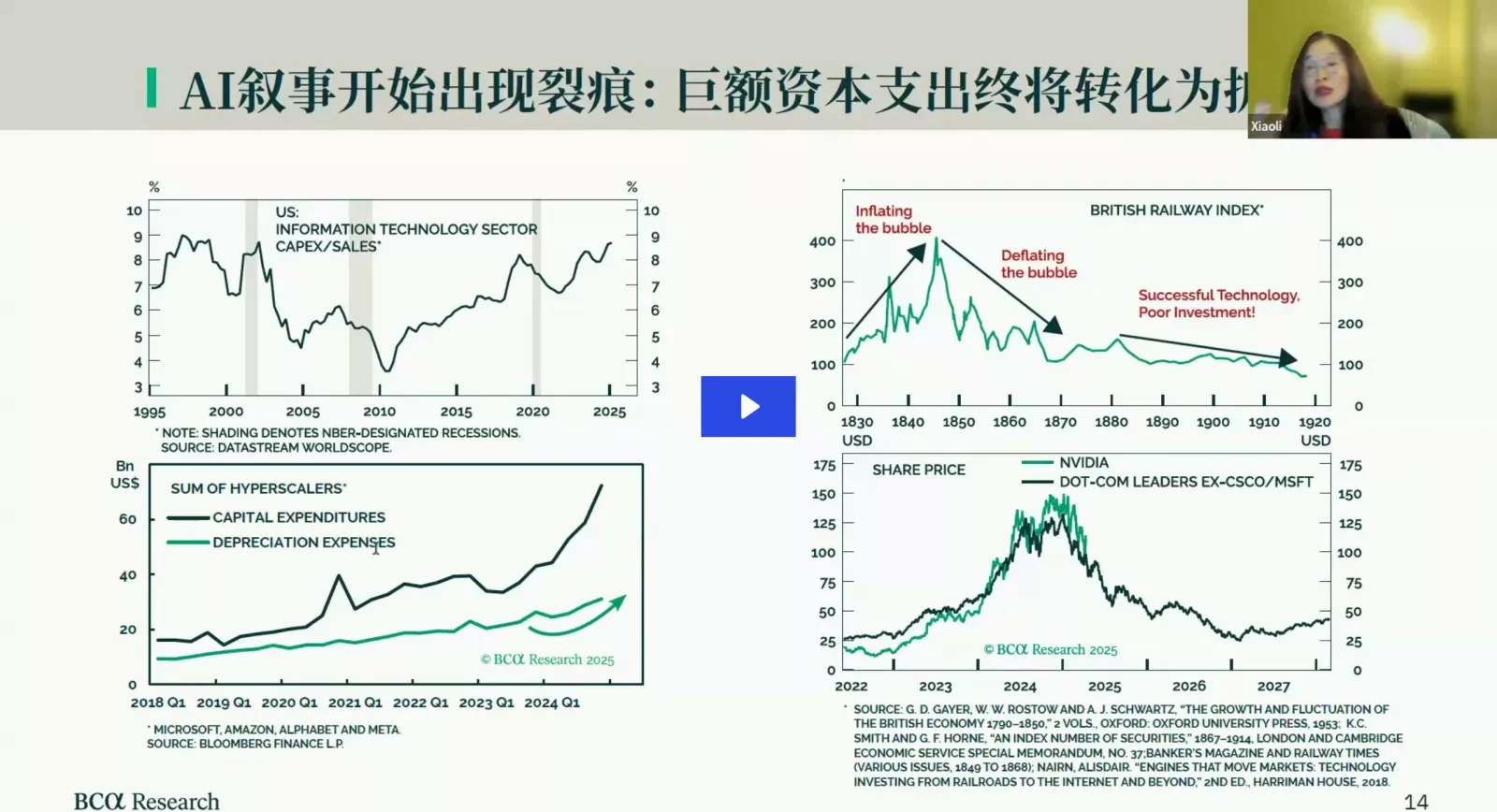

请于2025年4月17日星期四上午9:00(北京/香港/台北 时间)加入BCA全球资产配置高级策略师唐小莉的网络直播: 《聚焦宏观趋势,把握市场先机》。

The NY Fed Empire Manufacturing survey adds to recent stagflationary worries, reinforcing our underweight in risk assets and overweight in government bonds. The general business conditions index rose slightly to -8.1 but remains in contraction, while the…

I’d like to personally invite you to join me and my colleagues at BCA Research on Tuesday, April 15 (12 PM EDT/ 9 AM PST) for a webcast exclusive to long-term institutional investors.

We are pleased to share the replay of US Equity Market Intelligence Session, hosted by Chief US Equity Strategist Irene Tunkel.

Please join BCA Research's Chief US Equity Strategist, Irene Tunkel, for a US Equity Intelligence session on Wednesday, April 16 at 9:00 AM HKT, 11:00 AM AEST.

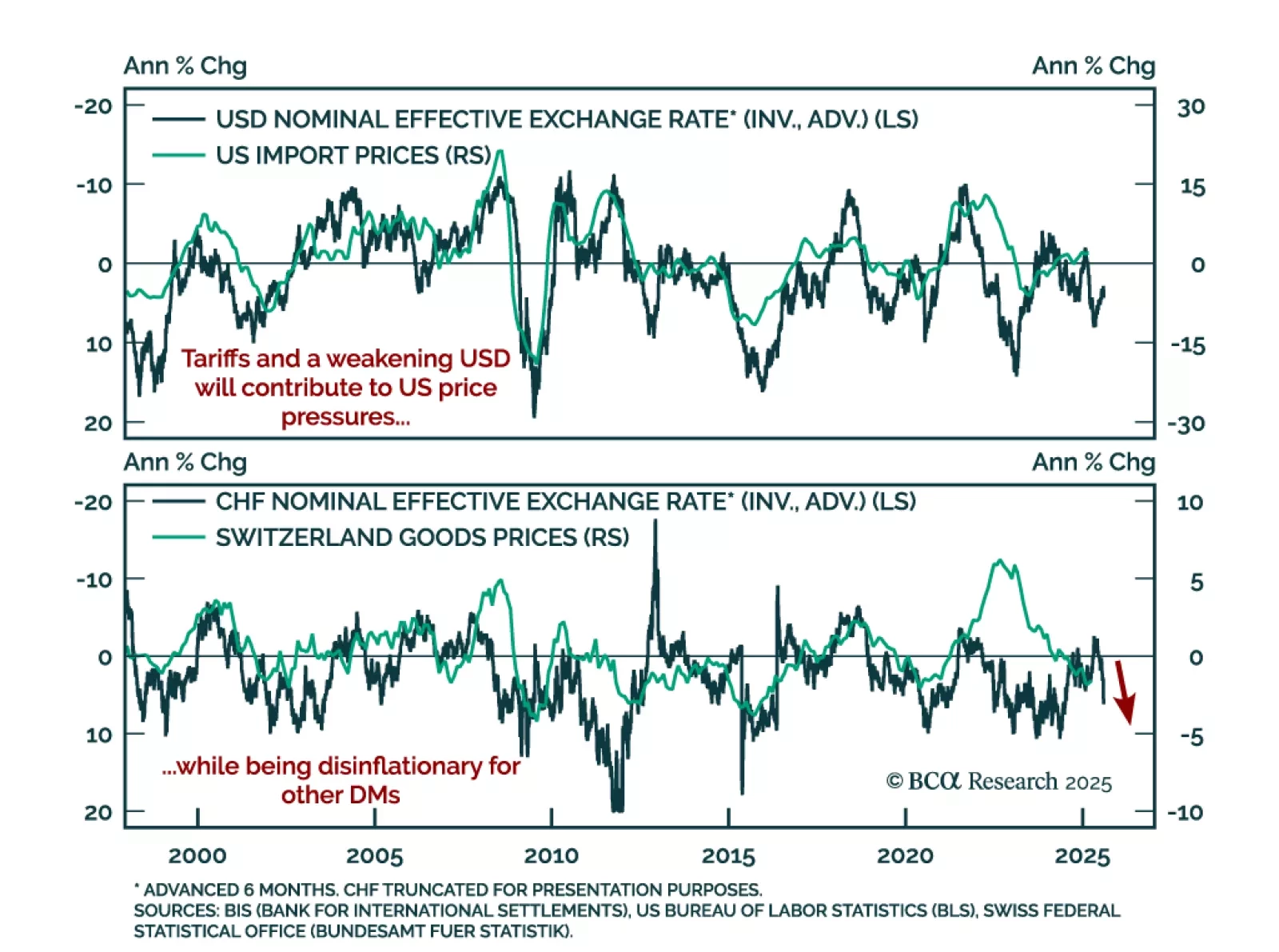

Tariff-driven inflation is diverging across economies, with the US facing mounting pressures while disinflation persists elsewhere. In theory, US tariffs should strengthen the dollar and weaken targeted currencies. In practice, the opposite has occurred: The…

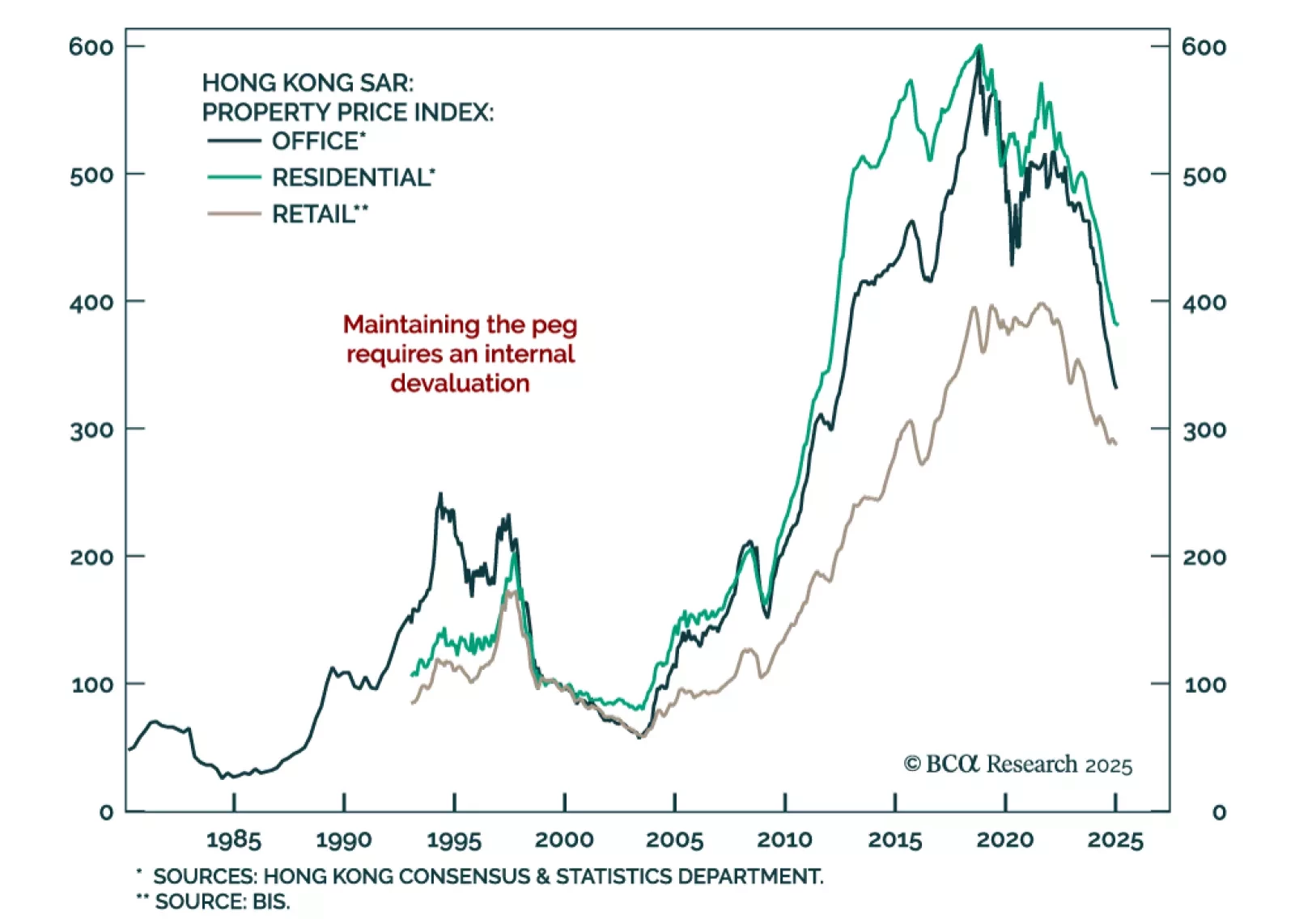

Our FX strategists expect the HKD peg to hold, but at the cost of prolonged economic weakness and debt deflation in Hong Kong. Interest rates remain too high for the local economy, yet monetary easing is off-limits due to the peg.The currency’s…