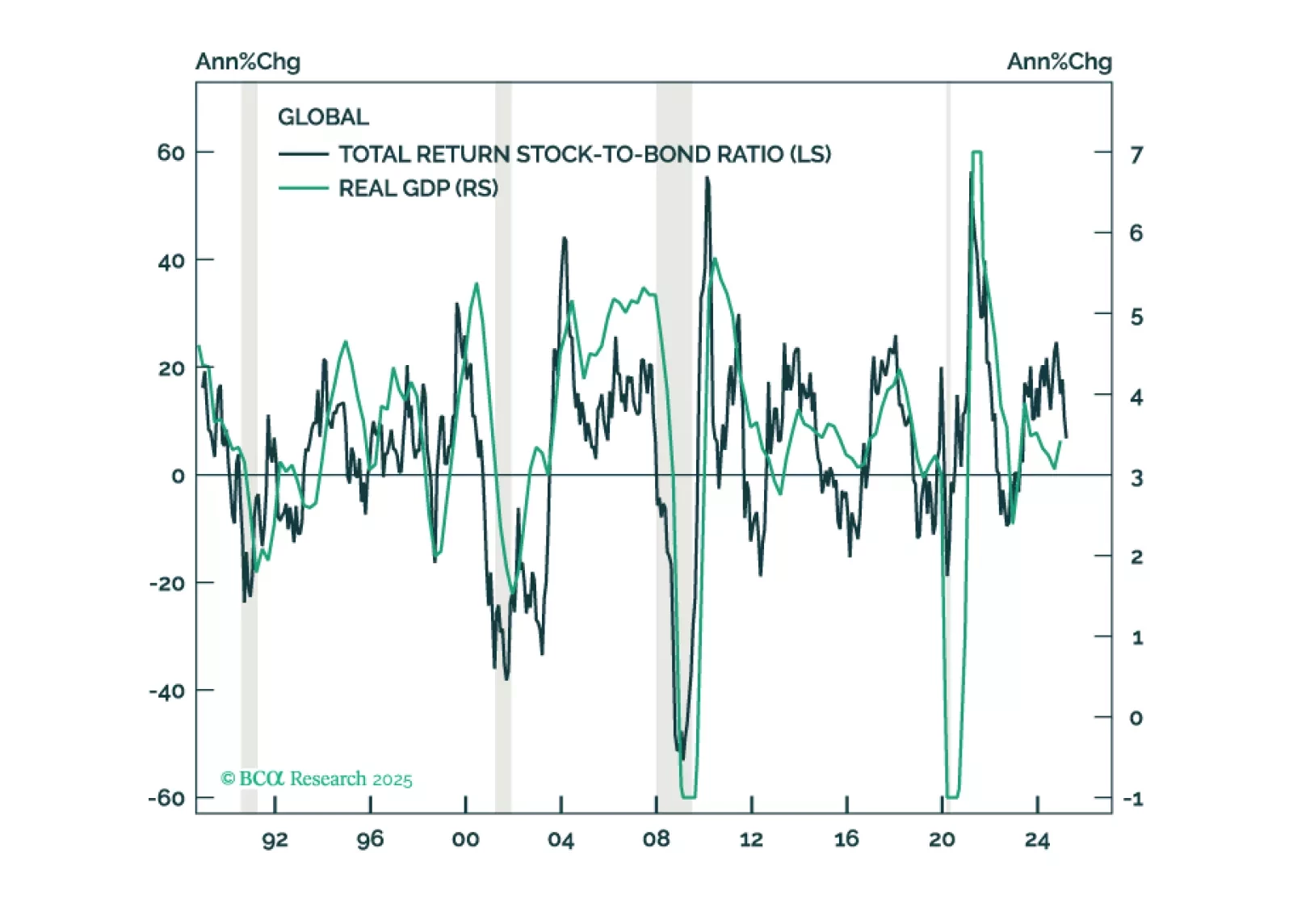

United States

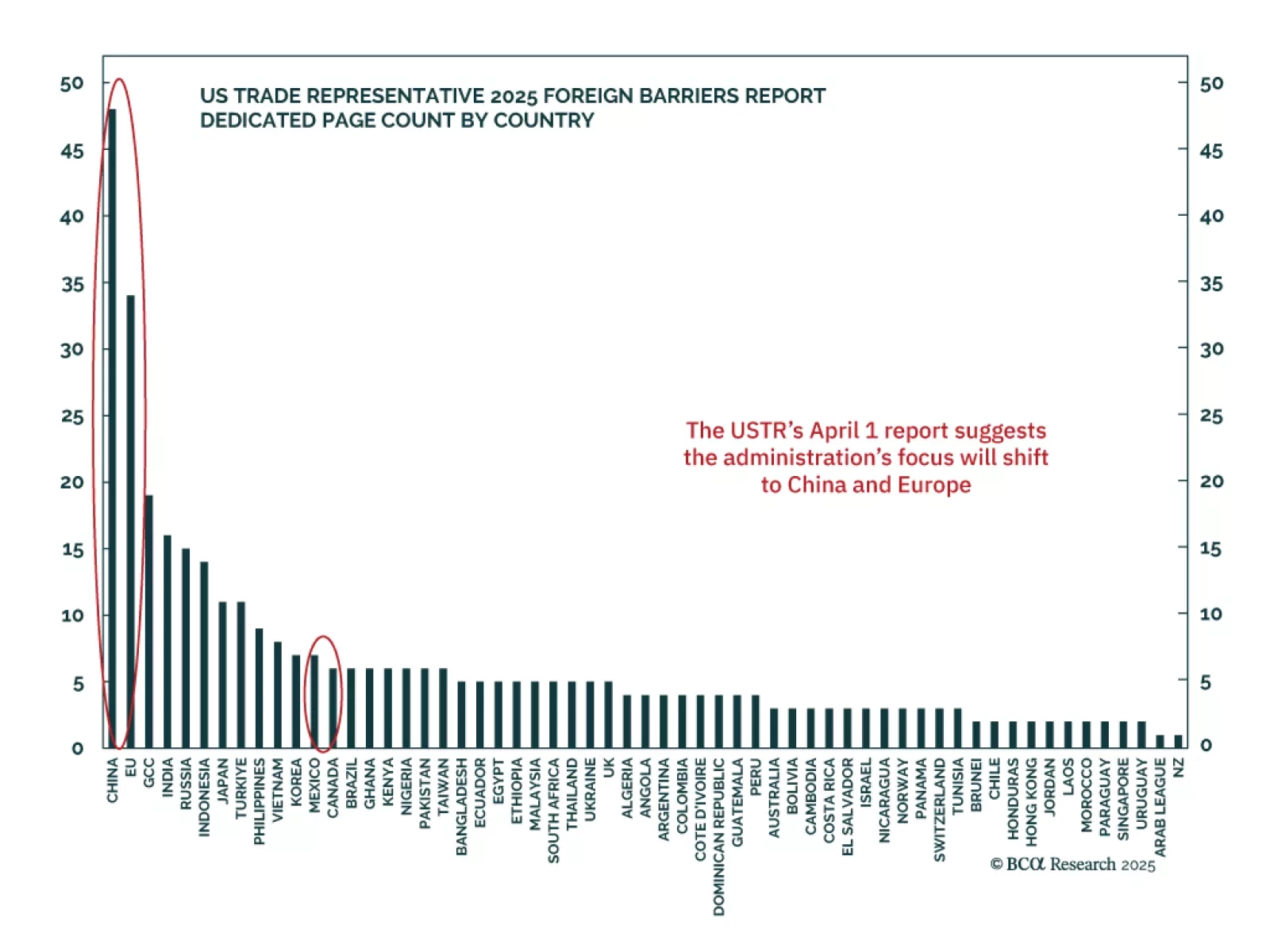

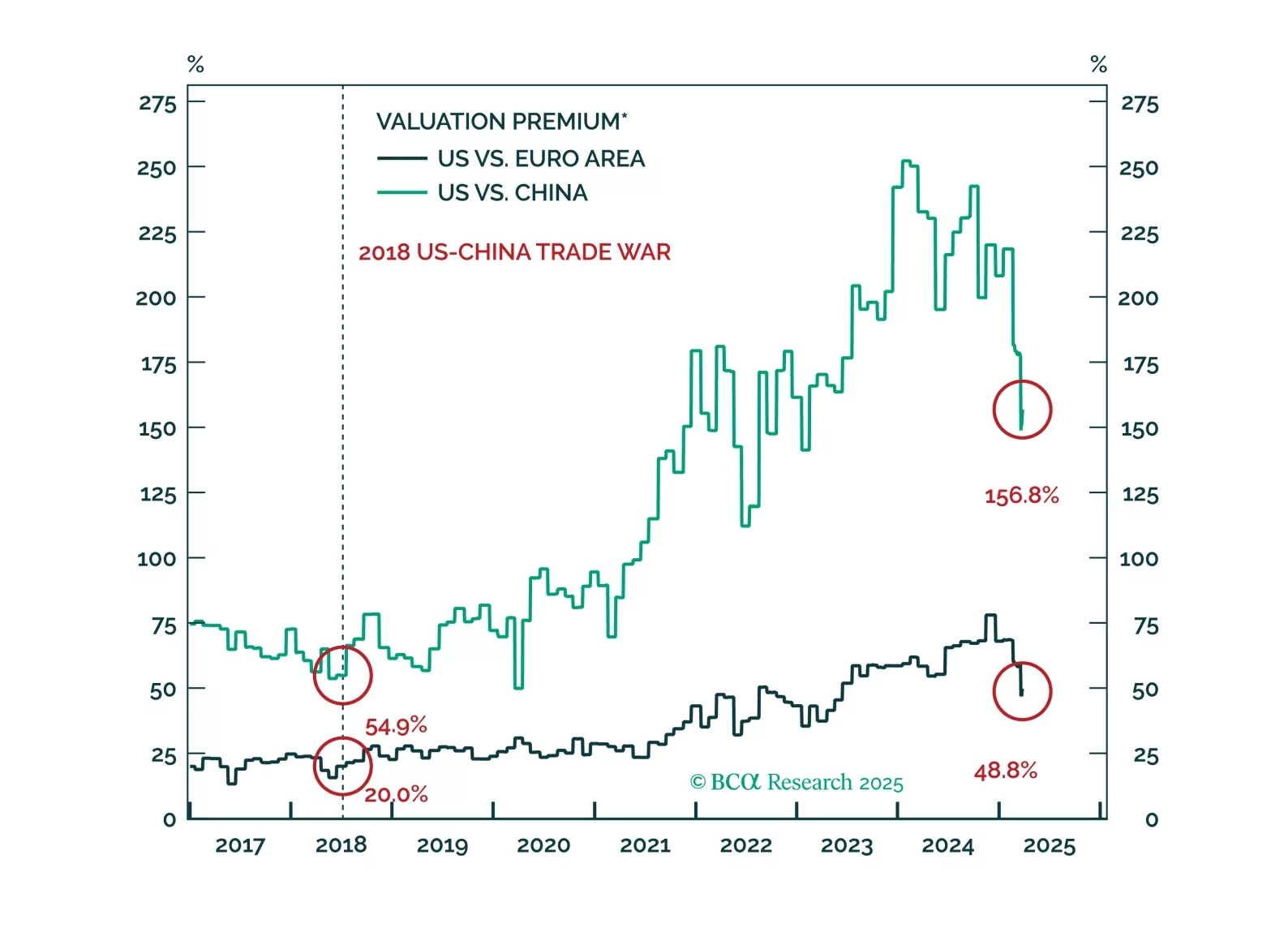

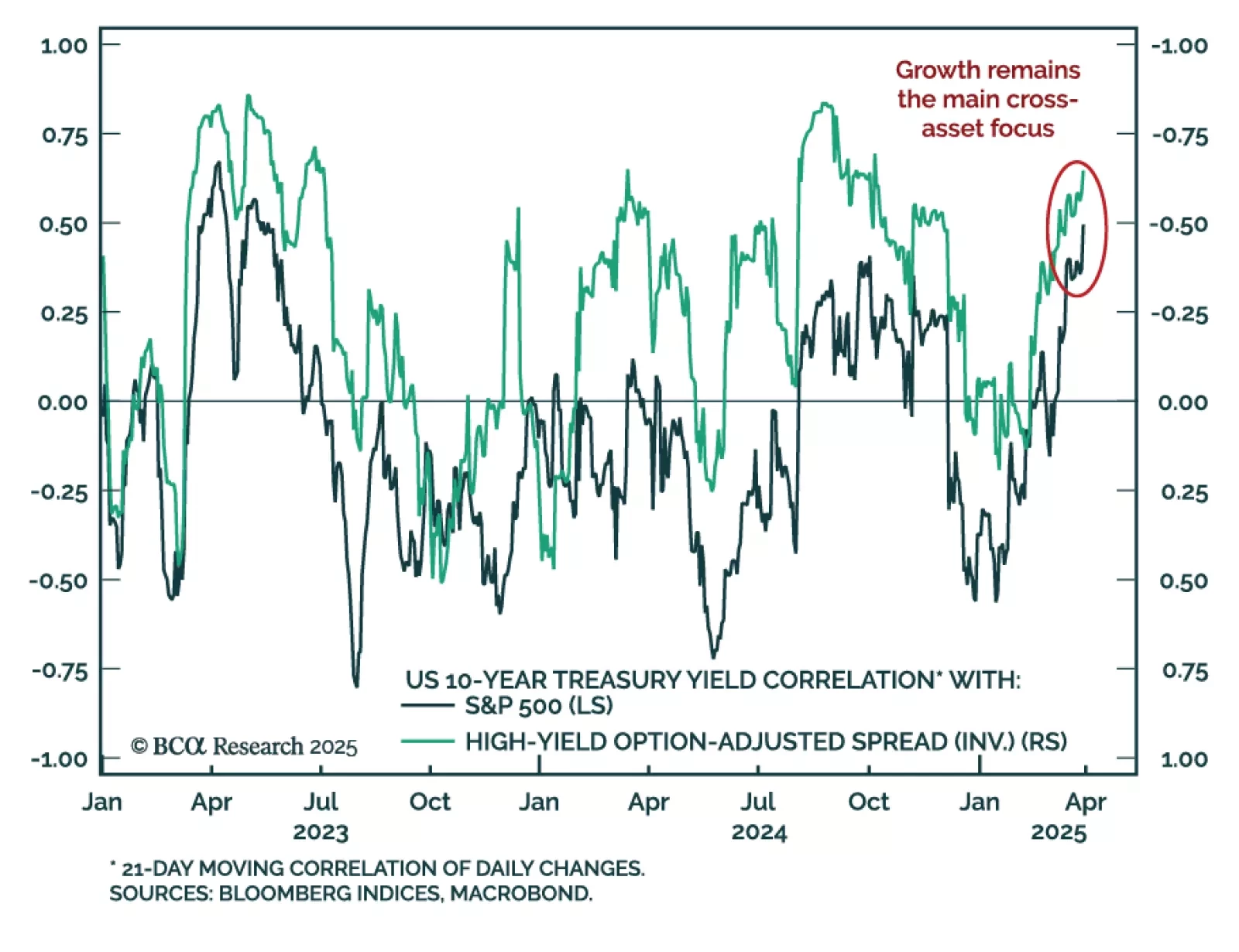

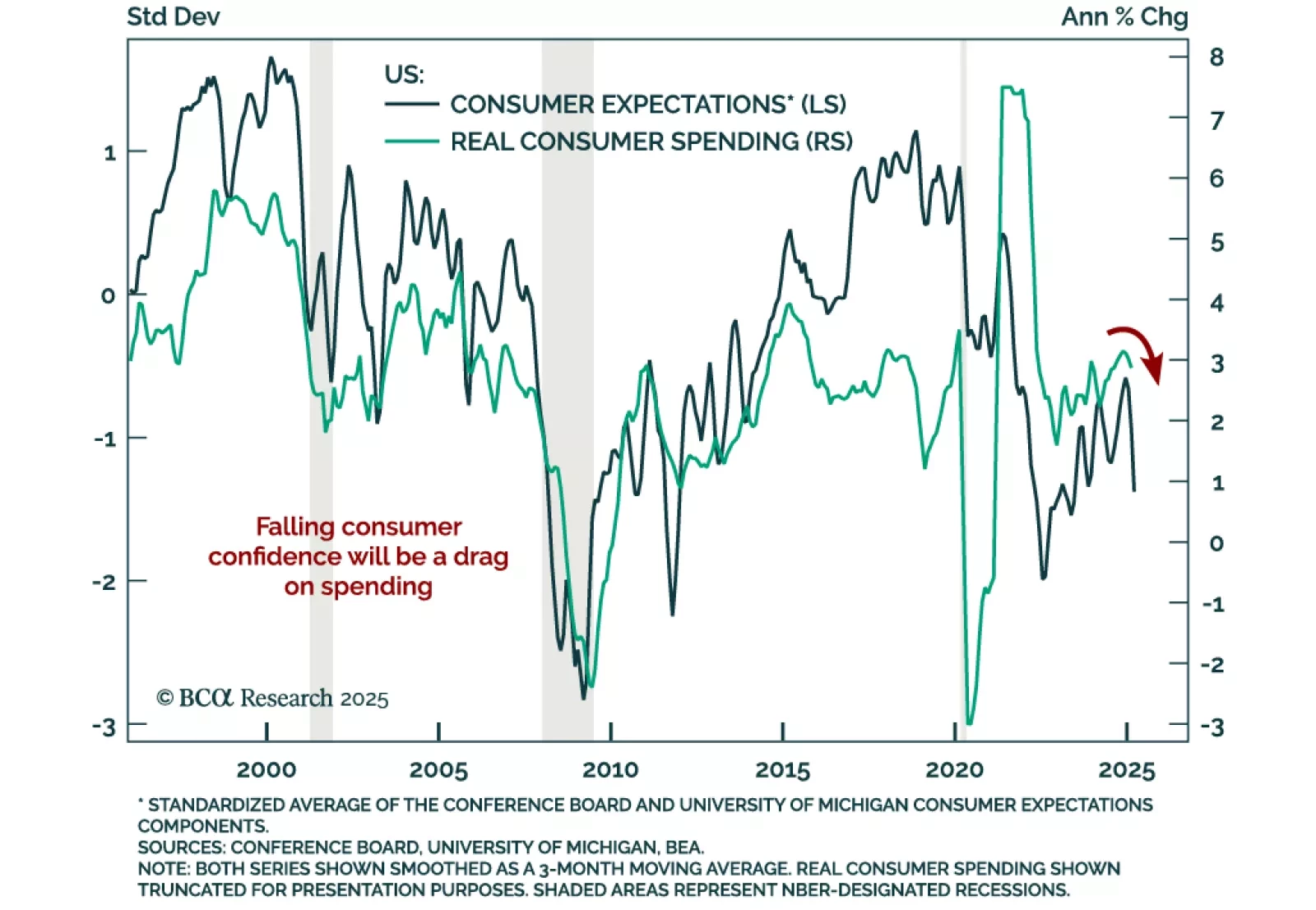

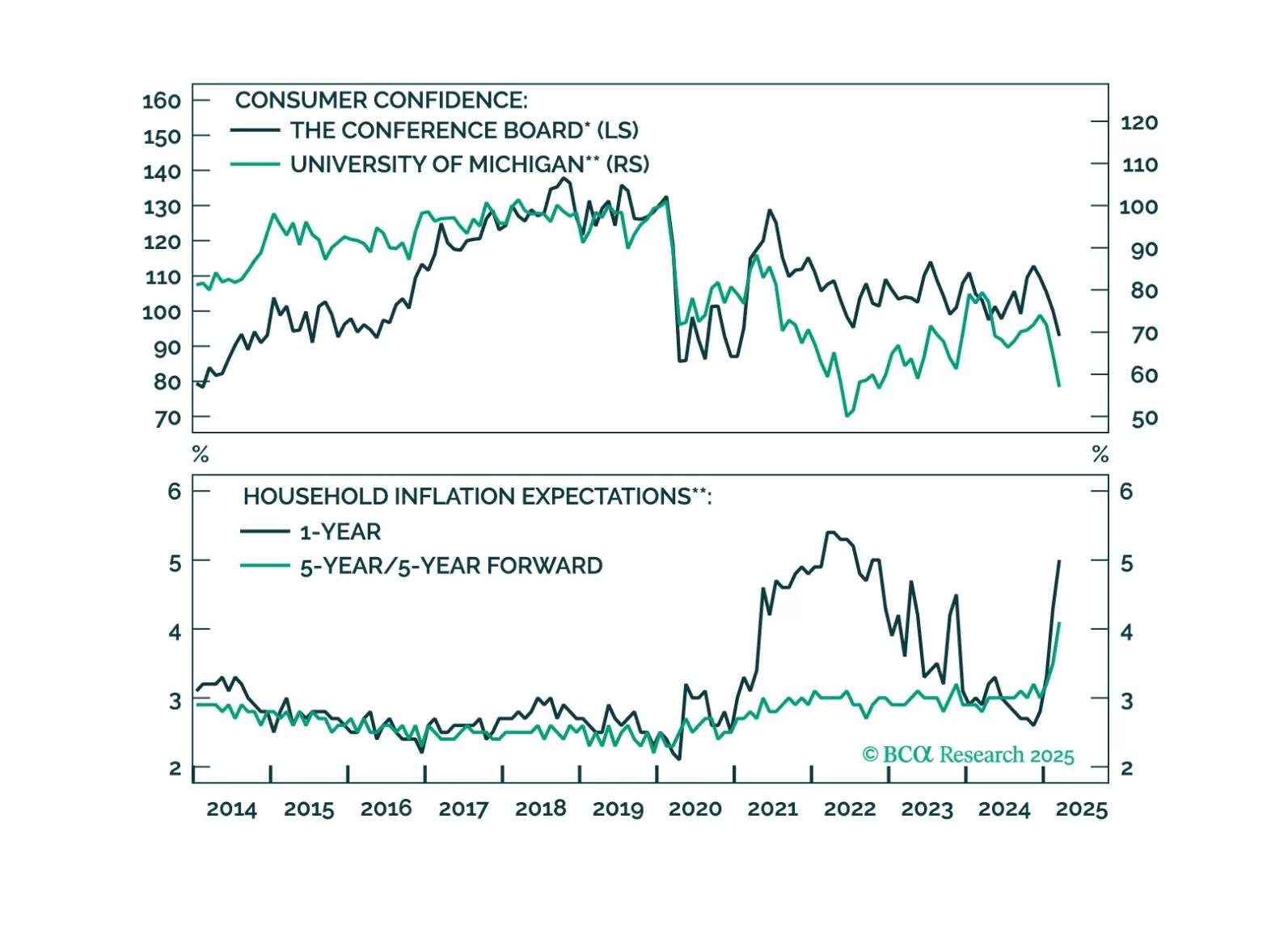

Trump’s foreign policy has been the focus for investors over the past few months. But is it really the underlying cause of the selloff? Market dynamics suggests that tariffs have only been a catalyst. In our view, investors should not focus on the man – Trump and his policy preferences – but should instead focus on the macro. Specifically, we outline three trends that will matter over the cyclical horizon: valuation and policy differences between the US and the rest of the world, the collapse of US animal spirits, and how the AI narrative has begun to crack. While markets could whipsaw around “Liberation Day,” this will only be the opening salvo of the negotiations. We believe that investors will be better served by focusing on these three forces – none of which are positive to risk assets. Remain defensively positioned.

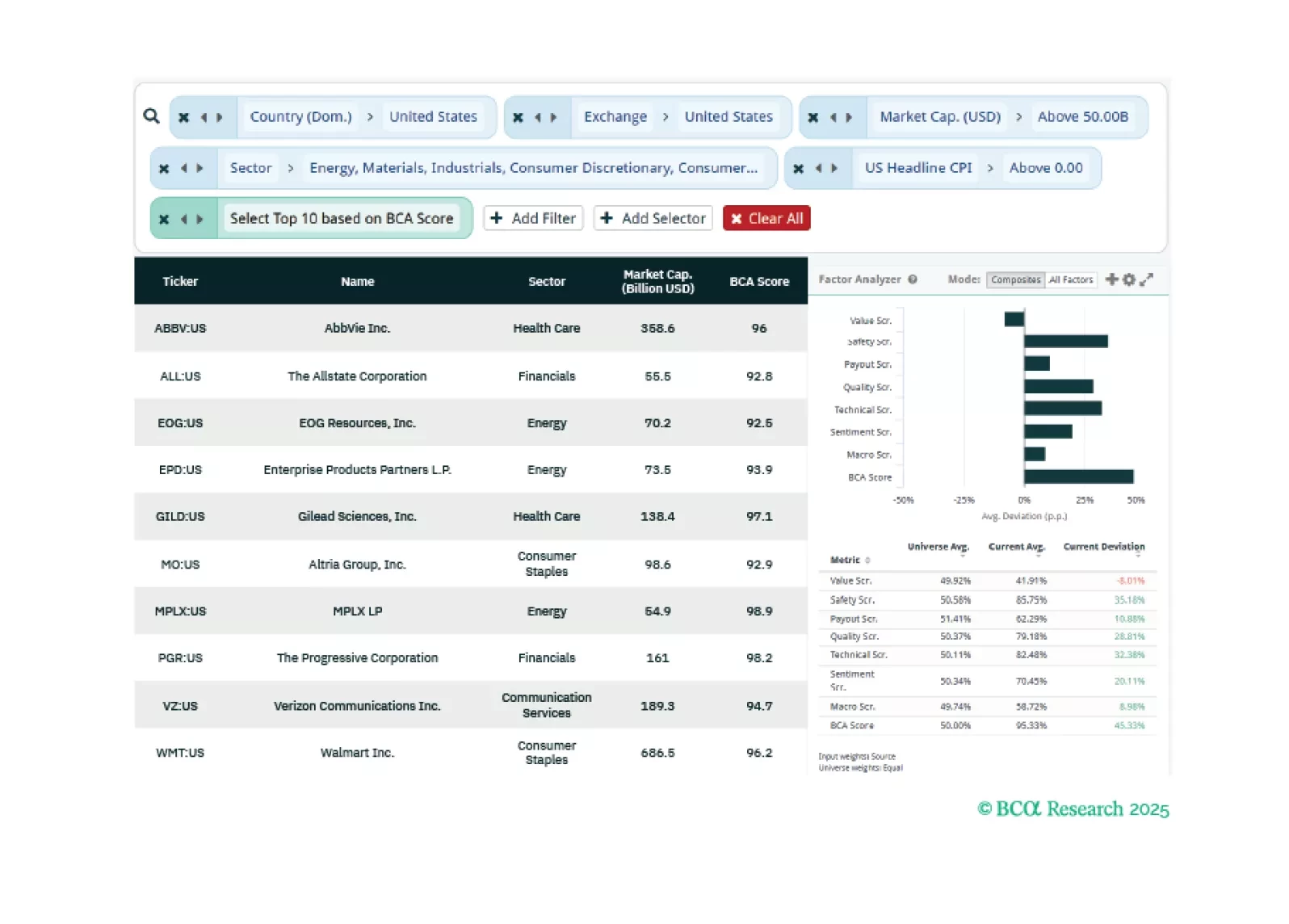

This week, our three screeners cover equity plays for if a US recession is not imminent, avoiding value traps, and which sectors exhibit the highest dividend payers.

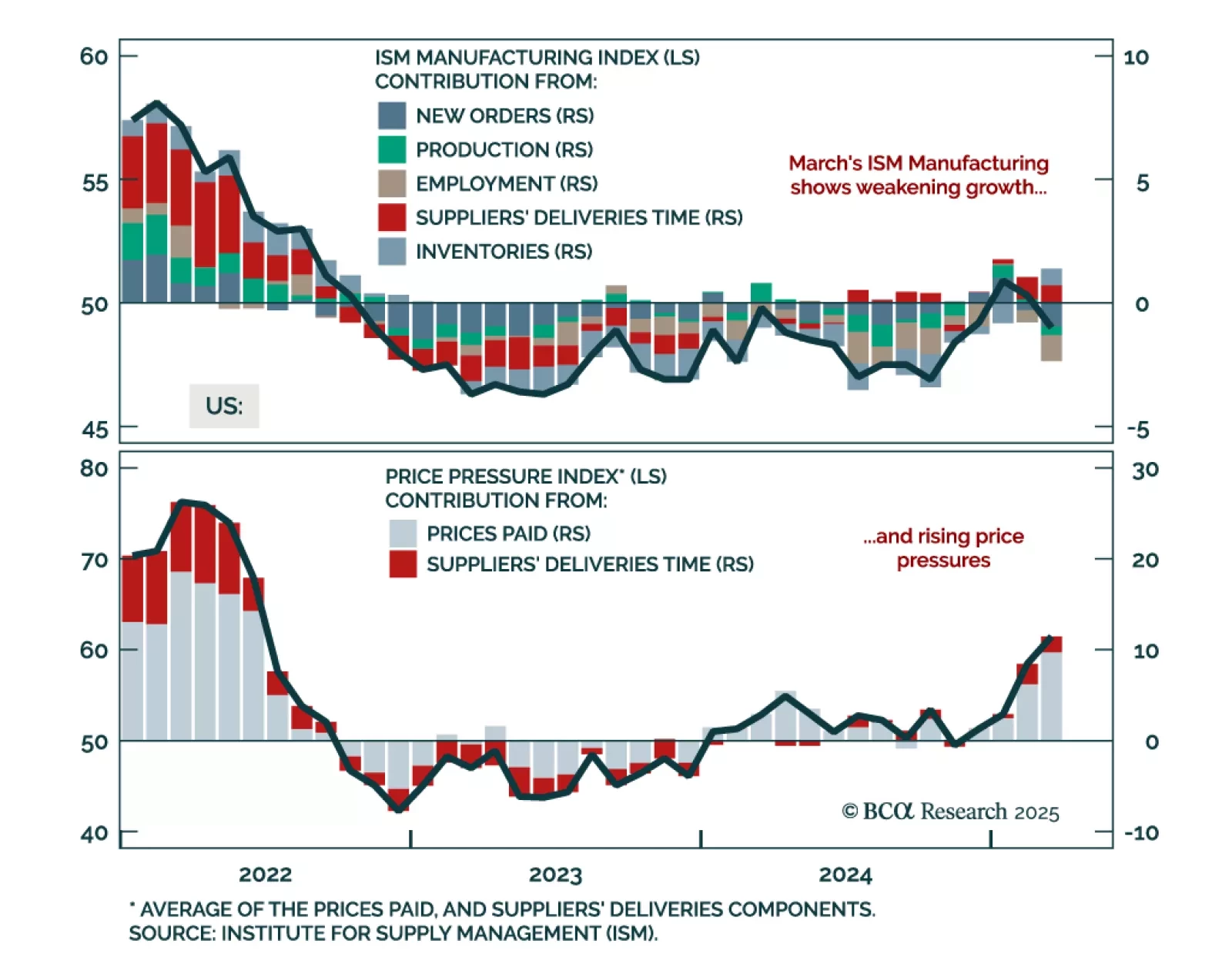

This morning’s weak consumer spending and strong inflation data reinforce our sense that the US economy is heading toward recession.

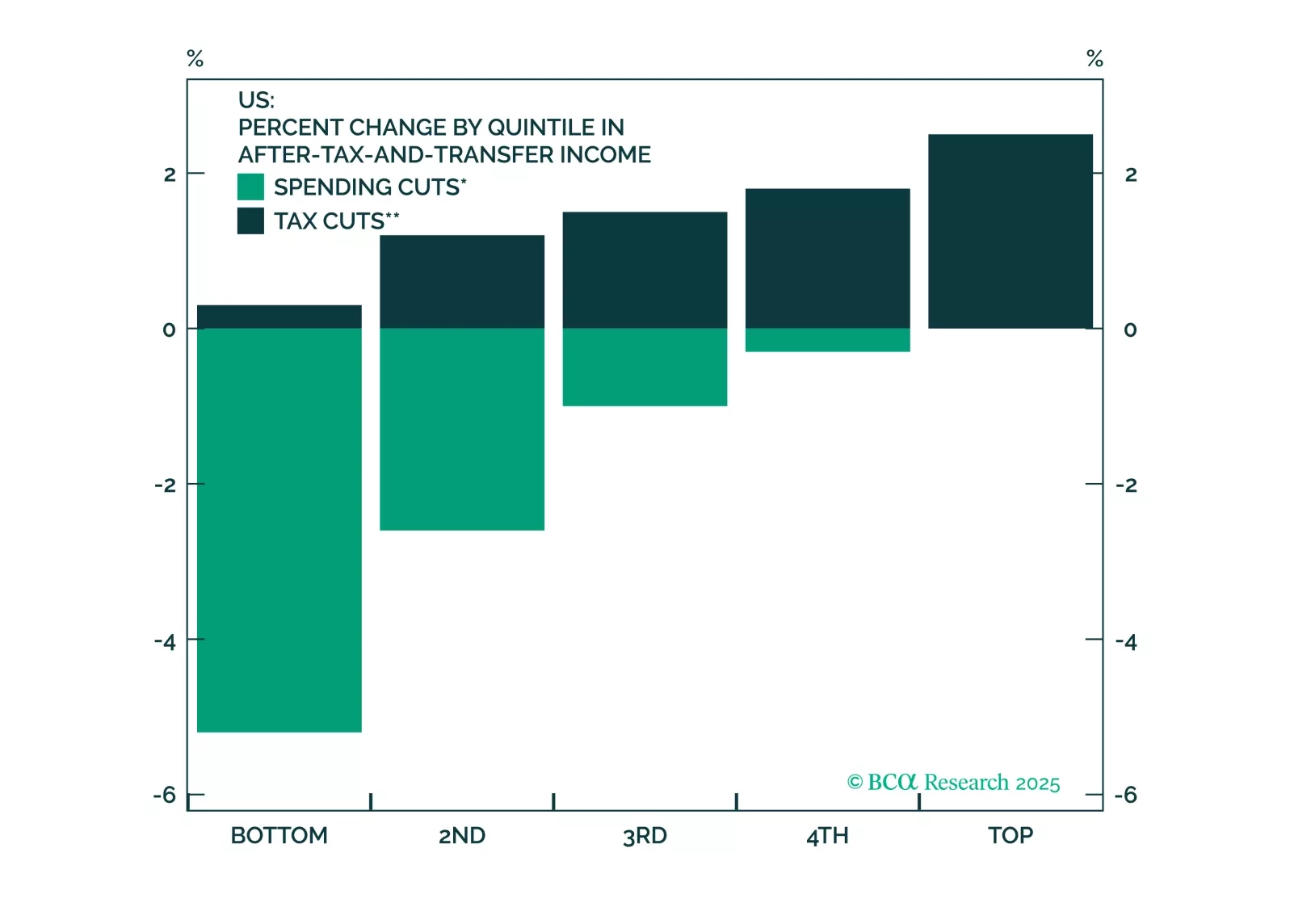

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.